Managerial Accounting: Balanced Scorecard for British American Tobacco

VerifiedAdded on 2023/06/05

|10

|2186

|228

Report

AI Summary

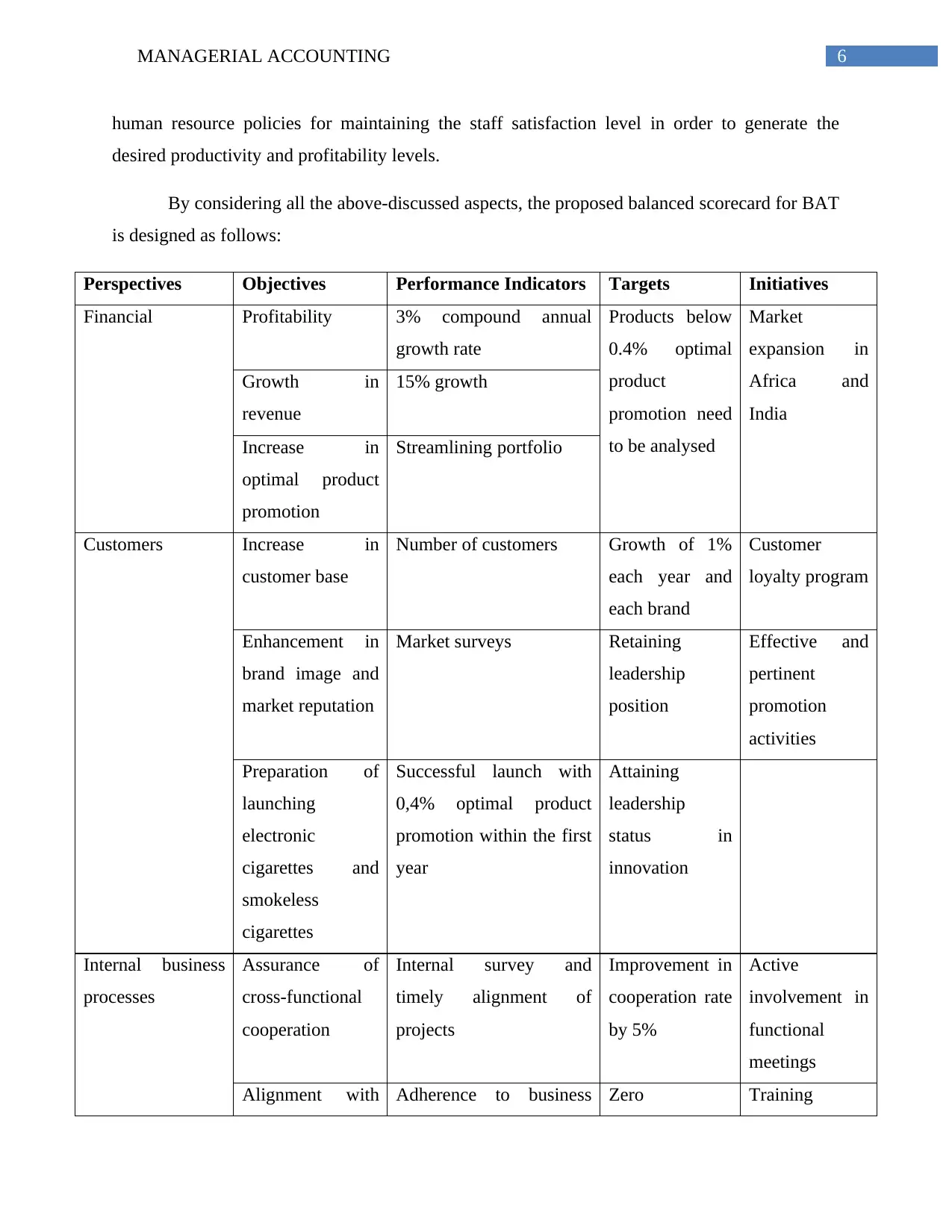

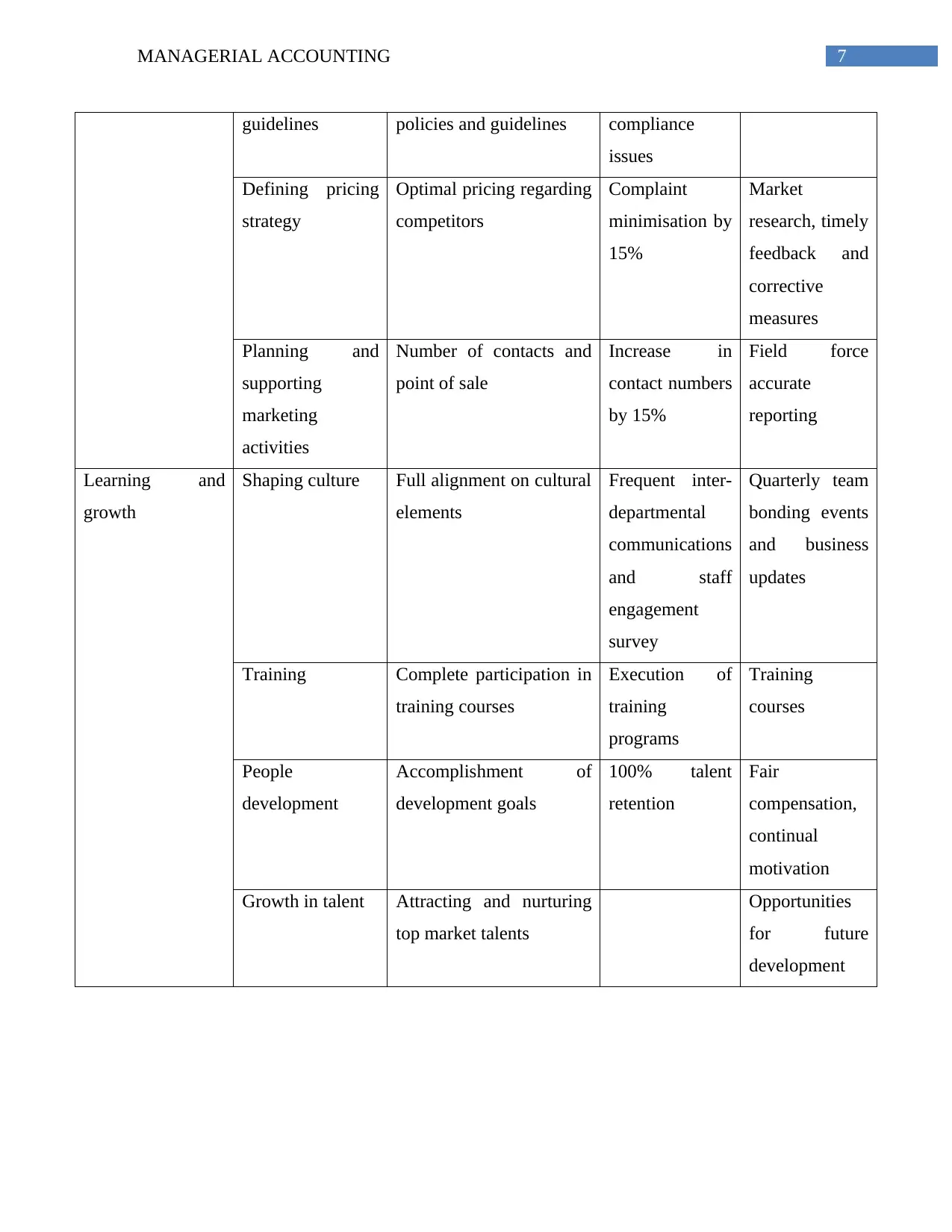

This report provides a comprehensive analysis of the balanced scorecard and its application in managerial accounting, specifically focusing on British American Tobacco (BAT). It outlines the four key perspectives of the balanced scorecard—financial, customer, internal business processes, and learning and growth—and sets strategic objectives for each perspective relevant to BAT. The report identifies key performance indicators (KPIs) for each strategic objective, such as profitability growth, customer base increase, and improved cross-functional cooperation. It also suggests initiatives for achieving these objectives, like market expansion, customer loyalty programs, and staff training. The balanced scorecard framework is tailored to BAT's context, considering the restrictions on tobacco advertising and the need for innovation in product offerings. This analysis aims to provide a strategic tool for BAT to enhance its performance and maintain a competitive edge in the tobacco industry. Desklib provides this document along with numerous other solved assignments for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.