Evaluating Balanced Scorecard Implementation at Toyota Corporation

VerifiedAdded on 2021/05/31

|18

|3808

|40

Report

AI Summary

This report evaluates the Balanced Scorecard (BSC) model, a modern management accounting method, for potential implementation at Toyota Corporation. The report begins with an introduction to Toyota, outlining its vision and mission. It then details the BSC model, explaining its four key perspectives: financial, customer, internal processes, and learning & growth. The report compares the BSC model to traditional performance measurement systems, highlighting the advantages of the BSC approach in aligning with company strategy and providing a more comprehensive view of performance. The report concludes by assessing the suitability of the BSC model for Toyota, offering insights to the CEO to understand the model's benefits and its potential to enhance the company's performance evaluation. The report emphasizes the BSC model's ability to improve communication, strategic alignment, and performance measurement accuracy compared to traditional methods. The report is intended to help Toyota evaluate the BSC model for its business.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 1

Introduction

The report is based on one of the modern management accounting methods that are Balanced

Scorecard model. Balanced scorecard model is used by numerous companies for effective

evaluation of the performance of the company. Being a newly appointed consultant in the

management consultancy firm you need to evaluate the current budgeting system of the client’s

firm. The client of the management consultancy is Toyota Corporation. CEO of the Toyota

Company currently attended a seminar of private companies that were related to the concept of

the balanced scorecard. The company is prepared to evaluate the suitability of the balanced

scorecard model to the Toyota Corporation.

The suitability of the BSC model can only be understood by the CEO of the company when they

know about the details related to the concept and its features. Along with this, the CEO should be

aware of the fact that the BSC is different from traditional performance measurement systems.

This report will help the CEO of the Toyota Company to understand the concept and the benefits

of the model which will contribute to understand the suitability of the model to the Toyota

Corporation.

Introduction

The report is based on one of the modern management accounting methods that are Balanced

Scorecard model. Balanced scorecard model is used by numerous companies for effective

evaluation of the performance of the company. Being a newly appointed consultant in the

management consultancy firm you need to evaluate the current budgeting system of the client’s

firm. The client of the management consultancy is Toyota Corporation. CEO of the Toyota

Company currently attended a seminar of private companies that were related to the concept of

the balanced scorecard. The company is prepared to evaluate the suitability of the balanced

scorecard model to the Toyota Corporation.

The suitability of the BSC model can only be understood by the CEO of the company when they

know about the details related to the concept and its features. Along with this, the CEO should be

aware of the fact that the BSC is different from traditional performance measurement systems.

This report will help the CEO of the Toyota Company to understand the concept and the benefits

of the model which will contribute to understand the suitability of the model to the Toyota

Corporation.

Management Accounting 2

Contents

Introduction......................................................................................................................................1

About Toyota corporation................................................................................................................3

A vision of Toyota.......................................................................................................................3

Balanced Scorecard.........................................................................................................................4

Features of Balanced Scorecard.......................................................................................................7

Comparison of balanced scorecard model with traditional performance measurement systems....8

Suitability for Toyota Corporation................................................................................................10

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

Contents

Introduction......................................................................................................................................1

About Toyota corporation................................................................................................................3

A vision of Toyota.......................................................................................................................3

Balanced Scorecard.........................................................................................................................4

Features of Balanced Scorecard.......................................................................................................7

Comparison of balanced scorecard model with traditional performance measurement systems....8

Suitability for Toyota Corporation................................................................................................10

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting 3

About Toyota corporation

Toyota Motor Corporation is well-known Japanese multination automotive manufacturer with

the headquarters in Toyota, Aichi, Japan. The company has provided its contribution towards a

prosperous society through the manufacture of automobiles, operating its business with the aim

of the vehicle sales and production. The company believes in diversity due to which the company

manufacture and sell different types of product across the globe (Toyota, 2018).

Vision of Toyota

Toyota vision is to lead the way to the future of the mobility with the motive to enriching the

lives of the people across the work with safety and responsibility. The company is committed

towards the quality, constant innovation and all the respect for the plant (Toyota, 2018). The aim

for which the company work is to exceed expectations with a smile. As of the year 2017, the

company is known as the world’s 2nd largest automotive manufacturer (Toyota, 2018). The

company was world’s leading automobile manufacturer who manufacturers more than 10 million

vehicles every year. This was done by the company since 2012 and at that time only the

company reported production of its 200-million vehicles (Toyota, 2018).

About Toyota corporation

Toyota Motor Corporation is well-known Japanese multination automotive manufacturer with

the headquarters in Toyota, Aichi, Japan. The company has provided its contribution towards a

prosperous society through the manufacture of automobiles, operating its business with the aim

of the vehicle sales and production. The company believes in diversity due to which the company

manufacture and sell different types of product across the globe (Toyota, 2018).

Vision of Toyota

Toyota vision is to lead the way to the future of the mobility with the motive to enriching the

lives of the people across the work with safety and responsibility. The company is committed

towards the quality, constant innovation and all the respect for the plant (Toyota, 2018). The aim

for which the company work is to exceed expectations with a smile. As of the year 2017, the

company is known as the world’s 2nd largest automotive manufacturer (Toyota, 2018). The

company was world’s leading automobile manufacturer who manufacturers more than 10 million

vehicles every year. This was done by the company since 2012 and at that time only the

company reported production of its 200-million vehicles (Toyota, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 4

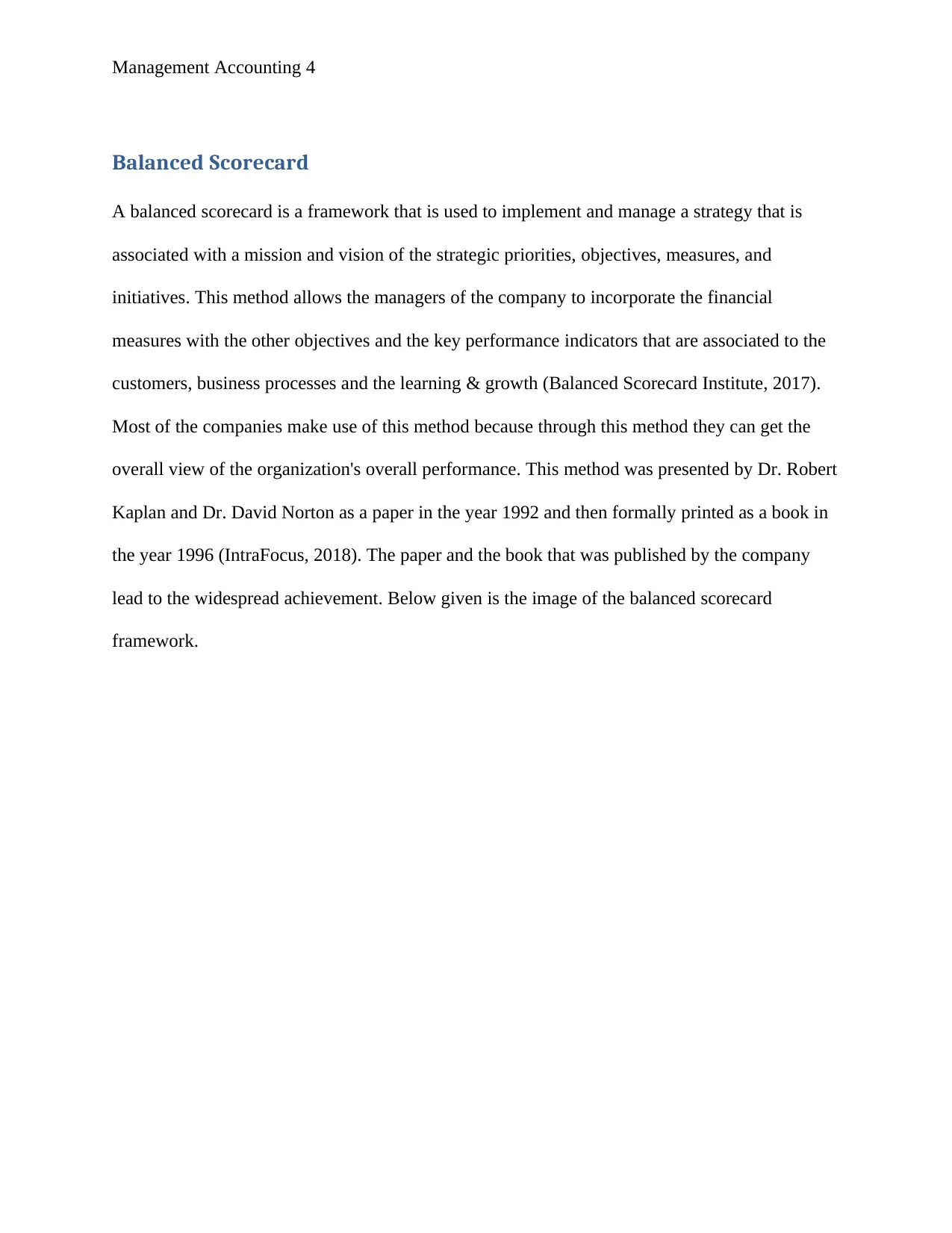

Balanced Scorecard

A balanced scorecard is a framework that is used to implement and manage a strategy that is

associated with a mission and vision of the strategic priorities, objectives, measures, and

initiatives. This method allows the managers of the company to incorporate the financial

measures with the other objectives and the key performance indicators that are associated to the

customers, business processes and the learning & growth (Balanced Scorecard Institute, 2017).

Most of the companies make use of this method because through this method they can get the

overall view of the organization's overall performance. This method was presented by Dr. Robert

Kaplan and Dr. David Norton as a paper in the year 1992 and then formally printed as a book in

the year 1996 (IntraFocus, 2018). The paper and the book that was published by the company

lead to the widespread achievement. Below given is the image of the balanced scorecard

framework.

Balanced Scorecard

A balanced scorecard is a framework that is used to implement and manage a strategy that is

associated with a mission and vision of the strategic priorities, objectives, measures, and

initiatives. This method allows the managers of the company to incorporate the financial

measures with the other objectives and the key performance indicators that are associated to the

customers, business processes and the learning & growth (Balanced Scorecard Institute, 2017).

Most of the companies make use of this method because through this method they can get the

overall view of the organization's overall performance. This method was presented by Dr. Robert

Kaplan and Dr. David Norton as a paper in the year 1992 and then formally printed as a book in

the year 1996 (IntraFocus, 2018). The paper and the book that was published by the company

lead to the widespread achievement. Below given is the image of the balanced scorecard

framework.

Management Accounting 5

(Source: Kaplan, Norton and Rugelsjoen, 2010)

The company doesn’t consider it as a scorecard but it is also identified as the methodology that is

mainly used by the company to determine a small number of financial and non-financial

objectives which are linked to the strategic priorities. This approach emphasizes the firm to think

about the ways through which they can measure the objective and what initiatives can be put in

place to meet the objective of the company (Paul, 2018). Balanced scorecard approach emphases

on the financial and non-financial objectives of a company that is attributed to the four areas

which are discussed below: -

Financial perspective

Considering the opinion of the Kaplan and Norton the financial perspective is one of the

important essential perspectives for the company that is required to be measured. The financial

(Source: Kaplan, Norton and Rugelsjoen, 2010)

The company doesn’t consider it as a scorecard but it is also identified as the methodology that is

mainly used by the company to determine a small number of financial and non-financial

objectives which are linked to the strategic priorities. This approach emphasizes the firm to think

about the ways through which they can measure the objective and what initiatives can be put in

place to meet the objective of the company (Paul, 2018). Balanced scorecard approach emphases

on the financial and non-financial objectives of a company that is attributed to the four areas

which are discussed below: -

Financial perspective

Considering the opinion of the Kaplan and Norton the financial perspective is one of the

important essential perspectives for the company that is required to be measured. The financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting 6

data or statistics is very important for every company to achieve the success and the competitive

advantage in the current working environment. Managers of the company need to pay the

attention towards the appropriate financial data on time. This financial perspective of the

balanced scorecard model ensures an effective return on investment in a firm along with the

effective management of the risk that is associated with the business (KPI Expert, 2018).

Financial goals should be aligned with the strategic planning, revenue and the productivity

variables that are presented as the performance indicators of the actions of the company.

Customer perspective

Modern management believes in studies the client-oriented business activities which are

essential for the business and for its strategy. Balanced scorecard model include this perspective

with the motive to precisely monitor the ways through which the company is delivering the value

to its customers with the use of the pointers of the outcomes and satisfaction like surveys and

continuously taking into account the deadline, cost, performance and the quality of the product

and services that are offered by the company. Low performance of the customer-oriented

activities might cause a decline of business (Agarwal, 2018). This perspective is very important

for the company because if the company is not able to satisfy the needs of the customers then

they won’t be able to continue their business no matter what the other activities are working

effectively or not.

Internal processes perspective

This internal process activity purposes to arrange a tree for the business process so that

monitoring and optimization of the performance can be done in an effective way from the

company’s point of view. most of the CEO found that the activities linked with the internal

data or statistics is very important for every company to achieve the success and the competitive

advantage in the current working environment. Managers of the company need to pay the

attention towards the appropriate financial data on time. This financial perspective of the

balanced scorecard model ensures an effective return on investment in a firm along with the

effective management of the risk that is associated with the business (KPI Expert, 2018).

Financial goals should be aligned with the strategic planning, revenue and the productivity

variables that are presented as the performance indicators of the actions of the company.

Customer perspective

Modern management believes in studies the client-oriented business activities which are

essential for the business and for its strategy. Balanced scorecard model include this perspective

with the motive to precisely monitor the ways through which the company is delivering the value

to its customers with the use of the pointers of the outcomes and satisfaction like surveys and

continuously taking into account the deadline, cost, performance and the quality of the product

and services that are offered by the company. Low performance of the customer-oriented

activities might cause a decline of business (Agarwal, 2018). This perspective is very important

for the company because if the company is not able to satisfy the needs of the customers then

they won’t be able to continue their business no matter what the other activities are working

effectively or not.

Internal processes perspective

This internal process activity purposes to arrange a tree for the business process so that

monitoring and optimization of the performance can be done in an effective way from the

company’s point of view. most of the CEO found that the activities linked with the internal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 7

process perspectives seem to be more sophisticated due to which they are not able to analyze the

performance of the internal business process. This method provides the support to the companies

to analyze the internal business processes (Erbasi and Parlakkaya, 2012). BSC model consists of

determining and mapping the processes which are essential to be accomplishing the company

objectives and applying those strategies for bringing the continuous improvement. BSC model

will support in analyzing those activities which are essential for adding the value to the products

and services of the company. The major motive behind measuring the performance is to satisfy

the needs of the shareholders of the company by providing them maximum returns.

Learning and growth perspective

Learning and growth of the employees in an organization are very essential because without this

the company is not able to perform its operations effectively. Employees of the company are

considered as the assets due to which it becomes the priority of the company to retain the

employees in the company. The growth of business and employees is only possible in the

organization when they make use of the skills and abilities because this is the only way through

which they can achieve the success (Valmohammadi and Ahmadi, 2015). Most of the companies

invest the amount because this is the way through which they can bring the long-term growth in

the operations of the business. BSC model helps the companies in evaluating the learning and

growth perspective of the company so that they can identify the loopholes and work effectively

to bring the improvement in proving training to the employees.

Features of Balanced Scorecard

BSC model provides the value added to the company so that they can map their strategies

effectively.

process perspectives seem to be more sophisticated due to which they are not able to analyze the

performance of the internal business process. This method provides the support to the companies

to analyze the internal business processes (Erbasi and Parlakkaya, 2012). BSC model consists of

determining and mapping the processes which are essential to be accomplishing the company

objectives and applying those strategies for bringing the continuous improvement. BSC model

will support in analyzing those activities which are essential for adding the value to the products

and services of the company. The major motive behind measuring the performance is to satisfy

the needs of the shareholders of the company by providing them maximum returns.

Learning and growth perspective

Learning and growth of the employees in an organization are very essential because without this

the company is not able to perform its operations effectively. Employees of the company are

considered as the assets due to which it becomes the priority of the company to retain the

employees in the company. The growth of business and employees is only possible in the

organization when they make use of the skills and abilities because this is the only way through

which they can achieve the success (Valmohammadi and Ahmadi, 2015). Most of the companies

invest the amount because this is the way through which they can bring the long-term growth in

the operations of the business. BSC model helps the companies in evaluating the learning and

growth perspective of the company so that they can identify the loopholes and work effectively

to bring the improvement in proving training to the employees.

Features of Balanced Scorecard

BSC model provides the value added to the company so that they can map their strategies

effectively.

Management Accounting 8

BSC contributes to improve the effective communication between the departments of the

company.

Balanced scorecard model measures the 4 perspectives which include financial, customer,

learning & growth and the business internal processes which are considered as a most

crucial perspective of the company.

This model gets align with the daily working and strategy of the company which is

essential for the accurate evaluation of the performance of firm (Lueg, 2015).

Balanced scorecard model points out the company’s effective strategy by focusing on the

cause and effect relationship of the firm.

The companies get the feedback to bring the improvement in the performance of the

organization which is only possible after effective analysis.

Balanced scorecard model helps the company for the effective communication as the

department of the companies interact because of the BSC model as this model provide the

analysis of the entire organization and all the activities of the company are interrelated

with each other (Kerai and Saleh, 2017).

Balanced scorecard model can be used by the company to monitor and measure the

progress of strategies that the company has implemented to support the working.

Comparison of balanced scorecard model with traditional performance

measurement systems

Balanced scorecard approach is different from the traditional performance system. Some of the

difference between both the approaches of the accounting method is explained in this section of

the report. Traditional performance system is totally different from the modern approach of the

BSC contributes to improve the effective communication between the departments of the

company.

Balanced scorecard model measures the 4 perspectives which include financial, customer,

learning & growth and the business internal processes which are considered as a most

crucial perspective of the company.

This model gets align with the daily working and strategy of the company which is

essential for the accurate evaluation of the performance of firm (Lueg, 2015).

Balanced scorecard model points out the company’s effective strategy by focusing on the

cause and effect relationship of the firm.

The companies get the feedback to bring the improvement in the performance of the

organization which is only possible after effective analysis.

Balanced scorecard model helps the company for the effective communication as the

department of the companies interact because of the BSC model as this model provide the

analysis of the entire organization and all the activities of the company are interrelated

with each other (Kerai and Saleh, 2017).

Balanced scorecard model can be used by the company to monitor and measure the

progress of strategies that the company has implemented to support the working.

Comparison of balanced scorecard model with traditional performance

measurement systems

Balanced scorecard approach is different from the traditional performance system. Some of the

difference between both the approaches of the accounting method is explained in this section of

the report. Traditional performance system is totally different from the modern approach of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting 9

accounting method. A balanced scorecard method is a modern approach which is used by most

of the companies in the current market because they know that the environment brings the

change in businesses. The traditional method is not appropriate for the current business

environment because this method doesn't bring the change in the evaluation of the performance

of the companies (Coe and Letza, 2014). The traditional method of accounting includes the

financial analysis of the company which can be done effectively with the use of the different

tools such as cash flow, ratios, financial statement and many others.

On the other hand, the balanced scorecard method provides the analysis of the performance of

the company with the help of the financial, customers, business internal process and learning &

growth perspective of the company. This is the modern approach to manage the accounting due

to which they include all the aspects that are essential for the business to be considered while

evaluating the performance of the company. Therefore, this can be said that it includes both the

financial and non-financial analysis. The traditional method of the accounting provides the true

picture to the company. On the other hand, the balanced scorecard method provides the analysis

along with the feedback to the company (Biazzo and Garengo, 2012). Along with this, BSC

model highlights the capabilities of the company that contributes to improve the performance of

the company.

One of the major difference between both the method is that Balanced scorecard model gets

align with the strategies and vision of the company. Considering the strategies, the BSC model

conducts the evaluation and provides the feedback to the firm. On the other hand, the traditional

accounting method doesn’t get linked with the strategies and vision of the company due to which

they are not able to provide the accurate results that fit with the strategies of the company.

accounting method. A balanced scorecard method is a modern approach which is used by most

of the companies in the current market because they know that the environment brings the

change in businesses. The traditional method is not appropriate for the current business

environment because this method doesn't bring the change in the evaluation of the performance

of the companies (Coe and Letza, 2014). The traditional method of accounting includes the

financial analysis of the company which can be done effectively with the use of the different

tools such as cash flow, ratios, financial statement and many others.

On the other hand, the balanced scorecard method provides the analysis of the performance of

the company with the help of the financial, customers, business internal process and learning &

growth perspective of the company. This is the modern approach to manage the accounting due

to which they include all the aspects that are essential for the business to be considered while

evaluating the performance of the company. Therefore, this can be said that it includes both the

financial and non-financial analysis. The traditional method of the accounting provides the true

picture to the company. On the other hand, the balanced scorecard method provides the analysis

along with the feedback to the company (Biazzo and Garengo, 2012). Along with this, BSC

model highlights the capabilities of the company that contributes to improve the performance of

the company.

One of the major difference between both the method is that Balanced scorecard model gets

align with the strategies and vision of the company. Considering the strategies, the BSC model

conducts the evaluation and provides the feedback to the firm. On the other hand, the traditional

accounting method doesn’t get linked with the strategies and vision of the company due to which

they are not able to provide the accurate results that fit with the strategies of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 10

Apart from this, another major difference that takes place between both the methods of the

accounting is the accuracy. The accuracy of the results is only possible in the BSC model as this

model is more accurate than the traditional method of the accounting (Amado, Santos and

Marques, 2012). Along with this, BSC model will help the company in achieving the success in

the near future which is possible only if the company has performed the effective implementation

of the balanced scorecard model.

The overall analysis between both the traditional and the balanced scorecard management

accounting reflect that the BSC model fulfills all the drawbacks of the traditional management

accounting model due to which it will be effective for the company if they will implement the

BSC model of the accounting management. Though, this is the fact that this model is difficult to

implement in the organization because the company needs to appoint an accounting expert who

can offer all the services to implement the balanced scorecard model. This will cost high for the

company as they have to pay high amount to the expert who will implement the balanced

scorecard model in the organization. After considering the whole analysis, it can be said that the

balanced scorecard method or approach is effective for the business in the dynamic world.

Suitability for Toyota Corporation

The suitability of the balanced scorecard model for the Toyota Corporation is discussed in this

section of the report. The below given is the analysis of every perspective that helps the company

in achieving the desired goals and objective which is essential for the business success.

Financial perspective: - Toyota Company has numerous numbers of strategic objectives

that the company is looking to measure the effective implementation of balanced

scorecard model. These strategic goals are a rise in the profitability of the company,

Apart from this, another major difference that takes place between both the methods of the

accounting is the accuracy. The accuracy of the results is only possible in the BSC model as this

model is more accurate than the traditional method of the accounting (Amado, Santos and

Marques, 2012). Along with this, BSC model will help the company in achieving the success in

the near future which is possible only if the company has performed the effective implementation

of the balanced scorecard model.

The overall analysis between both the traditional and the balanced scorecard management

accounting reflect that the BSC model fulfills all the drawbacks of the traditional management

accounting model due to which it will be effective for the company if they will implement the

BSC model of the accounting management. Though, this is the fact that this model is difficult to

implement in the organization because the company needs to appoint an accounting expert who

can offer all the services to implement the balanced scorecard model. This will cost high for the

company as they have to pay high amount to the expert who will implement the balanced

scorecard model in the organization. After considering the whole analysis, it can be said that the

balanced scorecard method or approach is effective for the business in the dynamic world.

Suitability for Toyota Corporation

The suitability of the balanced scorecard model for the Toyota Corporation is discussed in this

section of the report. The below given is the analysis of every perspective that helps the company

in achieving the desired goals and objective which is essential for the business success.

Financial perspective: - Toyota Company has numerous numbers of strategic objectives

that the company is looking to measure the effective implementation of balanced

scorecard model. These strategic goals are a rise in the profitability of the company,

Management Accounting 11

increasing the sales of the products and services of the company in the emerging markets

and the sustainable financial growth of the business in the current market. Moreover, the

strategic measures of the company include the lag indicators. The company can measure

these all objective with the help of the BSC as it includes all the ways through which the

company can measure the perspective (Keyes, 2016). Some of the measures that can be

used by the company include profit margin growth of Toyota, the rise in the cash flow of

the company and the participation in the emerging markets.

Customer perspective: - The major objective of the company from the customer

perspective is to regain the trust of the customers, enhance the effective communication,

maintaining an ethical approach towards the customers and becoming the worldwide

leader. The balanced scorecard model provides the support to the company through

which they can improve the working of the business. The company can measure the

objectives with the help of the balanced scorecard model. The BSC model will also

provide the effective way through which the company can improve the customer

satisfaction and retention (Agarwal, 2018). Toyota can measure the objectives with the

help of BSC and the ways through which the company can measure the strategic goals

are an improvement in the brand recognition of the company, brand trustworthiness and

the feedback that is received by the company after selling any of the cars.

Internal business process: - The internal business process is very important for the

company to evaluate which can be done with the help of the balanced scorecard model.

The company can make the strategy such as strengthen the establishment of the internal

system which is essential for the improvement in the quality, improvement in the product

development processes, innovative products and the rise in the research and development

increasing the sales of the products and services of the company in the emerging markets

and the sustainable financial growth of the business in the current market. Moreover, the

strategic measures of the company include the lag indicators. The company can measure

these all objective with the help of the BSC as it includes all the ways through which the

company can measure the perspective (Keyes, 2016). Some of the measures that can be

used by the company include profit margin growth of Toyota, the rise in the cash flow of

the company and the participation in the emerging markets.

Customer perspective: - The major objective of the company from the customer

perspective is to regain the trust of the customers, enhance the effective communication,

maintaining an ethical approach towards the customers and becoming the worldwide

leader. The balanced scorecard model provides the support to the company through

which they can improve the working of the business. The company can measure the

objectives with the help of the balanced scorecard model. The BSC model will also

provide the effective way through which the company can improve the customer

satisfaction and retention (Agarwal, 2018). Toyota can measure the objectives with the

help of BSC and the ways through which the company can measure the strategic goals

are an improvement in the brand recognition of the company, brand trustworthiness and

the feedback that is received by the company after selling any of the cars.

Internal business process: - The internal business process is very important for the

company to evaluate which can be done with the help of the balanced scorecard model.

The company can make the strategy such as strengthen the establishment of the internal

system which is essential for the improvement in the quality, improvement in the product

development processes, innovative products and the rise in the research and development

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.