ACC203 Management Accounting & Balanced Scorecard - Australia

VerifiedAdded on 2023/06/04

|14

|2188

|348

Report

AI Summary

This management accounting report discusses the factors contributing to the development of management accounting practices, emphasizing the role of compliance, control mechanisms, and competitive support. It evaluates the usefulness of the Balanced Scorecard method and applies these concepts to Qantas Airlines, identifying critical success factors (CSFs), key performance indicators (KPIs), and constructing a strategy map and balanced scorecard for the company. The report concludes that management accounting practices have evolved significantly due to compliance, regulatory controls, and competitive factors, with the Balanced Scorecard proving useful in improving financial performance and operational efficiency.

Management Accounting Report 1

Management Accounting Report

Management Accounting Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting Report 2

Contents

Part A..........................................................................................................................................................3

Introduction.................................................................................................................................................3

Main Discussions........................................................................................................................................3

The Role of the Compliance, Control Mechanism, and Competitive Support in influencing the

Management Accounting Practices..........................................................................................................3

Factors Contributing to the Development of Management Accounting Practices....................................5

Evaluation of the Usefulness of Balance Scorecard Method in the Management Accounting Practices..6

Part B Management Accounting Practices in Qantas Airlines.....................................................................9

Task 1 Critical Success Factors and Performance Indicators for Qantas Airlines....................................9

Task 2 Strategy Map..............................................................................................................................10

Task 3 Balance Scorecard......................................................................................................................11

Conclusion.................................................................................................................................................12

References.................................................................................................................................................13

Contents

Part A..........................................................................................................................................................3

Introduction.................................................................................................................................................3

Main Discussions........................................................................................................................................3

The Role of the Compliance, Control Mechanism, and Competitive Support in influencing the

Management Accounting Practices..........................................................................................................3

Factors Contributing to the Development of Management Accounting Practices....................................5

Evaluation of the Usefulness of Balance Scorecard Method in the Management Accounting Practices..6

Part B Management Accounting Practices in Qantas Airlines.....................................................................9

Task 1 Critical Success Factors and Performance Indicators for Qantas Airlines....................................9

Task 2 Strategy Map..............................................................................................................................10

Task 3 Balance Scorecard......................................................................................................................11

Conclusion.................................................................................................................................................12

References.................................................................................................................................................13

Management Accounting Report 3

Part A

Introduction

Management Accounting is an important process of preparing the accurate and timely

management reports, financial statements, and auditing reports based on the statistical figures,

financial data, and accounting information. It is also defined as a process of identifying,

preparing, measuring, analyzing, interpreting, and communicating information to assist the

management in the accomplishment of the organizational goals and business objectives. The

management accounting involves management decision-making, devising performance

management planning, performance management system, feedback in the financial reporting,

and control for the formulation and implementation of an effective strategy for determining the

future growth of the firm(Sunarni, 2013).This report is prepared to identify and analyze the

factors for contributing in the development of the management accounting system and practices.

It will also emphasize the evolution of the management accounting practices resulting from the

enforcement of the regulation compliance and internal control system in the organizations.

Main Discussions

The Role of the Compliance, Control Mechanism, and Competitive Support in influencing

the Management Accounting Practices

The compliance, control, and competitive support are such factors that are responsible for

shaping the management accounting practices in the organizations. The regulatory compliance

and control factors influence the management accounting practices, like the creation of the

standardized financial statements, investigating the expense reports and inventory cost reports,

and preparation of the financial budget and accounting policies. The compliance and control set

the industry standards and statistical control measures,enforce laws and regulations derived from

Part A

Introduction

Management Accounting is an important process of preparing the accurate and timely

management reports, financial statements, and auditing reports based on the statistical figures,

financial data, and accounting information. It is also defined as a process of identifying,

preparing, measuring, analyzing, interpreting, and communicating information to assist the

management in the accomplishment of the organizational goals and business objectives. The

management accounting involves management decision-making, devising performance

management planning, performance management system, feedback in the financial reporting,

and control for the formulation and implementation of an effective strategy for determining the

future growth of the firm(Sunarni, 2013).This report is prepared to identify and analyze the

factors for contributing in the development of the management accounting system and practices.

It will also emphasize the evolution of the management accounting practices resulting from the

enforcement of the regulation compliance and internal control system in the organizations.

Main Discussions

The Role of the Compliance, Control Mechanism, and Competitive Support in influencing

the Management Accounting Practices

The compliance, control, and competitive support are such factors that are responsible for

shaping the management accounting practices in the organizations. The regulatory compliance

and control factors influence the management accounting practices, like the creation of the

standardized financial statements, investigating the expense reports and inventory cost reports,

and preparation of the financial budget and accounting policies. The compliance and control set

the industry standards and statistical control measures,enforce laws and regulations derived from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting Report 4

the industry standards, internal business processes or ethical guidelines, IT governance, and

quality assurance. The compliance and control mechanism assist in examining whether the

current organizational strategies and policies and the financial performance measures are

compliance with the perspectives of the economic-financial, competencies and growth, and

customer/markers perceived by the stakeholders.The regulation mechanisms, like tax regulations,

effective compliance, and quality controls are required to add the strategic value for a firm by

meeting the strategic goals and objectives. On the other side, the non-compliance or control

failures cause for the significant loss of the business, producing the depressed stock market

valuations, distracting the senior management from their tasks, and even substantial threatening

cost (McKinsey& Company, 2015).

But, nowadays the modern businesses more focus on the competitive support than the

compliance and control for achieving the business objectives and strategic goals. The effective

control and compliance provide guidelines and regulations for performing the financial

functions, management of accounting operations, and auditing standards. Todays’ auditors,

accountants, and financial expertise place more emphasis on the competitive support for

achieving the financial, strategic, operational, and management objectives. The competitive

forces drive the firm for the changes in the accounting policies, auditing standards, financial

measures and statistics through installation of new accounting software system, knowledge

management practices, and information and communication technologies.

The modern business organizations look for the competitive support for creating the competitive

advantage instead of avoiding the trap of compliance and control. The intensity of the market

competition encourages the companies for using the standardized management accounting

practices to compete with the competitors and make better decisions (Nair &Nian, 2017). The

the industry standards, internal business processes or ethical guidelines, IT governance, and

quality assurance. The compliance and control mechanism assist in examining whether the

current organizational strategies and policies and the financial performance measures are

compliance with the perspectives of the economic-financial, competencies and growth, and

customer/markers perceived by the stakeholders.The regulation mechanisms, like tax regulations,

effective compliance, and quality controls are required to add the strategic value for a firm by

meeting the strategic goals and objectives. On the other side, the non-compliance or control

failures cause for the significant loss of the business, producing the depressed stock market

valuations, distracting the senior management from their tasks, and even substantial threatening

cost (McKinsey& Company, 2015).

But, nowadays the modern businesses more focus on the competitive support than the

compliance and control for achieving the business objectives and strategic goals. The effective

control and compliance provide guidelines and regulations for performing the financial

functions, management of accounting operations, and auditing standards. Todays’ auditors,

accountants, and financial expertise place more emphasis on the competitive support for

achieving the financial, strategic, operational, and management objectives. The competitive

forces drive the firm for the changes in the accounting policies, auditing standards, financial

measures and statistics through installation of new accounting software system, knowledge

management practices, and information and communication technologies.

The modern business organizations look for the competitive support for creating the competitive

advantage instead of avoiding the trap of compliance and control. The intensity of the market

competition encourages the companies for using the standardized management accounting

practices to compete with the competitors and make better decisions (Nair &Nian, 2017). The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting Report 5

competitive support enforces the business firms to make changes in the internal operational

processes, financial policies, and accounting system in adapting to the external environmental

fluctuations/ uncertainties and industry dynamics.

Factors Contributing to the Development of Management Accounting Practices

Both external (market competition and environmental uncertainties) and internal factors

(organizational structure, strategy, business size, the nature of a firm, and business line)

contribute to the development of the management accounting practices. The MA practices are

influenced by the factors, like the organizational size, corporate governance, stakeholders’

expectations, qualification level and experiences of the accounting staff, the intensity of the

competitive factors, and advanced production technologies.The corporate governance affects the

evolution of the MA practices because it sets structures, legal procedures, and policies for

enforcing the laws and regulatory environment for following the effective management

accounting practices through the internal control system, auditing standards, and accounting

information system software (CIMA, 2017).

The accounting information system is a factor, responsible for the accountability of the decisions

by increasing access to the information related to the financial, operational, customers, markets,

growth, and competitors for developing the strategic planning accordingly.The factors, like the

competitive support, stakeholders’ expectations and changing clients’ preferences and demand

patterns also encourage the SMEs or large corporations to maximize the standards of the

management accounting practices. In the sequence, these factors encourage the firms to consider

or allow the knowledge management tools (decision-support system, groupware, OLAP, Data

Analytics, IoT, Documented Management System, Information Management System, and

simulation tools) and information and communication technologies (e-commerce, EDI, extranet,

competitive support enforces the business firms to make changes in the internal operational

processes, financial policies, and accounting system in adapting to the external environmental

fluctuations/ uncertainties and industry dynamics.

Factors Contributing to the Development of Management Accounting Practices

Both external (market competition and environmental uncertainties) and internal factors

(organizational structure, strategy, business size, the nature of a firm, and business line)

contribute to the development of the management accounting practices. The MA practices are

influenced by the factors, like the organizational size, corporate governance, stakeholders’

expectations, qualification level and experiences of the accounting staff, the intensity of the

competitive factors, and advanced production technologies.The corporate governance affects the

evolution of the MA practices because it sets structures, legal procedures, and policies for

enforcing the laws and regulatory environment for following the effective management

accounting practices through the internal control system, auditing standards, and accounting

information system software (CIMA, 2017).

The accounting information system is a factor, responsible for the accountability of the decisions

by increasing access to the information related to the financial, operational, customers, markets,

growth, and competitors for developing the strategic planning accordingly.The factors, like the

competitive support, stakeholders’ expectations and changing clients’ preferences and demand

patterns also encourage the SMEs or large corporations to maximize the standards of the

management accounting practices. In the sequence, these factors encourage the firms to consider

or allow the knowledge management tools (decision-support system, groupware, OLAP, Data

Analytics, IoT, Documented Management System, Information Management System, and

simulation tools) and information and communication technologies (e-commerce, EDI, extranet,

Management Accounting Report 6

social media, intranet, and video communication applications) for increasing access to the

financial and operational performance.

The customer-oriented activities, globalization factor, the intensity of the competition, corporate

governance structure, accounting policies and techniques, quality-oriented initiatives,

organizational restructuring, information technology, and core competitive aims drive for the

changes in the management accounting practices. The skilled, knowledgeable, and qualified

accounting staffs and expertise auditors assist the management for taking better decisions on

fund management, budget, cash flow, and preparing of the financial statements(Leite, Fernandes,

&Leite, 2015).

The organization size and nature of the business industry is also an important factor for

influencing the accountancy management practices. The firm size, like SMEs, large-scale

business enterprises or MNCs require for the development of the accounting management

practices based on the business requirements and size of the businesses as well as nature of the

businesses (service industries, manufacturing, telecommunication, tourism, hospitality, foods

service or business firms).

Evaluation of the Usefulness of Balance Scorecard Method in the Management Accounting

Practices

The balance scorecard method is a performance measurement tool based on the performance

indicators and critical success factors that plays an important role for ensuring the effectiveness

of the management accounting practices. The BSC measures the financial performance of a firm

by combining the financial control measures with the non-financial control measures. This is

significant in both short-term and long-term financial goals and objectives by linking the internal

processes and business strategy of the firm with the mission, goals, and objectives. The Balance

social media, intranet, and video communication applications) for increasing access to the

financial and operational performance.

The customer-oriented activities, globalization factor, the intensity of the competition, corporate

governance structure, accounting policies and techniques, quality-oriented initiatives,

organizational restructuring, information technology, and core competitive aims drive for the

changes in the management accounting practices. The skilled, knowledgeable, and qualified

accounting staffs and expertise auditors assist the management for taking better decisions on

fund management, budget, cash flow, and preparing of the financial statements(Leite, Fernandes,

&Leite, 2015).

The organization size and nature of the business industry is also an important factor for

influencing the accountancy management practices. The firm size, like SMEs, large-scale

business enterprises or MNCs require for the development of the accounting management

practices based on the business requirements and size of the businesses as well as nature of the

businesses (service industries, manufacturing, telecommunication, tourism, hospitality, foods

service or business firms).

Evaluation of the Usefulness of Balance Scorecard Method in the Management Accounting

Practices

The balance scorecard method is a performance measurement tool based on the performance

indicators and critical success factors that plays an important role for ensuring the effectiveness

of the management accounting practices. The BSC measures the financial performance of a firm

by combining the financial control measures with the non-financial control measures. This is

significant in both short-term and long-term financial goals and objectives by linking the internal

processes and business strategy of the firm with the mission, goals, and objectives. The Balance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting Report 7

scorecard methodology is aimed at effective monitoring and control of the organizational

business operations. The BSC assists to provide the financial and operational performance and

relates the strategy to the planning in base with the CSFs and PI. It provides a platform for the

integration of both non-financial and financial measures, communicating the feedback of the

strategy, bond with the strategic planning and financial budgets, and increased focus on aligning

the business processes within the organization(Sadi, Vitor, &Antonio, 2010).

The BSC analyzes the firm’s financial performance from four perspectivesincluding the

financial, customers, learning and growth, and internal processes. The financial perspective is

related to maximizing the financial performance of the organization by increasing the revenues,

profits margins, smooth cash flow,and maximum stakeholders’ returns for the firm (CIMA,

2017). The learning and growth perspective is related to ensuring the long-term survival and

growth of the firm through the organizational learning culture and training and development

programs for enhancing the workforce competencies in order to attain the desired outcomes

within the organization.

Figure: Balance Scorecard Method

(Source: CIMA, 2017)

scorecard methodology is aimed at effective monitoring and control of the organizational

business operations. The BSC assists to provide the financial and operational performance and

relates the strategy to the planning in base with the CSFs and PI. It provides a platform for the

integration of both non-financial and financial measures, communicating the feedback of the

strategy, bond with the strategic planning and financial budgets, and increased focus on aligning

the business processes within the organization(Sadi, Vitor, &Antonio, 2010).

The BSC analyzes the firm’s financial performance from four perspectivesincluding the

financial, customers, learning and growth, and internal processes. The financial perspective is

related to maximizing the financial performance of the organization by increasing the revenues,

profits margins, smooth cash flow,and maximum stakeholders’ returns for the firm (CIMA,

2017). The learning and growth perspective is related to ensuring the long-term survival and

growth of the firm through the organizational learning culture and training and development

programs for enhancing the workforce competencies in order to attain the desired outcomes

within the organization.

Figure: Balance Scorecard Method

(Source: CIMA, 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting Report 8

The customer perspective is related to enhancing the customer satisfaction by satisfying their

needs, wants, and expectations through the effective customer service delivery. The internal

business process perspective is related to enhancing the effectiveness and efficiency of the

internal business processes and operations for improving the organizational production outcomes

and performance measures by reducing the operating costs, delays, defects, and manpower

efforts. The BSC could be useful in the SMEs or MNCs for clearly defining strategy,

communicating the strategy with the team members, aligning the organizational goals and

objectives with the strategy, linking the strategic components with the annual budgets and long-

term targets, aligning the strategic initiatives and conducting the periodic performance reviews

for bring improvement in the management accounting practices (Cooper, 2017).

The BSC could be useful in identifying the critical success factors (CSFs), key performance

indicators for the efficient production outcomes, creating an effective informational system, data

capture, and measurement system, and developing effective mechanisms to report to the

managers and staffs. It is useful to improve the performance of the internal outcomes and

resulting external outcomes and making better decisions based on the collected data and useful

information. The BSC could be useful for the firms in mapping strategy accordingly for adding

value to the firm and its stakeholders.

The customer perspective is related to enhancing the customer satisfaction by satisfying their

needs, wants, and expectations through the effective customer service delivery. The internal

business process perspective is related to enhancing the effectiveness and efficiency of the

internal business processes and operations for improving the organizational production outcomes

and performance measures by reducing the operating costs, delays, defects, and manpower

efforts. The BSC could be useful in the SMEs or MNCs for clearly defining strategy,

communicating the strategy with the team members, aligning the organizational goals and

objectives with the strategy, linking the strategic components with the annual budgets and long-

term targets, aligning the strategic initiatives and conducting the periodic performance reviews

for bring improvement in the management accounting practices (Cooper, 2017).

The BSC could be useful in identifying the critical success factors (CSFs), key performance

indicators for the efficient production outcomes, creating an effective informational system, data

capture, and measurement system, and developing effective mechanisms to report to the

managers and staffs. It is useful to improve the performance of the internal outcomes and

resulting external outcomes and making better decisions based on the collected data and useful

information. The BSC could be useful for the firms in mapping strategy accordingly for adding

value to the firm and its stakeholders.

Management Accounting Report 9

Part B Management Accounting Practices in Qantas Airlines

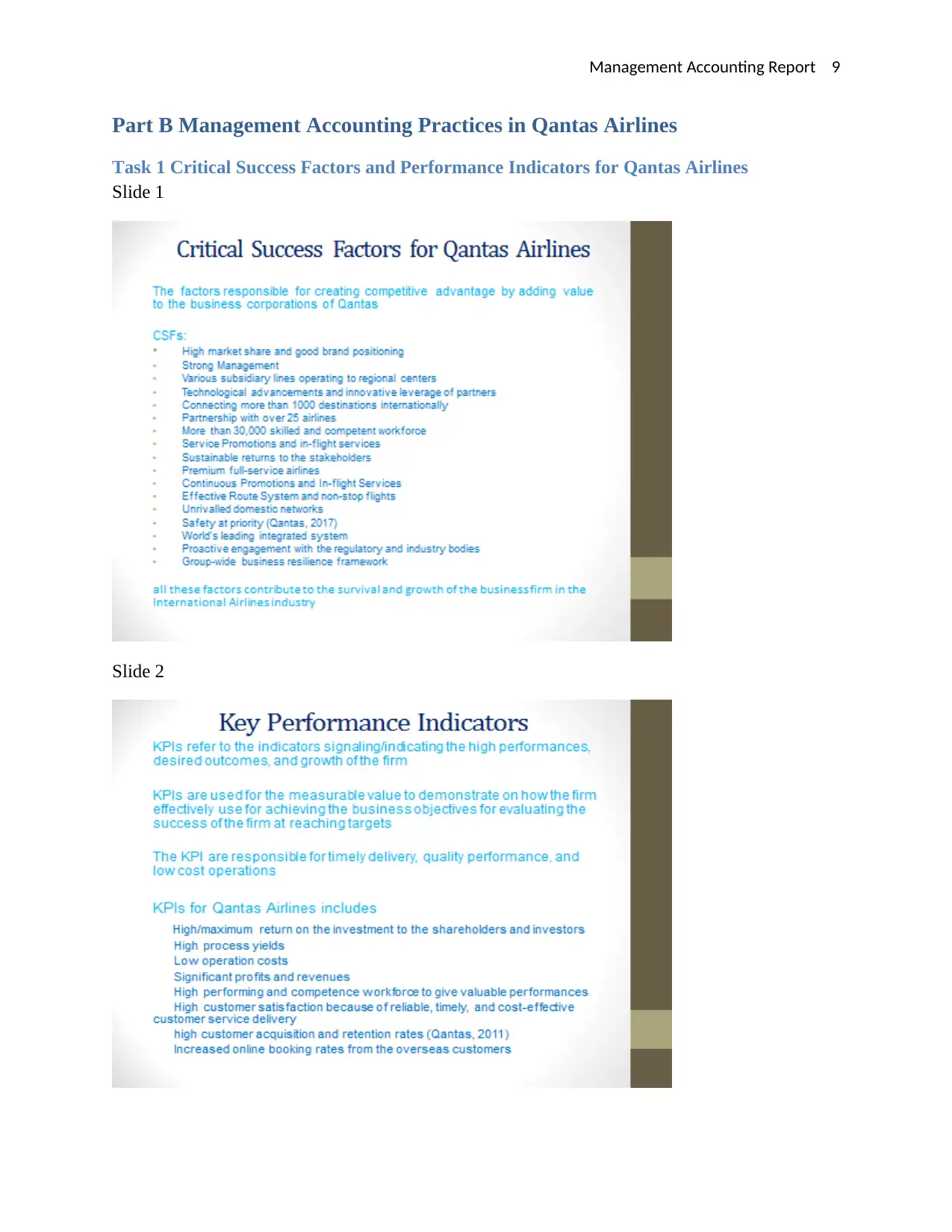

Task 1 Critical Success Factors and Performance Indicators for Qantas Airlines

Slide 1

Slide 2

Part B Management Accounting Practices in Qantas Airlines

Task 1 Critical Success Factors and Performance Indicators for Qantas Airlines

Slide 1

Slide 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting Report 10

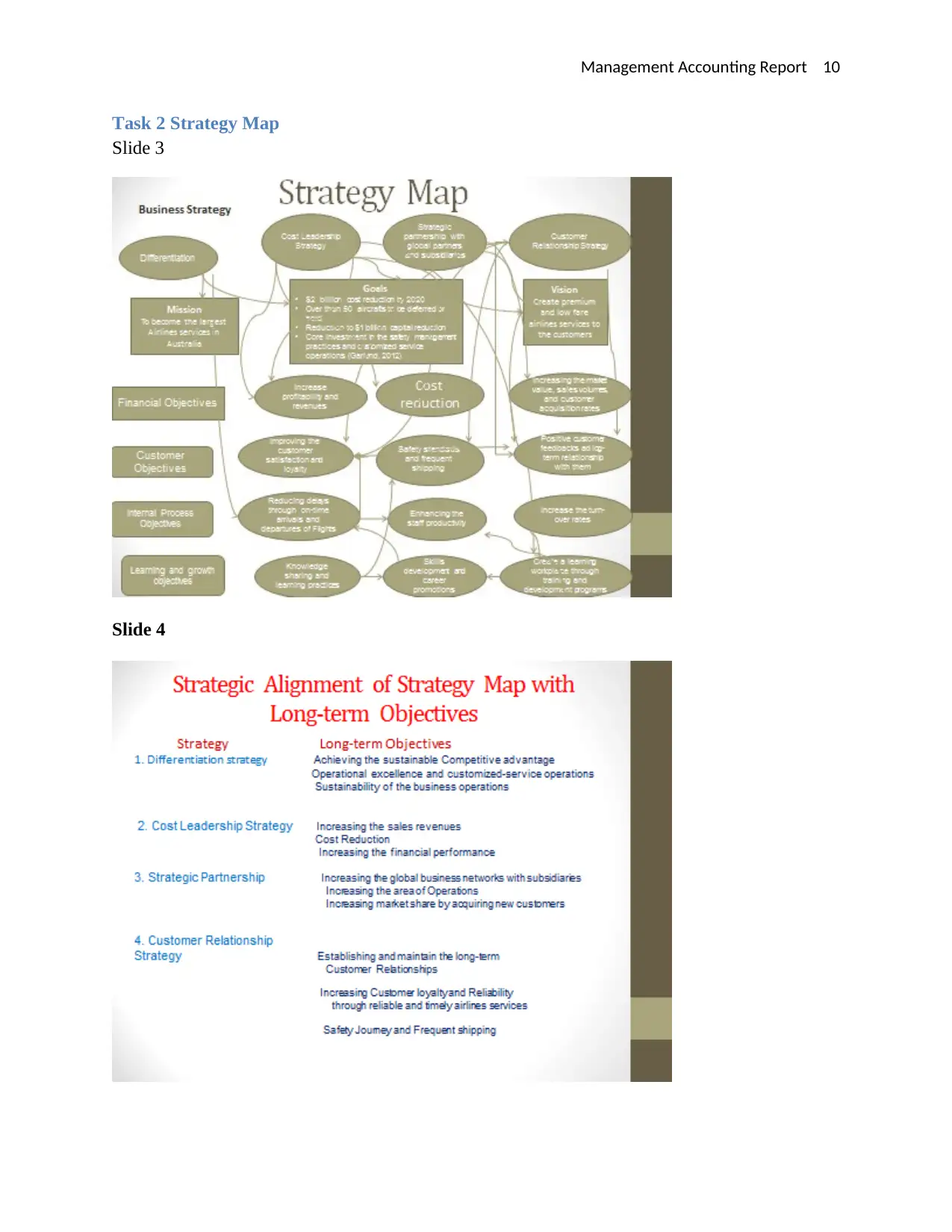

Task 2 Strategy Map

Slide 3

Slide 4

Task 2 Strategy Map

Slide 3

Slide 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting Report 11

Task 3 Balance Scorecard

Slide 5

Task 3 Balance Scorecard

Slide 5

Management Accounting Report 12

Conclusion

The management accounting process uses the financial data and accounting information for

preparing the financial statements and management accounting records on the regular basis and

accordingly providing appropriate feedback on the accounting system efficiency and financial

performance of the company. The management accounting practices have evolved and developed

significantly to the great extent as a result of increasing influence of the compliance, regulatory

controls, and competitive factors. There are several external and internal organizational factors

that support the mechanism and processes for the development of the management accounting

practices in the service industries or business enterprises. Additionally, the balance scorecard

method justified its usefulness for supporting the management accounting practices because it

provides the performance indicators for improving the financial performance, operational

efficiency through the improvement in the internal processes, customer service operations, and

measures to the organizational growth.

Conclusion

The management accounting process uses the financial data and accounting information for

preparing the financial statements and management accounting records on the regular basis and

accordingly providing appropriate feedback on the accounting system efficiency and financial

performance of the company. The management accounting practices have evolved and developed

significantly to the great extent as a result of increasing influence of the compliance, regulatory

controls, and competitive factors. There are several external and internal organizational factors

that support the mechanism and processes for the development of the management accounting

practices in the service industries or business enterprises. Additionally, the balance scorecard

method justified its usefulness for supporting the management accounting practices because it

provides the performance indicators for improving the financial performance, operational

efficiency through the improvement in the internal processes, customer service operations, and

measures to the organizational growth.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.