University Report: Balanced Scorecard for Retail Pharmacy

VerifiedAdded on 2021/05/31

|28

|7853

|42

Report

AI Summary

This report provides a comprehensive analysis of the Balanced Scorecard (BSC) as a performance measurement system and strategic tool for achieving long-term competitive advantage, particularly within the context of retail community pharmacies. The report explores the evolution and history of the BSC, examining its application in monitoring the transformation of organizational capital. It delves into the four key perspectives of the BSC: customer, learning and growth, internal processes, and financial, illustrating how each contributes to strategic goals. The report reviews existing literature to assess the BSC's suitability as a performance management system, correlating qualitative and quantitative data to predict future outcomes. It discusses the importance of aligning incentives, fostering innovation, and adapting to dynamic environments. The report also highlights the historical context of performance measurement, from financial accounting to the development of multi-dimensional frameworks and the integration of concepts like the triple bottom line. The study concludes by emphasizing the BSC's role in enhancing business transformation and sustaining competitive advantage within the retail sector. The report is a student contribution to Desklib, a platform providing AI-driven study tools for students.

Running head: BALANCED SCORECARD

Balanced Scorecard

University Name

Student Name

Authors’ Note

Balanced Scorecard

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

BALANCED SCORECARD

Executive Summary

Business concerns these days replicate dynamic intricate system and their behaviour cannot

be assessed effectually by means of a reductionist view regarding the same. Competitive

advantage can necessarily be considered as the capability to make the most of various

opportunities that take place both inside as well as outside business concerns and adapt to

satisfy the opportunities. In essence, it is alignment of external as well as internal

environment of business concerns that necessarily generate as well as sustain competitive

advantage. Fundamentally, the utilization of balance scorecard (BSC) as a performance

dimension as well as a strategic tool, contributes to survival of business concerns and success.

In essence, the adoption of BSC contributes towards specific kind of behaviour that is elicited

by means of usage of positive feedback. Basically, acceptable actions can be reinforced by

means of fitting culture (that is to say, norms as well as values) as well as rewards relatable to

the performance. Since the pace of transformation is enhancing, there is persistent demand

for both creativity as well as innovation. Again, agile and at the same time flexible BSC can

act as a strange attractor in particularly agent’s behaviour of the system, functioning in a

tumultuous and dynamic environment. Also, feedback with information is circulated

throughout the entire system, upgrading knowledge and finally enhancing performance in the

course of learning. Business concerns that are able to gain knowledge from business

environment and alter their internal arrangement can survive and time flourish through

alteration, which is considerably affected by strange attractors. Essentially, chaos theory can

aid in comprehending and enhancing the process of transformation through utilization of

balance scorecard.

BALANCED SCORECARD

Executive Summary

Business concerns these days replicate dynamic intricate system and their behaviour cannot

be assessed effectually by means of a reductionist view regarding the same. Competitive

advantage can necessarily be considered as the capability to make the most of various

opportunities that take place both inside as well as outside business concerns and adapt to

satisfy the opportunities. In essence, it is alignment of external as well as internal

environment of business concerns that necessarily generate as well as sustain competitive

advantage. Fundamentally, the utilization of balance scorecard (BSC) as a performance

dimension as well as a strategic tool, contributes to survival of business concerns and success.

In essence, the adoption of BSC contributes towards specific kind of behaviour that is elicited

by means of usage of positive feedback. Basically, acceptable actions can be reinforced by

means of fitting culture (that is to say, norms as well as values) as well as rewards relatable to

the performance. Since the pace of transformation is enhancing, there is persistent demand

for both creativity as well as innovation. Again, agile and at the same time flexible BSC can

act as a strange attractor in particularly agent’s behaviour of the system, functioning in a

tumultuous and dynamic environment. Also, feedback with information is circulated

throughout the entire system, upgrading knowledge and finally enhancing performance in the

course of learning. Business concerns that are able to gain knowledge from business

environment and alter their internal arrangement can survive and time flourish through

alteration, which is considerably affected by strange attractors. Essentially, chaos theory can

aid in comprehending and enhancing the process of transformation through utilization of

balance scorecard.

3

BALANCED SCORECARD

Topic: Using the Balanced Scorecard to Monitor the Transformation of Organisational

Capital, to Sustain Long Term Competitive Advantage in Retail Community Pharmacy in

Malta

Introduction

The current study elucidates illustratively the system of performance measurement that can

be used as a base to oversee the transformation of organizational capital in a bid to sustain

competitive advantage during the long term. For this, the current study embarks upon the

notion of balanced scorecard and elucidates illustratively about evolution and detailed history

of balanced scorecard. Furthermore, this study undertakes analysis of subsisting literature

presented by different scholars on the subject matter under deliberation. This segment

therefore systematically reviews past literature to examine whether BSC can be considered to

be an ideal performance management system for Retail community pharmacy. The study also

culminates with a detailed discussion on the establishment of whether a correlation exists

between the two sets of results (qualitative and quantitative data), that is to say, whether

literature on past events are indicative of future outcomes. Also, the study presents certain

uncommonly agreed upon perspectives that can qualify for inclusion in the balanced

scorecard for addition of value.

Defining Balance Scorecard

The balance scorecard is referred to as a mechanism of performance measurement system

that acts as an attractor tool contributing to enhancement of transformation procedure and

finally to competitive advantage of the corporation (Singh et al. 2018). Fundamentally,

balance scorecard can be utilized by top managers to assist in the process of formulation of

BALANCED SCORECARD

Topic: Using the Balanced Scorecard to Monitor the Transformation of Organisational

Capital, to Sustain Long Term Competitive Advantage in Retail Community Pharmacy in

Malta

Introduction

The current study elucidates illustratively the system of performance measurement that can

be used as a base to oversee the transformation of organizational capital in a bid to sustain

competitive advantage during the long term. For this, the current study embarks upon the

notion of balanced scorecard and elucidates illustratively about evolution and detailed history

of balanced scorecard. Furthermore, this study undertakes analysis of subsisting literature

presented by different scholars on the subject matter under deliberation. This segment

therefore systematically reviews past literature to examine whether BSC can be considered to

be an ideal performance management system for Retail community pharmacy. The study also

culminates with a detailed discussion on the establishment of whether a correlation exists

between the two sets of results (qualitative and quantitative data), that is to say, whether

literature on past events are indicative of future outcomes. Also, the study presents certain

uncommonly agreed upon perspectives that can qualify for inclusion in the balanced

scorecard for addition of value.

Defining Balance Scorecard

The balance scorecard is referred to as a mechanism of performance measurement system

that acts as an attractor tool contributing to enhancement of transformation procedure and

finally to competitive advantage of the corporation (Singh et al. 2018). Fundamentally,

balance scorecard can be utilized by top managers to assist in the process of formulation of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

BALANCED SCORECARD

strategy of the corporation and ways to measure level of performance (Hakkak and Ghodsi

2015). There are different perspectives that can be broadly categorised as learning and growth

perspective, capabilities of the employees, information system as well as capabilities of the

organization.

Four Different Perspectives of the Balanced Scorecard

As rightly indicated by Singh et al. (2018), long term objectives can be illustrated as the

outcome of the firm intending to attain over a specified time period. Chiarini (2016) says that

managers can be able to scope their own target in four different perspectives. This includes

enhancement of revenue from stretched amount of sales to subsisting customers, presentation

of solutions to different targeted clients, enhancement of excellence implementation in a bid

to satisfy demands of the customers by means of continuous enhancements. Also, this also

includes alignment of incentives as well as rewards with the business strategy. Chiarini

(2016) suggests that grand strategy can be referred to as a grand strategy that is necessarily a

comprehensive tactic guiding diverse major activities formulated to achieve long term

objectives.

-Perspective of customer: Long term outlook implies offering complete solutions to targeted

customers. Nonetheless, employees have the need to realize the position they intend to arrive

at. There are numerous business entities that have a corporate mission to concentrate on

specifically customers (Mehralian et al. 2017). Hence, performance of a business entity from

the perspective of the customers has now become a priority for firm’s management.

Distinctly, in case if business units intend to attain long term superior financial performance,

then they have the need to generate and deliver better financial performance. There is also

need to generate as well as deliver products/services that are necessarily valued by clients.

Wu and Liao (2014) suggests that the customer perspective can help business concerns to

BALANCED SCORECARD

strategy of the corporation and ways to measure level of performance (Hakkak and Ghodsi

2015). There are different perspectives that can be broadly categorised as learning and growth

perspective, capabilities of the employees, information system as well as capabilities of the

organization.

Four Different Perspectives of the Balanced Scorecard

As rightly indicated by Singh et al. (2018), long term objectives can be illustrated as the

outcome of the firm intending to attain over a specified time period. Chiarini (2016) says that

managers can be able to scope their own target in four different perspectives. This includes

enhancement of revenue from stretched amount of sales to subsisting customers, presentation

of solutions to different targeted clients, enhancement of excellence implementation in a bid

to satisfy demands of the customers by means of continuous enhancements. Also, this also

includes alignment of incentives as well as rewards with the business strategy. Chiarini

(2016) suggests that grand strategy can be referred to as a grand strategy that is necessarily a

comprehensive tactic guiding diverse major activities formulated to achieve long term

objectives.

-Perspective of customer: Long term outlook implies offering complete solutions to targeted

customers. Nonetheless, employees have the need to realize the position they intend to arrive

at. There are numerous business entities that have a corporate mission to concentrate on

specifically customers (Mehralian et al. 2017). Hence, performance of a business entity from

the perspective of the customers has now become a priority for firm’s management.

Distinctly, in case if business units intend to attain long term superior financial performance,

then they have the need to generate and deliver better financial performance. There is also

need to generate as well as deliver products/services that are necessarily valued by clients.

Wu and Liao (2014) suggests that the customer perspective can help business concerns to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

BALANCED SCORECARD

align customer outcome dimensions that include share of the market, acquisition as well as

retention of customers, satisfaction of the customers, profitability of customers, targeted set

of customers as well as specific market fragments. Essentially, this also aids in recognition

and at the same time measurement, explicitly, specific value propositions that they distribute

to different target customers along with market segments (Malagueño et al. 2017). In itself,

value proposition replicates different drivers together with the lead indicators for customer

outcome dimensions.

-Learning and growth: The perspective of learning as well as growth can align incentives

along with rewards of the employees with the stratagem. This dimension of the balance

scorecard effectively helps in augmentation of three different groups in a business concern. In

particular, human resources that concentrates on development strategies can help in attracting

as well as retaining talents. Again, learning and growth dimension also affects the group

namely, information technology (Dudin and Frolova 2015). In particular information

technology also delivers applications that upholds strategy, develops data of customers along

with information system. In addition to this, the perspective of organizational culture also

enhances culture of the organization and alignment also generates a customer-centric culture,

align objectives of the employees to accomplishment, sharing knowledge regarding best

exercises and customers.

-Perspective of internal processes: At a time when a corporation can distinctly shape

objectives regarding what they intend to deliver can help in determining strategies.

Essentially, internal procedures can be regarded as the core factor of attainment. Perkins et al.

(2014) suggest that managers have the need to define a all-inclusive internal process that

starts with innovation functions (recognizing existing as well as future needs of the customers

and thereafter designing a new solution to satisfy the identified requirements). The internal

process continues by means of operational processes (that includes delivering subsisting

BALANCED SCORECARD

align customer outcome dimensions that include share of the market, acquisition as well as

retention of customers, satisfaction of the customers, profitability of customers, targeted set

of customers as well as specific market fragments. Essentially, this also aids in recognition

and at the same time measurement, explicitly, specific value propositions that they distribute

to different target customers along with market segments (Malagueño et al. 2017). In itself,

value proposition replicates different drivers together with the lead indicators for customer

outcome dimensions.

-Learning and growth: The perspective of learning as well as growth can align incentives

along with rewards of the employees with the stratagem. This dimension of the balance

scorecard effectively helps in augmentation of three different groups in a business concern. In

particular, human resources that concentrates on development strategies can help in attracting

as well as retaining talents. Again, learning and growth dimension also affects the group

namely, information technology (Dudin and Frolova 2015). In particular information

technology also delivers applications that upholds strategy, develops data of customers along

with information system. In addition to this, the perspective of organizational culture also

enhances culture of the organization and alignment also generates a customer-centric culture,

align objectives of the employees to accomplishment, sharing knowledge regarding best

exercises and customers.

-Perspective of internal processes: At a time when a corporation can distinctly shape

objectives regarding what they intend to deliver can help in determining strategies.

Essentially, internal procedures can be regarded as the core factor of attainment. Perkins et al.

(2014) suggest that managers have the need to define a all-inclusive internal process that

starts with innovation functions (recognizing existing as well as future needs of the customers

and thereafter designing a new solution to satisfy the identified requirements). The internal

process continues by means of operational processes (that includes delivering subsisting

6

BALANCED SCORECARD

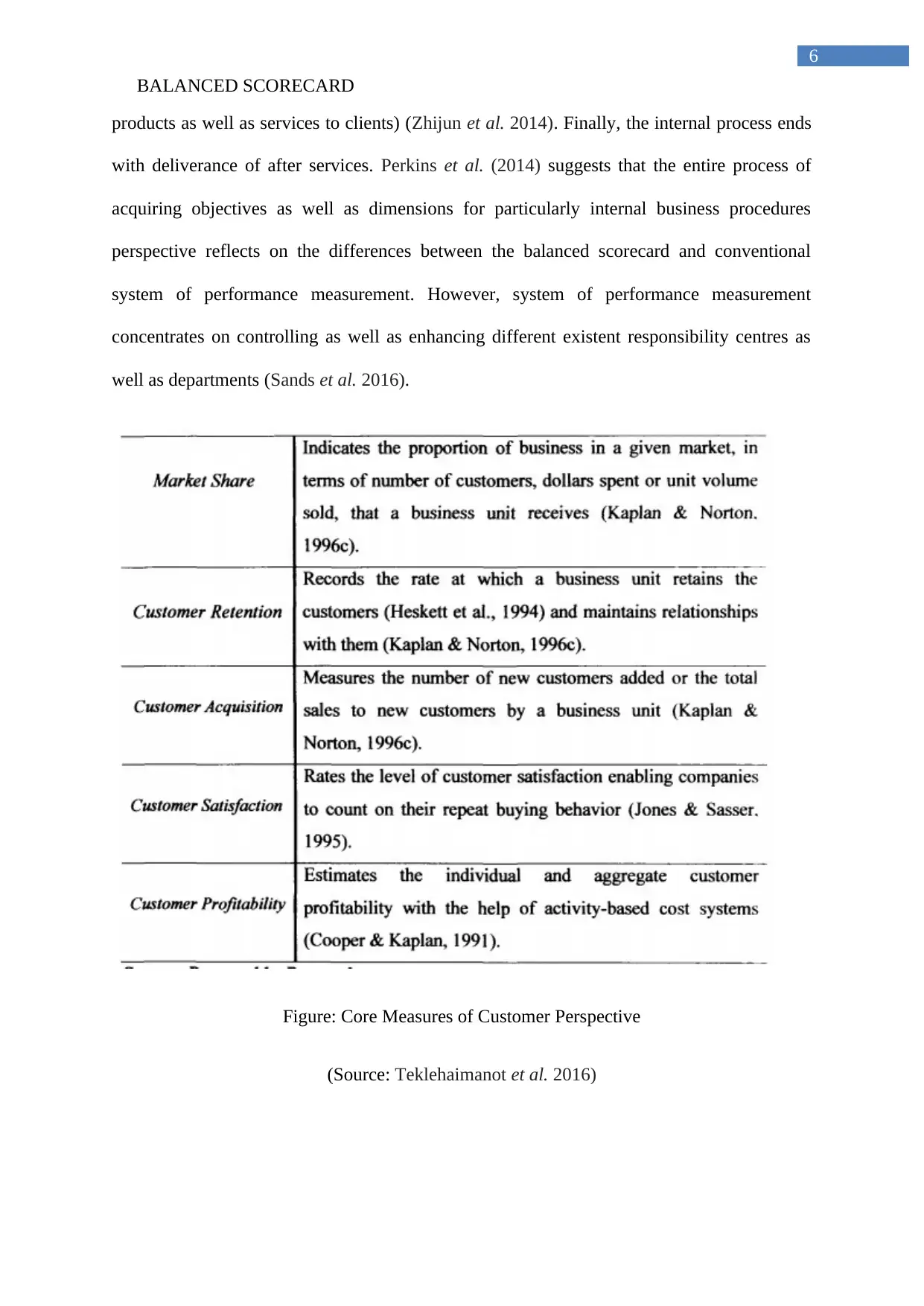

products as well as services to clients) (Zhijun et al. 2014). Finally, the internal process ends

with deliverance of after services. Perkins et al. (2014) suggests that the entire process of

acquiring objectives as well as dimensions for particularly internal business procedures

perspective reflects on the differences between the balanced scorecard and conventional

system of performance measurement. However, system of performance measurement

concentrates on controlling as well as enhancing different existent responsibility centres as

well as departments (Sands et al. 2016).

Figure: Core Measures of Customer Perspective

(Source: Teklehaimanot et al. 2016)

BALANCED SCORECARD

products as well as services to clients) (Zhijun et al. 2014). Finally, the internal process ends

with deliverance of after services. Perkins et al. (2014) suggests that the entire process of

acquiring objectives as well as dimensions for particularly internal business procedures

perspective reflects on the differences between the balanced scorecard and conventional

system of performance measurement. However, system of performance measurement

concentrates on controlling as well as enhancing different existent responsibility centres as

well as departments (Sands et al. 2016).

Figure: Core Measures of Customer Perspective

(Source: Teklehaimanot et al. 2016)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

BALANCED SCORECARD

Financial Perspective

As rightly indicated by Teklehaimanot et al. (2016), balanced scorecard is said to keep hold

of financial perspective as financial dimensions can be considered to be important in

summarizing different measureable economic upshots of activities already undertaken.

Fundamentally, financial performance dimensions replicate whether the strategy of the

company, process of implementation along with execution can contribute towards

augmentation of bottom line. Common financial goals relatable to firm’s profitability are

enumerated by operating earnings, return earned on employed capital or else economic value

added (Alolah et al. 2014).

In itself, there are three recognized stages of life cycle of business, namely, growth, sustain

and thereafter harvest. Growth phase refers to the early stage of the business lifecycle during

which products/services of the company has considerable growth potential (Agrawal et al.

2016). However, corporations operating at the sustain stage can attract huge investment as

well as reinvestment, however have the need to receive adequate returns on firm’s invested

capital. In essence, these businesses are probable to maintain their subsisting share of the

market and develop their business (Perramon et al. 2016). Thereafter, at the time when

business entities reach maturity phase of business life cycle, the entity harvests the

investments undertaken in the prior two stages. The main objective of this phase is to

optimize flow of cash to the business concern.

BALANCED SCORECARD

Financial Perspective

As rightly indicated by Teklehaimanot et al. (2016), balanced scorecard is said to keep hold

of financial perspective as financial dimensions can be considered to be important in

summarizing different measureable economic upshots of activities already undertaken.

Fundamentally, financial performance dimensions replicate whether the strategy of the

company, process of implementation along with execution can contribute towards

augmentation of bottom line. Common financial goals relatable to firm’s profitability are

enumerated by operating earnings, return earned on employed capital or else economic value

added (Alolah et al. 2014).

In itself, there are three recognized stages of life cycle of business, namely, growth, sustain

and thereafter harvest. Growth phase refers to the early stage of the business lifecycle during

which products/services of the company has considerable growth potential (Agrawal et al.

2016). However, corporations operating at the sustain stage can attract huge investment as

well as reinvestment, however have the need to receive adequate returns on firm’s invested

capital. In essence, these businesses are probable to maintain their subsisting share of the

market and develop their business (Perramon et al. 2016). Thereafter, at the time when

business entities reach maturity phase of business life cycle, the entity harvests the

investments undertaken in the prior two stages. The main objective of this phase is to

optimize flow of cash to the business concern.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

BALANCED SCORECARD

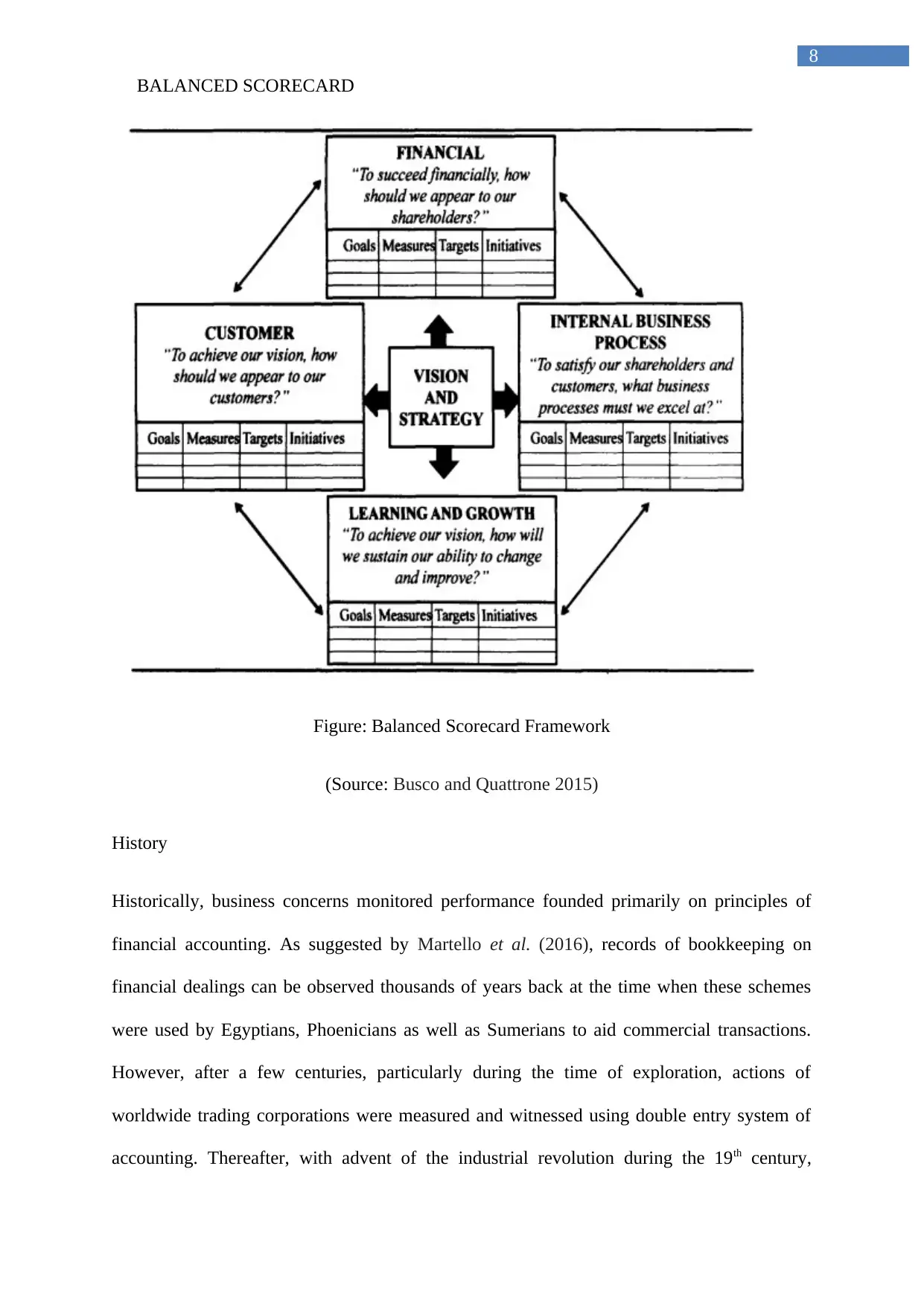

Figure: Balanced Scorecard Framework

(Source: Busco and Quattrone 2015)

History

Historically, business concerns monitored performance founded primarily on principles of

financial accounting. As suggested by Martello et al. (2016), records of bookkeeping on

financial dealings can be observed thousands of years back at the time when these schemes

were used by Egyptians, Phoenicians as well as Sumerians to aid commercial transactions.

However, after a few centuries, particularly during the time of exploration, actions of

worldwide trading corporations were measured and witnessed using double entry system of

accounting. Thereafter, with advent of the industrial revolution during the 19th century,

BALANCED SCORECARD

Figure: Balanced Scorecard Framework

(Source: Busco and Quattrone 2015)

History

Historically, business concerns monitored performance founded primarily on principles of

financial accounting. As suggested by Martello et al. (2016), records of bookkeeping on

financial dealings can be observed thousands of years back at the time when these schemes

were used by Egyptians, Phoenicians as well as Sumerians to aid commercial transactions.

However, after a few centuries, particularly during the time of exploration, actions of

worldwide trading corporations were measured and witnessed using double entry system of

accounting. Thereafter, with advent of the industrial revolution during the 19th century,

9

BALANCED SCORECARD

evaluation of financial performance using innovative methods began. During the period

1970s-80s a common expression of dissatisfaction with the conventional financial dimensions

became widespread (Zizlavsky 2014). However, during the period of 1980s and the period of

early 1990s, this dissatisfaction directed to a series of multi-dimensional performance

measurement structures.

In essence, the conceptual foundation for specifically balanced scorecard was designed

during the period 1980s-1990s by numerous academicians as well as practitioners in diverse

fields namely management accounting, performance enumeration plus accounting. During the

period 1990s, the Tableau de Board was developed by a French academician (Coe and Letza

2014). This was a performance measurement mechanism by engineers that associated

stratagems to both financial as well as non-financial dimensions. Regrettably, Tableau de

Board was certainly not brought into practice. During the period 1920s DuPont Corporation

developed the performance measurement system that concentrated on return on investment

calculations that again directed to the use of numerous financial ratios (Lawrie and Sulver

2015). Thereafter, period of Post-World War II actions shifted the concentration on

initiatives on quality as well as measurement of quality that again led to upshot that were not

exclusively financial. Hansen and Schaltegger (2016) correctly mentioned that Activity

Based Costing can be considered as the unique thought that directed towards development of

the framework of Balanced Scorecard. Bergeron (2017) mentions that activity based costing

is an accounting process of assigning costs of resources by means of diverse activities

undertaken to design products/services for different customers. As such, this is an attempt to

comprehend superior product, costs of customers as well as productivity. Bergeron (2017)

recommended a balanced view on operations of the corporation consisting of different

financial dimensions along with dimensions associated to strategy of marketing, works of

research and development, maintenance of social accountabilities and welfare of employees.

BALANCED SCORECARD

evaluation of financial performance using innovative methods began. During the period

1970s-80s a common expression of dissatisfaction with the conventional financial dimensions

became widespread (Zizlavsky 2014). However, during the period of 1980s and the period of

early 1990s, this dissatisfaction directed to a series of multi-dimensional performance

measurement structures.

In essence, the conceptual foundation for specifically balanced scorecard was designed

during the period 1980s-1990s by numerous academicians as well as practitioners in diverse

fields namely management accounting, performance enumeration plus accounting. During the

period 1990s, the Tableau de Board was developed by a French academician (Coe and Letza

2014). This was a performance measurement mechanism by engineers that associated

stratagems to both financial as well as non-financial dimensions. Regrettably, Tableau de

Board was certainly not brought into practice. During the period 1920s DuPont Corporation

developed the performance measurement system that concentrated on return on investment

calculations that again directed to the use of numerous financial ratios (Lawrie and Sulver

2015). Thereafter, period of Post-World War II actions shifted the concentration on

initiatives on quality as well as measurement of quality that again led to upshot that were not

exclusively financial. Hansen and Schaltegger (2016) correctly mentioned that Activity

Based Costing can be considered as the unique thought that directed towards development of

the framework of Balanced Scorecard. Bergeron (2017) mentions that activity based costing

is an accounting process of assigning costs of resources by means of diverse activities

undertaken to design products/services for different customers. As such, this is an attempt to

comprehend superior product, costs of customers as well as productivity. Bergeron (2017)

recommended a balanced view on operations of the corporation consisting of different

financial dimensions along with dimensions associated to strategy of marketing, works of

research and development, maintenance of social accountabilities and welfare of employees.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

BALANCED SCORECARD

The notions of triple bottom line with social accounting were necessarily introduced during

the period 1990s (Pimentel and Major 2014). These concepts were popularized in response to

the need to track and at the same time confirm corporate profits. Triple Bottom Line is

necessarily a performance reporting framework concentrated on sustainability necessities of

business concerns worldwide (Hoque 2014). In actual fact, this notion suggests concentration

on three social responsibilities that include enhancing economic prosperity, environmental

protection as well as social equity. The advent of the information era during the 20th century

made several suppositions of the industrial age outmoded. Bergeron (2017) highlighted that

continual enhancement methodologies namely total quality management, reengineering of

business processes along with involvement of employees stress the requirement of

performance dimensions for delivering impetus to this kind of performance enhancements.

Throughout the years, the balanced scorecard evolved from being a performance

measurement tool introduced by Kaplan and Norton to an effective tool for implementation

of strategies. Keyes (2016) pointed out that the balanced scorecard can acknowledge diverse

deficiencies in different system of business performance measurement. This system is

entirely dependent on financial dimensions and endeavours to overcome the deficiencies of

subsisting measurement systems by way of enumerating and evaluating outcomes across

wide range of actions. Hansen and Schaltegger (2016) mention three different stakeholders

namely, shareholders (financial point of view), customers (associations with customers) and

employees (referring to internal business procedures along with learning and growth).

However, this concept ignores two important stakeholders namely environmental as well as

social matters. This leads to examination of justification of inclusion of other factors in the

framework (de Andrade et al. 2016).

BALANCED SCORECARD

The notions of triple bottom line with social accounting were necessarily introduced during

the period 1990s (Pimentel and Major 2014). These concepts were popularized in response to

the need to track and at the same time confirm corporate profits. Triple Bottom Line is

necessarily a performance reporting framework concentrated on sustainability necessities of

business concerns worldwide (Hoque 2014). In actual fact, this notion suggests concentration

on three social responsibilities that include enhancing economic prosperity, environmental

protection as well as social equity. The advent of the information era during the 20th century

made several suppositions of the industrial age outmoded. Bergeron (2017) highlighted that

continual enhancement methodologies namely total quality management, reengineering of

business processes along with involvement of employees stress the requirement of

performance dimensions for delivering impetus to this kind of performance enhancements.

Throughout the years, the balanced scorecard evolved from being a performance

measurement tool introduced by Kaplan and Norton to an effective tool for implementation

of strategies. Keyes (2016) pointed out that the balanced scorecard can acknowledge diverse

deficiencies in different system of business performance measurement. This system is

entirely dependent on financial dimensions and endeavours to overcome the deficiencies of

subsisting measurement systems by way of enumerating and evaluating outcomes across

wide range of actions. Hansen and Schaltegger (2016) mention three different stakeholders

namely, shareholders (financial point of view), customers (associations with customers) and

employees (referring to internal business procedures along with learning and growth).

However, this concept ignores two important stakeholders namely environmental as well as

social matters. This leads to examination of justification of inclusion of other factors in the

framework (de Andrade et al. 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

BALANCED SCORECARD

Opinions on BSC

Recent researches on balance scorecard in retail setting

Prior literature indicates towards the fact that for a balance scorecard to generate optimal

performance, different facets need to be part of the arrangement. Studies conducted by

academicians stresses on two different facets namely, effectiveness of information and

support of managers of the entire system. Essentially, employees have the need to understand

that system delivers effectual information (Cooper et al. 2017). Case studies on retailer

namely Wildcat was hugely supportive of project as represented in the participation rate of

survey of over and above 72%. Particularly, Wildcat managers notices that balanced

scorecard is normally advantageous and this report about a positive attitude towards the same.

Furthermore, managers can report favourable awareness for most of the characteristics of

BSC along with functionality. It is also observed that positive managerial approaches towards

BSC are related to higher scores (Bobe et al. 2017). This in turn can be related to higher

financial performance. In case of retailers, conventional financial dimension at the operating

management level is actual sales compared to sales relative to specifically budgeted sales. A

corporation is a small number of merchandising corporations that is in charge of large

proportion of retail market of the product (Coe and Letza 2014). Different conventional

financial profit dimensions that are delayed until the end of reporting period, sales-to-plan

information is available virtually on demand by the manager. Essentially, an issue is about

timeliness in retail setting in which managers concentrate on data on sales (Hawari and Tahar

2015). The utilization of multi-dimensional performance measurement system that

incorporates varied non-financial measures can lead to delayed process of reporting

compared to sales based financial measures.

BALANCED SCORECARD

Opinions on BSC

Recent researches on balance scorecard in retail setting

Prior literature indicates towards the fact that for a balance scorecard to generate optimal

performance, different facets need to be part of the arrangement. Studies conducted by

academicians stresses on two different facets namely, effectiveness of information and

support of managers of the entire system. Essentially, employees have the need to understand

that system delivers effectual information (Cooper et al. 2017). Case studies on retailer

namely Wildcat was hugely supportive of project as represented in the participation rate of

survey of over and above 72%. Particularly, Wildcat managers notices that balanced

scorecard is normally advantageous and this report about a positive attitude towards the same.

Furthermore, managers can report favourable awareness for most of the characteristics of

BSC along with functionality. It is also observed that positive managerial approaches towards

BSC are related to higher scores (Bobe et al. 2017). This in turn can be related to higher

financial performance. In case of retailers, conventional financial dimension at the operating

management level is actual sales compared to sales relative to specifically budgeted sales. A

corporation is a small number of merchandising corporations that is in charge of large

proportion of retail market of the product (Coe and Letza 2014). Different conventional

financial profit dimensions that are delayed until the end of reporting period, sales-to-plan

information is available virtually on demand by the manager. Essentially, an issue is about

timeliness in retail setting in which managers concentrate on data on sales (Hawari and Tahar

2015). The utilization of multi-dimensional performance measurement system that

incorporates varied non-financial measures can lead to delayed process of reporting

compared to sales based financial measures.

12

BALANCED SCORECARD

Balanced scorecard can be used to enhance retail operations. For example, Tesco Plc can be

considered to be a worldwide as well as general merchandising retail firm established in the

UK. In this company, the property team is said to be at the central part of ongoing concern.

Essentially, operations particularly in property includes diverse aspects of purchasing,

building to particularly maintaining the stores. The company uses balanced scorecard for the

purpose of driving performance in the area of property segment of the business. Management

of the firm is of the view that basic principle of any system of measurement is essentially to

highlight specific areas of improvement (Coe and Letza 2014). In case if one fails to

enumerate, then it becomes difficult to control or else improve the operations. Therefore,

steering wheel can be considered to be an important instrument to gauge performance and to

steer overall business in the correct direction. By means of corporate governance, both

systems and framework to uphold in position, this can be considered to be vast value-add to

any kind of business. Particularly, at the firm Tesco, management use Steering Wheel that

was developed based on the principles of a balanced scorecard (Beard and Humphrey 2014).

Essentially, this was quickly as well as effectually rolled to diverse departments of the

company and is an important part of administration strategy at diverse echelons. As

mentioned in a study by Chiarini (2016), the stores of Tesco have a visual display of the

particular steering wheel and key dimensions behind it can be updated each and every week

for members of the staff to operate in a single direction. Especially within the role,

management of the firm utilize the steering wheel as a part of agenda of the meeting on

property leadership for making certain that the focus is at the top level. In itself, any kind of

under-performing dimensions thereafter are put forward in the meeting with appropriate plan

of action as well as timeliness. In essence, this is also complimented by particularly a visible

along with effective plan of communication for essentially the steering wheel. This takes in

display of wheel, summary as well as actions and diverse change projects that are initiated to

BALANCED SCORECARD

Balanced scorecard can be used to enhance retail operations. For example, Tesco Plc can be

considered to be a worldwide as well as general merchandising retail firm established in the

UK. In this company, the property team is said to be at the central part of ongoing concern.

Essentially, operations particularly in property includes diverse aspects of purchasing,

building to particularly maintaining the stores. The company uses balanced scorecard for the

purpose of driving performance in the area of property segment of the business. Management

of the firm is of the view that basic principle of any system of measurement is essentially to

highlight specific areas of improvement (Coe and Letza 2014). In case if one fails to

enumerate, then it becomes difficult to control or else improve the operations. Therefore,

steering wheel can be considered to be an important instrument to gauge performance and to

steer overall business in the correct direction. By means of corporate governance, both

systems and framework to uphold in position, this can be considered to be vast value-add to

any kind of business. Particularly, at the firm Tesco, management use Steering Wheel that

was developed based on the principles of a balanced scorecard (Beard and Humphrey 2014).

Essentially, this was quickly as well as effectually rolled to diverse departments of the

company and is an important part of administration strategy at diverse echelons. As

mentioned in a study by Chiarini (2016), the stores of Tesco have a visual display of the

particular steering wheel and key dimensions behind it can be updated each and every week

for members of the staff to operate in a single direction. Especially within the role,

management of the firm utilize the steering wheel as a part of agenda of the meeting on

property leadership for making certain that the focus is at the top level. In itself, any kind of

under-performing dimensions thereafter are put forward in the meeting with appropriate plan

of action as well as timeliness. In essence, this is also complimented by particularly a visible

along with effective plan of communication for essentially the steering wheel. This takes in

display of wheel, summary as well as actions and diverse change projects that are initiated to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.