Critical Evaluation of Development and Role of Balanced Scorecard

VerifiedAdded on 2019/12/03

|13

|3875

|429

Report

AI Summary

This report provides a critical evaluation of the development and role of the balanced scorecard (BSC) in production and service organizations. The report begins with an introduction to the BSC as a strategic performance tool used for aligning business activities with organizational vision and strategy. It then explores the development of the BSC, highlighting its origins with Kaplan and Norton and its evolution as a strategic management system. The report discusses the steps involved in developing a BSC, including defining a purpose statement, designing a change agenda, creating a strategic map, developing measures, and setting initiatives. It further analyzes the application of BSC in different organizational contexts, providing examples from companies like Apple Computer and Rockwater. The report also includes a critical analysis of the BSC, its role in strategic management, its advantages, and its limitations. Finally, the report concludes with a summary of the key findings and arguments presented throughout the analysis.

CRITICAL EVALUATION

OF DEVELOPMENT AND

ROLE OF BALANCED

SCORECARD IN

PRODUCTION AND

SERVICE

ORGANIZATIONS

OF DEVELOPMENT AND

ROLE OF BALANCED

SCORECARD IN

PRODUCTION AND

SERVICE

ORGANIZATIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................3

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

ILLUSTRATION INDEX

Illustration 1: Rockwater’s Balanced Scorecard..............................................................................6

2

Introduction......................................................................................................................................3

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

ILLUSTRATION INDEX

Illustration 1: Rockwater’s Balanced Scorecard..............................................................................6

2

INTRODUCTION

Balanced scorecard basically refers to as a strategic performance tool or strategic

planning and management system which is extensively used by every business and non-business

organization in order to align business activities with the vision and strategy of the organization.

Balance scorecard plays a vital role in an organization as it helps in strategic management and it

aids in aligning all the activities of an organization along with vision and strategy (Johanson and

et.al., 2006). This report has been emphasized on the development and role of balance scorecard

in a production as well as in service organization. Further, this report discuss the critical analysis

and argument of role and development of balance scorecard.

Development of Balance Scorecard

Balance scorecard which was developed by Robert Kaplan and David Norton in order to

deal with a problem, for instance, a firm reduce their customer service level so that current

earnings can be boosted but in future earning might get reduce due to reduction in customer

satisfaction. For that purpose, balance score card was developed. It is basically a strategic

performance management tool which is used by managers in order to keep track of the execution

of activities by employees and to monitor the consequences which will arise from their action

(Chavan, 2009). It measures financial data, customer satisfaction, business process and learning

measures. This translate the strategy of organization into four perspectives along with a balance

between the internal and external measures; between objective and subjective measures and

balance between performance results and the future results.

Balance scorecard is developed in a different manner in different organization depending

upon the nature of a company. In production firm it is developed in accordance with a operations

but it is altogether differently developed in a service sector company. Balance scorecard is

developed by following few steps such as firstly company has to build their purpose statement

which includes the information about how company will be different from its competitors and it

also includes objectives of a firm plus advantage plus scope of a company (Gurd and Gao, 2008).

It explains that what company is going to do, where the firm will win and where the organization

is going to do it. Second step is the designing of change agenda which states that change is an

ongoing process. This also states that what company needs so as to make it better for achieving

3

Balanced scorecard basically refers to as a strategic performance tool or strategic

planning and management system which is extensively used by every business and non-business

organization in order to align business activities with the vision and strategy of the organization.

Balance scorecard plays a vital role in an organization as it helps in strategic management and it

aids in aligning all the activities of an organization along with vision and strategy (Johanson and

et.al., 2006). This report has been emphasized on the development and role of balance scorecard

in a production as well as in service organization. Further, this report discuss the critical analysis

and argument of role and development of balance scorecard.

Development of Balance Scorecard

Balance scorecard which was developed by Robert Kaplan and David Norton in order to

deal with a problem, for instance, a firm reduce their customer service level so that current

earnings can be boosted but in future earning might get reduce due to reduction in customer

satisfaction. For that purpose, balance score card was developed. It is basically a strategic

performance management tool which is used by managers in order to keep track of the execution

of activities by employees and to monitor the consequences which will arise from their action

(Chavan, 2009). It measures financial data, customer satisfaction, business process and learning

measures. This translate the strategy of organization into four perspectives along with a balance

between the internal and external measures; between objective and subjective measures and

balance between performance results and the future results.

Balance scorecard is developed in a different manner in different organization depending

upon the nature of a company. In production firm it is developed in accordance with a operations

but it is altogether differently developed in a service sector company. Balance scorecard is

developed by following few steps such as firstly company has to build their purpose statement

which includes the information about how company will be different from its competitors and it

also includes objectives of a firm plus advantage plus scope of a company (Gurd and Gao, 2008).

It explains that what company is going to do, where the firm will win and where the organization

is going to do it. Second step is the designing of change agenda which states that change is an

ongoing process. This also states that what company needs so as to make it better for achieving

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the purpose of an organization. Thirdly, firm should make a map towards the destination in

which lots of wrong turn should be included while on the way to strategy execution. Cause and

effect should also be linked along with the strategic objective. Fourthly, after making a map the

next step is of creating great measures (Soderberg and et. al., 2011). Measures are created for

doing two things that is understanding what is not working in an organization and helps to

motivate. Company has to choose that measure which helps in driving the strategy. Then last

step is to set up some initiatives such as to focus on the strategy a company should stop doing

certain things which is less important. This initiatives has to be taken by firm in order to excel.

These were the few steps which is used in order to develop the balance scorecard.

The format of a BSC differs from company to company depending upon the data, nature

of the company that is manufacturing or service industry. However, some organization uses

spreadsheet and some uses a paragraph style in a word document. Many firms use a software for

the purpose of BSC development (Niven, 2010). Typically, balance scorecard is being used by

the company at the time of strategic planning and organizational change. Because this tool is

used to evaluate the performance of a firm and it helps in assessing the opportunities and threats

which is required to address while outlining the goals and objectives for the future.

Depth and coverage of practical issues and theory

BSC provides managers with a comprehensive framework which translates a strategic

objectives of a company into a consistent set of performance measures. Balance scorecard is not

only a management exercise but it is beyond it. It is a management system which can motivate

for the improvements in a critical areas such as product, process, customer and market

development. Many companies which desire to implement improvement programs such as

process re-engineering, total quality management and employee empowerment which lack a

sense of integration (Bischoff, 2013). At this time, BSC act as a focal point for the organization

in defining and communicating priorities to managers, employees and investors and even

customers. This scorecard is not a template which can be applied to all the businesses in general.

Different market situations, product category, competitive environment need different

scorecards. Every company devise customized scorecards in order to fit their mission, strategy,

technology and culture.

4

which lots of wrong turn should be included while on the way to strategy execution. Cause and

effect should also be linked along with the strategic objective. Fourthly, after making a map the

next step is of creating great measures (Soderberg and et. al., 2011). Measures are created for

doing two things that is understanding what is not working in an organization and helps to

motivate. Company has to choose that measure which helps in driving the strategy. Then last

step is to set up some initiatives such as to focus on the strategy a company should stop doing

certain things which is less important. This initiatives has to be taken by firm in order to excel.

These were the few steps which is used in order to develop the balance scorecard.

The format of a BSC differs from company to company depending upon the data, nature

of the company that is manufacturing or service industry. However, some organization uses

spreadsheet and some uses a paragraph style in a word document. Many firms use a software for

the purpose of BSC development (Niven, 2010). Typically, balance scorecard is being used by

the company at the time of strategic planning and organizational change. Because this tool is

used to evaluate the performance of a firm and it helps in assessing the opportunities and threats

which is required to address while outlining the goals and objectives for the future.

Depth and coverage of practical issues and theory

BSC provides managers with a comprehensive framework which translates a strategic

objectives of a company into a consistent set of performance measures. Balance scorecard is not

only a management exercise but it is beyond it. It is a management system which can motivate

for the improvements in a critical areas such as product, process, customer and market

development. Many companies which desire to implement improvement programs such as

process re-engineering, total quality management and employee empowerment which lack a

sense of integration (Bischoff, 2013). At this time, BSC act as a focal point for the organization

in defining and communicating priorities to managers, employees and investors and even

customers. This scorecard is not a template which can be applied to all the businesses in general.

Different market situations, product category, competitive environment need different

scorecards. Every company devise customized scorecards in order to fit their mission, strategy,

technology and culture.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In a company like Apple Computer, where BSC was developed for adjusting long-term

performance. Apple Computer had developed the BSC for the senior management in order to

focus on a strategy which would expand discussion beyond gross margin, return on equity and

market share. Apple's executive management team took out the measures on four perspective that

is for financial perspective, the company emphasized on shareholders value which was included

for a performance indicator. In contrast, shareholder value metric measures the impact of

proposed investments for business creation and development. This measure therefore, helps

senior managers in each major business units and assess the impact of the activities on the entire

organization's value. For customer perspective, it focused on market development and customer

satisfaction, this metrics has been introduced to direct employees to become customer-driven

company (FUJII, 2014). For the internal process, Apple concentrated on core competencies in

which company wanted to have user-friendly interfaces, powerful software architectures,

effective distribution system, etc. and lastly for the improvement and innovation perspective, it

emphasized on employee attitude. To gain employee commitment and alignment company

conducts a comprehensive employee survey so as to acquire knowledge that employees are

understanding the company's strategy and whether they are asked to deliver results which are

accordance with the strategy of a company. In market share metrics senior management wanted

to capture the huge market share as well as wanted to attract and retain software developers

within the company. At Apple Computers, BSC helped the senior management to focus on their

strategy and it served as a planning device instead of a control device. These five performance

indicators helped Apple in setting benchmark against best-in-class organization. In present, BSC

is used to build business plans and these are incorporated into senior executives compensation

plans.

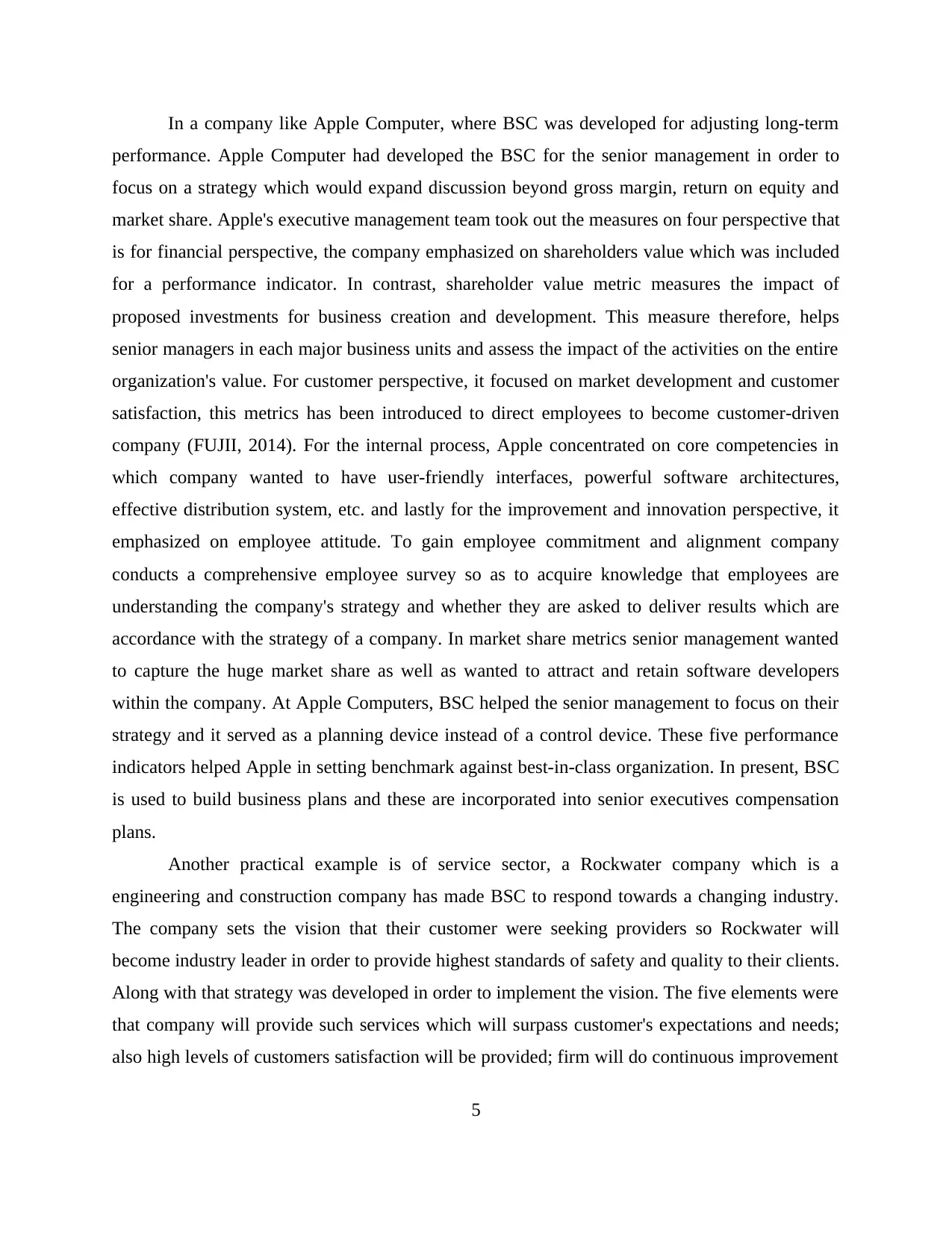

Another practical example is of service sector, a Rockwater company which is a

engineering and construction company has made BSC to respond towards a changing industry.

The company sets the vision that their customer were seeking providers so Rockwater will

become industry leader in order to provide highest standards of safety and quality to their clients.

Along with that strategy was developed in order to implement the vision. The five elements were

that company will provide such services which will surpass customer's expectations and needs;

also high levels of customers satisfaction will be provided; firm will do continuous improvement

5

performance. Apple Computer had developed the BSC for the senior management in order to

focus on a strategy which would expand discussion beyond gross margin, return on equity and

market share. Apple's executive management team took out the measures on four perspective that

is for financial perspective, the company emphasized on shareholders value which was included

for a performance indicator. In contrast, shareholder value metric measures the impact of

proposed investments for business creation and development. This measure therefore, helps

senior managers in each major business units and assess the impact of the activities on the entire

organization's value. For customer perspective, it focused on market development and customer

satisfaction, this metrics has been introduced to direct employees to become customer-driven

company (FUJII, 2014). For the internal process, Apple concentrated on core competencies in

which company wanted to have user-friendly interfaces, powerful software architectures,

effective distribution system, etc. and lastly for the improvement and innovation perspective, it

emphasized on employee attitude. To gain employee commitment and alignment company

conducts a comprehensive employee survey so as to acquire knowledge that employees are

understanding the company's strategy and whether they are asked to deliver results which are

accordance with the strategy of a company. In market share metrics senior management wanted

to capture the huge market share as well as wanted to attract and retain software developers

within the company. At Apple Computers, BSC helped the senior management to focus on their

strategy and it served as a planning device instead of a control device. These five performance

indicators helped Apple in setting benchmark against best-in-class organization. In present, BSC

is used to build business plans and these are incorporated into senior executives compensation

plans.

Another practical example is of service sector, a Rockwater company which is a

engineering and construction company has made BSC to respond towards a changing industry.

The company sets the vision that their customer were seeking providers so Rockwater will

become industry leader in order to provide highest standards of safety and quality to their clients.

Along with that strategy was developed in order to implement the vision. The five elements were

that company will provide such services which will surpass customer's expectations and needs;

also high levels of customers satisfaction will be provided; firm will do continuous improvement

5

in safety, equipment reliability, responsiveness and cost effectiveness. The company will acquire

high-quality employees and along with that shareholder expectations will be meet out. Senior

managers of this firm translated its vision and strategic objectives into four sets of performance

measure in a balance scorecard.

(Source: Putting the Balanced Scorecard to Work, 2015)

The Rockwater team deliberately thought about the choice of metric for the identification

stage. It also recognized that time spent with key prospects for discussing new work act as an

input measure rather than an output measure. The management team wanted to develop a metric

which can clearly communicate to all the employees of the organization about the importance of

building relationships with and satisfying customers. The management team also believed that

spending quality time with key customers was a prerequisite for influencing results. This input

6

Illustration 1: Rockwater’s Balanced Scorecard

high-quality employees and along with that shareholder expectations will be meet out. Senior

managers of this firm translated its vision and strategic objectives into four sets of performance

measure in a balance scorecard.

(Source: Putting the Balanced Scorecard to Work, 2015)

The Rockwater team deliberately thought about the choice of metric for the identification

stage. It also recognized that time spent with key prospects for discussing new work act as an

input measure rather than an output measure. The management team wanted to develop a metric

which can clearly communicate to all the employees of the organization about the importance of

building relationships with and satisfying customers. The management team also believed that

spending quality time with key customers was a prerequisite for influencing results. This input

6

Illustration 1: Rockwater’s Balanced Scorecard

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

measure was chosen with a due care to educate employees about the importance of working

closely which helps in identifying and satisfying customer needs.

Balance scorecard is also developed in Hotel industry, where it provides management

with a useful feedback for optimizing their organizations (Asefeso, 2013). In financial metrics

hotels include the revenue per guest and revenue per available room. These data are monitored

and also the amount generation of revenue properties and efficient utilization of space. Other

than these information, earning per share, net income and stock price are also listed in this

metrics. In a customer satisfaction metrics hotel includes target customers, retention rates,

complaints. In a hotel industry customer satisfaction is an important measure as it is a

competitive advantage for them. In a column of internal business process, maintenance costs,

accidents and quality measures are included. This metrics impact the net profit and earning per

share of a hotel. A hotel should have efficient and effective internal process as it is very crucial

for the competitive advantage. The last metrics of BSC includes the learning and growth of hotel

staff through continuous training, skills levels attainment and personnel turnover. If there is

personnel turnover than it shows that they are unhappy and through BSC this measure can be

known.

Critical Analysis and Arguments

Balance scorecards play a major role in both production as well as service organizations.

It not only measure the performance of financial aspect but also the non-financial aspects are

also added. To get the broader picture of the organization's performance all factors have to be

measured. Kalpan and Norton argued that the performance indicators should be chosen from four

different dimensions that is financial, customers, internal process and growth & learning. They

also said that company can stay focused and and at the same time it can see four different

perspectives. In order to justify Kalpan and Norton explained that new performance

measurement system is more active and empowering for the personnel because they will be less

controlled by the financial measurement systems but in fact can freely take actions and decisions

which help in fulfilling the strategic goals.

Kalpan and Norton developed the balance scorecard as a performance measurement but

then Punniyamoorthy and Murali (2008) argued that it can also be used as strategic management

7

closely which helps in identifying and satisfying customer needs.

Balance scorecard is also developed in Hotel industry, where it provides management

with a useful feedback for optimizing their organizations (Asefeso, 2013). In financial metrics

hotels include the revenue per guest and revenue per available room. These data are monitored

and also the amount generation of revenue properties and efficient utilization of space. Other

than these information, earning per share, net income and stock price are also listed in this

metrics. In a customer satisfaction metrics hotel includes target customers, retention rates,

complaints. In a hotel industry customer satisfaction is an important measure as it is a

competitive advantage for them. In a column of internal business process, maintenance costs,

accidents and quality measures are included. This metrics impact the net profit and earning per

share of a hotel. A hotel should have efficient and effective internal process as it is very crucial

for the competitive advantage. The last metrics of BSC includes the learning and growth of hotel

staff through continuous training, skills levels attainment and personnel turnover. If there is

personnel turnover than it shows that they are unhappy and through BSC this measure can be

known.

Critical Analysis and Arguments

Balance scorecards play a major role in both production as well as service organizations.

It not only measure the performance of financial aspect but also the non-financial aspects are

also added. To get the broader picture of the organization's performance all factors have to be

measured. Kalpan and Norton argued that the performance indicators should be chosen from four

different dimensions that is financial, customers, internal process and growth & learning. They

also said that company can stay focused and and at the same time it can see four different

perspectives. In order to justify Kalpan and Norton explained that new performance

measurement system is more active and empowering for the personnel because they will be less

controlled by the financial measurement systems but in fact can freely take actions and decisions

which help in fulfilling the strategic goals.

Kalpan and Norton developed the balance scorecard as a performance measurement but

then Punniyamoorthy and Murali (2008) argued that it can also be used as strategic management

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

systems. It is used to clarify the strategy to the organization as it translates the strategic objective

into quantifiable measures so that management can understand the strategy. Secondly it helps in

communicating the strategic objectives throughout the organization. It helps in translating higher

level objectives into operational objectives. Thirdly, BSC aids in planning, setting achievable

targets and initiatives are set to align efforts for reaching targets. And lastly, executives receives

feedback about the proceedings of strategy implementation as per the plan and learning is

developed about the success of the strategy.

However, Murby and Gould (2005) implies that BSC is also used for articulating the

vision and strategy of businesses. It helps in establishing objectives which support the business's

vision and objectives. Along with that, BSC helps in identifying the performance categories

which links the vision and strategy of business organization with its results. This also take

actions which help in closing unfavorable variations. Further, this helps in comparing the actual

data with that of desired data by collecting and analyzing performance data.

Kalpan and Norton firstly developed the balance scorecard in 1992 which was known as

1st Generation Balance Scorecard which had some loopholes given by Perkins, Grey and

Remmers (2014) Due to which initial design was discarded and authors recommended to bring

improvements. After that Kalpan and Norton were came up with the 2nd Generation Balance

Scorecard where two areas were focused that is filtering which means the process of choosing

specific measures of reporting and clustering which involves the decision about group measures

into perspectives. Many criticizer emphasized that BSC should have the linkage of cause-and-

effect relationship. Later on, refinement was done in 2nd Generation BSC and the developers

came up again with the 3rd Generation BSC so as to give more functionality and more strategic

relevance and this was the final scorecard which is still being used by the company.

Balance Scorecard is extensively used in major companies, however, Murby and Gould

(2005) argued that there are some organization which have become less successful while using a

balance scorecard. The survey showed the reasons that 78% companies did not linked the

strategic objectives along with the performance measures. 71% companies did not developed the

value-driver map; 50% did not involve non-financial measures. Company has to take care about

the following areas so as to avoid the mistakes in making balance scorecard. Although, balance

scorecard has been supported by many philosophers and big companies but have been criticized

8

into quantifiable measures so that management can understand the strategy. Secondly it helps in

communicating the strategic objectives throughout the organization. It helps in translating higher

level objectives into operational objectives. Thirdly, BSC aids in planning, setting achievable

targets and initiatives are set to align efforts for reaching targets. And lastly, executives receives

feedback about the proceedings of strategy implementation as per the plan and learning is

developed about the success of the strategy.

However, Murby and Gould (2005) implies that BSC is also used for articulating the

vision and strategy of businesses. It helps in establishing objectives which support the business's

vision and objectives. Along with that, BSC helps in identifying the performance categories

which links the vision and strategy of business organization with its results. This also take

actions which help in closing unfavorable variations. Further, this helps in comparing the actual

data with that of desired data by collecting and analyzing performance data.

Kalpan and Norton firstly developed the balance scorecard in 1992 which was known as

1st Generation Balance Scorecard which had some loopholes given by Perkins, Grey and

Remmers (2014) Due to which initial design was discarded and authors recommended to bring

improvements. After that Kalpan and Norton were came up with the 2nd Generation Balance

Scorecard where two areas were focused that is filtering which means the process of choosing

specific measures of reporting and clustering which involves the decision about group measures

into perspectives. Many criticizer emphasized that BSC should have the linkage of cause-and-

effect relationship. Later on, refinement was done in 2nd Generation BSC and the developers

came up again with the 3rd Generation BSC so as to give more functionality and more strategic

relevance and this was the final scorecard which is still being used by the company.

Balance Scorecard is extensively used in major companies, however, Murby and Gould

(2005) argued that there are some organization which have become less successful while using a

balance scorecard. The survey showed the reasons that 78% companies did not linked the

strategic objectives along with the performance measures. 71% companies did not developed the

value-driver map; 50% did not involve non-financial measures. Company has to take care about

the following areas so as to avoid the mistakes in making balance scorecard. Although, balance

scorecard has been supported by many philosophers and big companies but have been criticized

8

by some commentators. As per the viewpoint of Greiling (2010) BSC lacks the rationality and

logic in the original presentation. On the other hand, remarks have been made on the specific

issues which may result into the failure of scorecard in order to live up to its perceived potential

for implementation.

According to Perkins, Grey and Remmers (2014) the scorecard rely on performance

measures which might not be rooted in the company but which might be distributed in

hierarchical manner which reduce the likelihood of organizational buy-in. This model disregard

the external competition and technological advancement which may involve uncertainty in term

of risk and also it can threaten or discard the present strategy. However, critical analysis have

also been done and it was found that in the study of Murby and Gould (2005) stated that although

balance scorecard is widely used and accepted as a management tool but it has been challenged

and there is a lack of cause-and-effect relationship and right choice of measurement cannot be

assumed.

It is not necessary that balance scorecard will always lead and organization to gain

success. Sometimes wrong interpretation and implementation of BSC leads to a devastating

results which may impact the success of whole organization. For this purpose, company has to

hire a expertise to develop the scorecard for the company for which complete internal and

external analysis is being done. Company can use spreadsheet or word documents to make a

scorecard but also they can use a software for developing effective scorecards. However, this

involve heavy expenditure because company has to pay good remuneration to the expert and also

has to pay big amount for purchasing a software which will be used for making balance

scorecards. Punniyamoorthy and Murali (2008) stated that high risk is also involved as company

has to provide complete information to the expert about the strategic objectives, financial data,

employee performance, etc. which are confidential for the company and there are chances that

expert can reveal it in the front of a competitors which become problematic for a company. A

level of trust cannot be maintained.

According to Murby and Gould (2005) for developing an effective and efficient balance

scorecard, company has to employ a lot of time in doing market research, strategic planning,

target setting, doing surveys of employees. This is however, a time consuming process. On the

other hand, Kalpan and Norton (2006) argued that until and unless good amount of time will not

9

logic in the original presentation. On the other hand, remarks have been made on the specific

issues which may result into the failure of scorecard in order to live up to its perceived potential

for implementation.

According to Perkins, Grey and Remmers (2014) the scorecard rely on performance

measures which might not be rooted in the company but which might be distributed in

hierarchical manner which reduce the likelihood of organizational buy-in. This model disregard

the external competition and technological advancement which may involve uncertainty in term

of risk and also it can threaten or discard the present strategy. However, critical analysis have

also been done and it was found that in the study of Murby and Gould (2005) stated that although

balance scorecard is widely used and accepted as a management tool but it has been challenged

and there is a lack of cause-and-effect relationship and right choice of measurement cannot be

assumed.

It is not necessary that balance scorecard will always lead and organization to gain

success. Sometimes wrong interpretation and implementation of BSC leads to a devastating

results which may impact the success of whole organization. For this purpose, company has to

hire a expertise to develop the scorecard for the company for which complete internal and

external analysis is being done. Company can use spreadsheet or word documents to make a

scorecard but also they can use a software for developing effective scorecards. However, this

involve heavy expenditure because company has to pay good remuneration to the expert and also

has to pay big amount for purchasing a software which will be used for making balance

scorecards. Punniyamoorthy and Murali (2008) stated that high risk is also involved as company

has to provide complete information to the expert about the strategic objectives, financial data,

employee performance, etc. which are confidential for the company and there are chances that

expert can reveal it in the front of a competitors which become problematic for a company. A

level of trust cannot be maintained.

According to Murby and Gould (2005) for developing an effective and efficient balance

scorecard, company has to employ a lot of time in doing market research, strategic planning,

target setting, doing surveys of employees. This is however, a time consuming process. On the

other hand, Kalpan and Norton (2006) argued that until and unless good amount of time will not

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

be spent, a successful and efficient balance scorecard cannot be developed. Company develops

balance scorecard for a long term perspective so that company can chive its vision and strategy

but at the time of sudden change existing scorecard remains of no use as the policies and strategy

has to be changed on the spot. The cost and time which was involved while making the scorecard

get wasted and company may face huge loss or lesser profitability. The existi9ng model of BSC

lacks the time dimension which is a most fundamental area in any business organization and also

it is not a valid model because it relies on few measure which makes BSC critical point.

Similarly, BSC lack integration of top level and operational level measures which makes this

model unsuccessful and unacceptable by some managers. And the most important factor that this

model is not suitable in every business situations, company has to make different BSC in

different situation due to which company resist this model for strategic management tool. On the

other hand, Asefeso (2013) argued that it is not a template format which can be used in a same

format in every organization, BSC in production organization differs from the BSC of service

organization.

The existing Balance Scorecard is highly acceptable but still some company makes

mistake in developing effective BSC. Also this model lacks cause-and-effect relationship. For

this purpose, a new model should be developed which indicates that employee perspective

should also be included as they can represent greatest sources of value and it is not necessary that

every time quantitative detail should be included, the model should increase the flexibility so that

somethings should be kept at bug picture level. New model should be aimed at leaving some

aspects of performance open and it should allow creativity and innovations (FUJII, 2014).

CONCLUSION

After preparing this project report it can be concluded that Balance Scorecard is not only

a performance measure tool but it is also has widespread use as strategic management tool. This

is used extensively in almost all the organization but still many organization fails in getting

success even after following the balance scorecard., this is due to the improper use of BSC.

Some company does not include all the four perspective and sometimes include only financial

ansd aspect and fails to include non-financial aspects which result in failure of organization. This

report has focused on the implementation of BSC in many companies whether production or

10

balance scorecard for a long term perspective so that company can chive its vision and strategy

but at the time of sudden change existing scorecard remains of no use as the policies and strategy

has to be changed on the spot. The cost and time which was involved while making the scorecard

get wasted and company may face huge loss or lesser profitability. The existi9ng model of BSC

lacks the time dimension which is a most fundamental area in any business organization and also

it is not a valid model because it relies on few measure which makes BSC critical point.

Similarly, BSC lack integration of top level and operational level measures which makes this

model unsuccessful and unacceptable by some managers. And the most important factor that this

model is not suitable in every business situations, company has to make different BSC in

different situation due to which company resist this model for strategic management tool. On the

other hand, Asefeso (2013) argued that it is not a template format which can be used in a same

format in every organization, BSC in production organization differs from the BSC of service

organization.

The existing Balance Scorecard is highly acceptable but still some company makes

mistake in developing effective BSC. Also this model lacks cause-and-effect relationship. For

this purpose, a new model should be developed which indicates that employee perspective

should also be included as they can represent greatest sources of value and it is not necessary that

every time quantitative detail should be included, the model should increase the flexibility so that

somethings should be kept at bug picture level. New model should be aimed at leaving some

aspects of performance open and it should allow creativity and innovations (FUJII, 2014).

CONCLUSION

After preparing this project report it can be concluded that Balance Scorecard is not only

a performance measure tool but it is also has widespread use as strategic management tool. This

is used extensively in almost all the organization but still many organization fails in getting

success even after following the balance scorecard., this is due to the improper use of BSC.

Some company does not include all the four perspective and sometimes include only financial

ansd aspect and fails to include non-financial aspects which result in failure of organization. This

report has focused on the implementation of BSC in many companies whether production or

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

service sector. Both the sector have different set of balance scorecard and it is to be developed as

per the situation and nature of the company. It is however costly, time consuming process but it

can reflect effective results if used appropriately by an organization.

11

per the situation and nature of the company. It is however costly, time consuming process but it

can reflect effective results if used appropriately by an organization.

11

REFERENCES

Journals

Broccardo and Laura, 2010. An empirical study of the Balanced Scorecard as a flexible strategic

management and reporting tool. Economia Aziendale Online. 2. pp-81-91.

Chavan, M., 2009. The balanced scorecard: a new challenge. Journal of Management

Development. 28(5). pp.393–406.

Greiling, D., 2010. Balanced scorecard implementation in German non‐profit organisations.

International Journal of Productivity and Performance Management. 59(6). pp.534 –

554.

Gurd, B. and Gao, T., 2008. Lives in the balance: an analysis of the balanced scorecard (BSC) in

healthcare organizations. International Journal of Productivity and Performance

Management 57(1). pp.6–21.

Johanson, U. and et.al., 2006. Balancing dilemmas of the balanced scorecard. Accounting,

Auditing & Accountability Journal, 19(6). pp.842–857.

Kaplan and et. al., 1996. Using the Balanced Scorecard as a Strategic Management System.

Harvard Business Review. 74 (1). p75-85.

Kaplan and et.al., 1993. Putting the Balanced Scorecard to Work. Harvard Business Review.

71(5). pp-134-147.

Kaplan, R. S., 2012. The balanced scorecard: comments on balanced scorecard commentaries.

Journal of Accounting & Organizational Change. 8(4). pp.539 – 545.

Perkins, M., Grey, A. and Remmers, H., 2014. What do we really mean by “Balanced

Scorecard”?. International Journal of Productivity and Performance Management.

63(2). pp.148 – 169.

Punniyamoorthy, M. and R. Murali, R., 2008. Balanced score for the balanced scorecard: a

benchmarking tool. Benchmarking: An International Journal. 15(4). pp.420 – 443.

Soderberg, M. and et. al., 2011. When is a balanced scorecard a balanced scorecard?

International Journal of Productivity and Performance Management. 60(7). pp.688 –

708.

Books

Asefeso, A., 2013. Balanced Scorecard. AA Global Sourcing Ltd.

Bischoff, L. A., 2013. The Balanced Scorecard. GRIN Verlag.

FUJII, T., 2014. Balanced scorecard strategy management super guide. TOM PUBLISHING.

Kalpan, S. R. and Norton, P. D., 2006. Alignment: Using the Balanced Scorecard to Create

Corporate Synergies. Harvard Business Press.

12

Journals

Broccardo and Laura, 2010. An empirical study of the Balanced Scorecard as a flexible strategic

management and reporting tool. Economia Aziendale Online. 2. pp-81-91.

Chavan, M., 2009. The balanced scorecard: a new challenge. Journal of Management

Development. 28(5). pp.393–406.

Greiling, D., 2010. Balanced scorecard implementation in German non‐profit organisations.

International Journal of Productivity and Performance Management. 59(6). pp.534 –

554.

Gurd, B. and Gao, T., 2008. Lives in the balance: an analysis of the balanced scorecard (BSC) in

healthcare organizations. International Journal of Productivity and Performance

Management 57(1). pp.6–21.

Johanson, U. and et.al., 2006. Balancing dilemmas of the balanced scorecard. Accounting,

Auditing & Accountability Journal, 19(6). pp.842–857.

Kaplan and et. al., 1996. Using the Balanced Scorecard as a Strategic Management System.

Harvard Business Review. 74 (1). p75-85.

Kaplan and et.al., 1993. Putting the Balanced Scorecard to Work. Harvard Business Review.

71(5). pp-134-147.

Kaplan, R. S., 2012. The balanced scorecard: comments on balanced scorecard commentaries.

Journal of Accounting & Organizational Change. 8(4). pp.539 – 545.

Perkins, M., Grey, A. and Remmers, H., 2014. What do we really mean by “Balanced

Scorecard”?. International Journal of Productivity and Performance Management.

63(2). pp.148 – 169.

Punniyamoorthy, M. and R. Murali, R., 2008. Balanced score for the balanced scorecard: a

benchmarking tool. Benchmarking: An International Journal. 15(4). pp.420 – 443.

Soderberg, M. and et. al., 2011. When is a balanced scorecard a balanced scorecard?

International Journal of Productivity and Performance Management. 60(7). pp.688 –

708.

Books

Asefeso, A., 2013. Balanced Scorecard. AA Global Sourcing Ltd.

Bischoff, L. A., 2013. The Balanced Scorecard. GRIN Verlag.

FUJII, T., 2014. Balanced scorecard strategy management super guide. TOM PUBLISHING.

Kalpan, S. R. and Norton, P. D., 2006. Alignment: Using the Balanced Scorecard to Create

Corporate Synergies. Harvard Business Press.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.