Analyzing CMI Company's Performance: A Balanced Scorecard Project

VerifiedAdded on 2021/11/16

|12

|3002

|497

Project

AI Summary

This project presents a comprehensive analysis of CMI Company's performance and strategic planning using the Balanced Scorecard framework. The project begins with a detailed sales and production budget, including calculations for direct material usage, material purchase, direct labor, fixed production overhead, and the value of closing finished stock, culminating in a budgeted profit and loss account. It then delves into variance analysis, calculating and interpreting direct material, direct labor, variable production overhead, fixed overhead, and sales variances to assess the effectiveness of cost control and sales strategies. Finally, the project applies the Balanced Scorecard, outlining its components, perspectives (financial, customer, internal processes, and learning & growth), and strategic objectives, including a strategy map for high-quality product and furniture to customers, to evaluate and improve CMI Company's overall performance, providing a framework for strategic alignment and performance measurement.

1

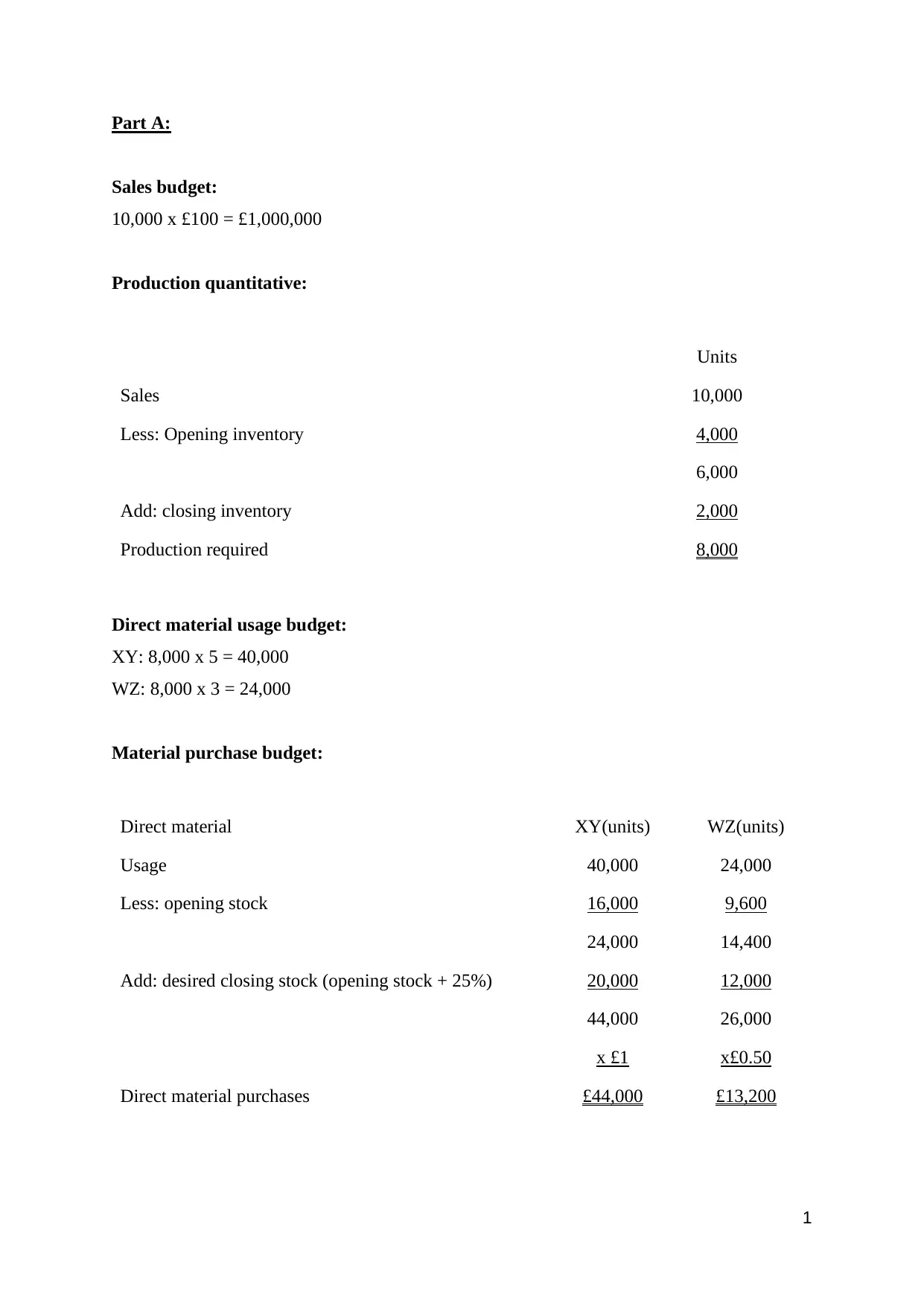

Part A:

Sales budget:

10,000 x £100 = £1,000,000

Production quantitative:

Units

Sales 10,000

Less: Opening inventory 4,000

6,000

Add: closing inventory 2,000

Production required 8,000

Direct material usage budget:

XY: 8,000 x 5 = 40,000

WZ: 8,000 x 3 = 24,000

Material purchase budget:

Direct material XY(units) WZ(units)

Usage 40,000 24,000

Less: opening stock 16,000 9,600

24,000 14,400

Add: desired closing stock (opening stock + 25%) 20,000 12,000

44,000 26,000

x £1 x£0.50

Direct material purchases £44,000 £13,200

Part A:

Sales budget:

10,000 x £100 = £1,000,000

Production quantitative:

Units

Sales 10,000

Less: Opening inventory 4,000

6,000

Add: closing inventory 2,000

Production required 8,000

Direct material usage budget:

XY: 8,000 x 5 = 40,000

WZ: 8,000 x 3 = 24,000

Material purchase budget:

Direct material XY(units) WZ(units)

Usage 40,000 24,000

Less: opening stock 16,000 9,600

24,000 14,400

Add: desired closing stock (opening stock + 25%) 20,000 12,000

44,000 26,000

x £1 x£0.50

Direct material purchases £44,000 £13,200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

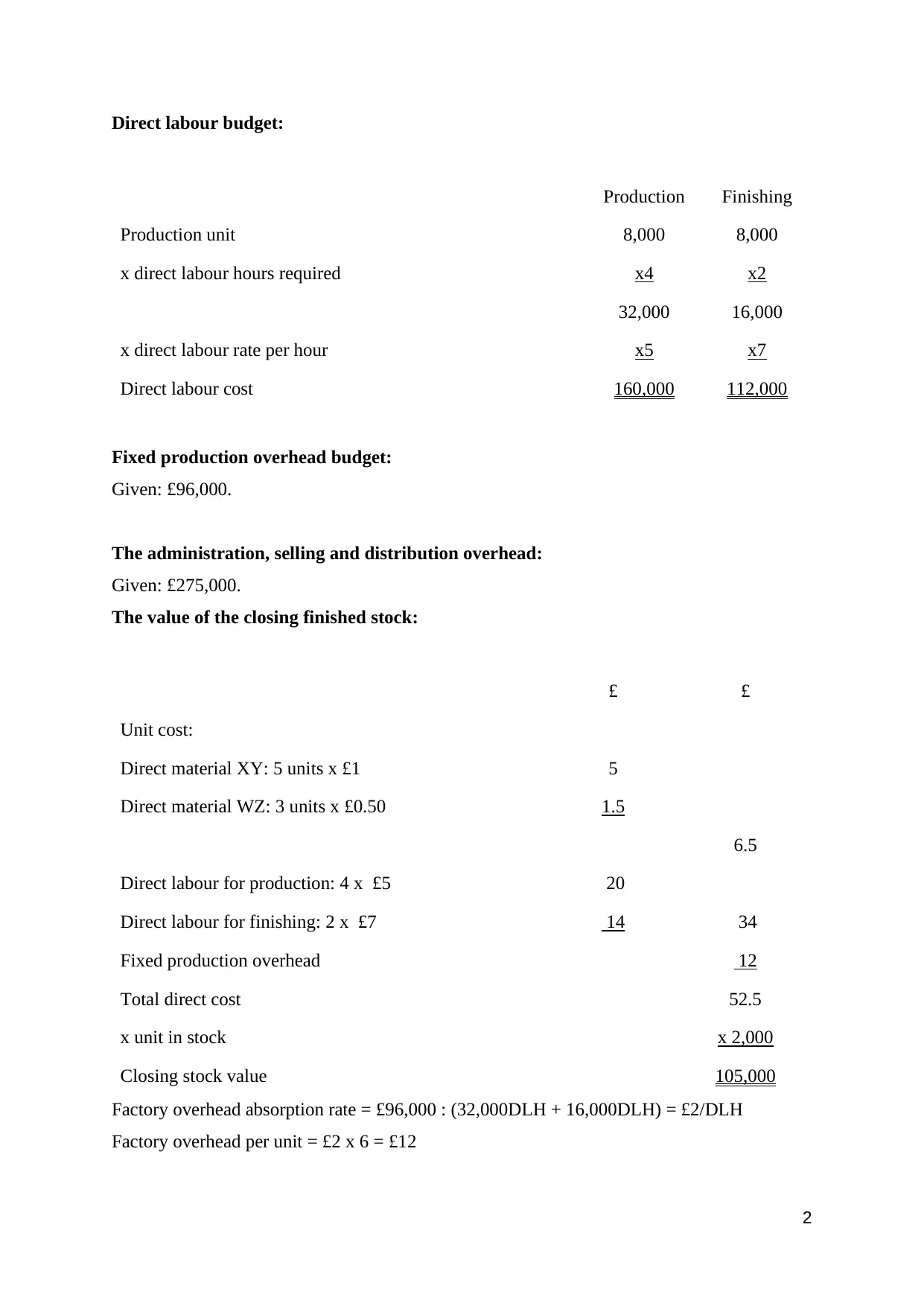

Direct labour budget:

Production Finishing

Production unit 8,000 8,000

x direct labour hours required x4 x2

32,000 16,000

x direct labour rate per hour x5 x7

Direct labour cost 160,000 112,000

Fixed production overhead budget:

Given: £96,000.

The administration, selling and distribution overhead:

Given: £275,000.

The value of the closing finished stock:

£ £

Unit cost:

Direct material XY: 5 units x £1 5

Direct material WZ: 3 units x £0.50 1.5

6.5

Direct labour for production: 4 x £5 20

Direct labour for finishing: 2 x £7 14 34

Fixed production overhead 12

Total direct cost 52.5

x unit in stock x 2,000

Closing stock value 105,000

Factory overhead absorption rate = £96,000 : (32,000DLH + 16,000DLH) = £2/DLH

Factory overhead per unit = £2 x 6 = £12

Direct labour budget:

Production Finishing

Production unit 8,000 8,000

x direct labour hours required x4 x2

32,000 16,000

x direct labour rate per hour x5 x7

Direct labour cost 160,000 112,000

Fixed production overhead budget:

Given: £96,000.

The administration, selling and distribution overhead:

Given: £275,000.

The value of the closing finished stock:

£ £

Unit cost:

Direct material XY: 5 units x £1 5

Direct material WZ: 3 units x £0.50 1.5

6.5

Direct labour for production: 4 x £5 20

Direct labour for finishing: 2 x £7 14 34

Fixed production overhead 12

Total direct cost 52.5

x unit in stock x 2,000

Closing stock value 105,000

Factory overhead absorption rate = £96,000 : (32,000DLH + 16,000DLH) = £2/DLH

Factory overhead per unit = £2 x 6 = £12

3

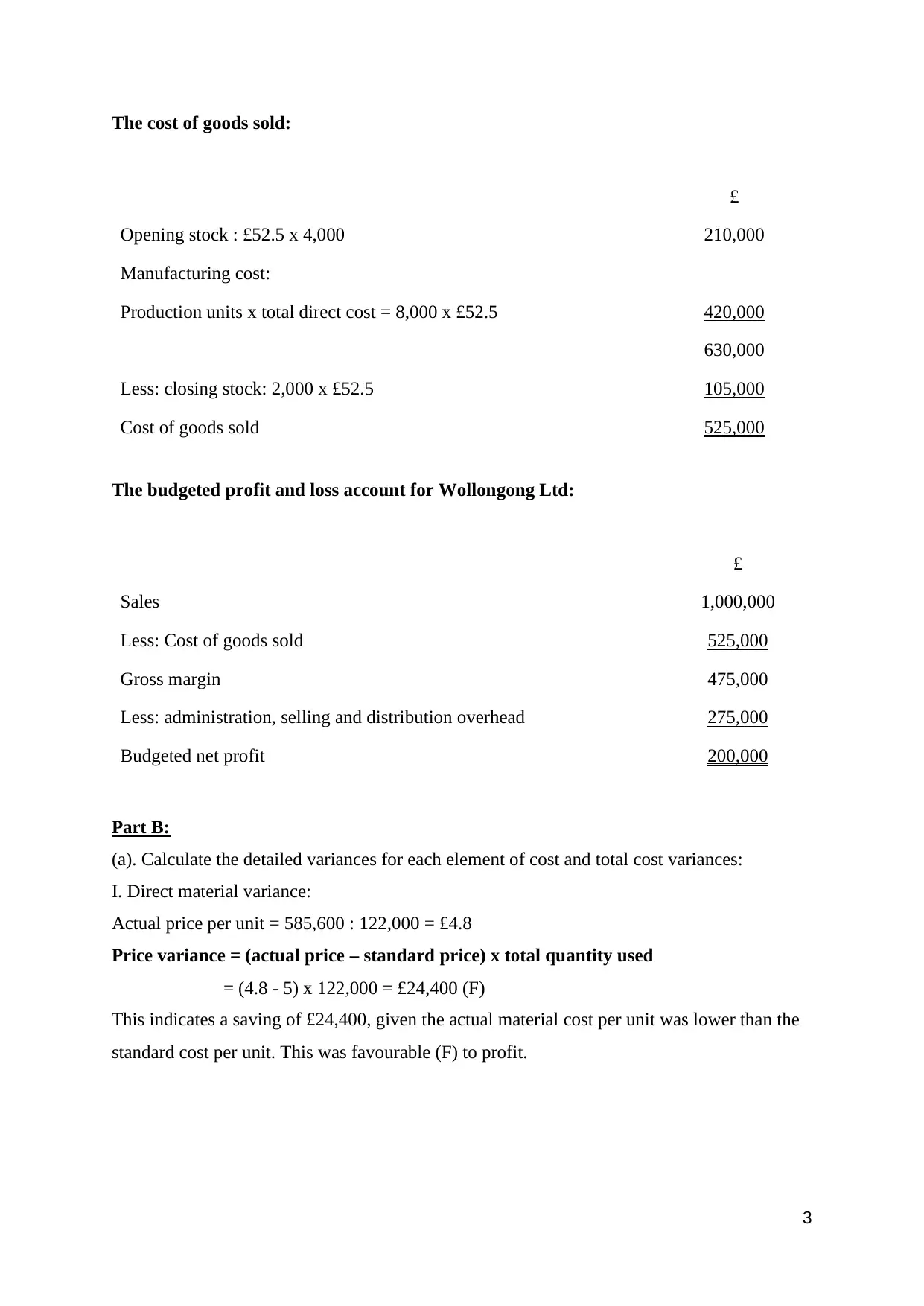

The cost of goods sold:

£

Opening stock : £52.5 x 4,000 210,000

Manufacturing cost:

Production units x total direct cost = 8,000 x £52.5 420,000

630,000

Less: closing stock: 2,000 x £52.5 105,000

Cost of goods sold 525,000

The budgeted profit and loss account for Wollongong Ltd:

£

Sales 1,000,000

Less: Cost of goods sold 525,000

Gross margin 475,000

Less: administration, selling and distribution overhead 275,000

Budgeted net profit 200,000

Part B:

(a). Calculate the detailed variances for each element of cost and total cost variances:

I. Direct material variance:

Actual price per unit = 585,600 : 122,000 = £4.8

Price variance = (actual price – standard price) x total quantity used

= (4.8 - 5) x 122,000 = £24,400 (F)

This indicates a saving of £24,400, given the actual material cost per unit was lower than the

standard cost per unit. This was favourable (F) to profit.

The cost of goods sold:

£

Opening stock : £52.5 x 4,000 210,000

Manufacturing cost:

Production units x total direct cost = 8,000 x £52.5 420,000

630,000

Less: closing stock: 2,000 x £52.5 105,000

Cost of goods sold 525,000

The budgeted profit and loss account for Wollongong Ltd:

£

Sales 1,000,000

Less: Cost of goods sold 525,000

Gross margin 475,000

Less: administration, selling and distribution overhead 275,000

Budgeted net profit 200,000

Part B:

(a). Calculate the detailed variances for each element of cost and total cost variances:

I. Direct material variance:

Actual price per unit = 585,600 : 122,000 = £4.8

Price variance = (actual price – standard price) x total quantity used

= (4.8 - 5) x 122,000 = £24,400 (F)

This indicates a saving of £24,400, given the actual material cost per unit was lower than the

standard cost per unit. This was favourable (F) to profit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

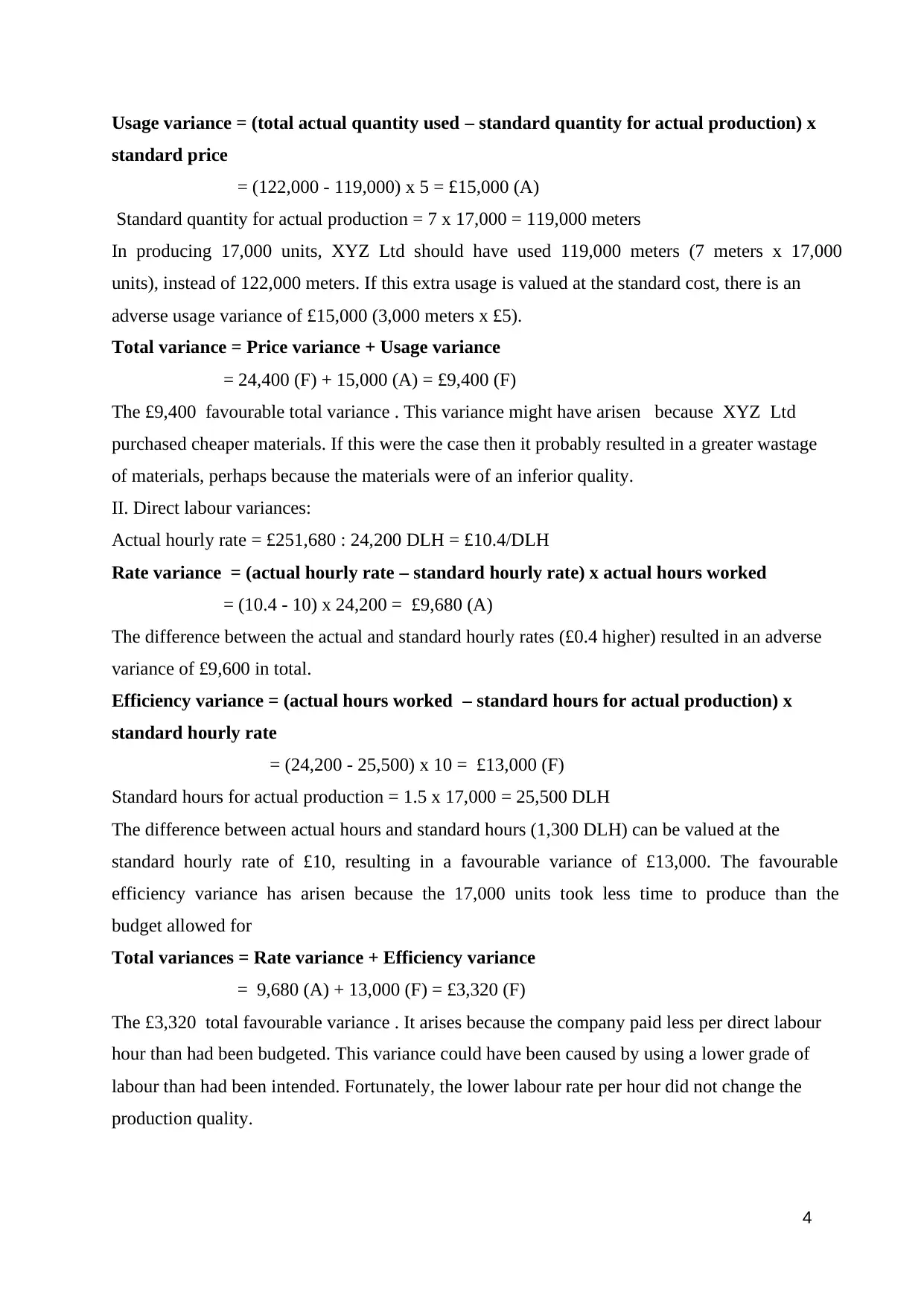

Usage variance = (total actual quantity used – standard quantity for actual production) x

standard price

= (122,000 - 119,000) x 5 = £15,000 (A)

Standard quantity for actual production = 7 x 17,000 = 119,000 meters

In producing 17,000 units, XYZ Ltd should have used 119,000 meters (7 meters x 17,000

units), instead of 122,000 meters. If this extra usage is valued at the standard cost, there is an

adverse usage variance of £15,000 (3,000 meters x £5).

Total variance = Price variance + Usage variance

= 24,400 (F) + 15,000 (A) = £9,400 (F)

The £9,400 favourable total variance . This variance might have arisen because XYZ Ltd

purchased cheaper materials. If this were the case then it probably resulted in a greater wastage

of materials, perhaps because the materials were of an inferior quality.

II. Direct labour variances:

Actual hourly rate = £251,680 : 24,200 DLH = £10.4/DLH

Rate variance = (actual hourly rate – standard hourly rate) x actual hours worked

= (10.4 - 10) x 24,200 = £9,680 (A)

The difference between the actual and standard hourly rates (£0.4 higher) resulted in an adverse

variance of £9,600 in total.

Efficiency variance = (actual hours worked – standard hours for actual production) x

standard hourly rate

= (24,200 - 25,500) x 10 = £13,000 (F)

Standard hours for actual production = 1.5 x 17,000 = 25,500 DLH

The difference between actual hours and standard hours (1,300 DLH) can be valued at the

standard hourly rate of £10, resulting in a favourable variance of £13,000. The favourable

efficiency variance has arisen because the 17,000 units took less time to produce than the

budget allowed for

Total variances = Rate variance + Efficiency variance

= 9,680 (A) + 13,000 (F) = £3,320 (F)

The £3,320 total favourable variance . It arises because the company paid less per direct labour

hour than had been budgeted. This variance could have been caused by using a lower grade of

labour than had been intended. Fortunately, the lower labour rate per hour did not change the

production quality.

Usage variance = (total actual quantity used – standard quantity for actual production) x

standard price

= (122,000 - 119,000) x 5 = £15,000 (A)

Standard quantity for actual production = 7 x 17,000 = 119,000 meters

In producing 17,000 units, XYZ Ltd should have used 119,000 meters (7 meters x 17,000

units), instead of 122,000 meters. If this extra usage is valued at the standard cost, there is an

adverse usage variance of £15,000 (3,000 meters x £5).

Total variance = Price variance + Usage variance

= 24,400 (F) + 15,000 (A) = £9,400 (F)

The £9,400 favourable total variance . This variance might have arisen because XYZ Ltd

purchased cheaper materials. If this were the case then it probably resulted in a greater wastage

of materials, perhaps because the materials were of an inferior quality.

II. Direct labour variances:

Actual hourly rate = £251,680 : 24,200 DLH = £10.4/DLH

Rate variance = (actual hourly rate – standard hourly rate) x actual hours worked

= (10.4 - 10) x 24,200 = £9,680 (A)

The difference between the actual and standard hourly rates (£0.4 higher) resulted in an adverse

variance of £9,600 in total.

Efficiency variance = (actual hours worked – standard hours for actual production) x

standard hourly rate

= (24,200 - 25,500) x 10 = £13,000 (F)

Standard hours for actual production = 1.5 x 17,000 = 25,500 DLH

The difference between actual hours and standard hours (1,300 DLH) can be valued at the

standard hourly rate of £10, resulting in a favourable variance of £13,000. The favourable

efficiency variance has arisen because the 17,000 units took less time to produce than the

budget allowed for

Total variances = Rate variance + Efficiency variance

= 9,680 (A) + 13,000 (F) = £3,320 (F)

The £3,320 total favourable variance . It arises because the company paid less per direct labour

hour than had been budgeted. This variance could have been caused by using a lower grade of

labour than had been intended. Fortunately, the lower labour rate per hour did not change the

production quality.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

III. Variable production overhead:

Variable overhead absorption rate = 6 : 1.5 = £4/DLH

Expenditure = actual variable overhead – (actual hours worked x Variable overhead

absorption rate)

= 98,000 - (24,200 x 4) = £1,200 (A)

The actual expenditure was £1,200 more than the budgeted expenditure based on actual

production.

Efficiency = (Actual hours worked - Standard hours for actual production) x Variable

overhead absorption rate

= (24,200 - 25,500) x 4 = £5,200 (F)

The actual efficiency was £5,200 less than the budgeted efficiency based on actual production.

Total = expenditure + efficiency

= £1,200 (A) + £5,200 (F) = £4,000 (F)

The favourable variance caused by lower actual direct labour hours can compensate for the

adverse expenditure variance although the actual Variable overhead is higher than the standard

Variable overhead.

IV. Fixed overhead variances:

Expenditure = Actual fixed overhead – Budgeted fixed expenditure

= 108,000 - 100,000 = £8,000 (A)

Budgeted fixed expenditure = 1,200,000 : 12 = £100,000

This actual expenditure was £8,000 more than the budgeted expenditure.

Total = Expenditure = £8,000 (A)

As the actual activity was more than the budgeted activity, there was £108,000 of fixed

overhead was absorbed into production instead of £100,000 expected in the budget.

V. Total cost variances:

Total cost variances = Total fixed overhead variances + total variable production

overhead + total direct labour variances + total direct material variance

= £8,000 (A) + £4,000 (F) + £3,320 (F) + £9,400 (F) = £8,720(F)

(b) Calculate the sales variances:

Sales volume profit variance = (actual quantity – budgeted quantity) x standard profit

per unit

= (17,000 - 15,000) x 14 = £28,000 (F)

Sales volume profit has a Favourable variance because 17,000 units were sold instead of

15,000 units as budgeted, therefore more profit contribution by £28,000

III. Variable production overhead:

Variable overhead absorption rate = 6 : 1.5 = £4/DLH

Expenditure = actual variable overhead – (actual hours worked x Variable overhead

absorption rate)

= 98,000 - (24,200 x 4) = £1,200 (A)

The actual expenditure was £1,200 more than the budgeted expenditure based on actual

production.

Efficiency = (Actual hours worked - Standard hours for actual production) x Variable

overhead absorption rate

= (24,200 - 25,500) x 4 = £5,200 (F)

The actual efficiency was £5,200 less than the budgeted efficiency based on actual production.

Total = expenditure + efficiency

= £1,200 (A) + £5,200 (F) = £4,000 (F)

The favourable variance caused by lower actual direct labour hours can compensate for the

adverse expenditure variance although the actual Variable overhead is higher than the standard

Variable overhead.

IV. Fixed overhead variances:

Expenditure = Actual fixed overhead – Budgeted fixed expenditure

= 108,000 - 100,000 = £8,000 (A)

Budgeted fixed expenditure = 1,200,000 : 12 = £100,000

This actual expenditure was £8,000 more than the budgeted expenditure.

Total = Expenditure = £8,000 (A)

As the actual activity was more than the budgeted activity, there was £108,000 of fixed

overhead was absorbed into production instead of £100,000 expected in the budget.

V. Total cost variances:

Total cost variances = Total fixed overhead variances + total variable production

overhead + total direct labour variances + total direct material variance

= £8,000 (A) + £4,000 (F) + £3,320 (F) + £9,400 (F) = £8,720(F)

(b) Calculate the sales variances:

Sales volume profit variance = (actual quantity – budgeted quantity) x standard profit

per unit

= (17,000 - 15,000) x 14 = £28,000 (F)

Sales volume profit has a Favourable variance because 17,000 units were sold instead of

15,000 units as budgeted, therefore more profit contribution by £28,000

6

Selling price variance = (actual selling price per unit – standard selling price per unit) x

actual sales quantity

= (67 - 70) x 17,000 = £51,000 (A)

Actual selling price per unit = 1,139,000 : 17,000 = £67

The actual selling price was £3 less than the standard selling price, so the variance is adverse

by £51,000

Total sales variance = Sales volume profit + selling price

= £28,000 (F) + £51,000 (A) = £23,000 (A)

The adverse variance caused by higher units sold but the actual selling price was lower

budgeted selling price.

Selling price variance = (actual selling price per unit – standard selling price per unit) x

actual sales quantity

= (67 - 70) x 17,000 = £51,000 (A)

Actual selling price per unit = 1,139,000 : 17,000 = £67

The actual selling price was £3 less than the standard selling price, so the variance is adverse

by £51,000

Total sales variance = Sales volume profit + selling price

= £28,000 (F) + £51,000 (A) = £23,000 (A)

The adverse variance caused by higher units sold but the actual selling price was lower

budgeted selling price.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1

Part B:

(c) Standard cost operating statement:

XYZ Ltd. Standard cost operating statement for the year to 31 january:

£

Budgeted sale: (15,000 x £70 per unit) 1,050,000

Less: Budgeted COGS: (15,000 x £56 per unit) 840,000

Budgeted contribution 210,000

Less: Budgeted fixed 100,000

Budgeted net profit 110,000

Sale volume profit variance 28,000

Budgeted profit from actual sales 138,000

Variance (F) (A)

£ £

Sale price 51,000

Direct material price 24,400

Direct material usage 15,000

Direct labour rate 9,680

Direct labour efficiency 13,000

Variable overhead expenditure 1,200

Variable overhead efficiency 5,200

Fixed overhead expenditure ______ 8,000

Actual contribution margin 42,600 84,280 42,280

Actual profit 95,720

Part B:

(c) Standard cost operating statement:

XYZ Ltd. Standard cost operating statement for the year to 31 january:

£

Budgeted sale: (15,000 x £70 per unit) 1,050,000

Less: Budgeted COGS: (15,000 x £56 per unit) 840,000

Budgeted contribution 210,000

Less: Budgeted fixed 100,000

Budgeted net profit 110,000

Sale volume profit variance 28,000

Budgeted profit from actual sales 138,000

Variance (F) (A)

£ £

Sale price 51,000

Direct material price 24,400

Direct material usage 15,000

Direct labour rate 9,680

Direct labour efficiency 13,000

Variable overhead expenditure 1,200

Variable overhead efficiency 5,200

Fixed overhead expenditure ______ 8,000

Actual contribution margin 42,600 84,280 42,280

Actual profit 95,720

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Part C:

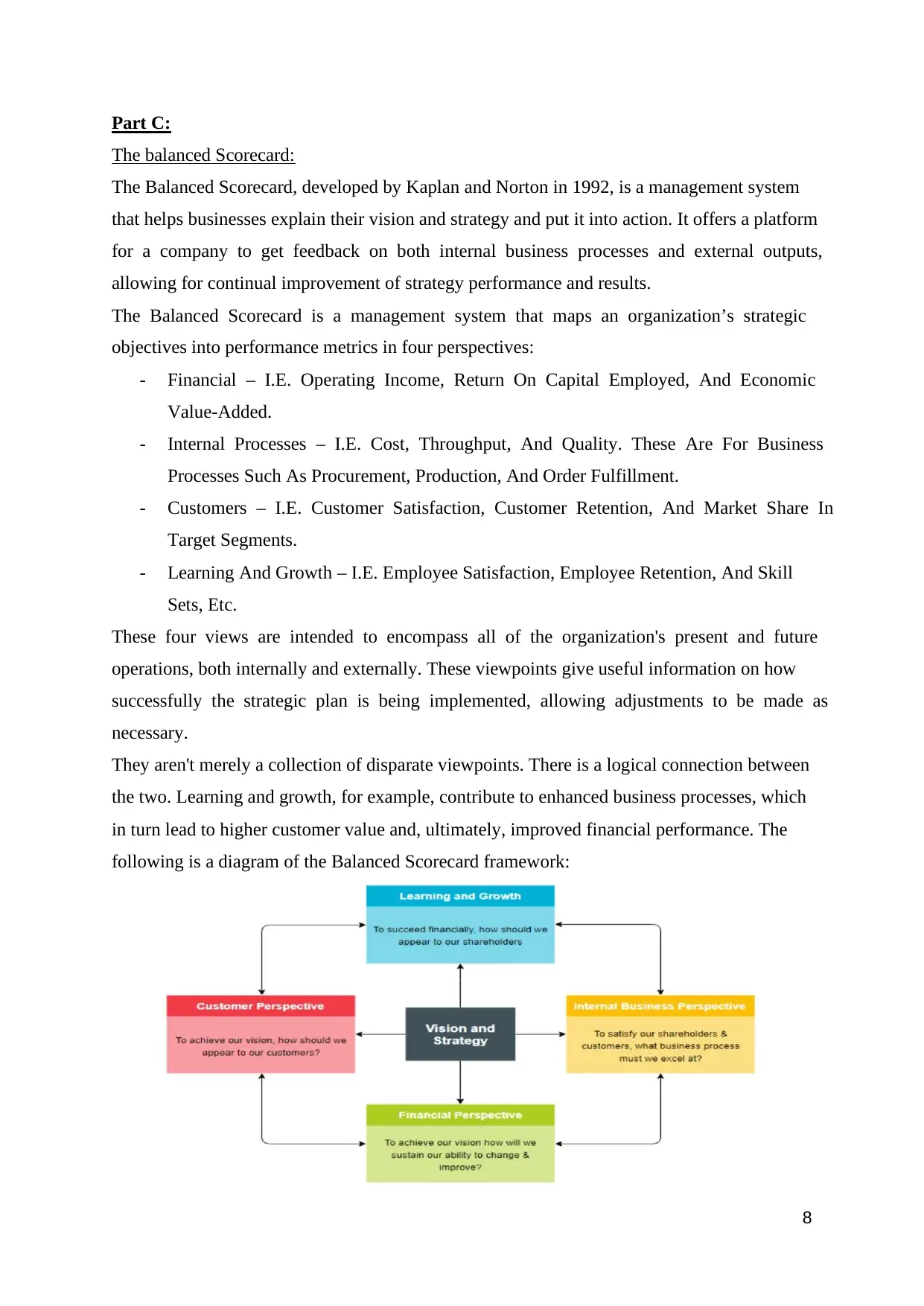

The balanced Scorecard:

The Balanced Scorecard, developed by Kaplan and Norton in 1992, is a management system

that helps businesses explain their vision and strategy and put it into action. It offers a platform

for a company to get feedback on both internal business processes and external outputs,

allowing for continual improvement of strategy performance and results.

The Balanced Scorecard is a management system that maps an organization’s strategic

objectives into performance metrics in four perspectives:

- Financial – I.E. Operating Income, Return On Capital Employed, And Economic

Value-Added.

- Internal Processes – I.E. Cost, Throughput, And Quality. These Are For Business

Processes Such As Procurement, Production, And Order Fulfillment.

- Customers – I.E. Customer Satisfaction, Customer Retention, And Market Share In

Target Segments.

- Learning And Growth – I.E. Employee Satisfaction, Employee Retention, And Skill

Sets, Etc.

These four views are intended to encompass all of the organization's present and future

operations, both internally and externally. These viewpoints give useful information on how

successfully the strategic plan is being implemented, allowing adjustments to be made as

necessary.

They aren't merely a collection of disparate viewpoints. There is a logical connection between

the two. Learning and growth, for example, contribute to enhanced business processes, which

in turn lead to higher customer value and, ultimately, improved financial performance. The

following is a diagram of the Balanced Scorecard framework:

Part C:

The balanced Scorecard:

The Balanced Scorecard, developed by Kaplan and Norton in 1992, is a management system

that helps businesses explain their vision and strategy and put it into action. It offers a platform

for a company to get feedback on both internal business processes and external outputs,

allowing for continual improvement of strategy performance and results.

The Balanced Scorecard is a management system that maps an organization’s strategic

objectives into performance metrics in four perspectives:

- Financial – I.E. Operating Income, Return On Capital Employed, And Economic

Value-Added.

- Internal Processes – I.E. Cost, Throughput, And Quality. These Are For Business

Processes Such As Procurement, Production, And Order Fulfillment.

- Customers – I.E. Customer Satisfaction, Customer Retention, And Market Share In

Target Segments.

- Learning And Growth – I.E. Employee Satisfaction, Employee Retention, And Skill

Sets, Etc.

These four views are intended to encompass all of the organization's present and future

operations, both internally and externally. These viewpoints give useful information on how

successfully the strategic plan is being implemented, allowing adjustments to be made as

necessary.

They aren't merely a collection of disparate viewpoints. There is a logical connection between

the two. Learning and growth, for example, contribute to enhanced business processes, which

in turn lead to higher customer value and, ultimately, improved financial performance. The

following is a diagram of the Balanced Scorecard framework:

9

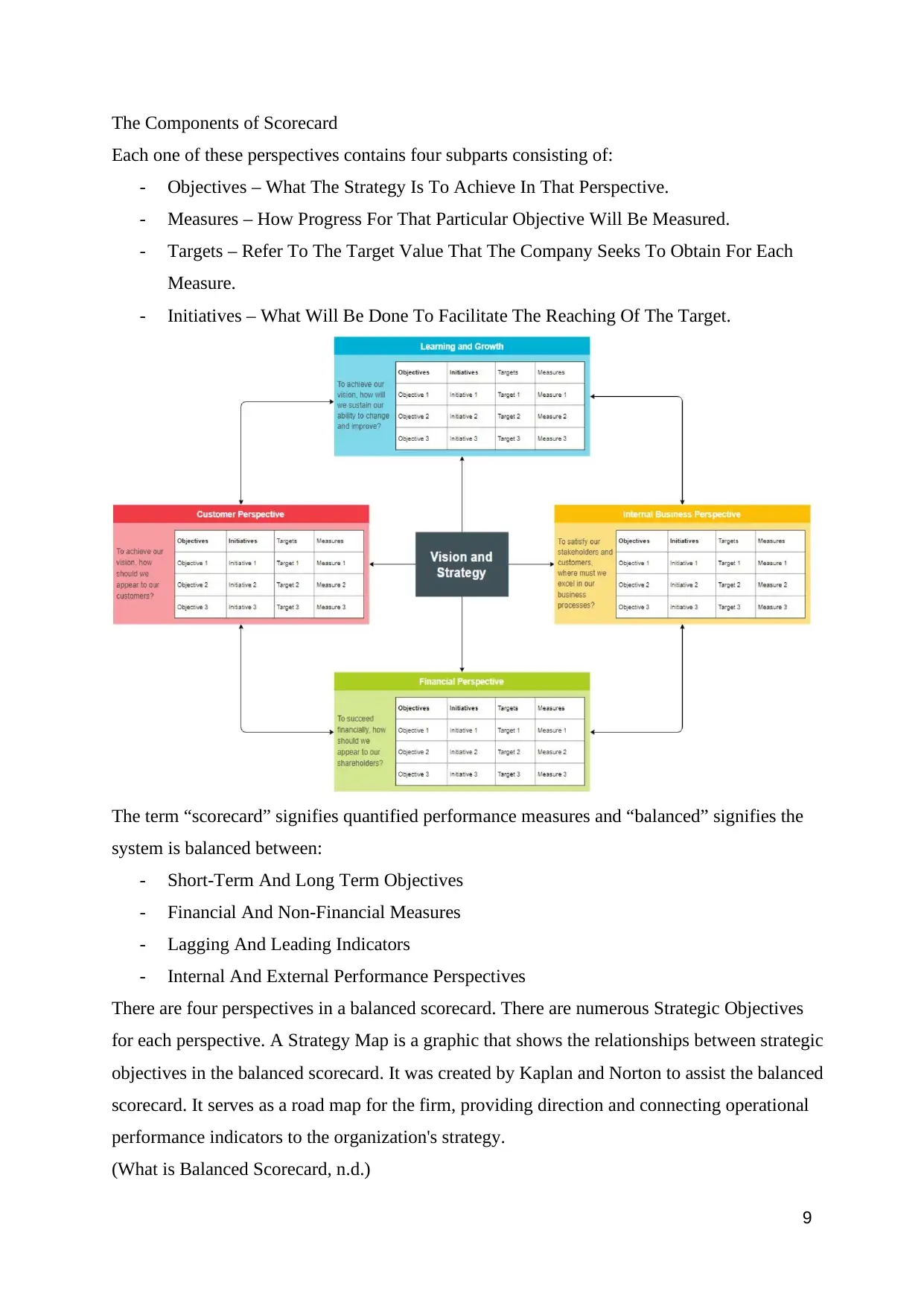

The Components of Scorecard

Each one of these perspectives contains four subparts consisting of:

- Objectives – What The Strategy Is To Achieve In That Perspective.

- Measures – How Progress For That Particular Objective Will Be Measured.

- Targets – Refer To The Target Value That The Company Seeks To Obtain For Each

Measure.

- Initiatives – What Will Be Done To Facilitate The Reaching Of The Target.

The term “scorecard” signifies quantified performance measures and “balanced” signifies the

system is balanced between:

- Short-Term And Long Term Objectives

- Financial And Non-Financial Measures

- Lagging And Leading Indicators

- Internal And External Performance Perspectives

There are four perspectives in a balanced scorecard. There are numerous Strategic Objectives

for each perspective. A Strategy Map is a graphic that shows the relationships between strategic

objectives in the balanced scorecard. It was created by Kaplan and Norton to assist the balanced

scorecard. It serves as a road map for the firm, providing direction and connecting operational

performance indicators to the organization's strategy.

(What is Balanced Scorecard, n.d.)

The Components of Scorecard

Each one of these perspectives contains four subparts consisting of:

- Objectives – What The Strategy Is To Achieve In That Perspective.

- Measures – How Progress For That Particular Objective Will Be Measured.

- Targets – Refer To The Target Value That The Company Seeks To Obtain For Each

Measure.

- Initiatives – What Will Be Done To Facilitate The Reaching Of The Target.

The term “scorecard” signifies quantified performance measures and “balanced” signifies the

system is balanced between:

- Short-Term And Long Term Objectives

- Financial And Non-Financial Measures

- Lagging And Leading Indicators

- Internal And External Performance Perspectives

There are four perspectives in a balanced scorecard. There are numerous Strategic Objectives

for each perspective. A Strategy Map is a graphic that shows the relationships between strategic

objectives in the balanced scorecard. It was created by Kaplan and Norton to assist the balanced

scorecard. It serves as a road map for the firm, providing direction and connecting operational

performance indicators to the organization's strategy.

(What is Balanced Scorecard, n.d.)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2

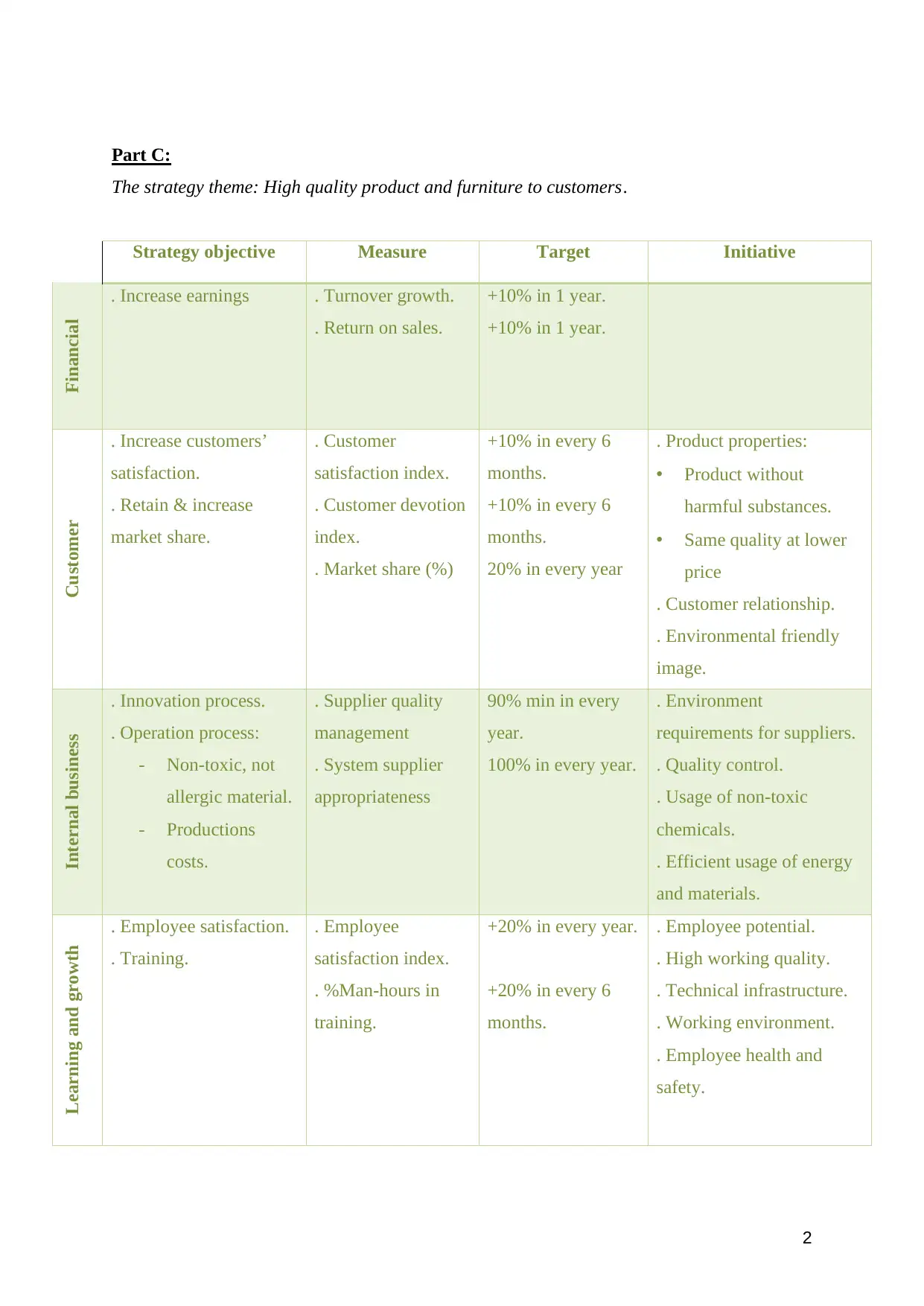

Part C:

The strategy theme: High quality product and furniture to customers.

Strategy objective Measure Target Initiative

Financial . Increase earnings . Turnover growth.

. Return on sales.

+10% in 1 year.

+10% in 1 year.

Customer

. Increase customers’

satisfaction.

. Retain & increase

market share.

. Customer

satisfaction index.

. Customer devotion

index.

. Market share (%)

+10% in every 6

months.

+10% in every 6

months.

20% in every year

. Product properties:

• Product without

harmful substances.

• Same quality at lower

price

. Customer relationship.

. Environmental friendly

image.

Internal business

. Innovation process.

. Operation process:

- Non-toxic, not

allergic material.

- Productions

costs.

. Supplier quality

management

. System supplier

appropriateness

90% min in every

year.

100% in every year.

. Environment

requirements for suppliers.

. Quality control.

. Usage of non-toxic

chemicals.

. Efficient usage of energy

and materials.

Learning and growth . Employee satisfaction.

. Training.

. Employee

satisfaction index.

. %Man-hours in

training.

+20% in every year.

+20% in every 6

months.

. Employee potential.

. High working quality.

. Technical infrastructure.

. Working environment.

. Employee health and

safety.

Part C:

The strategy theme: High quality product and furniture to customers.

Strategy objective Measure Target Initiative

Financial . Increase earnings . Turnover growth.

. Return on sales.

+10% in 1 year.

+10% in 1 year.

Customer

. Increase customers’

satisfaction.

. Retain & increase

market share.

. Customer

satisfaction index.

. Customer devotion

index.

. Market share (%)

+10% in every 6

months.

+10% in every 6

months.

20% in every year

. Product properties:

• Product without

harmful substances.

• Same quality at lower

price

. Customer relationship.

. Environmental friendly

image.

Internal business

. Innovation process.

. Operation process:

- Non-toxic, not

allergic material.

- Productions

costs.

. Supplier quality

management

. System supplier

appropriateness

90% min in every

year.

100% in every year.

. Environment

requirements for suppliers.

. Quality control.

. Usage of non-toxic

chemicals.

. Efficient usage of energy

and materials.

Learning and growth . Employee satisfaction.

. Training.

. Employee

satisfaction index.

. %Man-hours in

training.

+20% in every year.

+20% in every 6

months.

. Employee potential.

. High working quality.

. Technical infrastructure.

. Working environment.

. Employee health and

safety.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3

The strategy map of balanced scorecard is about High quality products and furniture to

customer of CMI company:

Beginning with the financial perspective of the strategy map, there is just one main objective:

"Increase Earnings." With two measurements are turnover growth and return on sales. There

are four different types of company's strategies: clean, efficient, innovative and progressive. A

company which follows the strategy on environmental and social objectives and measures to

reduce their costs. It will strive for identifying and exploiting “win-win-situations” and will

thus aim for the measures that help assess whether environmental and social standards are met

in the most cost efficient way. Its main objective is to minimize the cost-related ecological

damage per product or service unit, typically realized by savings of materials, energy, water

and waste. Measures would look at cost savings from pollution prevention rather than

monitoring end-of-pipe solutions. So that the target of two measurements is rise up to 10% in

the beginning year applying and can increase higher after years.

Concerning the consumer, two goals are stated: “Increase Customer Satisfaction” and “Retain

& Increase Market Share.” The metric "Customer Satisfaction Index" is offered for "Customer

Satisfaction," while two measures, "Customer Devotion Index" and "Percentage of Market

Share," are determined for "Retain & Increase Market Share." The third measure in this specific

theme and perspective (Percentage of Market Share), concerns the change of share (%), which

in turn comes from the qualitative characteristics contribution of company’s products. From

the customer’s perspective it is vital to tender products with lower price but of the same quality.

It is crucial for the company to be able to compete with the other producers on the market. The

price of a product is related to production costs as well as environmental friendly the products

are. It depends on the efficient use of energy and materials. So the eco-efficiency strategy is

very appropriate for the require about health aspect in nowadays of consumers with expect

products not to contain toxic and allergenic materials and not to cause allergies. The percentage

of “Customer Satisfaction Index”, "Customer Devotion Index" and "Percentage of Market

Share" measure, must be monitored and measured every six months from the started day of

eco-efficiency strategy and in every year for market share, and the target for this objective

suggests that increase 10% for Customer Satisfaction Index as well as Customer Devotion

Index and 20% for market shares.

The strategy map of balanced scorecard is about High quality products and furniture to

customer of CMI company:

Beginning with the financial perspective of the strategy map, there is just one main objective:

"Increase Earnings." With two measurements are turnover growth and return on sales. There

are four different types of company's strategies: clean, efficient, innovative and progressive. A

company which follows the strategy on environmental and social objectives and measures to

reduce their costs. It will strive for identifying and exploiting “win-win-situations” and will

thus aim for the measures that help assess whether environmental and social standards are met

in the most cost efficient way. Its main objective is to minimize the cost-related ecological

damage per product or service unit, typically realized by savings of materials, energy, water

and waste. Measures would look at cost savings from pollution prevention rather than

monitoring end-of-pipe solutions. So that the target of two measurements is rise up to 10% in

the beginning year applying and can increase higher after years.

Concerning the consumer, two goals are stated: “Increase Customer Satisfaction” and “Retain

& Increase Market Share.” The metric "Customer Satisfaction Index" is offered for "Customer

Satisfaction," while two measures, "Customer Devotion Index" and "Percentage of Market

Share," are determined for "Retain & Increase Market Share." The third measure in this specific

theme and perspective (Percentage of Market Share), concerns the change of share (%), which

in turn comes from the qualitative characteristics contribution of company’s products. From

the customer’s perspective it is vital to tender products with lower price but of the same quality.

It is crucial for the company to be able to compete with the other producers on the market. The

price of a product is related to production costs as well as environmental friendly the products

are. It depends on the efficient use of energy and materials. So the eco-efficiency strategy is

very appropriate for the require about health aspect in nowadays of consumers with expect

products not to contain toxic and allergenic materials and not to cause allergies. The percentage

of “Customer Satisfaction Index”, "Customer Devotion Index" and "Percentage of Market

Share" measure, must be monitored and measured every six months from the started day of

eco-efficiency strategy and in every year for market share, and the target for this objective

suggests that increase 10% for Customer Satisfaction Index as well as Customer Devotion

Index and 20% for market shares.

4

For internal business has two objectives: Innovation process and Operation process (Non-toxic,

not allergic material, productions costs). The two measures for these objectives are supplier

quality and system supplier appropriateness. The company’s suppliers must have been

approved by any accredited quality assurance organization. Purchased parts that do not

conform to specifications can impact every aspect of the company’s business. Both the buyer’s

approach and specification management are keys to controlling supplier quality. Competitive

cost, service, delivery time and product quality are fundamental criteria of the supplier

evaluation The initiative for internal business: environment requirements for suppliers quality

control, usage of non-toxic chemicals, efficient usage of energy and materials are very

important so that supplier quality management need to reach the target at least 90% min in

every year and the system supplier appropriateness has the target with 100% each year.

The two Internal Business objectives are associated with the respective objectives of learning

and growth perspective, “Training” and “Improve Employee Satisfaction”. The measure for

the first one (Training) is “Percentage of Man-hours in Training” with the target is increase

20% in each 6 months. Employees’ training is central to company’s strategy. Because the

company's goal is to produce eco-friendly products, the employees need to be trained in the

basics of the production process. Training will start from the managers and supervisors

afterwards will gradually increase the percentage of employees trained to 20% every six

months. “Employee Satisfaction Index” is the measure for the second objective (Improve

Employee Satisfaction) has the target is rise 20% in every year. The company's current goal is

to produce and supply healthy as well as environmentally friendly products. There will be many

changes in work that make employees feel pressure to learn new knowledge, so it is very

important for the company to pay attention to employee satisfaction during this time. So that

the initiative for this perspective is employee potential, high working quality, technical

infrastructure, working environment and employee health and safety for the target of rising up

employees satisfaction to 20% in each year.

For internal business has two objectives: Innovation process and Operation process (Non-toxic,

not allergic material, productions costs). The two measures for these objectives are supplier

quality and system supplier appropriateness. The company’s suppliers must have been

approved by any accredited quality assurance organization. Purchased parts that do not

conform to specifications can impact every aspect of the company’s business. Both the buyer’s

approach and specification management are keys to controlling supplier quality. Competitive

cost, service, delivery time and product quality are fundamental criteria of the supplier

evaluation The initiative for internal business: environment requirements for suppliers quality

control, usage of non-toxic chemicals, efficient usage of energy and materials are very

important so that supplier quality management need to reach the target at least 90% min in

every year and the system supplier appropriateness has the target with 100% each year.

The two Internal Business objectives are associated with the respective objectives of learning

and growth perspective, “Training” and “Improve Employee Satisfaction”. The measure for

the first one (Training) is “Percentage of Man-hours in Training” with the target is increase

20% in each 6 months. Employees’ training is central to company’s strategy. Because the

company's goal is to produce eco-friendly products, the employees need to be trained in the

basics of the production process. Training will start from the managers and supervisors

afterwards will gradually increase the percentage of employees trained to 20% every six

months. “Employee Satisfaction Index” is the measure for the second objective (Improve

Employee Satisfaction) has the target is rise 20% in every year. The company's current goal is

to produce and supply healthy as well as environmentally friendly products. There will be many

changes in work that make employees feel pressure to learn new knowledge, so it is very

important for the company to pay attention to employee satisfaction during this time. So that

the initiative for this perspective is employee potential, high working quality, technical

infrastructure, working environment and employee health and safety for the target of rising up

employees satisfaction to 20% in each year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.