GSBS6002: Analyzing the Effectiveness of Bank A's Online Security

VerifiedAdded on 2023/04/17

|18

|3401

|160

Report

AI Summary

This report assesses the effectiveness of Bank A's online security system by analyzing customer experiences with online fraud. It uses hypothesis testing and statistical techniques like T-tests and chi-square to evaluate the impact of security measures and the prevalence of fraud among Bank A's customers. The research involved surveying 2000 customers, with 420 providing comprehensive responses. The study identifies key factors contributing to online fraud, examines customer behaviors, and proposes recommendations for enhancing Bank A's security protocols to mitigate risks and improve customer trust. The findings highlight the importance of robust security measures and continuous monitoring to combat evolving online fraud techniques, ultimately aiming to strengthen Bank A's market position and protect its customers.

Running head: THE EFFECTIVENESS OF BANK A’S ONLINE SECURITY SYSTEM 0

The Effectiveness of Bank A’s Online Security System

RESEARCH REPORT

Student’s Name

Affiliation

The Effectiveness of Bank A’s Online Security System

RESEARCH REPORT

Student’s Name

Affiliation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EFFECTIVENESS OF BANK A’S ONLINE SECURITY SYSTEM 1

TABLE OF CONTENTS

1. Executive Summary 2

2. Introduction 2

3. Research Design 4

a. Research approach 4

b. Data collection Method 4

c. Sampling Procedures 4

d. Ethical considerations 4

4. Hypothesis Development 5

5. Statistical Technique and Justification 6

6. Results, Statistical and non statistical interpretation 7

7. Analysis and summary of statistical results 8

8. Recommendations 9

9. References 10

TABLE OF CONTENTS

1. Executive Summary 2

2. Introduction 2

3. Research Design 4

a. Research approach 4

b. Data collection Method 4

c. Sampling Procedures 4

d. Ethical considerations 4

4. Hypothesis Development 5

5. Statistical Technique and Justification 6

6. Results, Statistical and non statistical interpretation 7

7. Analysis and summary of statistical results 8

8. Recommendations 9

9. References 10

EFFECTIVENESS OF BANK A’S ONLINE SECURITY SYSTEM 2

1. Executive Summary

a. Data and method of Analysis

The research study used hypothesis parameters to get the mean difference in experience

with personal fraud compared to strategies of reducing fraud. T- Test results from the research

study worked on the value of t as (5.181456) is indicating a higher value compared to the critical

value of t at (1.987894) where the value of p that was used for comparing the significance level.

However, using the chi-square method it was realized that an association between the customer

banking online and experiencing card fraud. The number of customers not robbed indicated a

high percentage compared with those who experienced personal fraud (Hua, 2008).

b. Discussion of the subject matter.

Online banking is the way of conducting financial transactions through the website. The

method offers their customers every service that can be given manually. The services are offered

through internet banking in depositing money, transfers paying all the bills. The exercise is

carried out by the user by use of mobile phones, tablets desk tops electronic gadget that is

internet connected ( Pande & Zambreno, 2013).This method does not require physical

appearance of the clients all activities are carried at the customers own convenience. The mode

of banking faces few challenges such as connectivity and unavailable services for large sums of

money transaction.

Limitations

The research study work faced the following challenges that need to be encountered:

Scarcity of the research materials it proved difficult gathering information from the

customers.

1. Executive Summary

a. Data and method of Analysis

The research study used hypothesis parameters to get the mean difference in experience

with personal fraud compared to strategies of reducing fraud. T- Test results from the research

study worked on the value of t as (5.181456) is indicating a higher value compared to the critical

value of t at (1.987894) where the value of p that was used for comparing the significance level.

However, using the chi-square method it was realized that an association between the customer

banking online and experiencing card fraud. The number of customers not robbed indicated a

high percentage compared with those who experienced personal fraud (Hua, 2008).

b. Discussion of the subject matter.

Online banking is the way of conducting financial transactions through the website. The

method offers their customers every service that can be given manually. The services are offered

through internet banking in depositing money, transfers paying all the bills. The exercise is

carried out by the user by use of mobile phones, tablets desk tops electronic gadget that is

internet connected ( Pande & Zambreno, 2013).This method does not require physical

appearance of the clients all activities are carried at the customers own convenience. The mode

of banking faces few challenges such as connectivity and unavailable services for large sums of

money transaction.

Limitations

The research study work faced the following challenges that need to be encountered:

Scarcity of the research materials it proved difficult gathering information from the

customers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EFFECTIVENESS OF BANK A’S ONLINE SECURITY SYSTEM 3

Privacy/Secrecy of the customers was also a problem since the participants were not free

to share their personal experiences.

Poor attitude from the customers was a challenge since some clients were not unwilling

to answer survey questions.

Time was limited in conducting the research since the exercise was tiresome.

Effectiveness of Bank A’s Online Security System

2. Introduction

The research studies carried on internet banking security fraud technique is growing

especially with increased scandals verified with bank A’s company customers. The purpose of

carrying out this research study is to report and address online fraud experiences with Bank A’s

clients and seek ways of improving the security of the company. As a result, a survey on two

thousand customers was carried out considering the personal experiences on fraudulently

through the online transaction using Bank A. It is revealed that some of the customers using

Bank A face various challenges concerning personal fraud transaction using an online marketing

system. However, the research investigates on to improve the market share and discuses the

analysis of the data obtained while conducting the survey. The survey aimed at analyzing online

fraudulent experienced by the customers in relation to how the challenge can be solved or the

necessary measures to improve performance and effeteness of bank A. The outcome and the

results of the survey were statistically analyzed to test the comparison of the mean of the

variables and the predetermined means (Chua & Wareham, 2004).

a. Objectives of the analysis

Privacy/Secrecy of the customers was also a problem since the participants were not free

to share their personal experiences.

Poor attitude from the customers was a challenge since some clients were not unwilling

to answer survey questions.

Time was limited in conducting the research since the exercise was tiresome.

Effectiveness of Bank A’s Online Security System

2. Introduction

The research studies carried on internet banking security fraud technique is growing

especially with increased scandals verified with bank A’s company customers. The purpose of

carrying out this research study is to report and address online fraud experiences with Bank A’s

clients and seek ways of improving the security of the company. As a result, a survey on two

thousand customers was carried out considering the personal experiences on fraudulently

through the online transaction using Bank A. It is revealed that some of the customers using

Bank A face various challenges concerning personal fraud transaction using an online marketing

system. However, the research investigates on to improve the market share and discuses the

analysis of the data obtained while conducting the survey. The survey aimed at analyzing online

fraudulent experienced by the customers in relation to how the challenge can be solved or the

necessary measures to improve performance and effeteness of bank A. The outcome and the

results of the survey were statistically analyzed to test the comparison of the mean of the

variables and the predetermined means (Chua & Wareham, 2004).

a. Objectives of the analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EFFECTIVENESS OF BANK A’S ONLINE SECURITY SYSTEM 4

To determine internet banking customer’s behavior concerning online transactions and kind

of experience perceived using money line banking or the risks they incur. To determine the

sources and causes of internet bank thefts with bank A. Necessary measures to be put in place for

implementation in order to prevent online bank theft. (Duignan, 2013). To determine the

contributions of technology associated with internet banking and possible risks of IT in the

market. The study will research and determine if there are websites that are secure for online

services and banking. Therefore, it is advisable for the company to find ways of preventing

cooperative fraud bank in the financial institutions for better economic development (Dada,

2007).

Internet banking is highly growing since it provides quick access and saves the company

extra costs that may be incurred in making the transactions. However, it is argued that a third of

the customers surveyed suffered from fraudulent transaction cases. The research conducted

showed that there is a gradual increase in numbers with those customers who are using online

bank A (DeYoung, 2005). Arguably; we did not have the clients with the same challenges of

online fraudulent using online banking due to a different mode of the transaction such as manual

banking rather than online. Most of the online fraudulent banking happens in through the

customer’s username and password is shared to the third party. Two-thirds of the customers cited

being scammed through the emails sent to their accounts and risky sharing their personal

information in the hands of the fraudulent (Guriting $ Oly 2006).

3. Research Design

c. Research Approach

To determine internet banking customer’s behavior concerning online transactions and kind

of experience perceived using money line banking or the risks they incur. To determine the

sources and causes of internet bank thefts with bank A. Necessary measures to be put in place for

implementation in order to prevent online bank theft. (Duignan, 2013). To determine the

contributions of technology associated with internet banking and possible risks of IT in the

market. The study will research and determine if there are websites that are secure for online

services and banking. Therefore, it is advisable for the company to find ways of preventing

cooperative fraud bank in the financial institutions for better economic development (Dada,

2007).

Internet banking is highly growing since it provides quick access and saves the company

extra costs that may be incurred in making the transactions. However, it is argued that a third of

the customers surveyed suffered from fraudulent transaction cases. The research conducted

showed that there is a gradual increase in numbers with those customers who are using online

bank A (DeYoung, 2005). Arguably; we did not have the clients with the same challenges of

online fraudulent using online banking due to a different mode of the transaction such as manual

banking rather than online. Most of the online fraudulent banking happens in through the

customer’s username and password is shared to the third party. Two-thirds of the customers cited

being scammed through the emails sent to their accounts and risky sharing their personal

information in the hands of the fraudulent (Guriting $ Oly 2006).

3. Research Design

c. Research Approach

EFFECTIVENESS OF BANK A’S ONLINE SECURITY SYSTEM 5

In an attempt to handle these questions, the participants were required to respond to some

questions that required eight questions of comprehensive feedback. Arguably, the research

required to determine the number of individuals who have been falsified using online banking,

achieve the ethical results cited with bank A. The survey involved both female and male

participants of age ranging from twenty-eight to fifty-six who use online banking for accuracy

and reliability of data collection. The customer experience survey questions were administered

individually to the customers who assisted in data collection through their responses (Duman &

Ozcelik, 2011).

d. Data collection method

The 2000 customers intended to be interviewed only 420 customers responded

comprehensively in the survey conducted to complete the eight customer experience survey

questions to determine:

I. Whether the customers have owned a credit, debit card in the past 12 months?

II. Whether experienced credit online banking fraud in the last 12 months

III. The number of times the customers experienced card fraud in last 12 months

IV. How personal details obtained in most recent incident of card fraud

V. Card details copied or obtained during use

VI. Amount of time lost in most recent incident of credit card fraud

VII. Personal information

e. Sampling Procedures

The research study examined some subgroup of customers with or without the cards

concerning internet banking. The sampling procedure deployed was faced on face

In an attempt to handle these questions, the participants were required to respond to some

questions that required eight questions of comprehensive feedback. Arguably, the research

required to determine the number of individuals who have been falsified using online banking,

achieve the ethical results cited with bank A. The survey involved both female and male

participants of age ranging from twenty-eight to fifty-six who use online banking for accuracy

and reliability of data collection. The customer experience survey questions were administered

individually to the customers who assisted in data collection through their responses (Duman &

Ozcelik, 2011).

d. Data collection method

The 2000 customers intended to be interviewed only 420 customers responded

comprehensively in the survey conducted to complete the eight customer experience survey

questions to determine:

I. Whether the customers have owned a credit, debit card in the past 12 months?

II. Whether experienced credit online banking fraud in the last 12 months

III. The number of times the customers experienced card fraud in last 12 months

IV. How personal details obtained in most recent incident of card fraud

V. Card details copied or obtained during use

VI. Amount of time lost in most recent incident of credit card fraud

VII. Personal information

e. Sampling Procedures

The research study examined some subgroup of customers with or without the cards

concerning internet banking. The sampling procedure deployed was faced on face

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EFFECTIVENESS OF BANK A’S ONLINE SECURITY SYSTEM 6

communication for collecting data and information from the customers. The questions cut across

all the categories in terms of age, occupation, and gender.

f. Ethical consideration

The proposed research report will be explained to the individual participants, they are also

requested if they are willing to participate in the survey (Quah & Sriganesh, 2008). Once

confirmed the customers would be appreciated for their participation and contributions by

explaining the following ethical rules: Their personal name will not be associated with the

survey, all the contributions will be treated with high privacy, and all the participants are free to

refuse or agree to participate in the survey. The survey was used as a tool for collecting data and

information hence ethical conduct was necessary. It is also worth noting that the maintenance of

scientific rigor was important to the survey, some measures must be put in place for the

protection of high dignity to the participants involved in the survey. Respecting the participants

and keeping their privacy, never cause harm in any way. Professional code and regulations skills

should provide guidance and procures on how the research should be carried out (Guriting &

Oly, 2006).

4. Hypothesis Development

1. Is personal fraud experience the same across gender?

Null hypothesis (HO): Personal fraud experience of the surveyed customers is common across all

(female and male) gender.

Alternate hypothesis (HA): Personal experience on card fraud is not is common across all

(female and male) gender (Hosein, 2011).

communication for collecting data and information from the customers. The questions cut across

all the categories in terms of age, occupation, and gender.

f. Ethical consideration

The proposed research report will be explained to the individual participants, they are also

requested if they are willing to participate in the survey (Quah & Sriganesh, 2008). Once

confirmed the customers would be appreciated for their participation and contributions by

explaining the following ethical rules: Their personal name will not be associated with the

survey, all the contributions will be treated with high privacy, and all the participants are free to

refuse or agree to participate in the survey. The survey was used as a tool for collecting data and

information hence ethical conduct was necessary. It is also worth noting that the maintenance of

scientific rigor was important to the survey, some measures must be put in place for the

protection of high dignity to the participants involved in the survey. Respecting the participants

and keeping their privacy, never cause harm in any way. Professional code and regulations skills

should provide guidance and procures on how the research should be carried out (Guriting &

Oly, 2006).

4. Hypothesis Development

1. Is personal fraud experience the same across gender?

Null hypothesis (HO): Personal fraud experience of the surveyed customers is common across all

(female and male) gender.

Alternate hypothesis (HA): Personal experience on card fraud is not is common across all

(female and male) gender (Hosein, 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EFFECTIVENESS OF BANK A’S ONLINE SECURITY SYSTEM 7

2. Whether the customers experienced credit, debit or EFTPOS card fraud

Null hypothesis (HO): Personal fraud experience of the surveyed customers is common across all

(female and male) gender.

Alternate hypothesis (HA): Personal experience on card fraud is not is common across all

(female and male) gender (Yoon, 2010).

3. Number of times experienced card fraud in last 12 months

Null hypothesis (HO): Personal fraud experience of the surveyed customers is the same in a

number of times across all the (female and male) gender.

Alternate hypothesis (HA: Personal experience on card fraud is not the same in a number of

times across all (female and male) the genders.

4 How personal details obtained in most recent incident of card fraud

Null hypothesis (HO): Personal fraud experience of the surveyed customers is the same on

personal details of the clients.

Alternate hypothesis (HA): Personal experience on card fraud is not the same on personal details

of the clients.

5. Whether still finalizing issues associated with most recent credit card fraud

Null hypothesis (HO): Personal fraud experiences are the same across all the (female and male)

gender most recent credit card fraud

.

2. Whether the customers experienced credit, debit or EFTPOS card fraud

Null hypothesis (HO): Personal fraud experience of the surveyed customers is common across all

(female and male) gender.

Alternate hypothesis (HA): Personal experience on card fraud is not is common across all

(female and male) gender (Yoon, 2010).

3. Number of times experienced card fraud in last 12 months

Null hypothesis (HO): Personal fraud experience of the surveyed customers is the same in a

number of times across all the (female and male) gender.

Alternate hypothesis (HA: Personal experience on card fraud is not the same in a number of

times across all (female and male) the genders.

4 How personal details obtained in most recent incident of card fraud

Null hypothesis (HO): Personal fraud experience of the surveyed customers is the same on

personal details of the clients.

Alternate hypothesis (HA): Personal experience on card fraud is not the same on personal details

of the clients.

5. Whether still finalizing issues associated with most recent credit card fraud

Null hypothesis (HO): Personal fraud experiences are the same across all the (female and male)

gender most recent credit card fraud

.

EFFECTIVENESS OF BANK A’S ONLINE SECURITY SYSTEM 8

Alternate hypothesis (HA): Personal experience on card fraud is not the same across all the

(female and male) gender most recent credit card.

6. Amount of time lost in most recent incident of credit card fraud

Null hypothesis (HO): Personal fraud experience of the surveyed customers is common across all

(female and male) gender in the past one year.

Alternate hypothesis (HA): Personal experience on card fraud is not is common across all

(female and male) gender in the past one year.

7. What is your gender?

Null hypothesis (HO): Personal fraud experience of the surveyed customers is the same across all

(female and male) the gender.

Alternate hypothesis (HA): Personal experience on online banking is not the same in all the

(female and male) gender.

8. Personal fraud experience with age group.

Null hypothesis (HO): Personal fraud experience of the surveyed customers is common across all

(female and male) gender with age group.

Alternate hypothesis (HA): Personal experience on card fraud is not is common across all

(female and male) gender with age group.

5. Statistical Technique and Justification

Alternate hypothesis (HA): Personal experience on card fraud is not the same across all the

(female and male) gender most recent credit card.

6. Amount of time lost in most recent incident of credit card fraud

Null hypothesis (HO): Personal fraud experience of the surveyed customers is common across all

(female and male) gender in the past one year.

Alternate hypothesis (HA): Personal experience on card fraud is not is common across all

(female and male) gender in the past one year.

7. What is your gender?

Null hypothesis (HO): Personal fraud experience of the surveyed customers is the same across all

(female and male) the gender.

Alternate hypothesis (HA): Personal experience on online banking is not the same in all the

(female and male) gender.

8. Personal fraud experience with age group.

Null hypothesis (HO): Personal fraud experience of the surveyed customers is common across all

(female and male) gender with age group.

Alternate hypothesis (HA): Personal experience on card fraud is not is common across all

(female and male) gender with age group.

5. Statistical Technique and Justification

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EFFECTIVENESS OF BANK A’S ONLINE SECURITY SYSTEM 9

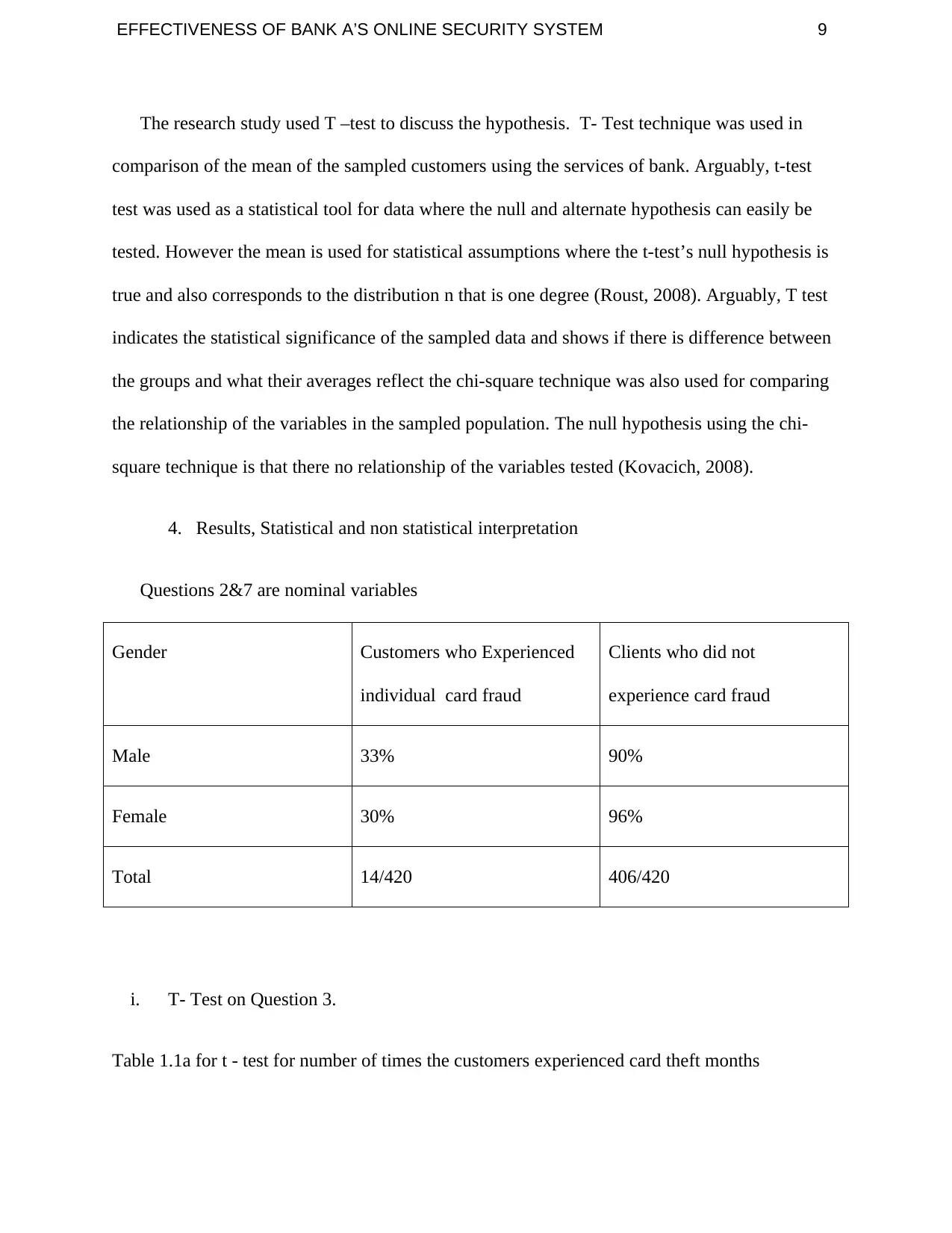

The research study used T –test to discuss the hypothesis. T- Test technique was used in

comparison of the mean of the sampled customers using the services of bank. Arguably, t-test

test was used as a statistical tool for data where the null and alternate hypothesis can easily be

tested. However the mean is used for statistical assumptions where the t-test’s null hypothesis is

true and also corresponds to the distribution n that is one degree (Roust, 2008). Arguably, T test

indicates the statistical significance of the sampled data and shows if there is difference between

the groups and what their averages reflect the chi-square technique was also used for comparing

the relationship of the variables in the sampled population. The null hypothesis using the chi-

square technique is that there no relationship of the variables tested (Kovacich, 2008).

4. Results, Statistical and non statistical interpretation

Questions 2&7 are nominal variables

Gender Customers who Experienced

individual card fraud

Clients who did not

experience card fraud

Male 33% 90%

Female 30% 96%

Total 14/420 406/420

i. T- Test on Question 3.

Table 1.1a for t - test for number of times the customers experienced card theft months

The research study used T –test to discuss the hypothesis. T- Test technique was used in

comparison of the mean of the sampled customers using the services of bank. Arguably, t-test

test was used as a statistical tool for data where the null and alternate hypothesis can easily be

tested. However the mean is used for statistical assumptions where the t-test’s null hypothesis is

true and also corresponds to the distribution n that is one degree (Roust, 2008). Arguably, T test

indicates the statistical significance of the sampled data and shows if there is difference between

the groups and what their averages reflect the chi-square technique was also used for comparing

the relationship of the variables in the sampled population. The null hypothesis using the chi-

square technique is that there no relationship of the variables tested (Kovacich, 2008).

4. Results, Statistical and non statistical interpretation

Questions 2&7 are nominal variables

Gender Customers who Experienced

individual card fraud

Clients who did not

experience card fraud

Male 33% 90%

Female 30% 96%

Total 14/420 406/420

i. T- Test on Question 3.

Table 1.1a for t - test for number of times the customers experienced card theft months

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EFFECTIVENESS OF BANK A’S ONLINE SECURITY SYSTEM 10

Experience on personal card

fraud

Effective strategy to reduce

fraud

Mean

Variance

Observations

Hypothesized mean difference

df

t calculated

P(T<t) for 1-tail

t Critical for 1-tail

P(T<t) for 2-tail

t Critical 2-tail

23.42341

68.52346

420

0

418

5.181456

2.567E-0.5

1.84563

0.0000874

1.987894

20

0

420

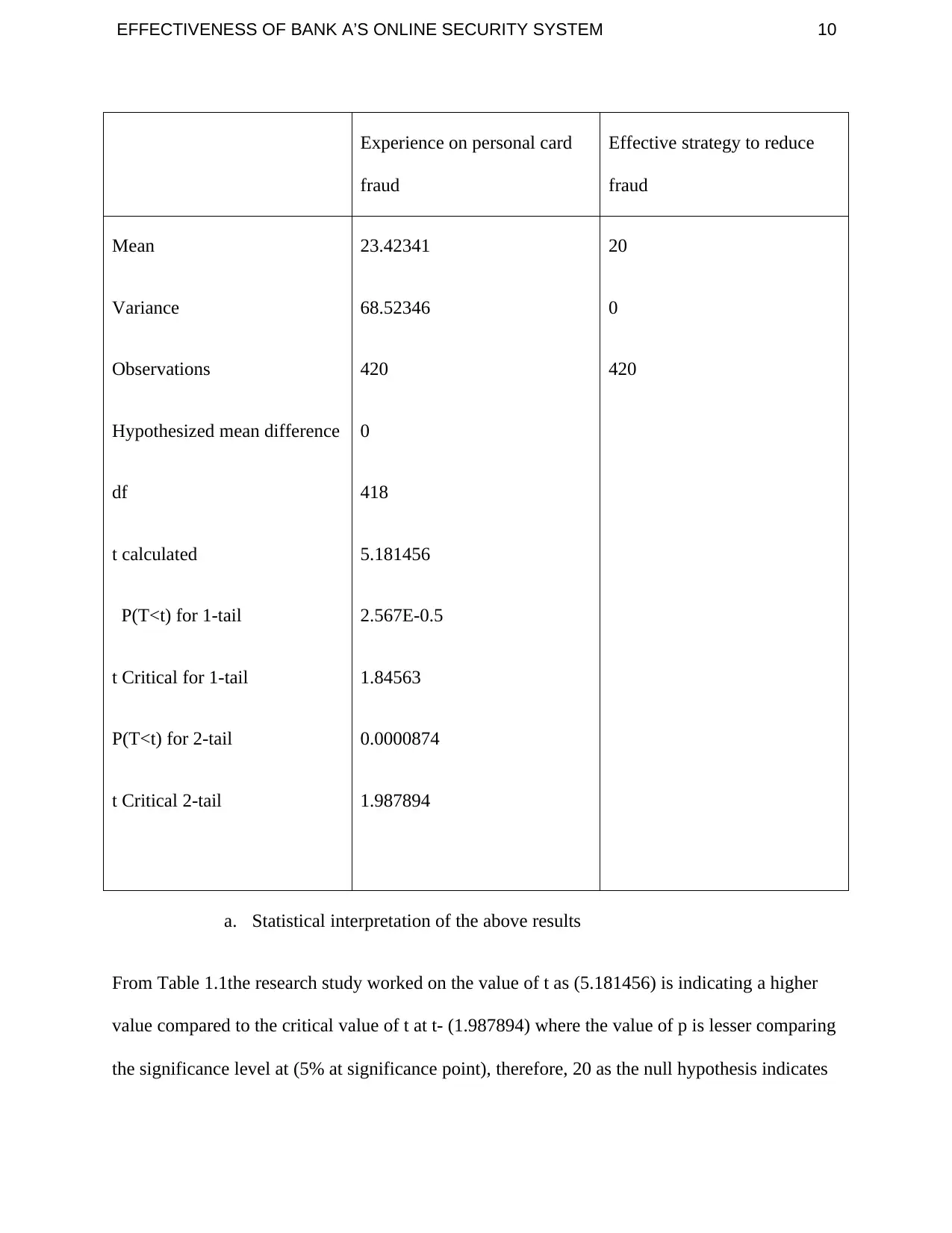

a. Statistical interpretation of the above results

From Table 1.1the research study worked on the value of t as (5.181456) is indicating a higher

value compared to the critical value of t at t- (1.987894) where the value of p is lesser comparing

the significance level at (5% at significance point), therefore, 20 as the null hypothesis indicates

Experience on personal card

fraud

Effective strategy to reduce

fraud

Mean

Variance

Observations

Hypothesized mean difference

df

t calculated

P(T<t) for 1-tail

t Critical for 1-tail

P(T<t) for 2-tail

t Critical 2-tail

23.42341

68.52346

420

0

418

5.181456

2.567E-0.5

1.84563

0.0000874

1.987894

20

0

420

a. Statistical interpretation of the above results

From Table 1.1the research study worked on the value of t as (5.181456) is indicating a higher

value compared to the critical value of t at t- (1.987894) where the value of p is lesser comparing

the significance level at (5% at significance point), therefore, 20 as the null hypothesis indicates

EFFECTIVENESS OF BANK A’S ONLINE SECURITY SYSTEM 11

is not number customers banking online with Bank A valued p at (0.0000874) at 5% significant

point (Yogi, 2011).

b. Non-statistical interpretation:

Average mean of online security (21.42341) is greater compared to the effective ways of

reducing bank fraud at 16 (value obtained from prediction model). Therefore, the average

numbers of the customers have experienced personal card fraud through internet banking with

bank A.

ii. Chi-square test on Question 4

Table 2: Chi-square test for personal details obtained in most recent card fraud

Recent card fraud

No. of customers with card

fraud cases

No. of customers with no

fraud card cases

14

406

3.333%

96.666%

Total number surveyed 420

Chi- square Tests

Pearson chi –square

Expected ratio

Association

Cases

Value

54.456

50.234

52.456

420

d

4

4

2

Statistical interpretation

There exists an association between the customer banking online and experiencing card fraud.

With 96.66% not robbed compared to 3.33% experience card fraud through online banking. U =0

is not number customers banking online with Bank A valued p at (0.0000874) at 5% significant

point (Yogi, 2011).

b. Non-statistical interpretation:

Average mean of online security (21.42341) is greater compared to the effective ways of

reducing bank fraud at 16 (value obtained from prediction model). Therefore, the average

numbers of the customers have experienced personal card fraud through internet banking with

bank A.

ii. Chi-square test on Question 4

Table 2: Chi-square test for personal details obtained in most recent card fraud

Recent card fraud

No. of customers with card

fraud cases

No. of customers with no

fraud card cases

14

406

3.333%

96.666%

Total number surveyed 420

Chi- square Tests

Pearson chi –square

Expected ratio

Association

Cases

Value

54.456

50.234

52.456

420

d

4

4

2

Statistical interpretation

There exists an association between the customer banking online and experiencing card fraud.

With 96.66% not robbed compared to 3.33% experience card fraud through online banking. U =0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.