BANK6002 - Bank Management Group Project: Risk Comparison Analysis

VerifiedAdded on 2022/09/07

|8

|1269

|34

Project

AI Summary

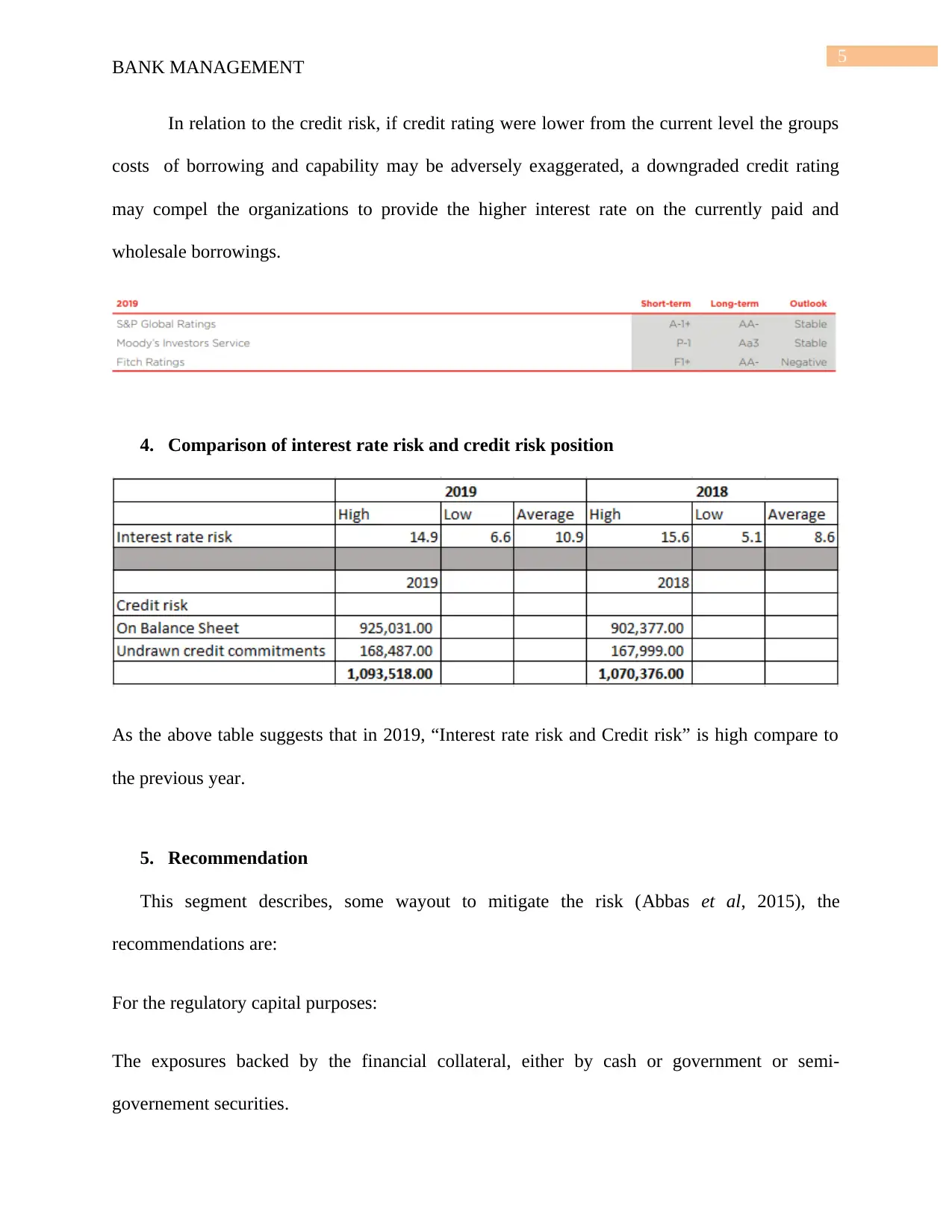

This student project, submitted on Desklib, provides a comprehensive analysis of bank management, specifically focusing on the interest rate risk and credit risk faced by financial institutions, such as Westpac Banking Corporation. The project analyzes the impact of the Reserve Bank of Australia's interest rate cuts on the bank's performance, including the effects on net interest margins, lending environments, and credit quality. It delves into the interest rate risk analysis, examining how fluctuations in interest rates can affect the bank's income and economic value. Moreover, it assesses credit risk by identifying the maximum credit exposure and potential impacts of credit rating downgrades. The project concludes with recommendations for mitigating these risks, including strategies for regulatory capital purposes and credit protection. The analysis incorporates data from 2019 and forecasts future interest rate trends, providing a practical understanding of risk management in the banking sector.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.