Business Finance: Report on Liquidity and Capital Structure of BOQ

VerifiedAdded on 2022/08/24

|12

|2940

|15

Report

AI Summary

This report provides a detailed financial analysis of the Bank of Queensland (BOQ), an Australian retail bank. It examines the bank's liquidity and capital structure from 2016 to 2019, utilizing financial ratios such as the current ratio, quick ratio, and debt ratio. The analysis includes a calculation of the cost of equity using the dividend growth model, offering insights into the required rate of return for shareholders. The report highlights BOQ's net working capital position, capital structure ratios, and overall financial risk. The findings suggest that the bank has a low working capital and a high debt ratio. The report also includes recommendations based on the financial data and industry trends, providing a comprehensive overview of BOQ's financial health and performance.

Running head: BUSINESS FINANCE

Business Finance

Name of the Student:

Name of the University:

Author’s Note:

Business Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS FINANCE

Table of Contents

Introduction......................................................................................................................................2

Discussion and Analysis..................................................................................................................2

Company Overview.....................................................................................................................2

Cost of Equity..............................................................................................................................4

Liquidity and Capital Structure...................................................................................................5

Capital Structure Ratio................................................................................................................6

Conclusion and Recommendations..................................................................................................9

References......................................................................................................................................10

Table of Contents

Introduction......................................................................................................................................2

Discussion and Analysis..................................................................................................................2

Company Overview.....................................................................................................................2

Cost of Equity..............................................................................................................................4

Liquidity and Capital Structure...................................................................................................5

Capital Structure Ratio................................................................................................................6

Conclusion and Recommendations..................................................................................................9

References......................................................................................................................................10

2BUSINESS FINANCE

Introduction

The assignment aims at evaluating the Bank of Queensland which is an Australian Retail

Bank that is having its headquarters in the Brisbane, Queensland. The analyzed bank is regarded

as one of the oldest operating financial institution in the Queensland and is having around 252

branches and 166 “owner managed” branches. The bank in specific has been analyzed in terms

of liquidity and capital structure whereby important aspects of the company has been analyzed in

order to get a review of the financial position of the company. Financial risk is one of the key

risk that the banking industry faces and the same has been well analyzed with the help of debt

ratio and total capital employed ratio which were some of the key aspects analyzed. On the other

hand, for analyzing the liquidity position of the company key ratio’s like current ratio and quick

ratio have been well deployed for the purpose of analyzing the financial statements of the

company. The application of the Dividend Growth Model has also been done specifically for the

purpose of well analyzing the Required Rate of Return from the stock analyzed (Boq.com.au

2020). From the view point of recommendation there were various factors and reasons which are

well associated with the company that have been analyzed based on the given set of numbers.

Discussion and Analysis

Company Overview

The analysis of the company has been done in specific with the help of the business

operations and activities that it undertakes for the purpose of well carrying on its business

activities. The Bank of Queensland is a key Australian Retail Bank that is headquartered in the

Brisbane, Queensland (Carletti, Goldstein and Leonello 2020). The analyzed bank is one of the

key and oldest operating financial institutions that is having around 252 branches throughout the

Australian region, which also includes the 78 corporate branches and a base of around 166

“owned managed” branches in the Australian Region. The bank is considered and regarded as

one of the top 100 Australian Companies that are ranked and marked in terms of market

capitalization on the Australian Securities Exchange. The company is well regulated with the

help of the Australian Prudential Regulation Authority and is also considered as an Authorized

Introduction

The assignment aims at evaluating the Bank of Queensland which is an Australian Retail

Bank that is having its headquarters in the Brisbane, Queensland. The analyzed bank is regarded

as one of the oldest operating financial institution in the Queensland and is having around 252

branches and 166 “owner managed” branches. The bank in specific has been analyzed in terms

of liquidity and capital structure whereby important aspects of the company has been analyzed in

order to get a review of the financial position of the company. Financial risk is one of the key

risk that the banking industry faces and the same has been well analyzed with the help of debt

ratio and total capital employed ratio which were some of the key aspects analyzed. On the other

hand, for analyzing the liquidity position of the company key ratio’s like current ratio and quick

ratio have been well deployed for the purpose of analyzing the financial statements of the

company. The application of the Dividend Growth Model has also been done specifically for the

purpose of well analyzing the Required Rate of Return from the stock analyzed (Boq.com.au

2020). From the view point of recommendation there were various factors and reasons which are

well associated with the company that have been analyzed based on the given set of numbers.

Discussion and Analysis

Company Overview

The analysis of the company has been done in specific with the help of the business

operations and activities that it undertakes for the purpose of well carrying on its business

activities. The Bank of Queensland is a key Australian Retail Bank that is headquartered in the

Brisbane, Queensland (Carletti, Goldstein and Leonello 2020). The analyzed bank is one of the

key and oldest operating financial institutions that is having around 252 branches throughout the

Australian region, which also includes the 78 corporate branches and a base of around 166

“owned managed” branches in the Australian Region. The bank is considered and regarded as

one of the top 100 Australian Companies that are ranked and marked in terms of market

capitalization on the Australian Securities Exchange. The company is well regulated with the

help of the Australian Prudential Regulation Authority and is also considered as an Authorized

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS FINANCE

Deposit taking institution. The key branches of the company in particular or key companies that

operates under the BOQ are as follows:

Virgin Money Australia: The BOQ offers and operates a number of brands that

is having a diversified range of products and services for the various personal and

business customers (Rehman et al., 2019).

BOQ Finance: The subsidiary is wholly owned by the BOQ, that well specializes

in management of assets, cash flows and other structured financial solutions.

BOQF is a key mid-market financier that provides deep industry and products

skills.

BOQ Specialist: BOQ Specializes in delivering distinctive banking solutions to

the niche market segments that well includes medical, dental and accounting

experts.

St. Andrew Insurance: St. Andrew acts as a leading Australian provider of

various life insurance products and consumer insurance products that are offered

by the company. Since, the year 1998, the company have been well helping to

protect the Australians by giving or delivering an innovative and streamlined

insurance solutions for various corporate partners and customers.

Net Working Capital Position

The net working capital shows the amount of liquidity that is available or present in the

company and the same can be well analyzed with the help of the current liabilities and current

assets that the company have reported for the time period analyzed. The net working capital of

the company has been well calculated with the help of the current assets less the amount of

current liabilities that the bank has reported. It is well important to analyze the working capital

that is available with the company and the same can be well analyzed with the help of the

changes and the movement that is observed in the current assets and the current liabilities of the

company. The net working capital of the Bank in the year 2018 was around -$7,125,000 and the

same has well decreased to an amount of -$4,507,000. The low working capital of the bank can

be well contributed to the fact that the increase in the current liabilities of the bank has been

much more than the increase in the current assets of the company, which have well decreased the

working capital. It is important that the management of the bank well maintains an adequate

Deposit taking institution. The key branches of the company in particular or key companies that

operates under the BOQ are as follows:

Virgin Money Australia: The BOQ offers and operates a number of brands that

is having a diversified range of products and services for the various personal and

business customers (Rehman et al., 2019).

BOQ Finance: The subsidiary is wholly owned by the BOQ, that well specializes

in management of assets, cash flows and other structured financial solutions.

BOQF is a key mid-market financier that provides deep industry and products

skills.

BOQ Specialist: BOQ Specializes in delivering distinctive banking solutions to

the niche market segments that well includes medical, dental and accounting

experts.

St. Andrew Insurance: St. Andrew acts as a leading Australian provider of

various life insurance products and consumer insurance products that are offered

by the company. Since, the year 1998, the company have been well helping to

protect the Australians by giving or delivering an innovative and streamlined

insurance solutions for various corporate partners and customers.

Net Working Capital Position

The net working capital shows the amount of liquidity that is available or present in the

company and the same can be well analyzed with the help of the current liabilities and current

assets that the company have reported for the time period analyzed. The net working capital of

the company has been well calculated with the help of the current assets less the amount of

current liabilities that the bank has reported. It is well important to analyze the working capital

that is available with the company and the same can be well analyzed with the help of the

changes and the movement that is observed in the current assets and the current liabilities of the

company. The net working capital of the Bank in the year 2018 was around -$7,125,000 and the

same has well decreased to an amount of -$4,507,000. The low working capital of the bank can

be well contributed to the fact that the increase in the current liabilities of the bank has been

much more than the increase in the current assets of the company, which have well decreased the

working capital. It is important that the management of the bank well maintains an adequate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS FINANCE

amount of working capital in the business so that the various business operations of the company

are well meet and the current obligations of the company are well paid in the due course of time

period. The current obligations or the current liabilities are in the form of accrued expenses or

the amount attributable to the accounts payables of the bank. It is important to note that since, the

bank are having a low amount of working capital they might have to and would be using long

term sources of finance for the purpose of meeting the current obligations of the company. The

better the management of the working capital the better is the operations and activities carried

out by the company for the purpose of handling the operations of the company.

Cost of Equity

The cost of equity for the firm can be well calculated with the help of the dividend

growth model whereby important aspects of the company has been well taken into considerations

including the price levels, dividend paid and the constant growth rate (Bao and Feng 2018). The

cost of equity for the firm has been well calculated with the help of the formula as shown below:

Po: Expected Dividend (D1)/(Required Return – Growth Rate).

Re: (Expected Dividend (Do*(1+g))/Price (Po)) + Growth Rate.

Re: (0.65*(1+5%)/7.51)+5%.

Re: 14.09%.

DIVIDEND GROWTH MODEL

REQUIRED RATE OF RETURN

DIVIDEND (DO) 0.65

DIVIDEND (D1) 0.68

GROWTH RATE 5%

PRICE (PO) 7.51

REQUIRED RETURN (RE) 14.09%

The cost of equity for the firm well shows the amount of return required or the minimum

return that is required by the shareholders of the company for taking the desired level of risk. In

order to well account for the required return the current share price or the prevailing share price

of the company has been taken into consideration (Sim and Wright 2017). The expected dividend

for the company has been calculated with the help of the dividend paid by the company in the

amount of working capital in the business so that the various business operations of the company

are well meet and the current obligations of the company are well paid in the due course of time

period. The current obligations or the current liabilities are in the form of accrued expenses or

the amount attributable to the accounts payables of the bank. It is important to note that since, the

bank are having a low amount of working capital they might have to and would be using long

term sources of finance for the purpose of meeting the current obligations of the company. The

better the management of the working capital the better is the operations and activities carried

out by the company for the purpose of handling the operations of the company.

Cost of Equity

The cost of equity for the firm can be well calculated with the help of the dividend

growth model whereby important aspects of the company has been well taken into considerations

including the price levels, dividend paid and the constant growth rate (Bao and Feng 2018). The

cost of equity for the firm has been well calculated with the help of the formula as shown below:

Po: Expected Dividend (D1)/(Required Return – Growth Rate).

Re: (Expected Dividend (Do*(1+g))/Price (Po)) + Growth Rate.

Re: (0.65*(1+5%)/7.51)+5%.

Re: 14.09%.

DIVIDEND GROWTH MODEL

REQUIRED RATE OF RETURN

DIVIDEND (DO) 0.65

DIVIDEND (D1) 0.68

GROWTH RATE 5%

PRICE (PO) 7.51

REQUIRED RETURN (RE) 14.09%

The cost of equity for the firm well shows the amount of return required or the minimum

return that is required by the shareholders of the company for taking the desired level of risk. In

order to well account for the required return the current share price or the prevailing share price

of the company has been taken into consideration (Sim and Wright 2017). The expected dividend

for the company has been calculated with the help of the dividend paid by the company in the

5BUSINESS FINANCE

last year multiplied by the constant growth model which was around 5%. The cost of equity for

the firm was calculated to be around 14.09% for the Bank of Queensland, which well reflects the

required rate of return that is derived or expected from the bank in the given set of time frame.

The cost of equity for the firm can be also calculated with the help of other key models like with

the help of the Capital Asset pricing model which well takes into account various market related

factors for determining the appropriate level of required return that is required by the

shareholders of the company for taking the level of risk that is undertaken. In this case since we

have incorporate the dividend discount model all the factors that are in well relation to the

company including the share price, dividend and the given set of information for the growth rate

the required rate of return for the stock has been calculated for current tine period.

Liquidity and Capital Structure

The liquidity and the capital structure of the company can be well analyzed by analyzing

the current assets and current liabilities that the company have reported in the financials for the

time period analyzed. On the other hand, the capital structure of the bank can be well analyzed

with the help and analyzing the application of debt that the company has done in correspondence

to the total assets and total capital that has been deployed for the year. The time period over

which the analysis has been well carried out for the firm has been for the period 2016-2019 and

the relevant changes that have been observed in the financials of the company for the stated time

period has been well taken into consideration (Mursalini, Husni and Hamidi 2017).

Liquidity Factor: The liquidity factor states how well the bank or the company is in managing

the current obligations of the company and the same can be well analyzed with the help of the

current ratio (Bouwman 2019). The metric states the amount of current assets that is primarily in

the form of cash & cash equivalents, accounts receivables and other short term investments that

the company well has in the stated time period for well tackling or for well paying off the current

obligations of the company. It is important that the company well manages there liquidity in a

crucial manner so that the current obligations of the company does not affect the business

operations or the various banking activities that is usually carried out by the bank

(Au.finance.yahoo.com 2019).

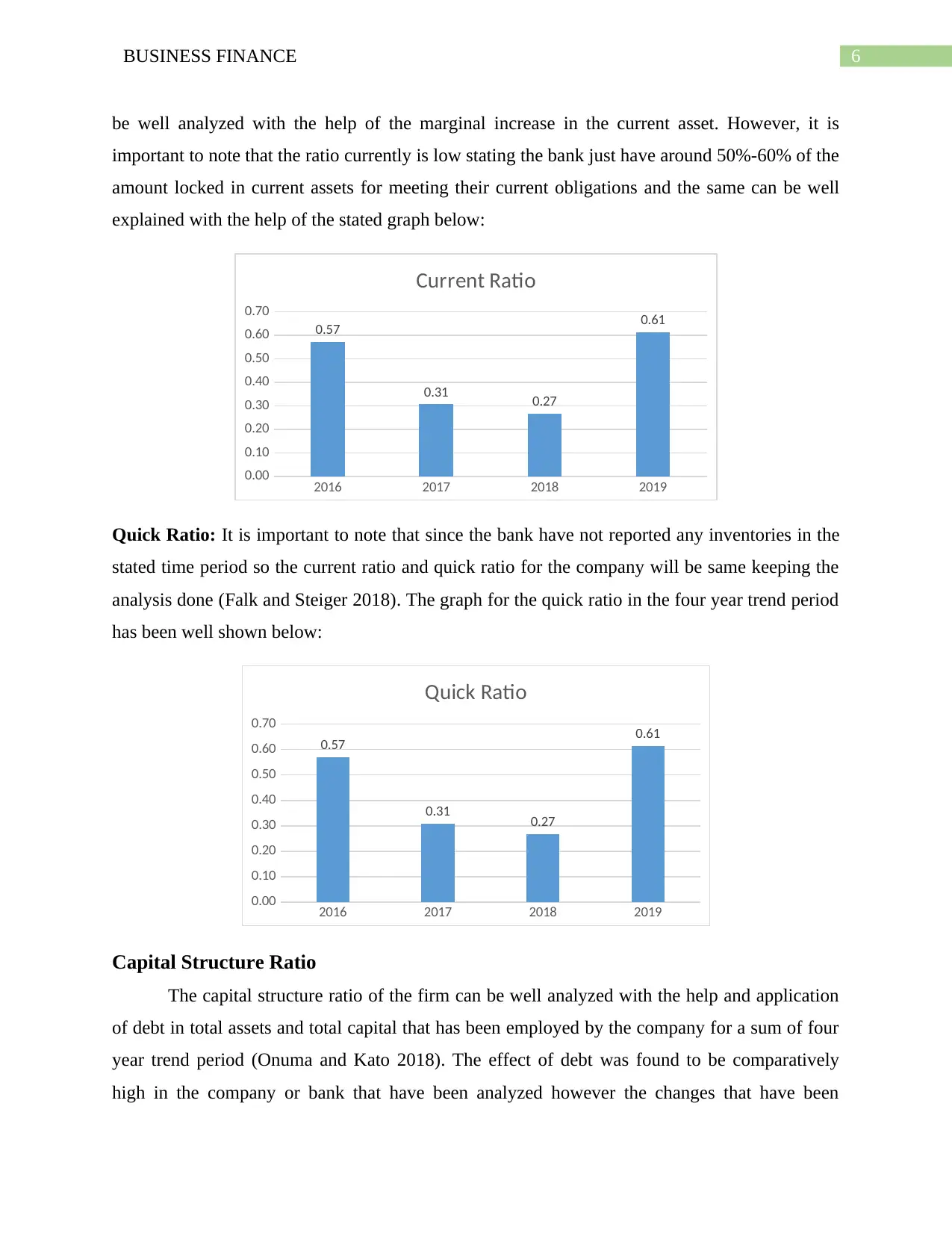

Current Ratio: The current ratio for the firm has been around 0.57 times in the year 2016 and

the same has well increased to around 0.61 times in the year 2019. The increase in the ratio can

last year multiplied by the constant growth model which was around 5%. The cost of equity for

the firm was calculated to be around 14.09% for the Bank of Queensland, which well reflects the

required rate of return that is derived or expected from the bank in the given set of time frame.

The cost of equity for the firm can be also calculated with the help of other key models like with

the help of the Capital Asset pricing model which well takes into account various market related

factors for determining the appropriate level of required return that is required by the

shareholders of the company for taking the level of risk that is undertaken. In this case since we

have incorporate the dividend discount model all the factors that are in well relation to the

company including the share price, dividend and the given set of information for the growth rate

the required rate of return for the stock has been calculated for current tine period.

Liquidity and Capital Structure

The liquidity and the capital structure of the company can be well analyzed by analyzing

the current assets and current liabilities that the company have reported in the financials for the

time period analyzed. On the other hand, the capital structure of the bank can be well analyzed

with the help and analyzing the application of debt that the company has done in correspondence

to the total assets and total capital that has been deployed for the year. The time period over

which the analysis has been well carried out for the firm has been for the period 2016-2019 and

the relevant changes that have been observed in the financials of the company for the stated time

period has been well taken into consideration (Mursalini, Husni and Hamidi 2017).

Liquidity Factor: The liquidity factor states how well the bank or the company is in managing

the current obligations of the company and the same can be well analyzed with the help of the

current ratio (Bouwman 2019). The metric states the amount of current assets that is primarily in

the form of cash & cash equivalents, accounts receivables and other short term investments that

the company well has in the stated time period for well tackling or for well paying off the current

obligations of the company. It is important that the company well manages there liquidity in a

crucial manner so that the current obligations of the company does not affect the business

operations or the various banking activities that is usually carried out by the bank

(Au.finance.yahoo.com 2019).

Current Ratio: The current ratio for the firm has been around 0.57 times in the year 2016 and

the same has well increased to around 0.61 times in the year 2019. The increase in the ratio can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS FINANCE

be well analyzed with the help of the marginal increase in the current asset. However, it is

important to note that the ratio currently is low stating the bank just have around 50%-60% of the

amount locked in current assets for meeting their current obligations and the same can be well

explained with the help of the stated graph below:

2016 2017 2018 2019

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.57

0.31 0.27

0.61

Current Ratio

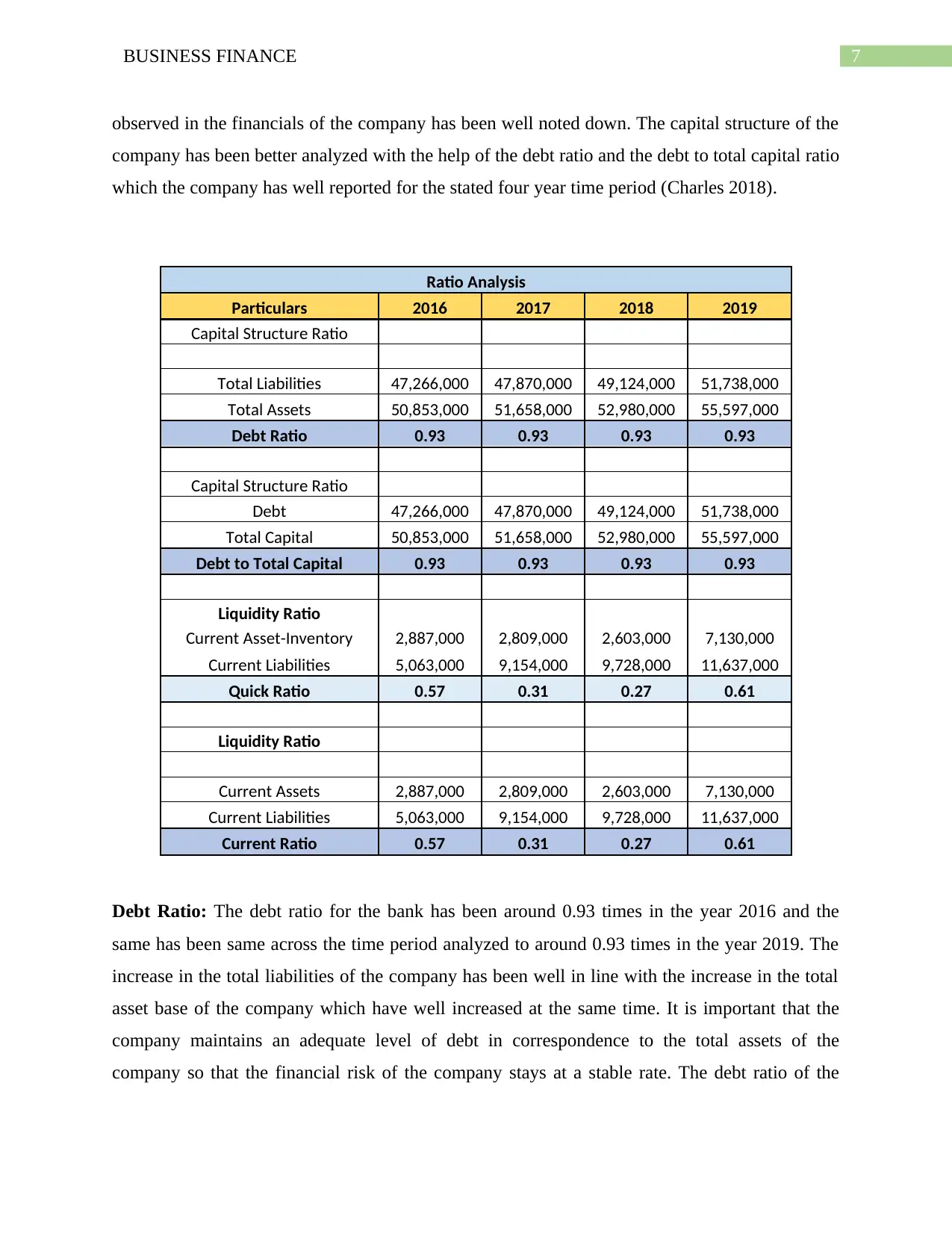

Quick Ratio: It is important to note that since the bank have not reported any inventories in the

stated time period so the current ratio and quick ratio for the company will be same keeping the

analysis done (Falk and Steiger 2018). The graph for the quick ratio in the four year trend period

has been well shown below:

2016 2017 2018 2019

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.57

0.31 0.27

0.61

Quick Ratio

Capital Structure Ratio

The capital structure ratio of the firm can be well analyzed with the help and application

of debt in total assets and total capital that has been employed by the company for a sum of four

year trend period (Onuma and Kato 2018). The effect of debt was found to be comparatively

high in the company or bank that have been analyzed however the changes that have been

be well analyzed with the help of the marginal increase in the current asset. However, it is

important to note that the ratio currently is low stating the bank just have around 50%-60% of the

amount locked in current assets for meeting their current obligations and the same can be well

explained with the help of the stated graph below:

2016 2017 2018 2019

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.57

0.31 0.27

0.61

Current Ratio

Quick Ratio: It is important to note that since the bank have not reported any inventories in the

stated time period so the current ratio and quick ratio for the company will be same keeping the

analysis done (Falk and Steiger 2018). The graph for the quick ratio in the four year trend period

has been well shown below:

2016 2017 2018 2019

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.57

0.31 0.27

0.61

Quick Ratio

Capital Structure Ratio

The capital structure ratio of the firm can be well analyzed with the help and application

of debt in total assets and total capital that has been employed by the company for a sum of four

year trend period (Onuma and Kato 2018). The effect of debt was found to be comparatively

high in the company or bank that have been analyzed however the changes that have been

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS FINANCE

observed in the financials of the company has been well noted down. The capital structure of the

company has been better analyzed with the help of the debt ratio and the debt to total capital ratio

which the company has well reported for the stated four year time period (Charles 2018).

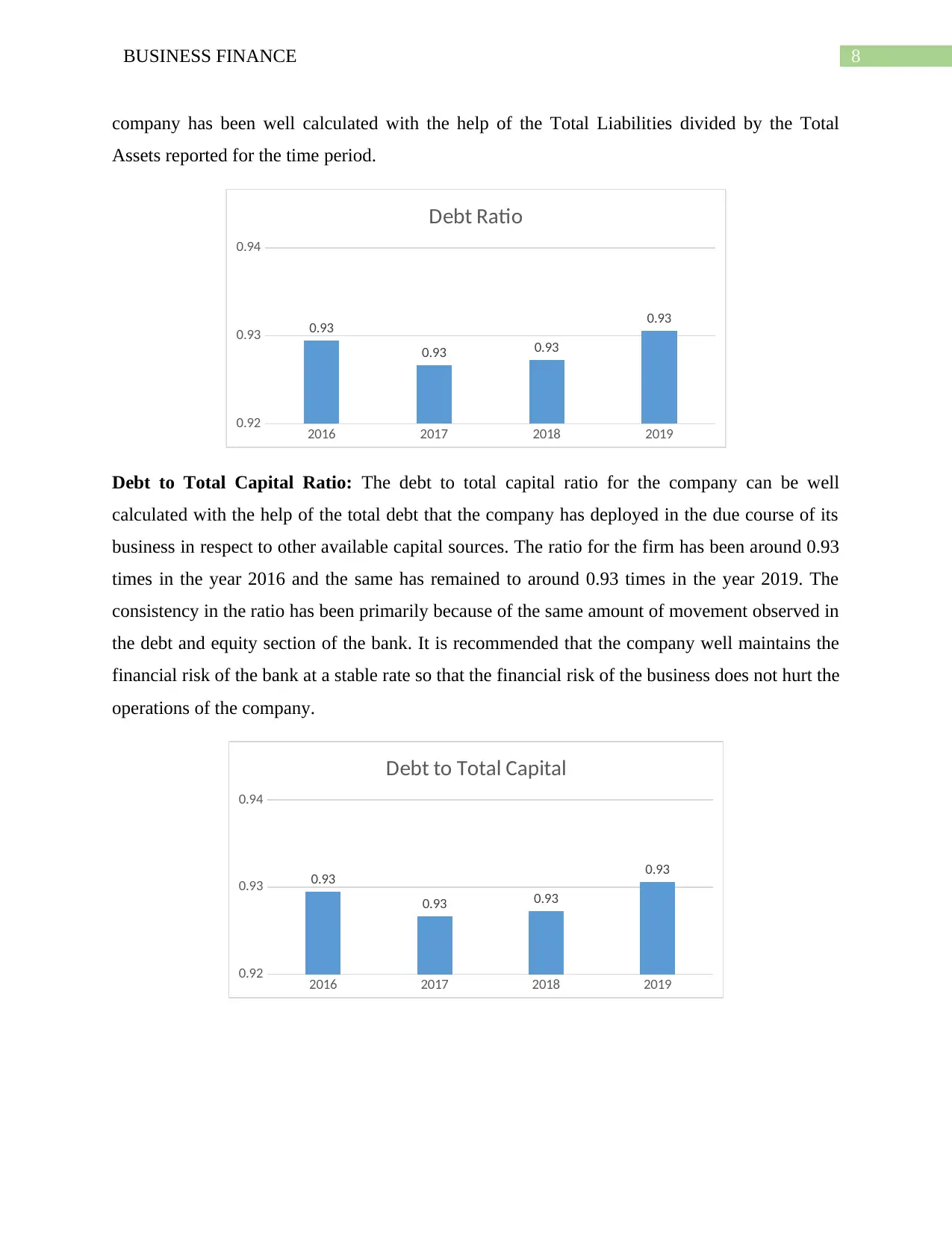

Ratio Analysis

Particulars 2016 2017 2018 2019

Capital Structure Ratio

Total Liabilities 47,266,000 47,870,000 49,124,000 51,738,000

Total Assets 50,853,000 51,658,000 52,980,000 55,597,000

Debt Ratio 0.93 0.93 0.93 0.93

Capital Structure Ratio

Debt 47,266,000 47,870,000 49,124,000 51,738,000

Total Capital 50,853,000 51,658,000 52,980,000 55,597,000

Debt to Total Capital 0.93 0.93 0.93 0.93

Liquidity Ratio

Current Asset-Inventory 2,887,000 2,809,000 2,603,000 7,130,000

Current Liabilities 5,063,000 9,154,000 9,728,000 11,637,000

Quick Ratio 0.57 0.31 0.27 0.61

Liquidity Ratio

Current Assets 2,887,000 2,809,000 2,603,000 7,130,000

Current Liabilities 5,063,000 9,154,000 9,728,000 11,637,000

Current Ratio 0.57 0.31 0.27 0.61

Debt Ratio: The debt ratio for the bank has been around 0.93 times in the year 2016 and the

same has been same across the time period analyzed to around 0.93 times in the year 2019. The

increase in the total liabilities of the company has been well in line with the increase in the total

asset base of the company which have well increased at the same time. It is important that the

company maintains an adequate level of debt in correspondence to the total assets of the

company so that the financial risk of the company stays at a stable rate. The debt ratio of the

observed in the financials of the company has been well noted down. The capital structure of the

company has been better analyzed with the help of the debt ratio and the debt to total capital ratio

which the company has well reported for the stated four year time period (Charles 2018).

Ratio Analysis

Particulars 2016 2017 2018 2019

Capital Structure Ratio

Total Liabilities 47,266,000 47,870,000 49,124,000 51,738,000

Total Assets 50,853,000 51,658,000 52,980,000 55,597,000

Debt Ratio 0.93 0.93 0.93 0.93

Capital Structure Ratio

Debt 47,266,000 47,870,000 49,124,000 51,738,000

Total Capital 50,853,000 51,658,000 52,980,000 55,597,000

Debt to Total Capital 0.93 0.93 0.93 0.93

Liquidity Ratio

Current Asset-Inventory 2,887,000 2,809,000 2,603,000 7,130,000

Current Liabilities 5,063,000 9,154,000 9,728,000 11,637,000

Quick Ratio 0.57 0.31 0.27 0.61

Liquidity Ratio

Current Assets 2,887,000 2,809,000 2,603,000 7,130,000

Current Liabilities 5,063,000 9,154,000 9,728,000 11,637,000

Current Ratio 0.57 0.31 0.27 0.61

Debt Ratio: The debt ratio for the bank has been around 0.93 times in the year 2016 and the

same has been same across the time period analyzed to around 0.93 times in the year 2019. The

increase in the total liabilities of the company has been well in line with the increase in the total

asset base of the company which have well increased at the same time. It is important that the

company maintains an adequate level of debt in correspondence to the total assets of the

company so that the financial risk of the company stays at a stable rate. The debt ratio of the

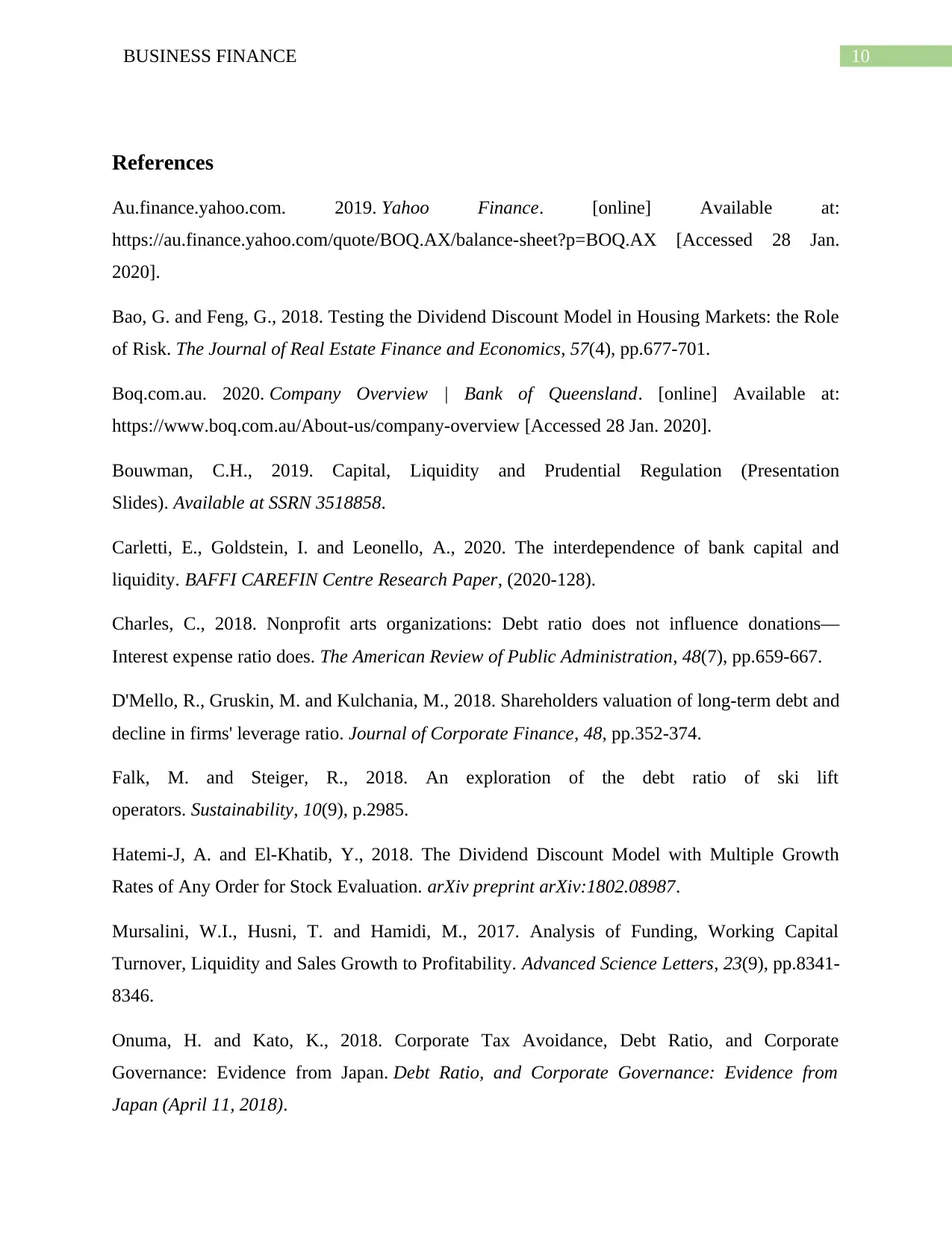

8BUSINESS FINANCE

company has been well calculated with the help of the Total Liabilities divided by the Total

Assets reported for the time period.

2016 2017 2018 2019

0.92

0.93

0.94

0.93

0.93 0.93

0.93

Debt Ratio

Debt to Total Capital Ratio: The debt to total capital ratio for the company can be well

calculated with the help of the total debt that the company has deployed in the due course of its

business in respect to other available capital sources. The ratio for the firm has been around 0.93

times in the year 2016 and the same has remained to around 0.93 times in the year 2019. The

consistency in the ratio has been primarily because of the same amount of movement observed in

the debt and equity section of the bank. It is recommended that the company well maintains the

financial risk of the bank at a stable rate so that the financial risk of the business does not hurt the

operations of the company.

2016 2017 2018 2019

0.92

0.93

0.94

0.93

0.93 0.93

0.93

Debt to Total Capital

company has been well calculated with the help of the Total Liabilities divided by the Total

Assets reported for the time period.

2016 2017 2018 2019

0.92

0.93

0.94

0.93

0.93 0.93

0.93

Debt Ratio

Debt to Total Capital Ratio: The debt to total capital ratio for the company can be well

calculated with the help of the total debt that the company has deployed in the due course of its

business in respect to other available capital sources. The ratio for the firm has been around 0.93

times in the year 2016 and the same has remained to around 0.93 times in the year 2019. The

consistency in the ratio has been primarily because of the same amount of movement observed in

the debt and equity section of the bank. It is recommended that the company well maintains the

financial risk of the bank at a stable rate so that the financial risk of the business does not hurt the

operations of the company.

2016 2017 2018 2019

0.92

0.93

0.94

0.93

0.93 0.93

0.93

Debt to Total Capital

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS FINANCE

Conclusion and Recommendations

The financial analysis of the company has been well done for a sum of four years

whereby important aspects of the company in the field of liquidity and capital structure of the

company has been analysed. The analysis well showed that the management of the bank should

take important steps for the purpose of well increasing the liquidity in the company. On the other

hand, the capital structure of the company also revealed that the effect or implication of debt in

the financials of the company has increased. The company should also undertake various aspects

of the risk management in account for the purpose of better analysis of the financial performance

and the financial position of the company.

Conclusion and Recommendations

The financial analysis of the company has been well done for a sum of four years

whereby important aspects of the company in the field of liquidity and capital structure of the

company has been analysed. The analysis well showed that the management of the bank should

take important steps for the purpose of well increasing the liquidity in the company. On the other

hand, the capital structure of the company also revealed that the effect or implication of debt in

the financials of the company has increased. The company should also undertake various aspects

of the risk management in account for the purpose of better analysis of the financial performance

and the financial position of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS FINANCE

References

Au.finance.yahoo.com. 2019. Yahoo Finance. [online] Available at:

https://au.finance.yahoo.com/quote/BOQ.AX/balance-sheet?p=BOQ.AX [Accessed 28 Jan.

2020].

Bao, G. and Feng, G., 2018. Testing the Dividend Discount Model in Housing Markets: the Role

of Risk. The Journal of Real Estate Finance and Economics, 57(4), pp.677-701.

Boq.com.au. 2020. Company Overview | Bank of Queensland. [online] Available at:

https://www.boq.com.au/About-us/company-overview [Accessed 28 Jan. 2020].

Bouwman, C.H., 2019. Capital, Liquidity and Prudential Regulation (Presentation

Slides). Available at SSRN 3518858.

Carletti, E., Goldstein, I. and Leonello, A., 2020. The interdependence of bank capital and

liquidity. BAFFI CAREFIN Centre Research Paper, (2020-128).

Charles, C., 2018. Nonprofit arts organizations: Debt ratio does not influence donations—

Interest expense ratio does. The American Review of Public Administration, 48(7), pp.659-667.

D'Mello, R., Gruskin, M. and Kulchania, M., 2018. Shareholders valuation of long-term debt and

decline in firms' leverage ratio. Journal of Corporate Finance, 48, pp.352-374.

Falk, M. and Steiger, R., 2018. An exploration of the debt ratio of ski lift

operators. Sustainability, 10(9), p.2985.

Hatemi-J, A. and El-Khatib, Y., 2018. The Dividend Discount Model with Multiple Growth

Rates of Any Order for Stock Evaluation. arXiv preprint arXiv:1802.08987.

Mursalini, W.I., Husni, T. and Hamidi, M., 2017. Analysis of Funding, Working Capital

Turnover, Liquidity and Sales Growth to Profitability. Advanced Science Letters, 23(9), pp.8341-

8346.

Onuma, H. and Kato, K., 2018. Corporate Tax Avoidance, Debt Ratio, and Corporate

Governance: Evidence from Japan. Debt Ratio, and Corporate Governance: Evidence from

Japan (April 11, 2018).

References

Au.finance.yahoo.com. 2019. Yahoo Finance. [online] Available at:

https://au.finance.yahoo.com/quote/BOQ.AX/balance-sheet?p=BOQ.AX [Accessed 28 Jan.

2020].

Bao, G. and Feng, G., 2018. Testing the Dividend Discount Model in Housing Markets: the Role

of Risk. The Journal of Real Estate Finance and Economics, 57(4), pp.677-701.

Boq.com.au. 2020. Company Overview | Bank of Queensland. [online] Available at:

https://www.boq.com.au/About-us/company-overview [Accessed 28 Jan. 2020].

Bouwman, C.H., 2019. Capital, Liquidity and Prudential Regulation (Presentation

Slides). Available at SSRN 3518858.

Carletti, E., Goldstein, I. and Leonello, A., 2020. The interdependence of bank capital and

liquidity. BAFFI CAREFIN Centre Research Paper, (2020-128).

Charles, C., 2018. Nonprofit arts organizations: Debt ratio does not influence donations—

Interest expense ratio does. The American Review of Public Administration, 48(7), pp.659-667.

D'Mello, R., Gruskin, M. and Kulchania, M., 2018. Shareholders valuation of long-term debt and

decline in firms' leverage ratio. Journal of Corporate Finance, 48, pp.352-374.

Falk, M. and Steiger, R., 2018. An exploration of the debt ratio of ski lift

operators. Sustainability, 10(9), p.2985.

Hatemi-J, A. and El-Khatib, Y., 2018. The Dividend Discount Model with Multiple Growth

Rates of Any Order for Stock Evaluation. arXiv preprint arXiv:1802.08987.

Mursalini, W.I., Husni, T. and Hamidi, M., 2017. Analysis of Funding, Working Capital

Turnover, Liquidity and Sales Growth to Profitability. Advanced Science Letters, 23(9), pp.8341-

8346.

Onuma, H. and Kato, K., 2018. Corporate Tax Avoidance, Debt Ratio, and Corporate

Governance: Evidence from Japan. Debt Ratio, and Corporate Governance: Evidence from

Japan (April 11, 2018).

11BUSINESS FINANCE

Rehman, A., Raza, Z., Rehman, H.U., Rehman, S.U. and Farooq, M., 2019. CAPITAL

STRUCTURE, LIQUIDITY AND FINANCIAL PERFORMANCE OF THE FIRMS IN

CEMENT AND SUGAR INDUSTRIES OF PAKISTAN. Journal Of Social Sciences &

Humanities, 3(1 & 2), pp.41-54.

Sim, T. and Wright, R., 2017. Stock valuation using the dividend discount model: An internal

rate of return Approach. Research in Finance, 33, pp.19-32.

Rehman, A., Raza, Z., Rehman, H.U., Rehman, S.U. and Farooq, M., 2019. CAPITAL

STRUCTURE, LIQUIDITY AND FINANCIAL PERFORMANCE OF THE FIRMS IN

CEMENT AND SUGAR INDUSTRIES OF PAKISTAN. Journal Of Social Sciences &

Humanities, 3(1 & 2), pp.41-54.

Sim, T. and Wright, R., 2017. Stock valuation using the dividend discount model: An internal

rate of return Approach. Research in Finance, 33, pp.19-32.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.