Audit Strategy Report for Bank of Queensland (BBAC601) - 2017-2018

VerifiedAdded on 2023/01/19

|16

|3613

|51

Report

AI Summary

This report presents an audit strategy for the Bank of Queensland (BOQ), focusing on the 2017-2018 financial year. It begins with an overview of the client, including its industry, regulatory environment, and nature as an Australian retail bank operating in banking and insurance segments. The report then delves into BOQ's accounting policies, covering areas such as plant, property, and equipment, inventory, accounts receivable, financial instruments, intangible assets, and revenue recognition. Additionally, it examines related party transactions. Part B of the report analyzes the client, discussing changes in accounting policies, preliminary analytical procedures, financial performance, objectives, strategies, and related business risks, concluding with an overall assessment. The report aims to assist newly appointed auditors in developing an effective audit strategy, referencing the annual report for the year ending 2018 and relevant auditing standards.

Running head: AUDITING & ASSURANCE

AUDITING & ASSURANCE

Name of the Student:

FAIZAN KHAN (S70396)

ATISH (S64756)

DANIAL (S62323)

HARIS ALI KHAN (S67251)

Name of the University:

Author Note

AUDITING & ASSURANCE

Name of the Student:

FAIZAN KHAN (S70396)

ATISH (S64756)

DANIAL (S62323)

HARIS ALI KHAN (S67251)

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING & ASSURANCE

Table of Contents

Part A: The Client......................................................................................................................3

Information about the client.......................................................................................................3

Industry, Regulatory and Other external factor..........................................................................3

Nature of the entity.....................................................................................................................5

Accounting Policy......................................................................................................................6

Policies w.r.t. Plant, property and Equipment........................................................................6

Policies w.r.t. Inventory.........................................................................................................6

Policies w.r.t. account receivables.........................................................................................6

Policies w.r.t. financial instruments.......................................................................................6

Policies w.r.t. intangible assets..............................................................................................6

Policies w.r.t. revenue recognition.........................................................................................6

Related Party and transactions with the related parties..............................................................7

Controlled entities..................................................................................................................7

Non-Controlled entities..............................................................................................................8

Other Related parties include the following...........................................................................8

Part B: Analysis of the client and impacts on the future audit work..........................................9

Changes in accounting policies and the impact of changes...................................................9

Preliminary analytical procedures........................................................................................10

Measurement and review of financial performance.................................................................11

Objectives, strategies and related business risks......................................................................11

Related business risks..............................................................................................................12

Table of Contents

Part A: The Client......................................................................................................................3

Information about the client.......................................................................................................3

Industry, Regulatory and Other external factor..........................................................................3

Nature of the entity.....................................................................................................................5

Accounting Policy......................................................................................................................6

Policies w.r.t. Plant, property and Equipment........................................................................6

Policies w.r.t. Inventory.........................................................................................................6

Policies w.r.t. account receivables.........................................................................................6

Policies w.r.t. financial instruments.......................................................................................6

Policies w.r.t. intangible assets..............................................................................................6

Policies w.r.t. revenue recognition.........................................................................................6

Related Party and transactions with the related parties..............................................................7

Controlled entities..................................................................................................................7

Non-Controlled entities..............................................................................................................8

Other Related parties include the following...........................................................................8

Part B: Analysis of the client and impacts on the future audit work..........................................9

Changes in accounting policies and the impact of changes...................................................9

Preliminary analytical procedures........................................................................................10

Measurement and review of financial performance.................................................................11

Objectives, strategies and related business risks......................................................................11

Related business risks..............................................................................................................12

2AUDITING & ASSURANCE

Conclusion................................................................................................................................12

Reference..................................................................................................................................14

Conclusion................................................................................................................................12

Reference..................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING & ASSURANCE

Part A: The Client

Information about the client

In the given case, our chosen client is the Bank of Queensland limited, which is listed

with the Australian Stock exchange. Along with that engaged in providing various financial

products and services in Australia together with its subsidiaries. It was established in the year

1874 as an Australian retail Bank. It is working in two different segments of Banking and

Insurance. The investment services of the Bank includes private banking, account and card

switching services. Our report is intended to assist the newly appointed auditor of the Bank in

the process of developing an Audit Strategy (Alieid 2016). In order to assist this purpose we

have taken the Annual report of the bank for the year ending 2018, which includes the

consolidated statement of financial position and financial performance, statement of changes

in equity and the cash Flow statement for the same period.

Industry, Regulatory and Other external factor

As it is quite clear from the message given by the Chairman, Managing, Director and

CEO of the bank in the Annual report for the Financial year ending 2018 that the year proved

to be a turmoil for the Banking Industry. Further, ids the reason why their focus was on the

implementation of such a strategy which can ensure them to remain fundamentally strong

(Alexander 2016).

The year 2018 had evidenced the strong scrutiny for the Banking sector. There were a

lot reports showing the fact that the industry failed to meet the expectation of its various

stakeholders in the same year. Few of those reports are royal commission’s report. Few of

these reports reflected the poorly performance of the industry as a result of which the

reputation of the few of the major Banks in the Industry had to lose their reputation too along

with the facing of significant inquiry into their operation (Arnott, et al 2017).

Part A: The Client

Information about the client

In the given case, our chosen client is the Bank of Queensland limited, which is listed

with the Australian Stock exchange. Along with that engaged in providing various financial

products and services in Australia together with its subsidiaries. It was established in the year

1874 as an Australian retail Bank. It is working in two different segments of Banking and

Insurance. The investment services of the Bank includes private banking, account and card

switching services. Our report is intended to assist the newly appointed auditor of the Bank in

the process of developing an Audit Strategy (Alieid 2016). In order to assist this purpose we

have taken the Annual report of the bank for the year ending 2018, which includes the

consolidated statement of financial position and financial performance, statement of changes

in equity and the cash Flow statement for the same period.

Industry, Regulatory and Other external factor

As it is quite clear from the message given by the Chairman, Managing, Director and

CEO of the bank in the Annual report for the Financial year ending 2018 that the year proved

to be a turmoil for the Banking Industry. Further, ids the reason why their focus was on the

implementation of such a strategy which can ensure them to remain fundamentally strong

(Alexander 2016).

The year 2018 had evidenced the strong scrutiny for the Banking sector. There were a

lot reports showing the fact that the industry failed to meet the expectation of its various

stakeholders in the same year. Few of those reports are royal commission’s report. Few of

these reports reflected the poorly performance of the industry as a result of which the

reputation of the few of the major Banks in the Industry had to lose their reputation too along

with the facing of significant inquiry into their operation (Arnott, et al 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING & ASSURANCE

.

It further states the fact that the operational environment of the industry too has

become quite challenging due to the major contributing actors like Slow credit growth,

regulatory change, high funding costs etc.

The major regulations, which are subject to the Corporation Act,2001, Royal

commission’s charter w.r.t. banking and financial services system, corporate governance

principles governed by ASX’s corporate governance council’s along with the IFRS and

Australian Auditing standards in relation to the preparation of Financial statement. Further,

treasury law amendment Bill 2017 also passed to ensure its applicability from July 1, 2018.

Similarly, the new banking code of practice got the affirmation from the ASIC (Goldman

2016).

Similarly, the regulation related to the consumer data rights is also in the process to

become effective as legislation.

In the recent times, Westpac Banking Corporation has emerged as one of the major

competitors as it has brought down the profit of the BOQ that was well reflected through its

surprisingly announced quarterly profit. The major competition it is facing due to its poorly

managed structure of retail banking and the lack of an effective Banking strategy to gain the

trust of the community.

The major competitors are St George bank Limited, National Australia bank Limited,

ANZ banking group limited, Commonwealth bank of Australia and Bank of Western

Australia Limited (Choy, 2018).

The products offered by the BOQ have very few market substitutes. Further, those

competitors providing the substitutes belong to the low profit earning industry. Again, these

.

It further states the fact that the operational environment of the industry too has

become quite challenging due to the major contributing actors like Slow credit growth,

regulatory change, high funding costs etc.

The major regulations, which are subject to the Corporation Act,2001, Royal

commission’s charter w.r.t. banking and financial services system, corporate governance

principles governed by ASX’s corporate governance council’s along with the IFRS and

Australian Auditing standards in relation to the preparation of Financial statement. Further,

treasury law amendment Bill 2017 also passed to ensure its applicability from July 1, 2018.

Similarly, the new banking code of practice got the affirmation from the ASIC (Goldman

2016).

Similarly, the regulation related to the consumer data rights is also in the process to

become effective as legislation.

In the recent times, Westpac Banking Corporation has emerged as one of the major

competitors as it has brought down the profit of the BOQ that was well reflected through its

surprisingly announced quarterly profit. The major competition it is facing due to its poorly

managed structure of retail banking and the lack of an effective Banking strategy to gain the

trust of the community.

The major competitors are St George bank Limited, National Australia bank Limited,

ANZ banking group limited, Commonwealth bank of Australia and Bank of Western

Australia Limited (Choy, 2018).

The products offered by the BOQ have very few market substitutes. Further, those

competitors providing the substitutes belong to the low profit earning industry. Again, these

5AUDITING & ASSURANCE

substitutes are of high quality with the nature of being too expensive, but the products offered

by the BOQ are relatively of lower value with the adequate quality.

Therefore, far as the threats to new entrants are concerned it seems quite weaker as

economies of scale in these industry ids difficult to achieve. Similarly, one more factor like

product differentiation in the industry in addition to the higher capital requirements too has

made it difficult to think about the new entrants. The strict government policies along with

the licensing regulations too have made it quite difficult for the new entry.

Nature of the entity

BOQ is primarily Woking in the area of Banking and Insurance Business identified as

two distinct business segments .It has more than 180 branches in Australia. The local owner

managers manage most of its branches. Its products and services are not only offered to the

individuals but to the business groups too. The bank is primarily targeting two categories of

the customers, the first being the retail customers and second being the small and medium

size enterprises (Fukukawa and Mock 2011).

In terms of personal Banking services, it providing the offerings in form of savings

and investment accounts, term deposits and day to day banking services, whereas in the field

of insurance it is offering the commercial, life and credit protection Insurance.

The Board of BOQ consists of ten directors out of which nine directors are having the

status of Non-Executive director and only one executive director. It has the other committees

like Remuneration committee and audit committees too in existence.

substitutes are of high quality with the nature of being too expensive, but the products offered

by the BOQ are relatively of lower value with the adequate quality.

Therefore, far as the threats to new entrants are concerned it seems quite weaker as

economies of scale in these industry ids difficult to achieve. Similarly, one more factor like

product differentiation in the industry in addition to the higher capital requirements too has

made it difficult to think about the new entrants. The strict government policies along with

the licensing regulations too have made it quite difficult for the new entry.

Nature of the entity

BOQ is primarily Woking in the area of Banking and Insurance Business identified as

two distinct business segments .It has more than 180 branches in Australia. The local owner

managers manage most of its branches. Its products and services are not only offered to the

individuals but to the business groups too. The bank is primarily targeting two categories of

the customers, the first being the retail customers and second being the small and medium

size enterprises (Fukukawa and Mock 2011).

In terms of personal Banking services, it providing the offerings in form of savings

and investment accounts, term deposits and day to day banking services, whereas in the field

of insurance it is offering the commercial, life and credit protection Insurance.

The Board of BOQ consists of ten directors out of which nine directors are having the

status of Non-Executive director and only one executive director. It has the other committees

like Remuneration committee and audit committees too in existence.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING & ASSURANCE

Accounting Policy

Policies w.r.t. Plant, property and Equipment

It has been mentioned in the notes and disclosures to the financial statement that the

plant, property and equipment has been recognized at original cost less accumulated

depreciation and accumulated impairment losses, if any. The cost of the self-constructed

assets include direct labour, materials and appropriate portion of the overheads (Werner

2017).

Policies w.r.t. Inventory

The inventory has been stated on perpetual system of accounting.

Policies w.r.t. account receivables

The Accounts receivables has been stated as total accounts receivables less provisions

and the amount is showing inclusive of the Goods and service tax.

Policies w.r.t. financial instruments

Financial assets and liabilities as provided below have been recognized at fair value

and their carrying value represents the fair value only. These are as follows:

Derivatives

Assets available for sale

Financial assets and liabilities designated at fair value through Profit and Loss

Policies w.r.t. intangible assets

Intangible assets have been recognised at cost less any accumulated amortisation and

any impairment losses. The income statement reflects separately the expenses incurred on

internally generated goodwill, brand and research costs (Jefferson 2017).

Accounting Policy

Policies w.r.t. Plant, property and Equipment

It has been mentioned in the notes and disclosures to the financial statement that the

plant, property and equipment has been recognized at original cost less accumulated

depreciation and accumulated impairment losses, if any. The cost of the self-constructed

assets include direct labour, materials and appropriate portion of the overheads (Werner

2017).

Policies w.r.t. Inventory

The inventory has been stated on perpetual system of accounting.

Policies w.r.t. account receivables

The Accounts receivables has been stated as total accounts receivables less provisions

and the amount is showing inclusive of the Goods and service tax.

Policies w.r.t. financial instruments

Financial assets and liabilities as provided below have been recognized at fair value

and their carrying value represents the fair value only. These are as follows:

Derivatives

Assets available for sale

Financial assets and liabilities designated at fair value through Profit and Loss

Policies w.r.t. intangible assets

Intangible assets have been recognised at cost less any accumulated amortisation and

any impairment losses. The income statement reflects separately the expenses incurred on

internally generated goodwill, brand and research costs (Jefferson 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING & ASSURANCE

Policies w.r.t. revenue recognition

Premium of the life insurance contract is recognised as revenue since the date of

attachment of risk. If there is premium with no due date then it is recognised on cash basis.

The premium with regular due dates are recognised on accrual basis. As per the policy of the

company, unpaid premiums are shown as revenue in the books when they are being secured

by the surrender value of the policy or during the grace period.

Investment incomes recognised on accrual basis.

Related Party and transactions with the related parties

Controlled Entities

In the course of given financial year there were multiple transactions between the

bank and its controlled entities. Further, it was also established that the Bank has gone into

several business operations and transaction with its operating controlled entities. The amount

given and taken from the controlled entities have generally been charged at normal rates other

than the B.Q.L Management Pty Ltd. B.O.Q Specialist Pty Ltd, BOQ Shares Plan Nominee

Pty Ltd, BOQ Home Pty Limited and few of the dormant entities (Heminway 2017).

The Bank has received the management fees from its operating control entities except

BOQ Home Pty Limited, BOQ Shares Plan Nominee Pty Ltd and few of the dormant entities.

The Bank had a related party relationship with equity accounted joint ventures.

Controlled entities

interest Amount of investment Principal activities

Controlled entities: 2018

%

2017

%

2018

$m

2017

$m

Series 2010-1

REDS Trust

Australia 100% 100% - - Securitisation

Series 2010-2

REDS Trust

Australia 100% 100% - - Securitisation

Series 2012-1E

REDS Trust

Australia 100% 100% - - Securitisation

Series 2013-1

REDS Trust

Australia 100% 100% - - Securitisation

Series 2014-1

EHP REDS

Australia - 100% - - Securitisation

Policies w.r.t. revenue recognition

Premium of the life insurance contract is recognised as revenue since the date of

attachment of risk. If there is premium with no due date then it is recognised on cash basis.

The premium with regular due dates are recognised on accrual basis. As per the policy of the

company, unpaid premiums are shown as revenue in the books when they are being secured

by the surrender value of the policy or during the grace period.

Investment incomes recognised on accrual basis.

Related Party and transactions with the related parties

Controlled Entities

In the course of given financial year there were multiple transactions between the

bank and its controlled entities. Further, it was also established that the Bank has gone into

several business operations and transaction with its operating controlled entities. The amount

given and taken from the controlled entities have generally been charged at normal rates other

than the B.Q.L Management Pty Ltd. B.O.Q Specialist Pty Ltd, BOQ Shares Plan Nominee

Pty Ltd, BOQ Home Pty Limited and few of the dormant entities (Heminway 2017).

The Bank has received the management fees from its operating control entities except

BOQ Home Pty Limited, BOQ Shares Plan Nominee Pty Ltd and few of the dormant entities.

The Bank had a related party relationship with equity accounted joint ventures.

Controlled entities

interest Amount of investment Principal activities

Controlled entities: 2018

%

2017

%

2018

$m

2017

$m

Series 2010-1

REDS Trust

Australia 100% 100% - - Securitisation

Series 2010-2

REDS Trust

Australia 100% 100% - - Securitisation

Series 2012-1E

REDS Trust

Australia 100% 100% - - Securitisation

Series 2013-1

REDS Trust

Australia 100% 100% - - Securitisation

Series 2014-1

EHP REDS

Australia - 100% - - Securitisation

8AUDITING & ASSURANCE

Trust

Series 2015-1

REDS Trust

Australia 100% 100% - - Securitisation

Series 2015-1

EHP REDS

Trust

Australia 100% 100% - - Securitisation

Series 2017-1

REDS Trust

Australia 100% 100% - - Securitisation

Series 2018-1

REDS Trust

Australia 100% - - - Securitisation

St Andrew’s

Australia

Services Pty

Ltd

Australia 100% 100% - - Insurance

St Andrew’s

Insurance

(Australia) Pty

Ltd

Australia 100% 100% - - General

insurance

St Andrew’s

Life Insurance

Pty Ltd

Australia 100% 100% - - Life insurance

Statewest

Financial

Planning Pty

Ltd

Australia 100% 100% - - Dormant

Statewest

Financial

Services Pty

Ltd

Australia - 100% - - Dormant

Virgin Money

(Australia) Pty

Limited

Australia 100% 100% 53 53 Financial

services

Virgin Money

Financial

Services Pty

Ltd

Australia 100% 100% - - Financial

services

Virgin Money Home Loans Pty Limited

Non-Controlled entities

There is no such transaction, which took place between the non-controlled entities and

the Bank.

Other Related parties include the following

Some of the other financial instrument transactions with key management personnel (KMPs)

and related parties are shown below.

Term Products

(Loans and

advances)

Total drawdowns/

(Repayments)

$

Total Loan/ OD

interest

$

Total Fees On

Loans / OD

$

KMP 2004249 140768 600

Other related parties (84727) 57711 240

Total 1919522 198479 840

Trust

Series 2015-1

REDS Trust

Australia 100% 100% - - Securitisation

Series 2015-1

EHP REDS

Trust

Australia 100% 100% - - Securitisation

Series 2017-1

REDS Trust

Australia 100% 100% - - Securitisation

Series 2018-1

REDS Trust

Australia 100% - - - Securitisation

St Andrew’s

Australia

Services Pty

Ltd

Australia 100% 100% - - Insurance

St Andrew’s

Insurance

(Australia) Pty

Ltd

Australia 100% 100% - - General

insurance

St Andrew’s

Life Insurance

Pty Ltd

Australia 100% 100% - - Life insurance

Statewest

Financial

Planning Pty

Ltd

Australia 100% 100% - - Dormant

Statewest

Financial

Services Pty

Ltd

Australia - 100% - - Dormant

Virgin Money

(Australia) Pty

Limited

Australia 100% 100% 53 53 Financial

services

Virgin Money

Financial

Services Pty

Ltd

Australia 100% 100% - - Financial

services

Virgin Money Home Loans Pty Limited

Non-Controlled entities

There is no such transaction, which took place between the non-controlled entities and

the Bank.

Other Related parties include the following

Some of the other financial instrument transactions with key management personnel (KMPs)

and related parties are shown below.

Term Products

(Loans and

advances)

Total drawdowns/

(Repayments)

$

Total Loan/ OD

interest

$

Total Fees On

Loans / OD

$

KMP 2004249 140768 600

Other related parties (84727) 57711 240

Total 1919522 198479 840

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING & ASSURANCE

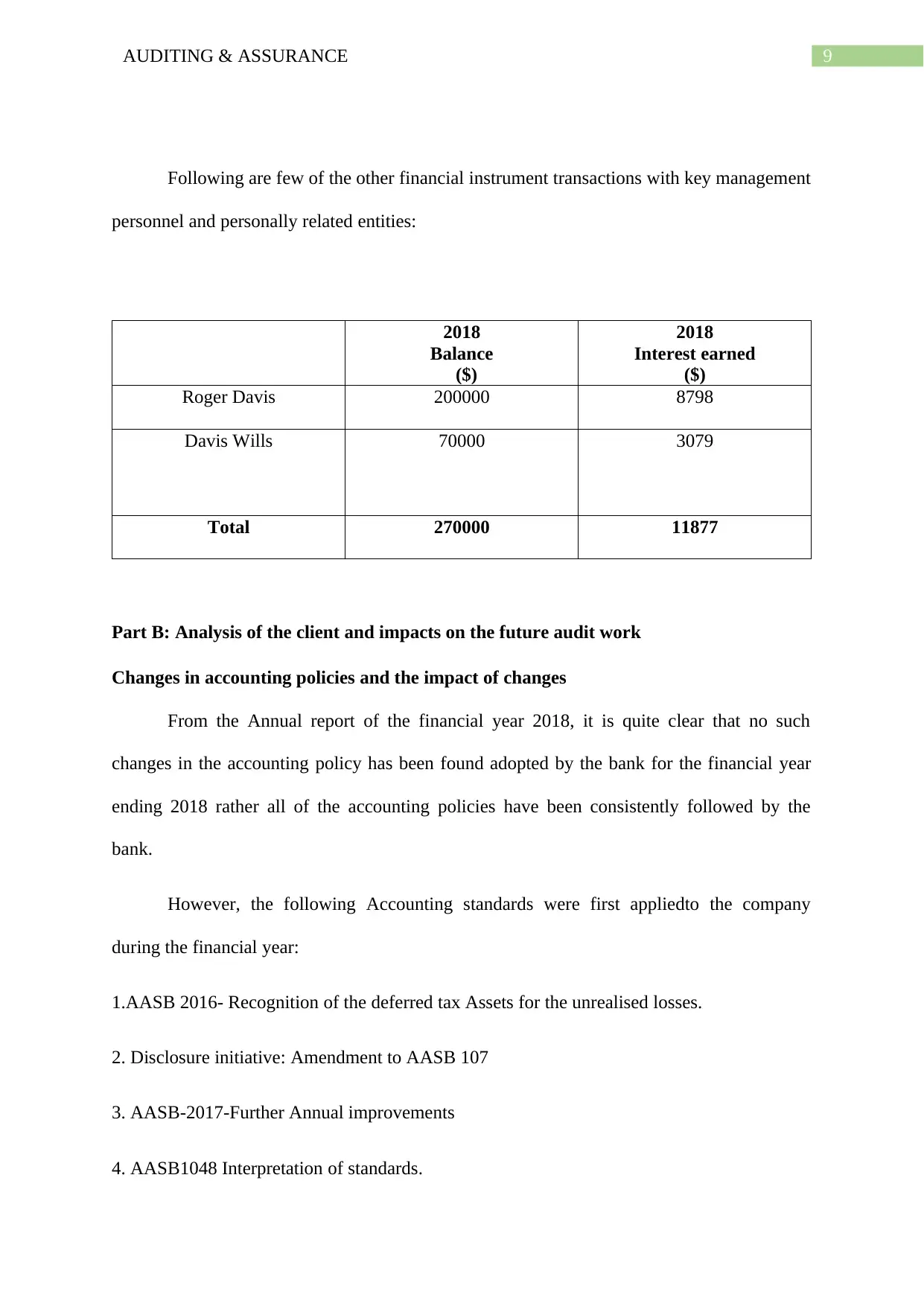

Following are few of the other financial instrument transactions with key management

personnel and personally related entities:

2018

Balance

($)

2018

Interest earned

($)

Roger Davis 200000 8798

Davis Wills 70000 3079

Total 270000 11877

Part B: Analysis of the client and impacts on the future audit work

Changes in accounting policies and the impact of changes

From the Annual report of the financial year 2018, it is quite clear that no such

changes in the accounting policy has been found adopted by the bank for the financial year

ending 2018 rather all of the accounting policies have been consistently followed by the

bank.

However, the following Accounting standards were first appliedto the company

during the financial year:

1.AASB 2016- Recognition of the deferred tax Assets for the unrealised losses.

2. Disclosure initiative: Amendment to AASB 107

3. AASB-2017-Further Annual improvements

4. AASB1048 Interpretation of standards.

Following are few of the other financial instrument transactions with key management

personnel and personally related entities:

2018

Balance

($)

2018

Interest earned

($)

Roger Davis 200000 8798

Davis Wills 70000 3079

Total 270000 11877

Part B: Analysis of the client and impacts on the future audit work

Changes in accounting policies and the impact of changes

From the Annual report of the financial year 2018, it is quite clear that no such

changes in the accounting policy has been found adopted by the bank for the financial year

ending 2018 rather all of the accounting policies have been consistently followed by the

bank.

However, the following Accounting standards were first appliedto the company

during the financial year:

1.AASB 2016- Recognition of the deferred tax Assets for the unrealised losses.

2. Disclosure initiative: Amendment to AASB 107

3. AASB-2017-Further Annual improvements

4. AASB1048 Interpretation of standards.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING & ASSURANCE

The major Accounting standards which are expected to significantly impact the future

financial years are:

1. AASB 9 This is going to change the measurement of the financial assets and

liabilities. This shall mandatorily be applicable from the September 1, 2018and it will

be replacing AASB 139, which was followed earlier.

2. The group has applied expected credit loss method, which replaced the previously

followed incurred loss approach.

3. AASB 15 Revenue from contracts with customers advocates the single model gives a

more comprehensive model for revenue recognition for contracts with customers and

replaces the AASB 18 and AASB111.

4. AASB 16 replaces AASB117 on accounting for lessees, which will result in lessee

recognising the right to use the asset and the corresponding lease liability in the

books.

5. An AASB 17insurance contract replaces AASB 4. As per the new model the

insurance liabilities shall represent the present value of future cash flows and include

the provision for the risk (Kangarluie and Aalizadeh 2017).

Preliminary analytical procedures

2018 2017

1. Current Ratio= Current Assets/ =6549/1040 =4906/1047

Current Liabilities =6.30 =4.69

2. Quick Assets ratio= Quick Assets/ Current liabilities=6543/1040

=4848/1047

=6.29 =4.63

3. Debt to equity Ratio=Long -term Debt/ Equity= 48388/3856=47153/3788

=12.55 =12.45

4. Net profit ratio= Net Profit/ Net Revenue =336/1121 =352/1103

=29.97% =31.91%

5. Return on Capital Employed=

6. EBDIT/Capital Employed= 1121/52244 =1103/50941

The major Accounting standards which are expected to significantly impact the future

financial years are:

1. AASB 9 This is going to change the measurement of the financial assets and

liabilities. This shall mandatorily be applicable from the September 1, 2018and it will

be replacing AASB 139, which was followed earlier.

2. The group has applied expected credit loss method, which replaced the previously

followed incurred loss approach.

3. AASB 15 Revenue from contracts with customers advocates the single model gives a

more comprehensive model for revenue recognition for contracts with customers and

replaces the AASB 18 and AASB111.

4. AASB 16 replaces AASB117 on accounting for lessees, which will result in lessee

recognising the right to use the asset and the corresponding lease liability in the

books.

5. An AASB 17insurance contract replaces AASB 4. As per the new model the

insurance liabilities shall represent the present value of future cash flows and include

the provision for the risk (Kangarluie and Aalizadeh 2017).

Preliminary analytical procedures

2018 2017

1. Current Ratio= Current Assets/ =6549/1040 =4906/1047

Current Liabilities =6.30 =4.69

2. Quick Assets ratio= Quick Assets/ Current liabilities=6543/1040

=4848/1047

=6.29 =4.63

3. Debt to equity Ratio=Long -term Debt/ Equity= 48388/3856=47153/3788

=12.55 =12.45

4. Net profit ratio= Net Profit/ Net Revenue =336/1121 =352/1103

=29.97% =31.91%

5. Return on Capital Employed=

6. EBDIT/Capital Employed= 1121/52244 =1103/50941

11AUDITING & ASSURANCE

=2.15% =2.17%

From the above calculation it is quite clear that the short term financial position of the

BOQ group seems to be much better which is being reflected from its current and quick ratio.

But in terms of its solvency ratio, the scenario seems to be quite dangerous as it is

overburdened with the debt in both of the financial year. Hence, it shall be a primary

responsibility of the Auditor to give a check that aforesaid liability is duly met or the bank

has the sufficient capacity to honour such debt when it is due (Belton 2017).

In terms of profitability ratio, the net profit margin reflects the quite better financial

position, though the return on capital employed it could not reflect the better financial

position or profitability ratio.

Measurement and review of financial performance

In terms of financial performance, this report analyse the following two information

of the company:

1. Remuneration report: - By analysing the remuneration report of the company it

can observed that the company provided the appropriate numeration to its directs

and other executive level officers. The company also considers all the related

standards while preparing the remuneration report for the company.

2. Contracts with the customers: - Same like the remuneration report, the company

also satisfies all the requirement of the related standards and the principles while

performing the contract with its customer as well as with the stakeholders of the

company.

Objectives, strategies and related business risks

The basic strategies of the BOQ are explained hereunder:

1. Customer In charge

=2.15% =2.17%

From the above calculation it is quite clear that the short term financial position of the

BOQ group seems to be much better which is being reflected from its current and quick ratio.

But in terms of its solvency ratio, the scenario seems to be quite dangerous as it is

overburdened with the debt in both of the financial year. Hence, it shall be a primary

responsibility of the Auditor to give a check that aforesaid liability is duly met or the bank

has the sufficient capacity to honour such debt when it is due (Belton 2017).

In terms of profitability ratio, the net profit margin reflects the quite better financial

position, though the return on capital employed it could not reflect the better financial

position or profitability ratio.

Measurement and review of financial performance

In terms of financial performance, this report analyse the following two information

of the company:

1. Remuneration report: - By analysing the remuneration report of the company it

can observed that the company provided the appropriate numeration to its directs

and other executive level officers. The company also considers all the related

standards while preparing the remuneration report for the company.

2. Contracts with the customers: - Same like the remuneration report, the company

also satisfies all the requirement of the related standards and the principles while

performing the contract with its customer as well as with the stakeholders of the

company.

Objectives, strategies and related business risks

The basic strategies of the BOQ are explained hereunder:

1. Customer In charge

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.