ACC2208 Accounting Practices Assignment 3: Cash Management Solutions

VerifiedAdded on 2022/09/06

|2

|272

|20

Practical Assignment

AI Summary

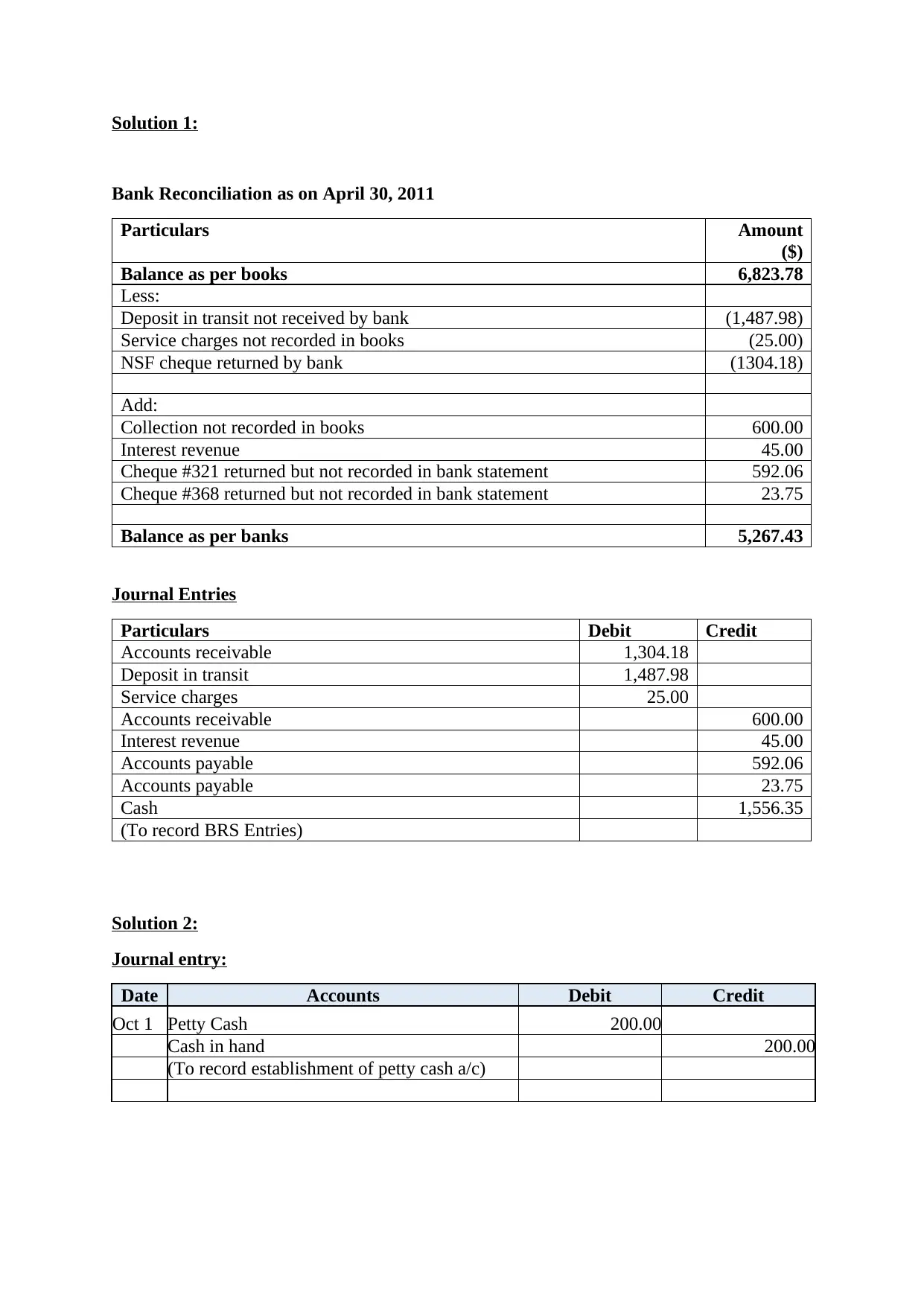

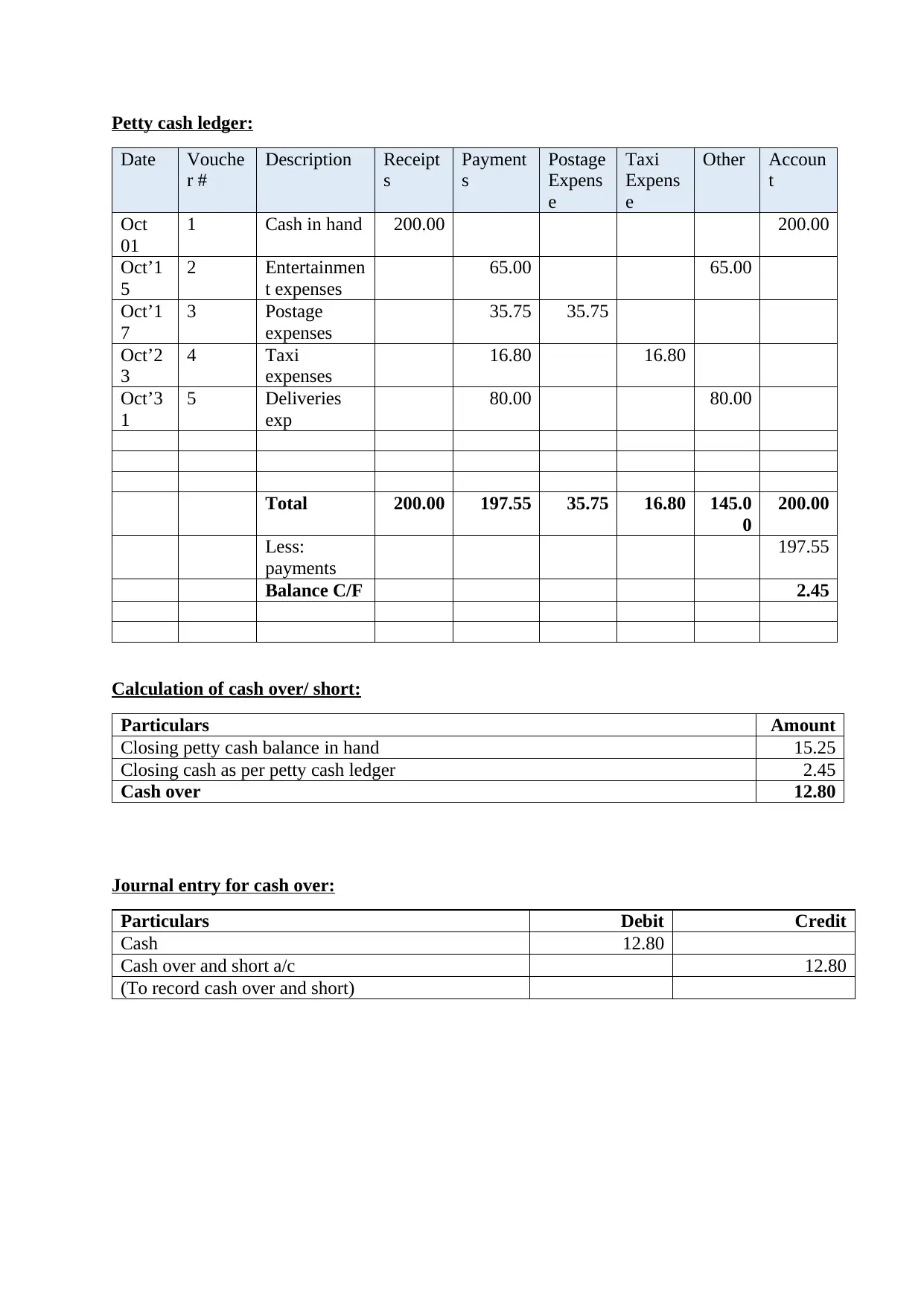

This document presents solutions for ACC2208 Accounting Practices Assignment 3, focusing on practical cash management skills. The assignment requires students to prepare a bank reconciliation statement, reconcile the company's cash account with the bank statement, and set up and manage a petty cash account by recording daily transactions. The solution provides a detailed bank reconciliation as of April 30, 2011, including adjustments for deposits in transit, service charges, NSF checks, and unrecorded collections and interest revenue. It also includes all necessary journal entries. Furthermore, the document provides a petty cash ledger, journal entries for establishing and managing the petty cash account, and the calculation of cash over or short, along with the relevant journal entries. The document is designed to help students understand and apply key accounting principles related to cash management within the context of an office administrative assistant role.

1 out of 2

![Bank Reconciliation and Petty Cash Analysis Report - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fqr%2F12003066b4c34975be8e8016d157389c.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.