Financial Accounting A2 Report: Bank Reconciliation Statement

VerifiedAdded on 2021/06/07

|20

|3906

|101

Report

AI Summary

This report, prepared for a Financial Accounting A2 assignment, focuses on the bank reconciliation statement for An Binh Ltd. It begins with an introduction to bank reconciliation, explaining its purpose and necessity in ensuring the accuracy of financial records. The report details the steps involved in preparing a bank reconciliation statement, including comparing bank statements and cash books to identify discrepancies. It then presents a case study using the bank statement and cash book of An Binh Ltd. to demonstrate the reconciliation process. Furthermore, the report addresses the reconciliation of control accounts, the identification of accounting errors, and the use of suspense accounts to correct these errors. It includes journal entries to correct the errors and a statement showing the adjusted net profit after correcting the errors, concluding with a discussion of how the errors have influenced the profit. The report uses the provided source documents to illustrate the concepts and calculations involved.

Financial Accounting

A2: Bank Reconciliation Statement for An Binh Ltd.

Lecture’s name: Nguyen Thi Tuong Tam

Student’s name: Huynh Quang Long

Student’s ID: B180049

Class: B1902.

Number of pages: 19 pages

1

A2: Bank Reconciliation Statement for An Binh Ltd.

Lecture’s name: Nguyen Thi Tuong Tam

Student’s name: Huynh Quang Long

Student’s ID: B180049

Class: B1902.

Number of pages: 19 pages

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION:....................................................................................................................3

LO3 Perform bank reconciliations to ensure company and bank records are correct:..............4

1.Concepts of Bank Reconciliation Statement:......................................................................4

2.Necessity of Bank Reconciliation Statement:.....................................................................4

3.Steps of prearing Bank Reconciliation Statement :.............................................................4

4. Bank Reconciliation Statement format:.............................................................................5

5. Source document:...............................................................................................................5

1.Compare the records in both the Bank statements and the Cash Book (bank column

only). Identify factors that have caused a variation in the balances :................................7

2.Prepare the bank reconciliation statement:.....................................................................9

LO4 Reconcile control accounts and shift recorded transactions from the suspense accounts

to the right accounts.................................................................................................................10

1.Concepts of errors in accounting:.....................................................................................10

2.Types of errors in accounting:...........................................................................................10

3.Concepts of suspens accounting:......................................................................................11

4. Source document:.............................................................................................................12

1.Re-prepare the extracted trial balance above accurately with the given information.

The only amended amount is the suspense's one:............................................................13

2. Show the journal entries to correct the errors:.............................................................14

3. Drawn up the suspense account for the difference between the trial balance totals and

show the correction to be made. Narratives are not required:..........................................16

4. Draw up a statement showing the adjusted net profit after correcting the above errors;

assumed that net profit had previously been calculated at £1,200 for the semi-annum

period ended on 30 June 20X9. Determine which errors have influenced to

profit( impact to sales and expenses)...............................................................................16

CONCLUSION:.......................................................................................................................18

Bibliography.............................................................................................................................19

2

INTRODUCTION:....................................................................................................................3

LO3 Perform bank reconciliations to ensure company and bank records are correct:..............4

1.Concepts of Bank Reconciliation Statement:......................................................................4

2.Necessity of Bank Reconciliation Statement:.....................................................................4

3.Steps of prearing Bank Reconciliation Statement :.............................................................4

4. Bank Reconciliation Statement format:.............................................................................5

5. Source document:...............................................................................................................5

1.Compare the records in both the Bank statements and the Cash Book (bank column

only). Identify factors that have caused a variation in the balances :................................7

2.Prepare the bank reconciliation statement:.....................................................................9

LO4 Reconcile control accounts and shift recorded transactions from the suspense accounts

to the right accounts.................................................................................................................10

1.Concepts of errors in accounting:.....................................................................................10

2.Types of errors in accounting:...........................................................................................10

3.Concepts of suspens accounting:......................................................................................11

4. Source document:.............................................................................................................12

1.Re-prepare the extracted trial balance above accurately with the given information.

The only amended amount is the suspense's one:............................................................13

2. Show the journal entries to correct the errors:.............................................................14

3. Drawn up the suspense account for the difference between the trial balance totals and

show the correction to be made. Narratives are not required:..........................................16

4. Draw up a statement showing the adjusted net profit after correcting the above errors;

assumed that net profit had previously been calculated at £1,200 for the semi-annum

period ended on 30 June 20X9. Determine which errors have influenced to

profit( impact to sales and expenses)...............................................................................16

CONCLUSION:.......................................................................................................................18

Bibliography.............................................................................................................................19

2

INTRODUCTION:

BANKING RECRUITMENT REPORT is written to explain the

difference between the bank balance stated in the bank

statement and the balance in cash book bank (bank - column) on

a specific date. It is a statement explaining how the bank

statements can be made to agree with the company's ledger.

And this article will clarify this issue through the example of

the Bank Reconciliation Statement for An Binh Ltd.

3

BANKING RECRUITMENT REPORT is written to explain the

difference between the bank balance stated in the bank

statement and the balance in cash book bank (bank - column) on

a specific date. It is a statement explaining how the bank

statements can be made to agree with the company's ledger.

And this article will clarify this issue through the example of

the Bank Reconciliation Statement for An Binh Ltd.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO3 Perform bank reconciliations to

ensure company and bank records are

correct:

1.Concepts of Bank Reconciliation Statement:

A bank reconciliation is the process of matching the balances in

an entity's accounting records for a cash account to the

corresponding information on a bank statement. The goal of this

process is to ascertain the differences between the two, and to

book changes to the accounting records as appropriate.

(accountingtools, 2018)

2.Necessity of Bank Reconciliation Statement:

Bank reconciliation statement ensures the accuracy of the

balances shown by the passbook and cash book.

The bank reconciliation statement provides a check on the

accuracy of entries made in both the books.

The bank reconciliation statement indicates any undue delay in

the collection and clearance of some cheques.

The bank reconciliation statement helps to detect and rectify

any errors committed in both the books.

Bank reconciliation statement helps to update the cash book by

discovering some entries not yet recorded. (gradeup, 2020)

3.Steps of prearing Bank Reconciliation Statement :

There are a total of 2 steps:

1.Compare the records in both the Bank statements/Pass Book

and the Cash Book (bank column only). Identify factors that

have caused a variation in the balances:

4

ensure company and bank records are

correct:

1.Concepts of Bank Reconciliation Statement:

A bank reconciliation is the process of matching the balances in

an entity's accounting records for a cash account to the

corresponding information on a bank statement. The goal of this

process is to ascertain the differences between the two, and to

book changes to the accounting records as appropriate.

(accountingtools, 2018)

2.Necessity of Bank Reconciliation Statement:

Bank reconciliation statement ensures the accuracy of the

balances shown by the passbook and cash book.

The bank reconciliation statement provides a check on the

accuracy of entries made in both the books.

The bank reconciliation statement indicates any undue delay in

the collection and clearance of some cheques.

The bank reconciliation statement helps to detect and rectify

any errors committed in both the books.

Bank reconciliation statement helps to update the cash book by

discovering some entries not yet recorded. (gradeup, 2020)

3.Steps of prearing Bank Reconciliation Statement :

There are a total of 2 steps:

1.Compare the records in both the Bank statements/Pass Book

and the Cash Book (bank column only). Identify factors that

have caused a variation in the balances:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tick the record(transaction) that both appeared in the Pass Book

and the Cash Book

Write down/List the different records/transactions ( the

transaction appeared in only Pass Book or Cash Book)

Analyse the different transactions.

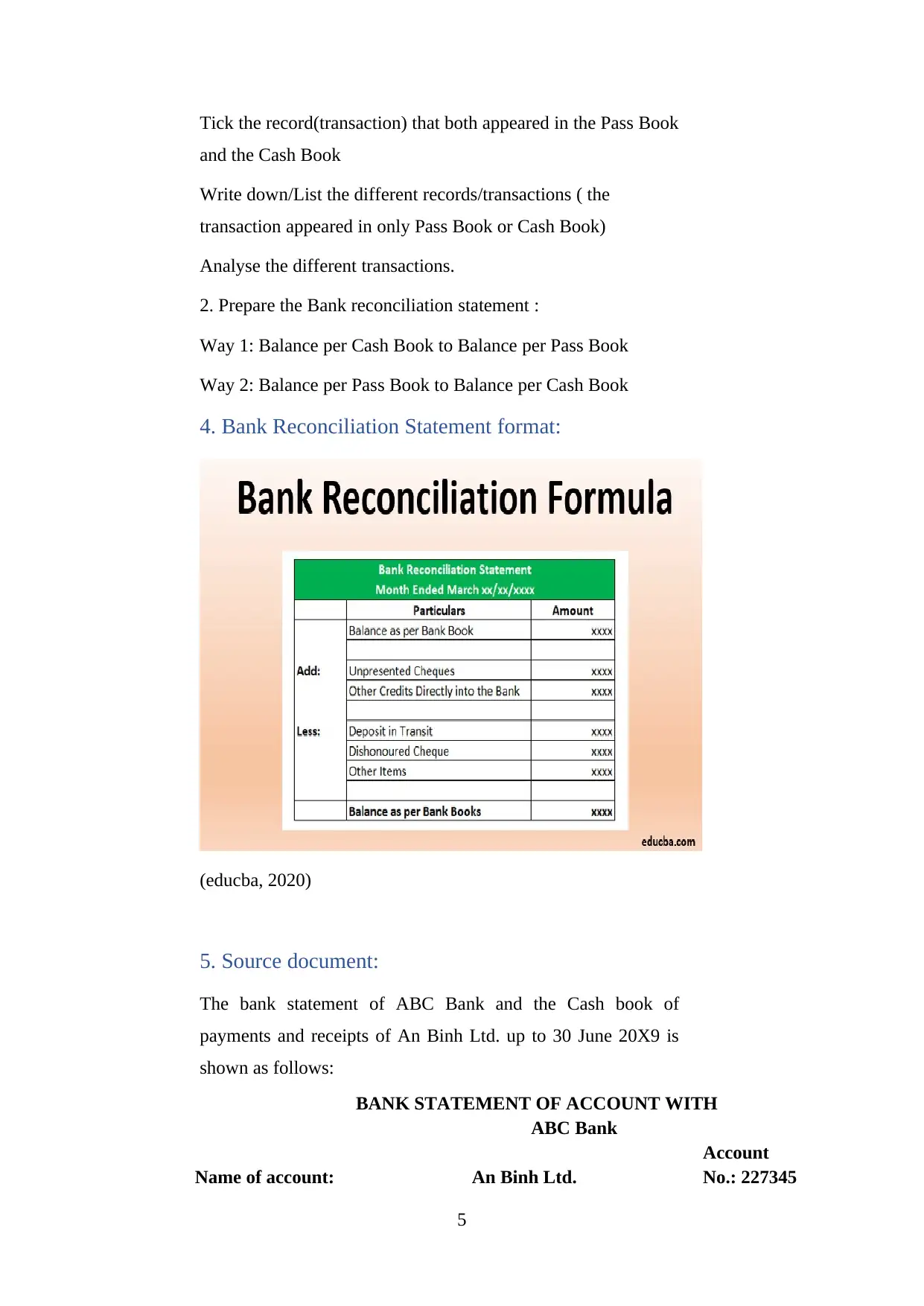

2. Prepare the Bank reconciliation statement :

Way 1: Balance per Cash Book to Balance per Pass Book

Way 2: Balance per Pass Book to Balance per Cash Book

4. Bank Reconciliation Statement format:

(educba, 2020)

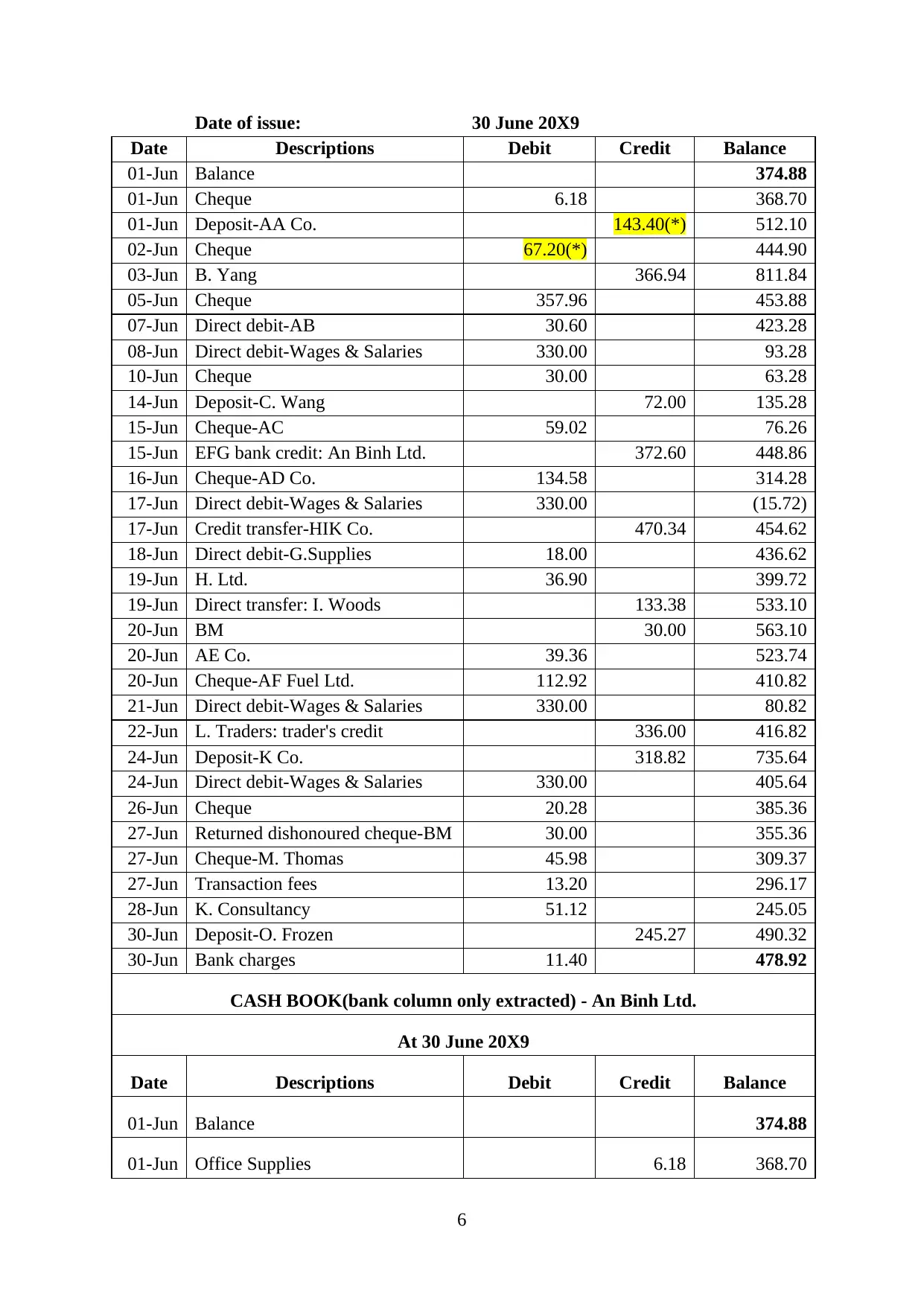

5. Source document:

The bank statement of ABC Bank and the Cash book of

payments and receipts of An Binh Ltd. up to 30 June 20X9 is

shown as follows:

BANK STATEMENT OF ACCOUNT WITH

ABC Bank

Name of account: An Binh Ltd.

Account

No.: 227345

5

and the Cash Book

Write down/List the different records/transactions ( the

transaction appeared in only Pass Book or Cash Book)

Analyse the different transactions.

2. Prepare the Bank reconciliation statement :

Way 1: Balance per Cash Book to Balance per Pass Book

Way 2: Balance per Pass Book to Balance per Cash Book

4. Bank Reconciliation Statement format:

(educba, 2020)

5. Source document:

The bank statement of ABC Bank and the Cash book of

payments and receipts of An Binh Ltd. up to 30 June 20X9 is

shown as follows:

BANK STATEMENT OF ACCOUNT WITH

ABC Bank

Name of account: An Binh Ltd.

Account

No.: 227345

5

Date of issue: 30 June 20X9

Date Descriptions Debit Credit Balance

01-Jun Balance 374.88

01-Jun Cheque 6.18 368.70

01-Jun Deposit-AA Co. 143.40(*) 512.10

02-Jun Cheque 67.20(*) 444.90

03-Jun B. Yang 366.94 811.84

05-Jun Cheque 357.96 453.88

07-Jun Direct debit-AB 30.60 423.28

08-Jun Direct debit-Wages & Salaries 330.00 93.28

10-Jun Cheque 30.00 63.28

14-Jun Deposit-C. Wang 72.00 135.28

15-Jun Cheque-AC 59.02 76.26

15-Jun EFG bank credit: An Binh Ltd. 372.60 448.86

16-Jun Cheque-AD Co. 134.58 314.28

17-Jun Direct debit-Wages & Salaries 330.00 (15.72)

17-Jun Credit transfer-HIK Co. 470.34 454.62

18-Jun Direct debit-G.Supplies 18.00 436.62

19-Jun H. Ltd. 36.90 399.72

19-Jun Direct transfer: I. Woods 133.38 533.10

20-Jun BM 30.00 563.10

20-Jun AE Co. 39.36 523.74

20-Jun Cheque-AF Fuel Ltd. 112.92 410.82

21-Jun Direct debit-Wages & Salaries 330.00 80.82

22-Jun L. Traders: trader's credit 336.00 416.82

24-Jun Deposit-K Co. 318.82 735.64

24-Jun Direct debit-Wages & Salaries 330.00 405.64

26-Jun Cheque 20.28 385.36

27-Jun Returned dishonoured cheque-BM 30.00 355.36

27-Jun Cheque-M. Thomas 45.98 309.37

27-Jun Transaction fees 13.20 296.17

28-Jun K. Consultancy 51.12 245.05

30-Jun Deposit-O. Frozen 245.27 490.32

30-Jun Bank charges 11.40 478.92

CASH BOOK(bank column only extracted) - An Binh Ltd.

At 30 June 20X9

Date Descriptions Debit Credit Balance

01-Jun Balance 374.88

01-Jun Office Supplies 6.18 368.70

6

Date Descriptions Debit Credit Balance

01-Jun Balance 374.88

01-Jun Cheque 6.18 368.70

01-Jun Deposit-AA Co. 143.40(*) 512.10

02-Jun Cheque 67.20(*) 444.90

03-Jun B. Yang 366.94 811.84

05-Jun Cheque 357.96 453.88

07-Jun Direct debit-AB 30.60 423.28

08-Jun Direct debit-Wages & Salaries 330.00 93.28

10-Jun Cheque 30.00 63.28

14-Jun Deposit-C. Wang 72.00 135.28

15-Jun Cheque-AC 59.02 76.26

15-Jun EFG bank credit: An Binh Ltd. 372.60 448.86

16-Jun Cheque-AD Co. 134.58 314.28

17-Jun Direct debit-Wages & Salaries 330.00 (15.72)

17-Jun Credit transfer-HIK Co. 470.34 454.62

18-Jun Direct debit-G.Supplies 18.00 436.62

19-Jun H. Ltd. 36.90 399.72

19-Jun Direct transfer: I. Woods 133.38 533.10

20-Jun BM 30.00 563.10

20-Jun AE Co. 39.36 523.74

20-Jun Cheque-AF Fuel Ltd. 112.92 410.82

21-Jun Direct debit-Wages & Salaries 330.00 80.82

22-Jun L. Traders: trader's credit 336.00 416.82

24-Jun Deposit-K Co. 318.82 735.64

24-Jun Direct debit-Wages & Salaries 330.00 405.64

26-Jun Cheque 20.28 385.36

27-Jun Returned dishonoured cheque-BM 30.00 355.36

27-Jun Cheque-M. Thomas 45.98 309.37

27-Jun Transaction fees 13.20 296.17

28-Jun K. Consultancy 51.12 245.05

30-Jun Deposit-O. Frozen 245.27 490.32

30-Jun Bank charges 11.40 478.92

CASH BOOK(bank column only extracted) - An Binh Ltd.

At 30 June 20X9

Date Descriptions Debit Credit Balance

01-Jun Balance 374.88

01-Jun Office Supplies 6.18 368.70

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

03-Jun Sales-B. Yang 366.94 735.64

05-Jun AA Co. 357.96 377.68

07-Jun AB-Stationery expenses 30.60 347.08

08-Jun Wages and Salary 330.00 17.08

10-Jun Cheque 30.00 (12.92)

14-Jun Sales-C.-Wang 72.00 59.08

15-Jun AC-Advertising fees 59.02 0.06

15-Jun Sales-EFG 372.60 372.66

16-Jun AD Co. 134.58 238.08

17-Jun Wages and Salary 330.00 -91.92

17-Jun HIK Co. 470.34 378.42

18-Jun Supplies Expenses-G. Supplies 18.00 360.42

19-Jun Supplies Expenses-H. Ltd. 36.90 323.52

19-Jun Sales-I.Woods 133.38 456.90

20-Jun Sales-BM 30.00 486.90

20-Jun Fuel expenses-AE Ltd. 39.36 447.54

20-Jun Fuel expense-AF 112.92 334.62

21-Jun Wages and Salary 330.00 4.62

21-Jun Sales-L. Traders 336.00 340.62

22-Jun Sales-K.Co. 318.82 659.44

24-Jun Wages and Salary direct debit 330.00 329.44

25-Jun Dishonoured cheque-BM (30.00) 299.44

26-Jun Gas expense 20.28 279.16

27-Jun M. Thomas Co. 45.98 233.17

27-Jun Transaction fees 13.20 219.97

28-Jun Account fees-K. Consultancy 51.12 168.85

7

05-Jun AA Co. 357.96 377.68

07-Jun AB-Stationery expenses 30.60 347.08

08-Jun Wages and Salary 330.00 17.08

10-Jun Cheque 30.00 (12.92)

14-Jun Sales-C.-Wang 72.00 59.08

15-Jun AC-Advertising fees 59.02 0.06

15-Jun Sales-EFG 372.60 372.66

16-Jun AD Co. 134.58 238.08

17-Jun Wages and Salary 330.00 -91.92

17-Jun HIK Co. 470.34 378.42

18-Jun Supplies Expenses-G. Supplies 18.00 360.42

19-Jun Supplies Expenses-H. Ltd. 36.90 323.52

19-Jun Sales-I.Woods 133.38 456.90

20-Jun Sales-BM 30.00 486.90

20-Jun Fuel expenses-AE Ltd. 39.36 447.54

20-Jun Fuel expense-AF 112.92 334.62

21-Jun Wages and Salary 330.00 4.62

21-Jun Sales-L. Traders 336.00 340.62

22-Jun Sales-K.Co. 318.82 659.44

24-Jun Wages and Salary direct debit 330.00 329.44

25-Jun Dishonoured cheque-BM (30.00) 299.44

26-Jun Gas expense 20.28 279.16

27-Jun M. Thomas Co. 45.98 233.17

27-Jun Transaction fees 13.20 219.97

28-Jun Account fees-K. Consultancy 51.12 168.85

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

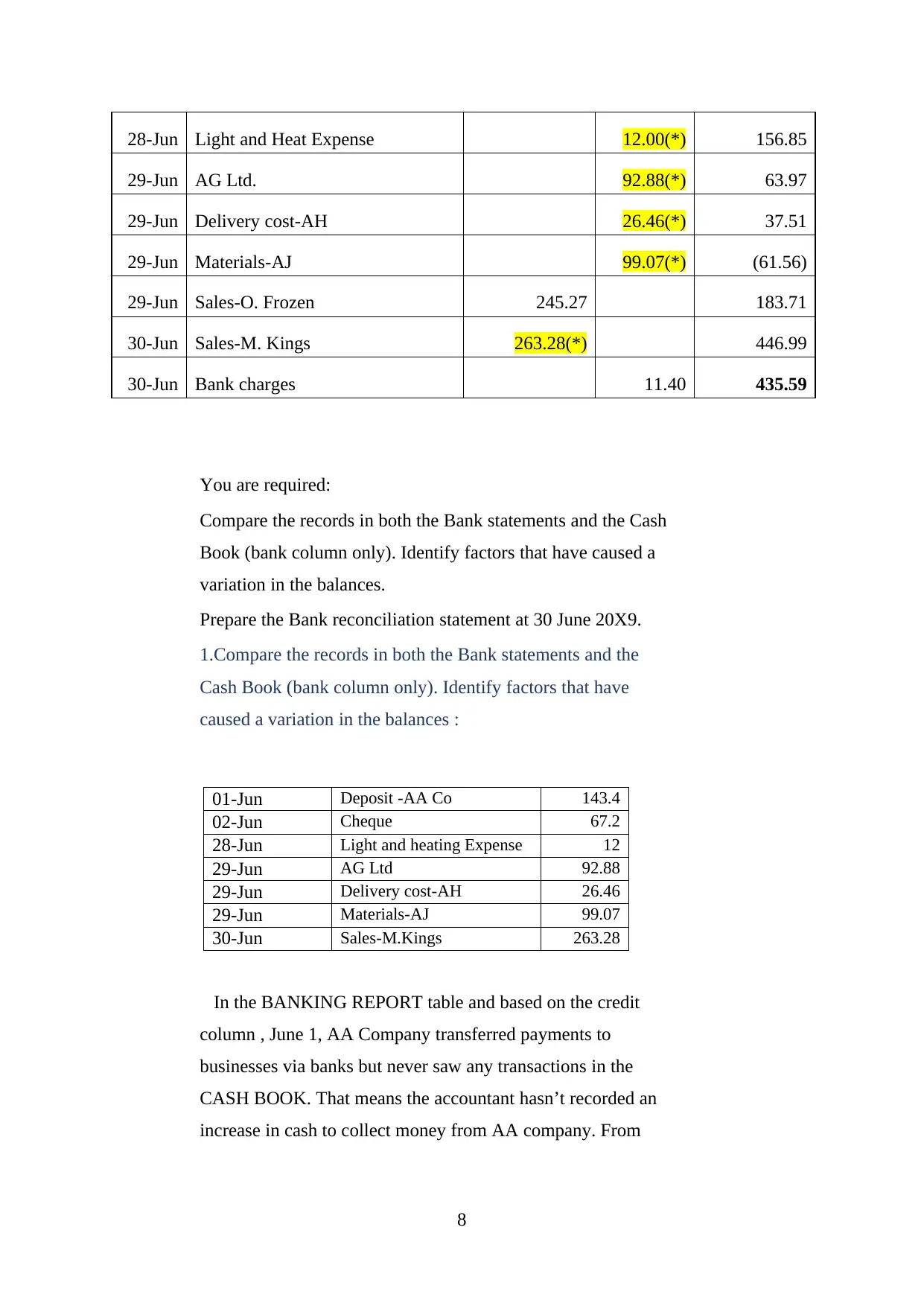

28-Jun Light and Heat Expense 12.00(*) 156.85

29-Jun AG Ltd. 92.88(*) 63.97

29-Jun Delivery cost-AH 26.46(*) 37.51

29-Jun Materials-AJ 99.07(*) (61.56)

29-Jun Sales-O. Frozen 245.27 183.71

30-Jun Sales-M. Kings 263.28(*) 446.99

30-Jun Bank charges 11.40 435.59

You are required:

Compare the records in both the Bank statements and the Cash

Book (bank column only). Identify factors that have caused a

variation in the balances.

Prepare the Bank reconciliation statement at 30 June 20X9.

1.Compare the records in both the Bank statements and the

Cash Book (bank column only). Identify factors that have

caused a variation in the balances :

01-Jun Deposit -AA Co 143.4

02-Jun Cheque 67.2

28-Jun Light and heating Expense 12

29-Jun AG Ltd 92.88

29-Jun Delivery cost-AH 26.46

29-Jun Materials-AJ 99.07

30-Jun Sales-M.Kings 263.28

In the BANKING REPORT table and based on the credit

column , June 1, AA Company transferred payments to

businesses via banks but never saw any transactions in the

CASH BOOK. That means the accountant hasn’t recorded an

increase in cash to collect money from AA company. From

8

29-Jun AG Ltd. 92.88(*) 63.97

29-Jun Delivery cost-AH 26.46(*) 37.51

29-Jun Materials-AJ 99.07(*) (61.56)

29-Jun Sales-O. Frozen 245.27 183.71

30-Jun Sales-M. Kings 263.28(*) 446.99

30-Jun Bank charges 11.40 435.59

You are required:

Compare the records in both the Bank statements and the Cash

Book (bank column only). Identify factors that have caused a

variation in the balances.

Prepare the Bank reconciliation statement at 30 June 20X9.

1.Compare the records in both the Bank statements and the

Cash Book (bank column only). Identify factors that have

caused a variation in the balances :

01-Jun Deposit -AA Co 143.4

02-Jun Cheque 67.2

28-Jun Light and heating Expense 12

29-Jun AG Ltd 92.88

29-Jun Delivery cost-AH 26.46

29-Jun Materials-AJ 99.07

30-Jun Sales-M.Kings 263.28

In the BANKING REPORT table and based on the credit

column , June 1, AA Company transferred payments to

businesses via banks but never saw any transactions in the

CASH BOOK. That means the accountant hasn’t recorded an

increase in cash to collect money from AA company. From

8

there we can see that was credited in the passbook, not debited

in the cashbook.

In the BANKING REPORT and based on the debit column,

June 2, the company debited by cheque but never saw any

transactions in CASH BOOK. That means the accountant did

not record the decrease in money from this. From there we can

see that already debited in passbook, not credited in the

cashbook.

In CASH BOOK and based on the Credit column, June 28,

the company paid Light and Heat Cost but never saw any

transaction in BANKING REPORT. That means the accountant

did not record the decrease in money from this. From there we

can see that already credited in cashbook, not debited in

passbook.

In CASH BOOK and based on the Credit column, 29-Jun, the

company paid for AG Ltd. but never saw any transaction in

BANKING REPORT. That means the accountant did not record

the decrease in money from this. From there we can see that

already credited in cashbook, not debited in passbook.

In CASH BOOK and based on the Credit column, 29-Jun, the

company paid for Delivery cost-AH but never saw any

transaction in BANKING REPORT. That means the accountant

did not record the decrease in money from this. From there we

can see that already credited in cashbook, not debited in

passbook.

In CASH BOOK and based on the Credit column, 29-Jun, the

company paid for Materials-AJ but never saw any transaction in

BANKING REPORT. That means the accountant did not record

the decrease in money from this. From there we can see that

already credited in cashbook, not debited in passbook.

In CASH BOOK and based on the debit column, 30-Jun, the

company debit by Sales-M. Kings but never saw any transaction

in BANKING REPORT. That means the accountant did not

9

in the cashbook.

In the BANKING REPORT and based on the debit column,

June 2, the company debited by cheque but never saw any

transactions in CASH BOOK. That means the accountant did

not record the decrease in money from this. From there we can

see that already debited in passbook, not credited in the

cashbook.

In CASH BOOK and based on the Credit column, June 28,

the company paid Light and Heat Cost but never saw any

transaction in BANKING REPORT. That means the accountant

did not record the decrease in money from this. From there we

can see that already credited in cashbook, not debited in

passbook.

In CASH BOOK and based on the Credit column, 29-Jun, the

company paid for AG Ltd. but never saw any transaction in

BANKING REPORT. That means the accountant did not record

the decrease in money from this. From there we can see that

already credited in cashbook, not debited in passbook.

In CASH BOOK and based on the Credit column, 29-Jun, the

company paid for Delivery cost-AH but never saw any

transaction in BANKING REPORT. That means the accountant

did not record the decrease in money from this. From there we

can see that already credited in cashbook, not debited in

passbook.

In CASH BOOK and based on the Credit column, 29-Jun, the

company paid for Materials-AJ but never saw any transaction in

BANKING REPORT. That means the accountant did not record

the decrease in money from this. From there we can see that

already credited in cashbook, not debited in passbook.

In CASH BOOK and based on the debit column, 30-Jun, the

company debit by Sales-M. Kings but never saw any transaction

in BANKING REPORT. That means the accountant did not

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

record the in increase money from this. From there we can see

that already debited in cash book, not credited in pass book.

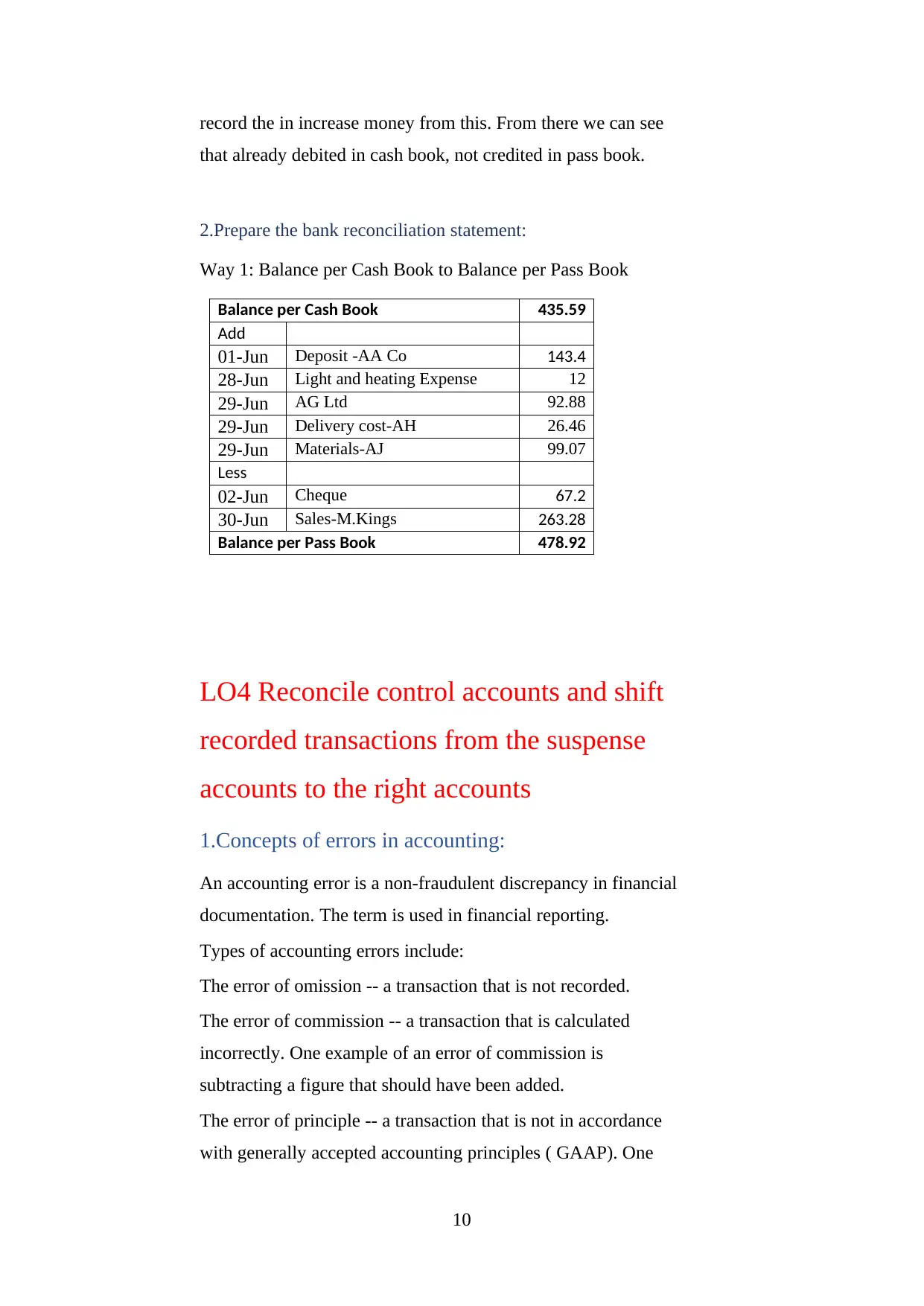

2.Prepare the bank reconciliation statement:

Way 1: Balance per Cash Book to Balance per Pass Book

Balance per Cash Book 435.59

Add

01-Jun Deposit -AA Co 143.4

28-Jun Light and heating Expense 12

29-Jun AG Ltd 92.88

29-Jun Delivery cost-AH 26.46

29-Jun Materials-AJ 99.07

Less

02-Jun Cheque 67.2

30-Jun Sales-M.Kings 263.28

Balance per Pass Book 478.92

LO4 Reconcile control accounts and shift

recorded transactions from the suspense

accounts to the right accounts

1.Concepts of errors in accounting:

An accounting error is a non-fraudulent discrepancy in financial

documentation. The term is used in financial reporting.

Types of accounting errors include:

The error of omission -- a transaction that is not recorded.

The error of commission -- a transaction that is calculated

incorrectly. One example of an error of commission is

subtracting a figure that should have been added.

The error of principle -- a transaction that is not in accordance

with generally accepted accounting principles ( GAAP). One

10

that already debited in cash book, not credited in pass book.

2.Prepare the bank reconciliation statement:

Way 1: Balance per Cash Book to Balance per Pass Book

Balance per Cash Book 435.59

Add

01-Jun Deposit -AA Co 143.4

28-Jun Light and heating Expense 12

29-Jun AG Ltd 92.88

29-Jun Delivery cost-AH 26.46

29-Jun Materials-AJ 99.07

Less

02-Jun Cheque 67.2

30-Jun Sales-M.Kings 263.28

Balance per Pass Book 478.92

LO4 Reconcile control accounts and shift

recorded transactions from the suspense

accounts to the right accounts

1.Concepts of errors in accounting:

An accounting error is a non-fraudulent discrepancy in financial

documentation. The term is used in financial reporting.

Types of accounting errors include:

The error of omission -- a transaction that is not recorded.

The error of commission -- a transaction that is calculated

incorrectly. One example of an error of commission is

subtracting a figure that should have been added.

The error of principle -- a transaction that is not in accordance

with generally accepted accounting principles ( GAAP). One

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

example of an accounting error of principle is an expenditure

that is placed in an inappropriate category.

If a company discovers that an accounting error significantly

affected a previous report, it usually issues a restatement of the

original release. (Rouse, 2020)

2.Types of errors in accounting:

There are several different types of errors in accounting.

Accounting errors are usually unintentional mistakes made

when recording journal entries.

Small accounting errors may not affect the final numbers in

financial statements. Or they might cause major distortions in

the overall figures. These types of errors require lots of time and

resources to find and correct them. (freshbooks, 2020)

1. Subsidiary Entries

Subsidiary entries are transactions that aren’t recorded

correctly. This mistake is only normally discovered during a

bank reconciliation, according to The Balance.

2. Error of Omission

An error of omission happens when you forget to enter a

transaction in the books. You may forget to enter an invoice

you’ve paid or the sale of a service.

3. Transposition Errors

When two digits are reversed (or “transposed”), an error is

created in the books. It’s a simple error but it completely throws

off your accounting.

4. Rounding Errors

Rounding a figure can make your accounting inaccurate and

create a series of future errors. Either people or accounting

software can make this mistake.

5. Errors of Principle

11

that is placed in an inappropriate category.

If a company discovers that an accounting error significantly

affected a previous report, it usually issues a restatement of the

original release. (Rouse, 2020)

2.Types of errors in accounting:

There are several different types of errors in accounting.

Accounting errors are usually unintentional mistakes made

when recording journal entries.

Small accounting errors may not affect the final numbers in

financial statements. Or they might cause major distortions in

the overall figures. These types of errors require lots of time and

resources to find and correct them. (freshbooks, 2020)

1. Subsidiary Entries

Subsidiary entries are transactions that aren’t recorded

correctly. This mistake is only normally discovered during a

bank reconciliation, according to The Balance.

2. Error of Omission

An error of omission happens when you forget to enter a

transaction in the books. You may forget to enter an invoice

you’ve paid or the sale of a service.

3. Transposition Errors

When two digits are reversed (or “transposed”), an error is

created in the books. It’s a simple error but it completely throws

off your accounting.

4. Rounding Errors

Rounding a figure can make your accounting inaccurate and

create a series of future errors. Either people or accounting

software can make this mistake.

5. Errors of Principle

11

A transaction that incorrectly uses an accounting principle is

called an error of principle. Errors of principle don’t meet the

generally accepted accounting principles (GAAP). It’s also

called an “input error” because, though the number is correct,

it’s recorded in the wrong account.

6. Errors of Reversal

When an entry is debited instead of being credited, or vice

versa, this is an error of reversal.

7. Errors of Commission

An error of commission occurs when an amount is entered right

and in the correct account but the value is wrong–i.e. it’s

subtracted instead of added or vice versa. (freshbooks, 2020)

3.Concepts of suspens accounting:

A suspense account is a general ledger account in which

amounts are temporarily recorded. The suspense account is used

because the appropriate general ledger account could not be

determined at the time that the transaction was recorded.

As soon as possible, the amount(s) in the suspense account

should be moved to the proper account(s). (accountingcoach,

2020)

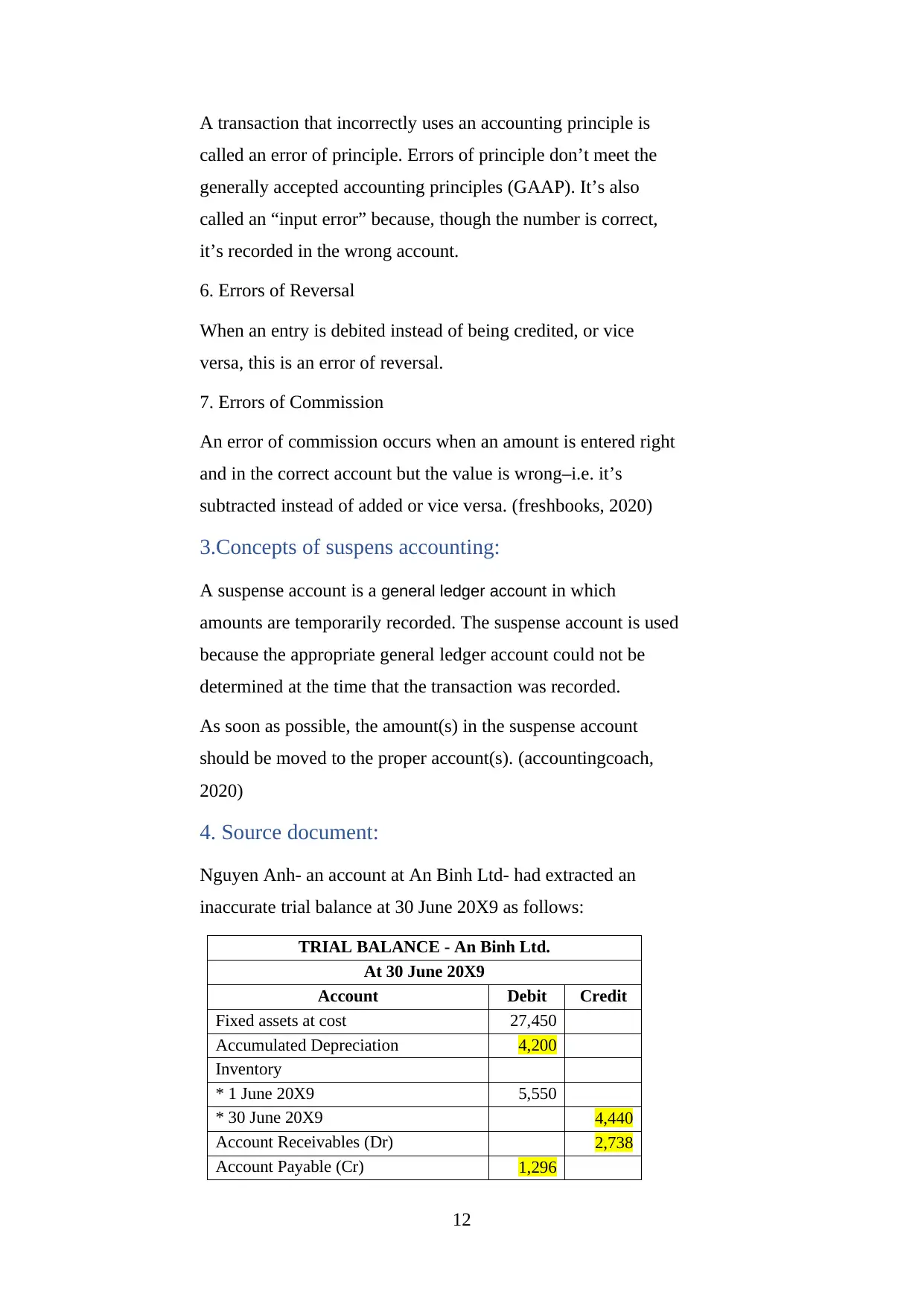

4. Source document:

Nguyen Anh- an account at An Binh Ltd- had extracted an

inaccurate trial balance at 30 June 20X9 as follows:

TRIAL BALANCE - An Binh Ltd.

At 30 June 20X9

Account Debit Credit

Fixed assets at cost 27,450

Accumulated Depreciation 4,200

Inventory

* 1 June 20X9 5,550

* 30 June 20X9 4,440

Account Receivables (Dr) 2,738

Account Payable (Cr) 1,296

12

called an error of principle. Errors of principle don’t meet the

generally accepted accounting principles (GAAP). It’s also

called an “input error” because, though the number is correct,

it’s recorded in the wrong account.

6. Errors of Reversal

When an entry is debited instead of being credited, or vice

versa, this is an error of reversal.

7. Errors of Commission

An error of commission occurs when an amount is entered right

and in the correct account but the value is wrong–i.e. it’s

subtracted instead of added or vice versa. (freshbooks, 2020)

3.Concepts of suspens accounting:

A suspense account is a general ledger account in which

amounts are temporarily recorded. The suspense account is used

because the appropriate general ledger account could not be

determined at the time that the transaction was recorded.

As soon as possible, the amount(s) in the suspense account

should be moved to the proper account(s). (accountingcoach,

2020)

4. Source document:

Nguyen Anh- an account at An Binh Ltd- had extracted an

inaccurate trial balance at 30 June 20X9 as follows:

TRIAL BALANCE - An Binh Ltd.

At 30 June 20X9

Account Debit Credit

Fixed assets at cost 27,450

Accumulated Depreciation 4,200

Inventory

* 1 June 20X9 5,550

* 30 June 20X9 4,440

Account Receivables (Dr) 2,738

Account Payable (Cr) 1,296

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.