Bank Reconciliation: Analyzing Discrepancies and Preparing Statements

VerifiedAdded on 2023/01/12

|5

|316

|82

Report

AI Summary

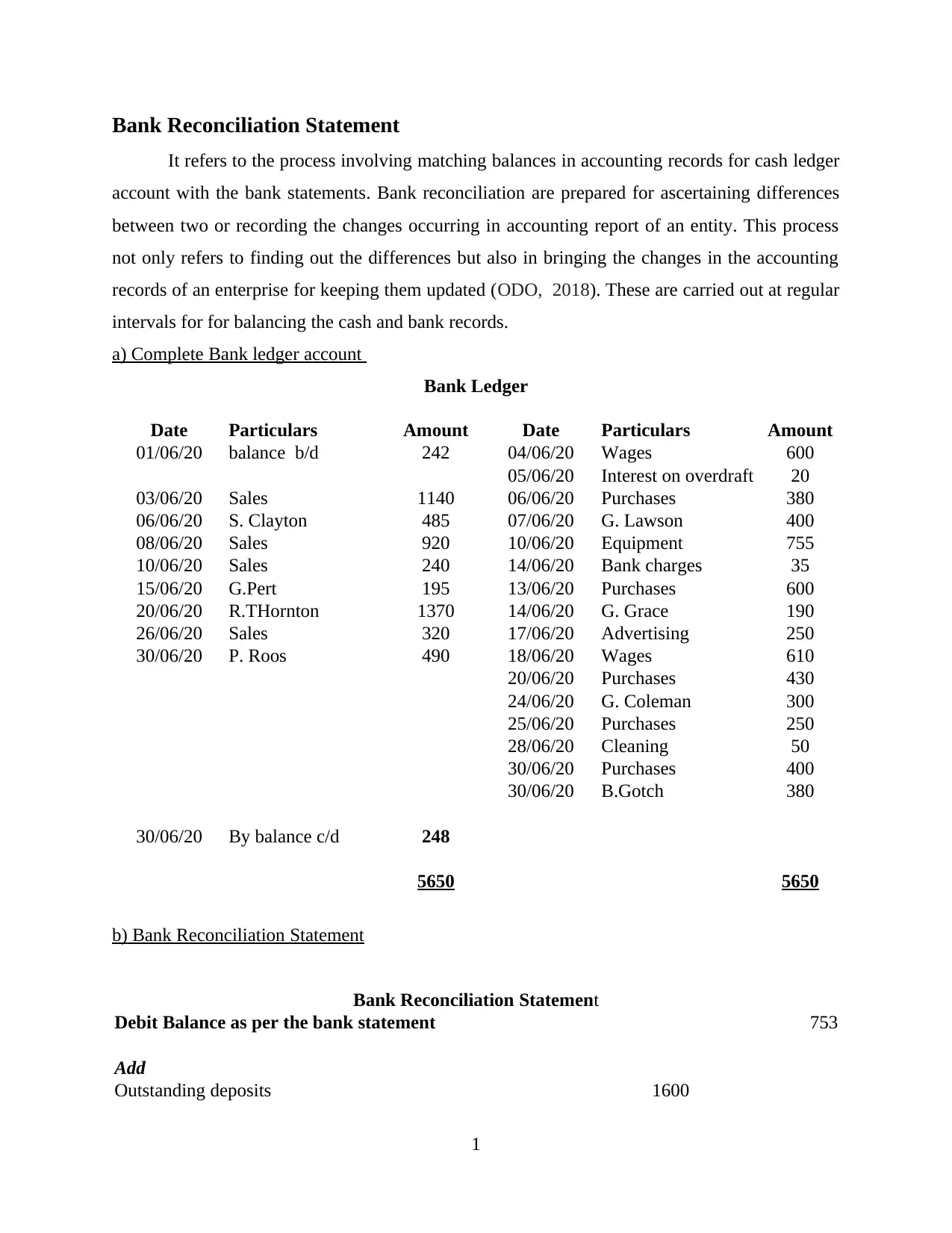

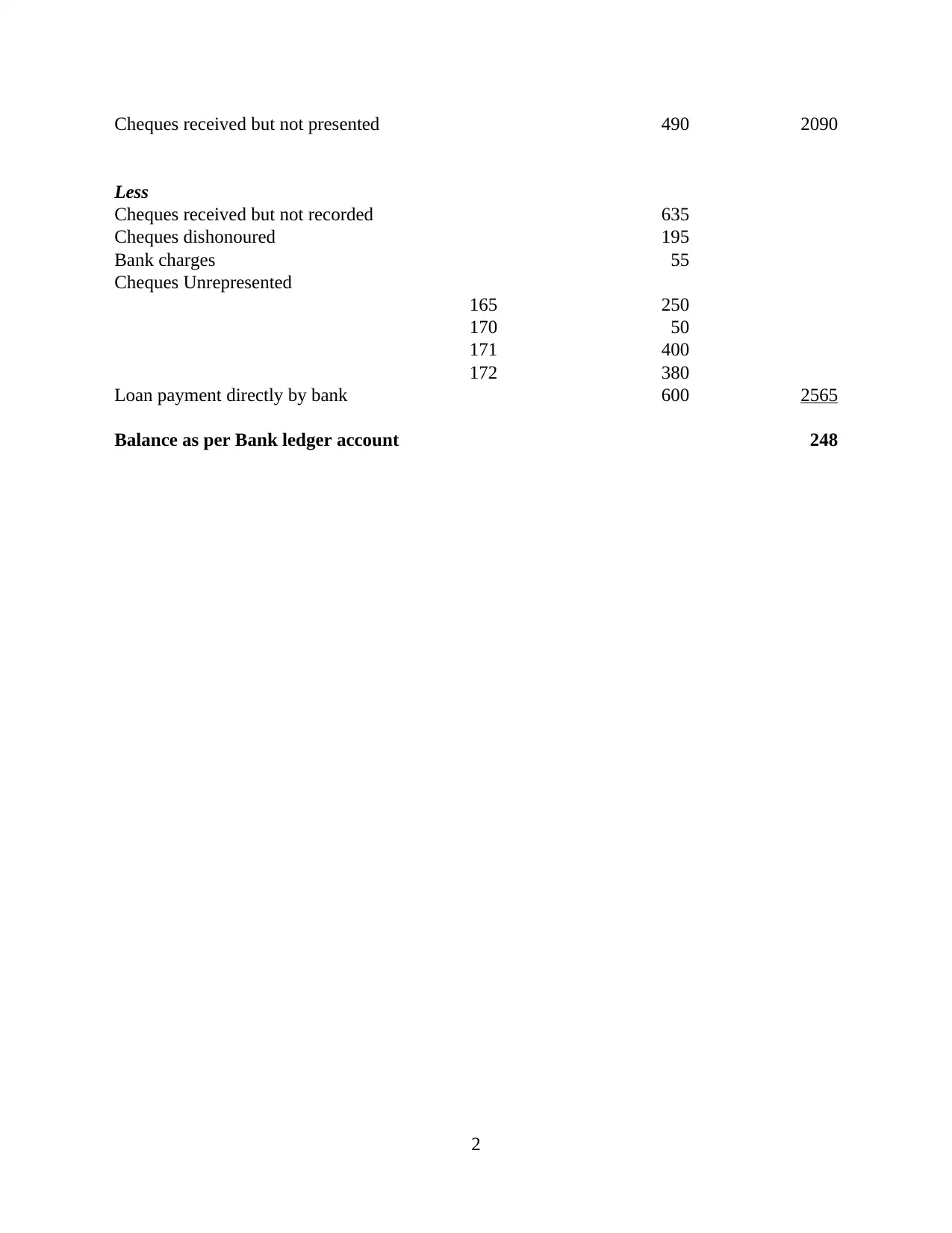

This report focuses on the process of bank reconciliation, a crucial aspect of financial accounting. It begins by defining bank reconciliation and its importance in aligning bank statements with accounting records. The report includes a detailed analysis of a bank ledger account, presenting transactions and balances. Following this, a bank reconciliation statement is presented, outlining the adjustments needed to reconcile the bank statement balance with the ledger balance. The statement incorporates items such as outstanding deposits, unpresented checks, bank charges, and dishonored checks. The report aims to demonstrate how to identify and address discrepancies between the bank statement and the company's records, ensuring accurate financial reporting and providing a clear understanding of the reconciliation process. References to relevant sources are also provided.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.