BNKG1002: Bank Analysis - Structure, Business Model, Risks, Consumers

VerifiedAdded on 2023/06/11

|12

|3718

|167

Report

AI Summary

This report provides an analysis of a commercial bank, focusing on its structure, business model, consumer base, and risk management strategies. Using the Bank of Maldives as an example, the report details the bank's organizational structure, including the roles of the CEO, board of directors, CFO, and risk management team. It examines various income sources, such as interest income and other sources like mutual fund distribution and wealth management services. The report also discusses the importance of customer relationship management (CRM) in meeting customer expectations and providing personalized services. Furthermore, it elaborates on the different forms of risk faced by banks, including credit risk and market risk, and the mitigation actions taken to overcome these risks, such as conducting thorough credit checks and using hedging contracts. The report highlights the significance of financial modeling in valuation, funding, and strategic decision-making, while also acknowledging its limitations in terms of time consumption and accuracy.

BANKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Structure and Business model of bank...............................................................................1

2.Describing consumer base and type of services provided: Customer management:...........4

3.Elaborating forms of risk faced by bank and mitigation actions to overcome the risk.:.....5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

1

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Structure and Business model of bank...............................................................................1

2.Describing consumer base and type of services provided: Customer management:...........4

3.Elaborating forms of risk faced by bank and mitigation actions to overcome the risk.:.....5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

1

INTRODUCTION

Banking is a financial institution which main function is to accept deposits and draft demand

deposits. The main role of banking is to maintain the financial stability. There are various

functions of bank such as keeping the deposits safe of customers and helps in advancing loans to

the firms, customers and homebuyers. There are different types of bank accounts such as current

account and savings account. The main objective of banking is to safeguard the deposits,

enhance living standard, capital formation and generate the employment level. This report

contains the structure and business model of the bank. The bank taken for this report is bank of

Maldives. The main vision is to set high standards of corporate governance and customer

satisfaction. There are different values of this bank are integrity, accessibility, customer first and

team work. It also encompasses the consumer base and types of services provided as a part of

customer management. There are various forms of risk which are faced by the bank and

mitigation actions to reduce the impact of the risk has been explained in this statement in detail

(Alam, Ramachandran and Nahomy, 2020).

MAIN BODY

1. Structure and Business model of bank.

The bank of Maldives is a commercial bank which is inaugurated on November, 1982. This

bank has started its operations as a joint venture bank which consists 60% of shares owned by

the government of Maldives. The remaining 40% of the shares are owned by international

finance investment company limited. In 1992, the government decided to sold the holding in

shares to the general public. It has 38 branches and 50 self-service banking centres. The bank of

Maldives also launches “BML Islamic “on 22 January 2015. There is various income which are

required occur in the banks are described as given below:

1. Interest income: It is the amount which the banks pay on the deposits to its customers and

customers also pay interest on loans. The difference between the two interest is known as

spread. It is a source of income which helps in raising the funds of the banks.

2. Other sources: There are various sources of income such as distribution of mutual funds,

distribution of insurance schemes, offering wealth management services and treasury

operations. These incomes are termed as income from other sources (Bach and et.al.,

2020).

2

Banking is a financial institution which main function is to accept deposits and draft demand

deposits. The main role of banking is to maintain the financial stability. There are various

functions of bank such as keeping the deposits safe of customers and helps in advancing loans to

the firms, customers and homebuyers. There are different types of bank accounts such as current

account and savings account. The main objective of banking is to safeguard the deposits,

enhance living standard, capital formation and generate the employment level. This report

contains the structure and business model of the bank. The bank taken for this report is bank of

Maldives. The main vision is to set high standards of corporate governance and customer

satisfaction. There are different values of this bank are integrity, accessibility, customer first and

team work. It also encompasses the consumer base and types of services provided as a part of

customer management. There are various forms of risk which are faced by the bank and

mitigation actions to reduce the impact of the risk has been explained in this statement in detail

(Alam, Ramachandran and Nahomy, 2020).

MAIN BODY

1. Structure and Business model of bank.

The bank of Maldives is a commercial bank which is inaugurated on November, 1982. This

bank has started its operations as a joint venture bank which consists 60% of shares owned by

the government of Maldives. The remaining 40% of the shares are owned by international

finance investment company limited. In 1992, the government decided to sold the holding in

shares to the general public. It has 38 branches and 50 self-service banking centres. The bank of

Maldives also launches “BML Islamic “on 22 January 2015. There is various income which are

required occur in the banks are described as given below:

1. Interest income: It is the amount which the banks pay on the deposits to its customers and

customers also pay interest on loans. The difference between the two interest is known as

spread. It is a source of income which helps in raising the funds of the banks.

2. Other sources: There are various sources of income such as distribution of mutual funds,

distribution of insurance schemes, offering wealth management services and treasury

operations. These incomes are termed as income from other sources (Bach and et.al.,

2020).

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

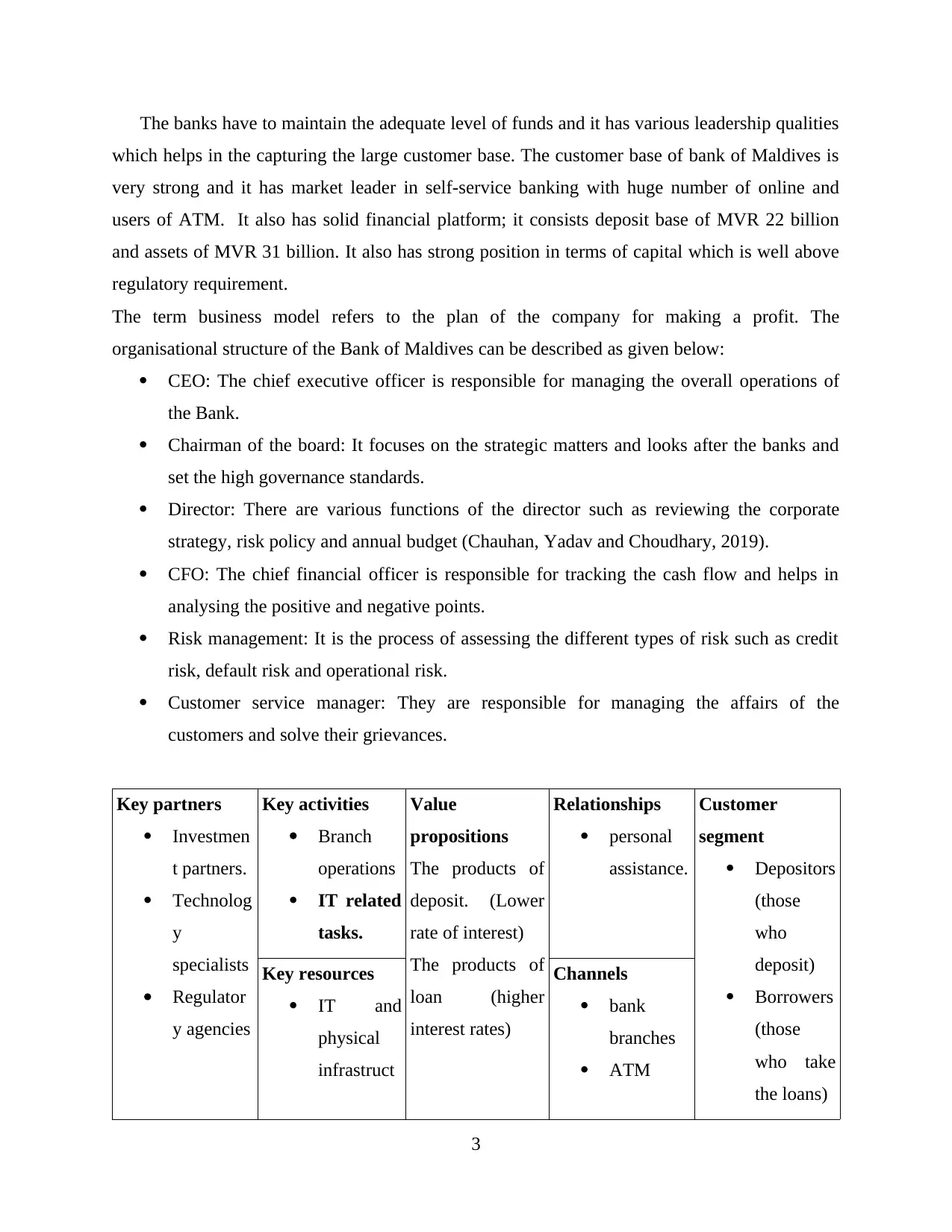

The banks have to maintain the adequate level of funds and it has various leadership qualities

which helps in the capturing the large customer base. The customer base of bank of Maldives is

very strong and it has market leader in self-service banking with huge number of online and

users of ATM. It also has solid financial platform; it consists deposit base of MVR 22 billion

and assets of MVR 31 billion. It also has strong position in terms of capital which is well above

regulatory requirement.

The term business model refers to the plan of the company for making a profit. The

organisational structure of the Bank of Maldives can be described as given below:

CEO: The chief executive officer is responsible for managing the overall operations of

the Bank.

Chairman of the board: It focuses on the strategic matters and looks after the banks and

set the high governance standards.

Director: There are various functions of the director such as reviewing the corporate

strategy, risk policy and annual budget (Chauhan, Yadav and Choudhary, 2019).

CFO: The chief financial officer is responsible for tracking the cash flow and helps in

analysing the positive and negative points.

Risk management: It is the process of assessing the different types of risk such as credit

risk, default risk and operational risk.

Customer service manager: They are responsible for managing the affairs of the

customers and solve their grievances.

Key partners

Investmen

t partners.

Technolog

y

specialists

Regulator

y agencies

Key activities

Branch

operations

IT related

tasks.

Value

propositions

The products of

deposit. (Lower

rate of interest)

The products of

loan (higher

interest rates)

Relationships

personal

assistance.

Customer

segment

Depositors

(those

who

deposit)

Borrowers

(those

who take

the loans)

Key resources

IT and

physical

infrastruct

Channels

bank

branches

ATM

3

which helps in the capturing the large customer base. The customer base of bank of Maldives is

very strong and it has market leader in self-service banking with huge number of online and

users of ATM. It also has solid financial platform; it consists deposit base of MVR 22 billion

and assets of MVR 31 billion. It also has strong position in terms of capital which is well above

regulatory requirement.

The term business model refers to the plan of the company for making a profit. The

organisational structure of the Bank of Maldives can be described as given below:

CEO: The chief executive officer is responsible for managing the overall operations of

the Bank.

Chairman of the board: It focuses on the strategic matters and looks after the banks and

set the high governance standards.

Director: There are various functions of the director such as reviewing the corporate

strategy, risk policy and annual budget (Chauhan, Yadav and Choudhary, 2019).

CFO: The chief financial officer is responsible for tracking the cash flow and helps in

analysing the positive and negative points.

Risk management: It is the process of assessing the different types of risk such as credit

risk, default risk and operational risk.

Customer service manager: They are responsible for managing the affairs of the

customers and solve their grievances.

Key partners

Investmen

t partners.

Technolog

y

specialists

Regulator

y agencies

Key activities

Branch

operations

IT related

tasks.

Value

propositions

The products of

deposit. (Lower

rate of interest)

The products of

loan (higher

interest rates)

Relationships

personal

assistance.

Customer

segment

Depositors

(those

who

deposit)

Borrowers

(those

who take

the loans)

Key resources

IT and

physical

infrastruct

Channels

bank

branches

ATM

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

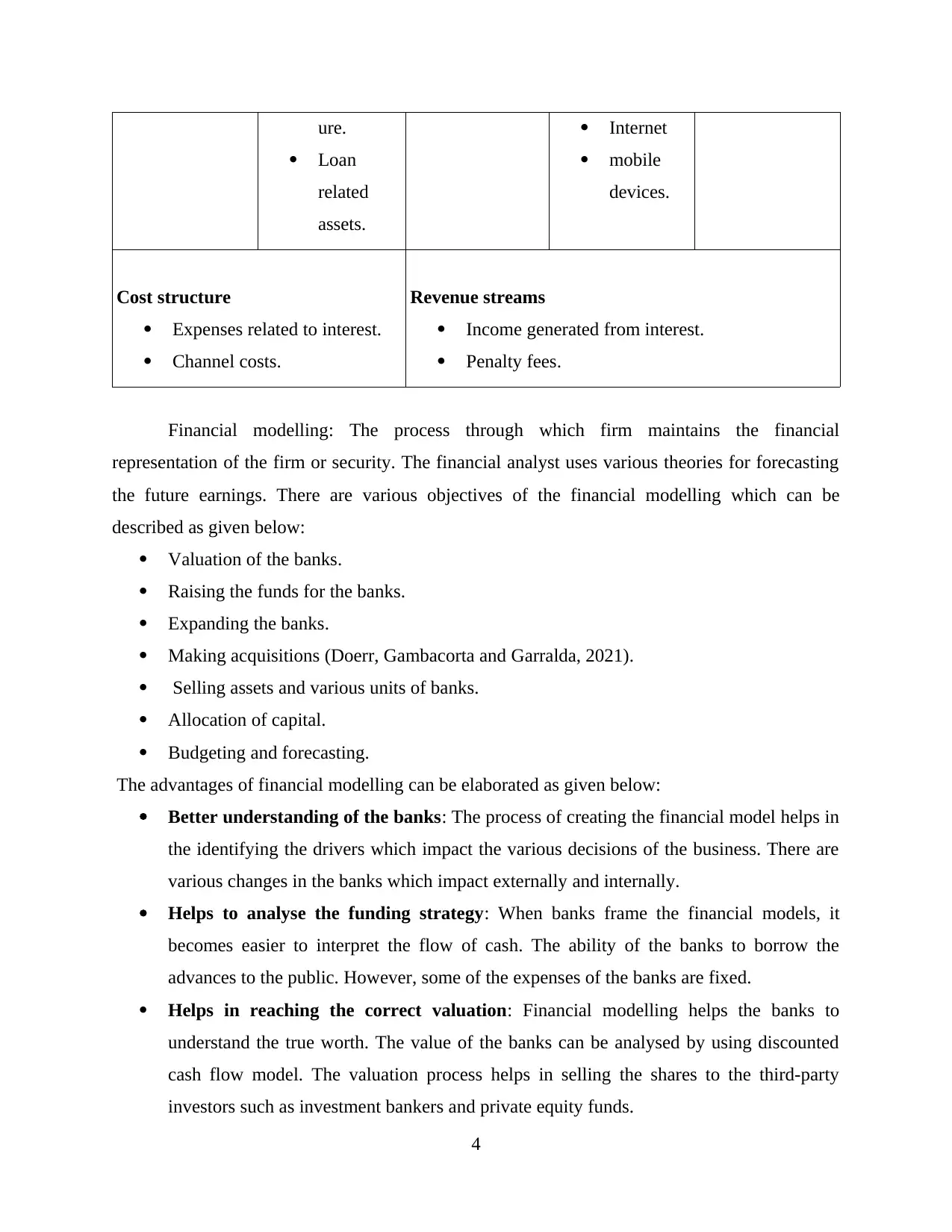

ure.

Loan

related

assets.

Internet

mobile

devices.

Cost structure

Expenses related to interest.

Channel costs.

Revenue streams

Income generated from interest.

Penalty fees.

Financial modelling: The process through which firm maintains the financial

representation of the firm or security. The financial analyst uses various theories for forecasting

the future earnings. There are various objectives of the financial modelling which can be

described as given below:

Valuation of the banks.

Raising the funds for the banks.

Expanding the banks.

Making acquisitions (Doerr, Gambacorta and Garralda, 2021).

Selling assets and various units of banks.

Allocation of capital.

Budgeting and forecasting.

The advantages of financial modelling can be elaborated as given below:

Better understanding of the banks: The process of creating the financial model helps in

the identifying the drivers which impact the various decisions of the business. There are

various changes in the banks which impact externally and internally.

Helps to analyse the funding strategy: When banks frame the financial models, it

becomes easier to interpret the flow of cash. The ability of the banks to borrow the

advances to the public. However, some of the expenses of the banks are fixed.

Helps in reaching the correct valuation: Financial modelling helps the banks to

understand the true worth. The value of the banks can be analysed by using discounted

cash flow model. The valuation process helps in selling the shares to the third-party

investors such as investment bankers and private equity funds.

4

Loan

related

assets.

Internet

mobile

devices.

Cost structure

Expenses related to interest.

Channel costs.

Revenue streams

Income generated from interest.

Penalty fees.

Financial modelling: The process through which firm maintains the financial

representation of the firm or security. The financial analyst uses various theories for forecasting

the future earnings. There are various objectives of the financial modelling which can be

described as given below:

Valuation of the banks.

Raising the funds for the banks.

Expanding the banks.

Making acquisitions (Doerr, Gambacorta and Garralda, 2021).

Selling assets and various units of banks.

Allocation of capital.

Budgeting and forecasting.

The advantages of financial modelling can be elaborated as given below:

Better understanding of the banks: The process of creating the financial model helps in

the identifying the drivers which impact the various decisions of the business. There are

various changes in the banks which impact externally and internally.

Helps to analyse the funding strategy: When banks frame the financial models, it

becomes easier to interpret the flow of cash. The ability of the banks to borrow the

advances to the public. However, some of the expenses of the banks are fixed.

Helps in reaching the correct valuation: Financial modelling helps the banks to

understand the true worth. The value of the banks can be analysed by using discounted

cash flow model. The valuation process helps in selling the shares to the third-party

investors such as investment bankers and private equity funds.

4

The disadvantages of financial modelling can be described as given below:

Time consuming: The process of financial modelling is a time consuming because it

consists various activities to be performed. The data is available in large volume and it

becomes difficult to manage. There is new software which require training of the

employees and increases the cost of the banks. The financial models have limited

applicability (Kuzmenko and Koibichuk, 2018).

Inaccurate: There was an incidence of subprime mortgage crisis in 2008, there are

various drawbacks of this model. There is lack in understanding factors such as interest

rates, tax rates and market shares with accuracy.

Soft factors not considered: There are various factors which are qualitative in nature.

There are various factors of cultural compatibility which does not consider the expenses

of the daily functions of the bank.

2.Describing consumer base and type of services provided: Customer management:

One of the important challenges that the banking business in the digital world is meeting

out the customer expectation. It is necessary for the bank to provide sound business solution to

their customers whether retain or corporate so that business should get expanded (Shome, Jabeen

and Rajaguru, 2018). The corporate customer of the bank wants goal-based planning,

personalized outreach, proactive insights and much more that must be provided by the banking

channels so that they retain them for the long run. Similar solution is provided by bank of

Maldives to their customer so that business will grow across the globe. Such thing will happen

only when there is separate block in the bank named as customer relationship management

(CRM).

The great and proper implementation of CRM will help the banking business to get the new

customer, helps in closing the deal made therein, and helps in giving the excellent customer

service. This system would help the bank in managing their customer and helps in understanding

their needs in a better way which provides them right solution on right time. Such system has

been implemented by the bank of Maldives in a more structured way so that each and every

customer the bank connected must be addressed completely. This system will enable the bank to

track of the information regarding the customer across the bank and also service will involve

5

Time consuming: The process of financial modelling is a time consuming because it

consists various activities to be performed. The data is available in large volume and it

becomes difficult to manage. There is new software which require training of the

employees and increases the cost of the banks. The financial models have limited

applicability (Kuzmenko and Koibichuk, 2018).

Inaccurate: There was an incidence of subprime mortgage crisis in 2008, there are

various drawbacks of this model. There is lack in understanding factors such as interest

rates, tax rates and market shares with accuracy.

Soft factors not considered: There are various factors which are qualitative in nature.

There are various factors of cultural compatibility which does not consider the expenses

of the daily functions of the bank.

2.Describing consumer base and type of services provided: Customer management:

One of the important challenges that the banking business in the digital world is meeting

out the customer expectation. It is necessary for the bank to provide sound business solution to

their customers whether retain or corporate so that business should get expanded (Shome, Jabeen

and Rajaguru, 2018). The corporate customer of the bank wants goal-based planning,

personalized outreach, proactive insights and much more that must be provided by the banking

channels so that they retain them for the long run. Similar solution is provided by bank of

Maldives to their customer so that business will grow across the globe. Such thing will happen

only when there is separate block in the bank named as customer relationship management

(CRM).

The great and proper implementation of CRM will help the banking business to get the new

customer, helps in closing the deal made therein, and helps in giving the excellent customer

service. This system would help the bank in managing their customer and helps in understanding

their needs in a better way which provides them right solution on right time. Such system has

been implemented by the bank of Maldives in a more structured way so that each and every

customer the bank connected must be addressed completely. This system will enable the bank to

track of the information regarding the customer across the bank and also service will involve

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

360-degree view regarding each customer and delivering tremendous service to customer which

not only satisfy their needs but also locks trust between them forever.

In the customer relationship management system has been put to place in the right prospect then

it will help in delivering digital first baking experience to the customer which are hold by bank

of Maldives. It will enable quick and clear on boarding to real time service responses and such

system help Maldives bank to embark digital transformation across both the online and mobile

banking experiences. In today’s world the importance of online transaction has increased with

the rapid growth rate and to maintain share in the market in is important for bank to provide

online banking solution through portal or application to their customer so that it will easier for

them to carry out the transaction smoothly (Tuna and Almahadin, 2021).

This system is very useful and helpful as it makes us very easier for generation of repots which

shows the customer data, engagement channels associated with the bank etc. With the help of

such information the marketing team can easily discover new engagement opportunities and can

deliver useful and personalized marketing facility to each and every banking customer they

possess in their business model. With the use of CRM, the bank of Maldives can deliver the

customer query on timely manner as it helps in minimising the repetition of work carried out

earlier in banks. The correct CRM can help the bank in justifying the needs of the customer, the

relationship that must be maintain and satisfying their financial goals and objective.

3.Elaborating forms of risk faced by bank and mitigation actions to overcome the risk.:

The risk that has been faced by the Bank of Maldives and their mitigation measures are been

mentioned under: -

Credit Risk:

Credit risk arises when where there are chances that the loan that has been given by them

are not paid on timely basis by borrowers who obtained loan from them. Such risk simply

means the risk of not receiving the payment on due course and those payments which are

not received non due dates are converted under this category (Al-Dmour, Dawood, and

Masa'deh, 2020). There are situations where borrower becomes insolvent and in order to

mitigate such risk the banks must conduct the complete and through check before

sanctioning the loan amount. Such loans must be granted to those individuals and

6

not only satisfy their needs but also locks trust between them forever.

In the customer relationship management system has been put to place in the right prospect then

it will help in delivering digital first baking experience to the customer which are hold by bank

of Maldives. It will enable quick and clear on boarding to real time service responses and such

system help Maldives bank to embark digital transformation across both the online and mobile

banking experiences. In today’s world the importance of online transaction has increased with

the rapid growth rate and to maintain share in the market in is important for bank to provide

online banking solution through portal or application to their customer so that it will easier for

them to carry out the transaction smoothly (Tuna and Almahadin, 2021).

This system is very useful and helpful as it makes us very easier for generation of repots which

shows the customer data, engagement channels associated with the bank etc. With the help of

such information the marketing team can easily discover new engagement opportunities and can

deliver useful and personalized marketing facility to each and every banking customer they

possess in their business model. With the use of CRM, the bank of Maldives can deliver the

customer query on timely manner as it helps in minimising the repetition of work carried out

earlier in banks. The correct CRM can help the bank in justifying the needs of the customer, the

relationship that must be maintain and satisfying their financial goals and objective.

3.Elaborating forms of risk faced by bank and mitigation actions to overcome the risk.:

The risk that has been faced by the Bank of Maldives and their mitigation measures are been

mentioned under: -

Credit Risk:

Credit risk arises when where there are chances that the loan that has been given by them

are not paid on timely basis by borrowers who obtained loan from them. Such risk simply

means the risk of not receiving the payment on due course and those payments which are

not received non due dates are converted under this category (Al-Dmour, Dawood, and

Masa'deh, 2020). There are situations where borrower becomes insolvent and in order to

mitigate such risk the banks must conduct the complete and through check before

sanctioning the loan amount. Such loans must be granted to those individuals and

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business persons who are not run out of the income during the period for which loan has

granted. Before sanctioning the loan, the credit worthiness must be checked with the help

of credit rating agencies that provide complete and accurate information so that bank of

Maldives can make informed decision in this regard.

Market Risk:

Apart from sanctioning the loan the Maldives bank is also engaged in investing the

significant amount in securities. Sometimes the reasons for holding such securities might

be treasury operations that carried out by them i.e. certain amount of funds has to be

invested in short term securities. However, there are various kinds of securities under

which the bank of Maldives grant loan to customer and such securities will create risk on

them. They are facing various amount of risk as such risk varies dependent upon the

nature of securities such as if they have invested in equity then they are exposed to equity

risk and if they made agreement in foreign currency transaction then they face foreign

currency risk. In order to mitigate or reduce the impact of such risk, the bank of Maldives

enter hedging contracts and also use various forms of financial derivate which are

available for sale in the financial market. With the help of entering such contracts such as

options, swaps, bank of Maldives can eliminate such risk to an acceptable level

collectively (Bai, Shi, and Sarkis, 2019).

Operational Risk:

The banks involved in many operations so that they can earn profit margins in their

business model. The bank of Maldives will be benefited as they are the larger bank and

have economies of scale. However, maintaining the internal processes consistently on the

huge scale in the difficult task all around. Such risk arises as the result of failed business

processes in day-to-day activities carried out the bank. Such risk faced by them majorly

due to hiring the wrong candidate or such risk may also arise due to failure in their

information system. In order to mitigate such risk bank of Maldives internal control

system must be effective all around the corner so that its impact could be reduced

accordingly otherwise their business will become bankrupt.

Liquidity Risk:

Such risk it another risk that is inherent to the banking system and such risk simply

means that the bank of Maldives will not be able to meet their obligations when the

7

granted. Before sanctioning the loan, the credit worthiness must be checked with the help

of credit rating agencies that provide complete and accurate information so that bank of

Maldives can make informed decision in this regard.

Market Risk:

Apart from sanctioning the loan the Maldives bank is also engaged in investing the

significant amount in securities. Sometimes the reasons for holding such securities might

be treasury operations that carried out by them i.e. certain amount of funds has to be

invested in short term securities. However, there are various kinds of securities under

which the bank of Maldives grant loan to customer and such securities will create risk on

them. They are facing various amount of risk as such risk varies dependent upon the

nature of securities such as if they have invested in equity then they are exposed to equity

risk and if they made agreement in foreign currency transaction then they face foreign

currency risk. In order to mitigate or reduce the impact of such risk, the bank of Maldives

enter hedging contracts and also use various forms of financial derivate which are

available for sale in the financial market. With the help of entering such contracts such as

options, swaps, bank of Maldives can eliminate such risk to an acceptable level

collectively (Bai, Shi, and Sarkis, 2019).

Operational Risk:

The banks involved in many operations so that they can earn profit margins in their

business model. The bank of Maldives will be benefited as they are the larger bank and

have economies of scale. However, maintaining the internal processes consistently on the

huge scale in the difficult task all around. Such risk arises as the result of failed business

processes in day-to-day activities carried out the bank. Such risk faced by them majorly

due to hiring the wrong candidate or such risk may also arise due to failure in their

information system. In order to mitigate such risk bank of Maldives internal control

system must be effective all around the corner so that its impact could be reduced

accordingly otherwise their business will become bankrupt.

Liquidity Risk:

Such risk it another risk that is inherent to the banking system and such risk simply

means that the bank of Maldives will not be able to meet their obligations when the

7

depositors arrive to the bank to withdraw their fund. However, such system will be

handled by the central bank of Maldives as they are getting backing for such a situation.

This situation is normally called as bank run and this will happen many times during the

history of modern banking. They are not very concerned about such risk due to backing

they got from the central bank which is considered as mitigating factor to reduce such

risk as central bank will divert of its resources to them as and when they get affected

(Famiyeh, Asante-Darko, and Kwarteng, 2018).

Reputational Risk:

Reputation is considered as an asset for the business as they work on the basis of trust

that people on them and reputation works as an intangible asset for them. If they maintain

their business for the longer period, that if would support their business and increase their

revenue over such period. The customer always willing to invest their funds in those

financial institution which they believe follow safe and good business practices. In order

to mitigate such risk, they simply can carry out fair trade practices and does not give any

monetary loss to their customer.

Business risk:

The banking and other financial institution are working with the help of advanced

technology and well diversifies in terms of products and services they offer to their

customers. The bank of Maldives mainly focussing towards resources they are using so

that their strategic goals could be achieved in the long run. Such risk could not be

mitigated as it is created due to inappropriate business objectives. Such risk is generally

faced by every business and to reduce such risk different measures and policies need to

be adopted by the bank of Maldives (Haseeb, 2018).

Systemic Risk:

Systemic risk arises due to connectivity between the banks altogether with other banking

and financial institution and sometimes such connectivity creates the problem for one

bank as they fail in their business due to failure of any other bank. The bank of Maldives

is also connected with other banks to carry out their operational activity as many

transactions has been taken place between the banks itself and they work like the

counterparty to each other and enters many transactions within the day. Therefore, due to

this connectivity the failure of one bank may impact bank of Maldives simultaneously

8

handled by the central bank of Maldives as they are getting backing for such a situation.

This situation is normally called as bank run and this will happen many times during the

history of modern banking. They are not very concerned about such risk due to backing

they got from the central bank which is considered as mitigating factor to reduce such

risk as central bank will divert of its resources to them as and when they get affected

(Famiyeh, Asante-Darko, and Kwarteng, 2018).

Reputational Risk:

Reputation is considered as an asset for the business as they work on the basis of trust

that people on them and reputation works as an intangible asset for them. If they maintain

their business for the longer period, that if would support their business and increase their

revenue over such period. The customer always willing to invest their funds in those

financial institution which they believe follow safe and good business practices. In order

to mitigate such risk, they simply can carry out fair trade practices and does not give any

monetary loss to their customer.

Business risk:

The banking and other financial institution are working with the help of advanced

technology and well diversifies in terms of products and services they offer to their

customers. The bank of Maldives mainly focussing towards resources they are using so

that their strategic goals could be achieved in the long run. Such risk could not be

mitigated as it is created due to inappropriate business objectives. Such risk is generally

faced by every business and to reduce such risk different measures and policies need to

be adopted by the bank of Maldives (Haseeb, 2018).

Systemic Risk:

Systemic risk arises due to connectivity between the banks altogether with other banking

and financial institution and sometimes such connectivity creates the problem for one

bank as they fail in their business due to failure of any other bank. The bank of Maldives

is also connected with other banks to carry out their operational activity as many

transactions has been taken place between the banks itself and they work like the

counterparty to each other and enters many transactions within the day. Therefore, due to

this connectivity the failure of one bank may impact bank of Maldives simultaneously

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and their operational activity gets affected. This basis nature of the bank will make them

prone to systemic risk and such risk does not disturb any individual bank but affect the

chain of numerous banks at one point of time. Therefore, it is important for them to keep

focus on their technical skills hold by management that would help them from surviving

from such a situation (Hayne, 2019).

CONCLUSION

From the above report, it can be concluded that banking is an institution which performs

various primary and secondary functions. The primary functions include the task of savings or

depositing the amount and advancing loans to the general public. It is necessary to understand

the structure of the banks and business model which helps in understanding the overall

composition of the bank. There are various departments in the banks which includes CEO,

managing director, chief financial officer, risk manager and customer service manager. There is

various cost, revenue, activities, value propositions and customer segment. The purpose of this

report to show the working of bank of Maldives and the risk they are facing internally and

externally and the measures from which such risk can be reduced accordingly. The mitigation

measures reduce the impact of such risk and such measures are not being adopted then business

may have got into losses and will not survive further. In today’s world the role of online

transaction has been increased with the rapid pace therefore bank of Maldives must make sure

that their operational are carried out safely so that disruption does not taken place in operational

hours of working.

9

prone to systemic risk and such risk does not disturb any individual bank but affect the

chain of numerous banks at one point of time. Therefore, it is important for them to keep

focus on their technical skills hold by management that would help them from surviving

from such a situation (Hayne, 2019).

CONCLUSION

From the above report, it can be concluded that banking is an institution which performs

various primary and secondary functions. The primary functions include the task of savings or

depositing the amount and advancing loans to the general public. It is necessary to understand

the structure of the banks and business model which helps in understanding the overall

composition of the bank. There are various departments in the banks which includes CEO,

managing director, chief financial officer, risk manager and customer service manager. There is

various cost, revenue, activities, value propositions and customer segment. The purpose of this

report to show the working of bank of Maldives and the risk they are facing internally and

externally and the measures from which such risk can be reduced accordingly. The mitigation

measures reduce the impact of such risk and such measures are not being adopted then business

may have got into losses and will not survive further. In today’s world the role of online

transaction has been increased with the rapid pace therefore bank of Maldives must make sure

that their operational are carried out safely so that disruption does not taken place in operational

hours of working.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Alam, N., Ramachandran, J. and Nahomy, A.H., 2020. The impact of corporate governance and

agency effect on earnings management–A test of the dual banking system. Research in

International Business and Finance, 54, p.101242.

Al-Dmour, R., Dawood, E.A.H., and Masa'deh, R.E., 2020. The effect of customer lifestyle

patterns on the use of mobile banking applications in Jordan. International Journal of

Electronic Marketing and Retailing, 11(3), pp.239-258.

Bach, M.P., and et.al., 2020. m-Banking quality and bank reputation. Sustainability, 12(10),

pp.1-18.

Bai, C., Shi, B., and Sarkis, J., 2019. Banking credit worthiness: Evaluating the complex

relationships. Omega, 83, pp.26-38.

Chauhan, V., Yadav, R. and Choudhary, V., 2019. Analyzing the impact of consumer

innovativeness and perceived risk in internet banking adoption: A study of Indian

consumers. International Journal of Bank Marketing.

Doerr, S., Gambacorta, L. and Garralda, J.M.S., 2021. Big data and machine learning in central

banking. BIS Working Papers, (930).

Famiyeh, S., Asante-Darko, D. and Kwarteng, A., 2018. Service quality, customer satisfaction,

and loyalty in the banking sector: The moderating role of organizational

culture. International Journal of Quality & Reliability Management.

Haseeb, M., 2018. Emerging issues in islamic banking & finance: Challenges and

Solutions. Academy of Accounting and Financial Studies Journal, 22, pp.1-5.

Hayne, K., 2019. Royal Commission into misconduct in the banking, superannuation and

financial services industry. Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry.

Kaakeh, A., Hassan, M.K. and Almazor, S.F.V.H., 2019. Factors affecting customers’ attitude

towards Islamic banking in UAE. International Journal of Emerging Markets.

Kuzmenko, O.V. and Koibichuk, V.V., 2018. Econometric modeling of the influence of relevant

indicators of gender policy on the efficiency of a banking system. Cybernetics and

Systems Analysis, 54(5). pp.687-695.

10

Books and Journals

Alam, N., Ramachandran, J. and Nahomy, A.H., 2020. The impact of corporate governance and

agency effect on earnings management–A test of the dual banking system. Research in

International Business and Finance, 54, p.101242.

Al-Dmour, R., Dawood, E.A.H., and Masa'deh, R.E., 2020. The effect of customer lifestyle

patterns on the use of mobile banking applications in Jordan. International Journal of

Electronic Marketing and Retailing, 11(3), pp.239-258.

Bach, M.P., and et.al., 2020. m-Banking quality and bank reputation. Sustainability, 12(10),

pp.1-18.

Bai, C., Shi, B., and Sarkis, J., 2019. Banking credit worthiness: Evaluating the complex

relationships. Omega, 83, pp.26-38.

Chauhan, V., Yadav, R. and Choudhary, V., 2019. Analyzing the impact of consumer

innovativeness and perceived risk in internet banking adoption: A study of Indian

consumers. International Journal of Bank Marketing.

Doerr, S., Gambacorta, L. and Garralda, J.M.S., 2021. Big data and machine learning in central

banking. BIS Working Papers, (930).

Famiyeh, S., Asante-Darko, D. and Kwarteng, A., 2018. Service quality, customer satisfaction,

and loyalty in the banking sector: The moderating role of organizational

culture. International Journal of Quality & Reliability Management.

Haseeb, M., 2018. Emerging issues in islamic banking & finance: Challenges and

Solutions. Academy of Accounting and Financial Studies Journal, 22, pp.1-5.

Hayne, K., 2019. Royal Commission into misconduct in the banking, superannuation and

financial services industry. Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry.

Kaakeh, A., Hassan, M.K. and Almazor, S.F.V.H., 2019. Factors affecting customers’ attitude

towards Islamic banking in UAE. International Journal of Emerging Markets.

Kuzmenko, O.V. and Koibichuk, V.V., 2018. Econometric modeling of the influence of relevant

indicators of gender policy on the efficiency of a banking system. Cybernetics and

Systems Analysis, 54(5). pp.687-695.

10

Lagarde, C., 2021. Climate change and central banking. Green Banking and Green Central

Banking, 24, p.151.

Naeem, M. and Ozuem, W., 2021. The role of social media in internet banking transition during

COVID-19 pandemic: Using multiple methods and sources in qualitative

research. Journal of Retailing and Consumer Services, 60, p.102483.

Omoregie, O.K., Addae, J.A., and Ofori, K.S., 2019. Factors influencing consumer loyalty:

evidence from the Ghanaian retail banking industry. International Journal of Bank

Marketing.

Shome, A., Jabeen, F. and Rajaguru, R., 2018. What drives consumer choice of Islamic banking

services in the United Arab Emirates? International Journal of Islamic and Middle

Eastern Finance and Management.

Tuna, G. and Almahadin, H.A., 2021. Does interest rate and its volatility affect banking sector

development? Empirical evidence from emerging market economies. Research in

International Business and Finance, 58, p.101436.

11

Banking, 24, p.151.

Naeem, M. and Ozuem, W., 2021. The role of social media in internet banking transition during

COVID-19 pandemic: Using multiple methods and sources in qualitative

research. Journal of Retailing and Consumer Services, 60, p.102483.

Omoregie, O.K., Addae, J.A., and Ofori, K.S., 2019. Factors influencing consumer loyalty:

evidence from the Ghanaian retail banking industry. International Journal of Bank

Marketing.

Shome, A., Jabeen, F. and Rajaguru, R., 2018. What drives consumer choice of Islamic banking

services in the United Arab Emirates? International Journal of Islamic and Middle

Eastern Finance and Management.

Tuna, G. and Almahadin, H.A., 2021. Does interest rate and its volatility affect banking sector

development? Empirical evidence from emerging market economies. Research in

International Business and Finance, 58, p.101436.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.