BANK 2007 Business Finance: Financial Analysis and Investment Advice

VerifiedAdded on 2023/06/18

|10

|2042

|483

Report

AI Summary

This report delves into business finance principles, addressing client financial inquiries and investment strategies. It explores compounding techniques, comparing their effectiveness against non-compounding methods and analyzing monthly versus annual compounding. The report discusses the concept of intrinsic value, its impact on investment decisions, and what occurs when asset selling prices fall below intrinsic value. Practical scenarios, including present value calculations for various investment options and annuity evaluations, are presented to guide client decision-making. The analysis includes calculations for future value, annual payments on loans, and the impact of compounding frequency. Ultimately, the report advises clients to favor compound interest for investments and simple interest for borrowing, providing a comprehensive guide to informed financial choices. Desklib provides access to similar solved assignments and resources for students.

Business finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Clients financial questions...............................................................................................................3

1....................................................................................................................................................3

2....................................................................................................................................................3

3....................................................................................................................................................4

4....................................................................................................................................................4

Clients Investment...........................................................................................................................5

1....................................................................................................................................................5

2....................................................................................................................................................5

3....................................................................................................................................................5

4....................................................................................................................................................6

5....................................................................................................................................................7

a)..................................................................................................................................................7

b)..................................................................................................................................................7

REFERENCES................................................................................................................................1

Clients financial questions...............................................................................................................3

1....................................................................................................................................................3

2....................................................................................................................................................3

3....................................................................................................................................................4

4....................................................................................................................................................4

Clients Investment...........................................................................................................................5

1....................................................................................................................................................5

2....................................................................................................................................................5

3....................................................................................................................................................5

4....................................................................................................................................................6

5....................................................................................................................................................7

a)..................................................................................................................................................7

b)..................................................................................................................................................7

REFERENCES................................................................................................................................1

INTRODUCTION

Business finance refers to the funds availed by the business owners for the start-up and

development of the businesses. The report will discuss the compounding technique of time value

of money to calculate the effective rate of interest. This report will also discuss why the non-

compounding technique is better than compounding technique along with why monthly

compounding is better than annual compounding. The report will also discuss the concept of

intrinsic value of assets and what happen when selling price of assets is lesser than the intrinsic

value. This report help in identifying business finance issues and their solution which help the

which company can attain its operational and financial objectives.

Clients financial questions

1.

The non-compounding technique is more preferable than annual compounding to the

investors because some time annual compounding became expensive as compared to monthly or

quarterly compounding. The annual interest is normally at higher rates because of the

compounding and when the investors get interest at the same rate throughout the year. Then

getting monthly and quarterly payment rather than annual payment is best as the investors will

get higher interest amount (Khechine, Raymond and Augier, 2020). But it is not that much affect

the income because basically there is no difference between the annual and monthly interest

when the investors want to withdraw the capital. The monthly interest income is preferable to the

investors even though the interest rate is lower because it provides cash in hand and strong

liquidity position to the investors.

2.

In case of simple interest rates, the interest amount is calculated on the outstanding principal

amount only and accordingly, the borrowing made on simple interest are considered to be

cheaper.

While in case of compounding interest rate, the amount of interest is calculated in each period on

the basis of outstanding principal amount + outstanding interest amount as well. Therefore, by

calculating an effective rate of interest is calculated for the purpose of determining the rate at

which interest is to be charged on the outstanding balance of both principal and interest amount

(Marty, 2020).

Business finance refers to the funds availed by the business owners for the start-up and

development of the businesses. The report will discuss the compounding technique of time value

of money to calculate the effective rate of interest. This report will also discuss why the non-

compounding technique is better than compounding technique along with why monthly

compounding is better than annual compounding. The report will also discuss the concept of

intrinsic value of assets and what happen when selling price of assets is lesser than the intrinsic

value. This report help in identifying business finance issues and their solution which help the

which company can attain its operational and financial objectives.

Clients financial questions

1.

The non-compounding technique is more preferable than annual compounding to the

investors because some time annual compounding became expensive as compared to monthly or

quarterly compounding. The annual interest is normally at higher rates because of the

compounding and when the investors get interest at the same rate throughout the year. Then

getting monthly and quarterly payment rather than annual payment is best as the investors will

get higher interest amount (Khechine, Raymond and Augier, 2020). But it is not that much affect

the income because basically there is no difference between the annual and monthly interest

when the investors want to withdraw the capital. The monthly interest income is preferable to the

investors even though the interest rate is lower because it provides cash in hand and strong

liquidity position to the investors.

2.

In case of simple interest rates, the interest amount is calculated on the outstanding principal

amount only and accordingly, the borrowing made on simple interest are considered to be

cheaper.

While in case of compounding interest rate, the amount of interest is calculated in each period on

the basis of outstanding principal amount + outstanding interest amount as well. Therefore, by

calculating an effective rate of interest is calculated for the purpose of determining the rate at

which interest is to be charged on the outstanding balance of both principal and interest amount

(Marty, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The differentiating interest amount can be illustrated as follows in case of both simple interest

and compound interest.

Effective rate of interest has to be calculated as follows in case of compounding interest rate:

Effective rate of interest = [1 + 0.092 / 12] 12 – 1 = 9.598%

Therefore, borrowing if done on simple interest rate will be costly due to a higher rate of 10%

interest charged and in case of compounding interest rate, it will cost 9.598% which is lower as

compared to simple interest rates. So, client would be suggested to borrow on compounding

interest rate basis.

3.

Intrinsic value is a measure which state the worth and value of the assets which is arrived

by using complex business model. It is basically the difference between the strike price of the

options and the current price of the underlying assets. The company estimate the intrinsic value

of assets using the fundamental and technical analysis because there is no standard model is

given for the intrinsic value calculations. Typically, investors try to use both qualitative and

quantitative method to measure the intrinsic value of the assets such as discounted cash flows.

The weighted average cost of capital is used to calculate the expected rate of return that an

investors wants to earn from their investment plan (García-Monleón, Danvila-del-Valle and

Lara, 2021). The investors need to understand that the intrinsic value is not real but an estimated

value which may be differed from the selling value of the assets. If the selling price is less than

its intrinsic value than investor will faces loss and in order to overcome it they need to increased

its stock and assets price to balance them. The intrinsic value of assets is less than its current

market value and selling price than its means assets are overpriced and need to be reduced.

4.

Effective rate is the one that create a compounding period in the duration of the payment plan.

This is denoted as the annual interest and compounding interest of different time frame. On the

other side nominal rate denote the interest payable in the respective time period. The key

difference between effective rate and nominal rate is that in context to effective rate the interest

is payable more as compare to the nominal rate (Irena and Mariana, 2017). The interest under the

effective rate increase as the time processes as it also consumes interest on interest like practice.

The role of the effective rate of interest is very effective in processing the loan rate to be higher.

The other side nominal rate does not charge interest over the interest which make this rate more

and compound interest.

Effective rate of interest has to be calculated as follows in case of compounding interest rate:

Effective rate of interest = [1 + 0.092 / 12] 12 – 1 = 9.598%

Therefore, borrowing if done on simple interest rate will be costly due to a higher rate of 10%

interest charged and in case of compounding interest rate, it will cost 9.598% which is lower as

compared to simple interest rates. So, client would be suggested to borrow on compounding

interest rate basis.

3.

Intrinsic value is a measure which state the worth and value of the assets which is arrived

by using complex business model. It is basically the difference between the strike price of the

options and the current price of the underlying assets. The company estimate the intrinsic value

of assets using the fundamental and technical analysis because there is no standard model is

given for the intrinsic value calculations. Typically, investors try to use both qualitative and

quantitative method to measure the intrinsic value of the assets such as discounted cash flows.

The weighted average cost of capital is used to calculate the expected rate of return that an

investors wants to earn from their investment plan (García-Monleón, Danvila-del-Valle and

Lara, 2021). The investors need to understand that the intrinsic value is not real but an estimated

value which may be differed from the selling value of the assets. If the selling price is less than

its intrinsic value than investor will faces loss and in order to overcome it they need to increased

its stock and assets price to balance them. The intrinsic value of assets is less than its current

market value and selling price than its means assets are overpriced and need to be reduced.

4.

Effective rate is the one that create a compounding period in the duration of the payment plan.

This is denoted as the annual interest and compounding interest of different time frame. On the

other side nominal rate denote the interest payable in the respective time period. The key

difference between effective rate and nominal rate is that in context to effective rate the interest

is payable more as compare to the nominal rate (Irena and Mariana, 2017). The interest under the

effective rate increase as the time processes as it also consumes interest on interest like practice.

The role of the effective rate of interest is very effective in processing the loan rate to be higher.

The other side nominal rate does not charge interest over the interest which make this rate more

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

affordable in nature. When it comes to investment decision effective rate provide more retrain to

the investor whereas the nominal rate provide a limited return over investment made.

While evaluating investment opportunities, client must go for those opportunities offering

effective rate of return over nominal rate of return because in case of nominal returns interests in

the form of return are provided only on the basis of principal amount invested, whereas in case of

effective rate of return client can obtain higher returns as interests are provided on both principle

and interest amount that has been accumulated every year.

Clients Investment

1.

Option 1: Present value of Cash Inflow: $100000

Option 2: Present value of Cash Inflow: cash inflow each year* present value annuity due

@12% for 10 years ($10000* 6.328) = $63280

Option 3: Present value of Cash Inflow: cash inflow at the end of year* present value of 12% at

10th year ($50000 + 150000* 0.322) = $98300

On the basis of above calculation present value of cash flow of each alternative it is

recommendable to the client to opt for first option as its is more profitable than other alternatives

(Bai and Wang, 2020).

2.

To have an accumulated amount equivalent to 15000 in 15 years, the amount needed to be

invested each year will be calculated as follows:

FV = P * [ (1 + r)n – 1 / r ]

Here, FV is the future value that is, 15000

P is the periodic payment or Annuity = ?

r is the rate of interest per period = 10%

n is the number of period = 15 years

Compounding = semi – annually

therefore, n will be taken as 30 and r will be taken as 5%.

15000 = P * [(1 + 5%)30 – 1 / 5%

15000 = P * [4.322 – 1] / 0.05

15000 = P * 66.44

15000 / 66.44 = P

the investor whereas the nominal rate provide a limited return over investment made.

While evaluating investment opportunities, client must go for those opportunities offering

effective rate of return over nominal rate of return because in case of nominal returns interests in

the form of return are provided only on the basis of principal amount invested, whereas in case of

effective rate of return client can obtain higher returns as interests are provided on both principle

and interest amount that has been accumulated every year.

Clients Investment

1.

Option 1: Present value of Cash Inflow: $100000

Option 2: Present value of Cash Inflow: cash inflow each year* present value annuity due

@12% for 10 years ($10000* 6.328) = $63280

Option 3: Present value of Cash Inflow: cash inflow at the end of year* present value of 12% at

10th year ($50000 + 150000* 0.322) = $98300

On the basis of above calculation present value of cash flow of each alternative it is

recommendable to the client to opt for first option as its is more profitable than other alternatives

(Bai and Wang, 2020).

2.

To have an accumulated amount equivalent to 15000 in 15 years, the amount needed to be

invested each year will be calculated as follows:

FV = P * [ (1 + r)n – 1 / r ]

Here, FV is the future value that is, 15000

P is the periodic payment or Annuity = ?

r is the rate of interest per period = 10%

n is the number of period = 15 years

Compounding = semi – annually

therefore, n will be taken as 30 and r will be taken as 5%.

15000 = P * [(1 + 5%)30 – 1 / 5%

15000 = P * [4.322 – 1] / 0.05

15000 = P * 66.44

15000 / 66.44 = P

P = 225.77

Therefore, every year Client need to invest 225.77 in order to have amount equivalent to 15000

in 15 years.

3.

1st year = $10000* 5% = $10500

2nd year = $10500* 5% = $11025

3rd year = $11025* 5% = $11576

4th year = $11576* 5% = $ 12155

5th year = $12155* 5% = $12763 - $7500 = $5263

6th year = $5263* 5% = $5526

7th year = $5526* 5% = $5802

8th year = $5802* 5% = $6092

Amount remain in the client account at the end of the 5th year will be = $5263 approx. if they

deposit $10000 current at the rate of 5% p.a. and after withdrawing $7500 in 5th year. It is

assumed that client will withdraw this amount at the end of the year.

The amount remain in account in the eight year is = $6092 approx.

4.

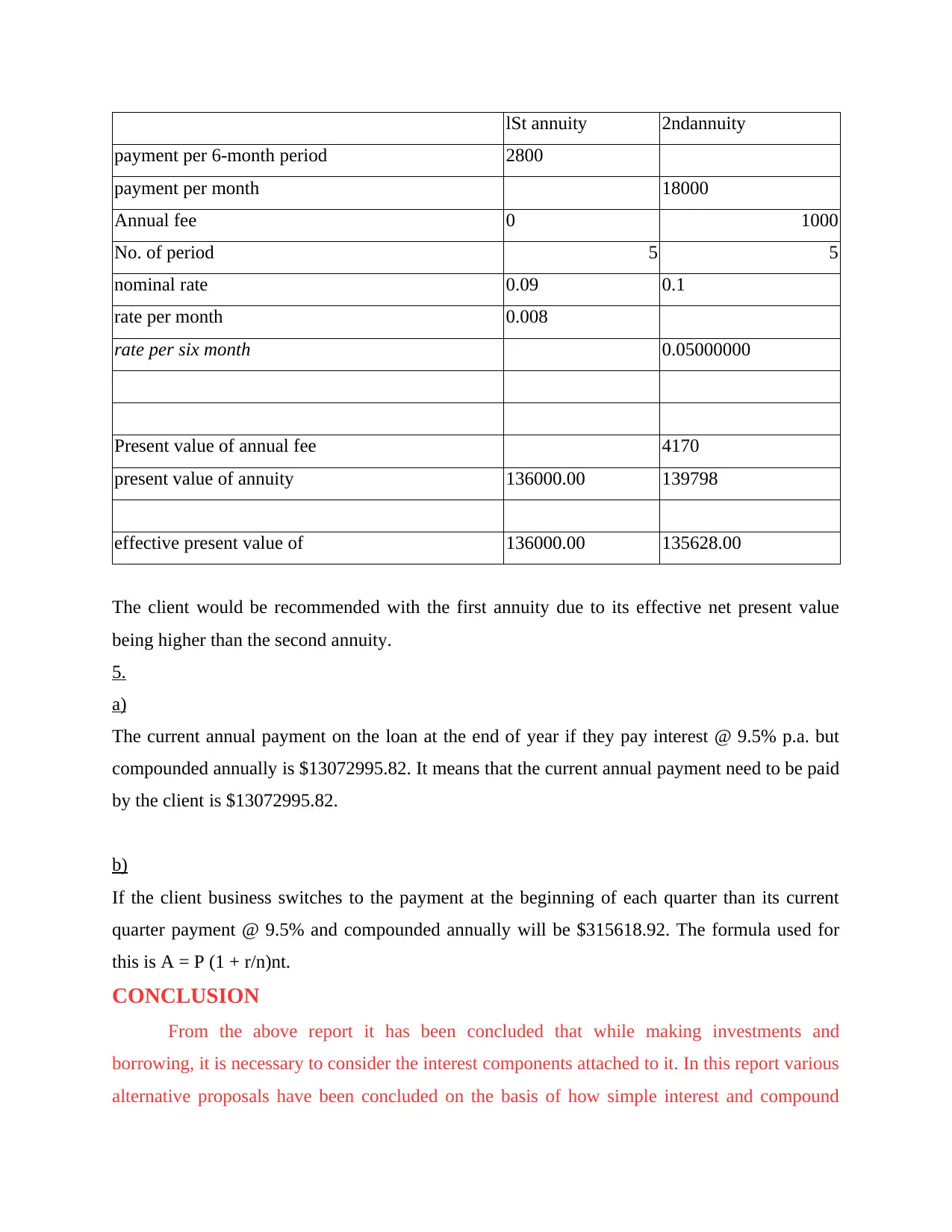

Evaluation of two annuities

Particulars of first annuity

Payment per month = 2800

Annual fee = 0

number of periods = 5 years

Nominal rate = 9% p.a.

Rate per month = 0.09 / 12 = 0.0075

Particulars of second annuity

Payment per six month's period = 18000

Annual fee = 1000

Number of periods = 5 years

Nominal rate = 10% p.a.

Rate per six months = 0.1 / 2 = 0.05

Therefore, every year Client need to invest 225.77 in order to have amount equivalent to 15000

in 15 years.

3.

1st year = $10000* 5% = $10500

2nd year = $10500* 5% = $11025

3rd year = $11025* 5% = $11576

4th year = $11576* 5% = $ 12155

5th year = $12155* 5% = $12763 - $7500 = $5263

6th year = $5263* 5% = $5526

7th year = $5526* 5% = $5802

8th year = $5802* 5% = $6092

Amount remain in the client account at the end of the 5th year will be = $5263 approx. if they

deposit $10000 current at the rate of 5% p.a. and after withdrawing $7500 in 5th year. It is

assumed that client will withdraw this amount at the end of the year.

The amount remain in account in the eight year is = $6092 approx.

4.

Evaluation of two annuities

Particulars of first annuity

Payment per month = 2800

Annual fee = 0

number of periods = 5 years

Nominal rate = 9% p.a.

Rate per month = 0.09 / 12 = 0.0075

Particulars of second annuity

Payment per six month's period = 18000

Annual fee = 1000

Number of periods = 5 years

Nominal rate = 10% p.a.

Rate per six months = 0.1 / 2 = 0.05

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

lSt annuity 2ndannuity

payment per 6-month period 2800

payment per month 18000

Annual fee 0 1000

No. of period 5 5

nominal rate 0.09 0.1

rate per month 0.008

rate per six month 0.05000000

Present value of annual fee 4170

present value of annuity 136000.00 139798

effective present value of 136000.00 135628.00

The client would be recommended with the first annuity due to its effective net present value

being higher than the second annuity.

5.

a)

The current annual payment on the loan at the end of year if they pay interest @ 9.5% p.a. but

compounded annually is $13072995.82. It means that the current annual payment need to be paid

by the client is $13072995.82.

b)

If the client business switches to the payment at the beginning of each quarter than its current

quarter payment @ 9.5% and compounded annually will be $315618.92. The formula used for

this is A = P (1 + r/n)nt.

CONCLUSION

From the above report it has been concluded that while making investments and

borrowing, it is necessary to consider the interest components attached to it. In this report various

alternative proposals have been concluded on the basis of how simple interest and compound

payment per 6-month period 2800

payment per month 18000

Annual fee 0 1000

No. of period 5 5

nominal rate 0.09 0.1

rate per month 0.008

rate per six month 0.05000000

Present value of annual fee 4170

present value of annuity 136000.00 139798

effective present value of 136000.00 135628.00

The client would be recommended with the first annuity due to its effective net present value

being higher than the second annuity.

5.

a)

The current annual payment on the loan at the end of year if they pay interest @ 9.5% p.a. but

compounded annually is $13072995.82. It means that the current annual payment need to be paid

by the client is $13072995.82.

b)

If the client business switches to the payment at the beginning of each quarter than its current

quarter payment @ 9.5% and compounded annually will be $315618.92. The formula used for

this is A = P (1 + r/n)nt.

CONCLUSION

From the above report it has been concluded that while making investments and

borrowing, it is necessary to consider the interest components attached to it. In this report various

alternative proposals have been concluded on the basis of how simple interest and compound

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

interest rates works and also the impact of time value of money has been evaluated that helps in

making it clear to the client what they needs to save today to get the required amount in future.

As per the findings of this report, it is to be recommended that while investing client should

choose investment opportunities having compound interest rate attached to it over simple interest

rate and at the time of borrowing, client should go for obtaining loan at a simple interest rates

over compound interest rates due to being cheaper.

making it clear to the client what they needs to save today to get the required amount in future.

As per the findings of this report, it is to be recommended that while investing client should

choose investment opportunities having compound interest rate attached to it over simple interest

rate and at the time of borrowing, client should go for obtaining loan at a simple interest rates

over compound interest rates due to being cheaper.

REFERENCES

Books and journals

Bai, B. and Wang, J., 2020. The role of growth mindset, self-efficacy and intrinsic value in self-

regulated learning and English language learning achievements. Language teaching

research, p.1362168820933190.

García-Monleón, F., Danvila-del-Valle, I. and Lara, F. J., 2021. Intrinsic value in crypto

currencies. Technological Forecasting and Social Change. 162. p.120393.

Irena, M. and Mariana, B., 2017. The Time Value of Money in Financial Management. Ovidius

University Annals, Economic Sciences Series. 17(2). pp.593-597.

Khechine, H., Raymond, B. and Augier, M., 2020. The adoption of a social learning system:

Intrinsic value in the UTAUT model. British Journal of Educational

Technology. 51(6). pp.2306-2325.

Marty, W., 2020. The Time Value of Money. In Fixed Income Analytics (pp. 5-17). Springer,

Cham.

1

Books and journals

Bai, B. and Wang, J., 2020. The role of growth mindset, self-efficacy and intrinsic value in self-

regulated learning and English language learning achievements. Language teaching

research, p.1362168820933190.

García-Monleón, F., Danvila-del-Valle, I. and Lara, F. J., 2021. Intrinsic value in crypto

currencies. Technological Forecasting and Social Change. 162. p.120393.

Irena, M. and Mariana, B., 2017. The Time Value of Money in Financial Management. Ovidius

University Annals, Economic Sciences Series. 17(2). pp.593-597.

Khechine, H., Raymond, B. and Augier, M., 2020. The adoption of a social learning system:

Intrinsic value in the UTAUT model. British Journal of Educational

Technology. 51(6). pp.2306-2325.

Marty, W., 2020. The Time Value of Money. In Fixed Income Analytics (pp. 5-17). Springer,

Cham.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.