Commercial Banking Technologies: Impact on US & Australian Banks

VerifiedAdded on 2023/06/14

|9

|2050

|383

Report

AI Summary

This report examines the impact of recent technological innovations on commercial banking, focusing on US and Australian financial institutions. It discusses how these technologies, including blockchain, digitization, automation, marketplace lending, and hybrid cloud, have influenced the net interest margins, profitability, and productivity of these institutions. The report further analyzes the ethical considerations and potential risks, such as data misuse and cyber security threats, associated with these advancements. While acknowledging these risks, the report concludes that the benefits, including improved services, increased customer base, and economies of scale, outweigh the challenges, leading to significant positive changes in the banking industry.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 07 April 2018.

1 | P a g e

By student name

Professor

University

Date: 07 April 2018.

1 | P a g e

2

Contents

Introduction.................................................................................................................................................3

Impact of the innovative technologies in US based financial institutions....................................................3

Impact of the innovative technologies in Australian based financial institutions........................................4

Ethical issues and common good analysis on the technological advancements..........................................6

Conclusion...................................................................................................................................................7

References...................................................................................................................................................8

2 | P a g e

Contents

Introduction.................................................................................................................................................3

Impact of the innovative technologies in US based financial institutions....................................................3

Impact of the innovative technologies in Australian based financial institutions........................................4

Ethical issues and common good analysis on the technological advancements..........................................6

Conclusion...................................................................................................................................................7

References...................................................................................................................................................8

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Introduction

In the given case, a research report has to be prepared on the commercial banking technologies

that have emerged off late and have become immensely important. The same has been discussed

in the below report where is shows that the technologies have not only helped in increasing the

net interest margins and other incomes of the financial institutions but also resulted in improving

the profitability and productivity as a whole (Alexander, 2016). The issue to be discussed here is

whether the technological improvements being taken in a positive way and how it has impacted

the US and Australian financial institutions in particular. Given the topic, the discussion has also

been done with respect to operating performance, inherent risks and difficulties in introducing

any financial innovation, how it results in economies of scale and its impact on risks of fraud and

crime (Belton, 2017).

Impact of the innovative technologies in US based financial institutions

The recent technology changes have impacted not only the retail banking market but also the

commercial banking, be it cash management services or working capital management.

Corporates have recognised that they are losing interest due to idle cash and thus now they find

the need to know the working capital and cash balance on real time basis. FIIs are investing big

time in technological investments to help corporates improve the efficiency of the business

(Chaudron, 2018). Banks and financial institutions are in the process of overhauling the back end

activities through digitization and automation of most of the jobs. They are using data analytics

to bring in new services like customer and vendor financing to help the mid and small sized

businesses and help growing the revenue and profitability of the bank. Some of the major

innovations that have come way in the US financial institutions are

1. Block chain technology: This has emerged as one of the greatest innovation of the era

removing the paper based trade finances. It is secured, transparent and gives the

authorization to the approved intermediaries over the network. It also reduces the counter

party default risk (Raghupathi & Wu, 2018).

3 | P a g e

Introduction

In the given case, a research report has to be prepared on the commercial banking technologies

that have emerged off late and have become immensely important. The same has been discussed

in the below report where is shows that the technologies have not only helped in increasing the

net interest margins and other incomes of the financial institutions but also resulted in improving

the profitability and productivity as a whole (Alexander, 2016). The issue to be discussed here is

whether the technological improvements being taken in a positive way and how it has impacted

the US and Australian financial institutions in particular. Given the topic, the discussion has also

been done with respect to operating performance, inherent risks and difficulties in introducing

any financial innovation, how it results in economies of scale and its impact on risks of fraud and

crime (Belton, 2017).

Impact of the innovative technologies in US based financial institutions

The recent technology changes have impacted not only the retail banking market but also the

commercial banking, be it cash management services or working capital management.

Corporates have recognised that they are losing interest due to idle cash and thus now they find

the need to know the working capital and cash balance on real time basis. FIIs are investing big

time in technological investments to help corporates improve the efficiency of the business

(Chaudron, 2018). Banks and financial institutions are in the process of overhauling the back end

activities through digitization and automation of most of the jobs. They are using data analytics

to bring in new services like customer and vendor financing to help the mid and small sized

businesses and help growing the revenue and profitability of the bank. Some of the major

innovations that have come way in the US financial institutions are

1. Block chain technology: This has emerged as one of the greatest innovation of the era

removing the paper based trade finances. It is secured, transparent and gives the

authorization to the approved intermediaries over the network. It also reduces the counter

party default risk (Raghupathi & Wu, 2018).

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

2. Digitization of the back office: With the advent of innovative technologies, banks and

financial institutions are trying to do away with the paper records and processing and

making it all digitized so that the entire process can be streamlined. This is not improving

productivity but helping in cost cutting (Davis, 2017).

3. Automation: This has made the most news as banks are now trying to limit all the human

interventions and manually driven processes in order to avoid scams and leverage the

work by improving the speed and accuracy of the operations and transaction processing.

4. Marketplace lender concept: In US, market place lenders are using various online

platforms to connect the borrowers or corporates in need of funds with the lenders or

investors of money which is enabling the transaction to be processed quickly and with

limited risks. This also enables the bank to increase its revenue by the way of commission

(Choy, 2018).

5. Hybrid Cloud technology: The cloud data services have helped the banks and financial

institutions to be agile and improve in terms of operational efficiency, faster processing

of payments and receipts, easy retrieval of data and customer master, security,

innovation, collaboration in ecosystem and finaly revenue and profit growth.

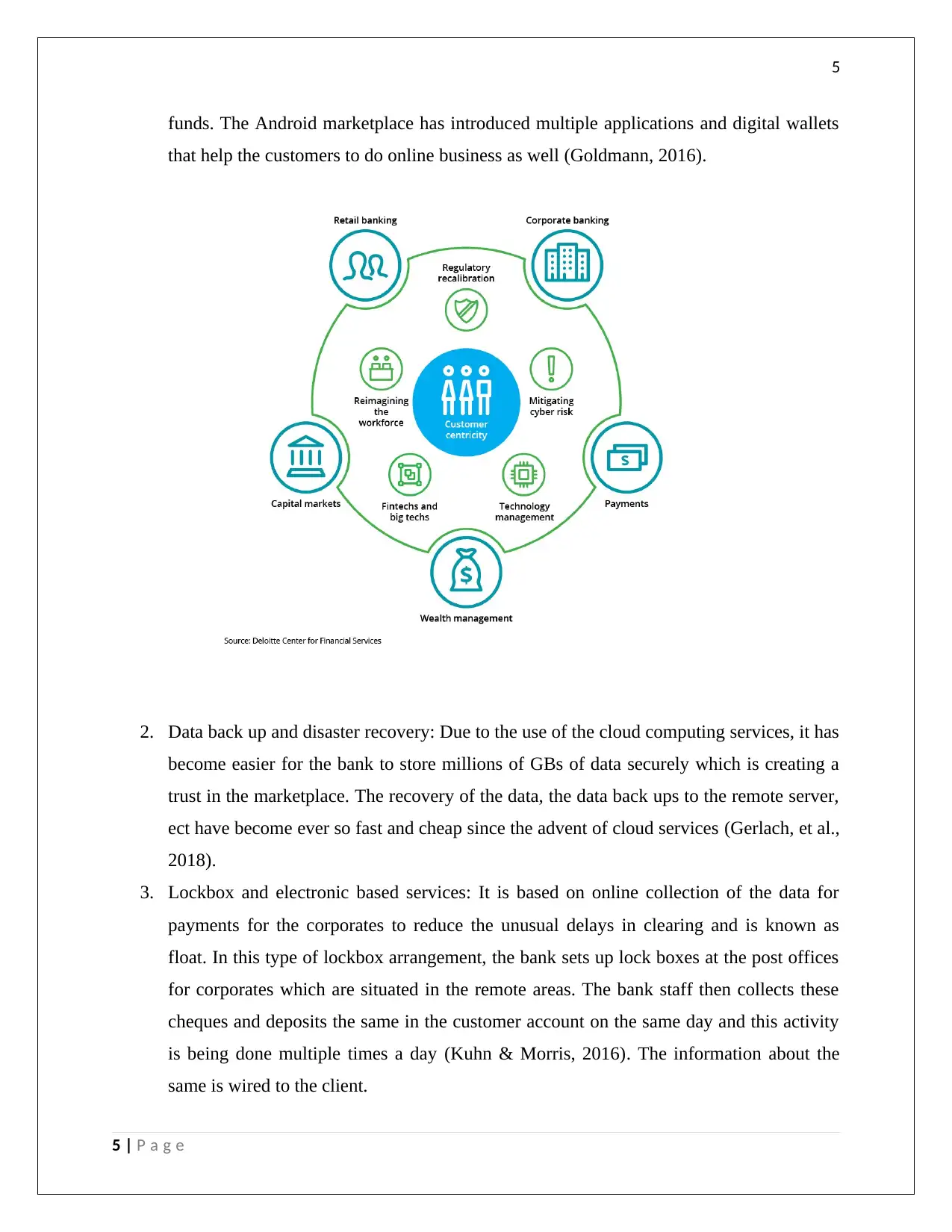

Impact of the innovative technologies in Australian based financial

institutions

The Australian banks and financial institutions have been other parties who have witnessed

multiple opportunities and risks with the growing technological advancements. The long term

growth has been targeted which involves mitigating the cyber risk, practising regulatory

recalibration under the umbrella of Australian laws, focusing on customer eccentricity and

redefining the workforce. The impact has been directly in the form of growth in GDP and

interest rates (Timothy, 2004). This has been sustainable and customers now are the only target

of the banks in terms of offering excellent and speedy services. Some of the innovative

technologies being used are:

1. Online banking and Mobile banking: This has helped the end customer off late to get the

funds anywhere at any time. This has also helped in reducing the risk of siphoning of

4 | P a g e

2. Digitization of the back office: With the advent of innovative technologies, banks and

financial institutions are trying to do away with the paper records and processing and

making it all digitized so that the entire process can be streamlined. This is not improving

productivity but helping in cost cutting (Davis, 2017).

3. Automation: This has made the most news as banks are now trying to limit all the human

interventions and manually driven processes in order to avoid scams and leverage the

work by improving the speed and accuracy of the operations and transaction processing.

4. Marketplace lender concept: In US, market place lenders are using various online

platforms to connect the borrowers or corporates in need of funds with the lenders or

investors of money which is enabling the transaction to be processed quickly and with

limited risks. This also enables the bank to increase its revenue by the way of commission

(Choy, 2018).

5. Hybrid Cloud technology: The cloud data services have helped the banks and financial

institutions to be agile and improve in terms of operational efficiency, faster processing

of payments and receipts, easy retrieval of data and customer master, security,

innovation, collaboration in ecosystem and finaly revenue and profit growth.

Impact of the innovative technologies in Australian based financial

institutions

The Australian banks and financial institutions have been other parties who have witnessed

multiple opportunities and risks with the growing technological advancements. The long term

growth has been targeted which involves mitigating the cyber risk, practising regulatory

recalibration under the umbrella of Australian laws, focusing on customer eccentricity and

redefining the workforce. The impact has been directly in the form of growth in GDP and

interest rates (Timothy, 2004). This has been sustainable and customers now are the only target

of the banks in terms of offering excellent and speedy services. Some of the innovative

technologies being used are:

1. Online banking and Mobile banking: This has helped the end customer off late to get the

funds anywhere at any time. This has also helped in reducing the risk of siphoning of

4 | P a g e

5

funds. The Android marketplace has introduced multiple applications and digital wallets

that help the customers to do online business as well (Goldmann, 2016).

2. Data back up and disaster recovery: Due to the use of the cloud computing services, it has

become easier for the bank to store millions of GBs of data securely which is creating a

trust in the marketplace. The recovery of the data, the data back ups to the remote server,

ect have become ever so fast and cheap since the advent of cloud services (Gerlach, et al.,

2018).

3. Lockbox and electronic based services: It is based on online collection of the data for

payments for the corporates to reduce the unusual delays in clearing and is known as

float. In this type of lockbox arrangement, the bank sets up lock boxes at the post offices

for corporates which are situated in the remote areas. The bank staff then collects these

cheques and deposits the same in the customer account on the same day and this activity

is being done multiple times a day (Kuhn & Morris, 2016). The information about the

same is wired to the client.

5 | P a g e

funds. The Android marketplace has introduced multiple applications and digital wallets

that help the customers to do online business as well (Goldmann, 2016).

2. Data back up and disaster recovery: Due to the use of the cloud computing services, it has

become easier for the bank to store millions of GBs of data securely which is creating a

trust in the marketplace. The recovery of the data, the data back ups to the remote server,

ect have become ever so fast and cheap since the advent of cloud services (Gerlach, et al.,

2018).

3. Lockbox and electronic based services: It is based on online collection of the data for

payments for the corporates to reduce the unusual delays in clearing and is known as

float. In this type of lockbox arrangement, the bank sets up lock boxes at the post offices

for corporates which are situated in the remote areas. The bank staff then collects these

cheques and deposits the same in the customer account on the same day and this activity

is being done multiple times a day (Kuhn & Morris, 2016). The information about the

same is wired to the client.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

4. Treasury management software: The banks have been using the treasury management

softwares which is much faster and accurate as compared to the manual means. As this is

risky and very sensitive area and involves a lot of investments and funds, banks have

installed a dedicated system to handle all the secure transactions. This is helped in

enabling ease of business services (Linden & Freeman, 2017).

5. Installation of ERP products and keeping it up to date: The ERP systems have brought

about a great deal of changes in the banking products and it helps in consolidation of the

data and thereby reporting of the profitability. This financial innovation has helped the

banks to derive economies of scale and reduce the cost incurred (Marques, 2018).

Ethical issues and common good analysis on the technological

advancements

With the rising advent in the area of technology and agility is services, there also comes ethical

concerns and the risks of misusing the customer data. When the clients data and ultra sensitive

information is being stored on the common server and on cloud, it also enhances the risk that the

same may be unutilised or may be leaked or may be used for unwarranted things. It is the

responsibility of the bank to make secure the same and protect it as the cloud technology as well

as the blockchain technology are something that is guided by logic and therefore, it can erupt and

cause leakage of data anytime. Besides this, there are many data which are kept or stored in the

common server and the same is accessible to a number of users therefore the banks needs to be

extra careful whie dealing with the same. This has also given rise to the crimes and the risks of

the fraud as it was seen that the debit and credit cards were hacked through other card material

and lots of funds were absconded through this. Therefore, online and mobile banking, the debit

and credit cards are need to be more secured and authenticated so that the security cannot be

breached easily.

However, there have been more positives than the quantum of risks and uncertainities being

offered by the innovations in technology. It has improved the services of the bank, the ease of

service for the customer, introduction of the various new banking products and services, the

agility and the speed of the services with which it is being offered. The commercial, retail as well

6 | P a g e

4. Treasury management software: The banks have been using the treasury management

softwares which is much faster and accurate as compared to the manual means. As this is

risky and very sensitive area and involves a lot of investments and funds, banks have

installed a dedicated system to handle all the secure transactions. This is helped in

enabling ease of business services (Linden & Freeman, 2017).

5. Installation of ERP products and keeping it up to date: The ERP systems have brought

about a great deal of changes in the banking products and it helps in consolidation of the

data and thereby reporting of the profitability. This financial innovation has helped the

banks to derive economies of scale and reduce the cost incurred (Marques, 2018).

Ethical issues and common good analysis on the technological

advancements

With the rising advent in the area of technology and agility is services, there also comes ethical

concerns and the risks of misusing the customer data. When the clients data and ultra sensitive

information is being stored on the common server and on cloud, it also enhances the risk that the

same may be unutilised or may be leaked or may be used for unwarranted things. It is the

responsibility of the bank to make secure the same and protect it as the cloud technology as well

as the blockchain technology are something that is guided by logic and therefore, it can erupt and

cause leakage of data anytime. Besides this, there are many data which are kept or stored in the

common server and the same is accessible to a number of users therefore the banks needs to be

extra careful whie dealing with the same. This has also given rise to the crimes and the risks of

the fraud as it was seen that the debit and credit cards were hacked through other card material

and lots of funds were absconded through this. Therefore, online and mobile banking, the debit

and credit cards are need to be more secured and authenticated so that the security cannot be

breached easily.

However, there have been more positives than the quantum of risks and uncertainities being

offered by the innovations in technology. It has improved the services of the bank, the ease of

service for the customer, introduction of the various new banking products and services, the

agility and the speed of the services with which it is being offered. The commercial, retail as well

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

as personal banking has been boosted with all these technological advancements and thereby

increased the margins and net interest income for the banks and the financial institutions. Also, it

has helped the banks to increase the customer base by reaching out to the areas where there are

connectivity issues.

Conclusion

From the above discussion and analysis on the varied technological innovations and

introductions in the banking and financial sector, it can be concluded that the same has had dual

effects. While it has brought about disruptive changes in the financial world with the blockchain

technology and cloud computing, it has also brought about the risks of hacking and cyber

security issues. The beneficiaries of all these have been the banks who have improved on the

balance sheet as well as the profit and loss statement over the years by increasing the customer

base and thereby net interest margin and other net income. It has resulted in economies of scale

all around the banking industry and is expected to bring further changes going forward.

7 | P a g e

as personal banking has been boosted with all these technological advancements and thereby

increased the margins and net interest income for the banks and the financial institutions. Also, it

has helped the banks to increase the customer base by reaching out to the areas where there are

connectivity issues.

Conclusion

From the above discussion and analysis on the varied technological innovations and

introductions in the banking and financial sector, it can be concluded that the same has had dual

effects. While it has brought about disruptive changes in the financial world with the blockchain

technology and cloud computing, it has also brought about the risks of hacking and cyber

security issues. The beneficiaries of all these have been the banks who have improved on the

balance sheet as well as the profit and loss statement over the years by increasing the customer

base and thereby net interest margin and other net income. It has resulted in economies of scale

all around the banking industry and is expected to bring further changes going forward.

7 | P a g e

8

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Chaudron, R., 2018. Bank's interest rate risk and profitability in a prolonged environment of low interest

rates. Journal of Banking and Finance, Volume 89, pp. 94-104.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, p. 145.

Davis, P., 2017. Value Investing: Do Quant Strategies Measure Up?. Financial Analysts Journal, pp. 1-172.

Gerlach, J., Mora, N. & Uysal, P., 2018. Bank funding costs in a rising interest rate environment. Journal

of Banking and Finance, Volume 87, pp. 164-186.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, Volume 4, pp. 103-112.

Kuhn, J. & Morris, B., 2016. IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Marques, R. P. F., 2018. Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, pp. 820-830.

Raghupathi, W. & Wu, S., 2018. The Strategic Association Between Information and Communication

Technologies and Sustainability: A Country-Level Study. IGI Global, disseminator of knowledge, p. 26.

Timothy, G., 2004. Managing interest rate risk in a rising rate environment. RMA Journal, Risk

Management Association (RMA), November.

8 | P a g e

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Chaudron, R., 2018. Bank's interest rate risk and profitability in a prolonged environment of low interest

rates. Journal of Banking and Finance, Volume 89, pp. 94-104.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, p. 145.

Davis, P., 2017. Value Investing: Do Quant Strategies Measure Up?. Financial Analysts Journal, pp. 1-172.

Gerlach, J., Mora, N. & Uysal, P., 2018. Bank funding costs in a rising interest rate environment. Journal

of Banking and Finance, Volume 87, pp. 164-186.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, Volume 4, pp. 103-112.

Kuhn, J. & Morris, B., 2016. IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Marques, R. P. F., 2018. Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, pp. 820-830.

Raghupathi, W. & Wu, S., 2018. The Strategic Association Between Information and Communication

Technologies and Sustainability: A Country-Level Study. IGI Global, disseminator of knowledge, p. 26.

Timothy, G., 2004. Managing interest rate risk in a rising rate environment. RMA Journal, Risk

Management Association (RMA), November.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.