Comprehensive Situational Analysis of Bankmed, Fall 2017, USJ-ISEB M1

VerifiedAdded on 2021/05/10

|36

|7867

|113

Report

AI Summary

This report presents a comprehensive situational analysis of Bankmed, a prominent Lebanese bank, examining its operations and financial standing. The analysis employs several strategic tools, including Porter's Five Forces to assess the competitive landscape, the 5 C's analysis to evaluate the company's internal and external environment, and the McKinsey 7-S framework to assess organizational effectiveness. A SWOT analysis is also included to identify the bank's strengths, weaknesses, opportunities, and threats. The report provides an overview of Bankmed's history, product lines, financial highlights from 2012 to 2016, and strategic initiatives. It delves into the political, economic, socio-cultural, and technological factors influencing the bank's performance. The report also assesses the competitive rivalry within the Lebanese banking sector, concluding with an in-depth evaluation of Bankmed's current position and strategic outlook. The report was prepared for a course at USJ-ISEB M1 in Fall 2017.

Situational Analysis of bankmed

Prepared by: Rim T. Ghandour

To: Professor Tony Jbeily

USJ-ISEB M1

Fall 2017

Prepared by: Rim T. Ghandour

To: Professor Tony Jbeily

USJ-ISEB M1

Fall 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

1. Introduction............................................................................................................................2

2. Porter 5 forces analysis...........................................................................................................4

2.1. Threat of New Entrants.......................................................................................................4

2.2. Power of Suppliers..............................................................................................................4

2.3. Power of Buyers..................................................................................................................4

2.4. Availability of Substitutes...................................................................................................5

2.5. Competitive Rivalry.............................................................................................................5

3. Bankmed 5 C’S Analysis..........................................................................................................6

3.1. Company.............................................................................................................................6

3.1.1. Profile.............................................................................................................................6

3.1.2. Financial highlights.........................................................................................................7

3.1.3. About Bankmed..............................................................................................................8

3.1.4. Product line...................................................................................................................10

3.2. Bankmed Expansion & Collaboration................................................................................12

3.3. Customers.........................................................................................................................15

3.4. Climate: PEST....................................................................................................................16

3.4.1. Political factors.............................................................................................................16

3.4.2. Economic factors...........................................................................................................17

3.4.3. Socio-cultural factors....................................................................................................18

3.4.4. Technological factors....................................................................................................19

3.5. Competitors......................................................................................................................20

4. The McKinsey 7-S..................................................................................................................21

4.1. Structure...........................................................................................................................21

4.1.1. Board of directors.........................................................................................................22

4.1.2. The Board Committees.................................................................................................23

4.1.3. Sound governance........................................................................................................24

4.2. System..............................................................................................................................24

4.3. Strategies..........................................................................................................................25

4.4. Skills..................................................................................................................................25

4.5. Style..................................................................................................................................25

1. Introduction............................................................................................................................2

2. Porter 5 forces analysis...........................................................................................................4

2.1. Threat of New Entrants.......................................................................................................4

2.2. Power of Suppliers..............................................................................................................4

2.3. Power of Buyers..................................................................................................................4

2.4. Availability of Substitutes...................................................................................................5

2.5. Competitive Rivalry.............................................................................................................5

3. Bankmed 5 C’S Analysis..........................................................................................................6

3.1. Company.............................................................................................................................6

3.1.1. Profile.............................................................................................................................6

3.1.2. Financial highlights.........................................................................................................7

3.1.3. About Bankmed..............................................................................................................8

3.1.4. Product line...................................................................................................................10

3.2. Bankmed Expansion & Collaboration................................................................................12

3.3. Customers.........................................................................................................................15

3.4. Climate: PEST....................................................................................................................16

3.4.1. Political factors.............................................................................................................16

3.4.2. Economic factors...........................................................................................................17

3.4.3. Socio-cultural factors....................................................................................................18

3.4.4. Technological factors....................................................................................................19

3.5. Competitors......................................................................................................................20

4. The McKinsey 7-S..................................................................................................................21

4.1. Structure...........................................................................................................................21

4.1.1. Board of directors.........................................................................................................22

4.1.2. The Board Committees.................................................................................................23

4.1.3. Sound governance........................................................................................................24

4.2. System..............................................................................................................................24

4.3. Strategies..........................................................................................................................25

4.4. Skills..................................................................................................................................25

4.5. Style..................................................................................................................................25

4.6. Staff...................................................................................................................................26

4.7. Shared values....................................................................................................................26

5. SWOT Analysis......................................................................................................................28

5.1. Strengths...........................................................................................................................29

5.2. Weaknesses......................................................................................................................30

5.3. Opportunities....................................................................................................................31

5.4. Threats..............................................................................................................................31

4.7. Shared values....................................................................................................................26

5. SWOT Analysis......................................................................................................................28

5.1. Strengths...........................................................................................................................29

5.2. Weaknesses......................................................................................................................30

5.3. Opportunities....................................................................................................................31

5.4. Threats..............................................................................................................................31

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Introduction

The Lebanese banking sector, financially sound and stable, plays a major

instrumental role in sustaining Lebanon's economic stability and prompting its

economy forward.

Representing 340 percent of Lebanon GDP, the banking sector is by far the most

important sector of the Lebanese economy.

Besides contributing the most to the GDP, the employment and the growth, it

continues to meet the financial needs of the economy, lending both private and

public sectors'.

It's important to precise that banks and other financial institutions in Lebanon are

under the jurisdiction of the Bank of Lebanon (BDL).

BDL's total reserves including gold, reached USD 55.9 billion. Its assets reached

117 billion with USD 11.9 billion in gold reserves as at end-September 2017.

Being the country's central bank, it is the bank regulatory authority, controlling

entries into the banking industry, defining the scope of banking activities and

setting prudential regulations and code of practice for banks.

Beside of BDL is the Banking control commission (BCC), who is responsible for

the supervision of banking activities by ensuring compliance with various

financial and banking rules and regulations. Banking activities are also subject to

both the Code of Commerce and the Code of Money and Credit.

Moreover, banks enlisted by the list of banks set up by BDL can be part of the

association of banks in Lebanon (ABL).

This association has important objectives such as strengthening the cooperation

of its member banks, representing them and defending collectively their interest

by working with the concerned authorities to find and develop the regulations and

promulgate the legislations. Also by enhancing the banking performance level

through improving the competences of its human resources and most importantly

reflecting a positive picture of the banking sector highlighting its fundamental role

in upholding the national economy.

The Lebanese banking sector, financially sound and stable, plays a major

instrumental role in sustaining Lebanon's economic stability and prompting its

economy forward.

Representing 340 percent of Lebanon GDP, the banking sector is by far the most

important sector of the Lebanese economy.

Besides contributing the most to the GDP, the employment and the growth, it

continues to meet the financial needs of the economy, lending both private and

public sectors'.

It's important to precise that banks and other financial institutions in Lebanon are

under the jurisdiction of the Bank of Lebanon (BDL).

BDL's total reserves including gold, reached USD 55.9 billion. Its assets reached

117 billion with USD 11.9 billion in gold reserves as at end-September 2017.

Being the country's central bank, it is the bank regulatory authority, controlling

entries into the banking industry, defining the scope of banking activities and

setting prudential regulations and code of practice for banks.

Beside of BDL is the Banking control commission (BCC), who is responsible for

the supervision of banking activities by ensuring compliance with various

financial and banking rules and regulations. Banking activities are also subject to

both the Code of Commerce and the Code of Money and Credit.

Moreover, banks enlisted by the list of banks set up by BDL can be part of the

association of banks in Lebanon (ABL).

This association has important objectives such as strengthening the cooperation

of its member banks, representing them and defending collectively their interest

by working with the concerned authorities to find and develop the regulations and

promulgate the legislations. Also by enhancing the banking performance level

through improving the competences of its human resources and most importantly

reflecting a positive picture of the banking sector highlighting its fundamental role

in upholding the national economy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Over the past decade, the Lebanese banking sector witnessed several

transformations, moving from a highly fragmented market to a somewhat

consolidated environment thanks to the central bank high requirements and

restrictions regarding the yearly opening of new branches.

Given that the Lebanese sector is overbanked, and due to the restrictions set by

the Central Bank, we believe that there is a room for a much more consolidated

environment reached through the acquisition of local banks by well-capitalized

large banking groups.

It’s important to share that the implementation of a strategic management system

is crucial to the survival of all organizations.

In the following situational analysis of Bankmed, we will intend to build a study of

the organization using many powerful tools to determine its current situation and

to help us propose consolidation and improvement actions.

transformations, moving from a highly fragmented market to a somewhat

consolidated environment thanks to the central bank high requirements and

restrictions regarding the yearly opening of new branches.

Given that the Lebanese sector is overbanked, and due to the restrictions set by

the Central Bank, we believe that there is a room for a much more consolidated

environment reached through the acquisition of local banks by well-capitalized

large banking groups.

It’s important to share that the implementation of a strategic management system

is crucial to the survival of all organizations.

In the following situational analysis of Bankmed, we will intend to build a study of

the organization using many powerful tools to determine its current situation and

to help us propose consolidation and improvement actions.

2. Porter 5 forces analysis

2.1. Threat of New Entrants

The biggest barrier of entry for the banking industry is trust, because the industry

deals with others money so people are more willing to place their trust with a well

known bank not with a new bank.

Also there are other factors such as the strict regulations and the international

compliance. To conclude, the barriers to entry are high for the banking industry.

2.2. Power of Suppliers

The primary resource of any bank is the capital. By this capital banks are able to

successfully respond to their customers borrowing needs while maintaining

enough liquidly and capital to meet withdrawal expectations.

There are four major suppliers of capital in the banking industry: Customer

deposits, mortgages and loans, mortgages-baked securities, loans from other

financial institutions. The power of supplier is based on the market, their power

fluctuate between medium to high.

2.3. Power of Buyers

The major factor affecting the power of buyers is the high switching costs.

If a person has one bank taking in charge all his banking needs (saving,

mortgage, checking, etc) it can be very annoying for him to switch to another

bank. But the internet has greatly increased the power of the consumer by

reducing the cost of comparing the prices of opening and holding accounts as

well as the rates offered by banks.

2.1. Threat of New Entrants

The biggest barrier of entry for the banking industry is trust, because the industry

deals with others money so people are more willing to place their trust with a well

known bank not with a new bank.

Also there are other factors such as the strict regulations and the international

compliance. To conclude, the barriers to entry are high for the banking industry.

2.2. Power of Suppliers

The primary resource of any bank is the capital. By this capital banks are able to

successfully respond to their customers borrowing needs while maintaining

enough liquidly and capital to meet withdrawal expectations.

There are four major suppliers of capital in the banking industry: Customer

deposits, mortgages and loans, mortgages-baked securities, loans from other

financial institutions. The power of supplier is based on the market, their power

fluctuate between medium to high.

2.3. Power of Buyers

The major factor affecting the power of buyers is the high switching costs.

If a person has one bank taking in charge all his banking needs (saving,

mortgage, checking, etc) it can be very annoying for him to switch to another

bank. But the internet has greatly increased the power of the consumer by

reducing the cost of comparing the prices of opening and holding accounts as

well as the rates offered by banks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

By this, we can admit that the power of buyer is relatively low to medium.

2.4. Availability of Substitutes

The largest threat for the banking industry is the threat of substitutes.

The industry suffers from non-banking companies offering some banking

services as insurances, mutual funds, fixed income securities or offering payment

method substitutes and loan. Often these non-banking companies offers interest

rates on payment lower then banks. The threat of availability of substitutes varies

from medium to high.

2.5. Competitive Rivalry

The banking competition is high because everyone who needs banking services

already has them. Because of this, banks attempt to attract customers from other

banks by many ways such as offering lower financing, higher rates, investment

services, and greater conveniences than competitors.

It’s all about which bank can offer both the best and fastest services, which has

caused banks to experience a lower ROA.

2.4. Availability of Substitutes

The largest threat for the banking industry is the threat of substitutes.

The industry suffers from non-banking companies offering some banking

services as insurances, mutual funds, fixed income securities or offering payment

method substitutes and loan. Often these non-banking companies offers interest

rates on payment lower then banks. The threat of availability of substitutes varies

from medium to high.

2.5. Competitive Rivalry

The banking competition is high because everyone who needs banking services

already has them. Because of this, banks attempt to attract customers from other

banks by many ways such as offering lower financing, higher rates, investment

services, and greater conveniences than competitors.

It’s all about which bank can offer both the best and fastest services, which has

caused banks to experience a lower ROA.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Bankmed 5 C’S Analysis

3.1. Company

3.1.1. Profile

Bank Name: Bankmed S.A.L

Ownership: GROUPMED HOLDING SAL

Chairman & General Manager: Mohammed Hariri

Executive General Manager: Mohamed Ali Beyhum

Head Office Clemenceau Beirut, Lebanon

Date of Establishment 1944

Number of Staff 2,658, 51.20% males and 48.80% females

Local ATMs: 131

Local Branches: 66

Overseas branches: 05 (Limassol, Baghdad, Basra, Erbil, Dubai)

Subsidiaries: 13

3.1. Company

3.1.1. Profile

Bank Name: Bankmed S.A.L

Ownership: GROUPMED HOLDING SAL

Chairman & General Manager: Mohammed Hariri

Executive General Manager: Mohamed Ali Beyhum

Head Office Clemenceau Beirut, Lebanon

Date of Establishment 1944

Number of Staff 2,658, 51.20% males and 48.80% females

Local ATMs: 131

Local Branches: 66

Overseas branches: 05 (Limassol, Baghdad, Basra, Erbil, Dubai)

Subsidiaries: 13

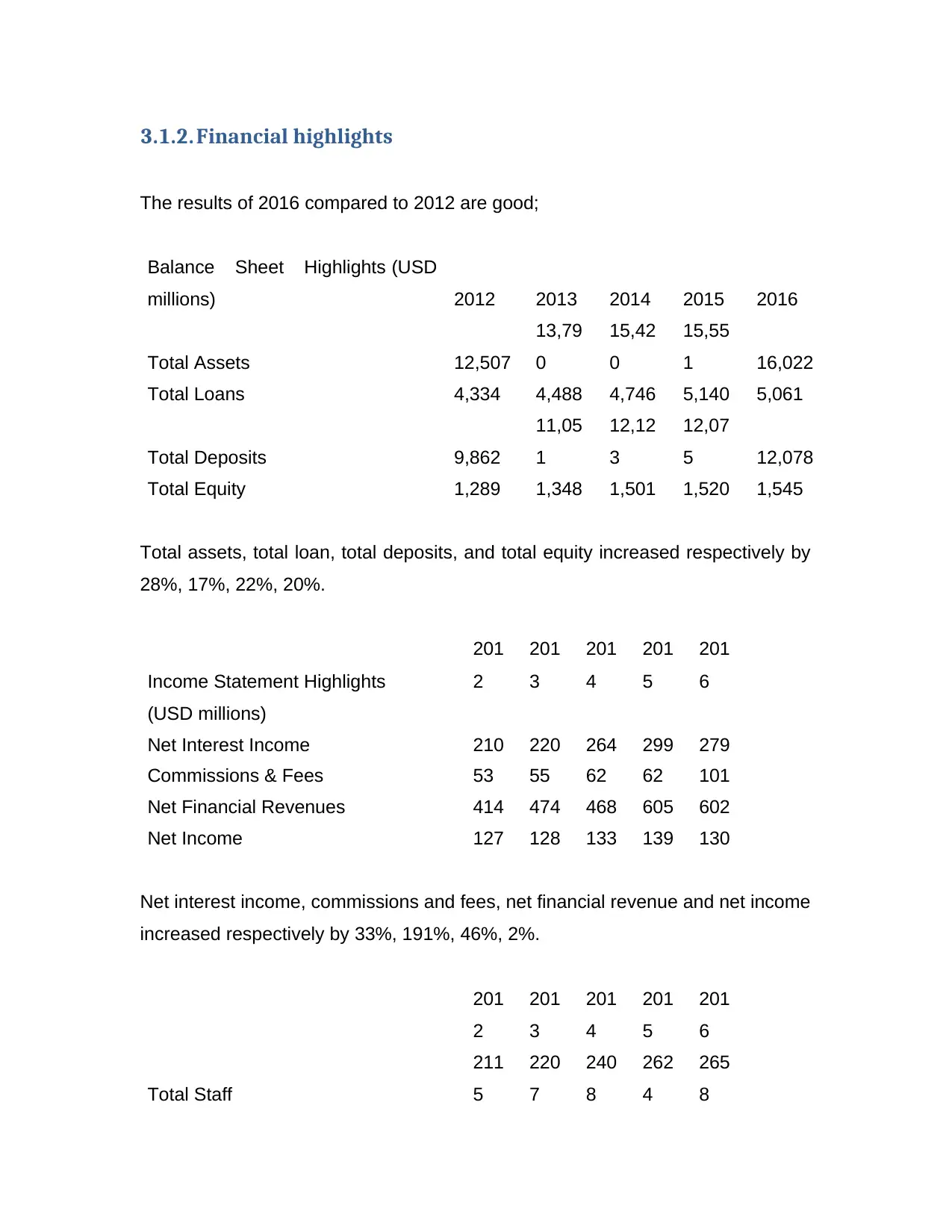

3.1.2. Financial highlights

The results of 2016 compared to 2012 are good;

Balance Sheet Highlights (USD

millions) 2012 2013 2014 2015 2016

Total Assets 12,507

13,79

0

15,42

0

15,55

1 16,022

Total Loans 4,334 4,488 4,746 5,140 5,061

Total Deposits 9,862

11,05

1

12,12

3

12,07

5 12,078

Total Equity 1,289 1,348 1,501 1,520 1,545

Total assets, total loan, total deposits, and total equity increased respectively by

28%, 17%, 22%, 20%.

Income Statement Highlights

201

2

201

3

201

4

201

5

201

6

(USD millions)

Net Interest Income 210 220 264 299 279

Commissions & Fees 53 55 62 62 101

Net Financial Revenues 414 474 468 605 602

Net Income 127 128 133 139 130

Net interest income, commissions and fees, net financial revenue and net income

increased respectively by 33%, 191%, 46%, 2%.

201

2

201

3

201

4

201

5

201

6

Total Staff

211

5

220

7

240

8

262

4

265

8

The results of 2016 compared to 2012 are good;

Balance Sheet Highlights (USD

millions) 2012 2013 2014 2015 2016

Total Assets 12,507

13,79

0

15,42

0

15,55

1 16,022

Total Loans 4,334 4,488 4,746 5,140 5,061

Total Deposits 9,862

11,05

1

12,12

3

12,07

5 12,078

Total Equity 1,289 1,348 1,501 1,520 1,545

Total assets, total loan, total deposits, and total equity increased respectively by

28%, 17%, 22%, 20%.

Income Statement Highlights

201

2

201

3

201

4

201

5

201

6

(USD millions)

Net Interest Income 210 220 264 299 279

Commissions & Fees 53 55 62 62 101

Net Financial Revenues 414 474 468 605 602

Net Income 127 128 133 139 130

Net interest income, commissions and fees, net financial revenue and net income

increased respectively by 33%, 191%, 46%, 2%.

201

2

201

3

201

4

201

5

201

6

Total Staff

211

5

220

7

240

8

262

4

265

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

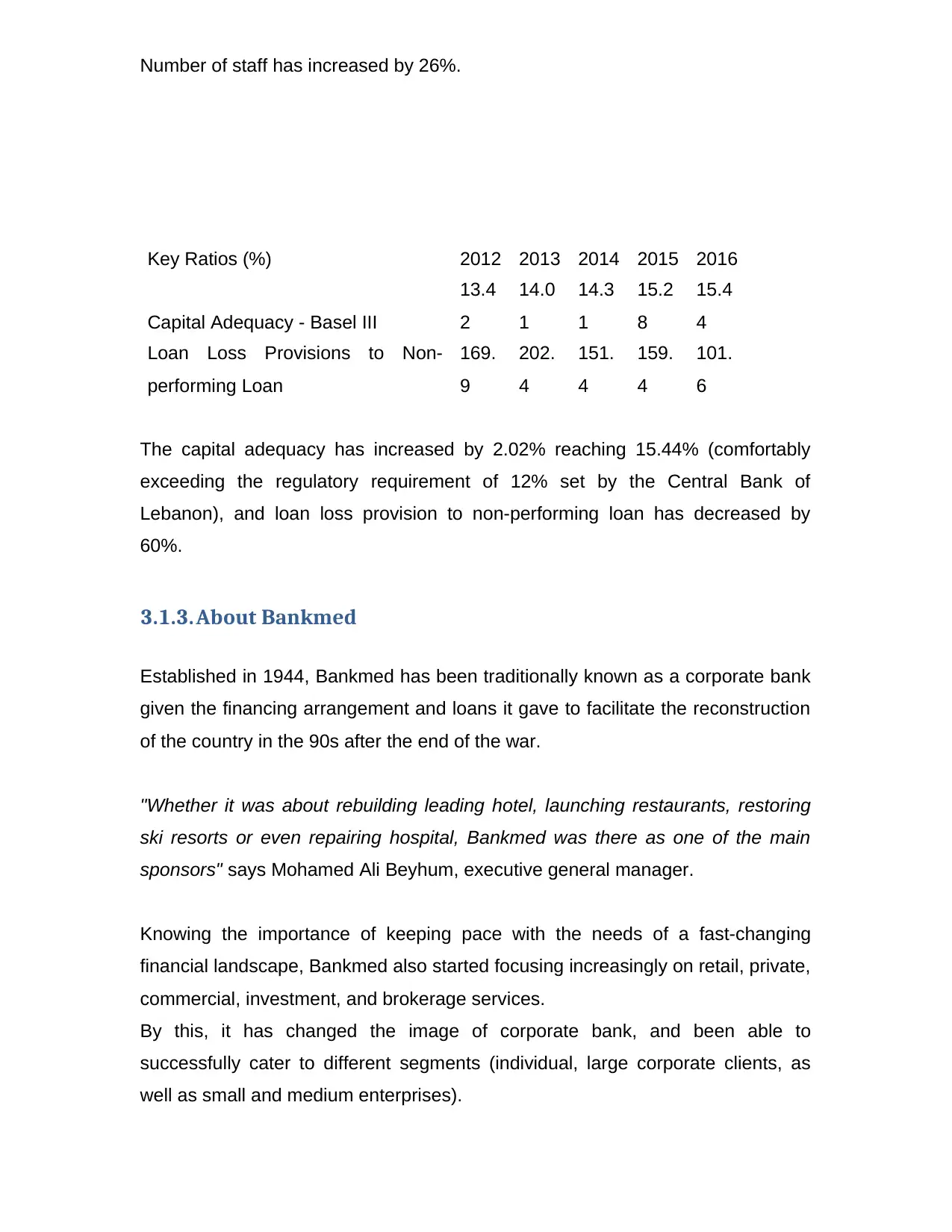

Number of staff has increased by 26%.

Key Ratios (%) 2012 2013 2014 2015 2016

Capital Adequacy - Basel III

13.4

2

14.0

1

14.3

1

15.2

8

15.4

4

Loan Loss Provisions to Non-

performing Loan

169.

9

202.

4

151.

4

159.

4

101.

6

The capital adequacy has increased by 2.02% reaching 15.44% (comfortably

exceeding the regulatory requirement of 12% set by the Central Bank of

Lebanon), and loan loss provision to non-performing loan has decreased by

60%.

3.1.3. About Bankmed

Established in 1944, Bankmed has been traditionally known as a corporate bank

given the financing arrangement and loans it gave to facilitate the reconstruction

of the country in the 90s after the end of the war.

"Whether it was about rebuilding leading hotel, launching restaurants, restoring

ski resorts or even repairing hospital, Bankmed was there as one of the main

sponsors" says Mohamed Ali Beyhum, executive general manager.

Knowing the importance of keeping pace with the needs of a fast-changing

financial landscape, Bankmed also started focusing increasingly on retail, private,

commercial, investment, and brokerage services.

By this, it has changed the image of corporate bank, and been able to

successfully cater to different segments (individual, large corporate clients, as

well as small and medium enterprises).

Key Ratios (%) 2012 2013 2014 2015 2016

Capital Adequacy - Basel III

13.4

2

14.0

1

14.3

1

15.2

8

15.4

4

Loan Loss Provisions to Non-

performing Loan

169.

9

202.

4

151.

4

159.

4

101.

6

The capital adequacy has increased by 2.02% reaching 15.44% (comfortably

exceeding the regulatory requirement of 12% set by the Central Bank of

Lebanon), and loan loss provision to non-performing loan has decreased by

60%.

3.1.3. About Bankmed

Established in 1944, Bankmed has been traditionally known as a corporate bank

given the financing arrangement and loans it gave to facilitate the reconstruction

of the country in the 90s after the end of the war.

"Whether it was about rebuilding leading hotel, launching restaurants, restoring

ski resorts or even repairing hospital, Bankmed was there as one of the main

sponsors" says Mohamed Ali Beyhum, executive general manager.

Knowing the importance of keeping pace with the needs of a fast-changing

financial landscape, Bankmed also started focusing increasingly on retail, private,

commercial, investment, and brokerage services.

By this, it has changed the image of corporate bank, and been able to

successfully cater to different segments (individual, large corporate clients, as

well as small and medium enterprises).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The market share of Bankmed has grown over the years and comprises

nowadays almost 10 percent of the total Lebanese banking system.

Keeping in mind the importance of diversification, Bankmed has been boosting

lending the small and middle market by signing an agreement with the Overseas

Private Investment Corporation (Opic) and Kafalat (a loan guarantee company

established by the government).

However, corporate banking is still the major activity of Bankmed as it holds one

of the major lending portfolios in the Lebanese market, having top tier corporate

clients and covering different industries. The commercial lending portfolio of

Bankmed witnessed considerable growth (25%) even during the spite of regional

turmoil and its financial consequences in 2011.

Bankmed has managed to expand its customer base and attract new client by

establishing an International Banking Business entity in order to serve its

customers outside Lebanon.

Taking into consideration the increasing demand on trade finance, Bankmed has

put efforts towards enhancing this opportunity. Thanks to its strong network

banking partners consisting of more than 70 names in over 55 countries, it has

been able to successfully expand its trade finance on both primary and

secondarily markets.

On the 27th of October 2016 it has successfully established its $500 Million Short

Term Certificates of Deposit Program (rated C (short-term) / B- (long term)

by S&P), marking the first Short Term Certificates of Deposit Program

established by a Lebanese bank in the international markets.

The Program is listed on the Luxembourg Stock Exchange, for now they will be

no initial sale or marketing of the Certificates in Lebanon.

By the end of 2016, bankmed's total assets stood at million US$16,022 (at

ex.rate 1508.00) it had customer deposits of US$ 12,078 and total loans of just

over US$5,061.

nowadays almost 10 percent of the total Lebanese banking system.

Keeping in mind the importance of diversification, Bankmed has been boosting

lending the small and middle market by signing an agreement with the Overseas

Private Investment Corporation (Opic) and Kafalat (a loan guarantee company

established by the government).

However, corporate banking is still the major activity of Bankmed as it holds one

of the major lending portfolios in the Lebanese market, having top tier corporate

clients and covering different industries. The commercial lending portfolio of

Bankmed witnessed considerable growth (25%) even during the spite of regional

turmoil and its financial consequences in 2011.

Bankmed has managed to expand its customer base and attract new client by

establishing an International Banking Business entity in order to serve its

customers outside Lebanon.

Taking into consideration the increasing demand on trade finance, Bankmed has

put efforts towards enhancing this opportunity. Thanks to its strong network

banking partners consisting of more than 70 names in over 55 countries, it has

been able to successfully expand its trade finance on both primary and

secondarily markets.

On the 27th of October 2016 it has successfully established its $500 Million Short

Term Certificates of Deposit Program (rated C (short-term) / B- (long term)

by S&P), marking the first Short Term Certificates of Deposit Program

established by a Lebanese bank in the international markets.

The Program is listed on the Luxembourg Stock Exchange, for now they will be

no initial sale or marketing of the Certificates in Lebanon.

By the end of 2016, bankmed's total assets stood at million US$16,022 (at

ex.rate 1508.00) it had customer deposits of US$ 12,078 and total loans of just

over US$5,061.

3.1.4. Product line

Bankmed S.A.L provides commercial and private banking products and services

to personal and business customers.

By continuously introducing unique retail product and services tailor-made to

customer’s individual needs, Bankmed’s retail banking has considerably grown

and its delivery channels has enhanced by adding new branches and entering

new markets.

Besides retail, Bankmed has offered to its customer wide chances to invest by

giving them access to local, regional and international markets through its

extensive and solid relationships with brokers and market makers around the

world. Bankmed’s treasury focused its efforts on structuring and marketing

different hedging and investment products. Also, a brokerage services is

available 24 hours a day has been handled by the bank’s wholly-owned

subsidiary (MedSecurities) introducing new investment products and services.

Products

Current and savings accounts, payroll accounts, safe boxes, loans (house, car

and personal), credit and debit cards, prepaid cards, business loans, overdrafts,

trade finance, subsidized loans, working capital financing and other facilities.

Services

Syndication services, wealth management and brokerage, investment banking

and treasury services, insurance brokerage services, corporate finance advisory

and asset management services, online and mobile banking services, merchant

services and real estate management services.

Bankmed S.A.L provides commercial and private banking products and services

to personal and business customers.

By continuously introducing unique retail product and services tailor-made to

customer’s individual needs, Bankmed’s retail banking has considerably grown

and its delivery channels has enhanced by adding new branches and entering

new markets.

Besides retail, Bankmed has offered to its customer wide chances to invest by

giving them access to local, regional and international markets through its

extensive and solid relationships with brokers and market makers around the

world. Bankmed’s treasury focused its efforts on structuring and marketing

different hedging and investment products. Also, a brokerage services is

available 24 hours a day has been handled by the bank’s wholly-owned

subsidiary (MedSecurities) introducing new investment products and services.

Products

Current and savings accounts, payroll accounts, safe boxes, loans (house, car

and personal), credit and debit cards, prepaid cards, business loans, overdrafts,

trade finance, subsidized loans, working capital financing and other facilities.

Services

Syndication services, wealth management and brokerage, investment banking

and treasury services, insurance brokerage services, corporate finance advisory

and asset management services, online and mobile banking services, merchant

services and real estate management services.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 36

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.