BAO2202 - Financial Accounting Report: Intangibles, Liabilities, Tax

VerifiedAdded on 2023/04/03

|24

|4755

|158

Report

AI Summary

This report critically evaluates the disclosures related to intangible assets, liabilities, and income tax of Myer Holdings Limited and Adelaide Brighton Limited, assessing their compliance with Australian Accounting Standards. The analysis involves reviewing the companies' 2018 annual reports, focusing on accounting policies and associated disclosures. The report examines the concept of a reporting entity, compares liabilities and intangible asset disclosures, and evaluates the disclosure of benefits, income tax expenses, and obligations. The study finds that while both organizations make assumptions and estimates in accordance with applicable standards, Myer Holdings provides more detailed disclosures of contingent liabilities and provisions compared to Adelaide Brighton. The report concludes by offering recommendations to enhance the transparency and usefulness of accounting information, highlighting the importance of adhering to general purpose financial reporting frameworks for effective decision-making by stakeholders.

Running head: FINANCIAL ACCOUNTING

Financial accounting

Name of the student

Name of the university

Student ID

Author note

Financial accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING

Executive summary:

The report demonstrate the critical evaluation of the disclosures related to intangible assets,

liabilities and income tax whether they are in compliance with the relevant accounting

standards of Australia. For the analysis purpose, Myer holdings limited and Adelaide

Brighton limited is selected from retail sector and material sector respectively. The evaluation

of the accounting policy and the associated disclosures are done by reviewing the annual

report for the financial year 2018. After the analysis of each section, the report also outlines

the recommendation concerning the accounts explained and its contribution to the

transparency and usefulness of accounting information.

Executive summary:

The report demonstrate the critical evaluation of the disclosures related to intangible assets,

liabilities and income tax whether they are in compliance with the relevant accounting

standards of Australia. For the analysis purpose, Myer holdings limited and Adelaide

Brighton limited is selected from retail sector and material sector respectively. The evaluation

of the accounting policy and the associated disclosures are done by reviewing the annual

report for the financial year 2018. After the analysis of each section, the report also outlines

the recommendation concerning the accounts explained and its contribution to the

transparency and usefulness of accounting information.

FINANCIAL ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................5

Evaluating the concept of reporting entity in the creation of quality information for financial

statements users:.........................................................................................................................5

Evaluating the compliance of the firms with the relevant accounting standard by comparing

the liabilities disclosure:.............................................................................................................7

Evaluating the compliance of the firms with the relevant accounting standard by comparing

the disclosure of intangible assets:...........................................................................................11

Evaluating the compliance of the firms with the relevant accounting standard by comparing

the disclosure of benefits, income tax expense and obligations:.............................................15

Conclusion:..............................................................................................................................19

References list:.........................................................................................................................20

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................5

Evaluating the concept of reporting entity in the creation of quality information for financial

statements users:.........................................................................................................................5

Evaluating the compliance of the firms with the relevant accounting standard by comparing

the liabilities disclosure:.............................................................................................................7

Evaluating the compliance of the firms with the relevant accounting standard by comparing

the disclosure of intangible assets:...........................................................................................11

Evaluating the compliance of the firms with the relevant accounting standard by comparing

the disclosure of benefits, income tax expense and obligations:.............................................15

Conclusion:..............................................................................................................................19

References list:.........................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING

Introduction:

The study elucidates the effects of the legal needs of the organizations listed on the

Australian stock exchange to conform to the financial reporting standards of Australia. It

demonstrates the compliance of the publically listed organizations to the relevant accounting

standards in various areas such as liabilities, leasing, earning per share, tax effect accounting

and intangibles. Reporting entity are required to make a reasonable expectation of the fact

that the users uses the framework of general purpose financial report to obtain an

understanding of the overall financial performance of entity. Assessment of the information

presented according to the reporting framework helps users in assuring the facts that

information have been represented faithfully. Such users can be employees, shareholder,

lenders, creditors and potential investors. It is essential for the entity to document whether

they have users who are dependent on assessing the entity as per the general purpose

financial reporting with the help of people charged with the governance (Efrag.org 2019).

The report prepared demonstrate the evaluation of compliance of reporting entire with the

relevant accounting standard in terms of contingent liabilities, intangible assets, earning per

share and taxation effect. For the analysis purpose, two companies have been chosen from

different industries that are Myer Holding limited from Retail industry and Adelaide Brighton

limited from Material industry.

For explaining the compliance of the reporting standards by different companies, it is

essential to discuss briefly the overview. Adelaide Brighton limited is a manufacturing

company based in Australia that is involved in the manufacturing of lime, cement and dry

blended products. Myer Holdings on other hand is a department store company that is based

in Australia and owns a designer brand for women’s wear and bide and sass. The evaluation

Introduction:

The study elucidates the effects of the legal needs of the organizations listed on the

Australian stock exchange to conform to the financial reporting standards of Australia. It

demonstrates the compliance of the publically listed organizations to the relevant accounting

standards in various areas such as liabilities, leasing, earning per share, tax effect accounting

and intangibles. Reporting entity are required to make a reasonable expectation of the fact

that the users uses the framework of general purpose financial report to obtain an

understanding of the overall financial performance of entity. Assessment of the information

presented according to the reporting framework helps users in assuring the facts that

information have been represented faithfully. Such users can be employees, shareholder,

lenders, creditors and potential investors. It is essential for the entity to document whether

they have users who are dependent on assessing the entity as per the general purpose

financial reporting with the help of people charged with the governance (Efrag.org 2019).

The report prepared demonstrate the evaluation of compliance of reporting entire with the

relevant accounting standard in terms of contingent liabilities, intangible assets, earning per

share and taxation effect. For the analysis purpose, two companies have been chosen from

different industries that are Myer Holding limited from Retail industry and Adelaide Brighton

limited from Material industry.

For explaining the compliance of the reporting standards by different companies, it is

essential to discuss briefly the overview. Adelaide Brighton limited is a manufacturing

company based in Australia that is involved in the manufacturing of lime, cement and dry

blended products. Myer Holdings on other hand is a department store company that is based

in Australia and owns a designer brand for women’s wear and bide and sass. The evaluation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING

of the compliance of the companies with the relevant accounting standards are discussed in

the section below.

Discussion:

Evaluating the concept of reporting entity in the creation of quality information for

financial statements users:

The existing regulations and legislation specifying the entities about general purpose

financial reporting have number of implicit alternative reporting entity concepts. The concept

of reporting entity is associated with the objective of general purpose financial reporting

which requires the entities to prepare the general purpose financial report if they are

dependent upon it. Users will be provided assistance in determining the financial position and

performance of reporting entity with the help of disclosures of the industry and the

consequence of deployment. Therefore, it is essential for the reporting entity to deploy the

information for managing the resources with the help of administrative or legal structure. It is

evident from the reporting entity concept that is reflected in the statement that the creation of

company does not mean that they would qualify as the reporting entity. The objective of

preparing the general purpose financial report is associated with the dependence of user on

the report for evaluating and making decisions relating to the allocation of resources (Simnett

and Huggins 2015).

The concepts of reporting entity developed through the financial reporting framework

helps in making the reporting and financial accounting logical and consistent, enabling the

overall enhanced communication and economic development of accounting and increasing

consistent by enhancing the compatibility of the standards. In addition to this, there is a

of the compliance of the companies with the relevant accounting standards are discussed in

the section below.

Discussion:

Evaluating the concept of reporting entity in the creation of quality information for

financial statements users:

The existing regulations and legislation specifying the entities about general purpose

financial reporting have number of implicit alternative reporting entity concepts. The concept

of reporting entity is associated with the objective of general purpose financial reporting

which requires the entities to prepare the general purpose financial report if they are

dependent upon it. Users will be provided assistance in determining the financial position and

performance of reporting entity with the help of disclosures of the industry and the

consequence of deployment. Therefore, it is essential for the reporting entity to deploy the

information for managing the resources with the help of administrative or legal structure. It is

evident from the reporting entity concept that is reflected in the statement that the creation of

company does not mean that they would qualify as the reporting entity. The objective of

preparing the general purpose financial report is associated with the dependence of user on

the report for evaluating and making decisions relating to the allocation of resources (Simnett

and Huggins 2015).

The concepts of reporting entity developed through the financial reporting framework

helps in making the reporting and financial accounting logical and consistent, enabling the

overall enhanced communication and economic development of accounting and increasing

consistent by enhancing the compatibility of the standards. In addition to this, there is a

FINANCIAL ACCOUNTING

significant contribution of the concept of reporting entity to the public confidence and in the

credibility of the financial information. Such reporting framework tends to emphasize on the

information usefulness that is contained in the financial report that is considered significant

for the users. However, there is criticizing of the focus of accounting principles on the

transactions and economic phenomenon that is expressed in monetary values (Aasb.gov.au

2019). It has been ascertained that the high quality of reporting helps users in providing

information that is relevant for making decisions and representing the economic reality of the

activities of company along with its financial condition in a faithful manner.

The current study on the importance of the reporting entity concepts is significant

because of continued growth of research in this particular area. This is in relation to the

substantial debate surrounding the implications of the approach of principle based concept to

the reporting entity and its potential impacts. It is pointed out by the researcher that there are

subjective issues in the basis of concept of reporting entity and this have a consequence on

the decision making of the individual. Nevertheless, the adopters and practitioner acts

genuinely and objectively in their compliance with the reporting framework which does not

results in generating significant cause of concern (Aasb.gov.au 2019). Furthermore, due to

the differential use of reporting methods, there is an impact on the quality of financial

reporting as well along with the concern of level of compliance. Therefore, accounting for

such issues would create an impact of the quality of the financial information provided by

reporting entity to the users of the financial statements. Some other researchers have also

presented the basis of arguments that the principle based approach of reporting entity does

not make any significant differences in the outcome of reporting. From the analysis of

different case studies by the researchers found that the concept of reporting entity is not

appropriately applied. Since the reporting entity concept is based on the principle, it is

essential to make choices that are made in the key financial information reporting. In such

significant contribution of the concept of reporting entity to the public confidence and in the

credibility of the financial information. Such reporting framework tends to emphasize on the

information usefulness that is contained in the financial report that is considered significant

for the users. However, there is criticizing of the focus of accounting principles on the

transactions and economic phenomenon that is expressed in monetary values (Aasb.gov.au

2019). It has been ascertained that the high quality of reporting helps users in providing

information that is relevant for making decisions and representing the economic reality of the

activities of company along with its financial condition in a faithful manner.

The current study on the importance of the reporting entity concepts is significant

because of continued growth of research in this particular area. This is in relation to the

substantial debate surrounding the implications of the approach of principle based concept to

the reporting entity and its potential impacts. It is pointed out by the researcher that there are

subjective issues in the basis of concept of reporting entity and this have a consequence on

the decision making of the individual. Nevertheless, the adopters and practitioner acts

genuinely and objectively in their compliance with the reporting framework which does not

results in generating significant cause of concern (Aasb.gov.au 2019). Furthermore, due to

the differential use of reporting methods, there is an impact on the quality of financial

reporting as well along with the concern of level of compliance. Therefore, accounting for

such issues would create an impact of the quality of the financial information provided by

reporting entity to the users of the financial statements. Some other researchers have also

presented the basis of arguments that the principle based approach of reporting entity does

not make any significant differences in the outcome of reporting. From the analysis of

different case studies by the researchers found that the concept of reporting entity is not

appropriately applied. Since the reporting entity concept is based on the principle, it is

essential to make choices that are made in the key financial information reporting. In such

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING

situation, any choices made by reporting entity to increase the relevance may results in

reducing the reliability of the information and users may not find high reliable information

relevant. Despite the fact of some issues associated with the reporting entity concept, it has

been found that the entities adopting the concept of reporting entities tends to provide

financial information that are of higher quality (Velte and Stawinoga 2017.). With regarding

the compliance issues faced by the firm, the rate of adopting the general purpose financial

reporting framework by the firm is lower that it probably should be. Therefore, from the

analysis of the reviews presented in the literature, it is inferred that the concept of reporting

entity helps in providing higher quality financial information though, there some areas where

it lacks in presentation if the financial information that helps in forming the decision making

of the users.

Evaluating the compliance of the firms with the relevant accounting standard by

comparing the liabilities disclosure:

In this section of the report, the disclosure of the liabilities of the chosen companies

has been evaluated by review their recent financial statements published in the annual report

of the financial year 2018. For analyzing the disclosure of liabilities such as provisions and

contingent liabilities, the accounting policies used by the firms have been accounted for.

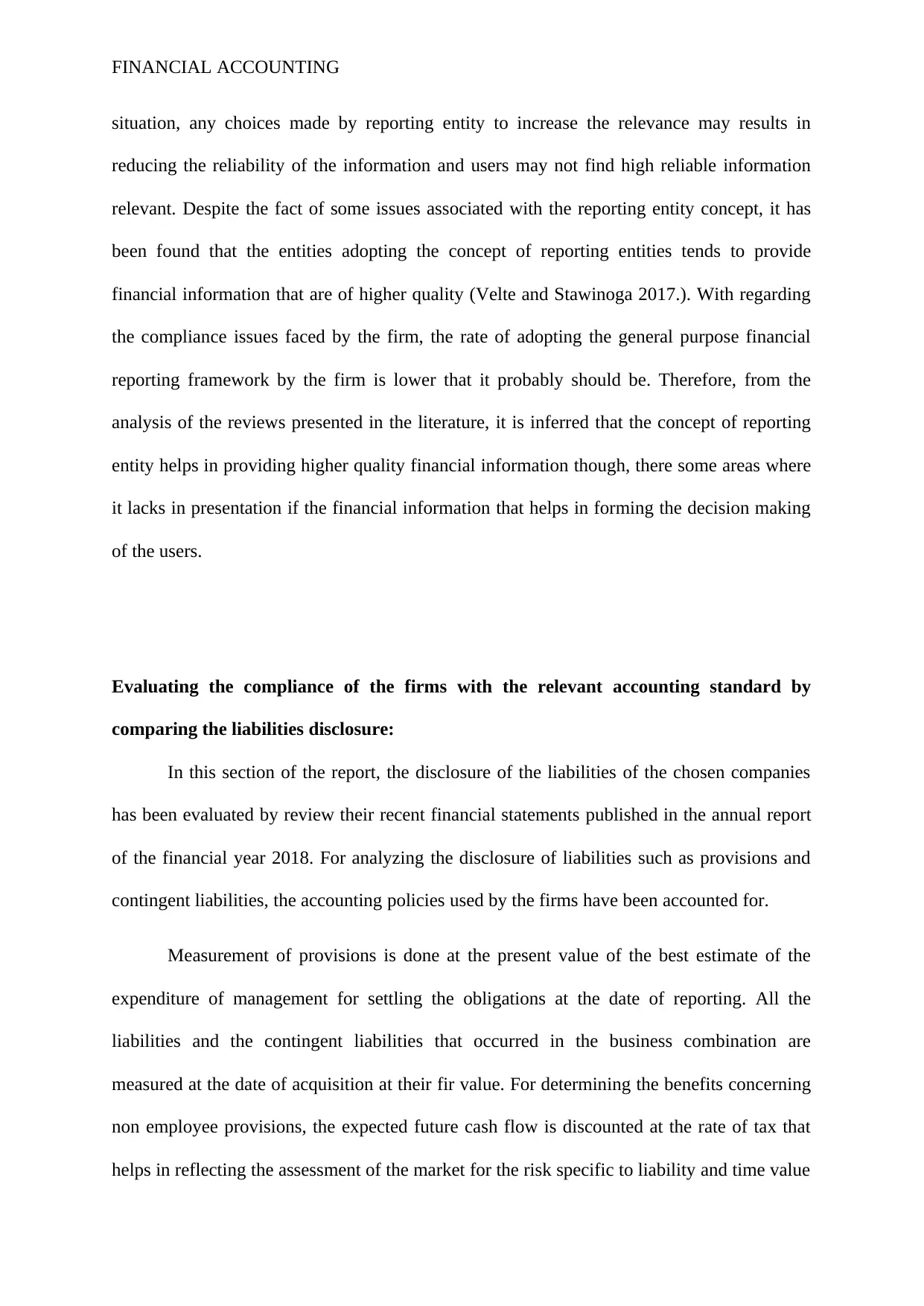

Measurement of provisions is done at the present value of the best estimate of the

expenditure of management for settling the obligations at the date of reporting. All the

liabilities and the contingent liabilities that occurred in the business combination are

measured at the date of acquisition at their fir value. For determining the benefits concerning

non employee provisions, the expected future cash flow is discounted at the rate of tax that

helps in reflecting the assessment of the market for the risk specific to liability and time value

situation, any choices made by reporting entity to increase the relevance may results in

reducing the reliability of the information and users may not find high reliable information

relevant. Despite the fact of some issues associated with the reporting entity concept, it has

been found that the entities adopting the concept of reporting entities tends to provide

financial information that are of higher quality (Velte and Stawinoga 2017.). With regarding

the compliance issues faced by the firm, the rate of adopting the general purpose financial

reporting framework by the firm is lower that it probably should be. Therefore, from the

analysis of the reviews presented in the literature, it is inferred that the concept of reporting

entity helps in providing higher quality financial information though, there some areas where

it lacks in presentation if the financial information that helps in forming the decision making

of the users.

Evaluating the compliance of the firms with the relevant accounting standard by

comparing the liabilities disclosure:

In this section of the report, the disclosure of the liabilities of the chosen companies

has been evaluated by review their recent financial statements published in the annual report

of the financial year 2018. For analyzing the disclosure of liabilities such as provisions and

contingent liabilities, the accounting policies used by the firms have been accounted for.

Measurement of provisions is done at the present value of the best estimate of the

expenditure of management for settling the obligations at the date of reporting. All the

liabilities and the contingent liabilities that occurred in the business combination are

measured at the date of acquisition at their fir value. For determining the benefits concerning

non employee provisions, the expected future cash flow is discounted at the rate of tax that

helps in reflecting the assessment of the market for the risk specific to liability and time value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING

of money (Adbri.com.au 2019). In addition to this, any increase in the provisions resulting

from the passage of time is recognized as interest expense.

Provisions:

(Source: Adbri.com.au 2019)

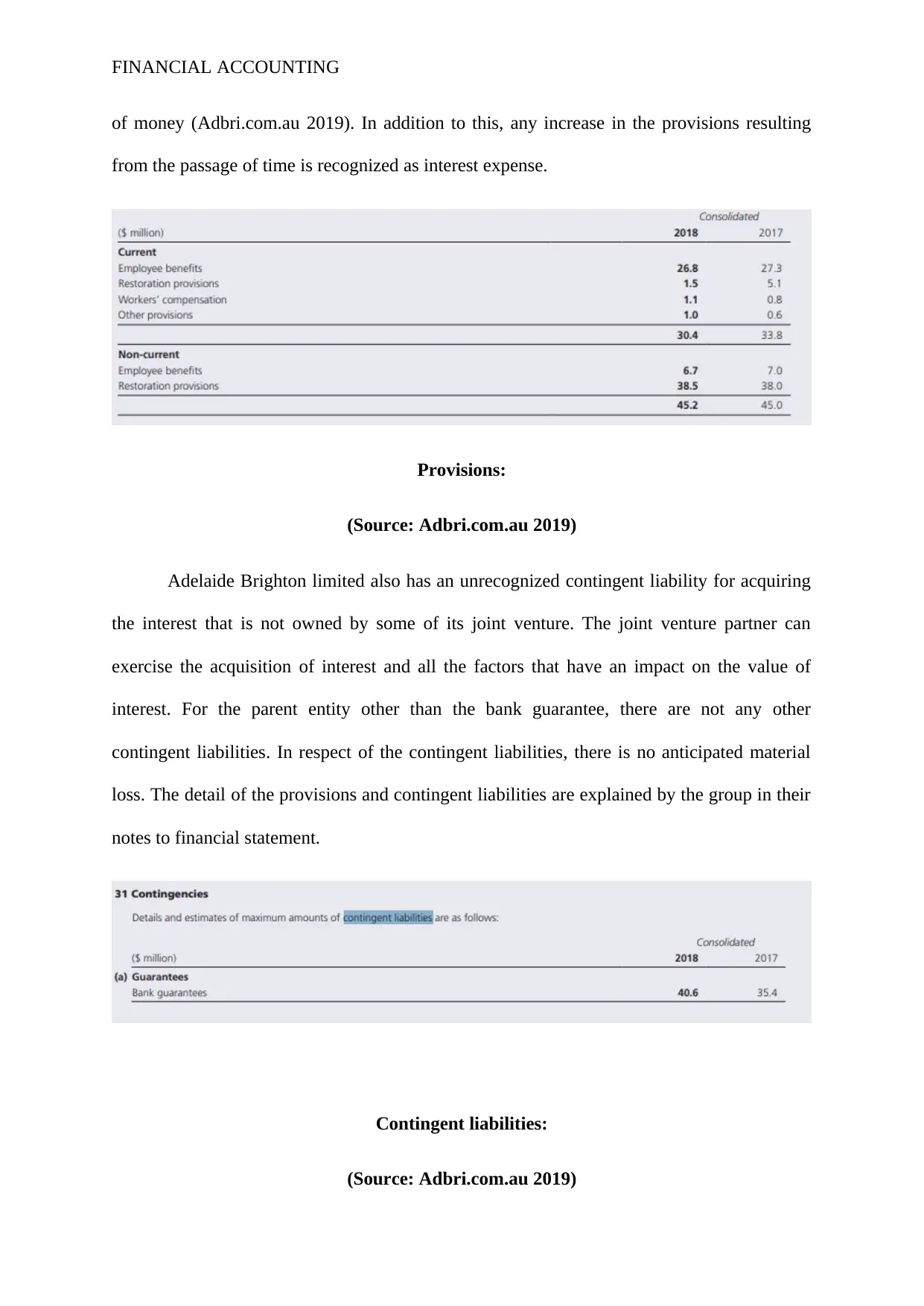

Adelaide Brighton limited also has an unrecognized contingent liability for acquiring

the interest that is not owned by some of its joint venture. The joint venture partner can

exercise the acquisition of interest and all the factors that have an impact on the value of

interest. For the parent entity other than the bank guarantee, there are not any other

contingent liabilities. In respect of the contingent liabilities, there is no anticipated material

loss. The detail of the provisions and contingent liabilities are explained by the group in their

notes to financial statement.

Contingent liabilities:

(Source: Adbri.com.au 2019)

of money (Adbri.com.au 2019). In addition to this, any increase in the provisions resulting

from the passage of time is recognized as interest expense.

Provisions:

(Source: Adbri.com.au 2019)

Adelaide Brighton limited also has an unrecognized contingent liability for acquiring

the interest that is not owned by some of its joint venture. The joint venture partner can

exercise the acquisition of interest and all the factors that have an impact on the value of

interest. For the parent entity other than the bank guarantee, there are not any other

contingent liabilities. In respect of the contingent liabilities, there is no anticipated material

loss. The detail of the provisions and contingent liabilities are explained by the group in their

notes to financial statement.

Contingent liabilities:

(Source: Adbri.com.au 2019)

FINANCIAL ACCOUNTING

For the provisions, there is a constructive and legal obligation on part of the group

that helps in estimating it in a reliably manner. The obligations concerning provision would

be settled by the outflow of economic benefits. Recognition of provision is done even when it

is likely to have an outflow with respect to the items include in the same obligation class

(Adbri.com.au 2019).

Myer Holding limited has constructive and legal obligations in recognizing the

provisions that occurred due to past events. In addition to this, there is a provision for future

operating losses as well. For settling the present obligation relating to provisions at the

reporting date, measurement of provisions are done at the best estimate of the measurement

made by management. Recognition of the provisions is done based on the claim projects

which are an estimate of the claims that have been incurred but they are not reported.

Moreover, determination of provisions are done by the group by utilizing an actuarially

determine method that is based on certain assumptions such as average claim size, future

inflation and administrative expenses that are to be claimed. There is annual review of all

such assumptions and the compensation expense of workers is affected by the reassessment

of such assumptions (emeraldinsight.com 2019). Therefore, it is outlined by the group that

the recognition of the provisions are done by deciding about the assumptions and judgment in

confirmation with reference to the accounting policies for computing the provisions relating

to strategic decision.

For the provisions, there is a constructive and legal obligation on part of the group

that helps in estimating it in a reliably manner. The obligations concerning provision would

be settled by the outflow of economic benefits. Recognition of provision is done even when it

is likely to have an outflow with respect to the items include in the same obligation class

(Adbri.com.au 2019).

Myer Holding limited has constructive and legal obligations in recognizing the

provisions that occurred due to past events. In addition to this, there is a provision for future

operating losses as well. For settling the present obligation relating to provisions at the

reporting date, measurement of provisions are done at the best estimate of the measurement

made by management. Recognition of the provisions is done based on the claim projects

which are an estimate of the claims that have been incurred but they are not reported.

Moreover, determination of provisions are done by the group by utilizing an actuarially

determine method that is based on certain assumptions such as average claim size, future

inflation and administrative expenses that are to be claimed. There is annual review of all

such assumptions and the compensation expense of workers is affected by the reassessment

of such assumptions (emeraldinsight.com 2019). Therefore, it is outlined by the group that

the recognition of the provisions are done by deciding about the assumptions and judgment in

confirmation with reference to the accounting policies for computing the provisions relating

to strategic decision.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING

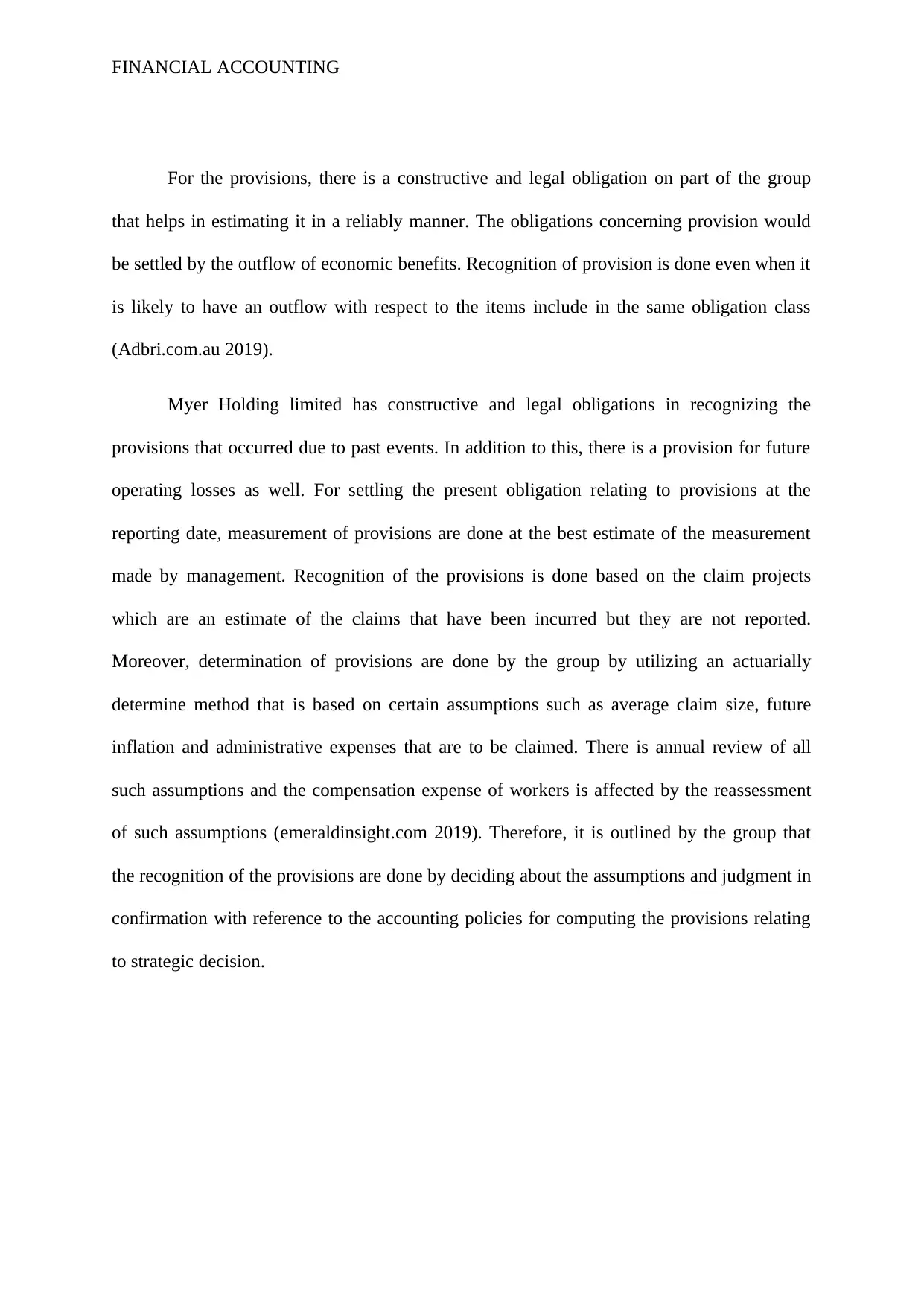

Provisions:

Source:

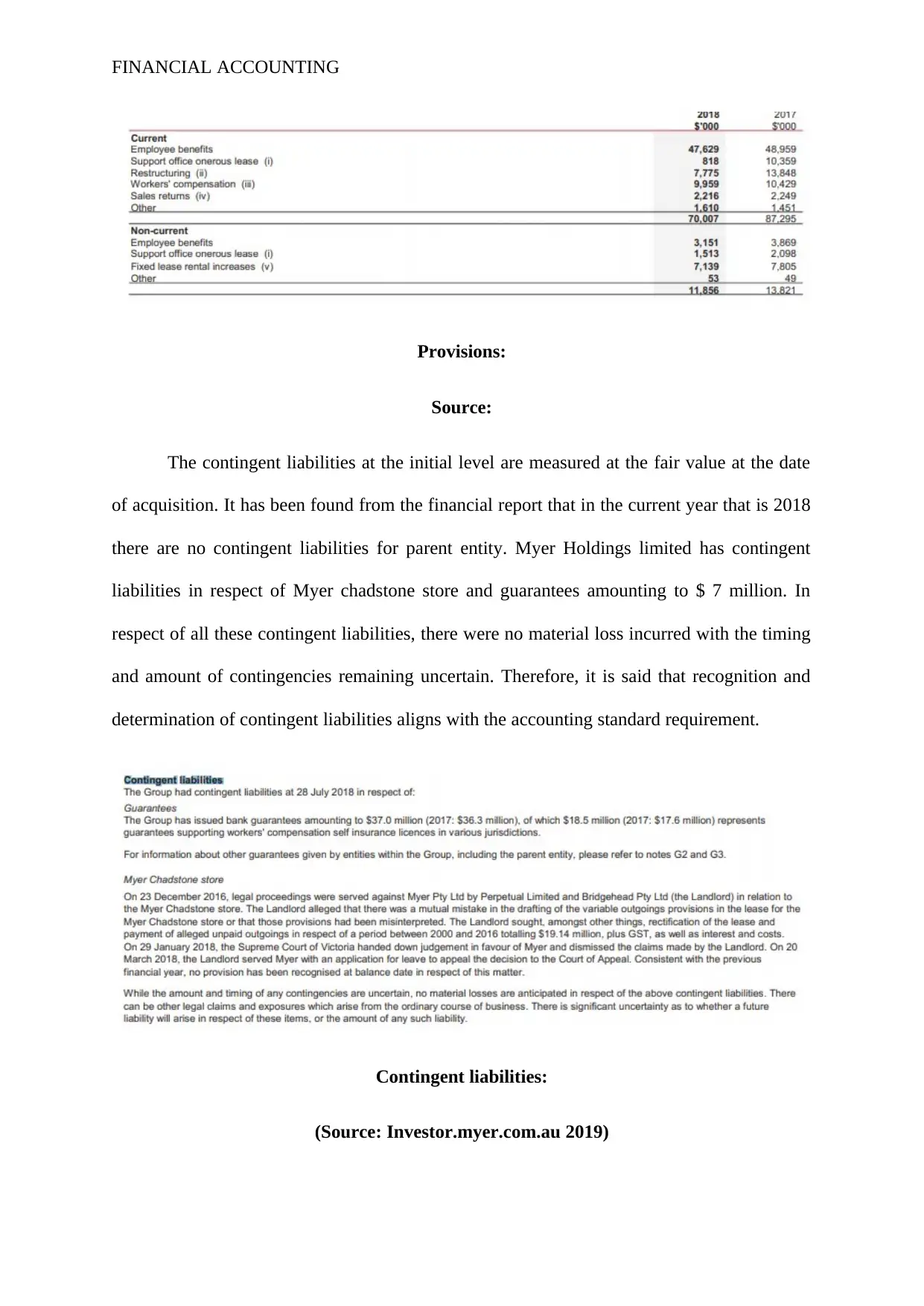

The contingent liabilities at the initial level are measured at the fair value at the date

of acquisition. It has been found from the financial report that in the current year that is 2018

there are no contingent liabilities for parent entity. Myer Holdings limited has contingent

liabilities in respect of Myer chadstone store and guarantees amounting to $ 7 million. In

respect of all these contingent liabilities, there were no material loss incurred with the timing

and amount of contingencies remaining uncertain. Therefore, it is said that recognition and

determination of contingent liabilities aligns with the accounting standard requirement.

Contingent liabilities:

(Source: Investor.myer.com.au 2019)

Provisions:

Source:

The contingent liabilities at the initial level are measured at the fair value at the date

of acquisition. It has been found from the financial report that in the current year that is 2018

there are no contingent liabilities for parent entity. Myer Holdings limited has contingent

liabilities in respect of Myer chadstone store and guarantees amounting to $ 7 million. In

respect of all these contingent liabilities, there were no material loss incurred with the timing

and amount of contingencies remaining uncertain. Therefore, it is said that recognition and

determination of contingent liabilities aligns with the accounting standard requirement.

Contingent liabilities:

(Source: Investor.myer.com.au 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING

The above section presented an analysis of the recognition and determination of

provision and liabilities for the two chosen companies. It has been found by reviewing the

financial statements that Myer holding limited provided a detailed disclosure of the

recognition of contingent liabilities and provisions compared to Adelaide Brighton limited.

However, both the organization has made the assumptions and estimates in the recognition of

liabilities in accordance with the requirements of the applicable Australian standard. All the

components of the provisions of the Myer holding is described separately as against Brighton

that only provided the disclosure of the figures and value of such accounts.

The disclosure quality relating to the liabilities can be done by disclosing higher

quantity of information. Moreover, the quality of the liabilities should be disclosed in an

adequate manner along with determination of measurement basis for the same. The

usefulness of the information relating to liabilities gets limited by the conceptually

inconsistent measurement of liabilities in the financial statements. Investors would be better

guided in their investment decision making if the measurement framework is established that

defines how the liabilities are measured and uses an economically relevant basis of

measurements. In addition to this, a complete and clear disclosure of the liabilities should be

provided to investors along with the measurement basis (Adbri.com.au 2019). There should

be a summary of all the types of contract, financial arrangement and commitments for

enhancing the transparency of information related to liabilities.

Evaluating the compliance of the firms with the relevant accounting standard by

comparing the disclosure of intangible assets:

This section of the report conducts an investigation into the compliance of the firms to

the relevant accounting standard in relation to the disclosure of intangible assets by reviewing

their financial statements. The obligations, benefits and expense associated with the income

The above section presented an analysis of the recognition and determination of

provision and liabilities for the two chosen companies. It has been found by reviewing the

financial statements that Myer holding limited provided a detailed disclosure of the

recognition of contingent liabilities and provisions compared to Adelaide Brighton limited.

However, both the organization has made the assumptions and estimates in the recognition of

liabilities in accordance with the requirements of the applicable Australian standard. All the

components of the provisions of the Myer holding is described separately as against Brighton

that only provided the disclosure of the figures and value of such accounts.

The disclosure quality relating to the liabilities can be done by disclosing higher

quantity of information. Moreover, the quality of the liabilities should be disclosed in an

adequate manner along with determination of measurement basis for the same. The

usefulness of the information relating to liabilities gets limited by the conceptually

inconsistent measurement of liabilities in the financial statements. Investors would be better

guided in their investment decision making if the measurement framework is established that

defines how the liabilities are measured and uses an economically relevant basis of

measurements. In addition to this, a complete and clear disclosure of the liabilities should be

provided to investors along with the measurement basis (Adbri.com.au 2019). There should

be a summary of all the types of contract, financial arrangement and commitments for

enhancing the transparency of information related to liabilities.

Evaluating the compliance of the firms with the relevant accounting standard by

comparing the disclosure of intangible assets:

This section of the report conducts an investigation into the compliance of the firms to

the relevant accounting standard in relation to the disclosure of intangible assets by reviewing

their financial statements. The obligations, benefits and expense associated with the income

FINANCIAL ACCOUNTING

tax are an accounting concept and there exist differences between income tax payable and

income tax expense.

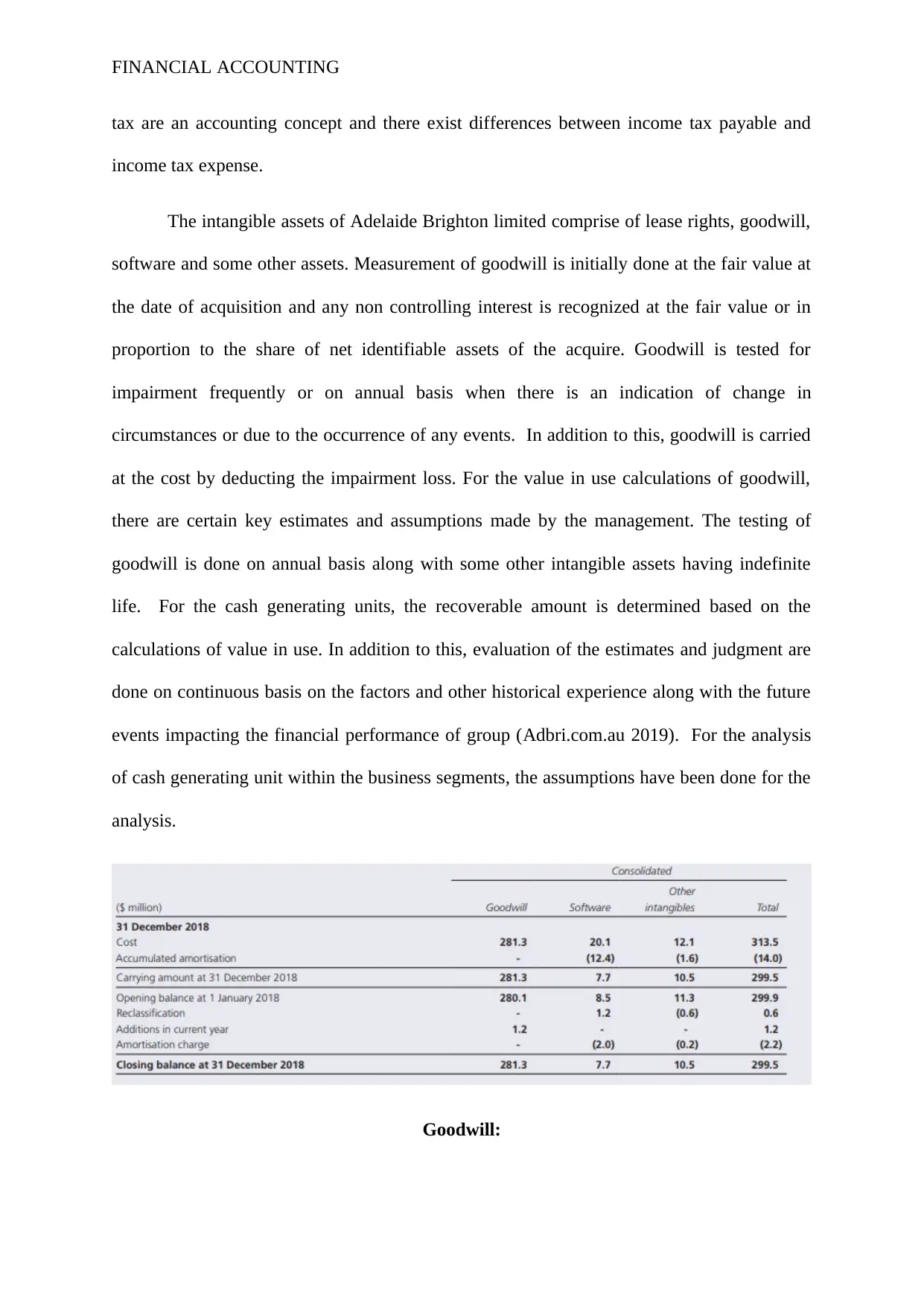

The intangible assets of Adelaide Brighton limited comprise of lease rights, goodwill,

software and some other assets. Measurement of goodwill is initially done at the fair value at

the date of acquisition and any non controlling interest is recognized at the fair value or in

proportion to the share of net identifiable assets of the acquire. Goodwill is tested for

impairment frequently or on annual basis when there is an indication of change in

circumstances or due to the occurrence of any events. In addition to this, goodwill is carried

at the cost by deducting the impairment loss. For the value in use calculations of goodwill,

there are certain key estimates and assumptions made by the management. The testing of

goodwill is done on annual basis along with some other intangible assets having indefinite

life. For the cash generating units, the recoverable amount is determined based on the

calculations of value in use. In addition to this, evaluation of the estimates and judgment are

done on continuous basis on the factors and other historical experience along with the future

events impacting the financial performance of group (Adbri.com.au 2019). For the analysis

of cash generating unit within the business segments, the assumptions have been done for the

analysis.

Goodwill:

tax are an accounting concept and there exist differences between income tax payable and

income tax expense.

The intangible assets of Adelaide Brighton limited comprise of lease rights, goodwill,

software and some other assets. Measurement of goodwill is initially done at the fair value at

the date of acquisition and any non controlling interest is recognized at the fair value or in

proportion to the share of net identifiable assets of the acquire. Goodwill is tested for

impairment frequently or on annual basis when there is an indication of change in

circumstances or due to the occurrence of any events. In addition to this, goodwill is carried

at the cost by deducting the impairment loss. For the value in use calculations of goodwill,

there are certain key estimates and assumptions made by the management. The testing of

goodwill is done on annual basis along with some other intangible assets having indefinite

life. For the cash generating units, the recoverable amount is determined based on the

calculations of value in use. In addition to this, evaluation of the estimates and judgment are

done on continuous basis on the factors and other historical experience along with the future

events impacting the financial performance of group (Adbri.com.au 2019). For the analysis

of cash generating unit within the business segments, the assumptions have been done for the

analysis.

Goodwill:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.