BAO3306 Auditing Report: Financial Audit of Konekt Limited, 2018

VerifiedAdded on 2023/03/31

|14

|3092

|428

Report

AI Summary

This report provides an in-depth analysis of the financial audit of Konekt Limited, focusing on identifying material misstatements and assessing audit risks. The report begins with an executive summary and introduction, outlining the scope of the audit and the objectives of the assessment. It then delves into key information, including an understanding of the client and an assessment of significant accounts. The analysis identifies five key accounts – sales, total expenses, cash and cash equivalents, intangible assets, and borrowings – that are potentially susceptible to material misstatement. For each account, the report discusses the nature of the potential misstatement and the audit procedures that should be applied. The report also considers the audit planning process, including the assessment of materiality and the identification of potential risks. The report also reviews the relevant auditing standards, such as ASA 300 and ASA 230. The report concludes with a summary of the findings and recommendations for improving the reliability of Konekt Limited's financial statements. The report also includes references to relevant auditing standards and the company's financial reports.

ASSIGNMENT

BAO3306 AUDITING

REPORT

BAO3306 AUDITING

REPORT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Semester 2, 2018

1. Executive summary

The assessment directly value the organization on the perspective of audit which is

relatively evaluate the financial statement for identifying the fair and true value that is

presented in its annual report. In addition, adequate audit plan has been evaluated and

form to identifying the relevant evidence, which helps in forming the audit opinion for

the organization. Moreover, audit steps are taken such as collecting the evidence and

analysing the proper application for audit standard which helps in improving the

reliability of the annual report that is presented by the organization. The analysis of

annual report has directly helps in identifying the five material accounts which can be

affected by the material misstatement. Hence, relevant evaluation of the audit

standards is conducted to identify the conditions of material misstatement present in

the annual report of the organization. Moreover, adequate evaluation has been

conducted for identifying the audit risk involved in the five identified balances which

is depicted in the annual report of the organization

1. Executive summary

The assessment directly value the organization on the perspective of audit which is

relatively evaluate the financial statement for identifying the fair and true value that is

presented in its annual report. In addition, adequate audit plan has been evaluated and

form to identifying the relevant evidence, which helps in forming the audit opinion for

the organization. Moreover, audit steps are taken such as collecting the evidence and

analysing the proper application for audit standard which helps in improving the

reliability of the annual report that is presented by the organization. The analysis of

annual report has directly helps in identifying the five material accounts which can be

affected by the material misstatement. Hence, relevant evaluation of the audit

standards is conducted to identify the conditions of material misstatement present in

the annual report of the organization. Moreover, adequate evaluation has been

conducted for identifying the audit risk involved in the five identified balances which

is depicted in the annual report of the organization

2. Introduction

The overall assessment directly evaluates the annual report of Konekt Limited

for identifying all the relevant material misstatement that is currently present in the

annual report of organization. Furthermore the assessment directly value the

organization on the perspective of audit which is relatively evaluate the financial

statement for identifying the fair and true value that is presented in its annual report.

In addition, adequate audit plan has been evaluated and form to identifying the

relevant evidence, which helps in forming the audit opinion for the organization.

Moreover, audit steps are taken such as collecting the evidence and analyzing the

proper application for audit standard which helps in improving the reliability of the

annual report that is presented by the organization. The analysis of annual report has

directly helps in identifying the five material accounts which can be affected by the

material misstatement. Hence, relevant evaluation of the audit standards is conducted

to identify the conditions of material misstatement present in the annual report of the

organization. Moreover, adequate evaluation has been conducted for identifying the

audit risk involved in the five identified balances which is depicted in the annual

report of the organization. The detection of the audit risk relatively help in identifying

the overall problems that is faced by the five identified accounts which need adequate

assessment of audit application.

The overall assessment directly evaluates the annual report of Konekt Limited

for identifying all the relevant material misstatement that is currently present in the

annual report of organization. Furthermore the assessment directly value the

organization on the perspective of audit which is relatively evaluate the financial

statement for identifying the fair and true value that is presented in its annual report.

In addition, adequate audit plan has been evaluated and form to identifying the

relevant evidence, which helps in forming the audit opinion for the organization.

Moreover, audit steps are taken such as collecting the evidence and analyzing the

proper application for audit standard which helps in improving the reliability of the

annual report that is presented by the organization. The analysis of annual report has

directly helps in identifying the five material accounts which can be affected by the

material misstatement. Hence, relevant evaluation of the audit standards is conducted

to identify the conditions of material misstatement present in the annual report of the

organization. Moreover, adequate evaluation has been conducted for identifying the

audit risk involved in the five identified balances which is depicted in the annual

report of the organization. The detection of the audit risk relatively help in identifying

the overall problems that is faced by the five identified accounts which need adequate

assessment of audit application.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Key information

a) Our understanding of the client

Evaluating the steps taken in key information collection

There are relevant steps that need to be taken into consideration for effectively

identifying the overall audit process that is conducted by auditors in an

organisation. The first step that needs to be taken into consideration is the

planning the activities for the audit process, as it allows the order to identify the

relevant paths in which the overall activities need to be conducted. With the help

of adequate planning approach, auditors are able to smoothly conduct the audit

process and able to collect the required level of audit evidence from the business

that could support the overall preparation of the audit report. More auditors also

need to identify and undertake computerisation of planning material as it

relatively helps in identifying the loopholes in the financial statement and

understand the level of inaccuracy that is presented in the report.

Moreover, the analysis also indicates that adequate Adherence to the auditing

standards needs to be conducted by the auditors for simultaneously applying the

audit procedures in the evidence collected from the organisation. This process

would eventually validate the audit process and identify the relevant material

misstatement that is present in the organisation. However, other steps need to be

taken by the auditors such as conducting and analytical review compliance test of

internal control external confirmation and substance of test for identifying the

dependence on audit programme. Furthermore, the audit also needs to determine

the timing and extent to which the audit procedure needs to be applied, as it helps

in under understanding the level of audit assertions present in the organisation

(Auasb.gov.au 2019).

Analysis of the business conducted by the Client

The main business operations of Konetkt Limited Is directly related to the

services that are provided by the organisation to its client regarding the health and

Risk Management Services. The company adequately provide adequate

information about the health and risk management conditions of a business the

client. The management needs to create an adequate workplace that would be safe

and Secure for the employees and it could be identified that the the management is

currently operating with an objective to build a workplace that has safe

environment.

Analysing the Audit program needed from the client

An adequate audit program needs to be formulated by the auditors during the

initial stage as it eventually helps in identifying the relevant steps and procedures

that need to be taken for effectively ensuring the smooth process of the audit.

Audit process also evaluates the overall annual report of the business for

adequately identifying the relevant guidelines and regulations that has been used

for formulating the financial statement. In accordance with Para 7 of ASA 300

Planning an Audit of the Financial Report, companies are mainly able to improve

the audit process, while minimising the negative impact on the Audit process that

is conducted on the organisation. Auditors adequately need to formulate an

adequate plan with relevant stages and steps for effectively improving the auditing

strategy and detecting the timing, direction and scope of the audit. The 2018

financial report has been conducted for identifying position of the company

development planning material that is currently present within the organisation.

a) Our understanding of the client

Evaluating the steps taken in key information collection

There are relevant steps that need to be taken into consideration for effectively

identifying the overall audit process that is conducted by auditors in an

organisation. The first step that needs to be taken into consideration is the

planning the activities for the audit process, as it allows the order to identify the

relevant paths in which the overall activities need to be conducted. With the help

of adequate planning approach, auditors are able to smoothly conduct the audit

process and able to collect the required level of audit evidence from the business

that could support the overall preparation of the audit report. More auditors also

need to identify and undertake computerisation of planning material as it

relatively helps in identifying the loopholes in the financial statement and

understand the level of inaccuracy that is presented in the report.

Moreover, the analysis also indicates that adequate Adherence to the auditing

standards needs to be conducted by the auditors for simultaneously applying the

audit procedures in the evidence collected from the organisation. This process

would eventually validate the audit process and identify the relevant material

misstatement that is present in the organisation. However, other steps need to be

taken by the auditors such as conducting and analytical review compliance test of

internal control external confirmation and substance of test for identifying the

dependence on audit programme. Furthermore, the audit also needs to determine

the timing and extent to which the audit procedure needs to be applied, as it helps

in under understanding the level of audit assertions present in the organisation

(Auasb.gov.au 2019).

Analysis of the business conducted by the Client

The main business operations of Konetkt Limited Is directly related to the

services that are provided by the organisation to its client regarding the health and

Risk Management Services. The company adequately provide adequate

information about the health and risk management conditions of a business the

client. The management needs to create an adequate workplace that would be safe

and Secure for the employees and it could be identified that the the management is

currently operating with an objective to build a workplace that has safe

environment.

Analysing the Audit program needed from the client

An adequate audit program needs to be formulated by the auditors during the

initial stage as it eventually helps in identifying the relevant steps and procedures

that need to be taken for effectively ensuring the smooth process of the audit.

Audit process also evaluates the overall annual report of the business for

adequately identifying the relevant guidelines and regulations that has been used

for formulating the financial statement. In accordance with Para 7 of ASA 300

Planning an Audit of the Financial Report, companies are mainly able to improve

the audit process, while minimising the negative impact on the Audit process that

is conducted on the organisation. Auditors adequately need to formulate an

adequate plan with relevant stages and steps for effectively improving the auditing

strategy and detecting the timing, direction and scope of the audit. The 2018

financial report has been conducted for identifying position of the company

development planning material that is currently present within the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DNA analysis of the audit programme would also effectively help in sharing the

provision that is presented in ASA 230 documentations, which eventually help in

identifying the relevant records that need to be evaluated for detecting the current

audit process of an organisation. if the analysis directly indicated that adequate

working papers also form a part of audit evidence as it relatively has in setting out

different procedures and tests, which were conducted by the auditor adequately

identifying and collecting the appropriate audit evidence of the business

(Auasb.gov.au 2019).

b) Our assessment of significant accounts

Material misstatement is an adequate problem for the auditor is which is

relatively detected from the financial statement of an organisation. The auditors

directly utilised information that is present in the annual report of the organisation

to detect the main responsibilities and determine the level of material

misstatement that is present within the organisation. However, the auditor has to

adequately provide and identify the risk of material misstatement truly

understanding of the overall environment of the entity. Moreover, the Assassin of

the risk is also needed as it effectively helps in identifying and understanding

DNA analysis of the audit programme would effectively help in sharing the

provision that is presented in ASA 230 documentations, which eventually help in

identifying the relevant records that need to be evaluated for detecting the current

audit process of an organisation. The analysis directly indicated that adequate

working papers also form a part of audit evidence as it relatively has in setting out

different procedures and tests, which were conducted by the auditor adequately

identifying and collecting the appropriate audit evidence of the business and its

current business environment.

Furthermore, the relevant evaluation is also required for identifying the

standard, which is required by the auditor's properly addressing the nature of the

business and the measures that is affecting its operational capability. The auditor

also needs to evaluate and conduct proper test for the internal control system that

has been established by the organisation throughout the years. Furthermore, the

main responsibility of the auditor is to ensure the financial statements are putting

the fair and true value of the organisation as per the accounting standards of the

region. Moreover, the annual report of Konekt Limited has been directly evaluated

to identify the key items that could be misstated by the Accountants of the

organisation (Auasb.gov.au 2019). The relevant key misstatement account of the

organisation is depicted as follows.

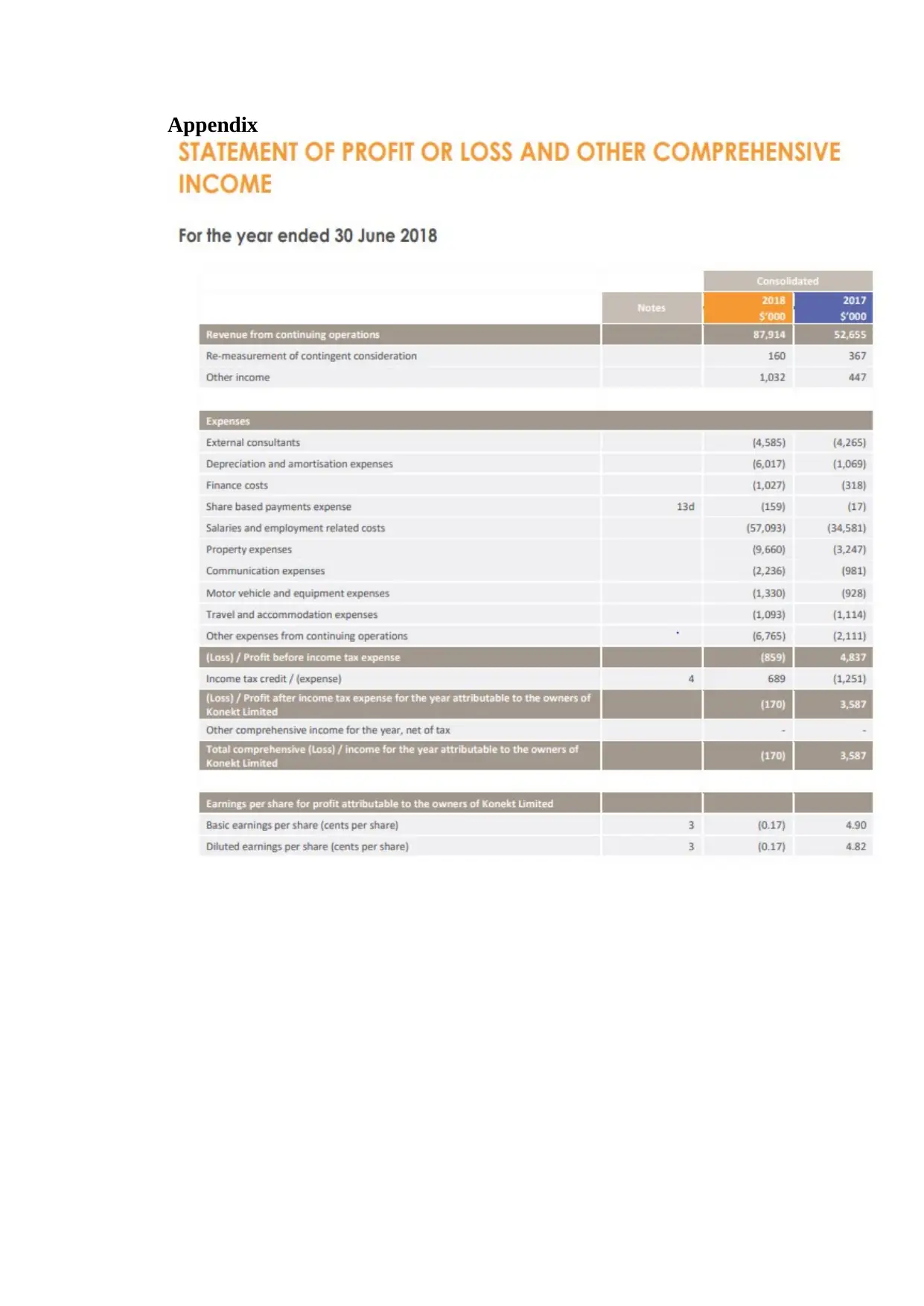

Sales: Sales is considered to be one of the major materially misstated accounts

in a business which directly portrays strong profit and loss conditions in the

annual report. More from the analysis it could be identified that sales

demonstrate in 2018 annual report could be increased tremendously as

comparison to previous year’s financial figures. The sales of the organisation

have a relatively soared higher in comparison to the previous financial year,

which is relevantly considered a problematic condition, which might be

influenced by material misstatement. The auditors in such case can adequately

evaluate the sales revenue presented in the annual report, which can be

overstated. Thus, the auditor needs to adequately apply proper substantiate

procedures for confirming or denying the material misstatement that is present

in sales figure of the organisation (Konekt.com.au 2019).

provision that is presented in ASA 230 documentations, which eventually help in

identifying the relevant records that need to be evaluated for detecting the current

audit process of an organisation. if the analysis directly indicated that adequate

working papers also form a part of audit evidence as it relatively has in setting out

different procedures and tests, which were conducted by the auditor adequately

identifying and collecting the appropriate audit evidence of the business

(Auasb.gov.au 2019).

b) Our assessment of significant accounts

Material misstatement is an adequate problem for the auditor is which is

relatively detected from the financial statement of an organisation. The auditors

directly utilised information that is present in the annual report of the organisation

to detect the main responsibilities and determine the level of material

misstatement that is present within the organisation. However, the auditor has to

adequately provide and identify the risk of material misstatement truly

understanding of the overall environment of the entity. Moreover, the Assassin of

the risk is also needed as it effectively helps in identifying and understanding

DNA analysis of the audit programme would effectively help in sharing the

provision that is presented in ASA 230 documentations, which eventually help in

identifying the relevant records that need to be evaluated for detecting the current

audit process of an organisation. The analysis directly indicated that adequate

working papers also form a part of audit evidence as it relatively has in setting out

different procedures and tests, which were conducted by the auditor adequately

identifying and collecting the appropriate audit evidence of the business and its

current business environment.

Furthermore, the relevant evaluation is also required for identifying the

standard, which is required by the auditor's properly addressing the nature of the

business and the measures that is affecting its operational capability. The auditor

also needs to evaluate and conduct proper test for the internal control system that

has been established by the organisation throughout the years. Furthermore, the

main responsibility of the auditor is to ensure the financial statements are putting

the fair and true value of the organisation as per the accounting standards of the

region. Moreover, the annual report of Konekt Limited has been directly evaluated

to identify the key items that could be misstated by the Accountants of the

organisation (Auasb.gov.au 2019). The relevant key misstatement account of the

organisation is depicted as follows.

Sales: Sales is considered to be one of the major materially misstated accounts

in a business which directly portrays strong profit and loss conditions in the

annual report. More from the analysis it could be identified that sales

demonstrate in 2018 annual report could be increased tremendously as

comparison to previous year’s financial figures. The sales of the organisation

have a relatively soared higher in comparison to the previous financial year,

which is relevantly considered a problematic condition, which might be

influenced by material misstatement. The auditors in such case can adequately

evaluate the sales revenue presented in the annual report, which can be

overstated. Thus, the auditor needs to adequately apply proper substantiate

procedures for confirming or denying the material misstatement that is present

in sales figure of the organisation (Konekt.com.au 2019).

Total expenses: The total expense of the organisation is also considered to be

under material misstatement measure, as it directly affects due overall profit

and loss conditions. From the analysis, it will be identified that some of the

expenses of the organisation soared unexpectedly during the financial year of

2018 in comparison to 2017. Relevant increment in the overall expenses as a

relatively reduce the level of revenues that has been generated by the

organisation during the financial. Therefore, it will be understood that the

expenses of the organisation might be influenced by material misstatement and

is not showing true and fair view of the financial conditions of the business.

Thus, the order to adequately need to consider their values of expenses that is

shown in the annual report such as depreciation, Finance cost, wages, salaries,

and other expenses in the profit loss statement of the organisation. In such

cases, the auditor need to adequately implement relevant audit procedures for

detecting the level of expenses that has been incurred by the organisation

during the financial year as it would eventually help in in judging the relevant

amount depicted in its annual report (Konekt.com.au 2019).

Cash and cash equivalents: The third major component that depicts the

problem related to Material misstatement is the cash and cash equivalents,

which is relatively increased during the financial year of 2018. The analysis of

the annual report has directly indicated that the business has shown an

inappropriate increment in the estimates of the cash and cash equivalent value

in comparison to previous financial year. This mainly forces the order to

analyse and check the value of the cash conditions that is currently being held

by the organisation. There might be a chance that the cash is relatively

misstated in the financial books of the organisation to effectively strengthen

the financial position of the organisation. The auditor need to apply

appropriate auditing procedures for ensuring the financial statement is

presented in a true and fair view, which directly indicates about the financial

position of the organisation. Moreover, the internal control conditions of the

organisation needs to be evaluated for identifying the cash management policy

that has been implemented by the company (Konekt.com.au 2019).

Intangible Assets: The major problem that can be identified in the annual

report of the organisation is in intangible asset valuation which is relatively

increased and indicate that the value is not been conducted in accordance with

the AASB standard. from the relevant evaluation of the annual report could be

identified that the company need to follow certain protocols are regarding the

valuation of intangible assets which is depicted in AASB 138 intangible

assets. However, the improper value shown in the balance sheet of the

intangible assets is relatively reflecting about the misstatements that are

conducted by the organisation in their annual report. Thus, the auditor need to

adequately devise an adequate procedure, which could support the detection

and verification of the values of the company's assets as it is essential to

determine the current financial condition of the organisation.

Borrowings: The last account that could be identified, as materially misstated

is the borrowings account depicted in the financial statement of the

organisation. The financial statements directly indicated that an incremental

borrowing was the fitness in the annual report of 2018, which directly

increases the level of leverage to the capital structure of the business. Hence,

the auditor needs to adequately analyse the current borrowings account of the

organisation for detecting the actual loans that is taken by the management to

under material misstatement measure, as it directly affects due overall profit

and loss conditions. From the analysis, it will be identified that some of the

expenses of the organisation soared unexpectedly during the financial year of

2018 in comparison to 2017. Relevant increment in the overall expenses as a

relatively reduce the level of revenues that has been generated by the

organisation during the financial. Therefore, it will be understood that the

expenses of the organisation might be influenced by material misstatement and

is not showing true and fair view of the financial conditions of the business.

Thus, the order to adequately need to consider their values of expenses that is

shown in the annual report such as depreciation, Finance cost, wages, salaries,

and other expenses in the profit loss statement of the organisation. In such

cases, the auditor need to adequately implement relevant audit procedures for

detecting the level of expenses that has been incurred by the organisation

during the financial year as it would eventually help in in judging the relevant

amount depicted in its annual report (Konekt.com.au 2019).

Cash and cash equivalents: The third major component that depicts the

problem related to Material misstatement is the cash and cash equivalents,

which is relatively increased during the financial year of 2018. The analysis of

the annual report has directly indicated that the business has shown an

inappropriate increment in the estimates of the cash and cash equivalent value

in comparison to previous financial year. This mainly forces the order to

analyse and check the value of the cash conditions that is currently being held

by the organisation. There might be a chance that the cash is relatively

misstated in the financial books of the organisation to effectively strengthen

the financial position of the organisation. The auditor need to apply

appropriate auditing procedures for ensuring the financial statement is

presented in a true and fair view, which directly indicates about the financial

position of the organisation. Moreover, the internal control conditions of the

organisation needs to be evaluated for identifying the cash management policy

that has been implemented by the company (Konekt.com.au 2019).

Intangible Assets: The major problem that can be identified in the annual

report of the organisation is in intangible asset valuation which is relatively

increased and indicate that the value is not been conducted in accordance with

the AASB standard. from the relevant evaluation of the annual report could be

identified that the company need to follow certain protocols are regarding the

valuation of intangible assets which is depicted in AASB 138 intangible

assets. However, the improper value shown in the balance sheet of the

intangible assets is relatively reflecting about the misstatements that are

conducted by the organisation in their annual report. Thus, the auditor need to

adequately devise an adequate procedure, which could support the detection

and verification of the values of the company's assets as it is essential to

determine the current financial condition of the organisation.

Borrowings: The last account that could be identified, as materially misstated

is the borrowings account depicted in the financial statement of the

organisation. The financial statements directly indicated that an incremental

borrowing was the fitness in the annual report of 2018, which directly

increases the level of leverage to the capital structure of the business. Hence,

the auditor needs to adequately analyse the current borrowings account of the

organisation for detecting the actual loans that is taken by the management to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

conduct the relevant operations. This evaluation can only be conducted with

adequate audit procedures that help in detecting the valuation condition of

each account. Moreover, the interest payment or expenses is also related to

borrowings where the increment in the borrowing levels has relatively sored

the interest expenses of the company, which needs to be addressed by the

auditors for authenticating the values of the balance sheet (Konekt.com.au

2019).

c) Our planning materiality

Planning materiality is relatively and adequate process which allows

the auditor to identify and detect material misstatement of the items that has

been shown in the financial statement. In order to determine the material of the

financial statements the auditor need to adequately identify the nature of the

item and the complexity in which the annual report has presented its value.

moreover the audit also need to identify and consider material for each of the

items that is presented in the financial statement as it would really help in

estimating the appropriate view of the current financial position of the

organisation. The relevant provision for the Material it needs to be conducted

by the organisation under the section ASA 320 Material asserting the material

items identified in the annual report of the organisation. In this process, the

auditors can adequately apply principle of professional scepticism all the

relevant items in the financial statement for denying for confirming the

presence of material misstatement in the annual report of the organisation.

The planning material it is relatively conducted by adequately

performing maturity on the account balance on the items presented in the

annual report. From the element analysis, it could be identified that planning

maturity estimates for the business as a relatively evaluated the total revenue

of the organisation, which has shown tremendous increment in the financial

year in comparison to previous year. Therefore, the auditor relatively

considered material misstatement provision of 0.5%, which represents the

material stated value of the total sales number. Consequently, adequate

calculation has been conducted for identifying the planning material

conditions effectively adding total revenues into 0.5%. The total revenue

generated by the organisation during the financial year of 2018 was it at the

levels of $87,914,000, while the materially misstated value is calculated to be

at the levels of $439,570 (Konekt.com.au 2019). The values of the Planning

material for total revenues have a relatively indicated overall material

misstatement that can be conducted during the financial report 2018. With the

help of adequate planning materiality auditors are able to access the material

item provide adequate opinion on the basis of the derived value.

adequate audit procedures that help in detecting the valuation condition of

each account. Moreover, the interest payment or expenses is also related to

borrowings where the increment in the borrowing levels has relatively sored

the interest expenses of the company, which needs to be addressed by the

auditors for authenticating the values of the balance sheet (Konekt.com.au

2019).

c) Our planning materiality

Planning materiality is relatively and adequate process which allows

the auditor to identify and detect material misstatement of the items that has

been shown in the financial statement. In order to determine the material of the

financial statements the auditor need to adequately identify the nature of the

item and the complexity in which the annual report has presented its value.

moreover the audit also need to identify and consider material for each of the

items that is presented in the financial statement as it would really help in

estimating the appropriate view of the current financial position of the

organisation. The relevant provision for the Material it needs to be conducted

by the organisation under the section ASA 320 Material asserting the material

items identified in the annual report of the organisation. In this process, the

auditors can adequately apply principle of professional scepticism all the

relevant items in the financial statement for denying for confirming the

presence of material misstatement in the annual report of the organisation.

The planning material it is relatively conducted by adequately

performing maturity on the account balance on the items presented in the

annual report. From the element analysis, it could be identified that planning

maturity estimates for the business as a relatively evaluated the total revenue

of the organisation, which has shown tremendous increment in the financial

year in comparison to previous year. Therefore, the auditor relatively

considered material misstatement provision of 0.5%, which represents the

material stated value of the total sales number. Consequently, adequate

calculation has been conducted for identifying the planning material

conditions effectively adding total revenues into 0.5%. The total revenue

generated by the organisation during the financial year of 2018 was it at the

levels of $87,914,000, while the materially misstated value is calculated to be

at the levels of $439,570 (Konekt.com.au 2019). The values of the Planning

material for total revenues have a relatively indicated overall material

misstatement that can be conducted during the financial report 2018. With the

help of adequate planning materiality auditors are able to access the material

item provide adequate opinion on the basis of the derived value.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

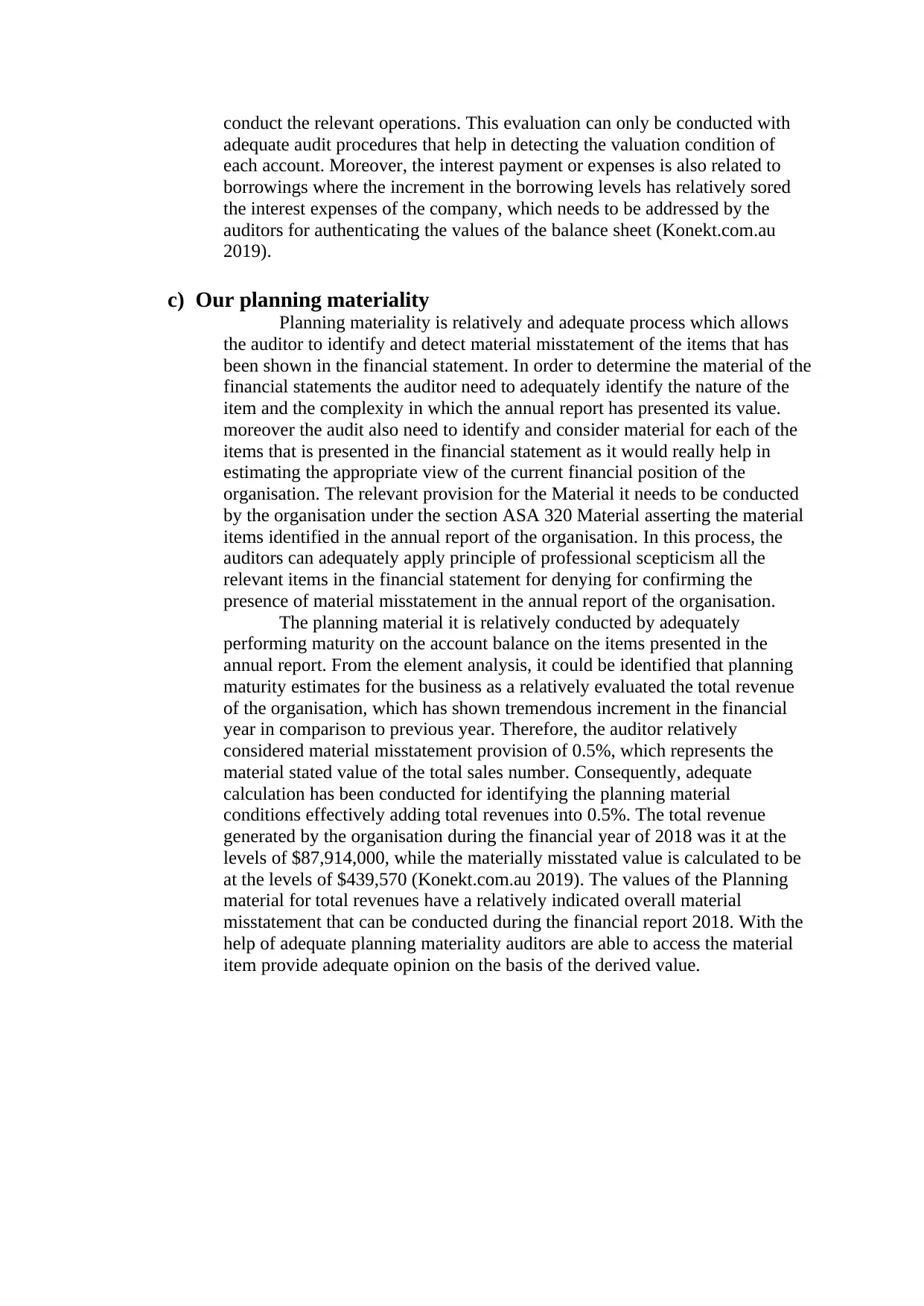

d) Our assessment of what can go wrong

The above table provide adequate information about the audit risk on the

selected areas of the balances, which is relatively derived by conducting adequate

misinterpretation in the annual report. the auditor's directly utilise and manage risk

by identifying and applying relevant audit risk model on the financial statements

of the company. The relevant audit risk is identified by calculating the detection

risk, control risk, and inheritance risk that is present in the annual report of the

company. The equation relatively helps in determining the level of total audit risk

that is present within the business and might reduce the authenticity of the

financial statement. The table directly trace the account balances of the identified

items for the organisation.

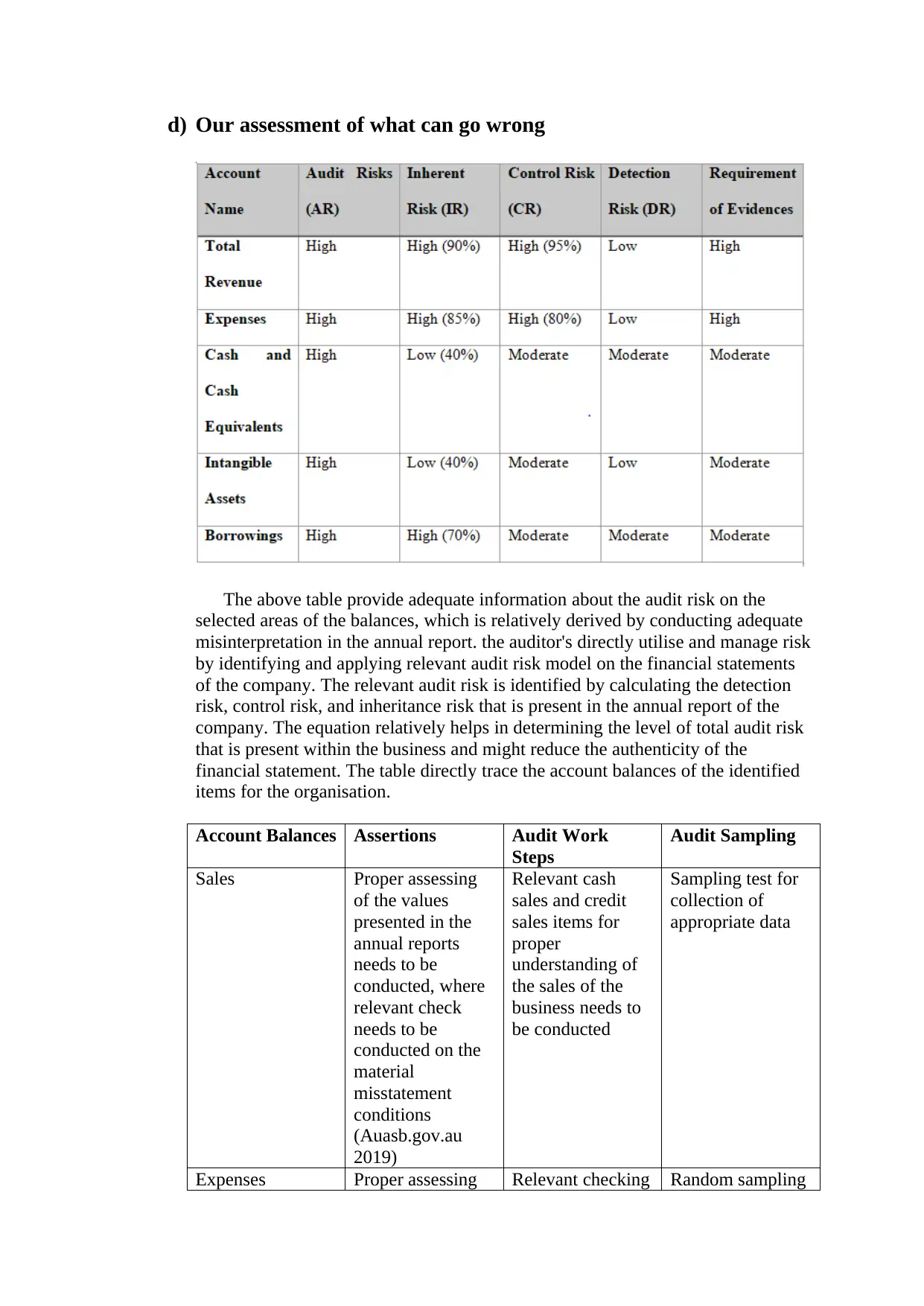

Account Balances Assertions Audit Work

Steps

Audit Sampling

Sales Proper assessing

of the values

presented in the

annual reports

needs to be

conducted, where

relevant check

needs to be

conducted on the

material

misstatement

conditions

(Auasb.gov.au

2019)

Relevant cash

sales and credit

sales items for

proper

understanding of

the sales of the

business needs to

be conducted

Sampling test for

collection of

appropriate data

Expenses Proper assessing Relevant checking Random sampling

The above table provide adequate information about the audit risk on the

selected areas of the balances, which is relatively derived by conducting adequate

misinterpretation in the annual report. the auditor's directly utilise and manage risk

by identifying and applying relevant audit risk model on the financial statements

of the company. The relevant audit risk is identified by calculating the detection

risk, control risk, and inheritance risk that is present in the annual report of the

company. The equation relatively helps in determining the level of total audit risk

that is present within the business and might reduce the authenticity of the

financial statement. The table directly trace the account balances of the identified

items for the organisation.

Account Balances Assertions Audit Work

Steps

Audit Sampling

Sales Proper assessing

of the values

presented in the

annual reports

needs to be

conducted, where

relevant check

needs to be

conducted on the

material

misstatement

conditions

(Auasb.gov.au

2019)

Relevant cash

sales and credit

sales items for

proper

understanding of

the sales of the

business needs to

be conducted

Sampling test for

collection of

appropriate data

Expenses Proper assessing Relevant checking Random sampling

of the expenses to

be conducted,

where adequate

evaluation of the

expenses needs to

be conducted.

Thus identifying

whether accurate

level of expenses

are being

portrayed by the

organization.

the internal

control system so

that the expenses

are properly

recorded for

identifying the

expenses of the

organization

approach

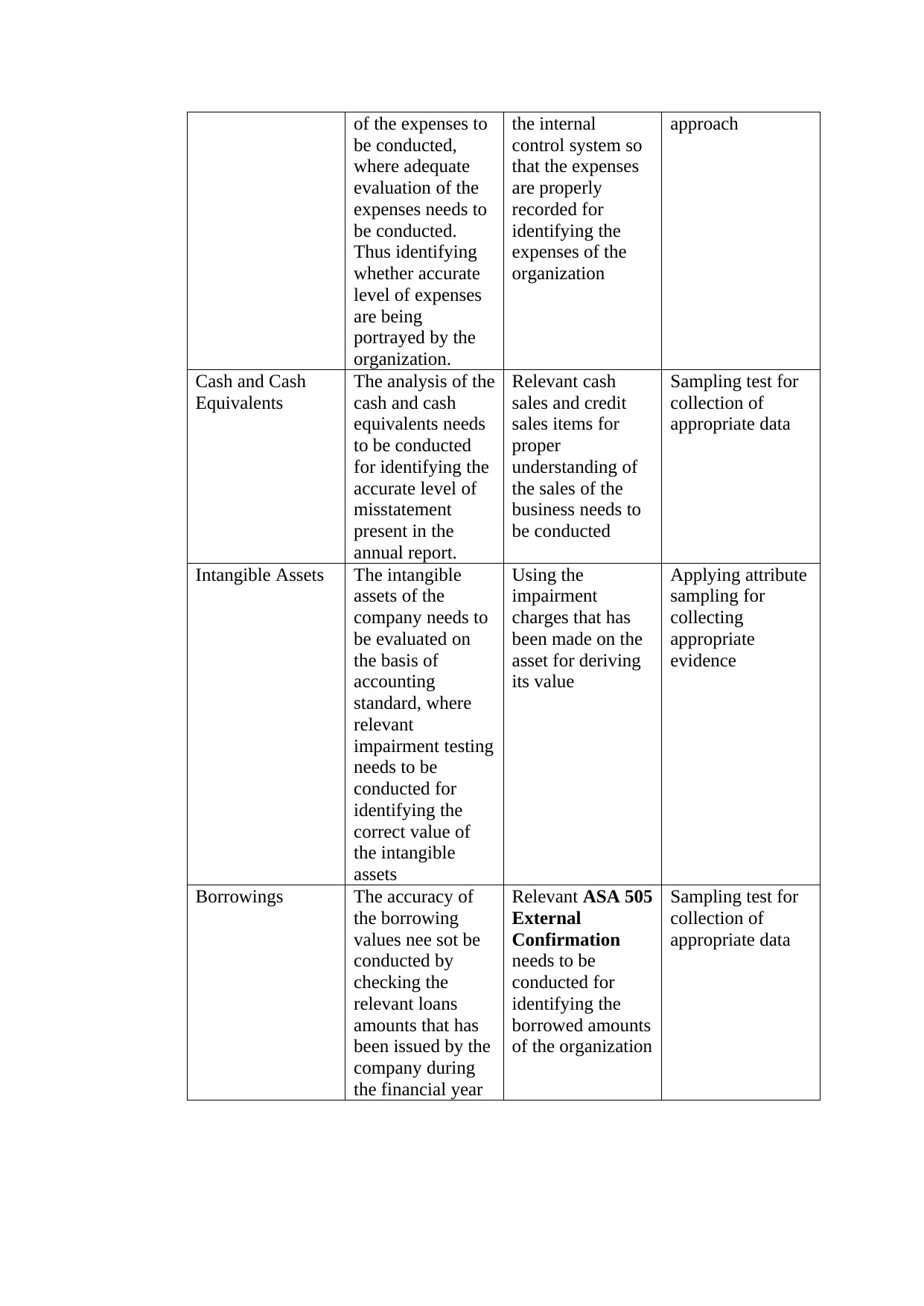

Cash and Cash

Equivalents

The analysis of the

cash and cash

equivalents needs

to be conducted

for identifying the

accurate level of

misstatement

present in the

annual report.

Relevant cash

sales and credit

sales items for

proper

understanding of

the sales of the

business needs to

be conducted

Sampling test for

collection of

appropriate data

Intangible Assets The intangible

assets of the

company needs to

be evaluated on

the basis of

accounting

standard, where

relevant

impairment testing

needs to be

conducted for

identifying the

correct value of

the intangible

assets

Using the

impairment

charges that has

been made on the

asset for deriving

its value

Applying attribute

sampling for

collecting

appropriate

evidence

Borrowings The accuracy of

the borrowing

values nee sot be

conducted by

checking the

relevant loans

amounts that has

been issued by the

company during

the financial year

Relevant ASA 505

External

Confirmation

needs to be

conducted for

identifying the

borrowed amounts

of the organization

Sampling test for

collection of

appropriate data

be conducted,

where adequate

evaluation of the

expenses needs to

be conducted.

Thus identifying

whether accurate

level of expenses

are being

portrayed by the

organization.

the internal

control system so

that the expenses

are properly

recorded for

identifying the

expenses of the

organization

approach

Cash and Cash

Equivalents

The analysis of the

cash and cash

equivalents needs

to be conducted

for identifying the

accurate level of

misstatement

present in the

annual report.

Relevant cash

sales and credit

sales items for

proper

understanding of

the sales of the

business needs to

be conducted

Sampling test for

collection of

appropriate data

Intangible Assets The intangible

assets of the

company needs to

be evaluated on

the basis of

accounting

standard, where

relevant

impairment testing

needs to be

conducted for

identifying the

correct value of

the intangible

assets

Using the

impairment

charges that has

been made on the

asset for deriving

its value

Applying attribute

sampling for

collecting

appropriate

evidence

Borrowings The accuracy of

the borrowing

values nee sot be

conducted by

checking the

relevant loans

amounts that has

been issued by the

company during

the financial year

Relevant ASA 505

External

Confirmation

needs to be

conducted for

identifying the

borrowed amounts

of the organization

Sampling test for

collection of

appropriate data

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Conclusion

The evaluation conducted in the above assessment directly indicates about the

planning process and programs that can be used by the auditor's effectively improving

the audit of the organisation. Moreover, the auditor's responsibility is to identify and

detect all the relevant material misstatement that is present in the annual report of the

organisation. Furthermore, the discussion as adequately help in identifying the

material misstatement that is present in Konekt Limited financial report 2018.

Relevant discussion has been conducted on the audit materiality and Audit risk model

for the organisation, which is relatively, helps in depicting the attributes of the audit

process. This is eventually helps in identifying the levels of measures that can be

preceded by the auditors for minimising the level of risk involved in audit.

Additionally, adequate discussion has been conducted to identify the relevant material

risk involved in the annual report of the organisation.

The evaluation conducted in the above assessment directly indicates about the

planning process and programs that can be used by the auditor's effectively improving

the audit of the organisation. Moreover, the auditor's responsibility is to identify and

detect all the relevant material misstatement that is present in the annual report of the

organisation. Furthermore, the discussion as adequately help in identifying the

material misstatement that is present in Konekt Limited financial report 2018.

Relevant discussion has been conducted on the audit materiality and Audit risk model

for the organisation, which is relatively, helps in depicting the attributes of the audit

process. This is eventually helps in identifying the levels of measures that can be

preceded by the auditors for minimising the level of risk involved in audit.

Additionally, adequate discussion has been conducted to identify the relevant material

risk involved in the annual report of the organisation.

Appendix

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.