BAP11 Principles of Accounting: Cash Flow Statement Analysis 2018

VerifiedAdded on 2023/06/09

|26

|3370

|403

Homework Assignment

AI Summary

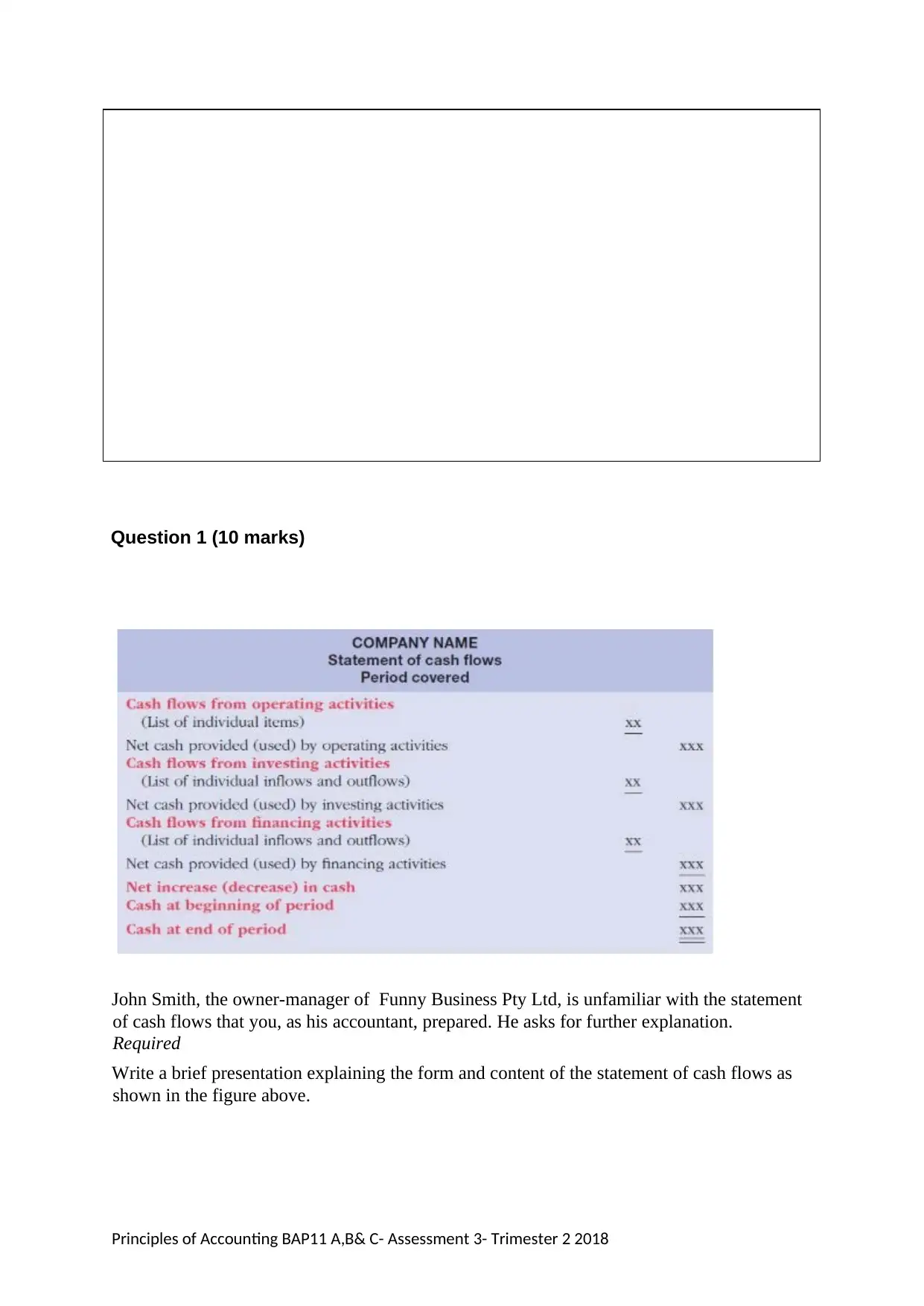

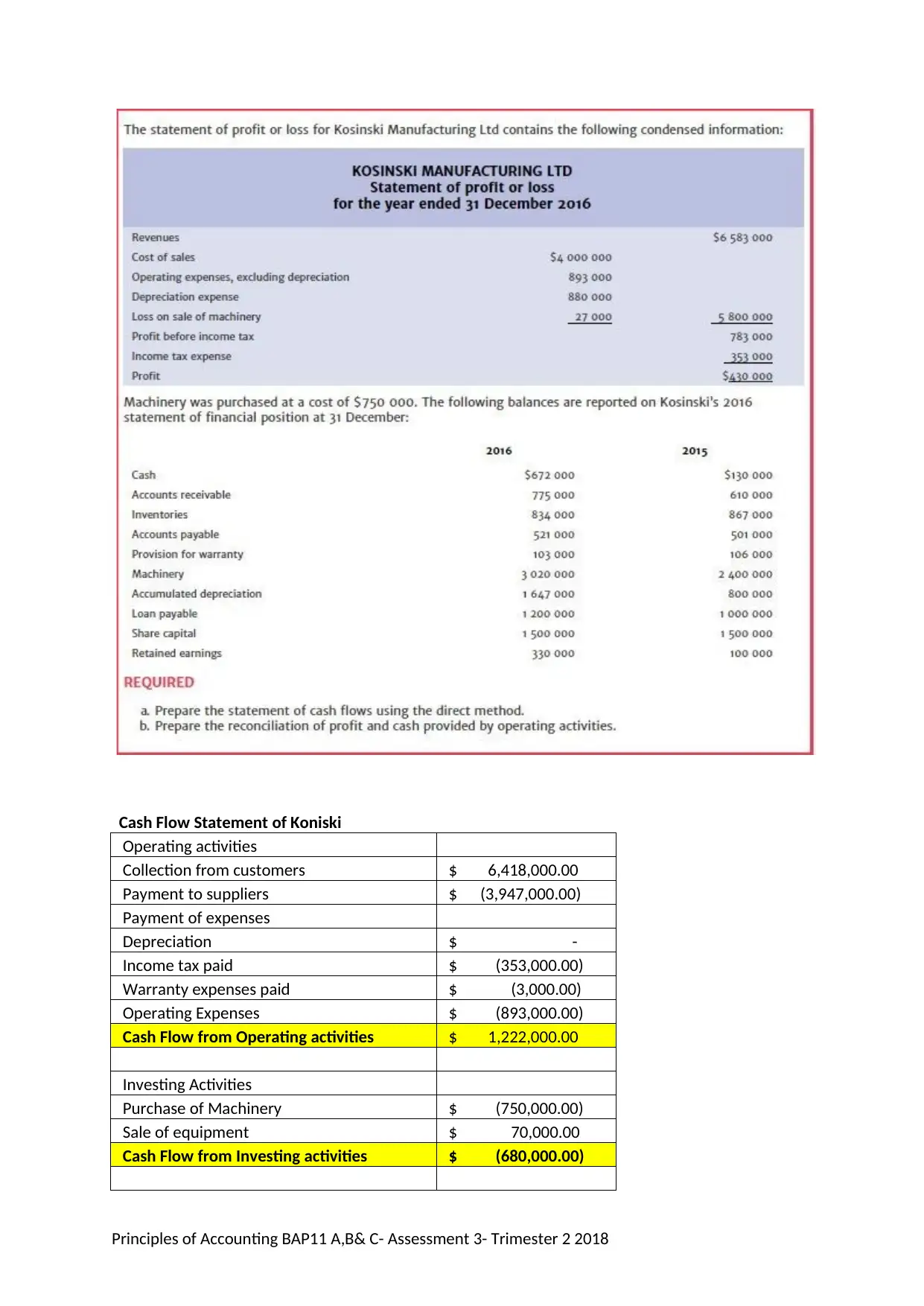

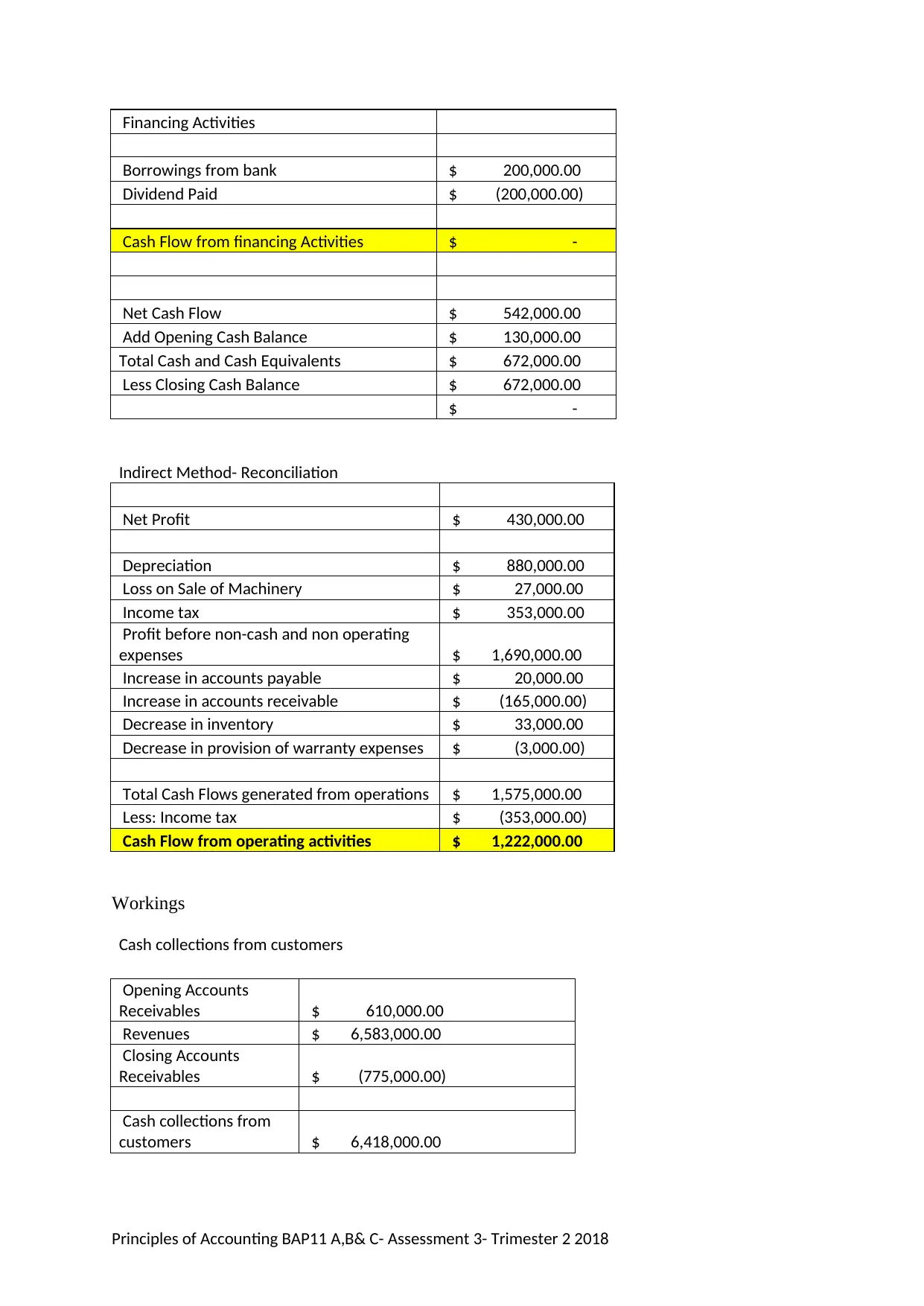

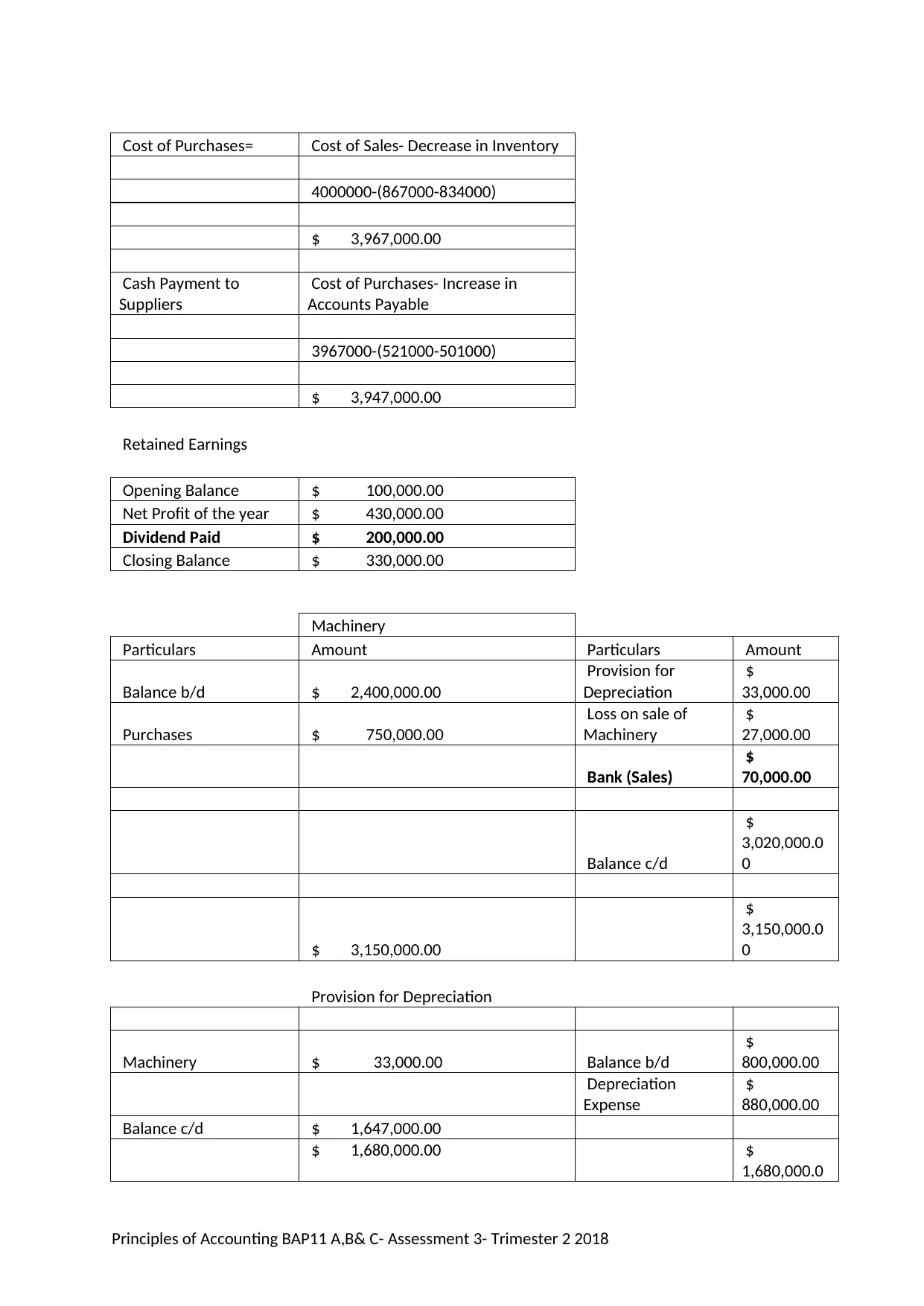

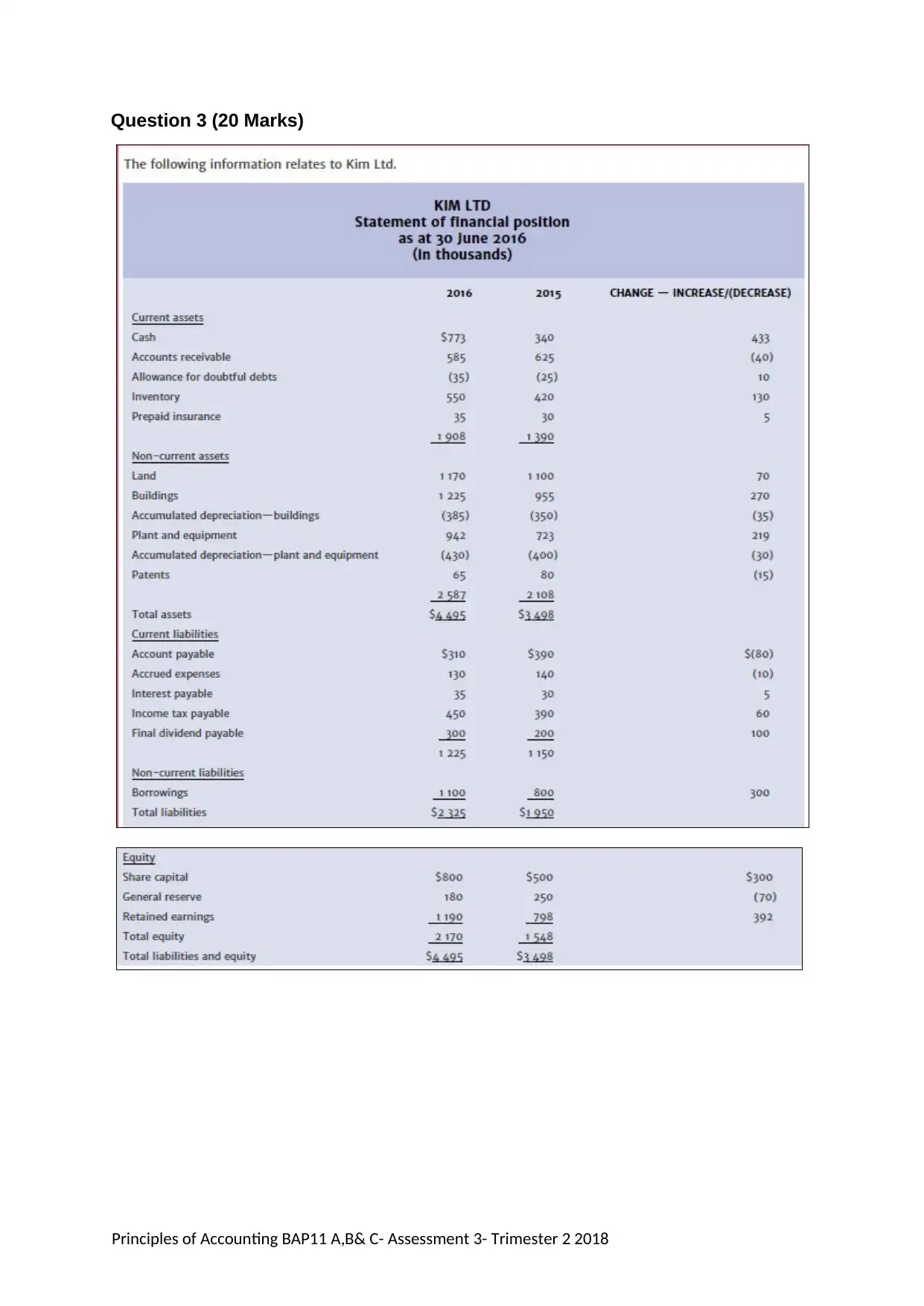

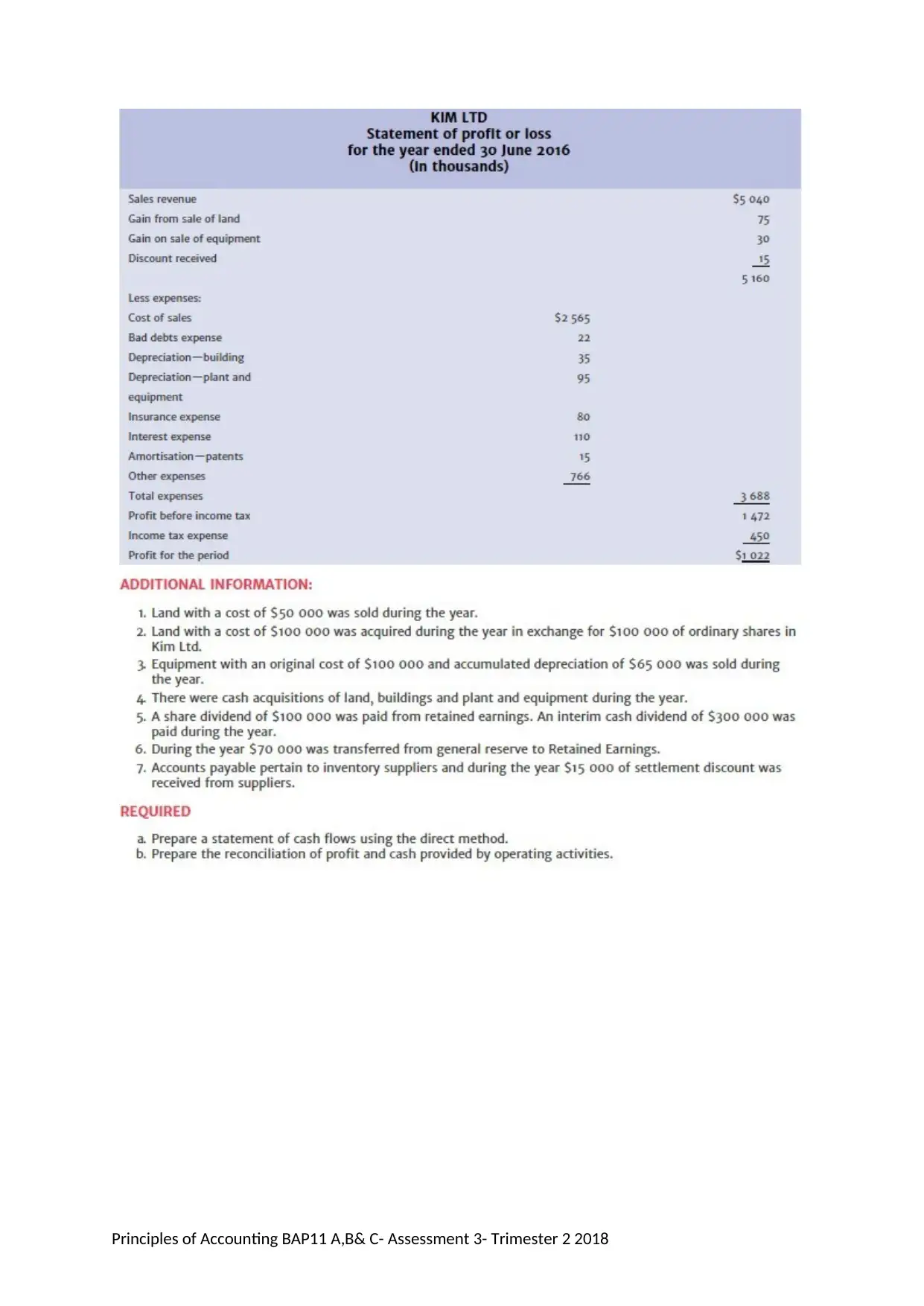

This assignment focuses on the preparation and analysis of cash flow statements, a crucial aspect of financial accounting. It includes a detailed explanation of the form and content of the cash flow statement, distinguishing between operating, investing, and financing activities. The assignment demonstrates both the direct and indirect methods of preparing the cash flow statement with numerical examples, including reconciliations and workings for cash collections from customers, payments to suppliers, and retained earnings. Additionally, it features multiple-choice questions to test understanding of key concepts related to cash flow statements. The document is available on Desklib, a platform offering a range of study tools and solved assignments for students.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.