Financial Analysis of Barclays: Market Factors and Demand Influences

VerifiedAdded on 2023/01/07

|14

|3333

|49

Report

AI Summary

This report provides a comprehensive analysis of Barclays, a British multinational bank and financial services company, focusing on its products, particularly life insurance. It begins with an overview of Barclays' history, products, and services, followed by a detailed market analysis, evaluating factors that influence demand. These factors include the price of substitutes and complements, customer income, tastes and preferences, demographics, and price sensitivity. The report examines how these factors impact Barclays' offerings and services, including the effects of consumer income and preferences. The analysis incorporates financial data, including net income and cash flow statements, to support the discussion of market dynamics and the influence of various factors on the demand for Barclays' products. The report concludes by summarizing the key findings and their implications for Barclays' business strategies and market position.

Management Economics –

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

MAIN BODY.................................................................................................................................................3

1. Overview of Barclays its products/services and history.......................................................................3

2. Market Analysis of Barclays to evaluate factors which influence its demand.....................................5

3. How factors influence the products and services of Barclays..............................................................9

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................12

INTRODUCTION...........................................................................................................................................3

MAIN BODY.................................................................................................................................................3

1. Overview of Barclays its products/services and history.......................................................................3

2. Market Analysis of Barclays to evaluate factors which influence its demand.....................................5

3. How factors influence the products and services of Barclays..............................................................9

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managerial economics is characterized as the method of combining different financial core

values within business activity and product. In order to sort out the business problems and other

financial activities use economical concept and theories to remove negative impact. In other

terms, management theory is based on the application of economic principles and logical

thinking to the appropriate decision-making problems. The crucial function is to encourage the

more efficient use of limited resources including such labor, capital and land. This has gained

popularity among businesses in the modern age because it wants to promote the leadership of full

financial documents in order to achieve particular market goals (Amran and Auzair, 2017). To

better understand the concept of the report selected organisation Barclays. It is a British

multinational investment bank and financial services company. The company deals in different

products and provides the service of life insurance to people. In this report consist of overview of

the organization and its essential products & services. Along with, analysis of market to identify

factors impact on the demand and influence the product & services.

MAIN BODY

1. Overview of Barclays its products/services and history

Barclays is British multinational bank and financial service company that operates

activities into different products. There are selecting product life insurance because in present

time every people wants to secure future and keep safe their loving one. Life insurance provides

something more than affirmation and economic freedom-if anything occurs to you, you can

secure a way of life for those you love. The business manages operate over 50 nations and hires

upwards of 140,000 people. It provides customers and companies the financing, investment,

security, and transformational services. The Banking Division has officially been identified one

of the world's greenest banks. As one of its online payment programs, Barclays provides

insurance policies and these comprise Aviva life insurance (Clikeman and Stevens, 2019).

Nonetheless, customers will not need to look for it anyway, as we will locate it for them while

performing our company's thorough check. Standard & General assuredness Company Limited

underwrites insurance coverage. Aviva's Barclays life insurance provides a large lump sum of up

to £ 500,000 and insurance payments of up to £ 5 that continue set for the lifetime of the policy.

This life insurance can be extended to UK citizens aged 18 to 66. Coverage begins on the

Managerial economics is characterized as the method of combining different financial core

values within business activity and product. In order to sort out the business problems and other

financial activities use economical concept and theories to remove negative impact. In other

terms, management theory is based on the application of economic principles and logical

thinking to the appropriate decision-making problems. The crucial function is to encourage the

more efficient use of limited resources including such labor, capital and land. This has gained

popularity among businesses in the modern age because it wants to promote the leadership of full

financial documents in order to achieve particular market goals (Amran and Auzair, 2017). To

better understand the concept of the report selected organisation Barclays. It is a British

multinational investment bank and financial services company. The company deals in different

products and provides the service of life insurance to people. In this report consist of overview of

the organization and its essential products & services. Along with, analysis of market to identify

factors impact on the demand and influence the product & services.

MAIN BODY

1. Overview of Barclays its products/services and history

Barclays is British multinational bank and financial service company that operates

activities into different products. There are selecting product life insurance because in present

time every people wants to secure future and keep safe their loving one. Life insurance provides

something more than affirmation and economic freedom-if anything occurs to you, you can

secure a way of life for those you love. The business manages operate over 50 nations and hires

upwards of 140,000 people. It provides customers and companies the financing, investment,

security, and transformational services. The Banking Division has officially been identified one

of the world's greenest banks. As one of its online payment programs, Barclays provides

insurance policies and these comprise Aviva life insurance (Clikeman and Stevens, 2019).

Nonetheless, customers will not need to look for it anyway, as we will locate it for them while

performing our company's thorough check. Standard & General assuredness Company Limited

underwrites insurance coverage. Aviva's Barclays life insurance provides a large lump sum of up

to £ 500,000 and insurance payments of up to £ 5 that continue set for the lifetime of the policy.

This life insurance can be extended to UK citizens aged 18 to 66. Coverage begins on the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

seventyth birth. Customers can choose policies for a rate or for a declining amount. The optimum

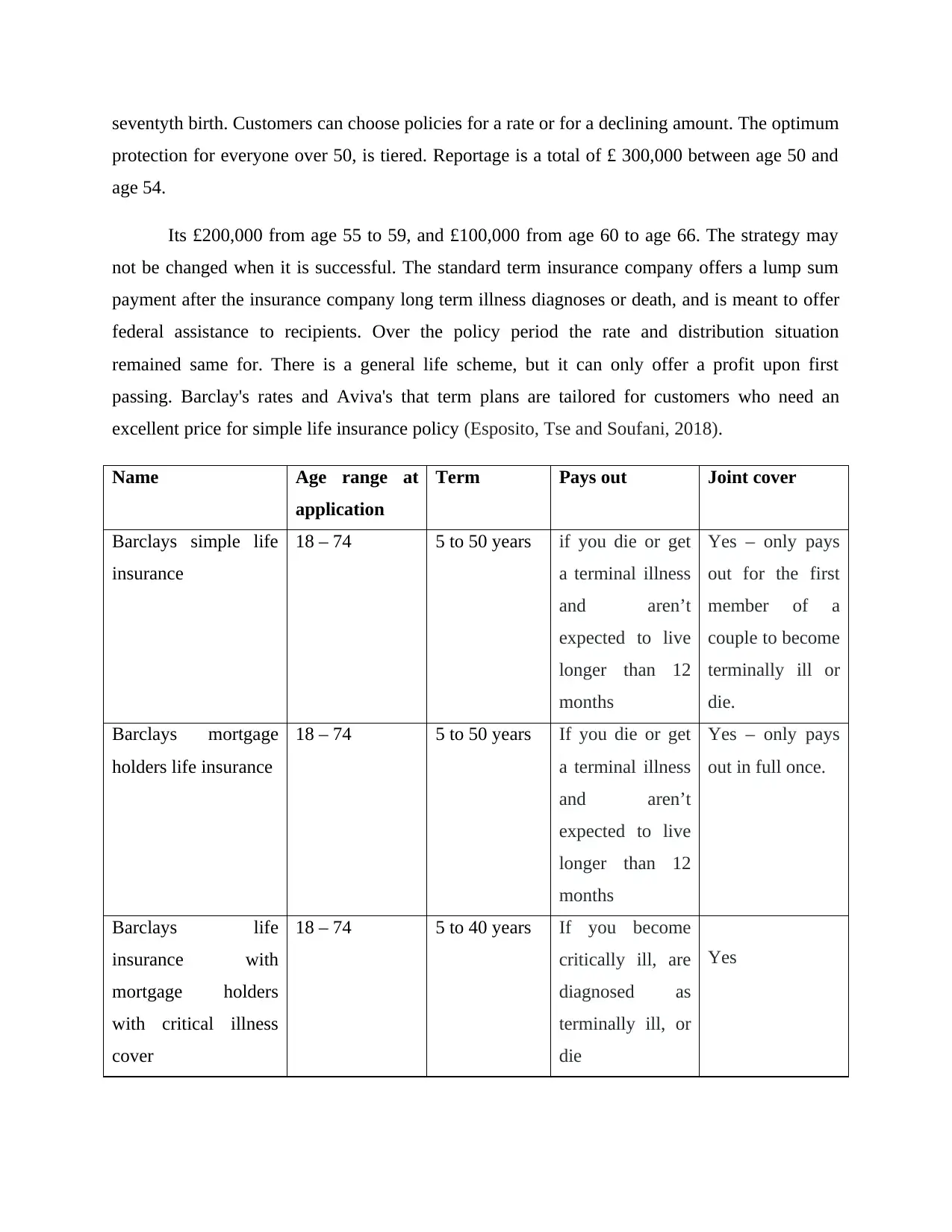

protection for everyone over 50, is tiered. Reportage is a total of £ 300,000 between age 50 and

age 54.

Its £200,000 from age 55 to 59, and £100,000 from age 60 to age 66. The strategy may

not be changed when it is successful. The standard term insurance company offers a lump sum

payment after the insurance company long term illness diagnoses or death, and is meant to offer

federal assistance to recipients. Over the policy period the rate and distribution situation

remained same for. There is a general life scheme, but it can only offer a profit upon first

passing. Barclay's rates and Aviva's that term plans are tailored for customers who need an

excellent price for simple life insurance policy (Esposito, Tse and Soufani, 2018).

Name Age range at

application

Term Pays out Joint cover

Barclays simple life

insurance

18 – 74 5 to 50 years if you die or get

a terminal illness

and aren’t

expected to live

longer than 12

months

Yes – only pays

out for the first

member of a

couple to become

terminally ill or

die.

Barclays mortgage

holders life insurance

18 – 74 5 to 50 years If you die or get

a terminal illness

and aren’t

expected to live

longer than 12

months

Yes – only pays

out in full once.

Barclays life

insurance with

mortgage holders

with critical illness

cover

18 – 74 5 to 40 years If you become

critically ill, are

diagnosed as

terminally ill, or

die

Yes

protection for everyone over 50, is tiered. Reportage is a total of £ 300,000 between age 50 and

age 54.

Its £200,000 from age 55 to 59, and £100,000 from age 60 to age 66. The strategy may

not be changed when it is successful. The standard term insurance company offers a lump sum

payment after the insurance company long term illness diagnoses or death, and is meant to offer

federal assistance to recipients. Over the policy period the rate and distribution situation

remained same for. There is a general life scheme, but it can only offer a profit upon first

passing. Barclay's rates and Aviva's that term plans are tailored for customers who need an

excellent price for simple life insurance policy (Esposito, Tse and Soufani, 2018).

Name Age range at

application

Term Pays out Joint cover

Barclays simple life

insurance

18 – 74 5 to 50 years if you die or get

a terminal illness

and aren’t

expected to live

longer than 12

months

Yes – only pays

out for the first

member of a

couple to become

terminally ill or

die.

Barclays mortgage

holders life insurance

18 – 74 5 to 50 years If you die or get

a terminal illness

and aren’t

expected to live

longer than 12

months

Yes – only pays

out in full once.

Barclays life

insurance with

mortgage holders

with critical illness

cover

18 – 74 5 to 40 years If you become

critically ill, are

diagnosed as

terminally ill, or

die

Yes

Barclays provides two different forms of life insurance coverage: Barclays Easy Life insurance

and Barclays Life Mortgage buyer’s policy. If people suffer or are treated with a fatal illness,

both must pay a lump sum payment. It ensures that your friends and families will have some

financial security in case you die mostly during duration of the scheme. As the title implies the

Easy Life Insurance Barclays is fairly straightforward (Ezzi, Jarboui and Zouari-Hadiji, 2020).

2. Market Analysis of Barclays to evaluate factors which influence its demand

In present time market capitalism it has been built that the production of goods and

services is based on numerous variables both positively and negatively. Thereby marketing

employees are forced to capitalize on these factors which determine the capital investment for

the particularly sensitive to the effects. Manager uses lifestyle influences in enterprises to decide

such as consumer desire, appetite and need, substitute and even some support merchandise, home

ownership that also involves establishing an even more suitable method for their production

process. This also translates to proactive forward-looking methods that can help competing with

economically difficult times and higher resolution of obvious risks. There are evaluating various

factors such as:

Price of substitute: If the supply of a commodity that accentuates a good declines, it just raises

the equilibrium quantity of the one and request with the other. If a replacement good's price

reduces than apply appropriate for that money produced, thus reduces the amount for the better

this is being substitutes for. In the context of Barclays company the substitute if life insurance of

other type of life insurance that provide the safety and security to people for longer period of

time. When people have not option of simple life insurance so they selects other type of life

insurance (Haghighi and Gerayli, 2019).

Price of complements: Complements are goods which are processed collectively. Substitutions

are goods where one may be consumed instead of the other. Even the costs of supplementary or

substitute goods change the consumer surplus. In present time Barclays face many competitors

who provide tough competition they are JPMorgan chase, HSBC and many others. Such as,

reduce interest of Barclay’s life insurance so it will provide advantage of other competitor

companies.

and Barclays Life Mortgage buyer’s policy. If people suffer or are treated with a fatal illness,

both must pay a lump sum payment. It ensures that your friends and families will have some

financial security in case you die mostly during duration of the scheme. As the title implies the

Easy Life Insurance Barclays is fairly straightforward (Ezzi, Jarboui and Zouari-Hadiji, 2020).

2. Market Analysis of Barclays to evaluate factors which influence its demand

In present time market capitalism it has been built that the production of goods and

services is based on numerous variables both positively and negatively. Thereby marketing

employees are forced to capitalize on these factors which determine the capital investment for

the particularly sensitive to the effects. Manager uses lifestyle influences in enterprises to decide

such as consumer desire, appetite and need, substitute and even some support merchandise, home

ownership that also involves establishing an even more suitable method for their production

process. This also translates to proactive forward-looking methods that can help competing with

economically difficult times and higher resolution of obvious risks. There are evaluating various

factors such as:

Price of substitute: If the supply of a commodity that accentuates a good declines, it just raises

the equilibrium quantity of the one and request with the other. If a replacement good's price

reduces than apply appropriate for that money produced, thus reduces the amount for the better

this is being substitutes for. In the context of Barclays company the substitute if life insurance of

other type of life insurance that provide the safety and security to people for longer period of

time. When people have not option of simple life insurance so they selects other type of life

insurance (Haghighi and Gerayli, 2019).

Price of complements: Complements are goods which are processed collectively. Substitutions

are goods where one may be consumed instead of the other. Even the costs of supplementary or

substitute goods change the consumer surplus. In present time Barclays face many competitors

who provide tough competition they are JPMorgan chase, HSBC and many others. Such as,

reduce interest of Barclay’s life insurance so it will provide advantage of other competitor

companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Customer income: Consumer revenue is the income a customer receives through either job or

spending, along with dividends paid to his owners by corporations, and the benefit gained by

acquiring an item, other than a home. After-tax profit is the amount a customer has left since

paying federal taxes. When customer income increase so they are investing more amount in the

life insurance and wants to secure their life. The selling of life insurance mainly depends on the

customer income and depends on their increasing and decreasing in effective manner. In case of

low income people do not invest into life insurance (Hitomi, 2017).

Customer taste and desire: A good for which the desires and preferences of clients are broader,

its demand would've been better and thus its equilibrium price would be stronger. People's

choices and desires for different products frequently shift and demand for them changes to the

structure. Now a day peoples aware for their life and want to secure future of their loving ones.

Thus they want to invest amount in life insurance and connect with the Barclays organisation to

cover up their future.

Price preference of consumers: Consumer preferences are characterized as the qualitative

(individual) preferences of the different bundles of commodities as determined by usefulness.

They allow certain bundles of products to be rated by the customer as per the degree of utility

they provide. Please note the interests are wealth- and priceless. Barclays offer different types of

life insurance to people according to their preference that helps to increase their selling in

positive manner. Along with company provide the facility to payment in lump sum method to

reduce problems (Huang, Nekrasov and Teoh, 2018).

Demographics: Demographics are a community analysis focused on such variables as age,

ethnicity, and sex. Demographic data pertains to empirically demonstrated socio-economic

information, which includes job opportunities, education, income, college enrollment, rates of

conception and birth, and also more. The life insurance cover to every type of people but it is

starting from the 15 years and at the end of 40 year to 50 year. A term life insurance policy will

protect you from 5 to 50 years, which will be paid out if you expire or are diagnosed with a fatal

disease. A scheme like this will help your relatives handle your finances while you're overseas,

then you're not going to have to risk leaving underneath a good pension. Or it can support the

family of day-to-day spending, making sure they retain their quality of life.

spending, along with dividends paid to his owners by corporations, and the benefit gained by

acquiring an item, other than a home. After-tax profit is the amount a customer has left since

paying federal taxes. When customer income increase so they are investing more amount in the

life insurance and wants to secure their life. The selling of life insurance mainly depends on the

customer income and depends on their increasing and decreasing in effective manner. In case of

low income people do not invest into life insurance (Hitomi, 2017).

Customer taste and desire: A good for which the desires and preferences of clients are broader,

its demand would've been better and thus its equilibrium price would be stronger. People's

choices and desires for different products frequently shift and demand for them changes to the

structure. Now a day peoples aware for their life and want to secure future of their loving ones.

Thus they want to invest amount in life insurance and connect with the Barclays organisation to

cover up their future.

Price preference of consumers: Consumer preferences are characterized as the qualitative

(individual) preferences of the different bundles of commodities as determined by usefulness.

They allow certain bundles of products to be rated by the customer as per the degree of utility

they provide. Please note the interests are wealth- and priceless. Barclays offer different types of

life insurance to people according to their preference that helps to increase their selling in

positive manner. Along with company provide the facility to payment in lump sum method to

reduce problems (Huang, Nekrasov and Teoh, 2018).

Demographics: Demographics are a community analysis focused on such variables as age,

ethnicity, and sex. Demographic data pertains to empirically demonstrated socio-economic

information, which includes job opportunities, education, income, college enrollment, rates of

conception and birth, and also more. The life insurance cover to every type of people but it is

starting from the 15 years and at the end of 40 year to 50 year. A term life insurance policy will

protect you from 5 to 50 years, which will be paid out if you expire or are diagnosed with a fatal

disease. A scheme like this will help your relatives handle your finances while you're overseas,

then you're not going to have to risk leaving underneath a good pension. Or it can support the

family of day-to-day spending, making sure they retain their quality of life.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

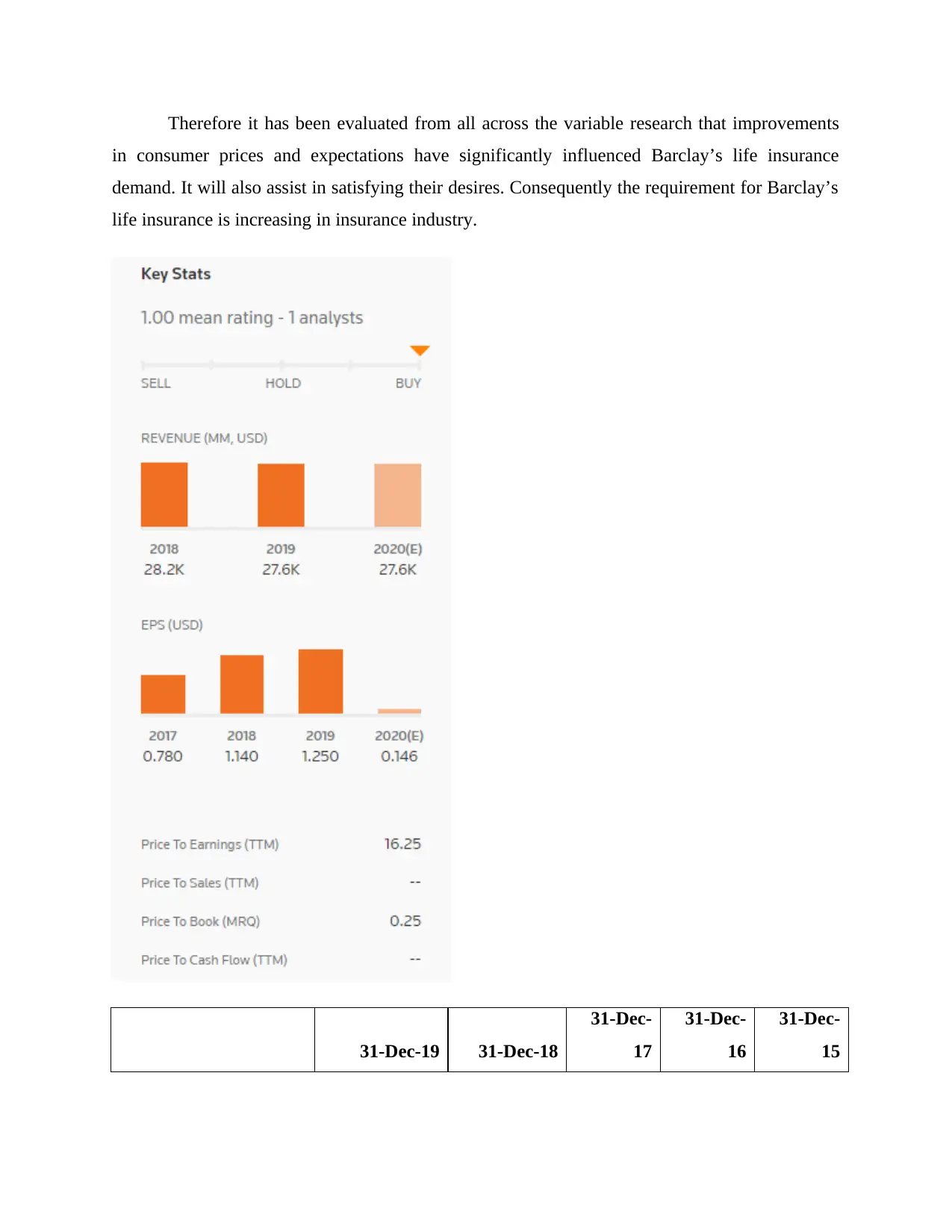

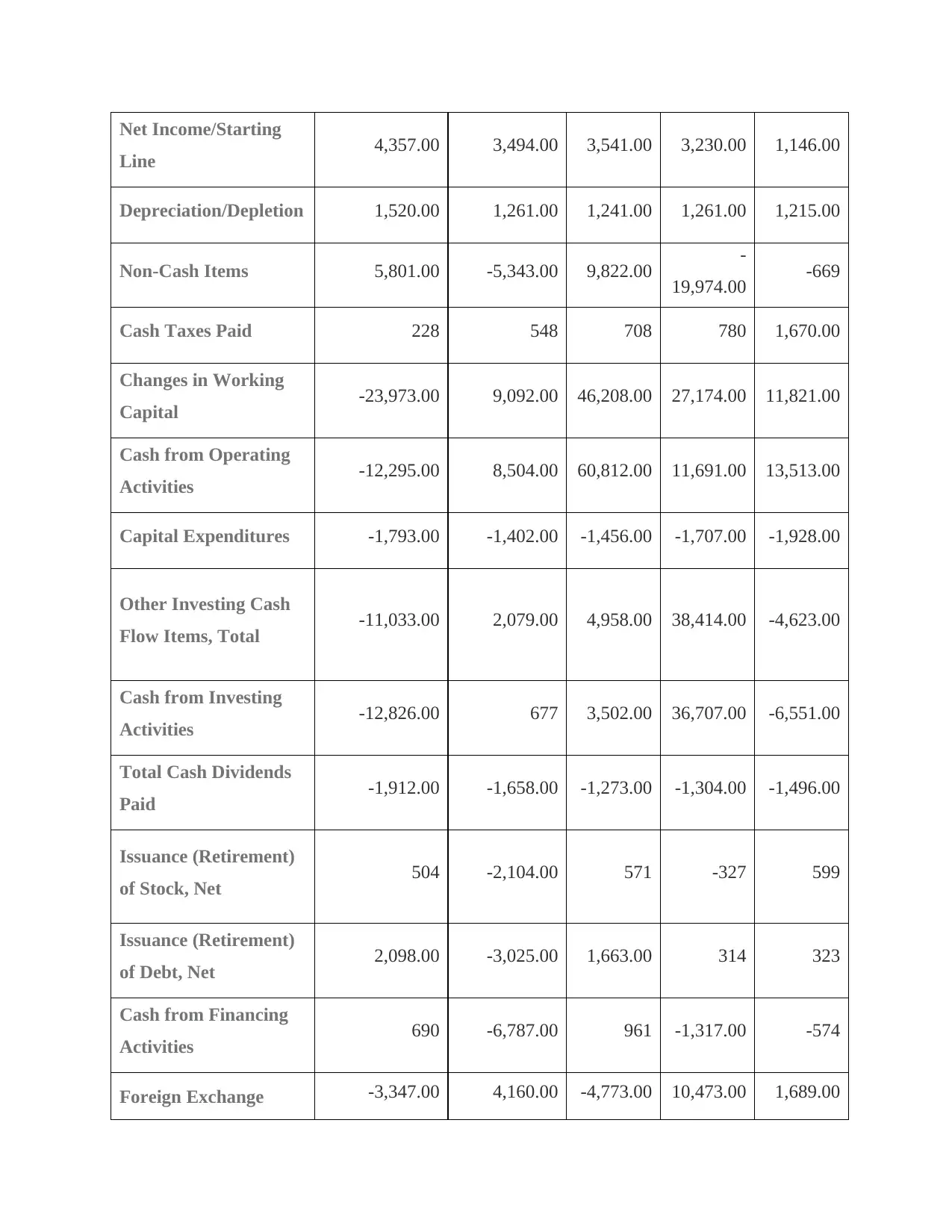

Therefore it has been evaluated from all across the variable research that improvements

in consumer prices and expectations have significantly influenced Barclay’s life insurance

demand. It will also assist in satisfying their desires. Consequently the requirement for Barclay’s

life insurance is increasing in insurance industry.

31-Dec-19 31-Dec-18

31-Dec-

17

31-Dec-

16

31-Dec-

15

in consumer prices and expectations have significantly influenced Barclay’s life insurance

demand. It will also assist in satisfying their desires. Consequently the requirement for Barclay’s

life insurance is increasing in insurance industry.

31-Dec-19 31-Dec-18

31-Dec-

17

31-Dec-

16

31-Dec-

15

Net Income/Starting

Line 4,357.00 3,494.00 3,541.00 3,230.00 1,146.00

Depreciation/Depletion 1,520.00 1,261.00 1,241.00 1,261.00 1,215.00

Non-Cash Items 5,801.00 -5,343.00 9,822.00 -

19,974.00 -669

Cash Taxes Paid 228 548 708 780 1,670.00

Changes in Working

Capital -23,973.00 9,092.00 46,208.00 27,174.00 11,821.00

Cash from Operating

Activities -12,295.00 8,504.00 60,812.00 11,691.00 13,513.00

Capital Expenditures -1,793.00 -1,402.00 -1,456.00 -1,707.00 -1,928.00

Other Investing Cash

Flow Items, Total -11,033.00 2,079.00 4,958.00 38,414.00 -4,623.00

Cash from Investing

Activities -12,826.00 677 3,502.00 36,707.00 -6,551.00

Total Cash Dividends

Paid -1,912.00 -1,658.00 -1,273.00 -1,304.00 -1,496.00

Issuance (Retirement)

of Stock, Net 504 -2,104.00 571 -327 599

Issuance (Retirement)

of Debt, Net 2,098.00 -3,025.00 1,663.00 314 323

Cash from Financing

Activities 690 -6,787.00 961 -1,317.00 -574

Foreign Exchange -3,347.00 4,160.00 -4,773.00 10,473.00 1,689.00

Line 4,357.00 3,494.00 3,541.00 3,230.00 1,146.00

Depreciation/Depletion 1,520.00 1,261.00 1,241.00 1,261.00 1,215.00

Non-Cash Items 5,801.00 -5,343.00 9,822.00 -

19,974.00 -669

Cash Taxes Paid 228 548 708 780 1,670.00

Changes in Working

Capital -23,973.00 9,092.00 46,208.00 27,174.00 11,821.00

Cash from Operating

Activities -12,295.00 8,504.00 60,812.00 11,691.00 13,513.00

Capital Expenditures -1,793.00 -1,402.00 -1,456.00 -1,707.00 -1,928.00

Other Investing Cash

Flow Items, Total -11,033.00 2,079.00 4,958.00 38,414.00 -4,623.00

Cash from Investing

Activities -12,826.00 677 3,502.00 36,707.00 -6,551.00

Total Cash Dividends

Paid -1,912.00 -1,658.00 -1,273.00 -1,304.00 -1,496.00

Issuance (Retirement)

of Stock, Net 504 -2,104.00 571 -327 599

Issuance (Retirement)

of Debt, Net 2,098.00 -3,025.00 1,663.00 314 323

Cash from Financing

Activities 690 -6,787.00 961 -1,317.00 -574

Foreign Exchange -3,347.00 4,160.00 -4,773.00 10,473.00 1,689.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Effects

Net Change in Cash -27,778.00 6,554.00 60,502.00 57,554.00 8,077.00

Financing Cash Flow

Items 104 -- -- --

3. How factors influence the products and services of Barclays

Because there are various factors present, such because customer expectations,

replacement and alternative pricing etc. impact Barclays' appetite for life insurance, both

positively and negatively. Therefore this organization is actively making improvements in goods

and services to address these demands and preserve its brand identity. For example –

restructuring the business globally to growing the challenge of replacements and supplements,

and give Barclays advantages in converting its dream (Kolasinski and Yang, 2018). According to

the law of demand rule, the increase in the price of just about every commodity was reported, the

weaker any need for shoppers to buy. In general, therefore, the demand of life insurance is

considered as versatile. Insurance is not really in the luxury sector because it acquires by the rich

people. Individuals may delay buying new cars especially if their costs are too high or even

beyond their income brackets. Offering good financial services along with other things is not

necessary, or a basic need for people. This also has a significant impact on the general consumer

credit access, wherein the folks who reside in high-ranking areas seek luxury purchases.

Luxury products or services including such luxury automobiles, specialist salons,

telephones and digital equipment and so on often carry higher elastic properties than

convenience-related objects, as they're being neglected by an individual for extended amounts of

time. Most of its aggregate economic the distributive bargaining, these are mentioned elsewhere

here:

Substitute availability: In the standard part, where it is easy to say that although the threat of

competitors is low, the elastic price of the product will also keep rising and there is a powerful

justification

Net Change in Cash -27,778.00 6,554.00 60,502.00 57,554.00 8,077.00

Financing Cash Flow

Items 104 -- -- --

3. How factors influence the products and services of Barclays

Because there are various factors present, such because customer expectations,

replacement and alternative pricing etc. impact Barclays' appetite for life insurance, both

positively and negatively. Therefore this organization is actively making improvements in goods

and services to address these demands and preserve its brand identity. For example –

restructuring the business globally to growing the challenge of replacements and supplements,

and give Barclays advantages in converting its dream (Kolasinski and Yang, 2018). According to

the law of demand rule, the increase in the price of just about every commodity was reported, the

weaker any need for shoppers to buy. In general, therefore, the demand of life insurance is

considered as versatile. Insurance is not really in the luxury sector because it acquires by the rich

people. Individuals may delay buying new cars especially if their costs are too high or even

beyond their income brackets. Offering good financial services along with other things is not

necessary, or a basic need for people. This also has a significant impact on the general consumer

credit access, wherein the folks who reside in high-ranking areas seek luxury purchases.

Luxury products or services including such luxury automobiles, specialist salons,

telephones and digital equipment and so on often carry higher elastic properties than

convenience-related objects, as they're being neglected by an individual for extended amounts of

time. Most of its aggregate economic the distributive bargaining, these are mentioned elsewhere

here:

Substitute availability: In the standard part, where it is easy to say that although the threat of

competitors is low, the elastic price of the product will also keep rising and there is a powerful

justification

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price level: Based on price-related demand conductivity it is clearly regarded as a determining

variable. Effectively, it has been said that expensive items like highly fitted PC, 4 K television,

and much more, display especially tough elasticity. While one of the other variables such as

reasonable product lines such as color coordinated bundle encapsulates, needle and so forth is

relatively elastic to take into account (Meccheri and Fanti, 2018).

Nature of commodity: Even the commodity structure influences and determines the elasticity of

the market. Different people may have different perceptions to the nature of the product, such as

comfort, price or necessity can be the good purchase for the product. When goods are not of

acceptable quality, the total demand may decline and the sales figure will be affected by the

applicable date

Consumption level: Those are believed to be the product that can be everyone from soft drinks,

candy, and so forth that doesn't come straight under the things that are needed or urgent. It can be

seen fortunately, that these products are mainly highly elastic in request. Consumers are

excluding this mainly if the price levels of such good and services are rising (Taj, Rashid and Bin

Tariq, 2019).

Pricing policy employ by business

There are identified different types of pricing policies that employ by the Barclays in

order to achieve

Competition pricing: Price competition is a mechanism by which certain firms use the fixed

prices. Using the price of a rival to just about price the specific goods. Offer or take a small

amount to match the value of a product or service (Mirza and et.al, 2019).

Demand pricing: Market pricing is also called demand-driven pricing, or pricing based on the

customers. This approach of pricing uses customer value of a product or service as the principal

aspect of establishing a price for products or service.

Cost plus pricing: This pricing strategy is a cost-based approach for trying to set services and

products prices. While determining the cost-plus level, consider the raw material costs and the

manufacturing costs and attach these to the operating costs of the products or company.

variable. Effectively, it has been said that expensive items like highly fitted PC, 4 K television,

and much more, display especially tough elasticity. While one of the other variables such as

reasonable product lines such as color coordinated bundle encapsulates, needle and so forth is

relatively elastic to take into account (Meccheri and Fanti, 2018).

Nature of commodity: Even the commodity structure influences and determines the elasticity of

the market. Different people may have different perceptions to the nature of the product, such as

comfort, price or necessity can be the good purchase for the product. When goods are not of

acceptable quality, the total demand may decline and the sales figure will be affected by the

applicable date

Consumption level: Those are believed to be the product that can be everyone from soft drinks,

candy, and so forth that doesn't come straight under the things that are needed or urgent. It can be

seen fortunately, that these products are mainly highly elastic in request. Consumers are

excluding this mainly if the price levels of such good and services are rising (Taj, Rashid and Bin

Tariq, 2019).

Pricing policy employ by business

There are identified different types of pricing policies that employ by the Barclays in

order to achieve

Competition pricing: Price competition is a mechanism by which certain firms use the fixed

prices. Using the price of a rival to just about price the specific goods. Offer or take a small

amount to match the value of a product or service (Mirza and et.al, 2019).

Demand pricing: Market pricing is also called demand-driven pricing, or pricing based on the

customers. This approach of pricing uses customer value of a product or service as the principal

aspect of establishing a price for products or service.

Cost plus pricing: This pricing strategy is a cost-based approach for trying to set services and

products prices. While determining the cost-plus level, consider the raw material costs and the

manufacturing costs and attach these to the operating costs of the products or company.

Price skimming: Businesses with a good competitive advantage use the pricing structure. They

join the high-priced services and goods sector. It is in order to get the most money. Until other

competitors may move in with identical, inexpensive services or goods, to get an early

replacement on manufacturing cost.

Economy pricing: A very common financial planning for distributors and retailers. The pricing

of the business is a simple form of advertising at low costs. It holds product prices down,

targeting sales in a specific target market which is highly price-sensitive (Stamatopoulos, 2018).

From the above pricing policies the Barclays Company apply the Cost plus pricing policy of

life insurance in order to get benefits.

CONCLUSION

It was inferred from the broader economic management analysis that a company can make

great business improvements by using the key concepts and their hypotheses. By implementing

supply and demand law to goods and services, a business may evaluate the influence of external

factors on its profits and selling rate and take corrective action. In the background of the

insurance industry, financial management says that by making thousands of life insurances each

year, this sector's contribution the main pivotal role in the development economy. In addition to

this, large-scale business operations also help to reduce the unemployment rate which inevitably

contributes to the growth of community as well.

join the high-priced services and goods sector. It is in order to get the most money. Until other

competitors may move in with identical, inexpensive services or goods, to get an early

replacement on manufacturing cost.

Economy pricing: A very common financial planning for distributors and retailers. The pricing

of the business is a simple form of advertising at low costs. It holds product prices down,

targeting sales in a specific target market which is highly price-sensitive (Stamatopoulos, 2018).

From the above pricing policies the Barclays Company apply the Cost plus pricing policy of

life insurance in order to get benefits.

CONCLUSION

It was inferred from the broader economic management analysis that a company can make

great business improvements by using the key concepts and their hypotheses. By implementing

supply and demand law to goods and services, a business may evaluate the influence of external

factors on its profits and selling rate and take corrective action. In the background of the

insurance industry, financial management says that by making thousands of life insurances each

year, this sector's contribution the main pivotal role in the development economy. In addition to

this, large-scale business operations also help to reduce the unemployment rate which inevitably

contributes to the growth of community as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.