Financial Analysis of Barclays: Data Handling and Decision Making

VerifiedAdded on 2021/01/03

|30

|5483

|457

Report

AI Summary

This report provides a detailed analysis of Barclays' financial performance, focusing on data handling and decision-making processes. It begins with an introduction to data handling techniques and their importance in financial analysis. The report then outlines the specific decision Barclays needs to make, which involves assessing the impact of operational performance on shareholder equity. The analysis utilizes financial data from Barclays' annual reports over a five-year period, including interest income, interest expense, net interest income, non-interest income, net operating income, and shareholder's equity. The report includes a discussion of the data mining procedures, data preparation, cleaning, and filtering processes. Descriptive data analysis is used to observe business performance, with correlations examined between net interest income, non-interest income, and stockholder's equity. The findings reveal a negative relationship between net interest income and shareholder equity, as well as a strong negative correlation between non-interest revenue and stockholder's equity. The report concludes with recommendations based on the analysis and provides references for further study. This report highlights the importance of data-driven decision-making in financial analysis and its impact on shareholder value.

DATA HANDLING AND

DECISION MAKING

DECISION MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION .....................................................................................................................................1

Statement of specific decision Barclays required to make..........................................................1

Descripting of relevant information used for analysis.................................................................4

a. Discussion of information related to business with representation of dataset.........................4

b. Obtaining of dataset with appropriate explanation..................................................................5

c. Importance of this statement in decision making process of business entity...........................5

Analysing the data mining procedures from data set...................................................................6

Data preparation, cleaning and filtering.......................................................................................6

Implicating the descriptive data analysis effective for immediate observation for business

performance.................................................................................................................................6

Developing organisational forecasting report............................................................................25

Visualisation and interpretation of outcomes............................................................................26

Decision making recommendations...........................................................................................26

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

INTRODUCTION...........................................................................................................................1

QUESTION .....................................................................................................................................1

Statement of specific decision Barclays required to make..........................................................1

Descripting of relevant information used for analysis.................................................................4

a. Discussion of information related to business with representation of dataset.........................4

b. Obtaining of dataset with appropriate explanation..................................................................5

c. Importance of this statement in decision making process of business entity...........................5

Analysing the data mining procedures from data set...................................................................6

Data preparation, cleaning and filtering.......................................................................................6

Implicating the descriptive data analysis effective for immediate observation for business

performance.................................................................................................................................6

Developing organisational forecasting report............................................................................25

Visualisation and interpretation of outcomes............................................................................26

Decision making recommendations...........................................................................................26

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

INTRODUCTION

Data handling is the techniques of collecting the data and managing it in the books of accounts which will be adequate and

effective with respect to make appropriate analysis over firm’s performance. To implicate the reformative changes in the operations of

Barclays which reflect in potential growth of this banking industry. The company have been operating in UK with facilitating the

internal banking services which is comprised of various activities such as Corporate banking, personal banking, investment

management and wealth management. In the present assessment there will be determination of the facts which are affecting the growth

of industry. The analysis will be based on analysing impacts of profitability on the amount of funds derived through shareholders.

Thus, the profitability of this banking industry will affect the number of investors in each period. It will be consisting influences of

statistical tools to analyse the relationship between variables.

QUESTION

Statement of specific decision Barclays required to make

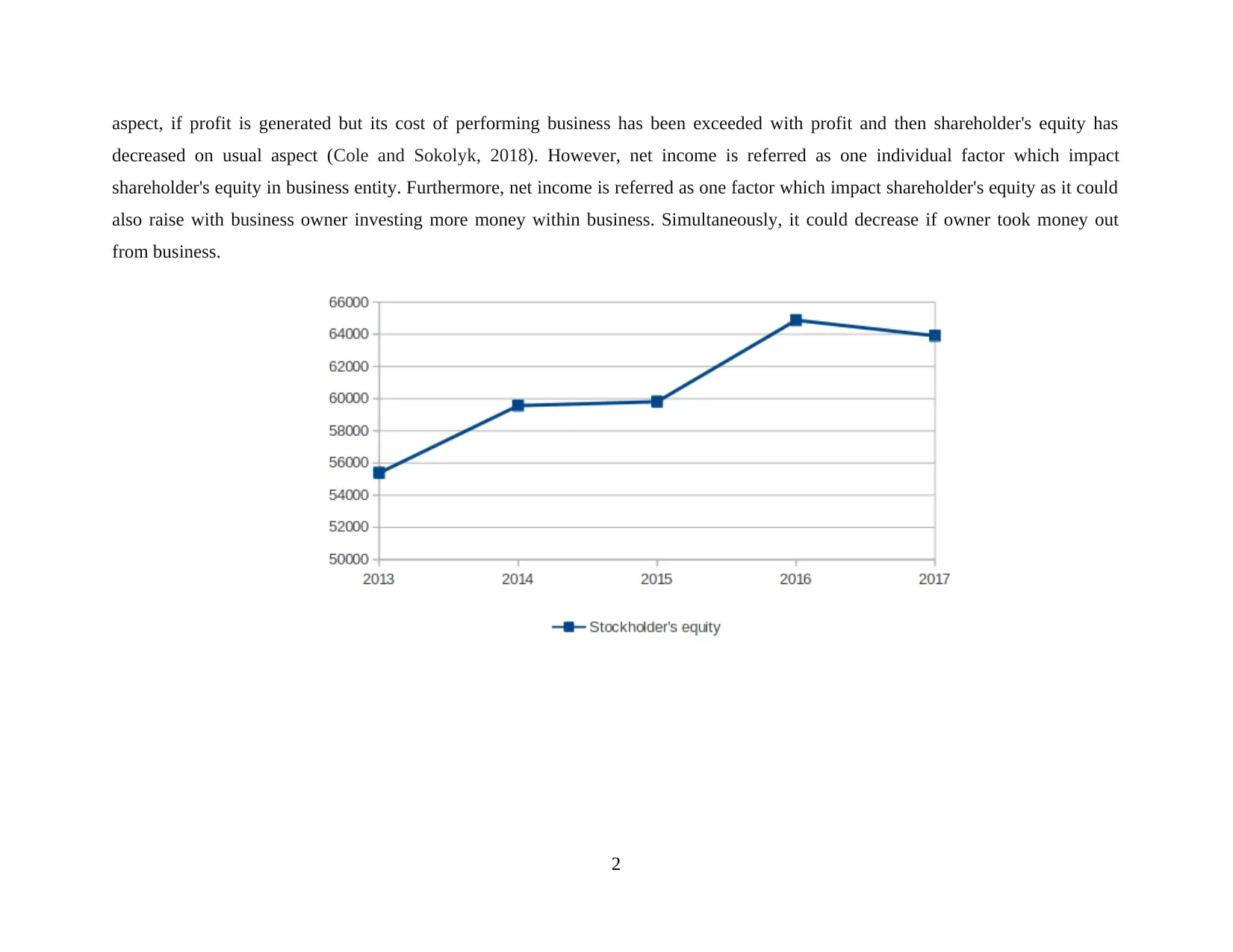

The operational performance of Barclays Plc analysed through measuring the consequences which affects the number of

shareholders to the organisation. To analyse such variations there will be collection of reliable information which have been gathered

from past 5 year’s performance of the organisation. The data is gathered through annual reports of the company. Income statement and

balance sheets are some major sources for gathering information regarding firm's financial performance of the company. It is

consisting of profits as well as revenue derived from operations. Along with this, there will be collection of details relevant with the

number of shareholder’s to be collected to analyse the information. The net income of organization contributes significant aspect for

identifying shareholder's equity. The net income is calculated by considering its revenues for specified duration and excluded the cost

of goods sold. The COGS consider all expenses which are used for operating business like payroll, advertising, rent, taxes and

equipment. In the similar aspect, shareholder's equity is liabilities which are excluded from its business assets as it is listed on

organization's balance sheet. It contributes to assets of company and impact the book value or shareholder's equity. If profit is

generated and with retention of portion of margin after excluding each cost where equity of owner generally increases. On the contrary

1

Data handling is the techniques of collecting the data and managing it in the books of accounts which will be adequate and

effective with respect to make appropriate analysis over firm’s performance. To implicate the reformative changes in the operations of

Barclays which reflect in potential growth of this banking industry. The company have been operating in UK with facilitating the

internal banking services which is comprised of various activities such as Corporate banking, personal banking, investment

management and wealth management. In the present assessment there will be determination of the facts which are affecting the growth

of industry. The analysis will be based on analysing impacts of profitability on the amount of funds derived through shareholders.

Thus, the profitability of this banking industry will affect the number of investors in each period. It will be consisting influences of

statistical tools to analyse the relationship between variables.

QUESTION

Statement of specific decision Barclays required to make

The operational performance of Barclays Plc analysed through measuring the consequences which affects the number of

shareholders to the organisation. To analyse such variations there will be collection of reliable information which have been gathered

from past 5 year’s performance of the organisation. The data is gathered through annual reports of the company. Income statement and

balance sheets are some major sources for gathering information regarding firm's financial performance of the company. It is

consisting of profits as well as revenue derived from operations. Along with this, there will be collection of details relevant with the

number of shareholder’s to be collected to analyse the information. The net income of organization contributes significant aspect for

identifying shareholder's equity. The net income is calculated by considering its revenues for specified duration and excluded the cost

of goods sold. The COGS consider all expenses which are used for operating business like payroll, advertising, rent, taxes and

equipment. In the similar aspect, shareholder's equity is liabilities which are excluded from its business assets as it is listed on

organization's balance sheet. It contributes to assets of company and impact the book value or shareholder's equity. If profit is

generated and with retention of portion of margin after excluding each cost where equity of owner generally increases. On the contrary

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

aspect, if profit is generated but its cost of performing business has been exceeded with profit and then shareholder's equity has

decreased on usual aspect (Cole and Sokolyk, 2018). However, net income is referred as one individual factor which impact

shareholder's equity in business entity. Furthermore, net income is referred as one factor which impact shareholder's equity as it could

also raise with business owner investing more money within business. Simultaneously, it could decrease if owner took money out

from business.

2

decreased on usual aspect (Cole and Sokolyk, 2018). However, net income is referred as one individual factor which impact

shareholder's equity in business entity. Furthermore, net income is referred as one factor which impact shareholder's equity as it could

also raise with business owner investing more money within business. Simultaneously, it could decrease if owner took money out

from business.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

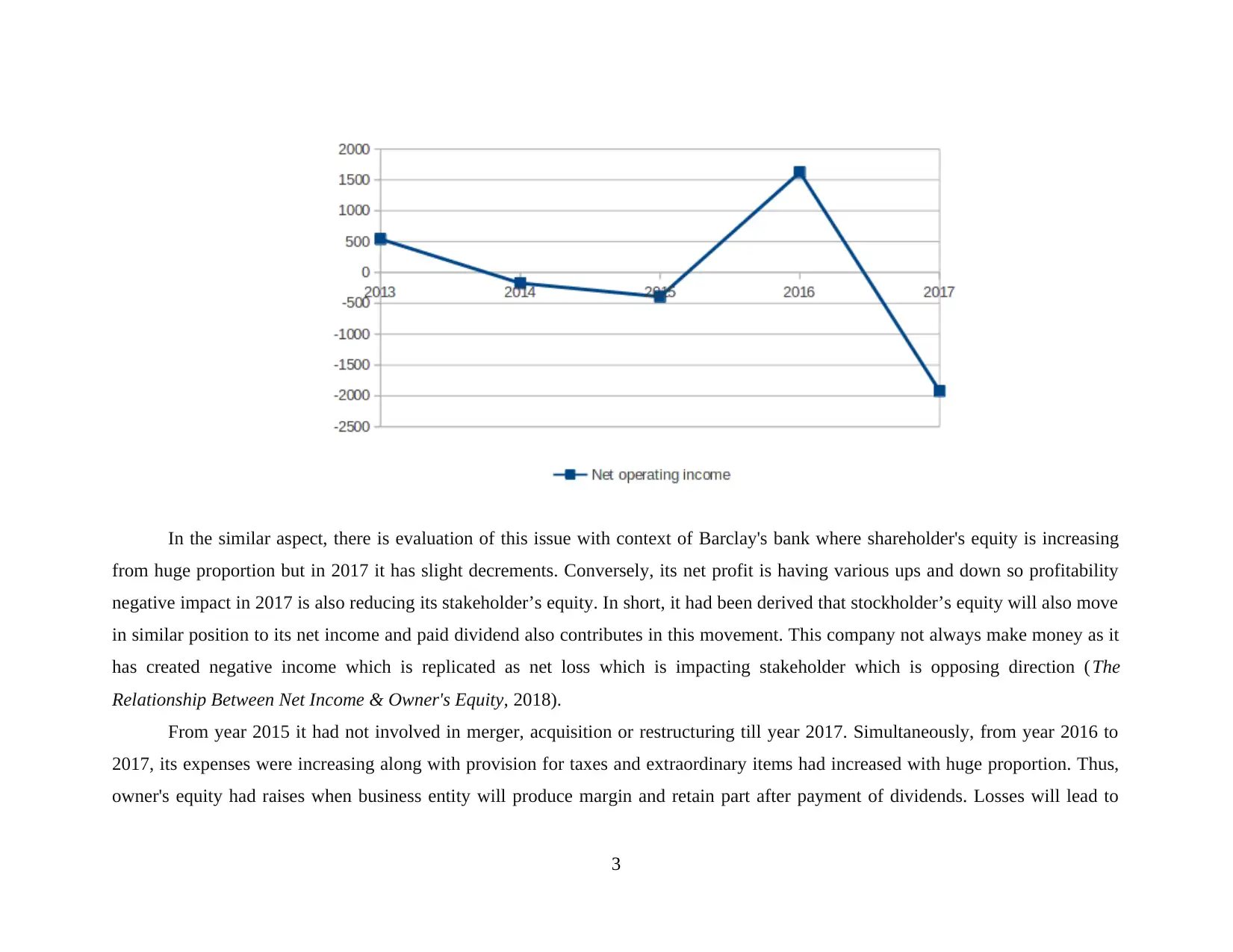

In the similar aspect, there is evaluation of this issue with context of Barclay's bank where shareholder's equity is increasing

from huge proportion but in 2017 it has slight decrements. Conversely, its net profit is having various ups and down so profitability

negative impact in 2017 is also reducing its stakeholder’s equity. In short, it had been derived that stockholder’s equity will also move

in similar position to its net income and paid dividend also contributes in this movement. This company not always make money as it

has created negative income which is replicated as net loss which is impacting stakeholder which is opposing direction ( The

Relationship Between Net Income & Owner's Equity, 2018).

From year 2015 it had not involved in merger, acquisition or restructuring till year 2017. Simultaneously, from year 2016 to

2017, its expenses were increasing along with provision for taxes and extraordinary items had increased with huge proportion. Thus,

owner's equity had raises when business entity will produce margin and retain part after payment of dividends. Losses will lead to

3

from huge proportion but in 2017 it has slight decrements. Conversely, its net profit is having various ups and down so profitability

negative impact in 2017 is also reducing its stakeholder’s equity. In short, it had been derived that stockholder’s equity will also move

in similar position to its net income and paid dividend also contributes in this movement. This company not always make money as it

has created negative income which is replicated as net loss which is impacting stakeholder which is opposing direction ( The

Relationship Between Net Income & Owner's Equity, 2018).

From year 2015 it had not involved in merger, acquisition or restructuring till year 2017. Simultaneously, from year 2016 to

2017, its expenses were increasing along with provision for taxes and extraordinary items had increased with huge proportion. Thus,

owner's equity had raises when business entity will produce margin and retain part after payment of dividends. Losses will lead to

3

decreasing this equity and owner could put additional cash for continuing its operations and sell off surplus assets for raising cash and

to liquidate its assets or to keep appropriate track of its expenses for increasing net income along with shareholder's equity.

In respect with the operational performance of the Barclays on which there have been use of 5 years of financial information

which will be measured to analyses the firm’s performance in this respective period. Thus, it must be said that there is requirement of

making operating changes which will help and govern the professionals in reducing the costs implicated in the operations.

Data integrity:

All data regarding Barclays plc is collected through audited financial reports or audited annual reports of the company. In this

regard, it can be said that the report contains data integrity, as the audited annual reports provides more reliable information than an

non audited financial reports.

Descripting of relevant information used for analysis

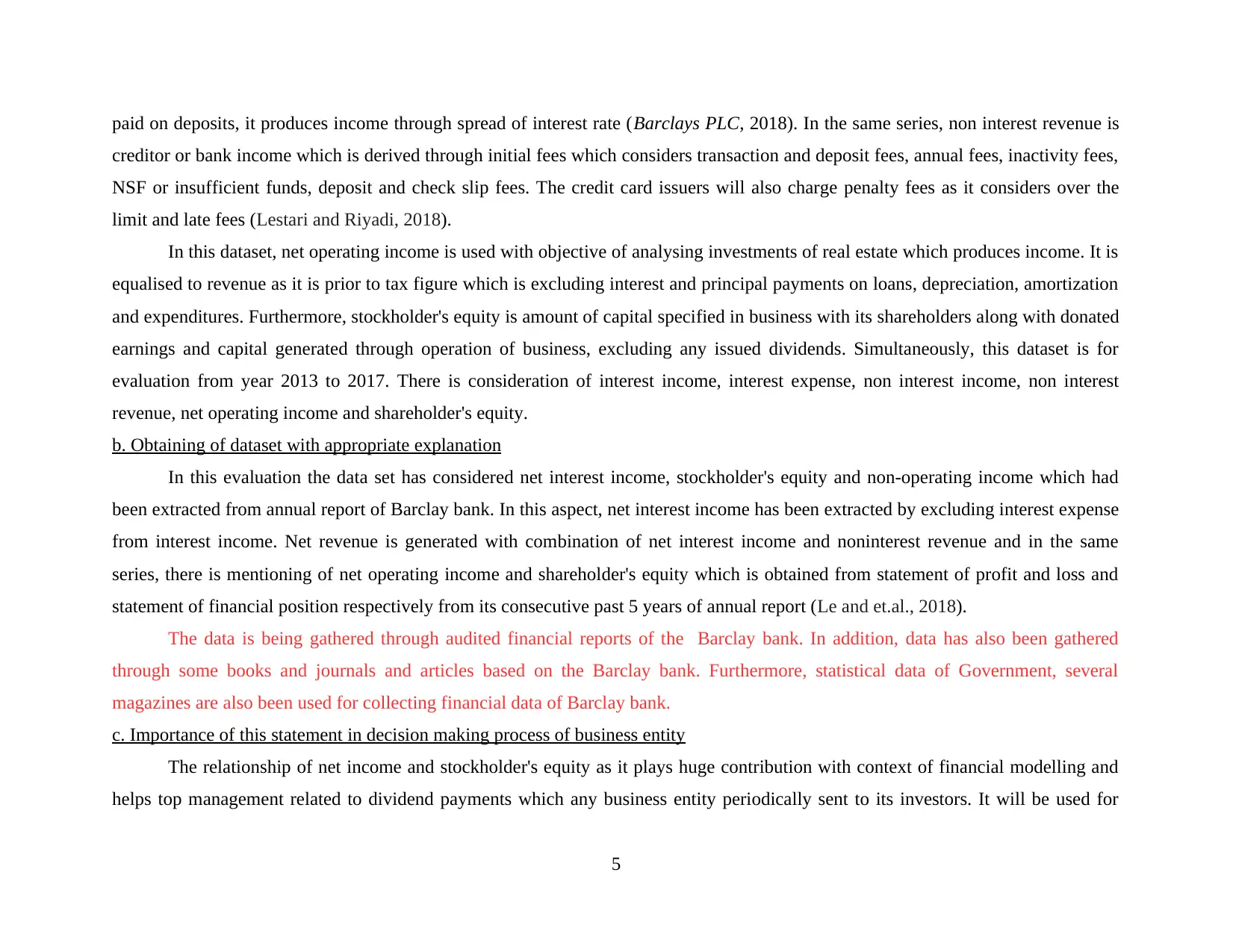

a. Discussion of information related to business with representation of dataset

Year

Interest

income

Interest

expenses

Net

interest

income

Non

interest

revenue

Net

revenue

Net

operating

income

Stockhold

er's equity

2013 18315 6715 11600 16844 28444 540 55385

2014 17363 5283 12080 13688 25768 -174 59567

2015 17201 4643 12558 13426 25984 -394 59810

2016 14541 4004 10537 10914 21451 1623 64873

2017 13631 3786 9845 11231 21076 -1922 63905

The main business of Barclay bank is for managing spread among deposits which is paid to consumer at particular rate which

had been gained from loans. In simple words, interest which had been earned by bank through loans is higher from interests which is

4

to liquidate its assets or to keep appropriate track of its expenses for increasing net income along with shareholder's equity.

In respect with the operational performance of the Barclays on which there have been use of 5 years of financial information

which will be measured to analyses the firm’s performance in this respective period. Thus, it must be said that there is requirement of

making operating changes which will help and govern the professionals in reducing the costs implicated in the operations.

Data integrity:

All data regarding Barclays plc is collected through audited financial reports or audited annual reports of the company. In this

regard, it can be said that the report contains data integrity, as the audited annual reports provides more reliable information than an

non audited financial reports.

Descripting of relevant information used for analysis

a. Discussion of information related to business with representation of dataset

Year

Interest

income

Interest

expenses

Net

interest

income

Non

interest

revenue

Net

revenue

Net

operating

income

Stockhold

er's equity

2013 18315 6715 11600 16844 28444 540 55385

2014 17363 5283 12080 13688 25768 -174 59567

2015 17201 4643 12558 13426 25984 -394 59810

2016 14541 4004 10537 10914 21451 1623 64873

2017 13631 3786 9845 11231 21076 -1922 63905

The main business of Barclay bank is for managing spread among deposits which is paid to consumer at particular rate which

had been gained from loans. In simple words, interest which had been earned by bank through loans is higher from interests which is

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

paid on deposits, it produces income through spread of interest rate (Barclays PLC, 2018). In the same series, non interest revenue is

creditor or bank income which is derived through initial fees which considers transaction and deposit fees, annual fees, inactivity fees,

NSF or insufficient funds, deposit and check slip fees. The credit card issuers will also charge penalty fees as it considers over the

limit and late fees (Lestari and Riyadi, 2018).

In this dataset, net operating income is used with objective of analysing investments of real estate which produces income. It is

equalised to revenue as it is prior to tax figure which is excluding interest and principal payments on loans, depreciation, amortization

and expenditures. Furthermore, stockholder's equity is amount of capital specified in business with its shareholders along with donated

earnings and capital generated through operation of business, excluding any issued dividends. Simultaneously, this dataset is for

evaluation from year 2013 to 2017. There is consideration of interest income, interest expense, non interest income, non interest

revenue, net operating income and shareholder's equity.

b. Obtaining of dataset with appropriate explanation

In this evaluation the data set has considered net interest income, stockholder's equity and non-operating income which had

been extracted from annual report of Barclay bank. In this aspect, net interest income has been extracted by excluding interest expense

from interest income. Net revenue is generated with combination of net interest income and noninterest revenue and in the same

series, there is mentioning of net operating income and shareholder's equity which is obtained from statement of profit and loss and

statement of financial position respectively from its consecutive past 5 years of annual report (Le and et.al., 2018).

The data is being gathered through audited financial reports of the Barclay bank. In addition, data has also been gathered

through some books and journals and articles based on the Barclay bank. Furthermore, statistical data of Government, several

magazines are also been used for collecting financial data of Barclay bank.

c. Importance of this statement in decision making process of business entity

The relationship of net income and stockholder's equity as it plays huge contribution with context of financial modelling and

helps top management related to dividend payments which any business entity periodically sent to its investors. It will be used for

5

creditor or bank income which is derived through initial fees which considers transaction and deposit fees, annual fees, inactivity fees,

NSF or insufficient funds, deposit and check slip fees. The credit card issuers will also charge penalty fees as it considers over the

limit and late fees (Lestari and Riyadi, 2018).

In this dataset, net operating income is used with objective of analysing investments of real estate which produces income. It is

equalised to revenue as it is prior to tax figure which is excluding interest and principal payments on loans, depreciation, amortization

and expenditures. Furthermore, stockholder's equity is amount of capital specified in business with its shareholders along with donated

earnings and capital generated through operation of business, excluding any issued dividends. Simultaneously, this dataset is for

evaluation from year 2013 to 2017. There is consideration of interest income, interest expense, non interest income, non interest

revenue, net operating income and shareholder's equity.

b. Obtaining of dataset with appropriate explanation

In this evaluation the data set has considered net interest income, stockholder's equity and non-operating income which had

been extracted from annual report of Barclay bank. In this aspect, net interest income has been extracted by excluding interest expense

from interest income. Net revenue is generated with combination of net interest income and noninterest revenue and in the same

series, there is mentioning of net operating income and shareholder's equity which is obtained from statement of profit and loss and

statement of financial position respectively from its consecutive past 5 years of annual report (Le and et.al., 2018).

The data is being gathered through audited financial reports of the Barclay bank. In addition, data has also been gathered

through some books and journals and articles based on the Barclay bank. Furthermore, statistical data of Government, several

magazines are also been used for collecting financial data of Barclay bank.

c. Importance of this statement in decision making process of business entity

The relationship of net income and stockholder's equity as it plays huge contribution with context of financial modelling and

helps top management related to dividend payments which any business entity periodically sent to its investors. It will be used for

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

maximising business value and to increase its impact on profit or margin. It is major tool which could be used for investing

perspective as it is extremely varied which is highly dependent on method of any individual organization. It is organised with

company perspective and pertained to ownership, preferred stock, paid in capital and for increment or diluting over time and

explanation about alteration in shareholder's equity.

In the same series, it will also help in gaining financial performance, position and for peer comparison as well along with

getting rough idea about dividends. In nutshell, it has been elaborated that for assisting in better decision making this relationship

helps majorly to investors, creditors and lenders. With perspective of investors, it performs fiscal analysis as basis of decision making

to invest or not whereas lending institutions will be examining financial health and confirms with presence of capacity for servicing

debt. This will help creditor as well, vendors with extension of credit might use this relationship for assessing credit worthiness of

business (Graham and Lin, 2018).

Analysing the data mining procedures from data set

Data preparation, cleaning and filtering

In respect with analysing the relationship between the profitability and number of shareholders to the firm there have been use of

various information such as Net income, operating income and shareholder equity of Barclays from 2013 to 2017 (Roth, 2018).

Implicating the descriptive data analysis effective for immediate observation for business performance

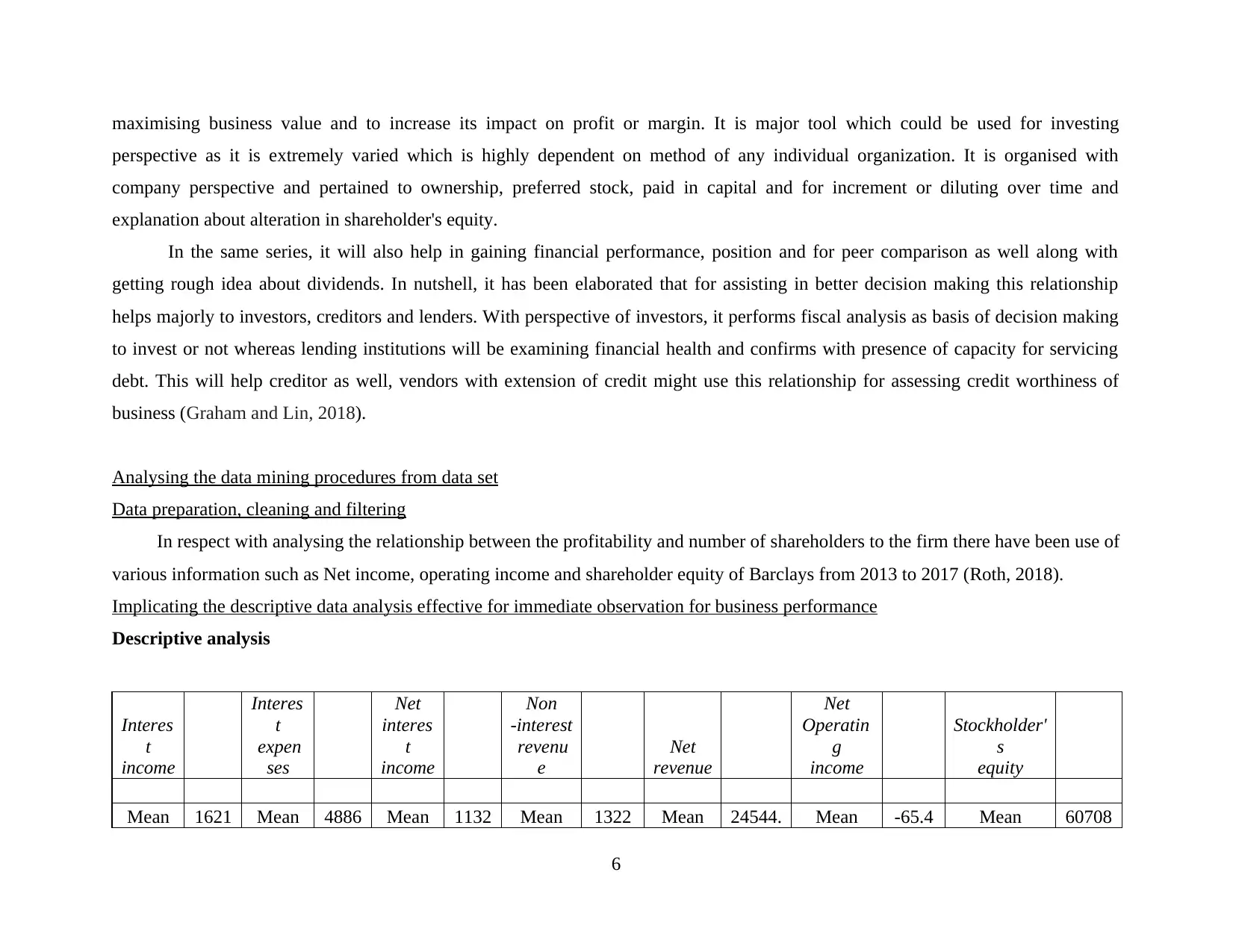

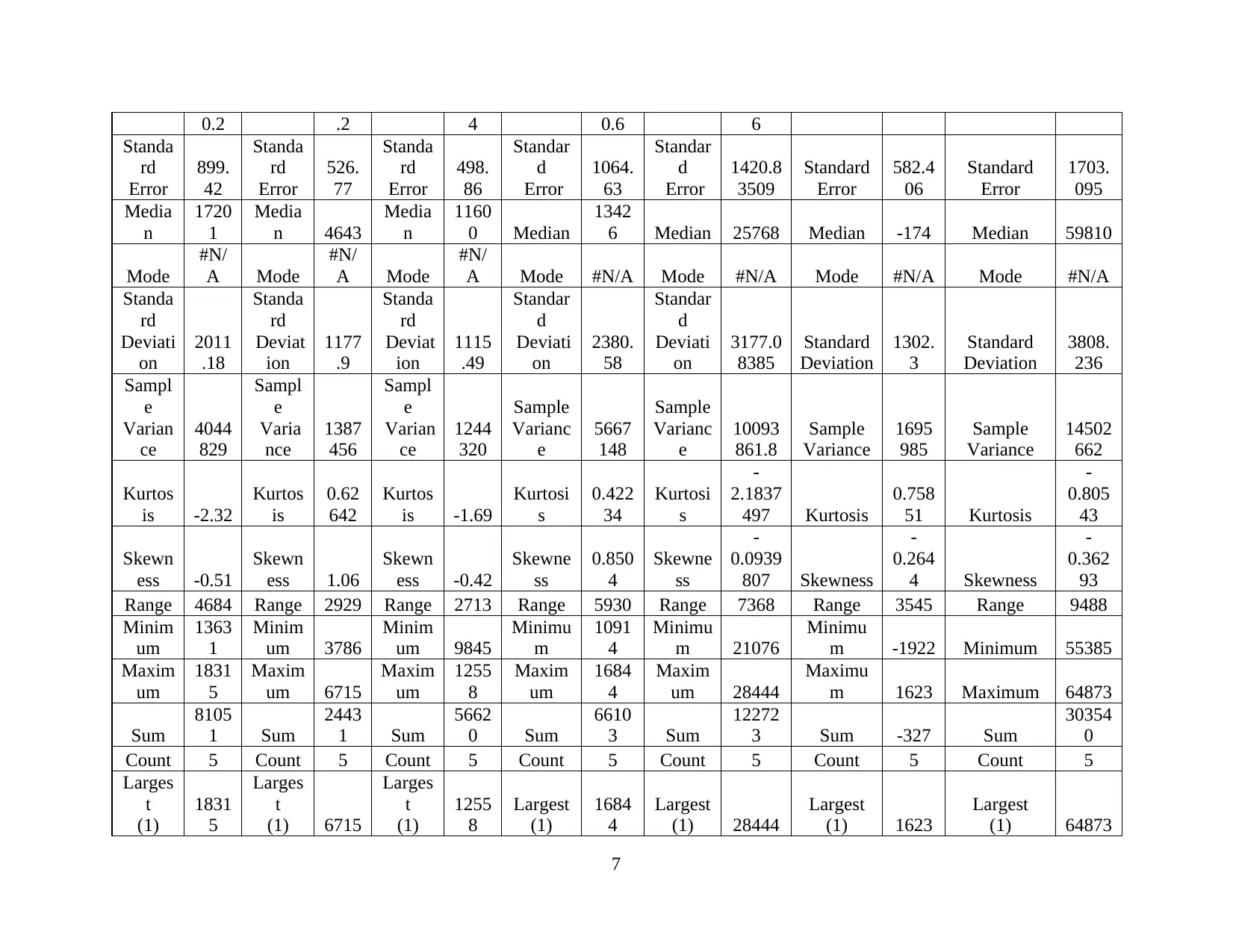

Descriptive analysis

Interes

t

income

Interes

t

expen

ses

Net

interes

t

income

Non

-interest

revenu

e

Net

revenue

Net

Operatin

g

income

Stockholder'

s

equity

Mean 1621 Mean 4886 Mean 1132 Mean 1322 Mean 24544. Mean -65.4 Mean 60708

6

perspective as it is extremely varied which is highly dependent on method of any individual organization. It is organised with

company perspective and pertained to ownership, preferred stock, paid in capital and for increment or diluting over time and

explanation about alteration in shareholder's equity.

In the same series, it will also help in gaining financial performance, position and for peer comparison as well along with

getting rough idea about dividends. In nutshell, it has been elaborated that for assisting in better decision making this relationship

helps majorly to investors, creditors and lenders. With perspective of investors, it performs fiscal analysis as basis of decision making

to invest or not whereas lending institutions will be examining financial health and confirms with presence of capacity for servicing

debt. This will help creditor as well, vendors with extension of credit might use this relationship for assessing credit worthiness of

business (Graham and Lin, 2018).

Analysing the data mining procedures from data set

Data preparation, cleaning and filtering

In respect with analysing the relationship between the profitability and number of shareholders to the firm there have been use of

various information such as Net income, operating income and shareholder equity of Barclays from 2013 to 2017 (Roth, 2018).

Implicating the descriptive data analysis effective for immediate observation for business performance

Descriptive analysis

Interes

t

income

Interes

t

expen

ses

Net

interes

t

income

Non

-interest

revenu

e

Net

revenue

Net

Operatin

g

income

Stockholder'

s

equity

Mean 1621 Mean 4886 Mean 1132 Mean 1322 Mean 24544. Mean -65.4 Mean 60708

6

0.2 .2 4 0.6 6

Standa

rd

Error

899.

42

Standa

rd

Error

526.

77

Standa

rd

Error

498.

86

Standar

d

Error

1064.

63

Standar

d

Error

1420.8

3509

Standard

Error

582.4

06

Standard

Error

1703.

095

Media

n

1720

1

Media

n 4643

Media

n

1160

0 Median

1342

6 Median 25768 Median -174 Median 59810

Mode

#N/

A Mode

#N/

A Mode

#N/

A Mode #N/A Mode #N/A Mode #N/A Mode #N/A

Standa

rd

Deviati

on

2011

.18

Standa

rd

Deviat

ion

1177

.9

Standa

rd

Deviat

ion

1115

.49

Standar

d

Deviati

on

2380.

58

Standar

d

Deviati

on

3177.0

8385

Standard

Deviation

1302.

3

Standard

Deviation

3808.

236

Sampl

e

Varian

ce

4044

829

Sampl

e

Varia

nce

1387

456

Sampl

e

Varian

ce

1244

320

Sample

Varianc

e

5667

148

Sample

Varianc

e

10093

861.8

Sample

Variance

1695

985

Sample

Variance

14502

662

Kurtos

is -2.32

Kurtos

is

0.62

642

Kurtos

is -1.69

Kurtosi

s

0.422

34

Kurtosi

s

-

2.1837

497 Kurtosis

0.758

51 Kurtosis

-

0.805

43

Skewn

ess -0.51

Skewn

ess 1.06

Skewn

ess -0.42

Skewne

ss

0.850

4

Skewne

ss

-

0.0939

807 Skewness

-

0.264

4 Skewness

-

0.362

93

Range 4684 Range 2929 Range 2713 Range 5930 Range 7368 Range 3545 Range 9488

Minim

um

1363

1

Minim

um 3786

Minim

um 9845

Minimu

m

1091

4

Minimu

m 21076

Minimu

m -1922 Minimum 55385

Maxim

um

1831

5

Maxim

um 6715

Maxim

um

1255

8

Maxim

um

1684

4

Maxim

um 28444

Maximu

m 1623 Maximum 64873

Sum

8105

1 Sum

2443

1 Sum

5662

0 Sum

6610

3 Sum

12272

3 Sum -327 Sum

30354

0

Count 5 Count 5 Count 5 Count 5 Count 5 Count 5 Count 5

Larges

t

(1)

1831

5

Larges

t

(1) 6715

Larges

t

(1)

1255

8

Largest

(1)

1684

4

Largest

(1) 28444

Largest

(1) 1623

Largest

(1) 64873

7

Standa

rd

Error

899.

42

Standa

rd

Error

526.

77

Standa

rd

Error

498.

86

Standar

d

Error

1064.

63

Standar

d

Error

1420.8

3509

Standard

Error

582.4

06

Standard

Error

1703.

095

Media

n

1720

1

Media

n 4643

Media

n

1160

0 Median

1342

6 Median 25768 Median -174 Median 59810

Mode

#N/

A Mode

#N/

A Mode

#N/

A Mode #N/A Mode #N/A Mode #N/A Mode #N/A

Standa

rd

Deviati

on

2011

.18

Standa

rd

Deviat

ion

1177

.9

Standa

rd

Deviat

ion

1115

.49

Standar

d

Deviati

on

2380.

58

Standar

d

Deviati

on

3177.0

8385

Standard

Deviation

1302.

3

Standard

Deviation

3808.

236

Sampl

e

Varian

ce

4044

829

Sampl

e

Varia

nce

1387

456

Sampl

e

Varian

ce

1244

320

Sample

Varianc

e

5667

148

Sample

Varianc

e

10093

861.8

Sample

Variance

1695

985

Sample

Variance

14502

662

Kurtos

is -2.32

Kurtos

is

0.62

642

Kurtos

is -1.69

Kurtosi

s

0.422

34

Kurtosi

s

-

2.1837

497 Kurtosis

0.758

51 Kurtosis

-

0.805

43

Skewn

ess -0.51

Skewn

ess 1.06

Skewn

ess -0.42

Skewne

ss

0.850

4

Skewne

ss

-

0.0939

807 Skewness

-

0.264

4 Skewness

-

0.362

93

Range 4684 Range 2929 Range 2713 Range 5930 Range 7368 Range 3545 Range 9488

Minim

um

1363

1

Minim

um 3786

Minim

um 9845

Minimu

m

1091

4

Minimu

m 21076

Minimu

m -1922 Minimum 55385

Maxim

um

1831

5

Maxim

um 6715

Maxim

um

1255

8

Maxim

um

1684

4

Maxim

um 28444

Maximu

m 1623 Maximum 64873

Sum

8105

1 Sum

2443

1 Sum

5662

0 Sum

6610

3 Sum

12272

3 Sum -327 Sum

30354

0

Count 5 Count 5 Count 5 Count 5 Count 5 Count 5 Count 5

Larges

t

(1)

1831

5

Larges

t

(1) 6715

Larges

t

(1)

1255

8

Largest

(1)

1684

4

Largest

(1) 28444

Largest

(1) 1623

Largest

(1) 64873

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Smalle

st

(1)

1363

1

Smalle

st

(1) 3786

Smalle

st

(1) 9845

Smalles

t

(1)

1091

4

Smalles

t

(1) 21076

Smallest

(1) -1922

Smallest

(1) 55385

Confid

ence

Level

(95.0%

)

2497

.2

Confid

ence

Level

(95.0%

)

1462

.56

Confid

ence

Level

(95.0%

)

1385

.06

Confide

nce

Level

(95.0%)

2955.

88

Confide

nce

Level

(95.0%

)

3944.8

7064

Confiden

ce

Level

(95.0%)

1617.

02

Confidence

Level

(95.0%)

4728.

55

Interpretation: On the basis of above listed descriptive analysis on which there have been use of various details and

ascertainment of statistical outcomes. Thus, the mean value of all the data which have been considered by researcher in this process

that defines results of revenue, profits and equity balance of the organisation. In analysing the outcomes on which it can be said that

there has been implication of various techniques which in turn will be useful and effective to have demonstration over the use of

techniques for growth planning and analysing the level of investors associated with the business. Therefore, the mean value of

variables which have been used by professionals such as revenue generated through interest by Barclays were average at 1621.02,

Interest expenses were 4886.2 respectively.

Therefore, such outcomes have represented that the net income through interest were 11324. Along with this, in analysing the

non-interest income of this banking industry which have presented the outcomes as 13220.6 which have present the net revenue of the

firm as 24544.6. In analysing the operating income of the organisation there have been determination of higher operating expenses

which have been incurred by industries were comparatively higher (3 Ways Big Data Can Influence Decision-Making for

Organizations, 2018). Thus, due to such impacts there have been reduction in the operating income of the business which is reflecting

the negative outcomes. Moreover, in respect with analysing the mean value of operating income which is -65.4. In analysing the

average value of shareholders of the firm in respective 5 years of period which have been determined as 60708.

Correlation analysis:

8

st

(1)

1363

1

Smalle

st

(1) 3786

Smalle

st

(1) 9845

Smalles

t

(1)

1091

4

Smalles

t

(1) 21076

Smallest

(1) -1922

Smallest

(1) 55385

Confid

ence

Level

(95.0%

)

2497

.2

Confid

ence

Level

(95.0%

)

1462

.56

Confid

ence

Level

(95.0%

)

1385

.06

Confide

nce

Level

(95.0%)

2955.

88

Confide

nce

Level

(95.0%

)

3944.8

7064

Confiden

ce

Level

(95.0%)

1617.

02

Confidence

Level

(95.0%)

4728.

55

Interpretation: On the basis of above listed descriptive analysis on which there have been use of various details and

ascertainment of statistical outcomes. Thus, the mean value of all the data which have been considered by researcher in this process

that defines results of revenue, profits and equity balance of the organisation. In analysing the outcomes on which it can be said that

there has been implication of various techniques which in turn will be useful and effective to have demonstration over the use of

techniques for growth planning and analysing the level of investors associated with the business. Therefore, the mean value of

variables which have been used by professionals such as revenue generated through interest by Barclays were average at 1621.02,

Interest expenses were 4886.2 respectively.

Therefore, such outcomes have represented that the net income through interest were 11324. Along with this, in analysing the

non-interest income of this banking industry which have presented the outcomes as 13220.6 which have present the net revenue of the

firm as 24544.6. In analysing the operating income of the organisation there have been determination of higher operating expenses

which have been incurred by industries were comparatively higher (3 Ways Big Data Can Influence Decision-Making for

Organizations, 2018). Thus, due to such impacts there have been reduction in the operating income of the business which is reflecting

the negative outcomes. Moreover, in respect with analysing the mean value of operating income which is -65.4. In analysing the

average value of shareholders of the firm in respective 5 years of period which have been determined as 60708.

Correlation analysis:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

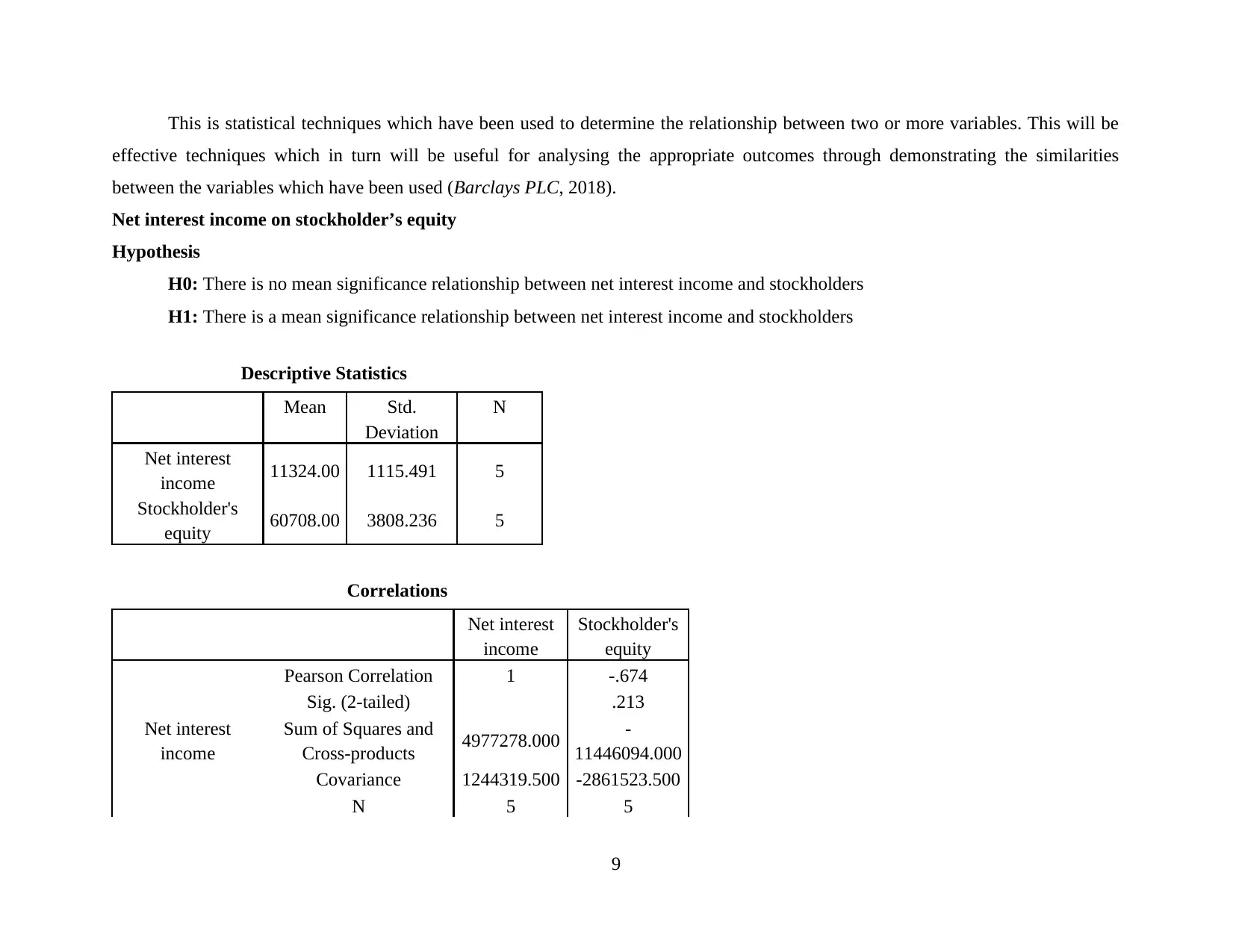

This is statistical techniques which have been used to determine the relationship between two or more variables. This will be

effective techniques which in turn will be useful for analysing the appropriate outcomes through demonstrating the similarities

between the variables which have been used (Barclays PLC, 2018).

Net interest income on stockholder’s equity

Hypothesis

H0: There is no mean significance relationship between net interest income and stockholders

H1: There is a mean significance relationship between net interest income and stockholders

Descriptive Statistics

Mean Std.

Deviation

N

Net interest

income 11324.00 1115.491 5

Stockholder's

equity 60708.00 3808.236 5

Correlations

Net interest

income

Stockholder's

equity

Net interest

income

Pearson Correlation 1 -.674

Sig. (2-tailed) .213

Sum of Squares and

Cross-products 4977278.000 -

11446094.000

Covariance 1244319.500 -2861523.500

N 5 5

9

effective techniques which in turn will be useful for analysing the appropriate outcomes through demonstrating the similarities

between the variables which have been used (Barclays PLC, 2018).

Net interest income on stockholder’s equity

Hypothesis

H0: There is no mean significance relationship between net interest income and stockholders

H1: There is a mean significance relationship between net interest income and stockholders

Descriptive Statistics

Mean Std.

Deviation

N

Net interest

income 11324.00 1115.491 5

Stockholder's

equity 60708.00 3808.236 5

Correlations

Net interest

income

Stockholder's

equity

Net interest

income

Pearson Correlation 1 -.674

Sig. (2-tailed) .213

Sum of Squares and

Cross-products 4977278.000 -

11446094.000

Covariance 1244319.500 -2861523.500

N 5 5

9

Stockholder's

equity

Pearson Correlation -.674 1

Sig. (2-tailed) .213

Sum of Squares and

Cross-products

-

11446094.00

0

58010648.000

Covariance -2861523.500 14502662.000

N 5 5

Interpretation: On the basis of analyzing the correlation among the net interest income and stockholders of the organisation.

The outcomes represented the negative results which in turn presenting that, there have been negative relationship between variables.

The level of defining relationship between the variables in -1 to +1. In accordance with these outcomes on which there have been

negative relationship among the variables. -0.674 proves the null hypothesis which defines that, there is no mean significance

relationship between net interest income and stockholders.

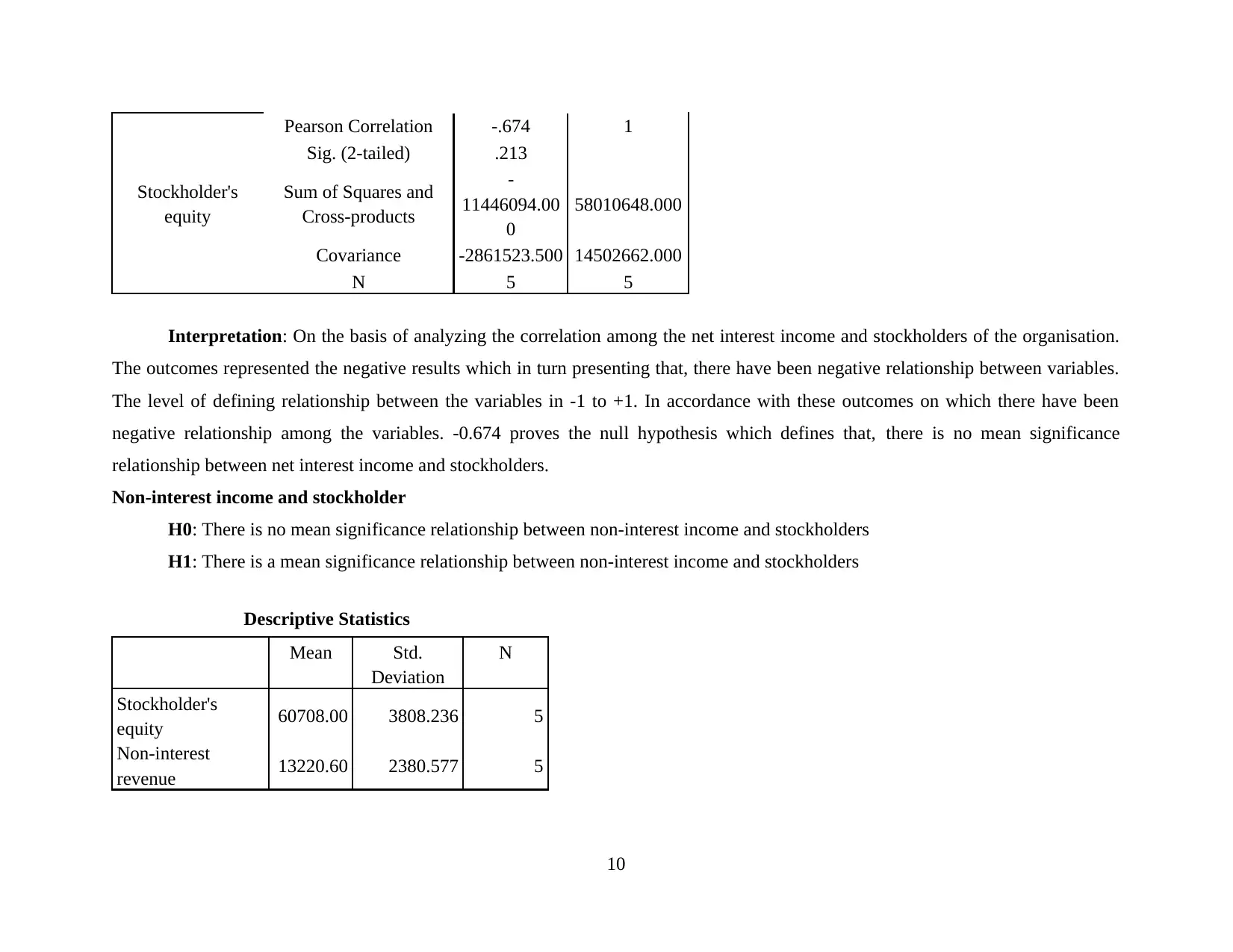

Non-interest income and stockholder

H0: There is no mean significance relationship between non-interest income and stockholders

H1: There is a mean significance relationship between non-interest income and stockholders

Descriptive Statistics

Mean Std.

Deviation

N

Stockholder's

equity 60708.00 3808.236 5

Non-interest

revenue 13220.60 2380.577 5

10

equity

Pearson Correlation -.674 1

Sig. (2-tailed) .213

Sum of Squares and

Cross-products

-

11446094.00

0

58010648.000

Covariance -2861523.500 14502662.000

N 5 5

Interpretation: On the basis of analyzing the correlation among the net interest income and stockholders of the organisation.

The outcomes represented the negative results which in turn presenting that, there have been negative relationship between variables.

The level of defining relationship between the variables in -1 to +1. In accordance with these outcomes on which there have been

negative relationship among the variables. -0.674 proves the null hypothesis which defines that, there is no mean significance

relationship between net interest income and stockholders.

Non-interest income and stockholder

H0: There is no mean significance relationship between non-interest income and stockholders

H1: There is a mean significance relationship between non-interest income and stockholders

Descriptive Statistics

Mean Std.

Deviation

N

Stockholder's

equity 60708.00 3808.236 5

Non-interest

revenue 13220.60 2380.577 5

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.