ACC510 S1 Financial Reporting: A Detailed Analysis of Barra Resources

VerifiedAdded on 2023/06/12

|15

|2345

|180

Report

AI Summary

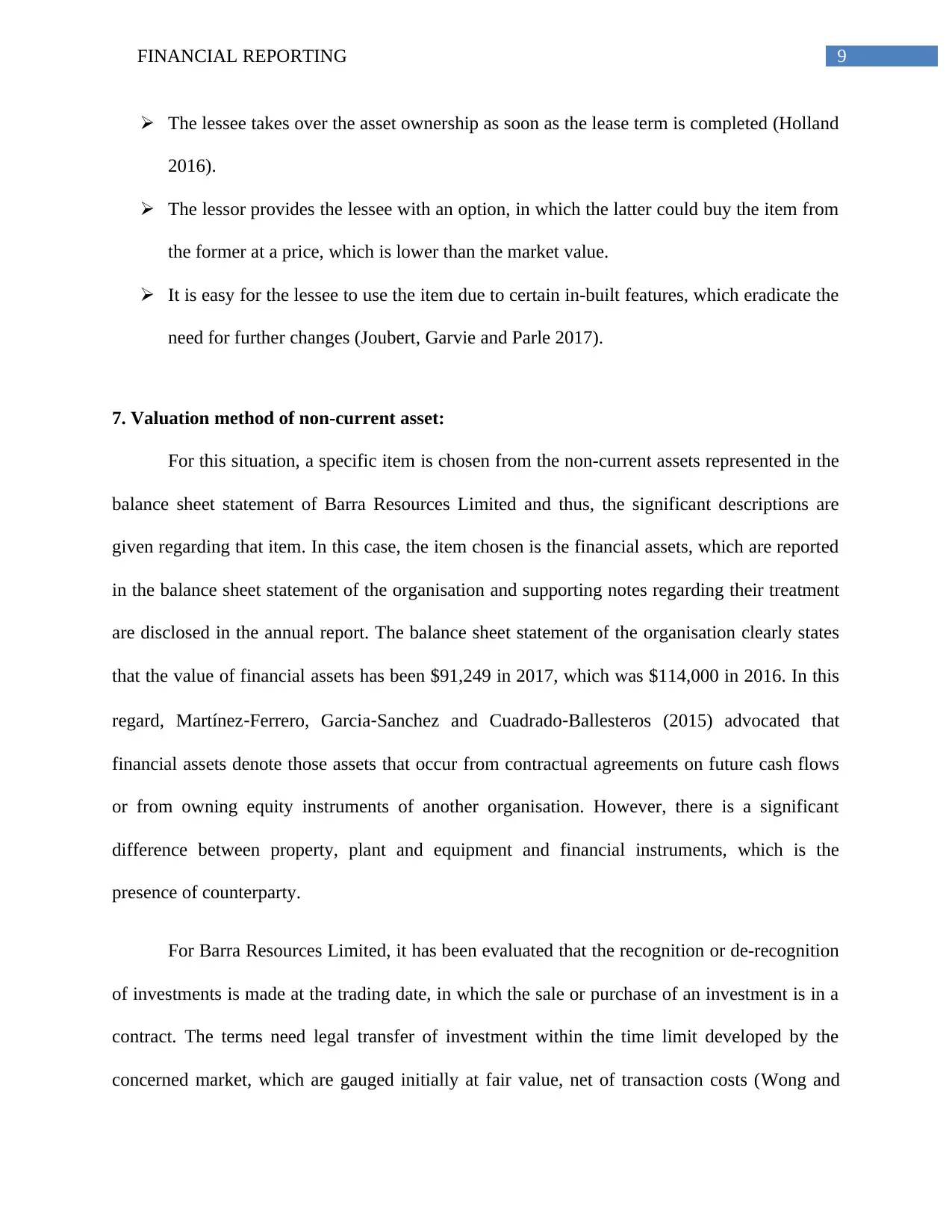

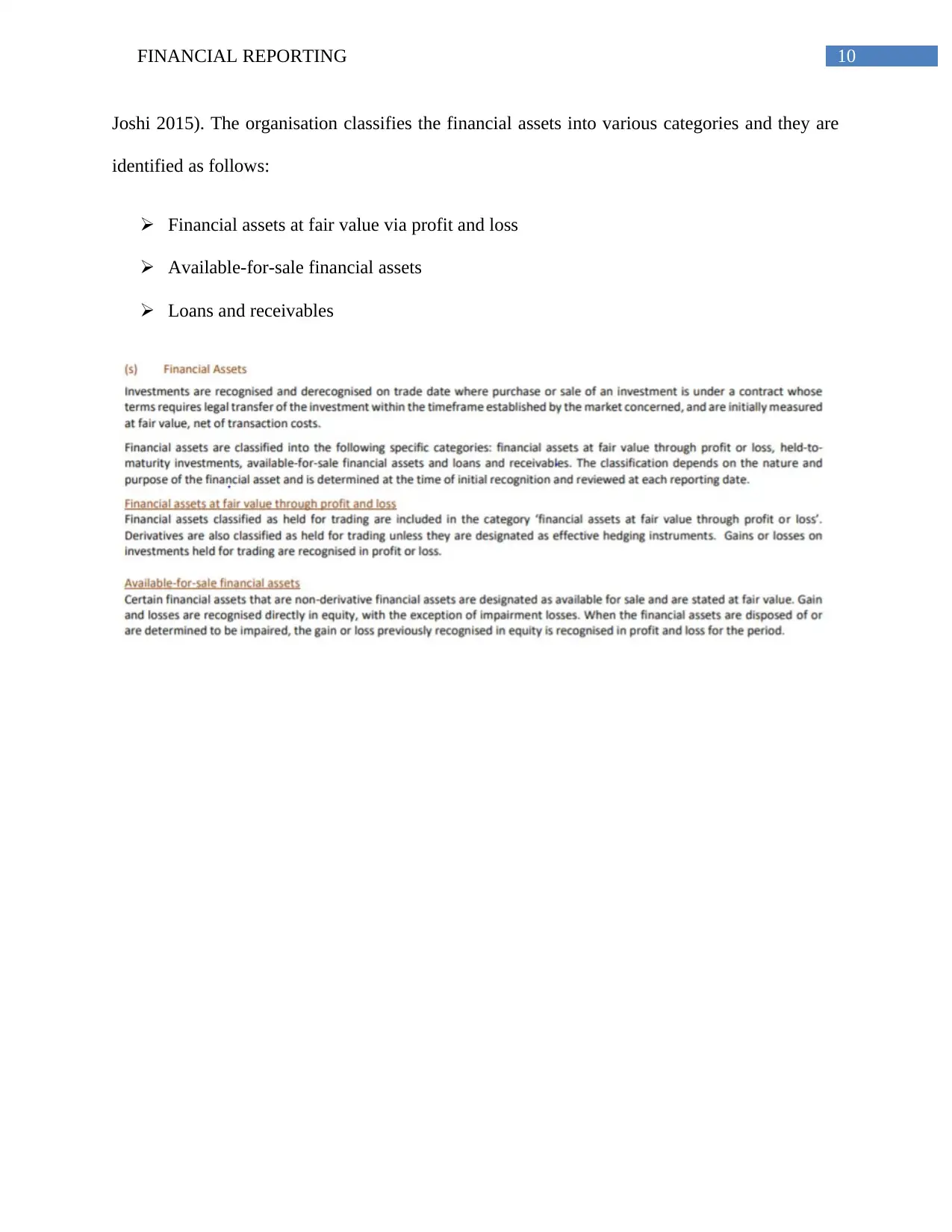

This report provides a detailed analysis of Barra Resources Limited's financial reporting practices based on their 2017 annual report. It examines the provisions and contingencies disclosed, including rehabilitation expenses and contingent liabilities related to terminated contracts, and discusses the recognition criteria and measurement issues associated with them. The report also analyzes the leased items recorded by the company, focusing on plant, property, and equipment, and explores the relevant classification and presentation requirements under AASB 16. A hypothetical scenario for reclassifying a leased item is presented, along with a discussion of the valuation method used for non-current assets, specifically financial assets, and an alternative valuation method using the equity method. The analysis concludes that Barra Resources Limited generally adheres to AASB norms, but suggests areas for improved disclosure to enhance financial reporting quality. Desklib provides access to a wealth of similar solved assignments and past papers for students.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.