Comprehensive Financial Analysis Report: Barrick Gold Corp

VerifiedAdded on 2023/06/10

|15

|2321

|55

Report

AI Summary

This report provides a financial analysis of Barrick Gold Corporation, a leading gold mining company. It examines the company's core business activities, changes in financial performance based on the chairman's message, and key financial ratios for 2014 and 2015. The analysis includes profitability, liquidity, efficiency, and solvency assessments, revealing that Barrick is facing challenges in maintaining its financial health due to declining revenues and rising operating expenses. The report concludes with recommendations to minimize inventory, reduce operating costs, and raise equity to alleviate the debt burden, suggesting measures to improve Barrick's financial position and competitive edge in the global marketplace. Desklib provides this report as a study resource, offering solved assignments and past papers for students.

Running head: ACCOUNTING FINANCIAL ANALYSIS

Accounting Financial Analysis

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounting Financial Analysis

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FINANCIAL ANALYSIS

Table of Contents

Executive Summary:..................................................................................................................2

Introduction:...............................................................................................................................3

Discussion/ Findings:.................................................................................................................4

1. Core business activity and/ or operating segments of Barrick Gold Corporation:............4

2. Significant changes in financial performance of the organisation from the chairman’s

message or managing director’s review:................................................................................4

3. Computation of the key financial ratios of Barrick Gold Corporation for the years 2014

and 2015:................................................................................................................................5

4. Overall assessment of Barrick Gold Corporation and its future prospects:.......................6

Conclusion and recommendations:..........................................................................................10

List of references:.....................................................................................................................11

Appendices:..............................................................................................................................13

Table of Contents

Executive Summary:..................................................................................................................2

Introduction:...............................................................................................................................3

Discussion/ Findings:.................................................................................................................4

1. Core business activity and/ or operating segments of Barrick Gold Corporation:............4

2. Significant changes in financial performance of the organisation from the chairman’s

message or managing director’s review:................................................................................4

3. Computation of the key financial ratios of Barrick Gold Corporation for the years 2014

and 2015:................................................................................................................................5

4. Overall assessment of Barrick Gold Corporation and its future prospects:.......................6

Conclusion and recommendations:..........................................................................................10

List of references:.....................................................................................................................11

Appendices:..............................................................................................................................13

2ACCOUNTING FINANCIAL ANALYSIS

Executive Summary:

The current report provides a brief overview of the financial condition of Barrick

Gold Corporation, which is one of the largest gold mining companies in the world. Even

though the organisation has succeeded in achieving its set financial targets in 2015 according

to chairman’s message, the financial analysis conducted states that it is struggling to maintain

its competitive position in the global marketplace. Hence, it is recommended to minimise

inventory, operating costs along with raising funds through issuance of additional equity

shares for minimising the overall debt burden.

Executive Summary:

The current report provides a brief overview of the financial condition of Barrick

Gold Corporation, which is one of the largest gold mining companies in the world. Even

though the organisation has succeeded in achieving its set financial targets in 2015 according

to chairman’s message, the financial analysis conducted states that it is struggling to maintain

its competitive position in the global marketplace. Hence, it is recommended to minimise

inventory, operating costs along with raising funds through issuance of additional equity

shares for minimising the overall debt burden.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FINANCIAL ANALYSIS

Introduction:

With the rising competition in the global marketplace, it has become difficult for the

business organisations to sustain their operations and other business activities (Epstein,

Buhovac and Yuthas 2015). The current report intends to provide a detailed overview of one

of the leading global gold mining companies, which is Barrick Gold Corporation. A key

overview of the organisation would be provided including its significant business activities

and any changes in financial performance based on the message of the chairperson or the

managing director. In addition, the paper would evaluate the financial performance of the

organisation by computing key financial ratios based on its consolidated financial statements

of the years 2014 and 2015. Finally, the report would shed light on providing valuable

suggestions to the organisation so that its financial performance could be improved in future.

Introduction:

With the rising competition in the global marketplace, it has become difficult for the

business organisations to sustain their operations and other business activities (Epstein,

Buhovac and Yuthas 2015). The current report intends to provide a detailed overview of one

of the leading global gold mining companies, which is Barrick Gold Corporation. A key

overview of the organisation would be provided including its significant business activities

and any changes in financial performance based on the message of the chairperson or the

managing director. In addition, the paper would evaluate the financial performance of the

organisation by computing key financial ratios based on its consolidated financial statements

of the years 2014 and 2015. Finally, the report would shed light on providing valuable

suggestions to the organisation so that its financial performance could be improved in future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FINANCIAL ANALYSIS

Discussion/ Findings:

1. Core business activity and/ or operating segments of Barrick Gold Corporation:

Barrick Gold Corporation is the leading gold mining firm in the world and the

headquarter of the firm is situated in Toronto, Ontario, Canada. The main business activity of

the organisation is its mining operations in Canada, Australia, Argentina, USA, Chile, Papua

New Guinea, Saudi Arabia, Zambia, the Dominican Republic and Peru (Barrick.com 2018).

Above 75% of gold production of the organisation is generated from US. In 2016, the

organisation produced 5.52 million ounces of gold at $798 per ounce and 415 million pounds

of copper at $2.05 per pound. On 31st December 2016, Barrick had 85.9 million ounces of

probable and proven gold reserves (Barrick.com 2018). The other major operating segments

of Barrick comprise of Goldstrike, Cortez, Nevada, Lagunas Norte, Turquoise Ridge, Acacia

Mining Plc, Pueblo Viejo and Pascua-Lama. With the help of its subsidiary, Acacia, the

organisation owns gold mines as well as exploration properties in Africa.

2. Significant changes in financial performance of the organisation from the chairman’s

message or managing director’s review:

According to the annual report of Barrick Gold Corporation in 2015, the following are

the significant changes in financial performance based on the message of the Executive

Chairman, John L. Thornton:

Strengthening balance sheet:

At the beginning of the year 2015, the organisation planned to minimise its total debt

by $3 billion. It has been found at the end of the year that the organisation managed to reduce

the same by $3.1 billion, which denotes its efficiency in minimising the overall debt burden

(Barrick.q4cdn.com 2018).

Discussion/ Findings:

1. Core business activity and/ or operating segments of Barrick Gold Corporation:

Barrick Gold Corporation is the leading gold mining firm in the world and the

headquarter of the firm is situated in Toronto, Ontario, Canada. The main business activity of

the organisation is its mining operations in Canada, Australia, Argentina, USA, Chile, Papua

New Guinea, Saudi Arabia, Zambia, the Dominican Republic and Peru (Barrick.com 2018).

Above 75% of gold production of the organisation is generated from US. In 2016, the

organisation produced 5.52 million ounces of gold at $798 per ounce and 415 million pounds

of copper at $2.05 per pound. On 31st December 2016, Barrick had 85.9 million ounces of

probable and proven gold reserves (Barrick.com 2018). The other major operating segments

of Barrick comprise of Goldstrike, Cortez, Nevada, Lagunas Norte, Turquoise Ridge, Acacia

Mining Plc, Pueblo Viejo and Pascua-Lama. With the help of its subsidiary, Acacia, the

organisation owns gold mines as well as exploration properties in Africa.

2. Significant changes in financial performance of the organisation from the chairman’s

message or managing director’s review:

According to the annual report of Barrick Gold Corporation in 2015, the following are

the significant changes in financial performance based on the message of the Executive

Chairman, John L. Thornton:

Strengthening balance sheet:

At the beginning of the year 2015, the organisation planned to minimise its total debt

by $3 billion. It has been found at the end of the year that the organisation managed to reduce

the same by $3.1 billion, which denotes its efficiency in minimising the overall debt burden

(Barrick.q4cdn.com 2018).

5ACCOUNTING FINANCIAL ANALYSIS

Maximisation of free cash flow:

Barrick intended to generate free cash flow amounting to $1,100 gold at the start of

the year. In fact, it managed to over achieve the set target by generating $0.5 billion free cash

flow at a recognised price of $1,157 gold. This is mainly achieved by conducting credit

checks on the customers (Amit and Villalonga 2014).

Cash costs:

Barrick intended to retain its cash costs between $600 and $640 per ounce. It

succeeded in achieving the same, as the actual cash cost incurred was $596 per ounce. This

signifies the ability of the organisation in minimising its cost of production by using latest

machinery and equipment (Friede, Busch and Bassen 2015).

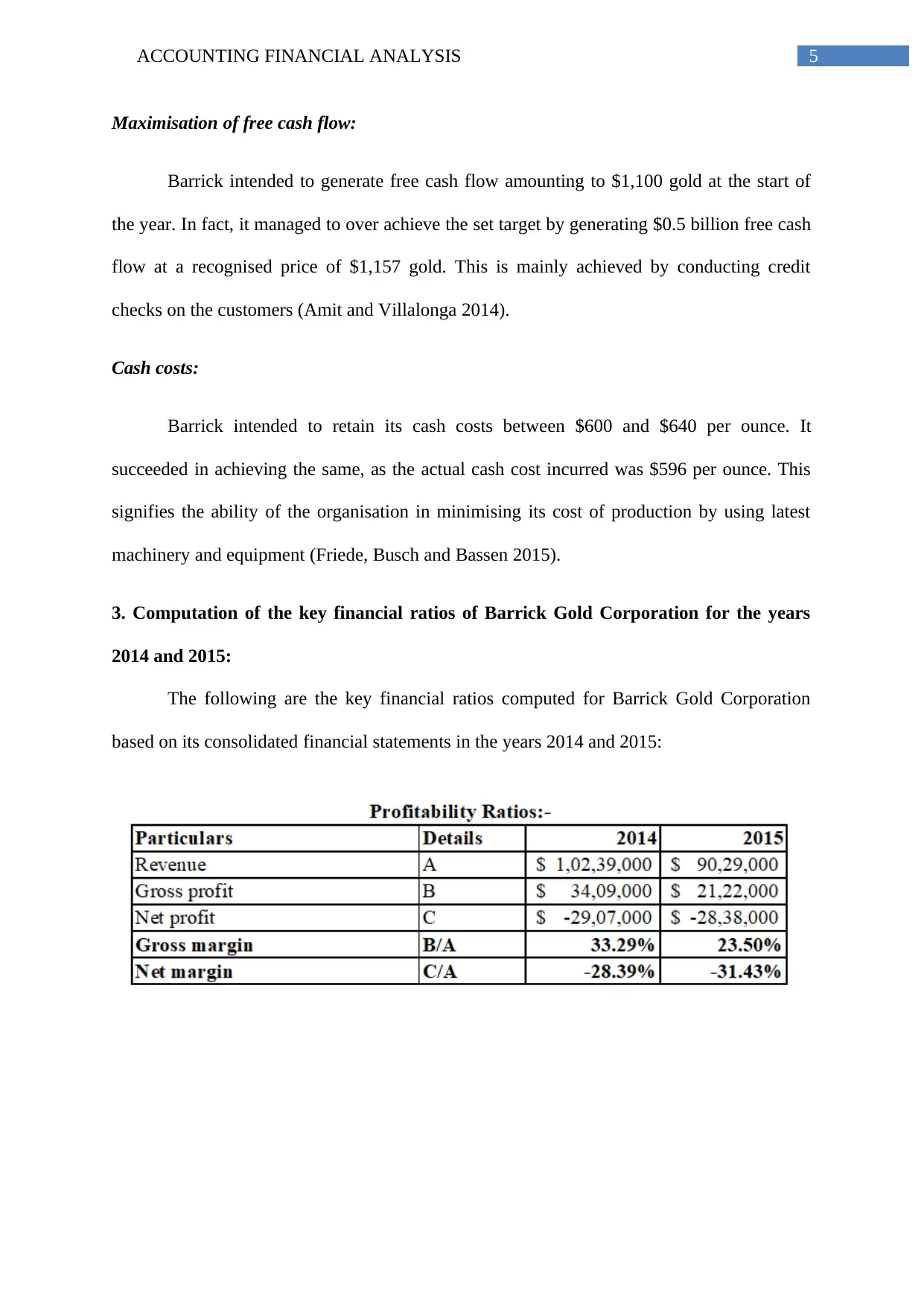

3. Computation of the key financial ratios of Barrick Gold Corporation for the years

2014 and 2015:

The following are the key financial ratios computed for Barrick Gold Corporation

based on its consolidated financial statements in the years 2014 and 2015:

Maximisation of free cash flow:

Barrick intended to generate free cash flow amounting to $1,100 gold at the start of

the year. In fact, it managed to over achieve the set target by generating $0.5 billion free cash

flow at a recognised price of $1,157 gold. This is mainly achieved by conducting credit

checks on the customers (Amit and Villalonga 2014).

Cash costs:

Barrick intended to retain its cash costs between $600 and $640 per ounce. It

succeeded in achieving the same, as the actual cash cost incurred was $596 per ounce. This

signifies the ability of the organisation in minimising its cost of production by using latest

machinery and equipment (Friede, Busch and Bassen 2015).

3. Computation of the key financial ratios of Barrick Gold Corporation for the years

2014 and 2015:

The following are the key financial ratios computed for Barrick Gold Corporation

based on its consolidated financial statements in the years 2014 and 2015:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FINANCIAL ANALYSIS

4. Overall assessment of Barrick Gold Corporation and its future prospects:

Based on the above-calculated ratios, the financial condition of Barrick Gold

Corporation could be analysed as follows:

4. Overall assessment of Barrick Gold Corporation and its future prospects:

Based on the above-calculated ratios, the financial condition of Barrick Gold

Corporation could be analysed as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FINANCIAL ANALYSIS

Profitability analysis:

In order to conduct the profitability analysis of Barrick, the two ratios that have been

taken into consideration include gross margin and net margin. In the words of Grant (2016),

gross margin is a financial ratio, which gauges the ability of an organisation in controlling its

costs. In case of Barrick Gold Corporation, gross margin has fallen from 33.29% in 2014 to

23.50% in 2015. The reason identified behind such decline in gross margin is the significant

fall in revenue base in 2015, while the cost of revenue for the organisation has increased in

the same year. This denotes that the organisation is struggling to generate adequate profit

from revenue after deducting its cost of goods sold.

Net margin gauges the overall profitability of an organisation by taking into

consideration all financing and operating expenses (Islam 2014). Thus, it denotes the amount

of revenue generated by an organisation for different corporate activities. For Barrick, the

ratio has been negative in both the years, as other operating expenses have been higher in

contrast to gross income. Thus, in terms of profitability, the organisation had been struggling

to maintain its position in the global marketplace.

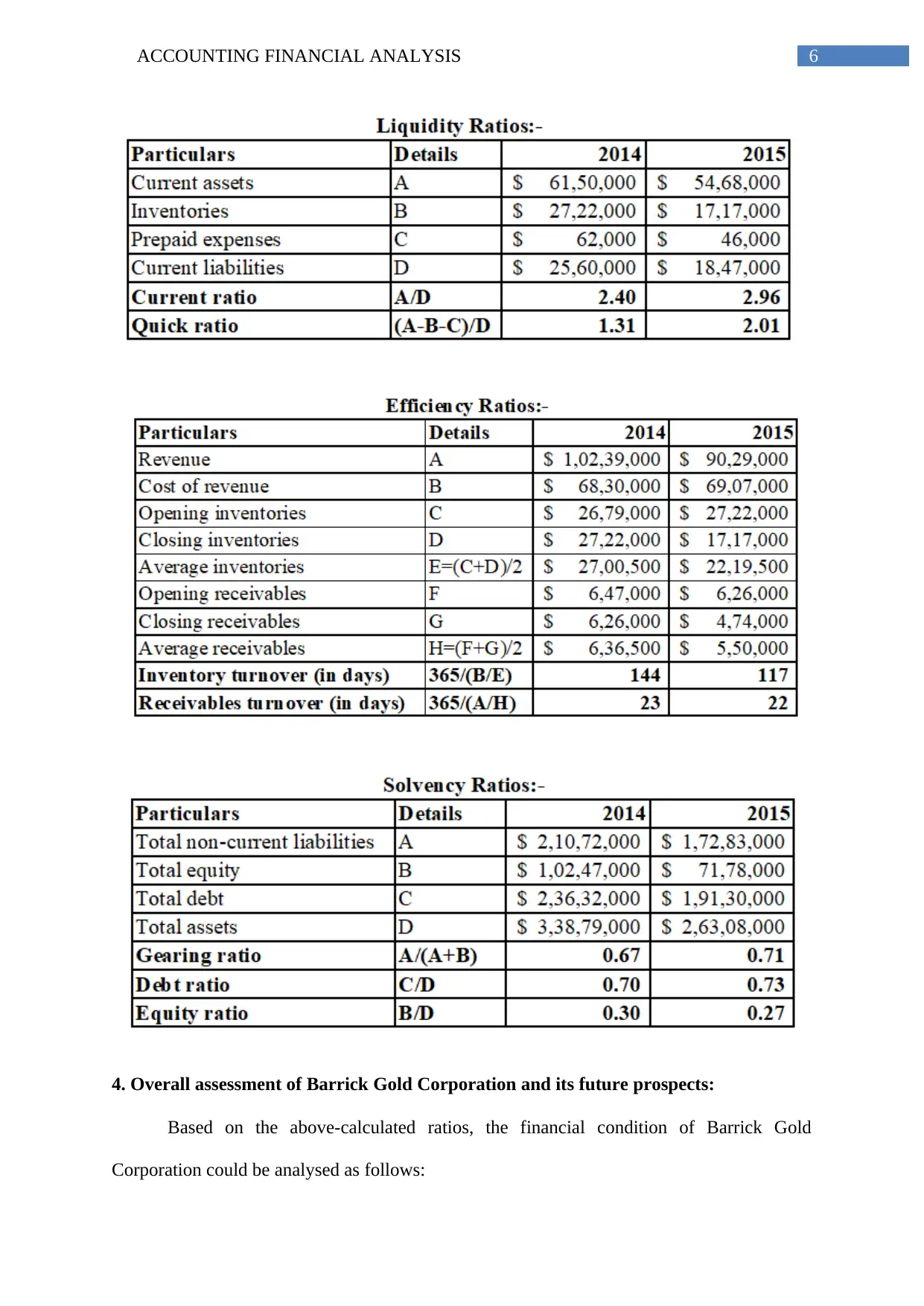

Liquidity analysis:

In order to conduct the liquidity analysis of Barrick, the two ratios that have been

taken into consideration include current ratio and quick ratio. Current ratio assists the

investors and creditors in gaining an overview of the liquidity of an organisation and its

ability to settle its current obligations (Miller-Nobles, TMattison and Matsumura 2016). An

ideal current ratio is considered as 2. In this case, the current ratio has increased from 2.40 in

2014 to 2.96 in 2015, which is much higher than the ideal standard. This is because of the

significant amount of inventory on hand and it denotes that Barrick is not utilising its assets

base properly for converting inventory into working capital. Therefore, a huge amount of

Profitability analysis:

In order to conduct the profitability analysis of Barrick, the two ratios that have been

taken into consideration include gross margin and net margin. In the words of Grant (2016),

gross margin is a financial ratio, which gauges the ability of an organisation in controlling its

costs. In case of Barrick Gold Corporation, gross margin has fallen from 33.29% in 2014 to

23.50% in 2015. The reason identified behind such decline in gross margin is the significant

fall in revenue base in 2015, while the cost of revenue for the organisation has increased in

the same year. This denotes that the organisation is struggling to generate adequate profit

from revenue after deducting its cost of goods sold.

Net margin gauges the overall profitability of an organisation by taking into

consideration all financing and operating expenses (Islam 2014). Thus, it denotes the amount

of revenue generated by an organisation for different corporate activities. For Barrick, the

ratio has been negative in both the years, as other operating expenses have been higher in

contrast to gross income. Thus, in terms of profitability, the organisation had been struggling

to maintain its position in the global marketplace.

Liquidity analysis:

In order to conduct the liquidity analysis of Barrick, the two ratios that have been

taken into consideration include current ratio and quick ratio. Current ratio assists the

investors and creditors in gaining an overview of the liquidity of an organisation and its

ability to settle its current obligations (Miller-Nobles, TMattison and Matsumura 2016). An

ideal current ratio is considered as 2. In this case, the current ratio has increased from 2.40 in

2014 to 2.96 in 2015, which is much higher than the ideal standard. This is because of the

significant amount of inventory on hand and it denotes that Barrick is not utilising its assets

base properly for converting inventory into working capital. Therefore, a huge amount of

8ACCOUNTING FINANCIAL ANALYSIS

cash is stuck in inventory base for the organisation, which could otherwise be used for

running its daily business operations.

Quick ratio gauges the capability of an organisation to settle its existing obligations

when they become due with quick assets only like cash, accounts receivable, marketable

securities and short-term investments (Liu 2018). For Barrick, the ratio has increased

significantly from 1.31 in 2014 to 2.01 in 2015, which again denotes improper utilisation of

short-term assets, as they could be used for future expansion projects.

Efficiency analysis:

In order to conduct the efficiency analysis of Barrick, the two ratios that have been

taken into consideration include receivables turnover and inventory turnover. Inventory

turnover ratio helps in depicting the efficiency of an organisation in managing its inventory

by comparing cost of revenue with average inventory for a year. A lower ratio in terms of

days is always favourable for an organisation (Wahlen, Baginski and Bradshaw 2014). In

case of Barrick, the ratio has fallen from 144 days in 2014 to 117 days in 2013, as it has

focused on minimising its inventory base greatly. Receivables turnover gauges the number of

times an organisation could convert its accounts receivable into cash in a year. For Barrick,

the ratio has fallen from 23 days in 2014 to 22 days in 2015 and thus, a slight improvement

could be seen in its efficiency position due to stringent credit policy for the customers (Vogel

2014).

Solvency analysis:

In order to conduct the solvency analysis of Barrick, the two ratios that have been

taken into consideration include gearing ratio, debt ratio and equity ratio. Gearing ratio

indicates the financial risk of a business organisation to which it is subjected, as additional

cash is stuck in inventory base for the organisation, which could otherwise be used for

running its daily business operations.

Quick ratio gauges the capability of an organisation to settle its existing obligations

when they become due with quick assets only like cash, accounts receivable, marketable

securities and short-term investments (Liu 2018). For Barrick, the ratio has increased

significantly from 1.31 in 2014 to 2.01 in 2015, which again denotes improper utilisation of

short-term assets, as they could be used for future expansion projects.

Efficiency analysis:

In order to conduct the efficiency analysis of Barrick, the two ratios that have been

taken into consideration include receivables turnover and inventory turnover. Inventory

turnover ratio helps in depicting the efficiency of an organisation in managing its inventory

by comparing cost of revenue with average inventory for a year. A lower ratio in terms of

days is always favourable for an organisation (Wahlen, Baginski and Bradshaw 2014). In

case of Barrick, the ratio has fallen from 144 days in 2014 to 117 days in 2013, as it has

focused on minimising its inventory base greatly. Receivables turnover gauges the number of

times an organisation could convert its accounts receivable into cash in a year. For Barrick,

the ratio has fallen from 23 days in 2014 to 22 days in 2015 and thus, a slight improvement

could be seen in its efficiency position due to stringent credit policy for the customers (Vogel

2014).

Solvency analysis:

In order to conduct the solvency analysis of Barrick, the two ratios that have been

taken into consideration include gearing ratio, debt ratio and equity ratio. Gearing ratio

indicates the financial risk of a business organisation to which it is subjected, as additional

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FINANCIAL ANALYSIS

debt could result in financial troubles (Wagner et al. 2015). In case of Barrick, the ratio has

increased from 0.67 in 2014 to 0.71 in 2015, which is much higher than the ideal standard of

0.5. This is because of the significant rise in deferred revenues in 2015 and repayment of

long-term loans by disposing a portion of its assets. Hence, it is placed in a risky position.

This is supported further by debt ratio and equity ratio, which have increased and declined

respectively over the years. Thus, in terms of solvency position, Barrick might experience

financial difficulties in future.

Hence, based on the above evaluation, it could be cited that Barrick has been

struggling to maintain its financial condition in the marketplace and thus, it needs to

undertake remedial measures for improving the same.

debt could result in financial troubles (Wagner et al. 2015). In case of Barrick, the ratio has

increased from 0.67 in 2014 to 0.71 in 2015, which is much higher than the ideal standard of

0.5. This is because of the significant rise in deferred revenues in 2015 and repayment of

long-term loans by disposing a portion of its assets. Hence, it is placed in a risky position.

This is supported further by debt ratio and equity ratio, which have increased and declined

respectively over the years. Thus, in terms of solvency position, Barrick might experience

financial difficulties in future.

Hence, based on the above evaluation, it could be cited that Barrick has been

struggling to maintain its financial condition in the marketplace and thus, it needs to

undertake remedial measures for improving the same.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FINANCIAL ANALYSIS

Conclusion and recommendations:

From the above discussion, it is evident that Barrick Gold Corporation is suffering

from financial troubles, as it incurred net losses in both the years due to significant decline in

revenue base and rise in operating expenses. In addition, it has focused on maintaining too

much inventory on hand and raising funds through debt, due to which it might lose its

competitive position in the marketplace. Therefore, it needs to minimise its inventory base so

that better liquidity position could be ensured. Moreover, it needs to reduce other operating

expenses in order to avoid further net losses. Finally, it is advised to raise some additional

equity shares in the market for avoiding the risky financial position of the business.

Conclusion and recommendations:

From the above discussion, it is evident that Barrick Gold Corporation is suffering

from financial troubles, as it incurred net losses in both the years due to significant decline in

revenue base and rise in operating expenses. In addition, it has focused on maintaining too

much inventory on hand and raising funds through debt, due to which it might lose its

competitive position in the marketplace. Therefore, it needs to minimise its inventory base so

that better liquidity position could be ensured. Moreover, it needs to reduce other operating

expenses in order to avoid further net losses. Finally, it is advised to raise some additional

equity shares in the market for avoiding the risky financial position of the business.

11ACCOUNTING FINANCIAL ANALYSIS

List of references:

Amit, R. and Villalonga, B., 2014. Financial performance of family firms. The Sage

handbook of family business, pp.157-178.

Barrick.com., 2018. Barrick Gold Corporation - Home . [online] Available at:

https://barrick.com/ [Accessed 21 Jul. 2018].

Barrick.q4cdn.com., 2018. [online] Available at:

https://barrick.q4cdn.com/788666289/files/doc_financials/annual/2015/Barrick-Annual-

Report-2015.pdf [Accessed 21 Jul. 2018].

Epstein, M.J., Buhovac, A.R. and Yuthas, K., 2015. Managing social, environmental and

financial performance simultaneously. Long range planning, 48(1), pp.35-45.

Friede, G., Busch, T. and Bassen, A., 2015. ESG and financial performance: aggregated

evidence from more than 2000 empirical studies. Journal of Sustainable Finance &

Investment, 5(4), pp.210-233.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. John Wiley &

Sons.

Islam, M.A., 2014. An analysis of the financial performance of national bank limited using

financial ratio. Journal of Behavioural Economics, Finance, Entrepreneurship, Accounting

and Transport, 2(5), pp.121-129.

Liu, Z., 2018. Financial Situation Assessment of a Selected Company.

Miller-Nobles, T.L., Mattison, B. and Matsumura, E.M., 2016. Horngren's Financial &

Managerial Accounting: The Managerial Chapters. Pearson.

List of references:

Amit, R. and Villalonga, B., 2014. Financial performance of family firms. The Sage

handbook of family business, pp.157-178.

Barrick.com., 2018. Barrick Gold Corporation - Home . [online] Available at:

https://barrick.com/ [Accessed 21 Jul. 2018].

Barrick.q4cdn.com., 2018. [online] Available at:

https://barrick.q4cdn.com/788666289/files/doc_financials/annual/2015/Barrick-Annual-

Report-2015.pdf [Accessed 21 Jul. 2018].

Epstein, M.J., Buhovac, A.R. and Yuthas, K., 2015. Managing social, environmental and

financial performance simultaneously. Long range planning, 48(1), pp.35-45.

Friede, G., Busch, T. and Bassen, A., 2015. ESG and financial performance: aggregated

evidence from more than 2000 empirical studies. Journal of Sustainable Finance &

Investment, 5(4), pp.210-233.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. John Wiley &

Sons.

Islam, M.A., 2014. An analysis of the financial performance of national bank limited using

financial ratio. Journal of Behavioural Economics, Finance, Entrepreneurship, Accounting

and Transport, 2(5), pp.121-129.

Liu, Z., 2018. Financial Situation Assessment of a Selected Company.

Miller-Nobles, T.L., Mattison, B. and Matsumura, E.M., 2016. Horngren's Financial &

Managerial Accounting: The Managerial Chapters. Pearson.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.