Finance Report: Analysis of Basel III Reforms and Operational Risks

VerifiedAdded on 2022/08/24

|21

|4603

|29

Report

AI Summary

This finance report provides a comprehensive analysis of the Basel III reforms, focusing on their impact on the banking industry and the management of operational risks. The report begins by outlining the primary motivations behind the implementation of Basel III, including the need to strengthen financial regulations, improve risk management, and promote economic stability in the wake of the 2008 financial crisis. It then delves into the key changes introduced by the reforms, such as the new definition of capital, the increased emphasis on common equity, and the three lines of defense approach to managing operational risks. The report also examines the specific challenges faced by banks in implementing Basel III, including balancing their interests with regulatory requirements, managing data, and adapting to national regulations. Furthermore, the report investigates the operational risks associated with technological advancements in banking, such as data breaches, IT disruptions, cyber fraud, and outsourcing. The report also discusses the role of the Australian Prudential Regulation Authority (APRA) in adopting and implementing the Basel III requirements, highlighting areas of divergence and the more conservative approach taken by APRA. The report concludes by comparing the Basel III guidelines with the previous Basel II guidelines, focusing on the methods for calculating minimum capital requirements for operational risk and emphasizing the challenges and complexities involved in effectively implementing the reforms. The report is a valuable resource for understanding the evolving landscape of financial regulation and the importance of risk management in the banking sector.

Running head: FINANCE

Finance

Name of the Student

Name of the University

Author Note

Finance

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCE

Table of Contents

Answer to Question 1...................................................................................................................2

Answer to Question 2...................................................................................................................6

Answer to Question 3...................................................................................................................7

Answer to Question 4...................................................................................................................9

Answer to Question 5.................................................................................................................12

References..................................................................................................................................18

FINANCE

Table of Contents

Answer to Question 1...................................................................................................................2

Answer to Question 2...................................................................................................................6

Answer to Question 3...................................................................................................................7

Answer to Question 4...................................................................................................................9

Answer to Question 5.................................................................................................................12

References..................................................................................................................................18

2

FINANCE

Answer to Question 1

a) The main reason behind the implementation of the Basel III reforms was to develop a set

of financial regulations which strengthened the aspects of regulation, supervision and risk

management within the banking industry. The impact of the 2008 Global Financial Crisis

had severely weakened the bank’s ability to handle the shocks occurring from the

financial stresses. Another lesson learned from these reforms was that for growth to

continue along with the technological advances and innovation, a stable economic and

fiscal sector was also extremely necessary. The transparency and disclosure policies of

the banks had also become severely weakened prior to the introduction of these reforms

(Fratianni and Pattison 2015). Hence, the primary aim was to continue the steps

undertaken by the previous accords of Basel I and Basel II and strengthen the regulations

prevalent in the banking industry across the world. The purpose of strengthening the

regulations was to prevent banks from taking more risks than they can afford to and stop

them from hurting the economy of the country they are operating in. It also promoted

economic recovery and stability in the financial sector of different countries on which

these systems became applicable (Dermine 2015).

b) Operational risk is one of the most inherent risks faced by banks as a part of the business.

The new framework ensures that banks adopt the three line of defence as a part of

managing the operational risks faced by them. These include the business line

management, an independent corporate operational risk management function and an

independent review of the operations of the entity. One of the major changes to the

framework was the new definition of the term capital agreed in July 2010. It was agreed

that higher quality capital was one which had an increased loss-absorbing capacity and

FINANCE

Answer to Question 1

a) The main reason behind the implementation of the Basel III reforms was to develop a set

of financial regulations which strengthened the aspects of regulation, supervision and risk

management within the banking industry. The impact of the 2008 Global Financial Crisis

had severely weakened the bank’s ability to handle the shocks occurring from the

financial stresses. Another lesson learned from these reforms was that for growth to

continue along with the technological advances and innovation, a stable economic and

fiscal sector was also extremely necessary. The transparency and disclosure policies of

the banks had also become severely weakened prior to the introduction of these reforms

(Fratianni and Pattison 2015). Hence, the primary aim was to continue the steps

undertaken by the previous accords of Basel I and Basel II and strengthen the regulations

prevalent in the banking industry across the world. The purpose of strengthening the

regulations was to prevent banks from taking more risks than they can afford to and stop

them from hurting the economy of the country they are operating in. It also promoted

economic recovery and stability in the financial sector of different countries on which

these systems became applicable (Dermine 2015).

b) Operational risk is one of the most inherent risks faced by banks as a part of the business.

The new framework ensures that banks adopt the three line of defence as a part of

managing the operational risks faced by them. These include the business line

management, an independent corporate operational risk management function and an

independent review of the operations of the entity. One of the major changes to the

framework was the new definition of the term capital agreed in July 2010. It was agreed

that higher quality capital was one which had an increased loss-absorbing capacity and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCE

allowed the banks to withstand longer periods of stress. One of the key changes is the

increased emphasis on common equity as the highest quality component of the bank’s

common capital. Any regulatory capital deductions are to be taken from the common

equity of the entity rather than the Tier 1 or Tier 2 capital owned by the bank. Hence,

banks can no longer display strong Tier 1 capital ratios with limited equity levels net of

the deductions. Apart from this, the senior management of the entity is charged with the

responsibility of identifying and assessing the operational risk inherent in all products,

materials and services provided by a business. All new products, processes and activities

of the bank should go through the approval process which fully assesses the operational

risk faced by the business (Cummings and Durrani 2016). A process should be

implemented by the management to regularly monitor the operational risk profiles of the

bank and the material exposure to losses. Reporting mechanisms should support the

proactive management of the operational risks thus identified. The public disclosures of a

bank should allow the stakeholders to assess the approach of a bank to the operational

risk management. A sufficient level of operational risk training should be provided to

employees at all levels in the organisation. The framework which is selected by a bank

for its operational risk management procedures should be a reflection of the nature, size,

complexity and risk profile of the bank. Another method of fully understanding the nature

and complexity of operational risk is to have all the components of the Basel III

Framework fully integrated into the risk management process of the organisation. The

results of the operational risk assessment of the bank’s performance should also be

incorporated into the overall bank business strategy development process. Every bank

should document the Basel III framework in the policies approved by the Board of

FINANCE

allowed the banks to withstand longer periods of stress. One of the key changes is the

increased emphasis on common equity as the highest quality component of the bank’s

common capital. Any regulatory capital deductions are to be taken from the common

equity of the entity rather than the Tier 1 or Tier 2 capital owned by the bank. Hence,

banks can no longer display strong Tier 1 capital ratios with limited equity levels net of

the deductions. Apart from this, the senior management of the entity is charged with the

responsibility of identifying and assessing the operational risk inherent in all products,

materials and services provided by a business. All new products, processes and activities

of the bank should go through the approval process which fully assesses the operational

risk faced by the business (Cummings and Durrani 2016). A process should be

implemented by the management to regularly monitor the operational risk profiles of the

bank and the material exposure to losses. Reporting mechanisms should support the

proactive management of the operational risks thus identified. The public disclosures of a

bank should allow the stakeholders to assess the approach of a bank to the operational

risk management. A sufficient level of operational risk training should be provided to

employees at all levels in the organisation. The framework which is selected by a bank

for its operational risk management procedures should be a reflection of the nature, size,

complexity and risk profile of the bank. Another method of fully understanding the nature

and complexity of operational risk is to have all the components of the Basel III

Framework fully integrated into the risk management process of the organisation. The

results of the operational risk assessment of the bank’s performance should also be

incorporated into the overall bank business strategy development process. Every bank

should document the Basel III framework in the policies approved by the Board of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCE

Directors and the definitions of operational risk and operational loss should be included

in the policies. The effectiveness of the framework would significantly decline without

appropriate measures taken by the banks to define both operational risk and operational

loss. The bank’s accepted risk appetite and tolerance and the threshold limits for the

inherent and residual risks should be clearly documented in the framework

documentation. The framework implemented as a part of the business should be regularly

reviewed and the operational risks associated with the changes in the operational policies

should be included in the framework (Cummings and Durrani 2018).

c) The Australian Prudential Regulation Authority (APRA) completed the adoption of the

Basel III requirements in November 2012 and brought them into action from 1 January

2013. After the adoption, the process adopted by the APRA was known as the assessment

work. This assessment work of APRA mainly consisted of three parts. The first phase is

known as the self-assessment by APRA. The second phase is called the off-and on-site

assessment phase and the third phase is known as the post-assessment review phase. The

off-and-on-site assessment phase is one of the most important phases of the procedures

undertaken by the APRA. It involved a travel to Sydney where the Assessment Team

held discussions with APRA, five internationally authorised deposit-taking institutions

(ADIs), two audit firms and a one credit rating agency of the business. The discussions

which took place gave an important overview and a better understanding about the

implementation of the Basel-based risk standards and their implementation in Australia.

The post-assessment review phase contained a thorough discussion on the review of the

findings of the review team and a technical review of the findings between various

boards. The Assessment team’s work and its interactions with APRA were controlled by

FINANCE

Directors and the definitions of operational risk and operational loss should be included

in the policies. The effectiveness of the framework would significantly decline without

appropriate measures taken by the banks to define both operational risk and operational

loss. The bank’s accepted risk appetite and tolerance and the threshold limits for the

inherent and residual risks should be clearly documented in the framework

documentation. The framework implemented as a part of the business should be regularly

reviewed and the operational risks associated with the changes in the operational policies

should be included in the framework (Cummings and Durrani 2018).

c) The Australian Prudential Regulation Authority (APRA) completed the adoption of the

Basel III requirements in November 2012 and brought them into action from 1 January

2013. After the adoption, the process adopted by the APRA was known as the assessment

work. This assessment work of APRA mainly consisted of three parts. The first phase is

known as the self-assessment by APRA. The second phase is called the off-and on-site

assessment phase and the third phase is known as the post-assessment review phase. The

off-and-on-site assessment phase is one of the most important phases of the procedures

undertaken by the APRA. It involved a travel to Sydney where the Assessment Team

held discussions with APRA, five internationally authorised deposit-taking institutions

(ADIs), two audit firms and a one credit rating agency of the business. The discussions

which took place gave an important overview and a better understanding about the

implementation of the Basel-based risk standards and their implementation in Australia.

The post-assessment review phase contained a thorough discussion on the review of the

findings of the review team and a technical review of the findings between various

boards. The Assessment team’s work and its interactions with APRA were controlled by

5

FINANCE

the Basel Committee Secretariat. Some of the aspects which were chosen to be

implemented by APRA include the definition of capital component as suggested by the

Basel Framework. One aspect where APRA chose to skip the recommendations of the

Basel Framework is in the implementation of the threshold deduction treatment, which is

a substantial increase in the conservatism within the rules of Basel III framework. Apart

from this, there are other areas of divergence in the manner of APRA’s approach to the

framework of Basel. The approach of APRA to the Australian Prudential Regime is much

more conservative than that of the Basel Framework. Hence, due to the regulations

implemented by APRA in its framework, any internationally active ADI operating within

Australia tends to face higher capital requirements. The capital requirements are almost

100 basis points higher than that of any other institutional institution subject to the

requirements of the Basel Framework worldwide (Atkin and Cheung 2017). The scope of

the approach consisted of two aspects which were followed in effectively implementing

the guidelines of the Basel Framework. The first aspect was the comparison of the capital

requirements under the Basel framework to ascertain if all the requirements under the

Basel Framework had been adopted. The second included the ascertainment of any

significant differences which existed between the domestic regulations and the Basel

Framework and their significance.

d) The main challenge faced by the banks when implementing the guidelines of Basel III is

to balance their interests with the requirements suggested by the regulator. The Basel III

is different from the previous regimes in the sense that it requires a greater integration

between the finance and risk management functions of a bank. However, in order to the

same, the main challenge is the differences in the people who are responsible for making

FINANCE

the Basel Committee Secretariat. Some of the aspects which were chosen to be

implemented by APRA include the definition of capital component as suggested by the

Basel Framework. One aspect where APRA chose to skip the recommendations of the

Basel Framework is in the implementation of the threshold deduction treatment, which is

a substantial increase in the conservatism within the rules of Basel III framework. Apart

from this, there are other areas of divergence in the manner of APRA’s approach to the

framework of Basel. The approach of APRA to the Australian Prudential Regime is much

more conservative than that of the Basel Framework. Hence, due to the regulations

implemented by APRA in its framework, any internationally active ADI operating within

Australia tends to face higher capital requirements. The capital requirements are almost

100 basis points higher than that of any other institutional institution subject to the

requirements of the Basel Framework worldwide (Atkin and Cheung 2017). The scope of

the approach consisted of two aspects which were followed in effectively implementing

the guidelines of the Basel Framework. The first aspect was the comparison of the capital

requirements under the Basel framework to ascertain if all the requirements under the

Basel Framework had been adopted. The second included the ascertainment of any

significant differences which existed between the domestic regulations and the Basel

Framework and their significance.

d) The main challenge faced by the banks when implementing the guidelines of Basel III is

to balance their interests with the requirements suggested by the regulator. The Basel III

is different from the previous regimes in the sense that it requires a greater integration

between the finance and risk management functions of a bank. However, in order to the

same, the main challenge is the differences in the people who are responsible for making

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCE

the decisions and those charged with management of risk. While Basel III is consistent in

the guidelines, the main challenge lies in the manner in which it is interpreted by the

banks belonging to different countries. The Basel II regulations were completely adopted

by some of the European banks while it was not adopted by the US banks. Hence,

completely adopting a new framework would be a significant challenge for the US banks

(Jones and Zeitz 2017). The national regulations prevailing in some of the countries may

make it difficult for a bank to adopt the Basel III regulations in the manner in which they

exist. Managing the data which reflects the bank’s credit, concentration and risk

management profiles all at the same time is another significant challenge. Stress testing

or understanding the impact of important market events on the key ratios of business also

takes a significant time from when they are initially implemented (Ahmed et al. 2015).

Answer to Question 2

One of the main operational risks which is faced by every bank due to the

implementation of technological advancements as a part of its business is the breach of the data

belonging to the customers and the employees. Cybersecurity is an increasingly worrying area in

banking and accounts for a significant amount of money spent by the banks in implementing the

information-technology based services. Data Theft, unauthorised access and employee

negligence all play a part in compromising the data of the consumers. Some of the examples of

recent times included the cyber-attack on the credit reporting agency Equifax. IT disruption is

the second operational risk faced by the banks implementing technology as a part of their

processes. A cyber-attack or issues arising from causes like human error or failure caused due to

aging hardware is enough to cause disruptions in the processes implemented by a bank. As it

happened in the WannaCry attack of 2017, the amounts spent on restoring the systems are way

FINANCE

the decisions and those charged with management of risk. While Basel III is consistent in

the guidelines, the main challenge lies in the manner in which it is interpreted by the

banks belonging to different countries. The Basel II regulations were completely adopted

by some of the European banks while it was not adopted by the US banks. Hence,

completely adopting a new framework would be a significant challenge for the US banks

(Jones and Zeitz 2017). The national regulations prevailing in some of the countries may

make it difficult for a bank to adopt the Basel III regulations in the manner in which they

exist. Managing the data which reflects the bank’s credit, concentration and risk

management profiles all at the same time is another significant challenge. Stress testing

or understanding the impact of important market events on the key ratios of business also

takes a significant time from when they are initially implemented (Ahmed et al. 2015).

Answer to Question 2

One of the main operational risks which is faced by every bank due to the

implementation of technological advancements as a part of its business is the breach of the data

belonging to the customers and the employees. Cybersecurity is an increasingly worrying area in

banking and accounts for a significant amount of money spent by the banks in implementing the

information-technology based services. Data Theft, unauthorised access and employee

negligence all play a part in compromising the data of the consumers. Some of the examples of

recent times included the cyber-attack on the credit reporting agency Equifax. IT disruption is

the second operational risk faced by the banks implementing technology as a part of their

processes. A cyber-attack or issues arising from causes like human error or failure caused due to

aging hardware is enough to cause disruptions in the processes implemented by a bank. As it

happened in the WannaCry attack of 2017, the amounts spent on restoring the systems are way

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCE

higher than the payments made to the hackers themselves (Mohurle and Patil 2017). Any

vulnerability in the software of a bank provides an entry point to the users to the outer perimeters

of a bank and is a cause for concern. Cyber fraud undertaken by some of the people in the form

of phishing attacks like those which hit the Switzerland banks in 2017 are an important

operational risk faced by the businesses in the long run. A non-linear relationship between the

normal management of the company and the internal IT controls implemented by it results in the

occurrence of frauds which redirect payments from the banks and steal the funds available with

them. Outsourcing is another common phenomenon which occurs with the use of the

technological advancements of the business. Most of the banks in Australia have continued their

reliance on the vast networks of external vendors to help them increase the capacity of their

online platform management which helps them in grinding extra capacity. This results in

increasing the operational risks of compromising the data of the business and in disrupting the IT

environment of the business. Significant action may also be taken by the regulators to prevent the

use of outsourcing as a part of the business. Mis-Selling of financial products is another

operational risk faced by the businesses. The IT systems run on the basis of algorithmic software

which works on a set of predetermined set of instructions. The Royal Bank of Scotland was sued

by a Federal Housing Finance Agency for selling mortgage-backed securities to it (Zhang, Zhao

and Zhao 2015). The cost of settlement was as high as $5.5 billion. Hence, the technological

advancements may also mislead the business in certain scenarios.

Answer to Question 3

The Basel III guidelines replaces the previously existing Basel II guidelines in calculating

the minimum capital requirements for the operational risk faced by businesses. The Standardised

Approach adopted by the Basel III reforms replaces all the pre-existing methods of calculating

FINANCE

higher than the payments made to the hackers themselves (Mohurle and Patil 2017). Any

vulnerability in the software of a bank provides an entry point to the users to the outer perimeters

of a bank and is a cause for concern. Cyber fraud undertaken by some of the people in the form

of phishing attacks like those which hit the Switzerland banks in 2017 are an important

operational risk faced by the businesses in the long run. A non-linear relationship between the

normal management of the company and the internal IT controls implemented by it results in the

occurrence of frauds which redirect payments from the banks and steal the funds available with

them. Outsourcing is another common phenomenon which occurs with the use of the

technological advancements of the business. Most of the banks in Australia have continued their

reliance on the vast networks of external vendors to help them increase the capacity of their

online platform management which helps them in grinding extra capacity. This results in

increasing the operational risks of compromising the data of the business and in disrupting the IT

environment of the business. Significant action may also be taken by the regulators to prevent the

use of outsourcing as a part of the business. Mis-Selling of financial products is another

operational risk faced by the businesses. The IT systems run on the basis of algorithmic software

which works on a set of predetermined set of instructions. The Royal Bank of Scotland was sued

by a Federal Housing Finance Agency for selling mortgage-backed securities to it (Zhang, Zhao

and Zhao 2015). The cost of settlement was as high as $5.5 billion. Hence, the technological

advancements may also mislead the business in certain scenarios.

Answer to Question 3

The Basel III guidelines replaces the previously existing Basel II guidelines in calculating

the minimum capital requirements for the operational risk faced by businesses. The Standardised

Approach adopted by the Basel III reforms replaces all the pre-existing methods of calculating

8

FINANCE

the minimum capital requirements for operational risk suggested by the guidelines of Basel II. In

the Basel-II guidelines, the approaches which were used in calculating the operational risk

capital included the Standardised Approach, the Basic Indicator Approach and the Advanced

Measurement Approaches. The Basic Indicator Approach suggested that the banks must hold

capital for operational risk which was equal to the average of the three year’s positive gross

income of the bank. Any negative gross income should be excluded from the calculation of the

average gross income for the past three years. In the Standardised Approach, the activities of the

bank are divided into eight business lines. These included corporate finance, trading &sales,

commercial banking, retail banking, agency services, asset management, payment & settlement

and retail brokerage. The minimum capital of the business is calculated on the basis of

multiplying the gross income of a business to a beta factor assigned to a particular business line

(Cecchetti 2016). The gross income, here, was only the total income of the business lines and not

the income of the institution as a whole. Under the Advanced Measurement Approaches, the

regulatory capital requirement will be equal to the risk measure generated by the internal

operational risk measurement system of the business. However, the usage of the Advanced

Measurement Approaches was based on the approval received from the regulatory supervisor

guiding the business. In the Basel III guidelines, the standardised approach is based on three

components. These are the Business Indicator, a financial-statement-based proxy, the Business

indicator component, a set of regulatory determined marginal coefficients and the Internal Loss

multiplier, a scaling factor based on previous losses. In case of the Australian banking

community, the APRA adopted more stringent measures than those suggested by the Basel

guidelines. In case of major banks like ANZ, National Australia Bank and Westpac, the

minimum capital was increased by the bank by an amount of $500 million each. This was done

FINANCE

the minimum capital requirements for operational risk suggested by the guidelines of Basel II. In

the Basel-II guidelines, the approaches which were used in calculating the operational risk

capital included the Standardised Approach, the Basic Indicator Approach and the Advanced

Measurement Approaches. The Basic Indicator Approach suggested that the banks must hold

capital for operational risk which was equal to the average of the three year’s positive gross

income of the bank. Any negative gross income should be excluded from the calculation of the

average gross income for the past three years. In the Standardised Approach, the activities of the

bank are divided into eight business lines. These included corporate finance, trading &sales,

commercial banking, retail banking, agency services, asset management, payment & settlement

and retail brokerage. The minimum capital of the business is calculated on the basis of

multiplying the gross income of a business to a beta factor assigned to a particular business line

(Cecchetti 2016). The gross income, here, was only the total income of the business lines and not

the income of the institution as a whole. Under the Advanced Measurement Approaches, the

regulatory capital requirement will be equal to the risk measure generated by the internal

operational risk measurement system of the business. However, the usage of the Advanced

Measurement Approaches was based on the approval received from the regulatory supervisor

guiding the business. In the Basel III guidelines, the standardised approach is based on three

components. These are the Business Indicator, a financial-statement-based proxy, the Business

indicator component, a set of regulatory determined marginal coefficients and the Internal Loss

multiplier, a scaling factor based on previous losses. In case of the Australian banking

community, the APRA adopted more stringent measures than those suggested by the Basel

guidelines. In case of major banks like ANZ, National Australia Bank and Westpac, the

minimum capital was increased by the bank by an amount of $500 million each. This was done

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCE

to reflect the higher operational risk identified in their risk governance self-assessments. APRA

is also considering the implementation of an additional operating risk capital requirement on the

banks (Li et al. 2016) Due to the latest findings about the risk management procedures in the

various Australian banks and the risks faced by them, The recent measures and observations of

APRA suggests that there is an increasing need to strengthen the non-financial risk management

to ensure that the accountabilities of the business are clearly understood by all the banks.

Answer to Question 4

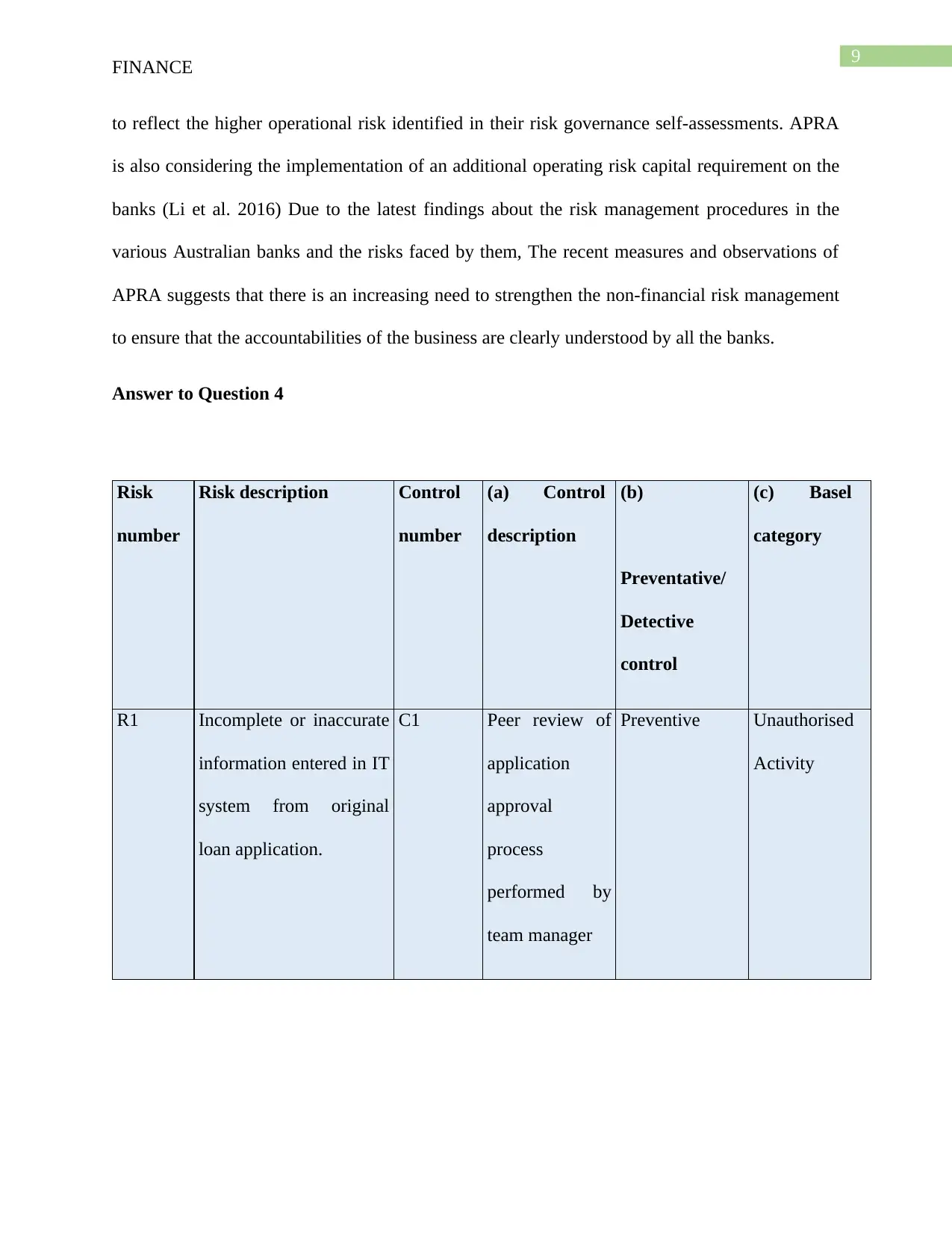

Risk

number

Risk description Control

number

(a) Control

description

(b)

Preventative/

Detective

control

(c) Basel

category

R1 Incomplete or inaccurate

information entered in IT

system from original

loan application.

C1 Peer review of

application

approval

process

performed by

team manager

Preventive Unauthorised

Activity

FINANCE

to reflect the higher operational risk identified in their risk governance self-assessments. APRA

is also considering the implementation of an additional operating risk capital requirement on the

banks (Li et al. 2016) Due to the latest findings about the risk management procedures in the

various Australian banks and the risks faced by them, The recent measures and observations of

APRA suggests that there is an increasing need to strengthen the non-financial risk management

to ensure that the accountabilities of the business are clearly understood by all the banks.

Answer to Question 4

Risk

number

Risk description Control

number

(a) Control

description

(b)

Preventative/

Detective

control

(c) Basel

category

R1 Incomplete or inaccurate

information entered in IT

system from original

loan application.

C1 Peer review of

application

approval

process

performed by

team manager

Preventive Unauthorised

Activity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCE

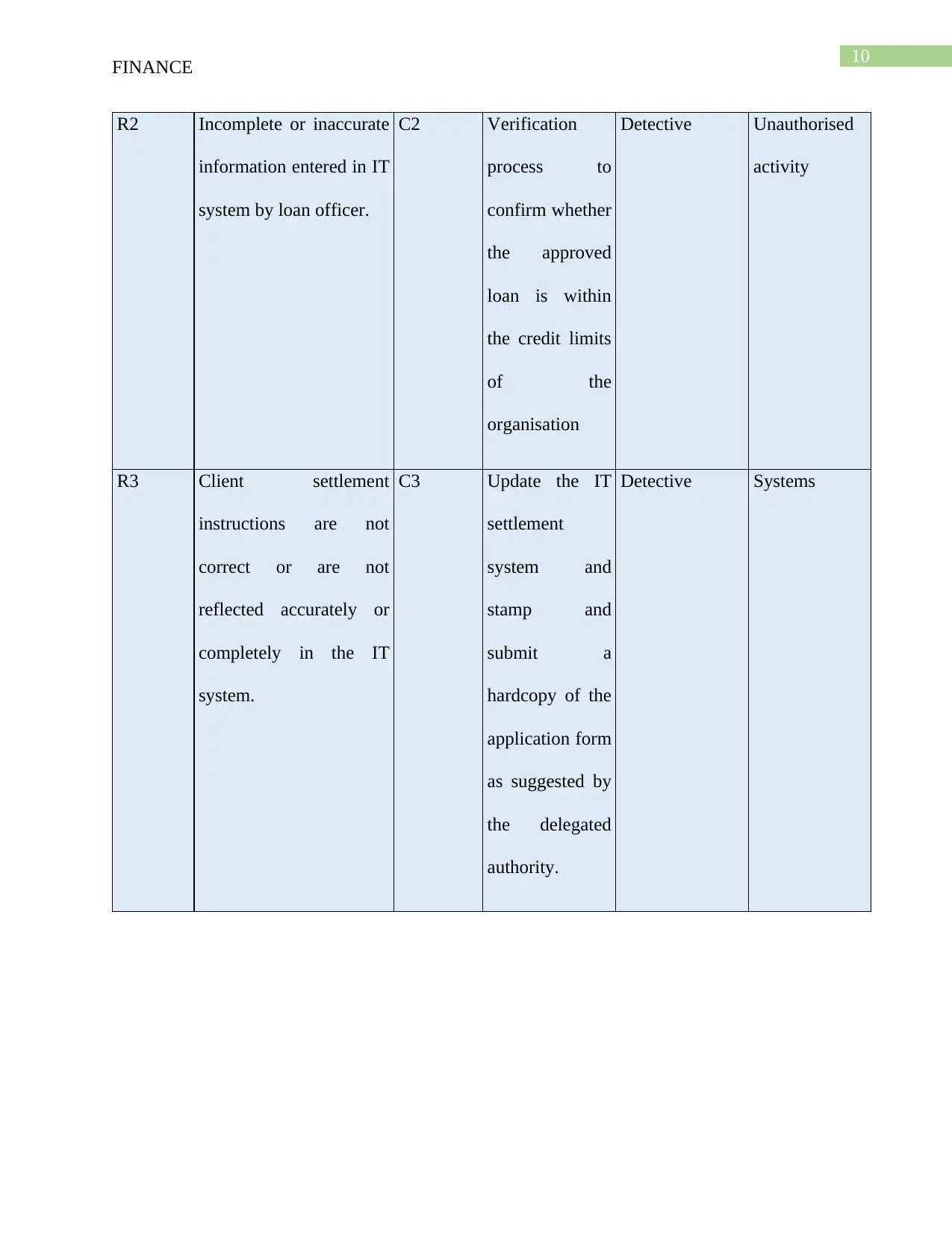

R2 Incomplete or inaccurate

information entered in IT

system by loan officer.

C2 Verification

process to

confirm whether

the approved

loan is within

the credit limits

of the

organisation

Detective Unauthorised

activity

R3 Client settlement

instructions are not

correct or are not

reflected accurately or

completely in the IT

system.

C3 Update the IT

settlement

system and

stamp and

submit a

hardcopy of the

application form

as suggested by

the delegated

authority.

Detective Systems

FINANCE

R2 Incomplete or inaccurate

information entered in IT

system by loan officer.

C2 Verification

process to

confirm whether

the approved

loan is within

the credit limits

of the

organisation

Detective Unauthorised

activity

R3 Client settlement

instructions are not

correct or are not

reflected accurately or

completely in the IT

system.

C3 Update the IT

settlement

system and

stamp and

submit a

hardcopy of the

application form

as suggested by

the delegated

authority.

Detective Systems

11

FINANCE

R4 Client/loan application

documentation is not

retained in accordance

with regulatory

requirements.

C4 Daily

reconciliation of

the records to

ensure that the

business does

not miss out on

any necessary

documents as

suggested by

the required

authorities.

Preventive Transaction

Capture,

Execution and

Maintenance

R5 Settlement amount is

inconsistent with the

loan approved; or

incorrect bank accounts

are affected during the

settlement process.

C5 Upgrade the IT

systems to

automatically

update the client

details and loan

balances as well

as the

drawdown

details

Detective Transaction

Capture,

Execution and

Maintenance

FINANCE

R4 Client/loan application

documentation is not

retained in accordance

with regulatory

requirements.

C4 Daily

reconciliation of

the records to

ensure that the

business does

not miss out on

any necessary

documents as

suggested by

the required

authorities.

Preventive Transaction

Capture,

Execution and

Maintenance

R5 Settlement amount is

inconsistent with the

loan approved; or

incorrect bank accounts

are affected during the

settlement process.

C5 Upgrade the IT

systems to

automatically

update the client

details and loan

balances as well

as the

drawdown

details

Detective Transaction

Capture,

Execution and

Maintenance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.