Enterprise Risk Management: A Case Study of Bauhaus HK Company

VerifiedAdded on 2020/07/23

|13

|2938

|62

Report

AI Summary

This project report focuses on the risk management process applicable to Bauhaus HK Company, covering the identification, evaluation, and impact of internal and external risks. It categorizes risks using a likelihood and impact grid and proposes risk-mitigating strategies to minimize both internal and external risks. The report emphasizes the importance of audit and managing financial, operating, and other risks through effective strategies to ensure smooth business operations. It details the five-step risk management process, including identifying, analyzing, prioritizing, assigning ownership, responding to, and monitoring risks. Furthermore, it distinguishes between preventable, strategy, and unavoidable risks, providing a SHELL model for risk analysis and mitigation. The report also outlines various risk mitigation strategies, emphasizing the need for thorough analysis and evaluation of potential threats and hazards to minimize their impact on operational activities.

ENTERPRISE RISK

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Risk management process applied to Bauhaus HK Company................................................1

2. Identification, evaluation the nature and impact of internal and external risk........................2

3. Categorise the risks using the likelihood and impact grid......................................................4

4. Risk Mitigating Strategies to minimize internal and external risk..........................................5

CONCLUSION................................................................................................................................6

REFERENCES ...............................................................................................................................7

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Risk management process applied to Bauhaus HK Company................................................1

2. Identification, evaluation the nature and impact of internal and external risk........................2

3. Categorise the risks using the likelihood and impact grid......................................................4

4. Risk Mitigating Strategies to minimize internal and external risk..........................................5

CONCLUSION................................................................................................................................6

REFERENCES ...............................................................................................................................7

EXECUTIVE SUMMARY

This project report is intended primarily to focus on risk management process which need

to be applied by an organisation. It also covered internal and external risk which adversely affect

the performance of company. This project report also describes the importance of audit and

managing financial, operating and other risks through implementing effective risk mitigating

strategies which help company to run business operations smoothly.

INTRODUCTION

Enterprise risk management minimizes the effects on business's capital and earning

through planning, organising, leading, and controlling the activities of an organisation. The

manager of an organisation is held responsible to monitors the risk associated with accidental

losses as well as risk related to the operational, financial and others risk in effective and efficient

manner (Lin, Wen and Yu, 2012). Therefore certain steps need to be taken by companies such as

British Airways, Tesco Plcetc.to identify and evaluate risk whether the risk is internal and

external and later on certain strategies to be implemented for mitigating risk.

TASK 1

1. Risk management process applied to Bauhaus HK Company

Risk involve internal and external risk which adversely affect the strategic plan,

operational and financial objective of an organisation. Therefore manager of an organisation is

held responsible to take various steps in order to identify and evaluate these risk and implement

certain actions which helps in minimising these risk in effective and efficient manner. So there

are five risk management process steps which helps in monitoring the several types of risk:

This project report is intended primarily to focus on risk management process which need

to be applied by an organisation. It also covered internal and external risk which adversely affect

the performance of company. This project report also describes the importance of audit and

managing financial, operating and other risks through implementing effective risk mitigating

strategies which help company to run business operations smoothly.

INTRODUCTION

Enterprise risk management minimizes the effects on business's capital and earning

through planning, organising, leading, and controlling the activities of an organisation. The

manager of an organisation is held responsible to monitors the risk associated with accidental

losses as well as risk related to the operational, financial and others risk in effective and efficient

manner (Lin, Wen and Yu, 2012). Therefore certain steps need to be taken by companies such as

British Airways, Tesco Plcetc.to identify and evaluate risk whether the risk is internal and

external and later on certain strategies to be implemented for mitigating risk.

TASK 1

1. Risk management process applied to Bauhaus HK Company

Risk involve internal and external risk which adversely affect the strategic plan,

operational and financial objective of an organisation. Therefore manager of an organisation is

held responsible to take various steps in order to identify and evaluate these risk and implement

certain actions which helps in minimising these risk in effective and efficient manner. So there

are five risk management process steps which helps in monitoring the several types of risk:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Identify the risk: The manager of Bauhaus HK Company should need to recognize and

describe the risks that adversely affect their fashion stores related project and its

outcomes. Through Brainstorming the manager can able to look at a problem and create

ideas in order to minimize that problem. After identifying risk, the manager of Bauhaus

HK company should assure that the risk that may arises during the completion of project,

is noted in their risk register (Aebi, Sabato and Schmid, 2012).The manager should not be

overconfident and need to concentrate on the complex situation that affects needs of

project. Analyse the risk: After listing the different risk that may arises in future in risk register,

the next step is to determine how these risks affects the performance of an organisation.

The nature of risk should also be mentioned in their risk register. The manager should

need to concentrate on avoiding potential litigation, addressing regulatory issues, and

complying with new legislation so that the risk cannot affects their available resources,

schedule and budget. Prioritize the Risk: The manager of Bauhaus HK company should need to be ranked their

risk based on their consequences. Some risk required immediate attentions and some risk

made a little impact in the overall activities of an organisation. Therefore it is must for

the management to devote their time according to the nature of risk and their

consequences. Assign an owner to the risk: To monitoring and handling the risk, certain person is need

to be appointed who is responsible to listing the risk in risk register(Smith and Watkins,

2012). Generally the manager of an organisation is authorised to take certain actions and

strategies in order to reduce the minimize the risk. Respond to the risk: The authorised person should need to develop strategies or some

preventative plan in order to handling the risk according to their consequences. The

employees and manager should need to communicate with each other and decide the

plans to implement to resolve the risk.

Monitor and review the risk: This is the step where the authorised person should need to

monitor, track and review risks. It should be done through different means of

communication such as conducting face-to-face meeting, or through email or text or

describe the risks that adversely affect their fashion stores related project and its

outcomes. Through Brainstorming the manager can able to look at a problem and create

ideas in order to minimize that problem. After identifying risk, the manager of Bauhaus

HK company should assure that the risk that may arises during the completion of project,

is noted in their risk register (Aebi, Sabato and Schmid, 2012).The manager should not be

overconfident and need to concentrate on the complex situation that affects needs of

project. Analyse the risk: After listing the different risk that may arises in future in risk register,

the next step is to determine how these risks affects the performance of an organisation.

The nature of risk should also be mentioned in their risk register. The manager should

need to concentrate on avoiding potential litigation, addressing regulatory issues, and

complying with new legislation so that the risk cannot affects their available resources,

schedule and budget. Prioritize the Risk: The manager of Bauhaus HK company should need to be ranked their

risk based on their consequences. Some risk required immediate attentions and some risk

made a little impact in the overall activities of an organisation. Therefore it is must for

the management to devote their time according to the nature of risk and their

consequences. Assign an owner to the risk: To monitoring and handling the risk, certain person is need

to be appointed who is responsible to listing the risk in risk register(Smith and Watkins,

2012). Generally the manager of an organisation is authorised to take certain actions and

strategies in order to reduce the minimize the risk. Respond to the risk: The authorised person should need to develop strategies or some

preventative plan in order to handling the risk according to their consequences. The

employees and manager should need to communicate with each other and decide the

plans to implement to resolve the risk.

Monitor and review the risk: This is the step where the authorised person should need to

monitor, track and review risks. It should be done through different means of

communication such as conducting face-to-face meeting, or through email or text or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

through management software tool. The transparency is must which allows them to get

specific information about the risks.

2. Identification, evaluation the nature and impact of internal and external risk

A company can reduce negative exposure to business risk by identifying internal and

external risk.

Internal risk: Risk that arises within the organisation in the form of personnel issues or

infrastructure problems etc. is known as Internal Risk.

The three internal risk factors which influences the performance of an organisation are as

follows: Human Factors: Risk that may arise in an organisation from human factors can includes

union strikes, dishonesty by employees, ineffective management or leadership, and

failure on the part of external producers or suppliers. Technological Factors: Risk that arises in an organisation from technological factors

includes unforeseen changes in delivery or distribution of goods and services of company

(Blome and Schoenherr2011). Physical risk: This risk is related to the loss of damage to the assets of a company.

Analysis and impact of one Internal Risk:

Human Factors: Risk related to the Human factors affect the operational activities of an

organisation in the form of union strikes, dishonesty by employees, ineffective management or

leadership, and failure on the part of external producers or suppliers. Therefore it is important to

understand that individuals and groups act differently in different situations. If there is any

misunderstanding or misbehave with their employees may lead to dissatisfaction . Therefore the

incentives must be provide to their employees and stakeholder in order to provide them

maximum level of satisfaction.

External Risk: Risk that arises form outside of a company's organisation are known as

external risk. This type of risk cannot be controlled, or forecasted therefore difficult to minimize

these risks (BoltonChen and Wang,2011). This type of risk includes: Economic Factors: The risk that arises outside of the organisation includes the changes

in market condition which influences their activities or task.

specific information about the risks.

2. Identification, evaluation the nature and impact of internal and external risk

A company can reduce negative exposure to business risk by identifying internal and

external risk.

Internal risk: Risk that arises within the organisation in the form of personnel issues or

infrastructure problems etc. is known as Internal Risk.

The three internal risk factors which influences the performance of an organisation are as

follows: Human Factors: Risk that may arise in an organisation from human factors can includes

union strikes, dishonesty by employees, ineffective management or leadership, and

failure on the part of external producers or suppliers. Technological Factors: Risk that arises in an organisation from technological factors

includes unforeseen changes in delivery or distribution of goods and services of company

(Blome and Schoenherr2011). Physical risk: This risk is related to the loss of damage to the assets of a company.

Analysis and impact of one Internal Risk:

Human Factors: Risk related to the Human factors affect the operational activities of an

organisation in the form of union strikes, dishonesty by employees, ineffective management or

leadership, and failure on the part of external producers or suppliers. Therefore it is important to

understand that individuals and groups act differently in different situations. If there is any

misunderstanding or misbehave with their employees may lead to dissatisfaction . Therefore the

incentives must be provide to their employees and stakeholder in order to provide them

maximum level of satisfaction.

External Risk: Risk that arises form outside of a company's organisation are known as

external risk. This type of risk cannot be controlled, or forecasted therefore difficult to minimize

these risks (BoltonChen and Wang,2011). This type of risk includes: Economic Factors: The risk that arises outside of the organisation includes the changes

in market condition which influences their activities or task.

Natural Factors: It includes risk related to the natural disaster that affect normal business

operations. Political risk: It includes risk related to the changes in the political environment.

Evaluation and impact of one external risk:

Natural factors: This risk is related to the natural disaster that adversely affect the

normal operations and it cannot be controlled and managed. Therefore the management cannot

make any strategies or plans for minimizing this risk (Liu, Low and He2011.). Thus this risk if

arise can damage and exploit the operational activities through which the probability condition of

an organisation may also affect. As this type of external risk is unpredictable and uncontrollable

so it is required for the management to concentrate on their identification and the mitigation of

their impact. Identifying possible catastrophes and preparing a plan in order to perform before

this type of risk occur. For example Insurance is one of the instrument that deals with some

uncontrollable risks but having insurance for covering the unpredictable risk helps in preventing

the damage that made by these types of external risks

3. Categorise the risks using the likelihood and impact grid

Risks may fall into three categories therefore risk arises from any category can be fatal to

a strategies of company and even its survival.

Category I:

Preventable risk:

These are the internal risks that arises within the organisation which are controllable and

need to be eliminate or avoided. Examples of such risks are the risks from employees' and

managers' unauthorised, illegal, unethical, incorrect, or inappropriate actions and the risks arise

through breakdown in operational processes. The companies should take care of the defects and

errors so that they cannot damage to the enterprise otherwise avoidance of such errors will result

more costly to the enterprise. The risk category is well managed through active prevention,

monitoring operational processes and guiding behaviour of the people and the decisions towards

desired norms.

Category II:

Strategy risks:

In order to generate superior returns form the strategies, a company should accept some

risk voluntarily. Strategy risks are different from the preventable risk as these risks are not

operations. Political risk: It includes risk related to the changes in the political environment.

Evaluation and impact of one external risk:

Natural factors: This risk is related to the natural disaster that adversely affect the

normal operations and it cannot be controlled and managed. Therefore the management cannot

make any strategies or plans for minimizing this risk (Liu, Low and He2011.). Thus this risk if

arise can damage and exploit the operational activities through which the probability condition of

an organisation may also affect. As this type of external risk is unpredictable and uncontrollable

so it is required for the management to concentrate on their identification and the mitigation of

their impact. Identifying possible catastrophes and preparing a plan in order to perform before

this type of risk occur. For example Insurance is one of the instrument that deals with some

uncontrollable risks but having insurance for covering the unpredictable risk helps in preventing

the damage that made by these types of external risks

3. Categorise the risks using the likelihood and impact grid

Risks may fall into three categories therefore risk arises from any category can be fatal to

a strategies of company and even its survival.

Category I:

Preventable risk:

These are the internal risks that arises within the organisation which are controllable and

need to be eliminate or avoided. Examples of such risks are the risks from employees' and

managers' unauthorised, illegal, unethical, incorrect, or inappropriate actions and the risks arise

through breakdown in operational processes. The companies should take care of the defects and

errors so that they cannot damage to the enterprise otherwise avoidance of such errors will result

more costly to the enterprise. The risk category is well managed through active prevention,

monitoring operational processes and guiding behaviour of the people and the decisions towards

desired norms.

Category II:

Strategy risks:

In order to generate superior returns form the strategies, a company should accept some

risk voluntarily. Strategy risks are different from the preventable risk as these risks are not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

inherently desirable. A strategy with a motive of getting high expected returns generally requires

the company to take on significant risks and managing or monitoring these risks in order to

capture the potential gains. In order to manage this type of risk, the cost benefit of undertaking

the risk should need to be fully understood and analyses and thereafter a contingency plan must

be made in order to deal with a disastrous situation. Therefore the better company should be

considered if they understood and make plan for strategic risk in order to get cost benefit which

helps them to compete with their competitors.

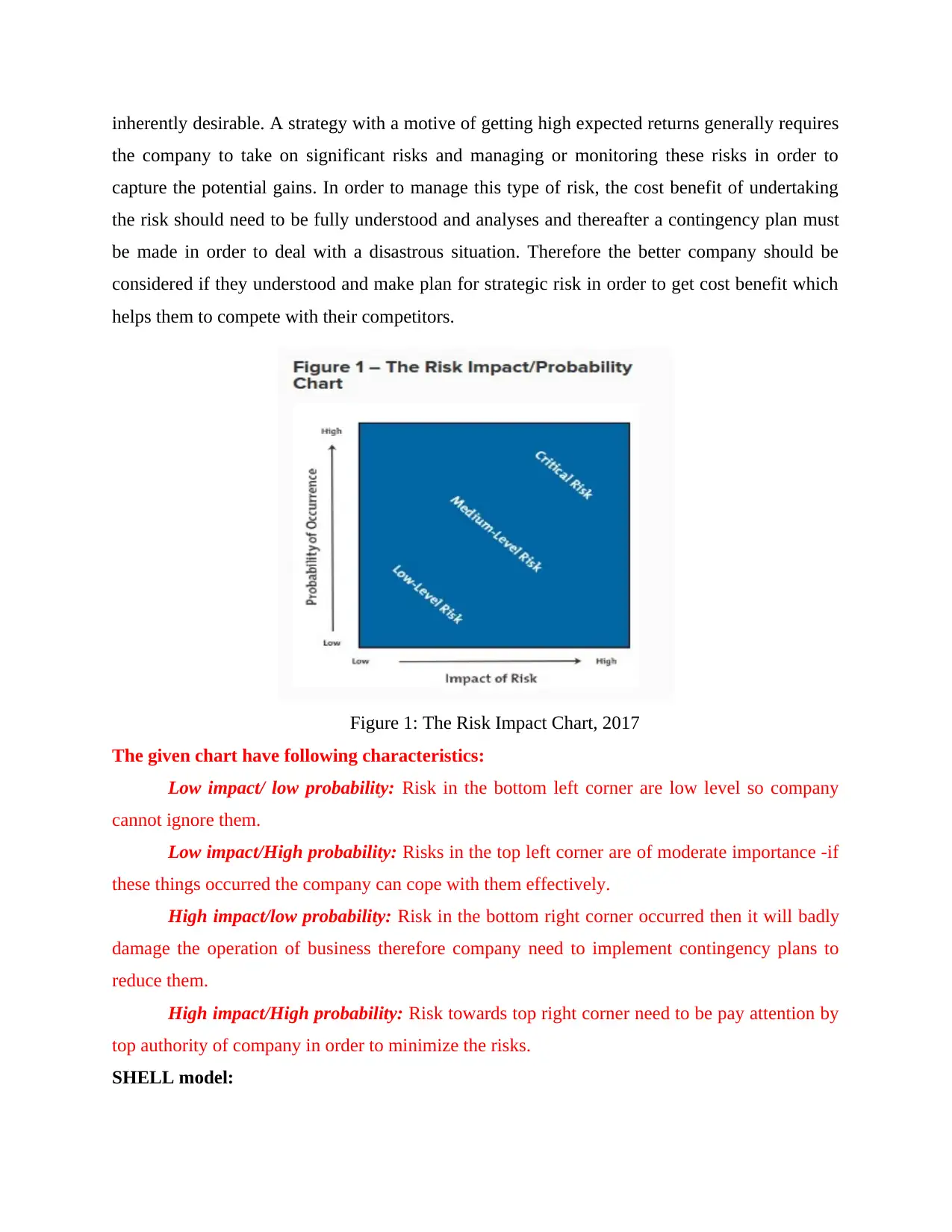

Figure 1: The Risk Impact Chart, 2017

The given chart have following characteristics:

Low impact/ low probability: Risk in the bottom left corner are low level so company

cannot ignore them.

Low impact/High probability: Risks in the top left corner are of moderate importance -if

these things occurred the company can cope with them effectively.

High impact/low probability: Risk in the bottom right corner occurred then it will badly

damage the operation of business therefore company need to implement contingency plans to

reduce them.

High impact/High probability: Risk towards top right corner need to be pay attention by

top authority of company in order to minimize the risks.

SHELL model:

the company to take on significant risks and managing or monitoring these risks in order to

capture the potential gains. In order to manage this type of risk, the cost benefit of undertaking

the risk should need to be fully understood and analyses and thereafter a contingency plan must

be made in order to deal with a disastrous situation. Therefore the better company should be

considered if they understood and make plan for strategic risk in order to get cost benefit which

helps them to compete with their competitors.

Figure 1: The Risk Impact Chart, 2017

The given chart have following characteristics:

Low impact/ low probability: Risk in the bottom left corner are low level so company

cannot ignore them.

Low impact/High probability: Risks in the top left corner are of moderate importance -if

these things occurred the company can cope with them effectively.

High impact/low probability: Risk in the bottom right corner occurred then it will badly

damage the operation of business therefore company need to implement contingency plans to

reduce them.

High impact/High probability: Risk towards top right corner need to be pay attention by

top authority of company in order to minimize the risks.

SHELL model:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

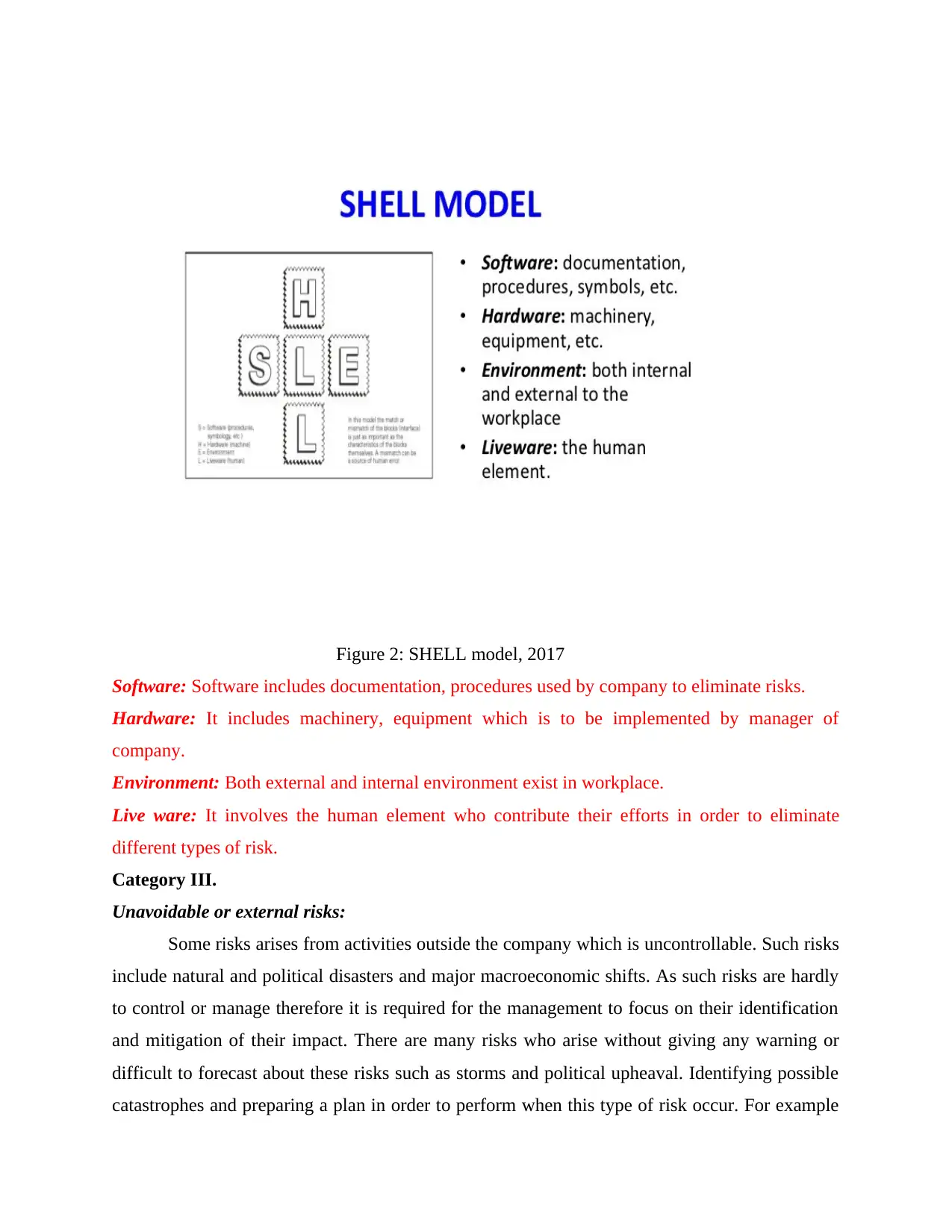

Figure 2: SHELL model, 2017

Software: Software includes documentation, procedures used by company to eliminate risks.

Hardware: It includes machinery, equipment which is to be implemented by manager of

company.

Environment: Both external and internal environment exist in workplace.

Live ware: It involves the human element who contribute their efforts in order to eliminate

different types of risk.

Category III.

Unavoidable or external risks:

Some risks arises from activities outside the company which is uncontrollable. Such risks

include natural and political disasters and major macroeconomic shifts. As such risks are hardly

to control or manage therefore it is required for the management to focus on their identification

and mitigation of their impact. There are many risks who arise without giving any warning or

difficult to forecast about these risks such as storms and political upheaval. Identifying possible

catastrophes and preparing a plan in order to perform when this type of risk occur. For example

Software: Software includes documentation, procedures used by company to eliminate risks.

Hardware: It includes machinery, equipment which is to be implemented by manager of

company.

Environment: Both external and internal environment exist in workplace.

Live ware: It involves the human element who contribute their efforts in order to eliminate

different types of risk.

Category III.

Unavoidable or external risks:

Some risks arises from activities outside the company which is uncontrollable. Such risks

include natural and political disasters and major macroeconomic shifts. As such risks are hardly

to control or manage therefore it is required for the management to focus on their identification

and mitigation of their impact. There are many risks who arise without giving any warning or

difficult to forecast about these risks such as storms and political upheaval. Identifying possible

catastrophes and preparing a plan in order to perform when this type of risk occur. For example

Insurance is way of dealing with some uncontrollable risks but having insurance for covering the

unpredictable risk helps in preventing the damage that made by these types of external risks.

4. Risk Mitigating Strategies to minimize internal and external risk

Risk management includes front-end planning about the managing and mitigating the risk

after identifying certain risk. Therefore risk mitigation strategies and specific action plans should

be incorporated in order to managing the risk in effective manner. Risk mitigation plans should:

Characterise the root cause of risks that have been identified and quantified as early as

possible in order to find out the information about the risks.

Evaluate risk interactions and common cause

Identify alternative mitigation strategies, methods and tools of each major risk.

Assess and prioritize mitigation alternatives.

Select and utilize the resource requires for specific risk mitigation alternatives.

Communicate planning should be done to all factors for implementation

Risk mitigation strategies is necessarily required after making a thorough analysing and

evaluation of the possible threats, hazards that can affect or influence business operations. The

purpose of such strategies is to eliminate and reduce risk before it damage the operational

activities (Alhawari and et. al., 2012.). The best practices require that known and perceived risks

be analysed according to the degree and likelihood of the adverse results that are anticipated to

take place. All such risk analysed should need to be documented according to their priorities.

There are five ways through which organisation can manage internal as well as external: Accept the risk: It means that management should first identified the risk and resolve

according to their consequences. This is a good strategy to use for every small risk that

wont have much impact on the operational activities (Alhawari and et. al., 2012). Avoid the risk: When the risk is uncontrolled and cannot managed then the management

should need to avoid the risk and put their efforts to solve those risks which are

controlled and managed in effective and efficient manner. Transfer the risk: It means if authorised person is unable to control or managed the risk

then they should need to transfer their risk to someone who is capable in handling the

risk.

unpredictable risk helps in preventing the damage that made by these types of external risks.

4. Risk Mitigating Strategies to minimize internal and external risk

Risk management includes front-end planning about the managing and mitigating the risk

after identifying certain risk. Therefore risk mitigation strategies and specific action plans should

be incorporated in order to managing the risk in effective manner. Risk mitigation plans should:

Characterise the root cause of risks that have been identified and quantified as early as

possible in order to find out the information about the risks.

Evaluate risk interactions and common cause

Identify alternative mitigation strategies, methods and tools of each major risk.

Assess and prioritize mitigation alternatives.

Select and utilize the resource requires for specific risk mitigation alternatives.

Communicate planning should be done to all factors for implementation

Risk mitigation strategies is necessarily required after making a thorough analysing and

evaluation of the possible threats, hazards that can affect or influence business operations. The

purpose of such strategies is to eliminate and reduce risk before it damage the operational

activities (Alhawari and et. al., 2012.). The best practices require that known and perceived risks

be analysed according to the degree and likelihood of the adverse results that are anticipated to

take place. All such risk analysed should need to be documented according to their priorities.

There are five ways through which organisation can manage internal as well as external: Accept the risk: It means that management should first identified the risk and resolve

according to their consequences. This is a good strategy to use for every small risk that

wont have much impact on the operational activities (Alhawari and et. al., 2012). Avoid the risk: When the risk is uncontrolled and cannot managed then the management

should need to avoid the risk and put their efforts to solve those risks which are

controlled and managed in effective and efficient manner. Transfer the risk: It means if authorised person is unable to control or managed the risk

then they should need to transfer their risk to someone who is capable in handling the

risk.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Mitigate the risk: Certain actions and tools are ned to be implemented to reduce the risk

in effective and efficient manner (Brustbauer, 2016.). Proper training and guidance

should need to provided which helps in control and tackle the risk without facing any

problems. Exploit the risk: The acceptance, avoidance, transference and mitigation are required to

use when the risk has a negative impact on the operational, financial related activities.

Overview of Financial position of Bauhaus HK company:

Financial review:

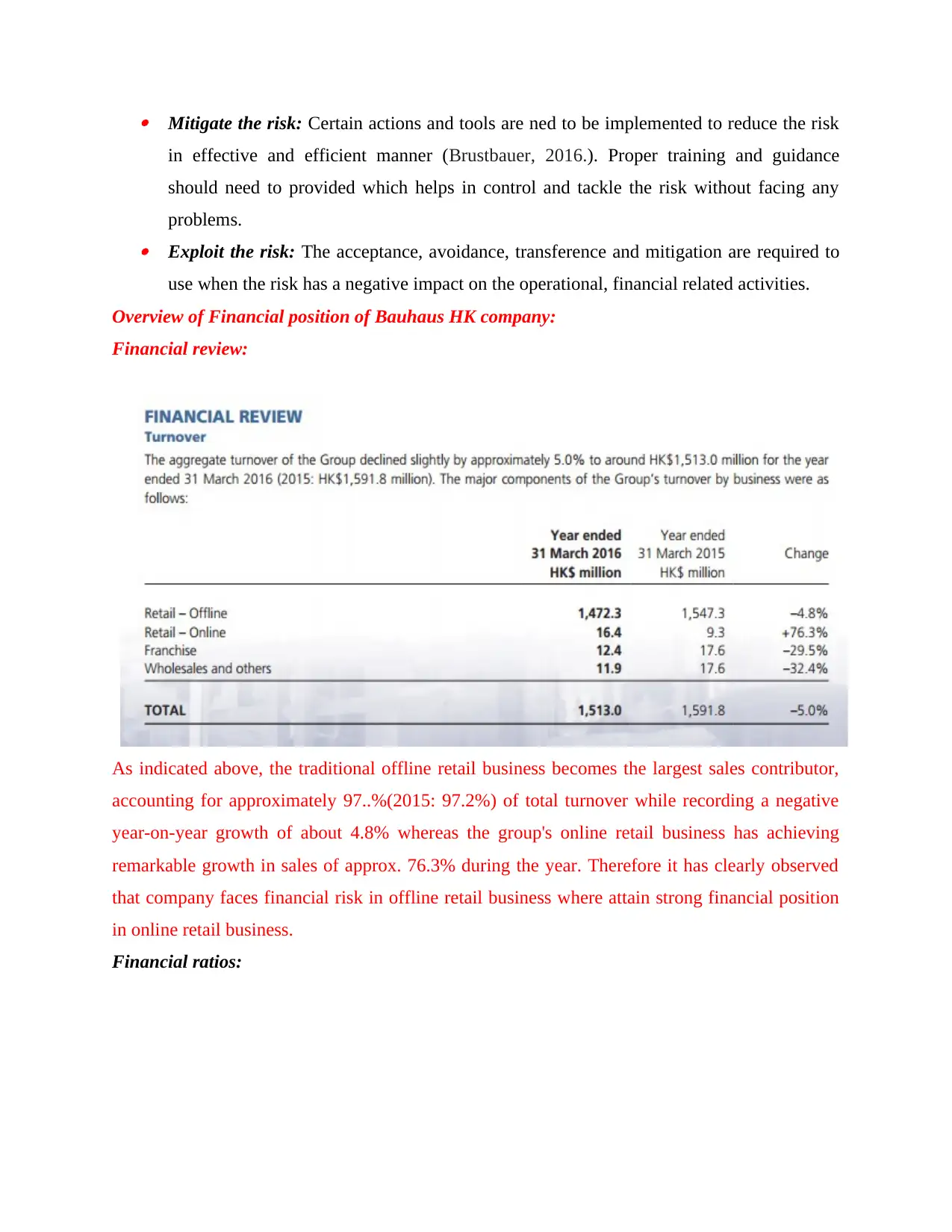

As indicated above, the traditional offline retail business becomes the largest sales contributor,

accounting for approximately 97..%(2015: 97.2%) of total turnover while recording a negative

year-on-year growth of about 4.8% whereas the group's online retail business has achieving

remarkable growth in sales of approx. 76.3% during the year. Therefore it has clearly observed

that company faces financial risk in offline retail business where attain strong financial position

in online retail business.

Financial ratios:

in effective and efficient manner (Brustbauer, 2016.). Proper training and guidance

should need to provided which helps in control and tackle the risk without facing any

problems. Exploit the risk: The acceptance, avoidance, transference and mitigation are required to

use when the risk has a negative impact on the operational, financial related activities.

Overview of Financial position of Bauhaus HK company:

Financial review:

As indicated above, the traditional offline retail business becomes the largest sales contributor,

accounting for approximately 97..%(2015: 97.2%) of total turnover while recording a negative

year-on-year growth of about 4.8% whereas the group's online retail business has achieving

remarkable growth in sales of approx. 76.3% during the year. Therefore it has clearly observed

that company faces financial risk in offline retail business where attain strong financial position

in online retail business.

Financial ratios:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

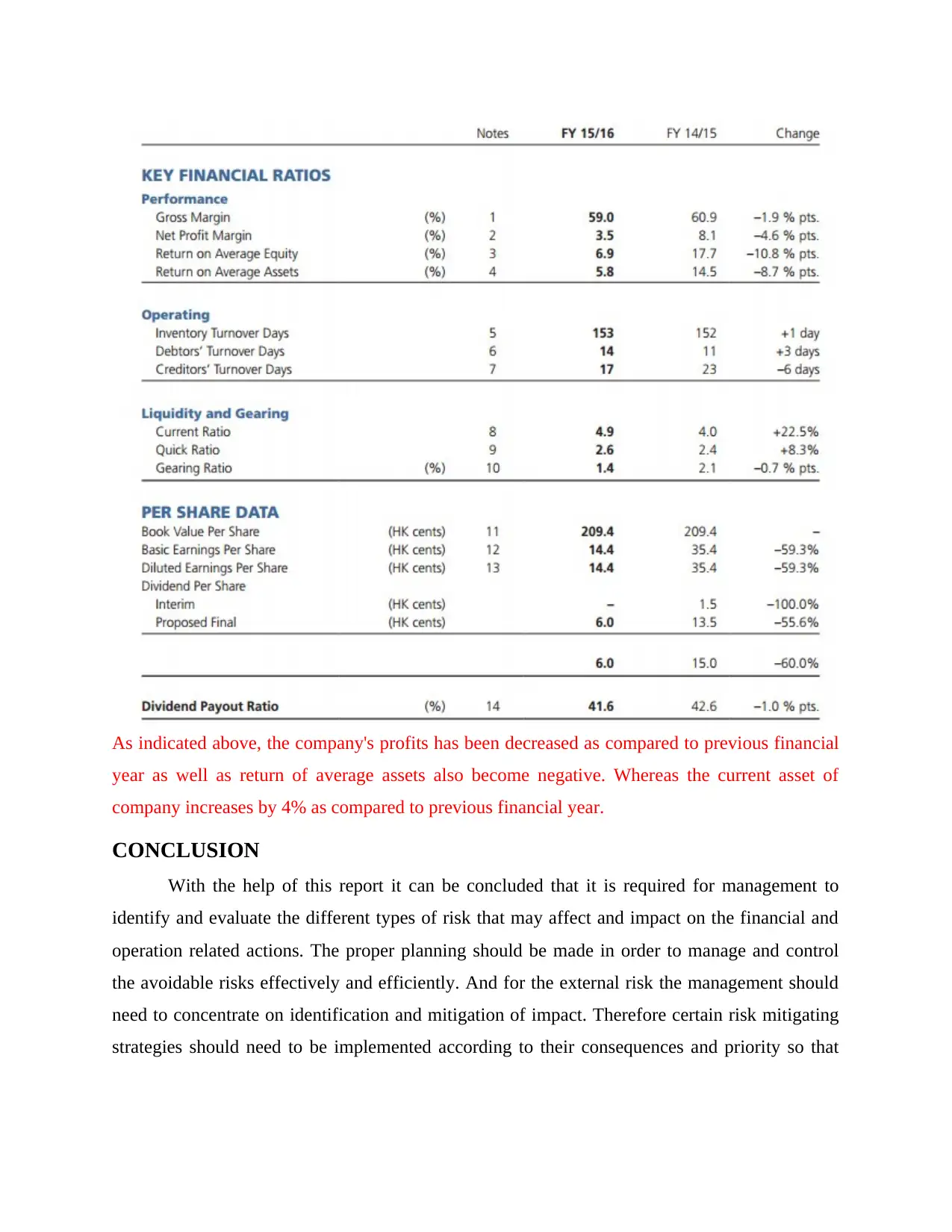

As indicated above, the company's profits has been decreased as compared to previous financial

year as well as return of average assets also become negative. Whereas the current asset of

company increases by 4% as compared to previous financial year.

CONCLUSION

With the help of this report it can be concluded that it is required for management to

identify and evaluate the different types of risk that may affect and impact on the financial and

operation related actions. The proper planning should be made in order to manage and control

the avoidable risks effectively and efficiently. And for the external risk the management should

need to concentrate on identification and mitigation of impact. Therefore certain risk mitigating

strategies should need to be implemented according to their consequences and priority so that

year as well as return of average assets also become negative. Whereas the current asset of

company increases by 4% as compared to previous financial year.

CONCLUSION

With the help of this report it can be concluded that it is required for management to

identify and evaluate the different types of risk that may affect and impact on the financial and

operation related actions. The proper planning should be made in order to manage and control

the avoidable risks effectively and efficiently. And for the external risk the management should

need to concentrate on identification and mitigation of impact. Therefore certain risk mitigating

strategies should need to be implemented according to their consequences and priority so that

there is no hindrance come in organisational activities which helps in achieving their desired

objectives.

objectives.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.