Baulkham Hills Shire Council Cost Allocation: ACCT20076 Analysis

VerifiedAdded on 2023/06/07

|10

|780

|370

Practical Assignment

AI Summary

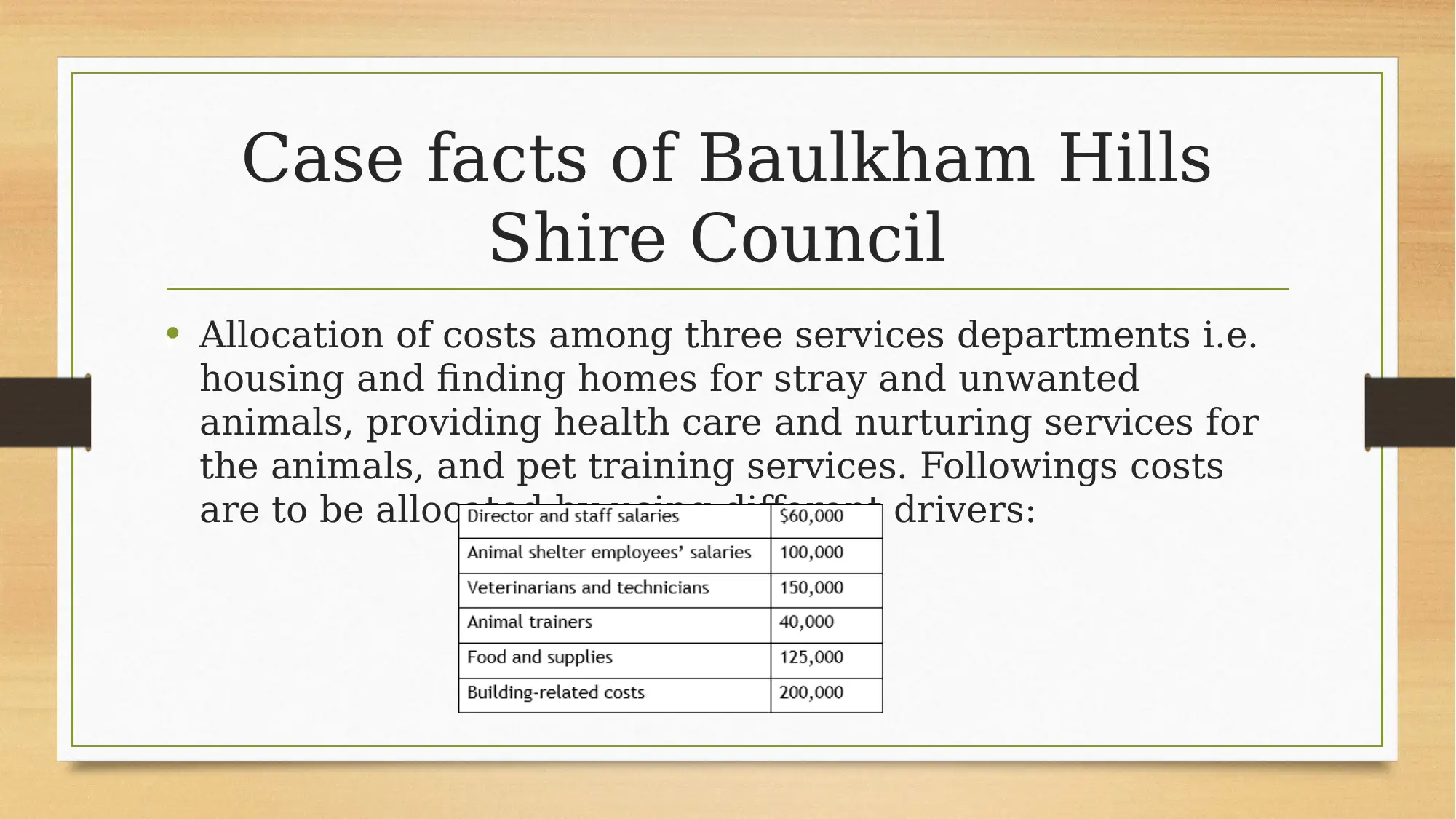

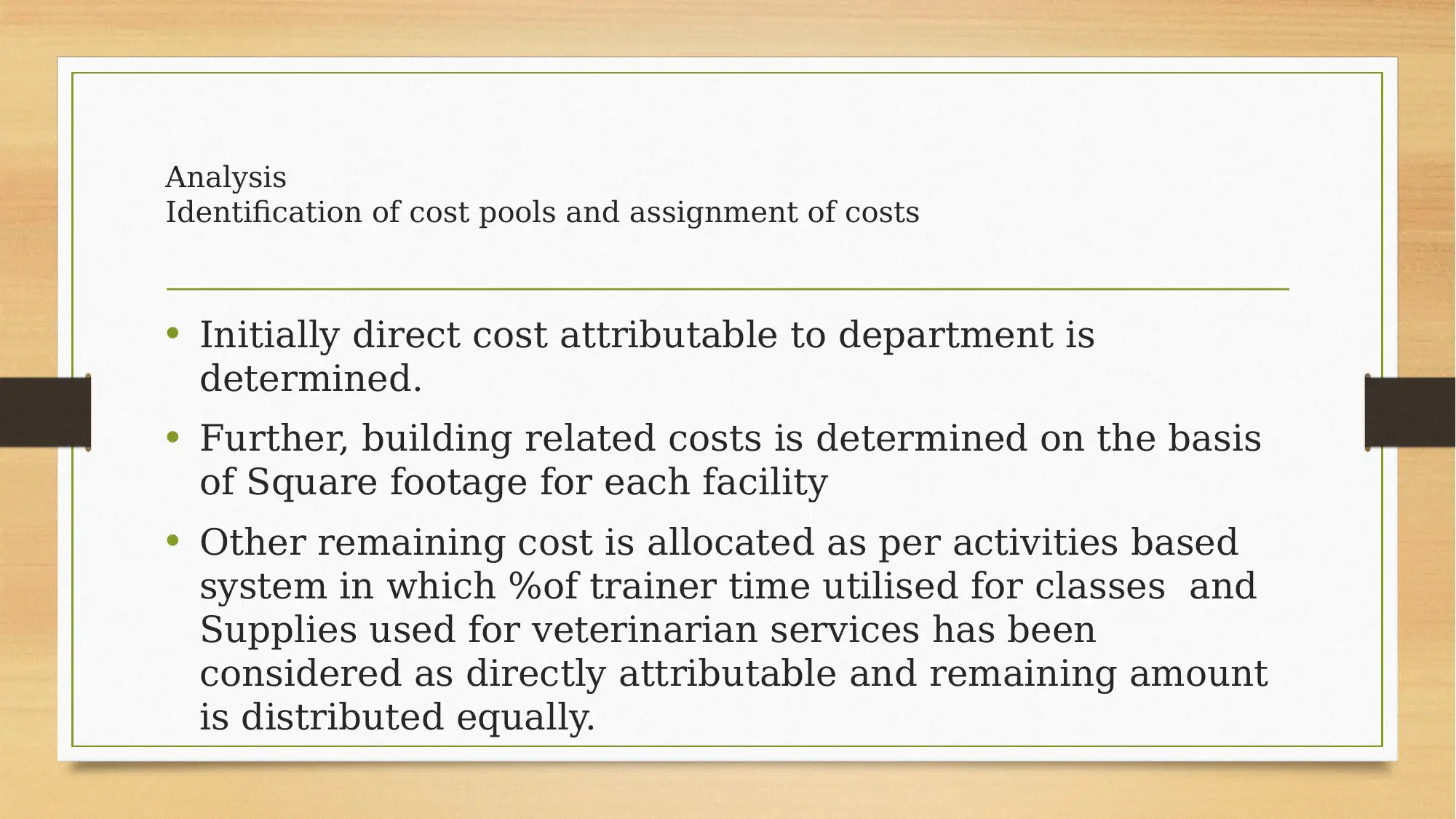

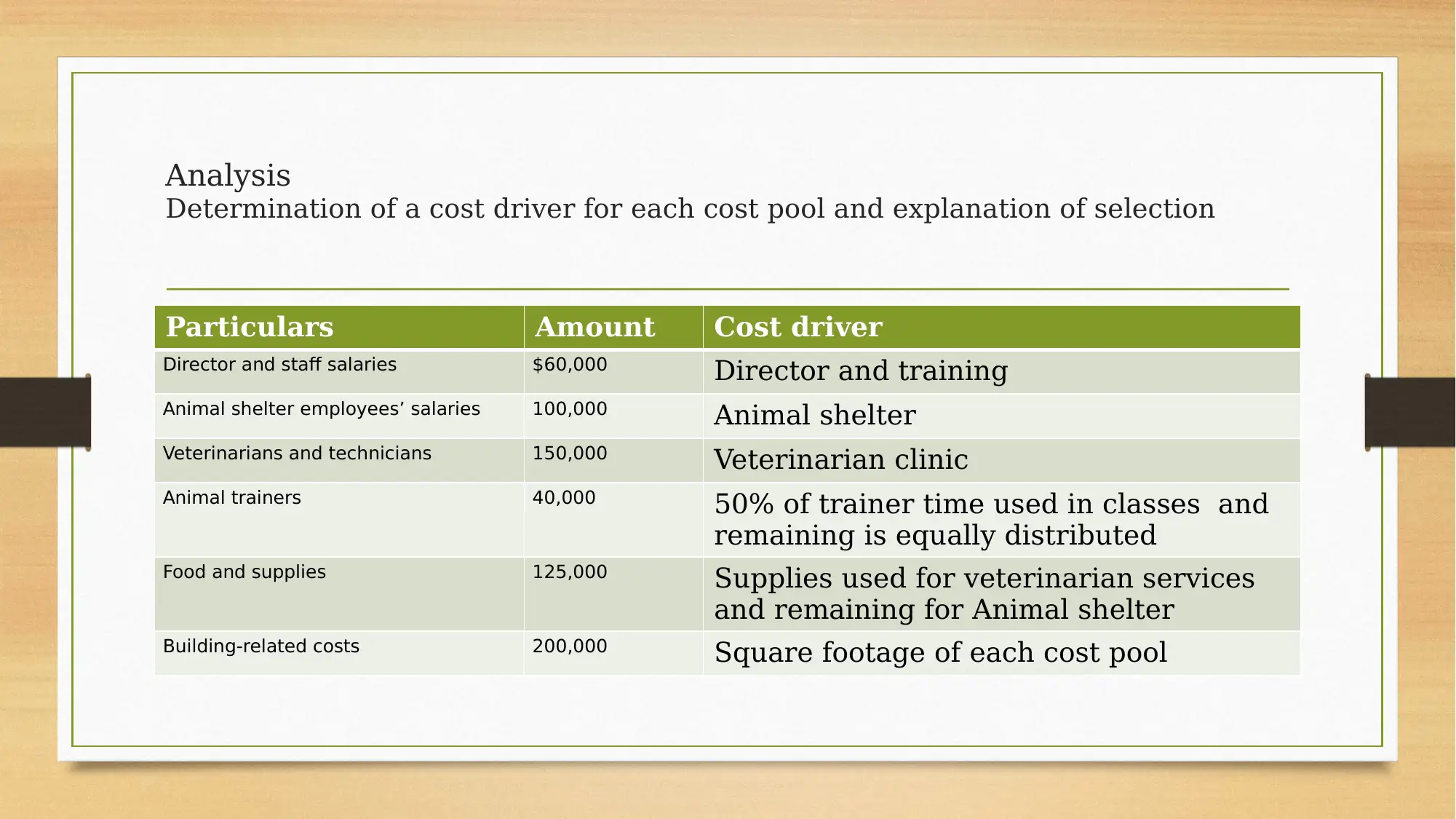

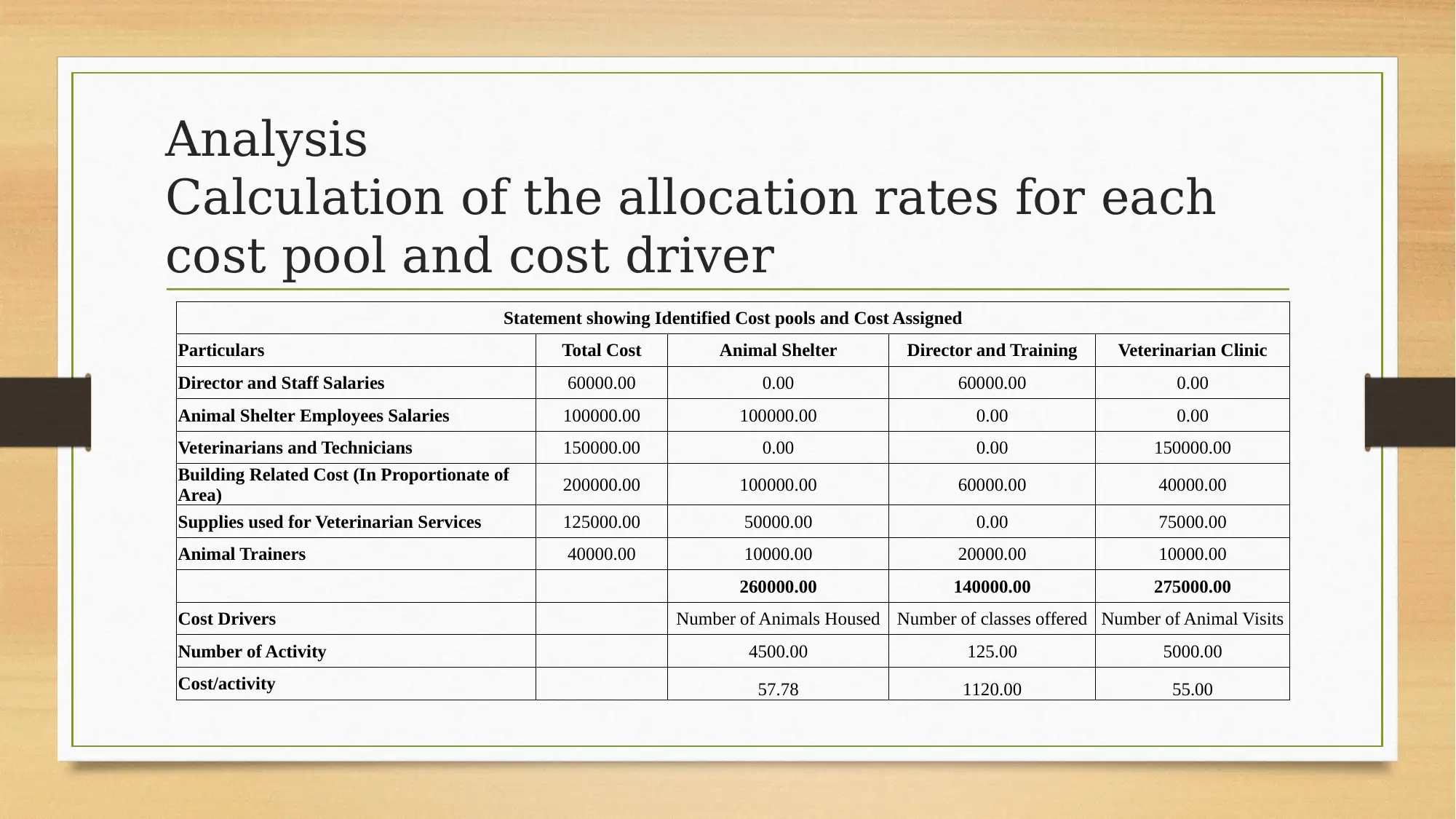

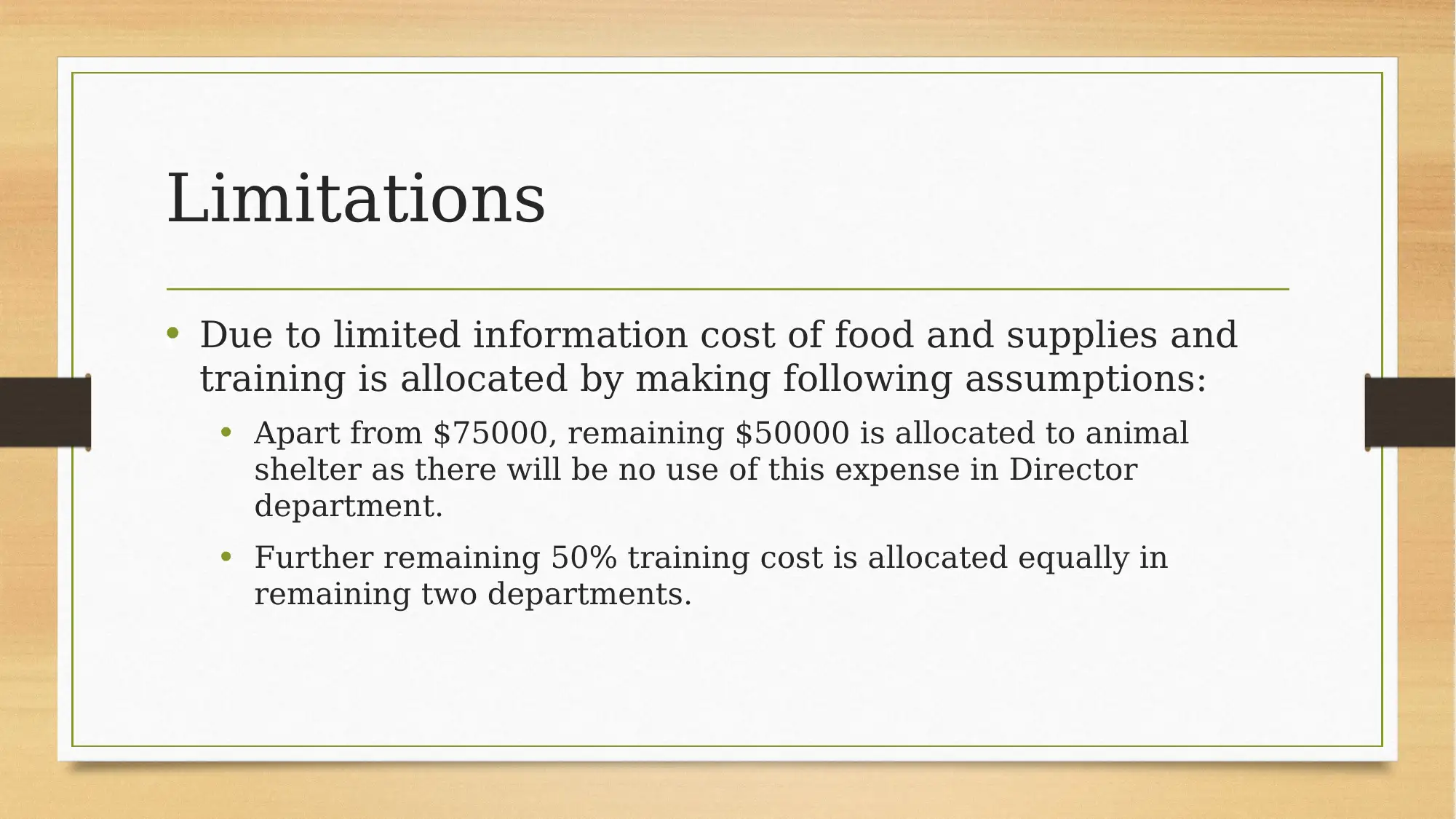

This assignment presents a practical application of activity-based costing (ABC) to allocate costs within the Baulkham Hills Shire Council, specifically across three service departments: animal shelter, veterinary clinic, and director/training. The solution begins with an executive summary outlining the problem of cost allocation and the rationale for using ABC over traditional costing methods, emphasizing its accuracy in allocating indirect costs. The analysis identifies cost pools and assigns costs based on direct attribution, square footage, and activity-based drivers such as trainer time and supplies used. The document details the calculation of allocation rates for each cost pool and cost driver, demonstrating how the costs are distributed across the departments. The findings highlight the benefits of ABC in determining service prices and overall costs, while acknowledging limitations in the allocation of certain expenses due to data constraints. The assignment concludes with a discussion of the limitations and references supporting the methodology. This assignment is a solution to ACCT20076 and provides a comprehensive example of cost accounting principles.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.