BBAC501: Cost-Volume-Profit Analysis Report for Daphne Int'l

VerifiedAdded on 2023/06/07

|7

|2622

|110

Report

AI Summary

This report presents a comprehensive cost-volume-profit (CVP) analysis of Daphne International Holdings Limited (DIHL), a major shoe manufacturer. It calculates the company's budgeted net profit for 2018, determines break-even points for different shoe types (Shoe-A, Shoe-B, and Shoe-C) considering a constant sales mix, and computes the margin of safety in both units and sales dollars. The analysis also explores the impact of changes in variable manufacturing and selling costs on the break-even point. Furthermore, it suggests an optimal sales mix to maximize profitability given production constraints. The report uses data provided by DIHL's finance department and addresses various requirements related to CVP analysis, offering insights into DIHL's financial performance and decision-making processes.

BBAC501 Group Assignment-18T3

Assignment

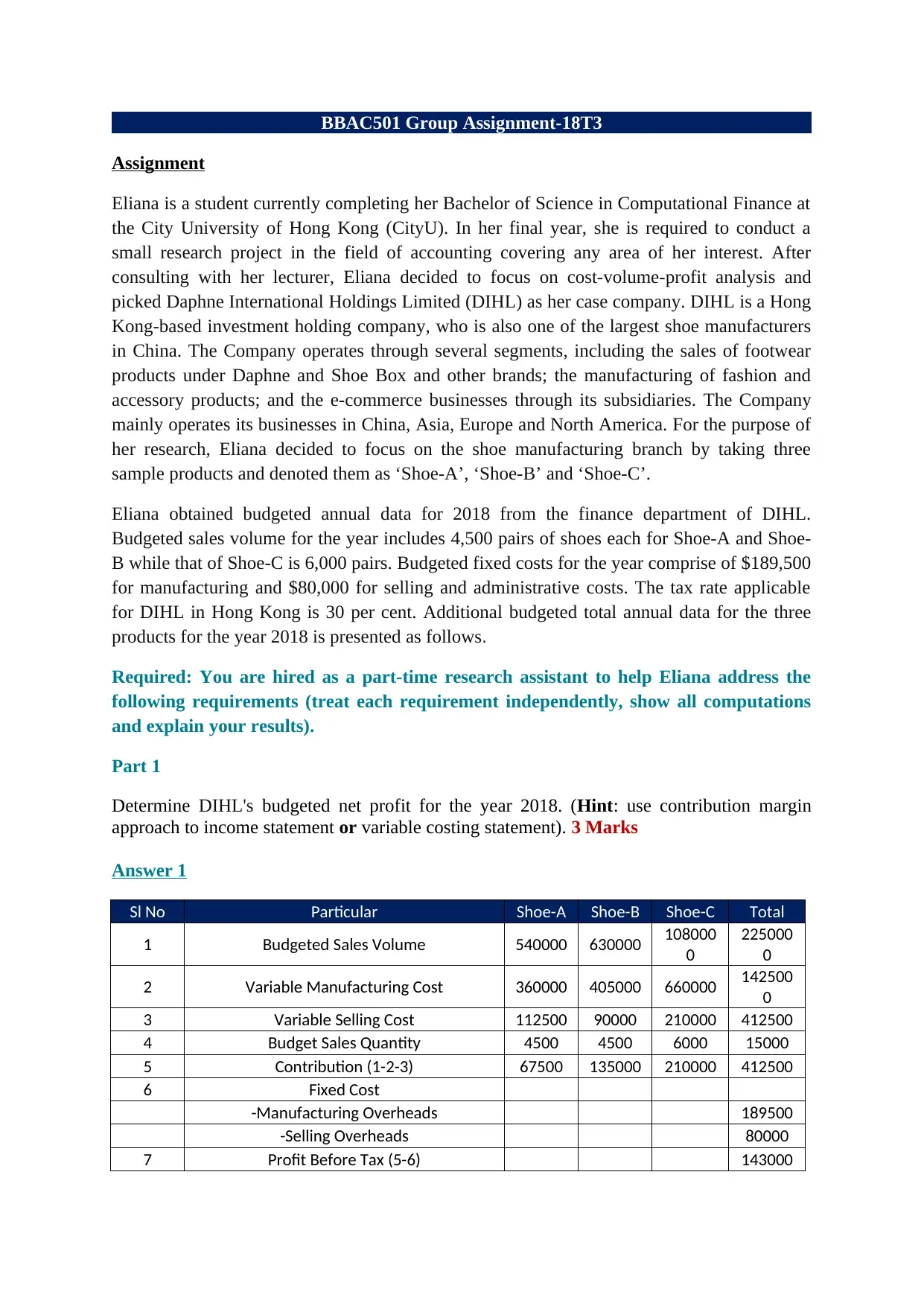

Eliana is a student currently completing her Bachelor of Science in Computational Finance at

the City University of Hong Kong (CityU). In her final year, she is required to conduct a

small research project in the field of accounting covering any area of her interest. After

consulting with her lecturer, Eliana decided to focus on cost-volume-profit analysis and

picked Daphne International Holdings Limited (DIHL) as her case company. DIHL is a Hong

Kong-based investment holding company, who is also one of the largest shoe manufacturers

in China. The Company operates through several segments, including the sales of footwear

products under Daphne and Shoe Box and other brands; the manufacturing of fashion and

accessory products; and the e-commerce businesses through its subsidiaries. The Company

mainly operates its businesses in China, Asia, Europe and North America. For the purpose of

her research, Eliana decided to focus on the shoe manufacturing branch by taking three

sample products and denoted them as ‘Shoe-A’, ‘Shoe-B’ and ‘Shoe-C’.

Eliana obtained budgeted annual data for 2018 from the finance department of DIHL.

Budgeted sales volume for the year includes 4,500 pairs of shoes each for Shoe-A and Shoe-

B while that of Shoe-C is 6,000 pairs. Budgeted fixed costs for the year comprise of $189,500

for manufacturing and $80,000 for selling and administrative costs. The tax rate applicable

for DIHL in Hong Kong is 30 per cent. Additional budgeted total annual data for the three

products for the year 2018 is presented as follows.

Required: You are hired as a part-time research assistant to help Eliana address the

following requirements (treat each requirement independently, show all computations

and explain your results).

Part 1

Determine DIHL's budgeted net profit for the year 2018. (Hint: use contribution margin

approach to income statement or variable costing statement). 3 Marks

Answer 1

Sl No Particular Shoe-A Shoe-B Shoe-C Total

1 Budgeted Sales Volume 540000 630000 108000

0

225000

0

2 Variable Manufacturing Cost 360000 405000 660000 142500

0

3 Variable Selling Cost 112500 90000 210000 412500

4 Budget Sales Quantity 4500 4500 6000 15000

5 Contribution (1-2-3) 67500 135000 210000 412500

6 Fixed Cost

-Manufacturing Overheads 189500

-Selling Overheads 80000

7 Profit Before Tax (5-6) 143000

Assignment

Eliana is a student currently completing her Bachelor of Science in Computational Finance at

the City University of Hong Kong (CityU). In her final year, she is required to conduct a

small research project in the field of accounting covering any area of her interest. After

consulting with her lecturer, Eliana decided to focus on cost-volume-profit analysis and

picked Daphne International Holdings Limited (DIHL) as her case company. DIHL is a Hong

Kong-based investment holding company, who is also one of the largest shoe manufacturers

in China. The Company operates through several segments, including the sales of footwear

products under Daphne and Shoe Box and other brands; the manufacturing of fashion and

accessory products; and the e-commerce businesses through its subsidiaries. The Company

mainly operates its businesses in China, Asia, Europe and North America. For the purpose of

her research, Eliana decided to focus on the shoe manufacturing branch by taking three

sample products and denoted them as ‘Shoe-A’, ‘Shoe-B’ and ‘Shoe-C’.

Eliana obtained budgeted annual data for 2018 from the finance department of DIHL.

Budgeted sales volume for the year includes 4,500 pairs of shoes each for Shoe-A and Shoe-

B while that of Shoe-C is 6,000 pairs. Budgeted fixed costs for the year comprise of $189,500

for manufacturing and $80,000 for selling and administrative costs. The tax rate applicable

for DIHL in Hong Kong is 30 per cent. Additional budgeted total annual data for the three

products for the year 2018 is presented as follows.

Required: You are hired as a part-time research assistant to help Eliana address the

following requirements (treat each requirement independently, show all computations

and explain your results).

Part 1

Determine DIHL's budgeted net profit for the year 2018. (Hint: use contribution margin

approach to income statement or variable costing statement). 3 Marks

Answer 1

Sl No Particular Shoe-A Shoe-B Shoe-C Total

1 Budgeted Sales Volume 540000 630000 108000

0

225000

0

2 Variable Manufacturing Cost 360000 405000 660000 142500

0

3 Variable Selling Cost 112500 90000 210000 412500

4 Budget Sales Quantity 4500 4500 6000 15000

5 Contribution (1-2-3) 67500 135000 210000 412500

6 Fixed Cost

-Manufacturing Overheads 189500

-Selling Overheads 80000

7 Profit Before Tax (5-6) 143000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8 Tax (7*30%) 42900

9 Net Profit (7-8) 100100

The above computation has been carried out by Using formula of Sales less variable cost i.e.

contribution. Further, contribution is reduced by Fixed Cost to give profit before tax. Post

that, tax has been deducted on profits @30% as stated in the details given above to give net

profit by manufacturing shoes.(Anon., n.d.)

Further, fixed cost has not been allocated over different grade of shoes as the question states

about DIHL’s budgeted profitability and not on profit of individual shoes. Accordingly, the

budgeted profit of the company stands at AUD 100,100/-.

Part 2

Assuming the sales mix remains constant though out 2018, determine how many pairs of

shoes must be sold for each type in order to breakeven. 4 Marks

Answer 2

Sl No Particular Shoe-

A Shoe-B Shoe-C Total

1 Budgeted Sales Volume 540000 630000 108000

0

225000

0

2 Per Unit Sales Price (1/7) 120 140 180

3 Variable Manufacturing Cost 360000 405000 660000 142500

0

4 Per Unit Variable manufacturing Cost

(3/7) 80 90 110

5 Variable Selling Cost 112500 90000 210000 412500

6 Per Unit Variable Selling Cost (5/7) 25 20 35

7 Budget Sales Quantity 4500 4500 6000 15000

8 Contribution (1-3-5) 67500 135000 210000 412500

9 Per Unit Contribution (8/7) 15 30 35

10 Sales Mix (4500:4500:6000) 3 3 4 10

11 Contribution under sales mix (9*10) 45 90 140 275

12 Fixed Cost

13 -Manufacturing Overheads 189500

14 -Selling Overheads 80000

15 Total Fixed Cost 269500

16 Break Even quantity (15/11)*10 9800

17 Number of pairs to be ordered 2940 2940 3920 9800

On perusal of the table, one can understand that breakeven sales for the company stands at

9800 units based on sales mix computed above. The formula for computation of breakeven

quantity has been provided here-in-below(WebFinance Inc, 2018)

(Fixed Cost of company/ Contribution as per sales mix)* Sales Mix Quantity.

9 Net Profit (7-8) 100100

The above computation has been carried out by Using formula of Sales less variable cost i.e.

contribution. Further, contribution is reduced by Fixed Cost to give profit before tax. Post

that, tax has been deducted on profits @30% as stated in the details given above to give net

profit by manufacturing shoes.(Anon., n.d.)

Further, fixed cost has not been allocated over different grade of shoes as the question states

about DIHL’s budgeted profitability and not on profit of individual shoes. Accordingly, the

budgeted profit of the company stands at AUD 100,100/-.

Part 2

Assuming the sales mix remains constant though out 2018, determine how many pairs of

shoes must be sold for each type in order to breakeven. 4 Marks

Answer 2

Sl No Particular Shoe-

A Shoe-B Shoe-C Total

1 Budgeted Sales Volume 540000 630000 108000

0

225000

0

2 Per Unit Sales Price (1/7) 120 140 180

3 Variable Manufacturing Cost 360000 405000 660000 142500

0

4 Per Unit Variable manufacturing Cost

(3/7) 80 90 110

5 Variable Selling Cost 112500 90000 210000 412500

6 Per Unit Variable Selling Cost (5/7) 25 20 35

7 Budget Sales Quantity 4500 4500 6000 15000

8 Contribution (1-3-5) 67500 135000 210000 412500

9 Per Unit Contribution (8/7) 15 30 35

10 Sales Mix (4500:4500:6000) 3 3 4 10

11 Contribution under sales mix (9*10) 45 90 140 275

12 Fixed Cost

13 -Manufacturing Overheads 189500

14 -Selling Overheads 80000

15 Total Fixed Cost 269500

16 Break Even quantity (15/11)*10 9800

17 Number of pairs to be ordered 2940 2940 3920 9800

On perusal of the table, one can understand that breakeven sales for the company stands at

9800 units based on sales mix computed above. The formula for computation of breakeven

quantity has been provided here-in-below(WebFinance Inc, 2018)

(Fixed Cost of company/ Contribution as per sales mix)* Sales Mix Quantity.

Further, sales mix has been derived by taking ratio of budgeted sales quantity provided in

question.

In addition contribution per unit has been derived by computing contribution per grade of

shoe divided by total budgeted sales quantity of such grade.

Post the aforesaid; the breakeven quantity has been allocated over each grade on the basis of

sales mix. Thus, the break-even sales of each shoe grade is 2940, 2940 and 3920 units for A,

B and C respectively.

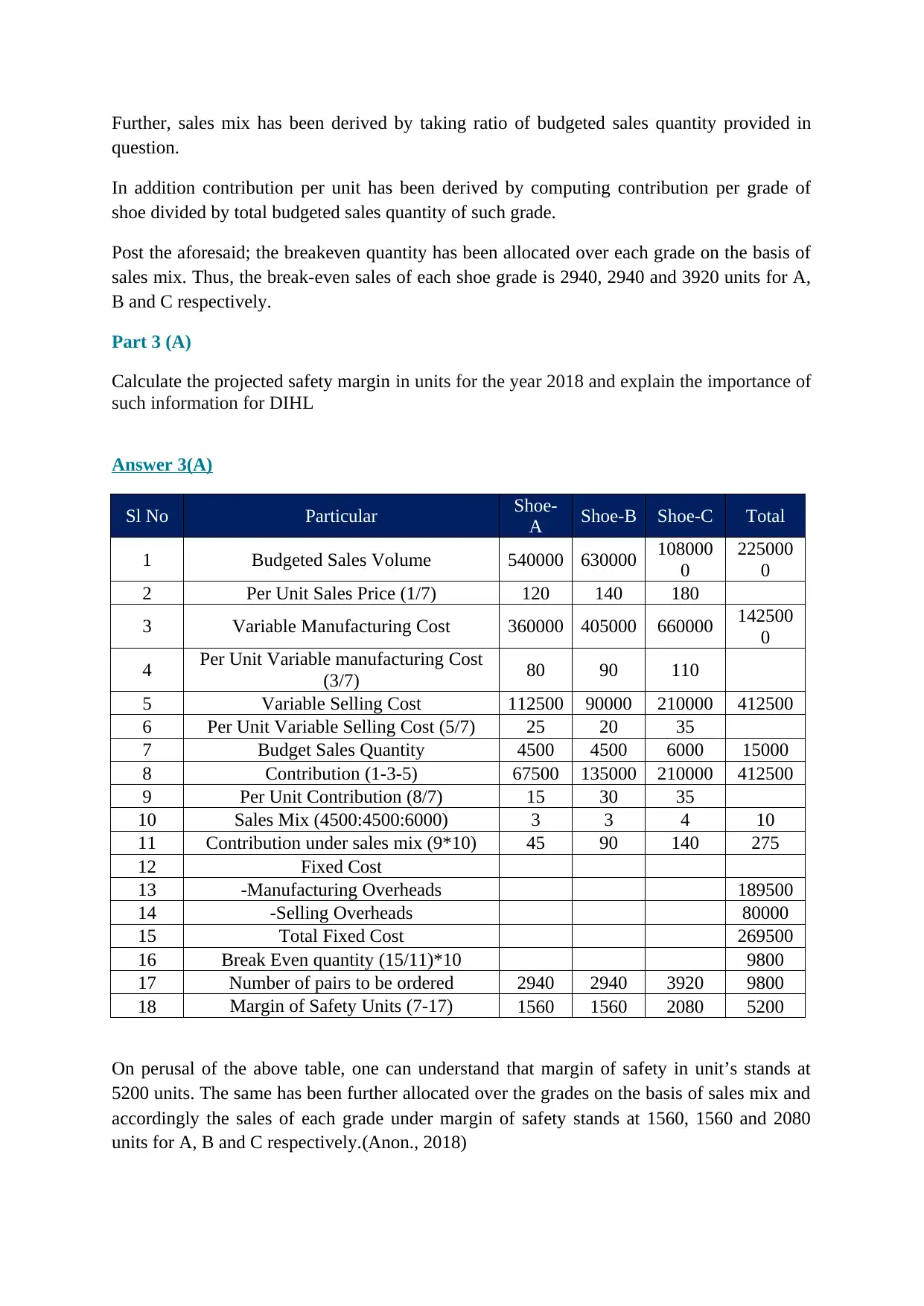

Part 3 (A)

Calculate the projected safety margin in units for the year 2018 and explain the importance of

such information for DIHL

Answer 3(A)

Sl No Particular Shoe-

A Shoe-B Shoe-C Total

1 Budgeted Sales Volume 540000 630000 108000

0

225000

0

2 Per Unit Sales Price (1/7) 120 140 180

3 Variable Manufacturing Cost 360000 405000 660000 142500

0

4 Per Unit Variable manufacturing Cost

(3/7) 80 90 110

5 Variable Selling Cost 112500 90000 210000 412500

6 Per Unit Variable Selling Cost (5/7) 25 20 35

7 Budget Sales Quantity 4500 4500 6000 15000

8 Contribution (1-3-5) 67500 135000 210000 412500

9 Per Unit Contribution (8/7) 15 30 35

10 Sales Mix (4500:4500:6000) 3 3 4 10

11 Contribution under sales mix (9*10) 45 90 140 275

12 Fixed Cost

13 -Manufacturing Overheads 189500

14 -Selling Overheads 80000

15 Total Fixed Cost 269500

16 Break Even quantity (15/11)*10 9800

17 Number of pairs to be ordered 2940 2940 3920 9800

18 Margin of Safety Units (7-17) 1560 1560 2080 5200

On perusal of the above table, one can understand that margin of safety in unit’s stands at

5200 units. The same has been further allocated over the grades on the basis of sales mix and

accordingly the sales of each grade under margin of safety stands at 1560, 1560 and 2080

units for A, B and C respectively.(Anon., 2018)

question.

In addition contribution per unit has been derived by computing contribution per grade of

shoe divided by total budgeted sales quantity of such grade.

Post the aforesaid; the breakeven quantity has been allocated over each grade on the basis of

sales mix. Thus, the break-even sales of each shoe grade is 2940, 2940 and 3920 units for A,

B and C respectively.

Part 3 (A)

Calculate the projected safety margin in units for the year 2018 and explain the importance of

such information for DIHL

Answer 3(A)

Sl No Particular Shoe-

A Shoe-B Shoe-C Total

1 Budgeted Sales Volume 540000 630000 108000

0

225000

0

2 Per Unit Sales Price (1/7) 120 140 180

3 Variable Manufacturing Cost 360000 405000 660000 142500

0

4 Per Unit Variable manufacturing Cost

(3/7) 80 90 110

5 Variable Selling Cost 112500 90000 210000 412500

6 Per Unit Variable Selling Cost (5/7) 25 20 35

7 Budget Sales Quantity 4500 4500 6000 15000

8 Contribution (1-3-5) 67500 135000 210000 412500

9 Per Unit Contribution (8/7) 15 30 35

10 Sales Mix (4500:4500:6000) 3 3 4 10

11 Contribution under sales mix (9*10) 45 90 140 275

12 Fixed Cost

13 -Manufacturing Overheads 189500

14 -Selling Overheads 80000

15 Total Fixed Cost 269500

16 Break Even quantity (15/11)*10 9800

17 Number of pairs to be ordered 2940 2940 3920 9800

18 Margin of Safety Units (7-17) 1560 1560 2080 5200

On perusal of the above table, one can understand that margin of safety in unit’s stands at

5200 units. The same has been further allocated over the grades on the basis of sales mix and

accordingly the sales of each grade under margin of safety stands at 1560, 1560 and 2080

units for A, B and C respectively.(Anon., 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Further, margin of safety units have been computed using the formula provided here-in-

below:

Total Budgeted sales Quantity-Break Even Sales Quantity.

Further, the importance of margin of safety has been described here-in-below

(a) It helps to analyse the management regarding the decline in sales of quantity which can

lead to break-even;

(b) It helps in decision making regarding expansion in sales;

(c) Higher Margin of Safety is indicative of chances of profitability being high;(Accounting

For Management, 2018)

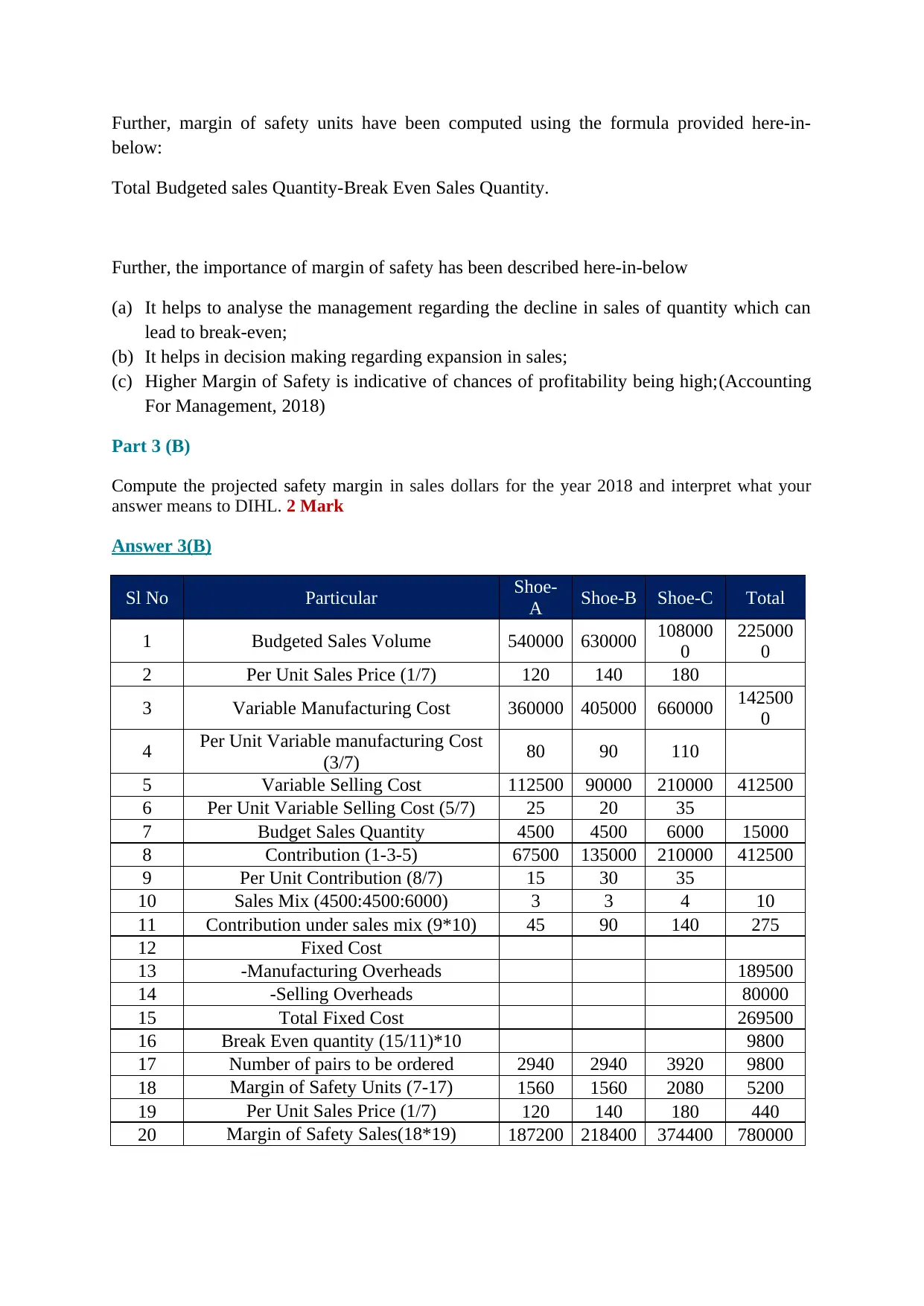

Part 3 (B)

Compute the projected safety margin in sales dollars for the year 2018 and interpret what your

answer means to DIHL. 2 Mark

Answer 3(B)

Sl No Particular Shoe-

A Shoe-B Shoe-C Total

1 Budgeted Sales Volume 540000 630000 108000

0

225000

0

2 Per Unit Sales Price (1/7) 120 140 180

3 Variable Manufacturing Cost 360000 405000 660000 142500

0

4 Per Unit Variable manufacturing Cost

(3/7) 80 90 110

5 Variable Selling Cost 112500 90000 210000 412500

6 Per Unit Variable Selling Cost (5/7) 25 20 35

7 Budget Sales Quantity 4500 4500 6000 15000

8 Contribution (1-3-5) 67500 135000 210000 412500

9 Per Unit Contribution (8/7) 15 30 35

10 Sales Mix (4500:4500:6000) 3 3 4 10

11 Contribution under sales mix (9*10) 45 90 140 275

12 Fixed Cost

13 -Manufacturing Overheads 189500

14 -Selling Overheads 80000

15 Total Fixed Cost 269500

16 Break Even quantity (15/11)*10 9800

17 Number of pairs to be ordered 2940 2940 3920 9800

18 Margin of Safety Units (7-17) 1560 1560 2080 5200

19 Per Unit Sales Price (1/7) 120 140 180 440

20 Margin of Safety Sales(18*19) 187200 218400 374400 780000

below:

Total Budgeted sales Quantity-Break Even Sales Quantity.

Further, the importance of margin of safety has been described here-in-below

(a) It helps to analyse the management regarding the decline in sales of quantity which can

lead to break-even;

(b) It helps in decision making regarding expansion in sales;

(c) Higher Margin of Safety is indicative of chances of profitability being high;(Accounting

For Management, 2018)

Part 3 (B)

Compute the projected safety margin in sales dollars for the year 2018 and interpret what your

answer means to DIHL. 2 Mark

Answer 3(B)

Sl No Particular Shoe-

A Shoe-B Shoe-C Total

1 Budgeted Sales Volume 540000 630000 108000

0

225000

0

2 Per Unit Sales Price (1/7) 120 140 180

3 Variable Manufacturing Cost 360000 405000 660000 142500

0

4 Per Unit Variable manufacturing Cost

(3/7) 80 90 110

5 Variable Selling Cost 112500 90000 210000 412500

6 Per Unit Variable Selling Cost (5/7) 25 20 35

7 Budget Sales Quantity 4500 4500 6000 15000

8 Contribution (1-3-5) 67500 135000 210000 412500

9 Per Unit Contribution (8/7) 15 30 35

10 Sales Mix (4500:4500:6000) 3 3 4 10

11 Contribution under sales mix (9*10) 45 90 140 275

12 Fixed Cost

13 -Manufacturing Overheads 189500

14 -Selling Overheads 80000

15 Total Fixed Cost 269500

16 Break Even quantity (15/11)*10 9800

17 Number of pairs to be ordered 2940 2940 3920 9800

18 Margin of Safety Units (7-17) 1560 1560 2080 5200

19 Per Unit Sales Price (1/7) 120 140 180 440

20 Margin of Safety Sales(18*19) 187200 218400 374400 780000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

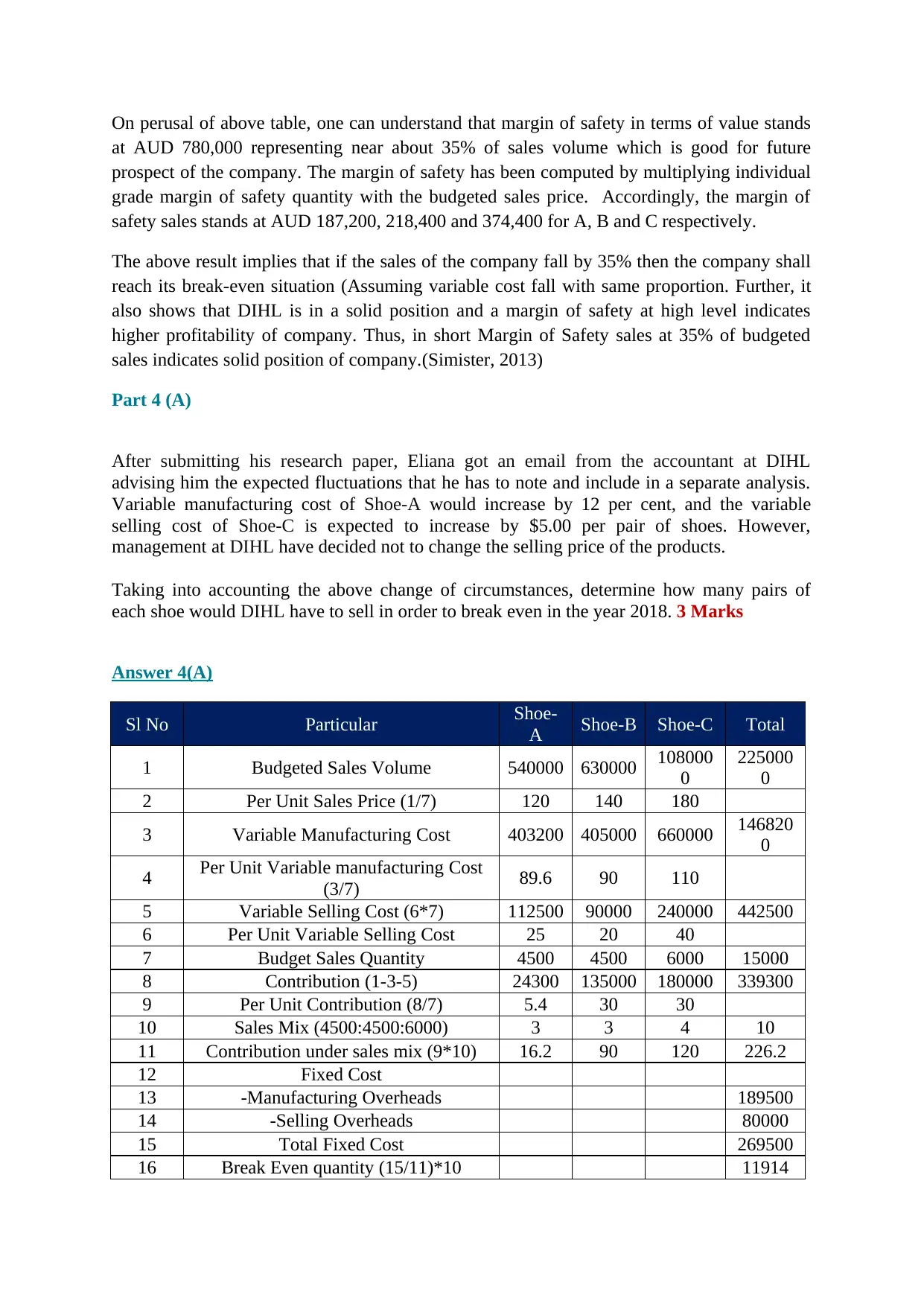

On perusal of above table, one can understand that margin of safety in terms of value stands

at AUD 780,000 representing near about 35% of sales volume which is good for future

prospect of the company. The margin of safety has been computed by multiplying individual

grade margin of safety quantity with the budgeted sales price. Accordingly, the margin of

safety sales stands at AUD 187,200, 218,400 and 374,400 for A, B and C respectively.

The above result implies that if the sales of the company fall by 35% then the company shall

reach its break-even situation (Assuming variable cost fall with same proportion. Further, it

also shows that DIHL is in a solid position and a margin of safety at high level indicates

higher profitability of company. Thus, in short Margin of Safety sales at 35% of budgeted

sales indicates solid position of company.(Simister, 2013)

Part 4 (A)

After submitting his research paper, Eliana got an email from the accountant at DIHL

advising him the expected fluctuations that he has to note and include in a separate analysis.

Variable manufacturing cost of Shoe-A would increase by 12 per cent, and the variable

selling cost of Shoe-C is expected to increase by $5.00 per pair of shoes. However,

management at DIHL have decided not to change the selling price of the products.

Taking into accounting the above change of circumstances, determine how many pairs of

each shoe would DIHL have to sell in order to break even in the year 2018. 3 Marks

Answer 4(A)

Sl No Particular Shoe-

A Shoe-B Shoe-C Total

1 Budgeted Sales Volume 540000 630000 108000

0

225000

0

2 Per Unit Sales Price (1/7) 120 140 180

3 Variable Manufacturing Cost 403200 405000 660000 146820

0

4 Per Unit Variable manufacturing Cost

(3/7) 89.6 90 110

5 Variable Selling Cost (6*7) 112500 90000 240000 442500

6 Per Unit Variable Selling Cost 25 20 40

7 Budget Sales Quantity 4500 4500 6000 15000

8 Contribution (1-3-5) 24300 135000 180000 339300

9 Per Unit Contribution (8/7) 5.4 30 30

10 Sales Mix (4500:4500:6000) 3 3 4 10

11 Contribution under sales mix (9*10) 16.2 90 120 226.2

12 Fixed Cost

13 -Manufacturing Overheads 189500

14 -Selling Overheads 80000

15 Total Fixed Cost 269500

16 Break Even quantity (15/11)*10 11914

at AUD 780,000 representing near about 35% of sales volume which is good for future

prospect of the company. The margin of safety has been computed by multiplying individual

grade margin of safety quantity with the budgeted sales price. Accordingly, the margin of

safety sales stands at AUD 187,200, 218,400 and 374,400 for A, B and C respectively.

The above result implies that if the sales of the company fall by 35% then the company shall

reach its break-even situation (Assuming variable cost fall with same proportion. Further, it

also shows that DIHL is in a solid position and a margin of safety at high level indicates

higher profitability of company. Thus, in short Margin of Safety sales at 35% of budgeted

sales indicates solid position of company.(Simister, 2013)

Part 4 (A)

After submitting his research paper, Eliana got an email from the accountant at DIHL

advising him the expected fluctuations that he has to note and include in a separate analysis.

Variable manufacturing cost of Shoe-A would increase by 12 per cent, and the variable

selling cost of Shoe-C is expected to increase by $5.00 per pair of shoes. However,

management at DIHL have decided not to change the selling price of the products.

Taking into accounting the above change of circumstances, determine how many pairs of

each shoe would DIHL have to sell in order to break even in the year 2018. 3 Marks

Answer 4(A)

Sl No Particular Shoe-

A Shoe-B Shoe-C Total

1 Budgeted Sales Volume 540000 630000 108000

0

225000

0

2 Per Unit Sales Price (1/7) 120 140 180

3 Variable Manufacturing Cost 403200 405000 660000 146820

0

4 Per Unit Variable manufacturing Cost

(3/7) 89.6 90 110

5 Variable Selling Cost (6*7) 112500 90000 240000 442500

6 Per Unit Variable Selling Cost 25 20 40

7 Budget Sales Quantity 4500 4500 6000 15000

8 Contribution (1-3-5) 24300 135000 180000 339300

9 Per Unit Contribution (8/7) 5.4 30 30

10 Sales Mix (4500:4500:6000) 3 3 4 10

11 Contribution under sales mix (9*10) 16.2 90 120 226.2

12 Fixed Cost

13 -Manufacturing Overheads 189500

14 -Selling Overheads 80000

15 Total Fixed Cost 269500

16 Break Even quantity (15/11)*10 11914

17 Number of pairs to be ordered 3576 3576 4768 11920

On the basis of details provided in the above stated question required alteration in the

projection has been made, thus, one can see that breakeven quantity of the company has

increased from 9800 units to 11914 units (11920 units to be in alignment with sales mix) on

account of change in contribution per unit for two grades of shoes. Further, the Contribution

on the basis of sales mix has also changed from 275 to 226.2 resulting in increase in break-

even quantity which is not good for the company.

Accordingly, the break-even quantity has been allocated over different grade of shoes on the

basis of sales mix. Thus, the break-even quantity for grade A, B and C stands at 3576, 3576

and 4768 units.

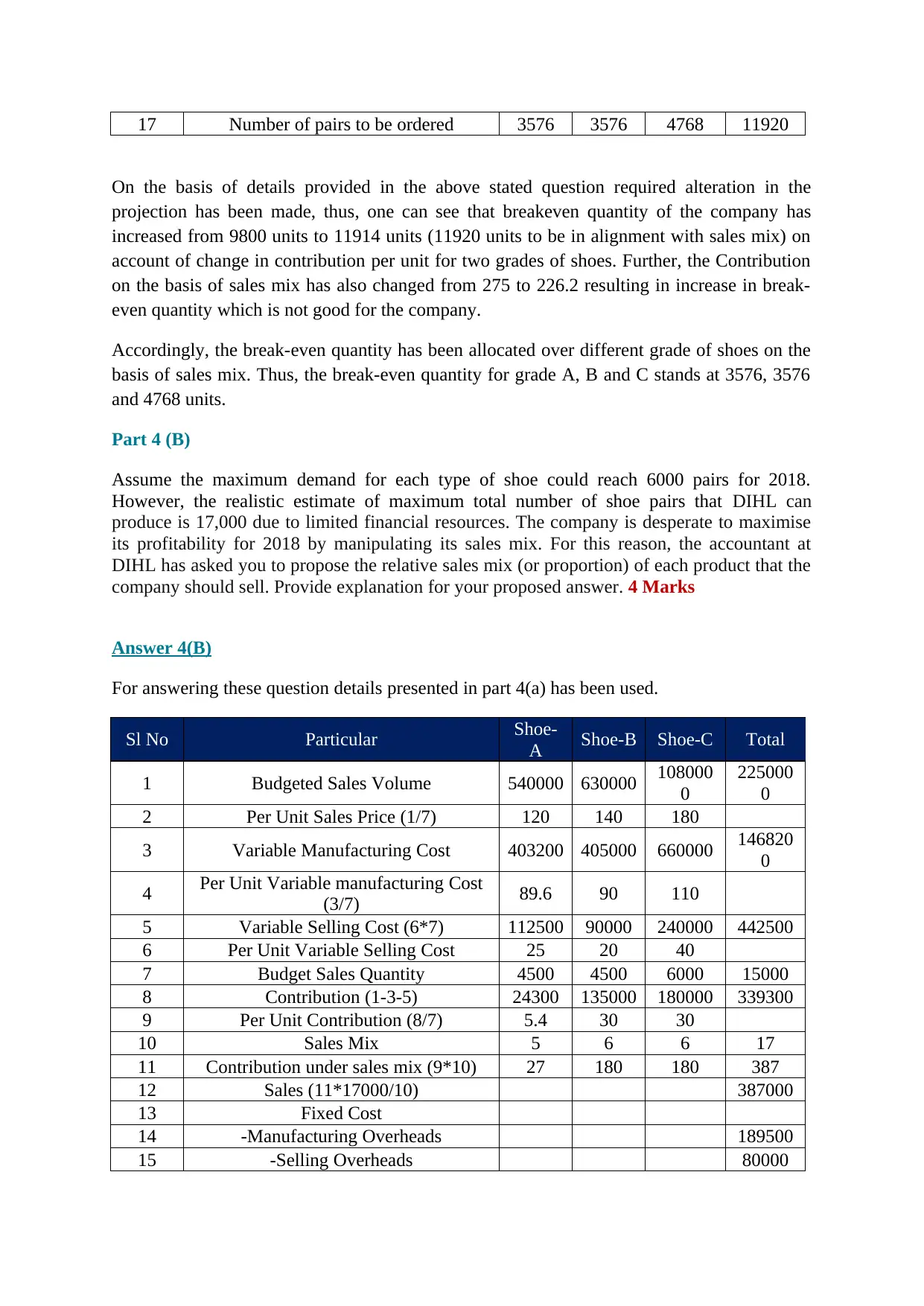

Part 4 (B)

Assume the maximum demand for each type of shoe could reach 6000 pairs for 2018.

However, the realistic estimate of maximum total number of shoe pairs that DIHL can

produce is 17,000 due to limited financial resources. The company is desperate to maximise

its profitability for 2018 by manipulating its sales mix. For this reason, the accountant at

DIHL has asked you to propose the relative sales mix (or proportion) of each product that the

company should sell. Provide explanation for your proposed answer. 4 Marks

Answer 4(B)

For answering these question details presented in part 4(a) has been used.

Sl No Particular Shoe-

A Shoe-B Shoe-C Total

1 Budgeted Sales Volume 540000 630000 108000

0

225000

0

2 Per Unit Sales Price (1/7) 120 140 180

3 Variable Manufacturing Cost 403200 405000 660000 146820

0

4 Per Unit Variable manufacturing Cost

(3/7) 89.6 90 110

5 Variable Selling Cost (6*7) 112500 90000 240000 442500

6 Per Unit Variable Selling Cost 25 20 40

7 Budget Sales Quantity 4500 4500 6000 15000

8 Contribution (1-3-5) 24300 135000 180000 339300

9 Per Unit Contribution (8/7) 5.4 30 30

10 Sales Mix 5 6 6 17

11 Contribution under sales mix (9*10) 27 180 180 387

12 Sales (11*17000/10) 387000

13 Fixed Cost

14 -Manufacturing Overheads 189500

15 -Selling Overheads 80000

On the basis of details provided in the above stated question required alteration in the

projection has been made, thus, one can see that breakeven quantity of the company has

increased from 9800 units to 11914 units (11920 units to be in alignment with sales mix) on

account of change in contribution per unit for two grades of shoes. Further, the Contribution

on the basis of sales mix has also changed from 275 to 226.2 resulting in increase in break-

even quantity which is not good for the company.

Accordingly, the break-even quantity has been allocated over different grade of shoes on the

basis of sales mix. Thus, the break-even quantity for grade A, B and C stands at 3576, 3576

and 4768 units.

Part 4 (B)

Assume the maximum demand for each type of shoe could reach 6000 pairs for 2018.

However, the realistic estimate of maximum total number of shoe pairs that DIHL can

produce is 17,000 due to limited financial resources. The company is desperate to maximise

its profitability for 2018 by manipulating its sales mix. For this reason, the accountant at

DIHL has asked you to propose the relative sales mix (or proportion) of each product that the

company should sell. Provide explanation for your proposed answer. 4 Marks

Answer 4(B)

For answering these question details presented in part 4(a) has been used.

Sl No Particular Shoe-

A Shoe-B Shoe-C Total

1 Budgeted Sales Volume 540000 630000 108000

0

225000

0

2 Per Unit Sales Price (1/7) 120 140 180

3 Variable Manufacturing Cost 403200 405000 660000 146820

0

4 Per Unit Variable manufacturing Cost

(3/7) 89.6 90 110

5 Variable Selling Cost (6*7) 112500 90000 240000 442500

6 Per Unit Variable Selling Cost 25 20 40

7 Budget Sales Quantity 4500 4500 6000 15000

8 Contribution (1-3-5) 24300 135000 180000 339300

9 Per Unit Contribution (8/7) 5.4 30 30

10 Sales Mix 5 6 6 17

11 Contribution under sales mix (9*10) 27 180 180 387

12 Sales (11*17000/10) 387000

13 Fixed Cost

14 -Manufacturing Overheads 189500

15 -Selling Overheads 80000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

16 Total Fixed Cost 269500

17 Profit (12-16) 117500

On perusal of the above table, one can understand that the sales mix has been chosen at 5:6:6

for shoes A, B and C respectively as the contribution is maximum under grade B and C.

Thus, more quantity of grade b and c shall be prepared compared to grade a. However, there

is a cap of 6000 units of each grade and overall manufacturing of 17000 Units. Thus, grade b

and c has been given preference. According, the sales stand at 5000, 6000 and 6000 for

grades A, B and C respectively.

Further, the maximum profit that can be attained under the current situation stands as AUD

117,500.(Ingram Digital Media, inc , 2018)

References:

Accounting For Management, 2018, Margin of safety, [Online]

Available at: https://www.accountingformanagement.org/margin-of-safety/

[Accessed 15 September 2018].

Anon., 2018, Margin of Safety, [Online]

Available at: https://www.myaccountingcourse.com/financial-ratios/margin-of-safety

[Accessed 15 September 2018].

Anon., n.d, Contribution Margin, [Online]

Available at: http://financeformulas.net/Contribution-Margin.html

[Accessed 15 September 2018].

Ingram Digital Media, inc , 2018, Product Mix and Constrained Resources, [Online]

Available at: https://accountinginfocus.com/managerial-accounting-2/short-term-decision-making/

product-mix-and-constrained-resources/

[Accessed 15 September 2018].

Simister, P., 2013, What Is The Margin Of Safety In Break Even Analysis And Why Is It Important?.

[Online]

Available at: http://businessdevelopmentadvice.com/blog/what-is-the-margin-of-safety-in-break-even-

analysis-and-why-is-it-important/

[Accessed 15 September 2018].

WebFinance Inc, 2018, breakeven formula, [Online]

Available at: http://www.businessdictionary.com/definition/breakeven-formula.html

[Accessed 15 September 2018].

17 Profit (12-16) 117500

On perusal of the above table, one can understand that the sales mix has been chosen at 5:6:6

for shoes A, B and C respectively as the contribution is maximum under grade B and C.

Thus, more quantity of grade b and c shall be prepared compared to grade a. However, there

is a cap of 6000 units of each grade and overall manufacturing of 17000 Units. Thus, grade b

and c has been given preference. According, the sales stand at 5000, 6000 and 6000 for

grades A, B and C respectively.

Further, the maximum profit that can be attained under the current situation stands as AUD

117,500.(Ingram Digital Media, inc , 2018)

References:

Accounting For Management, 2018, Margin of safety, [Online]

Available at: https://www.accountingformanagement.org/margin-of-safety/

[Accessed 15 September 2018].

Anon., 2018, Margin of Safety, [Online]

Available at: https://www.myaccountingcourse.com/financial-ratios/margin-of-safety

[Accessed 15 September 2018].

Anon., n.d, Contribution Margin, [Online]

Available at: http://financeformulas.net/Contribution-Margin.html

[Accessed 15 September 2018].

Ingram Digital Media, inc , 2018, Product Mix and Constrained Resources, [Online]

Available at: https://accountinginfocus.com/managerial-accounting-2/short-term-decision-making/

product-mix-and-constrained-resources/

[Accessed 15 September 2018].

Simister, P., 2013, What Is The Margin Of Safety In Break Even Analysis And Why Is It Important?.

[Online]

Available at: http://businessdevelopmentadvice.com/blog/what-is-the-margin-of-safety-in-break-even-

analysis-and-why-is-it-important/

[Accessed 15 September 2018].

WebFinance Inc, 2018, breakeven formula, [Online]

Available at: http://www.businessdictionary.com/definition/breakeven-formula.html

[Accessed 15 September 2018].

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.