Detailed Audit Strategy Report for ANZ Bank - BBAC601 Assurance

VerifiedAdded on 2023/06/12

|8

|1911

|154

Report

AI Summary

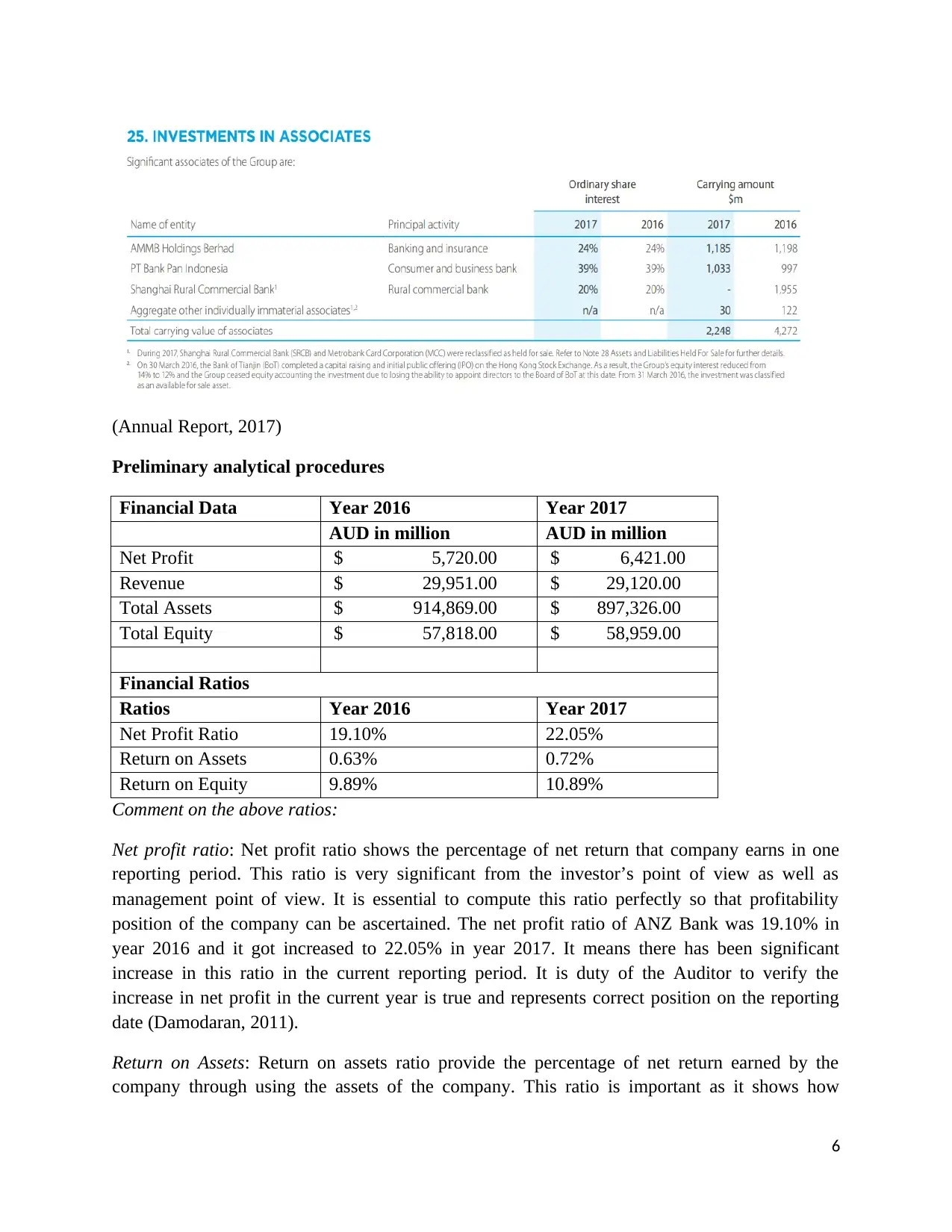

This report presents a comprehensive audit strategy for ANZ Bank, developed within the context of an Auditing & Assurance assignment (BBAC601). It begins by outlining the client's profile, including its establishment, operations, and the financial reporting period under consideration. The report details the external factors influencing the bank, such as economic conditions, laws, competition, and government support. It also examines the nature of the entity, its customers, suppliers, ownership structure, and accounting policies, highlighting changes in accounting standards and related-party disclosures. Preliminary analytical procedures are conducted, including an analysis of financial data and key ratios like net profit ratio, return on assets, and return on equity, providing insights into the bank's financial performance. The report concludes by discussing the bank's objectives, strategies, related business risks, and the measurement and review of its financial performance.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.