Detailed Report on Management Accounting for BCM Construction Ltd

VerifiedAdded on 2021/02/22

|16

|3541

|465

Report

AI Summary

This report provides a comprehensive overview of management accounting practices within BCM Construction Ltd, a UK-based construction company. It explores various management accounting systems, including inventory management, price optimization, cost accounting, and job costing, highlighting their applications and benefits. The report delves into different management accounting reporting techniques such as variance analysis, budgeting, performance reporting, activity-based costing, and standard costing, examining how BCM utilizes these methods for internal decision-making and performance evaluation. The analysis integrates management accounting systems with organizational processes and discusses the advantages of each system. Furthermore, the report covers the use of planning tools and forecasting budgets, offering insights into how management accounting supports financial problem-solving and contributes to sustainable success within the company. The report also includes detailed information on the techniques and methods used in management accounting reporting, providing a clear understanding of how BCM Construction Ltd. uses these techniques and tools to effectively manage its financial operations.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Different techniques and methods used for management accounting reporting:.........................3

Management accounting system and management accounting reporting is integrated within

organisational processes:.............................................................................................................5

Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs:...........................................................................................6

ACTIVITY 2....................................................................................................................................8

Use of planning tools used in management accounting...............................................................8

Uses of different planing tools in forecasting budget..................................................................9

CONCLUSION..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Different techniques and methods used for management accounting reporting:.........................3

Management accounting system and management accounting reporting is integrated within

organisational processes:.............................................................................................................5

Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs:...........................................................................................6

ACTIVITY 2....................................................................................................................................8

Use of planning tools used in management accounting...............................................................8

Uses of different planing tools in forecasting budget..................................................................9

CONCLUSION..............................................................................................................................11

INTRODUCTION

Management accounting system refers to organisation's internal system that assist in

measuring and evaluating various process for management of business organisation (Arnaboldi,

Lapsley and Steccolini, 2015). It provide relevant data or information that can be used by

managerial personnel to take effective decisions and to handle adverse situations. This report

covers management accounting and its various aspects, core requirement of various management

accounting system and their benefits, different methods of management accounting reporting,

use of planning tools and, advantages and disadvantages of different planning tools in the context

of BCM Construction Ltd. BCM is UK based medium sized construction company, contractor

related to infrastructure project in transport and rail sector. This report also cover comparison

about way in which organisation can use management accounting to respond to various financial

problems and explanation about how responding to financial problems, management accounting

can lead organisations to sustainable success.

ACTIVITY 1

Management accounting system is a process which combines key organisational activities such

as identification, collection, selecting and evaluating the accounting information and data for

assisting management to take strategic decisions and to analyse organisation's performance.

Under management accounting system, managerial personnels analyse and identifies events that

may happen in business organisation and around business organisation while considering

organisation's core needs and objectives. Main focus of management accounting system is to

provide a framework that can assist management to achieve organisation's goals and objectives in

efficient manner. In BCM construction Ltd, management accounting systems is used by

management to identify, choose, gather and analyse the information which ultimately help

organisation to frame strategies and develop action plans. There are some major management

accounting system like price optimisation system, inventory management system, job costing

system, cost accounting system etc. that are used by management to identify any particular

problem and assess the performance of organisation during a particular period. Following are the

significant management accounting system used by management of BCM, as follows:

Inventory management system: It is most commonly used management accounting system that

is used by business organisations to manage various inventories such as finished goods, raw

1

Management accounting system refers to organisation's internal system that assist in

measuring and evaluating various process for management of business organisation (Arnaboldi,

Lapsley and Steccolini, 2015). It provide relevant data or information that can be used by

managerial personnel to take effective decisions and to handle adverse situations. This report

covers management accounting and its various aspects, core requirement of various management

accounting system and their benefits, different methods of management accounting reporting,

use of planning tools and, advantages and disadvantages of different planning tools in the context

of BCM Construction Ltd. BCM is UK based medium sized construction company, contractor

related to infrastructure project in transport and rail sector. This report also cover comparison

about way in which organisation can use management accounting to respond to various financial

problems and explanation about how responding to financial problems, management accounting

can lead organisations to sustainable success.

ACTIVITY 1

Management accounting system is a process which combines key organisational activities such

as identification, collection, selecting and evaluating the accounting information and data for

assisting management to take strategic decisions and to analyse organisation's performance.

Under management accounting system, managerial personnels analyse and identifies events that

may happen in business organisation and around business organisation while considering

organisation's core needs and objectives. Main focus of management accounting system is to

provide a framework that can assist management to achieve organisation's goals and objectives in

efficient manner. In BCM construction Ltd, management accounting systems is used by

management to identify, choose, gather and analyse the information which ultimately help

organisation to frame strategies and develop action plans. There are some major management

accounting system like price optimisation system, inventory management system, job costing

system, cost accounting system etc. that are used by management to identify any particular

problem and assess the performance of organisation during a particular period. Following are the

significant management accounting system used by management of BCM, as follows:

Inventory management system: It is most commonly used management accounting system that

is used by business organisations to manage various inventories such as finished goods, raw

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

material, WIP, spare tools etc. This system provide assistance to accountants and management to

analyse the movement and flow of inventory within organisation which ensures proper

availability of inventories in organisation (Boiral, 2016). Various methods are adopted by

management to manage inventories like LIFO, FIFO and weighted average method. In BCM

construction Ltd this system is used to check the availability of raw construction material on

construction site and to avoid any storage or other inventory cost, which also assist company to

reduce any abnormal costs related to inventories.

Price optimisation system: Price optimisation system is a technical system used by

business organisation to asses how customer or consumer may respond at different – different

price levels for its various products and services. This system is applied by business organisation

to fix and determine the proper retail price of product. In BCM this system is applied by

management to minimise the contract price while maintaining their current profit margin. This

system help to gain competitive advantages to company. It also assist management in effective

utilisation of various resources of company.

Cost accounting system: It is most significant management accounting system which is

used by management to optimise the cost of product of its product and services. It help to assess

the excessive cost incurred by organisation. It also provide comparative analysis of various cost

which help to estimate or project future cost. It provides early identification of any event that

may be incur any additional cost. In BCM, this system is used to analyse the cost of construction

project and any escalation in cost of project. Company is using this system to asses the viability

of any new construction project. It is also used to evaluate the cost of construction project to

maximise project profit by reducing various unproductive costs.

Job costing system: This unique but important management accounting system, which is

used by, business organisations, wants to allocate various cost to different jobs and task. This

system is generally use by business organisations for internal analysis of costs by classifying

them as job or task to evaluate the viability of any particular job. Job order costing system is

apply to assign and accumulate various manufacturing and production costs of single unit of

output. In BCM, this system is use when various construction projects of company are different

from each other or are of different nature and each of them has significant costs. Company is

using this system to classify this significant cost as job to enhance accountability. Following are

some important information is which are necessary for job costing system, as follows:

2

analyse the movement and flow of inventory within organisation which ensures proper

availability of inventories in organisation (Boiral, 2016). Various methods are adopted by

management to manage inventories like LIFO, FIFO and weighted average method. In BCM

construction Ltd this system is used to check the availability of raw construction material on

construction site and to avoid any storage or other inventory cost, which also assist company to

reduce any abnormal costs related to inventories.

Price optimisation system: Price optimisation system is a technical system used by

business organisation to asses how customer or consumer may respond at different – different

price levels for its various products and services. This system is applied by business organisation

to fix and determine the proper retail price of product. In BCM this system is applied by

management to minimise the contract price while maintaining their current profit margin. This

system help to gain competitive advantages to company. It also assist management in effective

utilisation of various resources of company.

Cost accounting system: It is most significant management accounting system which is

used by management to optimise the cost of product of its product and services. It help to assess

the excessive cost incurred by organisation. It also provide comparative analysis of various cost

which help to estimate or project future cost. It provides early identification of any event that

may be incur any additional cost. In BCM, this system is used to analyse the cost of construction

project and any escalation in cost of project. Company is using this system to asses the viability

of any new construction project. It is also used to evaluate the cost of construction project to

maximise project profit by reducing various unproductive costs.

Job costing system: This unique but important management accounting system, which is

used by, business organisations, wants to allocate various cost to different jobs and task. This

system is generally use by business organisations for internal analysis of costs by classifying

them as job or task to evaluate the viability of any particular job. Job order costing system is

apply to assign and accumulate various manufacturing and production costs of single unit of

output. In BCM, this system is use when various construction projects of company are different

from each other or are of different nature and each of them has significant costs. Company is

using this system to classify this significant cost as job to enhance accountability. Following are

some important information is which are necessary for job costing system, as follows:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct martial: Under job, costing system information of direct material is required to

allocate or assign them to particular task or job. In BCM accountants and project managers

collects information of direct material and allocate them to particular task.

Direct Labour: Labour cost is use in job costing system, to classify labour cost incurred

on particular job or task. In BCM, labour engaged in particular project is classified and allocated

to calculate overall project cost (Booth, 2018).

Different techniques and methods used for management accounting reporting:

In management accounting system, reporting is done by lower level managers to top-

level management. Main purpose of reporting under management accounting system is to

provide a complete idea about management accounting process and its various aspects. Managers

in various formats do such reporting, as there is no specific format is prescribed. It is done as per

requirement of organisation. There are one or more techniques and methods to report matter or

facts under management accounting system. These methods are form as per different – different

requirements of business organisation. In small and medium sized enterprises like BCM,

reporting is effective manner for assessment of overall performance and to form new strategies

or action plans. In BCM, responsible managerial personnel’s through different reports and

methods of reporting communicates the significant matters or issues to higher-level management.

Then by using these reports management form strategies to achieve organisation's objectives and

evaluate whether there is modification required in existing strategy. Following are some major

techniques and methods applied by BCM for reporting, as follows:

Variance analysis: This type of management accounting reporting method is use to

analyse and evaluate the deviation of forecasted amounts or actual amounts to identify any weak

area in production and manufacturing process. This method is use to recognise or identify the

main reason of any difference or variation between actual and budgeted amount. A variance

reported in report may be favourable or unfavourable; an unfavourable or adverse variance is

required to be analyse critically. Focus of managers and accountants by reporting under this

method is to find out any under or over utilisation of company's resources. In BCM, variance for

various construction management to identify any adverse difference computes costs. If any

unfavourable variance identified then management take actions for reducing or eliminating such

variance. A quantity variance identified in construction project shows that company used

excessive input (Bromiley and et.al, 2015).

3

allocate or assign them to particular task or job. In BCM accountants and project managers

collects information of direct material and allocate them to particular task.

Direct Labour: Labour cost is use in job costing system, to classify labour cost incurred

on particular job or task. In BCM, labour engaged in particular project is classified and allocated

to calculate overall project cost (Booth, 2018).

Different techniques and methods used for management accounting reporting:

In management accounting system, reporting is done by lower level managers to top-

level management. Main purpose of reporting under management accounting system is to

provide a complete idea about management accounting process and its various aspects. Managers

in various formats do such reporting, as there is no specific format is prescribed. It is done as per

requirement of organisation. There are one or more techniques and methods to report matter or

facts under management accounting system. These methods are form as per different – different

requirements of business organisation. In small and medium sized enterprises like BCM,

reporting is effective manner for assessment of overall performance and to form new strategies

or action plans. In BCM, responsible managerial personnel’s through different reports and

methods of reporting communicates the significant matters or issues to higher-level management.

Then by using these reports management form strategies to achieve organisation's objectives and

evaluate whether there is modification required in existing strategy. Following are some major

techniques and methods applied by BCM for reporting, as follows:

Variance analysis: This type of management accounting reporting method is use to

analyse and evaluate the deviation of forecasted amounts or actual amounts to identify any weak

area in production and manufacturing process. This method is use to recognise or identify the

main reason of any difference or variation between actual and budgeted amount. A variance

reported in report may be favourable or unfavourable; an unfavourable or adverse variance is

required to be analyse critically. Focus of managers and accountants by reporting under this

method is to find out any under or over utilisation of company's resources. In BCM, variance for

various construction management to identify any adverse difference computes costs. If any

unfavourable variance identified then management take actions for reducing or eliminating such

variance. A quantity variance identified in construction project shows that company used

excessive input (Bromiley and et.al, 2015).

3

Budgeting: It is essential tool for business organisation to assess their present and future

performance, and to formulate strategies as per projection. Under this method of reporting,

managers forecast the income and expenses to calculate projected income or profit, which

provides a comparative analysis of present and future performance of business organisation.

Managers prepare actions plan to achieve such projected performance. In BCM, manager

prepares various budgets like cash budget, sales budgets, purchase budgets etc. to analyse the

overall present and future performance of company. Management take vital business decisions as

per outputs of different budgets.

Performance Report: Under this method of reporting overall organisations performance

as well as employee’s performance is analysed for a particular period. This report emphasises on

proper utilisation of human resources. It also used to optimise the aggregate employees costs. In

BCM, using this reporting technique performance of project managers, engineers, administration

employees etc. are awarded as per their commitment to company. In company, employee

engagement policies are framed as per performance report.

Activity based costing (ABC): In activity based costing, managers classifies and allot

various expenses or costs to different overhead activities and then assign them to various costs.

Using this reporting system, organisation can identify and analyse critically the relationship

between various costs, functions, overheads and products. Through analysis of this relationship,

indirect costs are allocated more effectively than traditional method. Although, it is complex to

allocate some expenses using this technique. Indirect costs for example staff salaries,

management costs etc. are difficult to allocate to a particular product. In BCM, this method is

used to allocate indirect cost related to particular construction project to analyse the relationship

of costs and overall project (Bryer, 2013).

Standard costing: Under this method of management accounting reporting a critical

comparison made between standard amount and actual amount of item related to organisation's

product or service. This system evaluated organisation efficiency to operate its functions as

compare to standards fixed as per previous performance of organisation. Reporting can be done

on monthly, quarterly or annually as per organisation's requirement. In BCM, project managers

determine the standards as per their experience, previous performance and industry trends. Then

after a particular period of time actual performance is compared with such standards to assess

their performance.

4

performance, and to formulate strategies as per projection. Under this method of reporting,

managers forecast the income and expenses to calculate projected income or profit, which

provides a comparative analysis of present and future performance of business organisation.

Managers prepare actions plan to achieve such projected performance. In BCM, manager

prepares various budgets like cash budget, sales budgets, purchase budgets etc. to analyse the

overall present and future performance of company. Management take vital business decisions as

per outputs of different budgets.

Performance Report: Under this method of reporting overall organisations performance

as well as employee’s performance is analysed for a particular period. This report emphasises on

proper utilisation of human resources. It also used to optimise the aggregate employees costs. In

BCM, using this reporting technique performance of project managers, engineers, administration

employees etc. are awarded as per their commitment to company. In company, employee

engagement policies are framed as per performance report.

Activity based costing (ABC): In activity based costing, managers classifies and allot

various expenses or costs to different overhead activities and then assign them to various costs.

Using this reporting system, organisation can identify and analyse critically the relationship

between various costs, functions, overheads and products. Through analysis of this relationship,

indirect costs are allocated more effectively than traditional method. Although, it is complex to

allocate some expenses using this technique. Indirect costs for example staff salaries,

management costs etc. are difficult to allocate to a particular product. In BCM, this method is

used to allocate indirect cost related to particular construction project to analyse the relationship

of costs and overall project (Bryer, 2013).

Standard costing: Under this method of management accounting reporting a critical

comparison made between standard amount and actual amount of item related to organisation's

product or service. This system evaluated organisation efficiency to operate its functions as

compare to standards fixed as per previous performance of organisation. Reporting can be done

on monthly, quarterly or annually as per organisation's requirement. In BCM, project managers

determine the standards as per their experience, previous performance and industry trends. Then

after a particular period of time actual performance is compared with such standards to assess

their performance.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

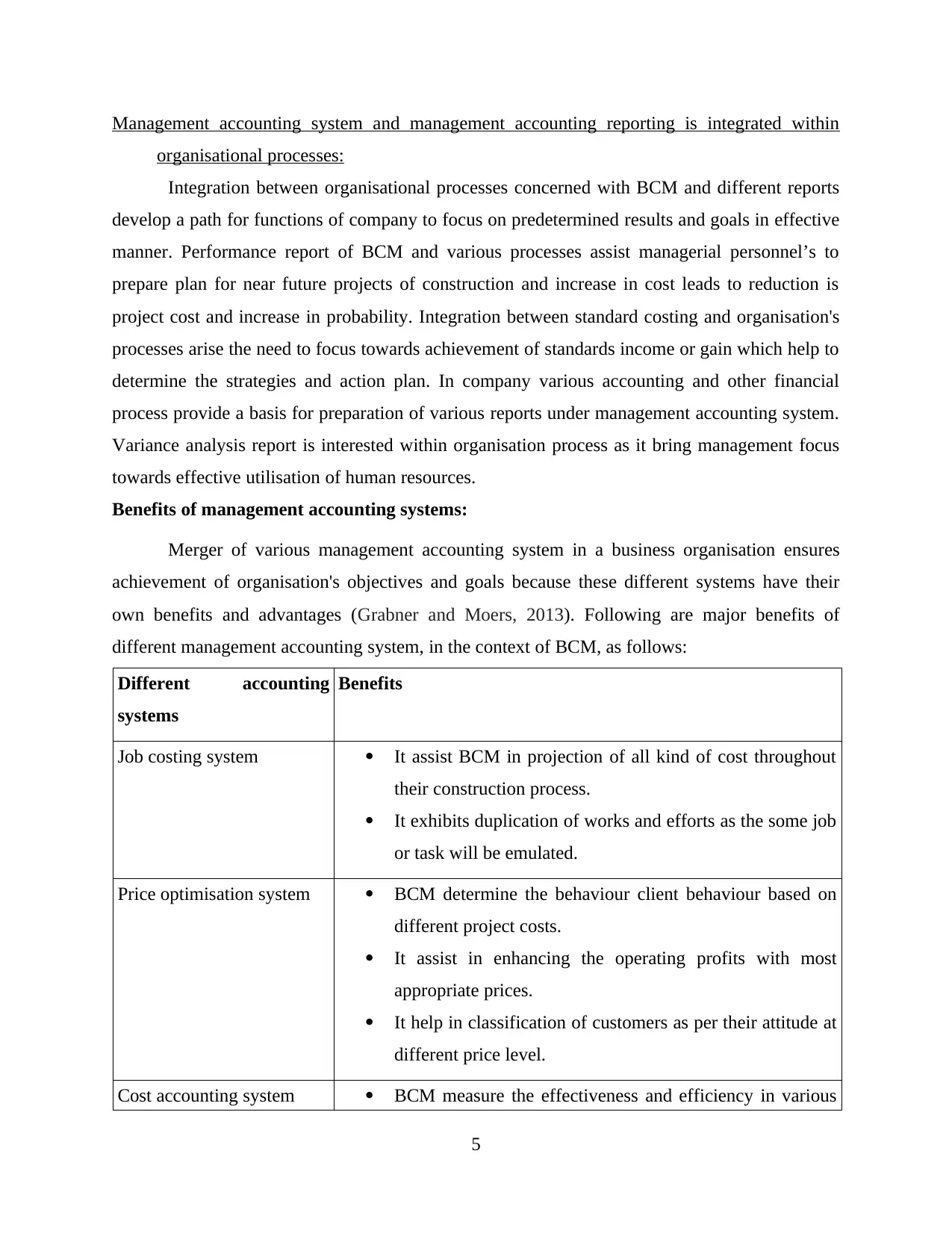

Management accounting system and management accounting reporting is integrated within

organisational processes:

Integration between organisational processes concerned with BCM and different reports

develop a path for functions of company to focus on predetermined results and goals in effective

manner. Performance report of BCM and various processes assist managerial personnel’s to

prepare plan for near future projects of construction and increase in cost leads to reduction is

project cost and increase in probability. Integration between standard costing and organisation's

processes arise the need to focus towards achievement of standards income or gain which help to

determine the strategies and action plan. In company various accounting and other financial

process provide a basis for preparation of various reports under management accounting system.

Variance analysis report is interested within organisation process as it bring management focus

towards effective utilisation of human resources.

Benefits of management accounting systems:

Merger of various management accounting system in a business organisation ensures

achievement of organisation's objectives and goals because these different systems have their

own benefits and advantages (Grabner and Moers, 2013). Following are major benefits of

different management accounting system, in the context of BCM, as follows:

Different accounting

systems

Benefits

Job costing system It assist BCM in projection of all kind of cost throughout

their construction process.

It exhibits duplication of works and efforts as the some job

or task will be emulated.

Price optimisation system BCM determine the behaviour client behaviour based on

different project costs.

It assist in enhancing the operating profits with most

appropriate prices.

It help in classification of customers as per their attitude at

different price level.

Cost accounting system BCM measure the effectiveness and efficiency in various

5

organisational processes:

Integration between organisational processes concerned with BCM and different reports

develop a path for functions of company to focus on predetermined results and goals in effective

manner. Performance report of BCM and various processes assist managerial personnel’s to

prepare plan for near future projects of construction and increase in cost leads to reduction is

project cost and increase in probability. Integration between standard costing and organisation's

processes arise the need to focus towards achievement of standards income or gain which help to

determine the strategies and action plan. In company various accounting and other financial

process provide a basis for preparation of various reports under management accounting system.

Variance analysis report is interested within organisation process as it bring management focus

towards effective utilisation of human resources.

Benefits of management accounting systems:

Merger of various management accounting system in a business organisation ensures

achievement of organisation's objectives and goals because these different systems have their

own benefits and advantages (Grabner and Moers, 2013). Following are major benefits of

different management accounting system, in the context of BCM, as follows:

Different accounting

systems

Benefits

Job costing system It assist BCM in projection of all kind of cost throughout

their construction process.

It exhibits duplication of works and efforts as the some job

or task will be emulated.

Price optimisation system BCM determine the behaviour client behaviour based on

different project costs.

It assist in enhancing the operating profits with most

appropriate prices.

It help in classification of customers as per their attitude at

different price level.

Cost accounting system BCM measure the effectiveness and efficiency in various

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

construction processes and then help in improving by

using this system.

It assist company to determine the cost of projects and

reduction of prices.

It provide essential information for planning process.

Inventory Management

System

It help BCM to increase the accuracy inventory orders.

It improve the effectiveness and efficiency and assist in

saving money and time.

It reduce the additional inventory costs that may occur due

to mismanagement of inventories.

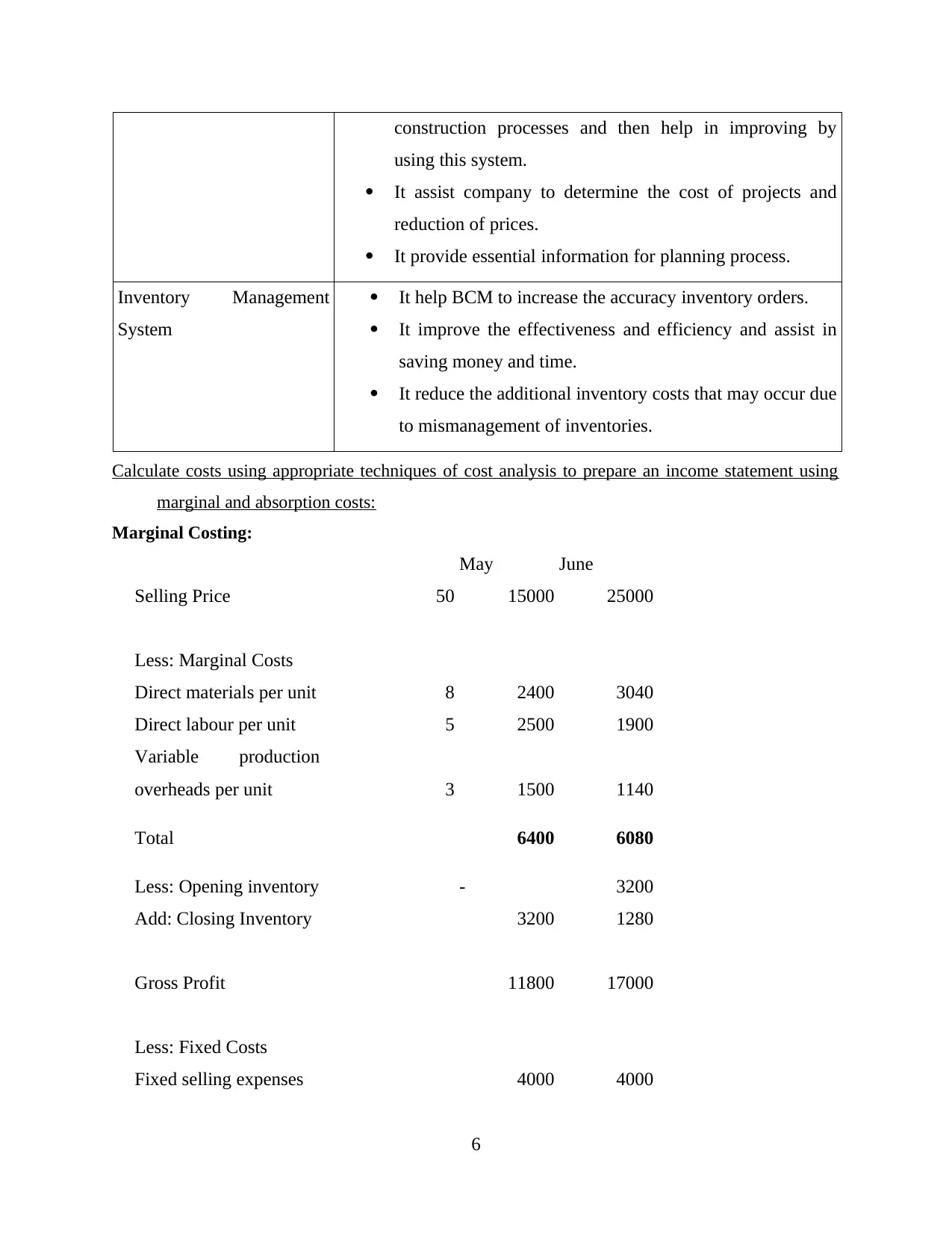

Calculate costs using appropriate techniques of cost analysis to prepare an income statement using

marginal and absorption costs:

Marginal Costing:

May June

Selling Price 50 15000 25000

Less: Marginal Costs

Direct materials per unit 8 2400 3040

Direct labour per unit 5 2500 1900

Variable production

overheads per unit 3 1500 1140

Total 6400 6080

Less: Opening inventory - 3200

Add: Closing Inventory 3200 1280

Gross Profit 11800 17000

Less: Fixed Costs

Fixed selling expenses 4000 4000

6

using this system.

It assist company to determine the cost of projects and

reduction of prices.

It provide essential information for planning process.

Inventory Management

System

It help BCM to increase the accuracy inventory orders.

It improve the effectiveness and efficiency and assist in

saving money and time.

It reduce the additional inventory costs that may occur due

to mismanagement of inventories.

Calculate costs using appropriate techniques of cost analysis to prepare an income statement using

marginal and absorption costs:

Marginal Costing:

May June

Selling Price 50 15000 25000

Less: Marginal Costs

Direct materials per unit 8 2400 3040

Direct labour per unit 5 2500 1900

Variable production

overheads per unit 3 1500 1140

Total 6400 6080

Less: Opening inventory - 3200

Add: Closing Inventory 3200 1280

Gross Profit 11800 17000

Less: Fixed Costs

Fixed selling expenses 4000 4000

6

Fixed admin expenses 2000 2000

Fixed Production cost 4000 4000

Less: Sales commission 750 1250

Net Profit 1050 5750

Absorption Costing:

May June

Selling Price 50 15000 25000

Less: Absorption Costs

Direct materials per unit 8 4000 3040

Direct labour per unit 5 2500 1900

Variable production

overheads per unit 3 1500 1140

Fixed Production cost 10 3000 3800

Total 11000 9880

Less: Opening inventory - 5200

Add: Closing Inventory 5200 2080

Gross Profit 9200 17200

Less: Fixed Costs

Fixed selling expenses 4000 4000

Fixed admin expenses 2000 2000

Less: Sales commission 750 1250

Net Profit -550 6150

7

Fixed Production cost 4000 4000

Less: Sales commission 750 1250

Net Profit 1050 5750

Absorption Costing:

May June

Selling Price 50 15000 25000

Less: Absorption Costs

Direct materials per unit 8 4000 3040

Direct labour per unit 5 2500 1900

Variable production

overheads per unit 3 1500 1140

Fixed Production cost 10 3000 3800

Total 11000 9880

Less: Opening inventory - 5200

Add: Closing Inventory 5200 2080

Gross Profit 9200 17200

Less: Fixed Costs

Fixed selling expenses 4000 4000

Fixed admin expenses 2000 2000

Less: Sales commission 750 1250

Net Profit -550 6150

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

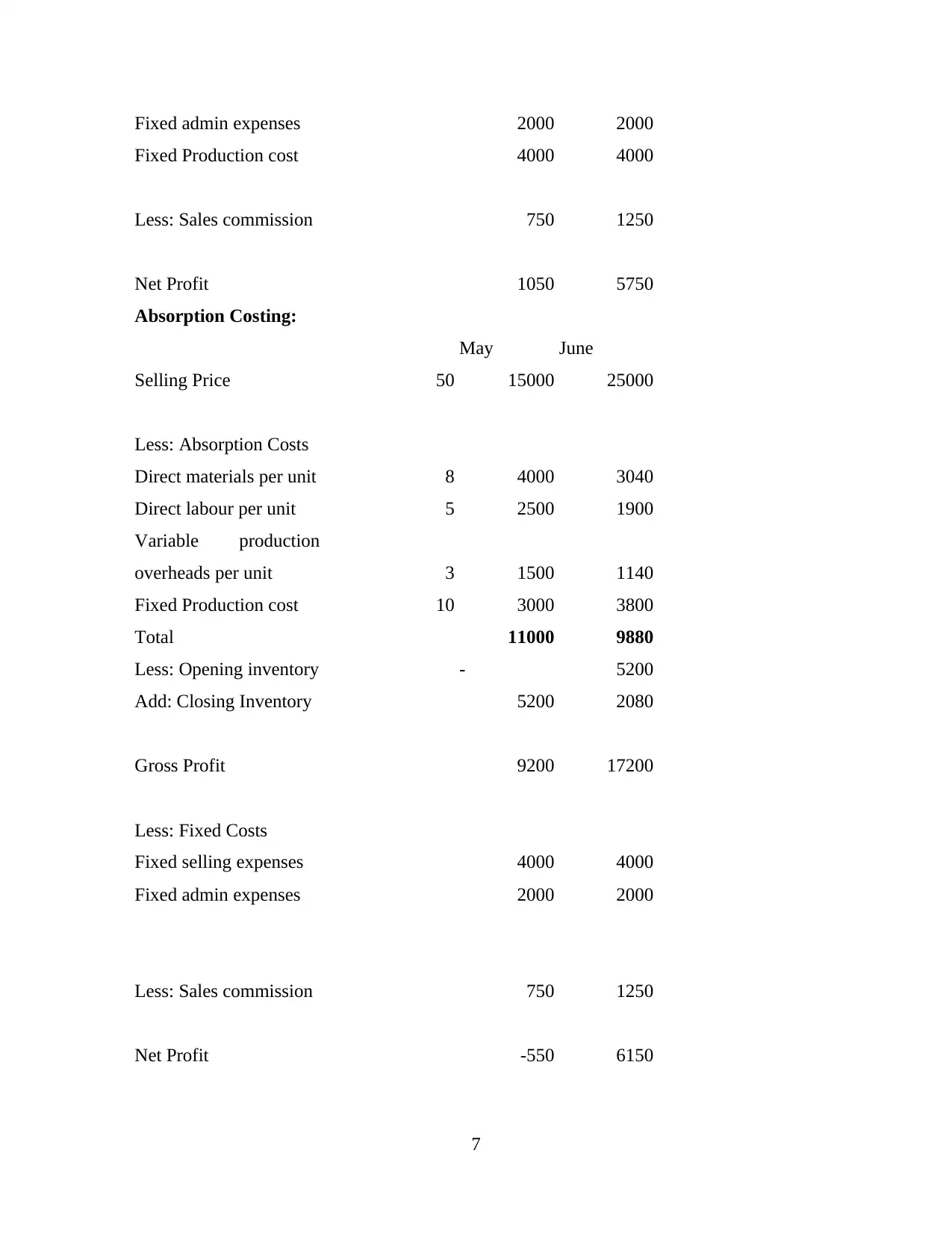

Budgeted and actual cost of metal used in

producing Product A

Budgeted material cost

per unit of the product 2kg at £10/kg

Actual output 1000 units

Actual material

purchased and used 2200kg

Actual material cost £20,900

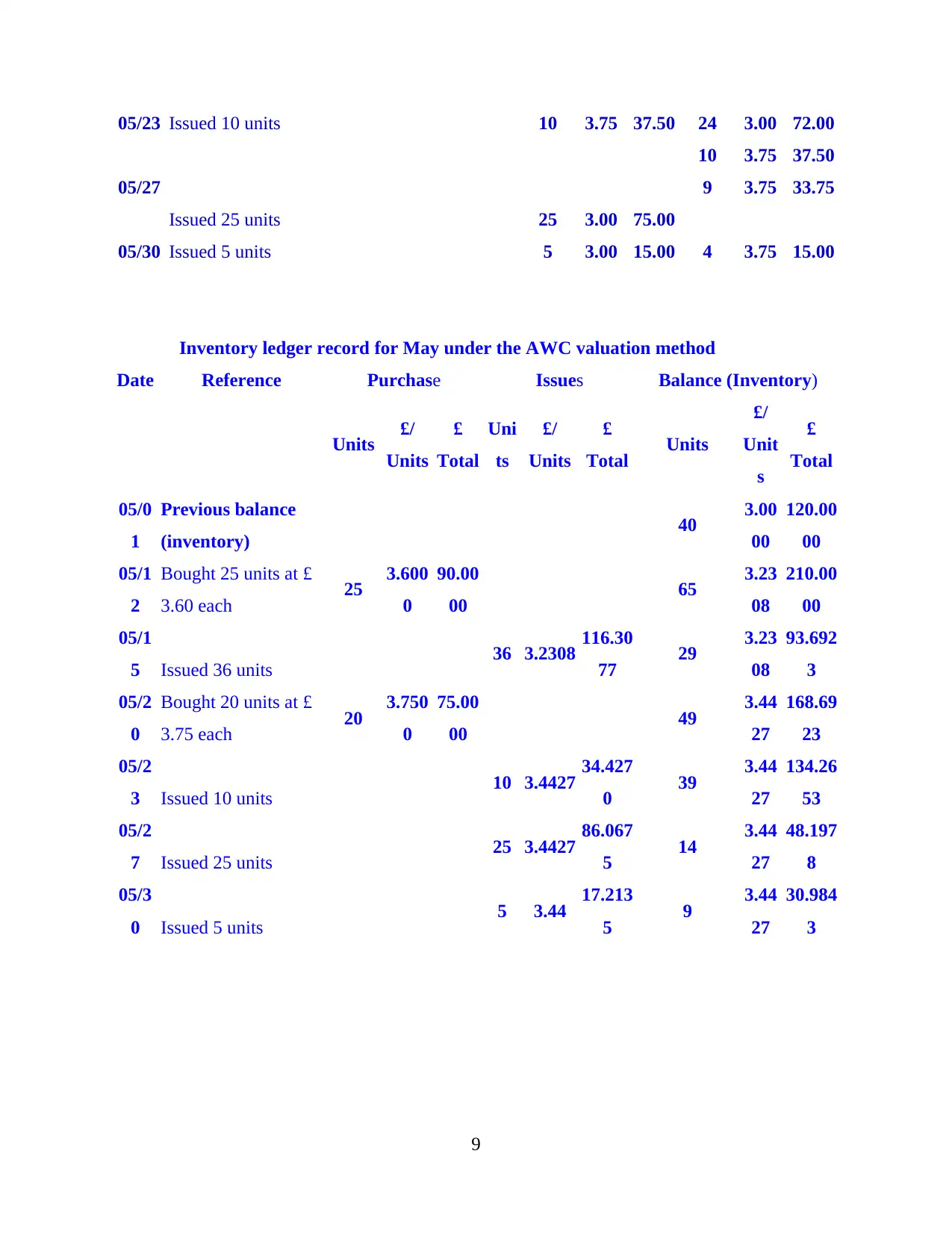

Inventory ledger record for May under the LIFO valuation method

Date Reference Purchase Issues Balance

(Inventory)

Units £/

Units

£

Total Units £/

Units

£

Total Units £/

Units

£

Total

05/01 Previous balance

(inventory) 40 3.00 120.0

0

05/12 40 3.00 120.0

0

Bought 25 units at £ 3.60

each 20 3.60 72.00 20 3.60 72.00

05/15 20 3.60 72.00

Issued 36 units 16 3.00 48.00 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20 units at £ 3.75

each 20 3.75 75.00 20 3.75 75.00

8

producing Product A

Budgeted material cost

per unit of the product 2kg at £10/kg

Actual output 1000 units

Actual material

purchased and used 2200kg

Actual material cost £20,900

Inventory ledger record for May under the LIFO valuation method

Date Reference Purchase Issues Balance

(Inventory)

Units £/

Units

£

Total Units £/

Units

£

Total Units £/

Units

£

Total

05/01 Previous balance

(inventory) 40 3.00 120.0

0

05/12 40 3.00 120.0

0

Bought 25 units at £ 3.60

each 20 3.60 72.00 20 3.60 72.00

05/15 20 3.60 72.00

Issued 36 units 16 3.00 48.00 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20 units at £ 3.75

each 20 3.75 75.00 20 3.75 75.00

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

05/23 Issued 10 units 10 3.75 37.50 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

Issued 25 units 25 3.00 75.00

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

Inventory ledger record for May under the AWC valuation method

Date Reference Purchase Issues Balance (Inventory)

Units £/

Units

£

Total

Uni

ts

£/

Units

£

Total Units

£/

Unit

s

£

Total

05/0

1

Previous balance

(inventory) 40 3.00

00

120.00

00

05/1

2

Bought 25 units at £

3.60 each 25 3.600

0

90.00

00 65 3.23

08

210.00

00

05/1

5 Issued 36 units 36 3.2308 116.30

77 29 3.23

08

93.692

3

05/2

0

Bought 20 units at £

3.75 each 20 3.750

0

75.00

00 49 3.44

27

168.69

23

05/2

3 Issued 10 units 10 3.4427 34.427

0 39 3.44

27

134.26

53

05/2

7 Issued 25 units 25 3.4427 86.067

5 14 3.44

27

48.197

8

05/3

0 Issued 5 units 5 3.44 17.213

5 9 3.44

27

30.984

3

9

10 3.75 37.50

05/27 9 3.75 33.75

Issued 25 units 25 3.00 75.00

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

Inventory ledger record for May under the AWC valuation method

Date Reference Purchase Issues Balance (Inventory)

Units £/

Units

£

Total

Uni

ts

£/

Units

£

Total Units

£/

Unit

s

£

Total

05/0

1

Previous balance

(inventory) 40 3.00

00

120.00

00

05/1

2

Bought 25 units at £

3.60 each 25 3.600

0

90.00

00 65 3.23

08

210.00

00

05/1

5 Issued 36 units 36 3.2308 116.30

77 29 3.23

08

93.692

3

05/2

0

Bought 20 units at £

3.75 each 20 3.750

0

75.00

00 49 3.44

27

168.69

23

05/2

3 Issued 10 units 10 3.4427 34.427

0 39 3.44

27

134.26

53

05/2

7 Issued 25 units 25 3.4427 86.067

5 14 3.44

27

48.197

8

05/3

0 Issued 5 units 5 3.44 17.213

5 9 3.44

27

30.984

3

9

ACTIVITY 2

Use of planning tools used in management accounting

BUDGET: It refers to projection and forecasting of various costs or expenses, incomes

and resources during a specified period of time and generally complied and re analysed on

periodic basis. It is used by business organisations as internal tool and used to develop new

strategies and plans. Budget is business statements that combines estimation of various costs,

income or revenues that exhibits organisation's performance in near future. It is used by

management to formulate and develop strategies to achieve the budgeted performance within

specified time. It also point out towards the need of amendment in strategies and action plan in

order to achieve organisation's objectives and goals. In BCM, accountants and managers prepare

budgets and then top management use these budgets to develop strategies and action plan while

considering short term and long-term objectives of company. In company, cash budget is used to

analyse the movement and availability of cash to avoid any difficulties in near future. Budget is

tool of budgetary control through which organisation can control their various budgets to ensure

profitability. Budgetary control is a regular process performed by managers to assess the

performance and set financial plans though various budgets (Granlund and Lukka, 2017).

Following are key advantages and disadvantages of various planning tools applied in budgetary

control, as follows:

Cash Budget

It is most considerable planning tool that mainly includes forecasting and estimation of

cash inflow and outflow within an enterprise in respect of a particular period. This budget

specifically used to measure the availability of cash in an organisation to operate. In BCM, first

cash is allotted for each of its construction project than cash budget is prepared by budget to

ensure that enough cash is available to perform various activities. It point out towards need of

cash for particular function or activity. A detailed cash budget help to identify any theft or loss of

cash in organisation.

Advantages: In BCM, this method is used to track the movement of cash at online and

real time basis, help to maintain liquidity position within company.

Disadvantages: Accountants to manipulate or hide the actual performance or company

can use some time cash budget.

Operating Budget

10

Use of planning tools used in management accounting

BUDGET: It refers to projection and forecasting of various costs or expenses, incomes

and resources during a specified period of time and generally complied and re analysed on

periodic basis. It is used by business organisations as internal tool and used to develop new

strategies and plans. Budget is business statements that combines estimation of various costs,

income or revenues that exhibits organisation's performance in near future. It is used by

management to formulate and develop strategies to achieve the budgeted performance within

specified time. It also point out towards the need of amendment in strategies and action plan in

order to achieve organisation's objectives and goals. In BCM, accountants and managers prepare

budgets and then top management use these budgets to develop strategies and action plan while

considering short term and long-term objectives of company. In company, cash budget is used to

analyse the movement and availability of cash to avoid any difficulties in near future. Budget is

tool of budgetary control through which organisation can control their various budgets to ensure

profitability. Budgetary control is a regular process performed by managers to assess the

performance and set financial plans though various budgets (Granlund and Lukka, 2017).

Following are key advantages and disadvantages of various planning tools applied in budgetary

control, as follows:

Cash Budget

It is most considerable planning tool that mainly includes forecasting and estimation of

cash inflow and outflow within an enterprise in respect of a particular period. This budget

specifically used to measure the availability of cash in an organisation to operate. In BCM, first

cash is allotted for each of its construction project than cash budget is prepared by budget to

ensure that enough cash is available to perform various activities. It point out towards need of

cash for particular function or activity. A detailed cash budget help to identify any theft or loss of

cash in organisation.

Advantages: In BCM, this method is used to track the movement of cash at online and

real time basis, help to maintain liquidity position within company.

Disadvantages: Accountants to manipulate or hide the actual performance or company

can use some time cash budget.

Operating Budget

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.