BEA602 Finance Assignment 1: Options Strategies, Pricing, and Models

VerifiedAdded on 2022/12/27

|13

|1965

|90

Homework Assignment

AI Summary

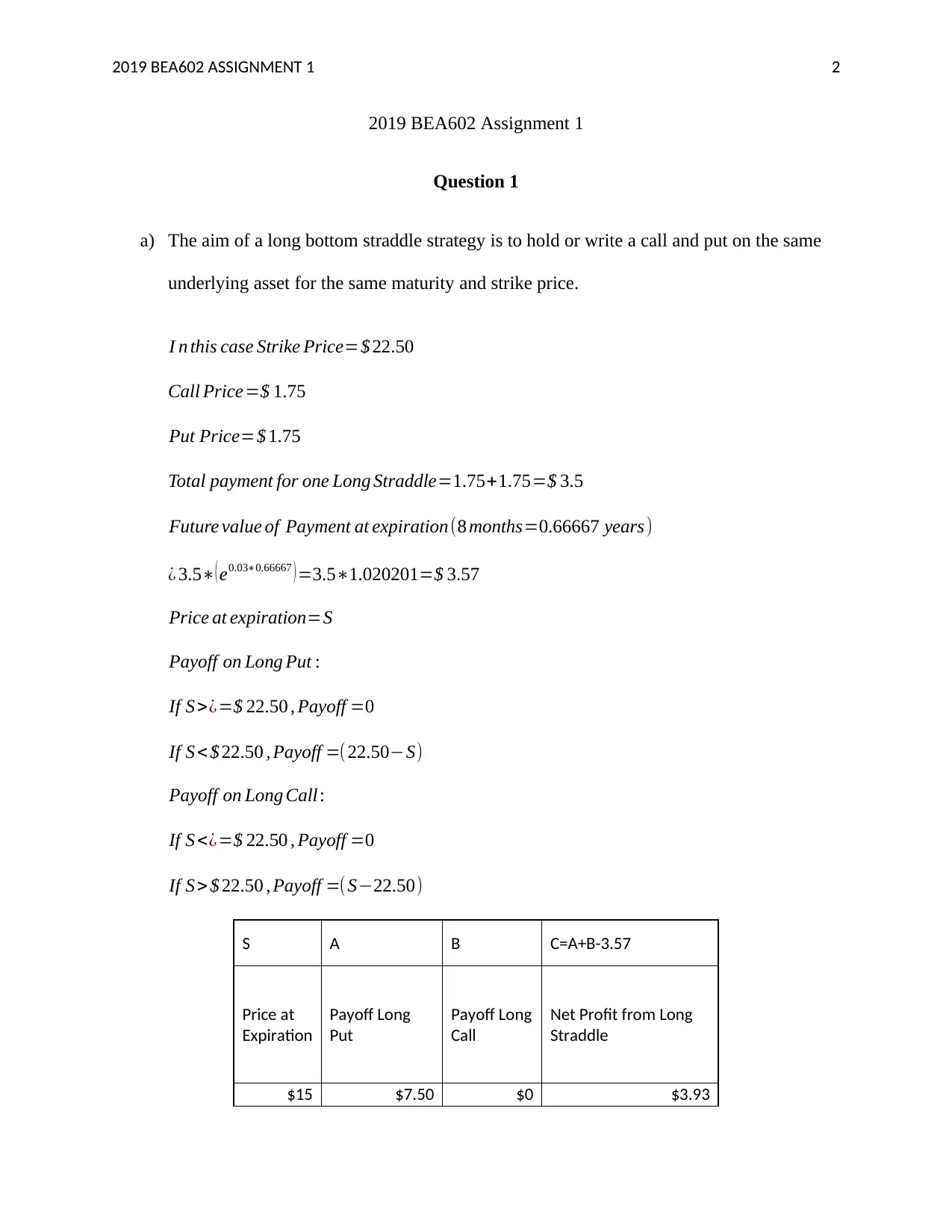

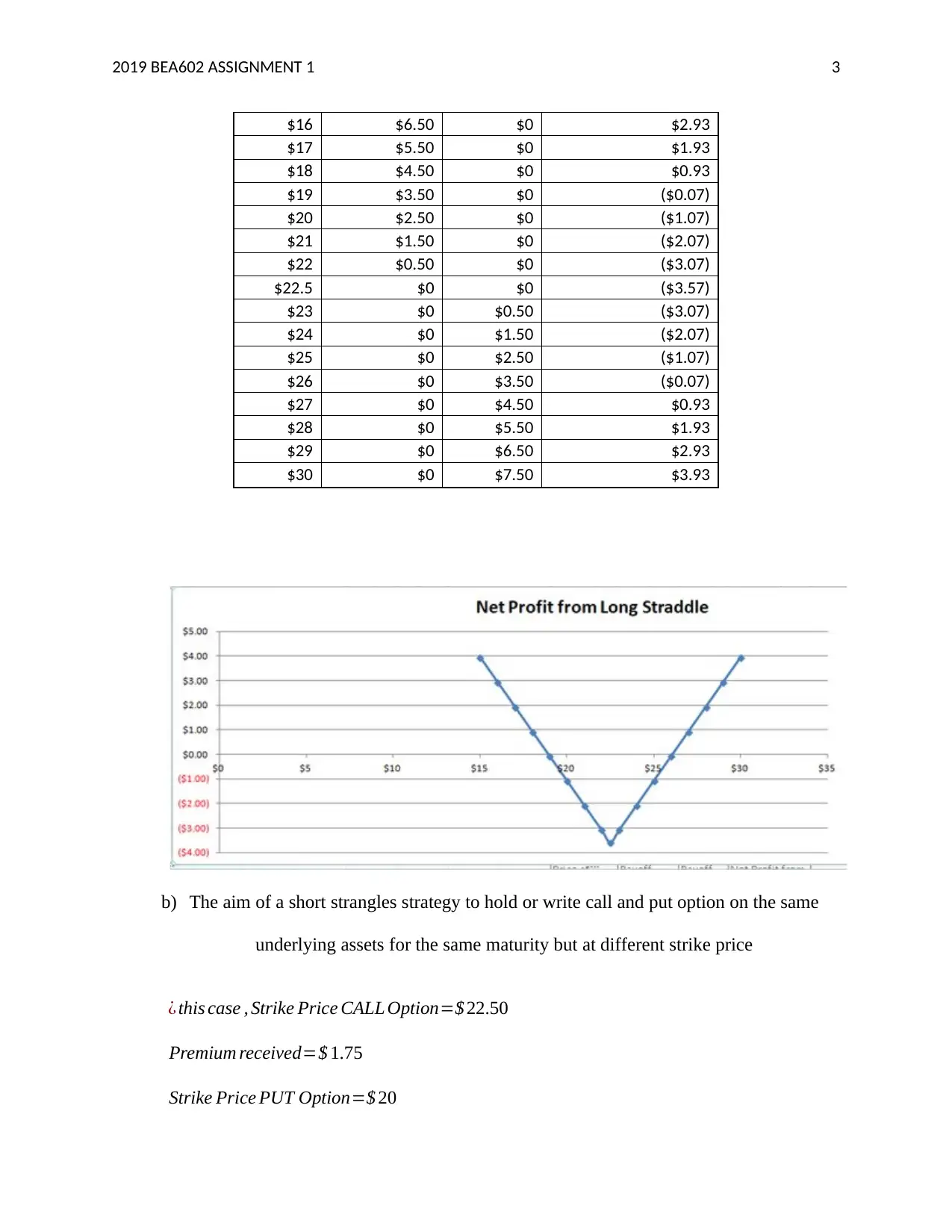

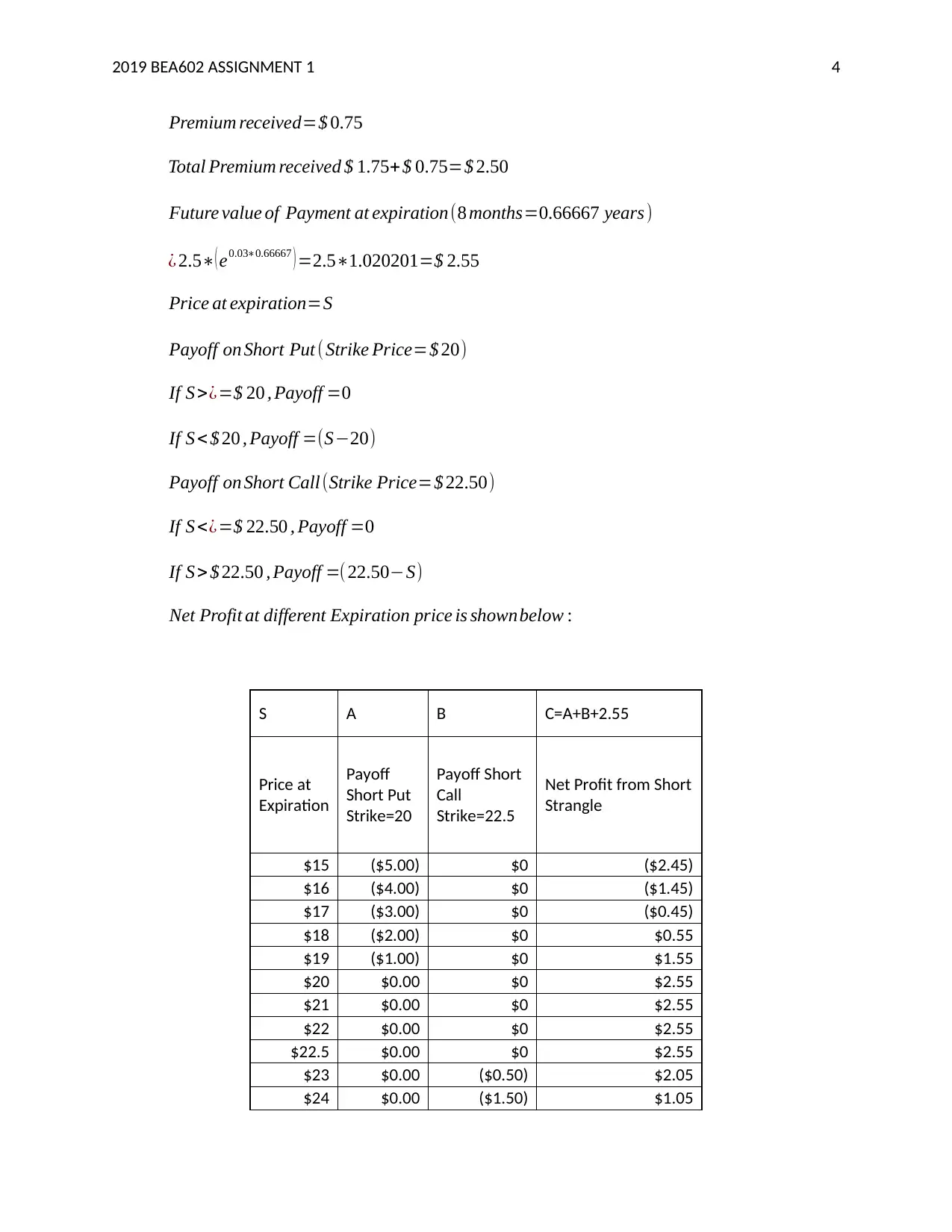

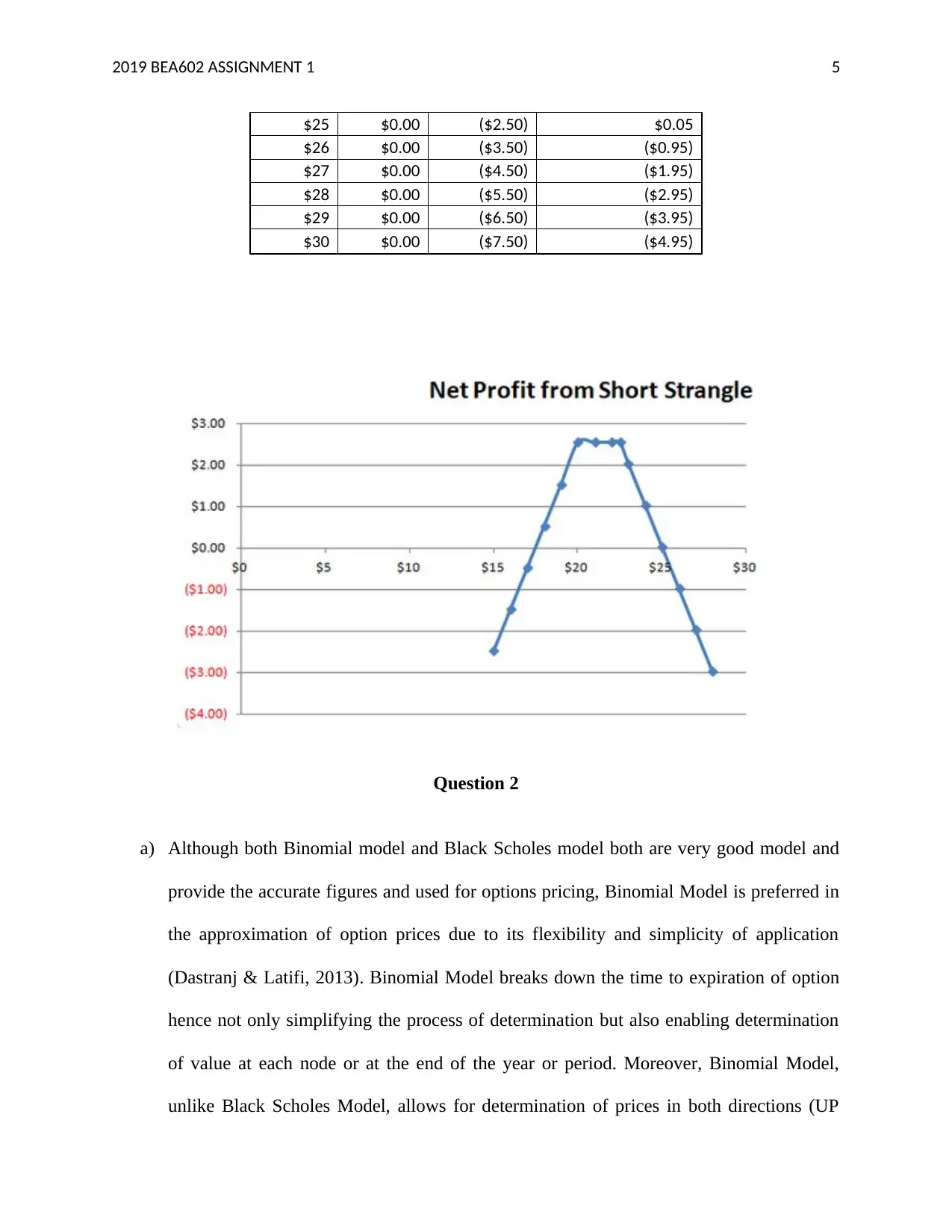

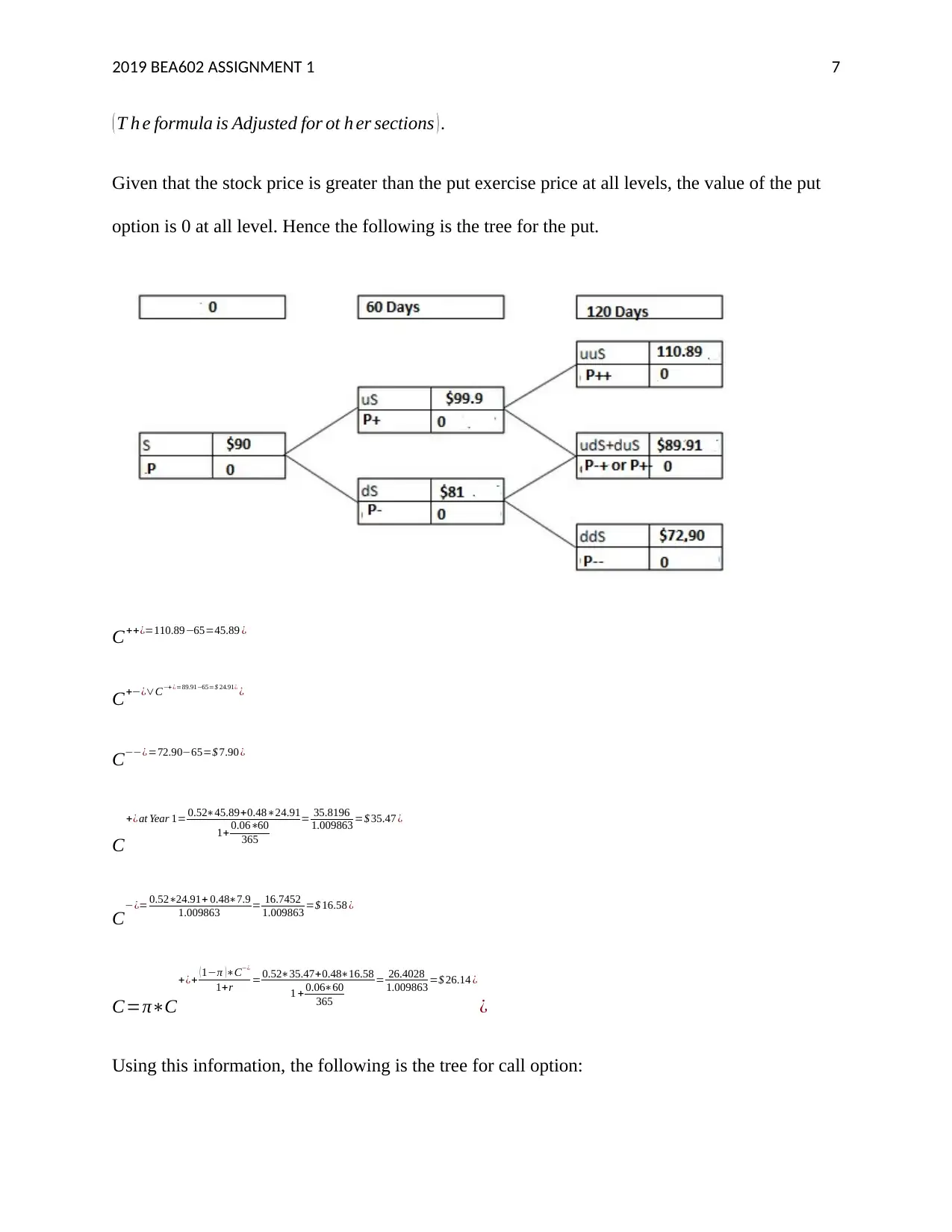

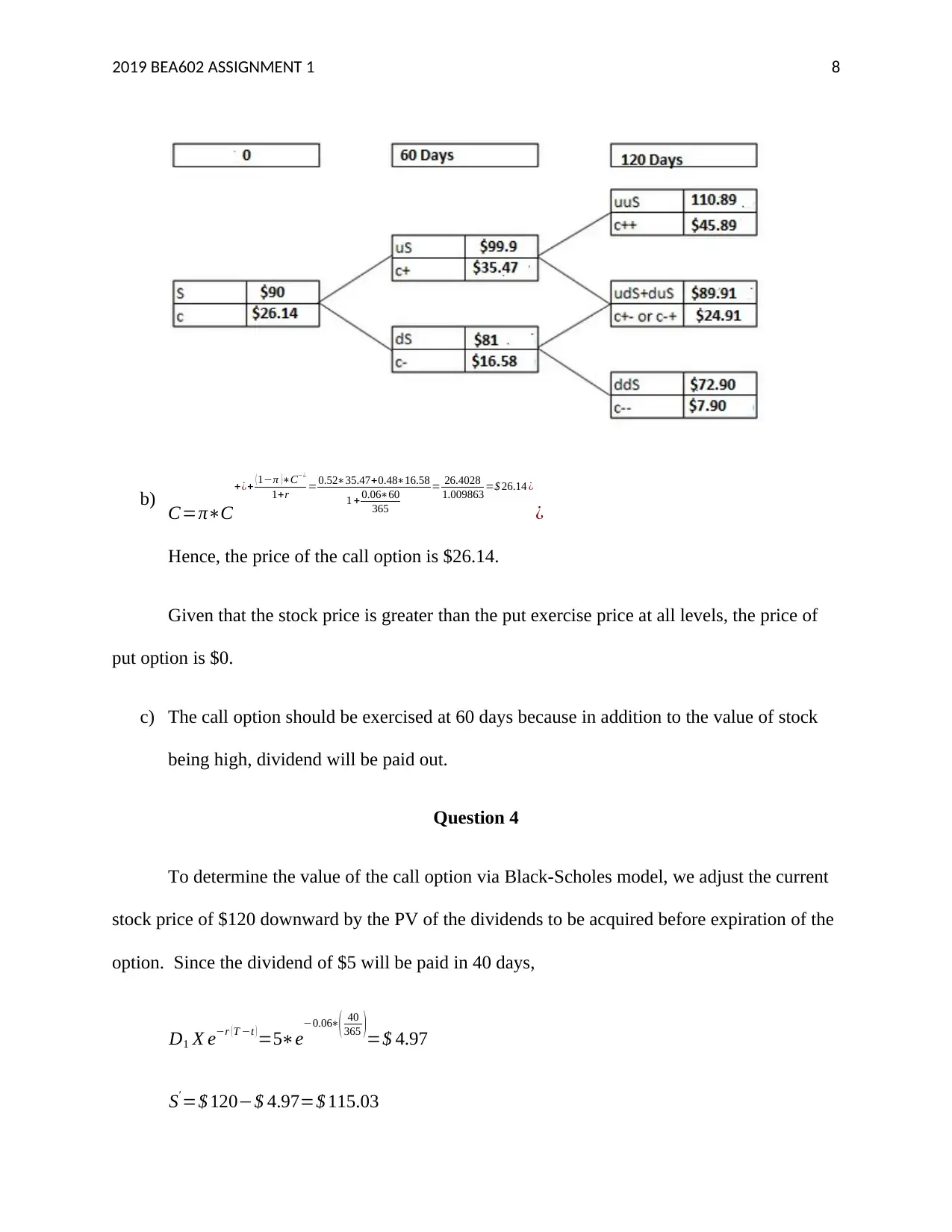

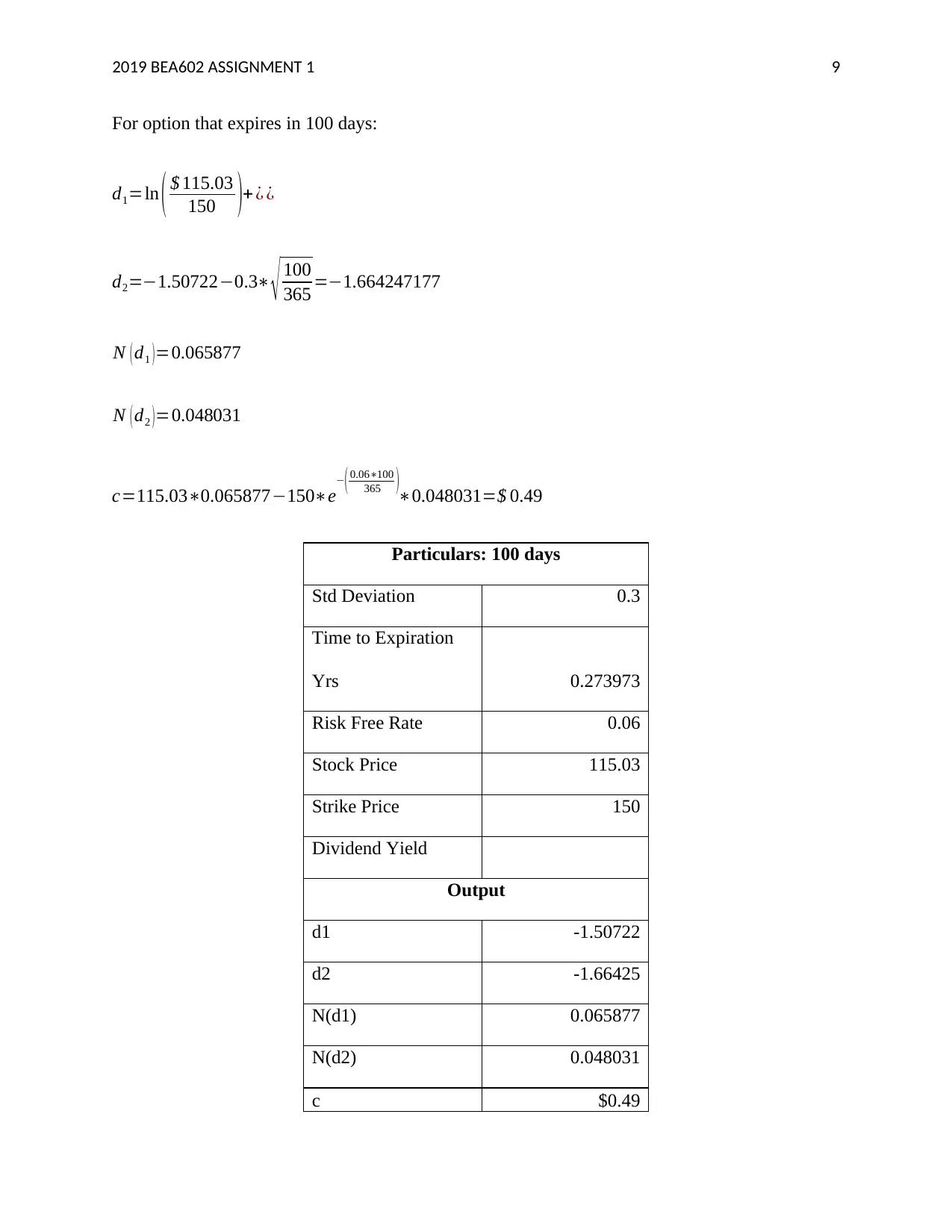

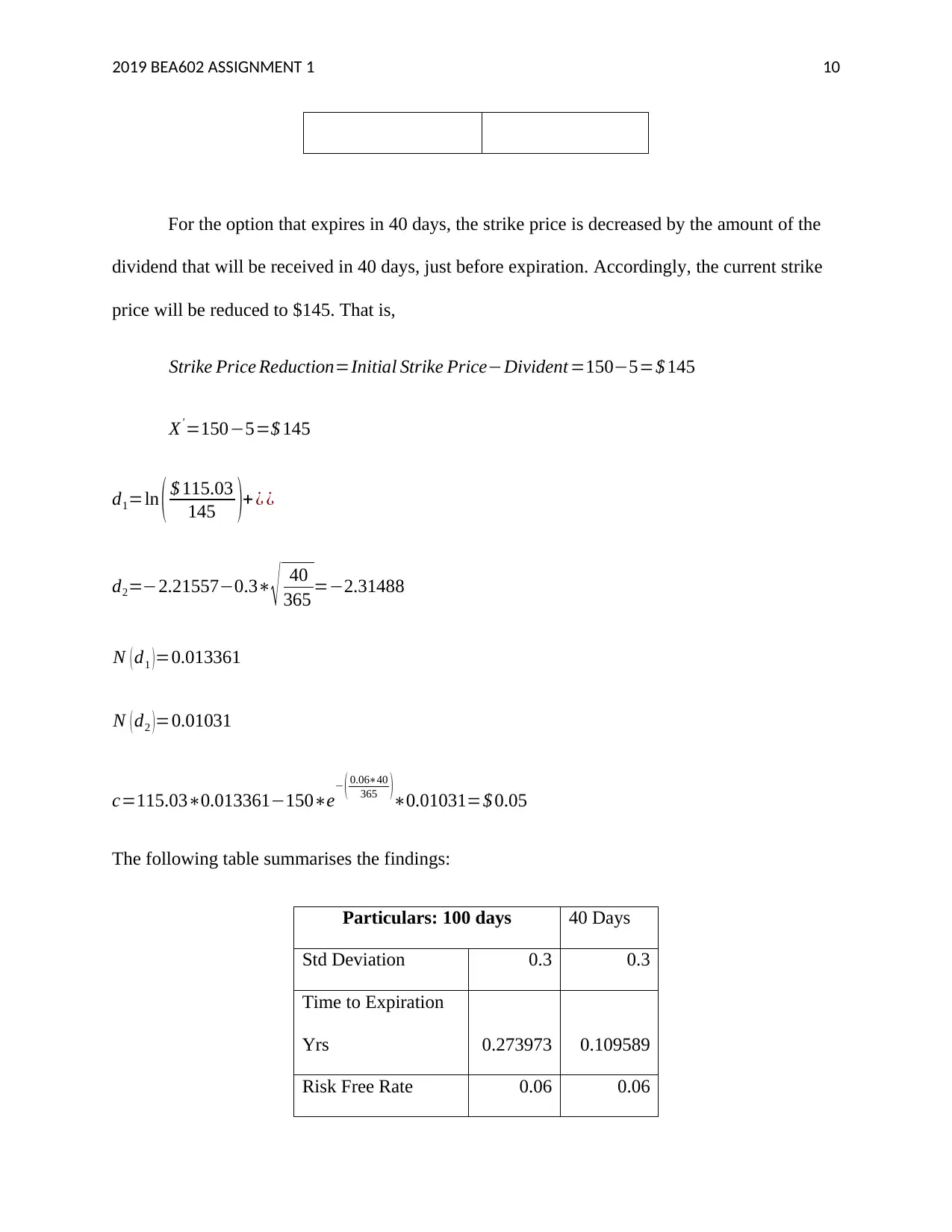

This assignment solution for BEA602 covers various aspects of financial options. It begins with analyzing straddle and strangle strategies, including payoff calculations and future value considerations. The solution then delves into option pricing models, comparing the binomial model to the Black-Scholes model, highlighting their applications and advantages. The binomial model is applied to price American call and put options, demonstrating the construction of stock trees and option valuation at different time periods. Further, the Black-Scholes model is employed to price an American call option, taking into account dividends and time to expiration. Finally, the assignment addresses portfolio construction, specifically creating a delta and gamma-neutral portfolio using call options, with detailed calculations to achieve neutrality. The assignment provides a comprehensive overview of options trading and valuation techniques.

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.