BEA602 Finance Assignment: Deep Dive into Futures, Hedging, and Swaps

VerifiedAdded on 2023/06/03

|7

|1213

|173

Homework Assignment

AI Summary

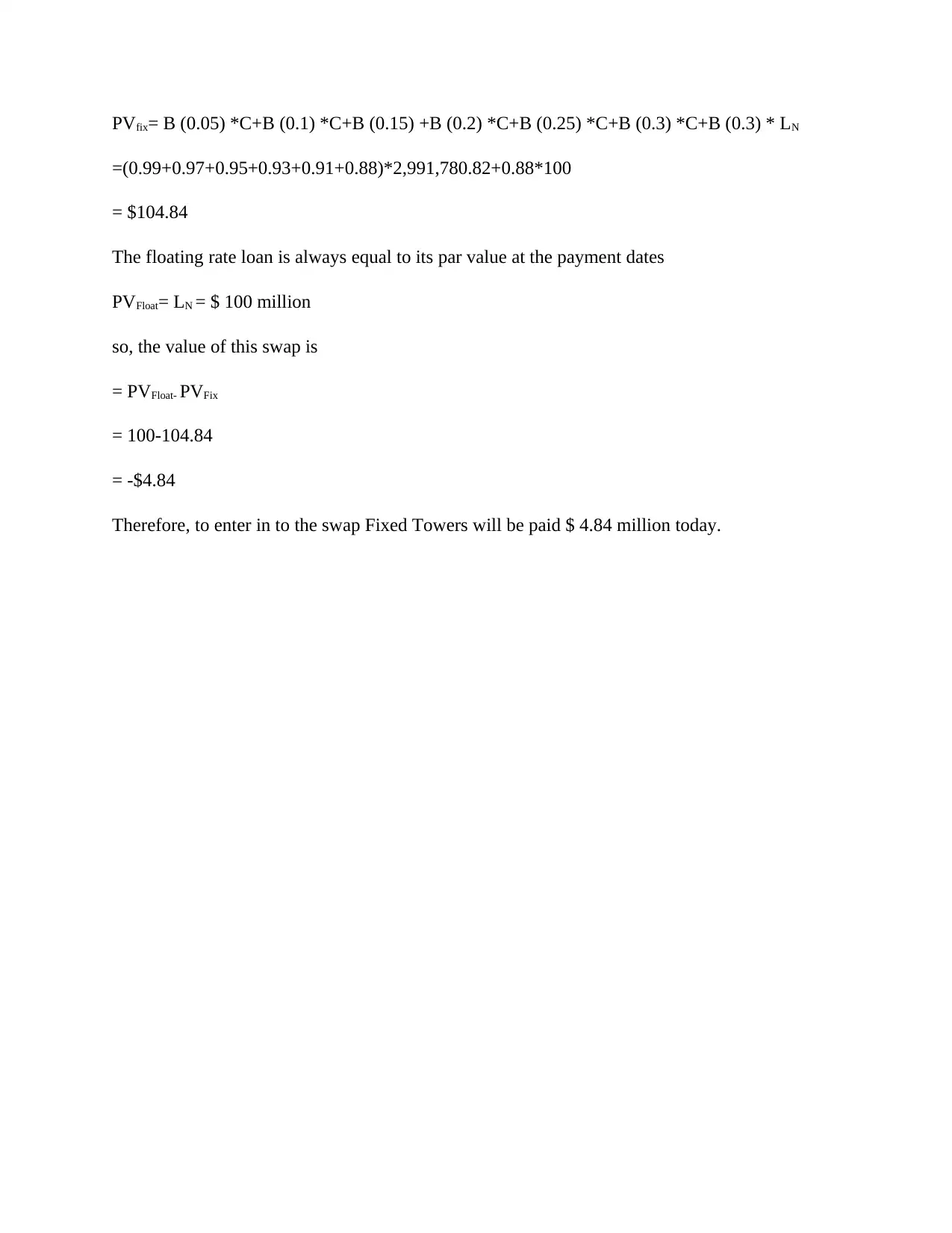

This assignment provides solutions to questions related to futures contracts, hedging strategies, and interest rate swaps. It explains the open interest in futures contracts, the convergence of futures prices to spot prices, and arbitrage opportunities. It also calculates the risk-minimization hedge ratio for a cocoa merchant and determines the number of contracts to trade. Furthermore, it discusses hedging strategies for portfolio withdrawals using S&P 500 futures and explains the construction of swaps using floating and fixed-rate bonds, including calculations for fixed payments and swap values. The document includes relevant references to support the analysis and solutions provided. Desklib offers a range of resources for students, including similar assignments and past papers.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.