Comprehensive Financial Analysis of Bega Cheese Limited (2014-2016)

VerifiedAdded on 2023/06/06

|13

|3564

|194

Report

AI Summary

This report presents a financial statement analysis of Bega Cheese Limited, a leading Australian dairy company, examining its performance from 2014 to 2016 using ratio analysis. The analysis reveals a decline in overall financial performance during 2015 and 2016 compared to 2014, with deteriorating profitability and increasing gearing ratios. While solvency remained normal until 2016, efficiency in managing assets like inventories and accounts receivables was lacking, leading to excessive funds tied up in these assets. The report assesses profitability using Return on Equity (ROE), Return on Assets (ROA), and Net Profit Margin (NPM), and evaluates efficiency through inventory turnover, asset turnover, and accounts receivable settlement periods. Liquidity is assessed using current and quick ratios, and gearing is also analyzed. The report concludes with recommendations and highlights the need for improved working capital management and strategic reinvestment decisions to enhance financial performance. Graphs are used to clearly represent the financial performance of Bega from different aspects.

Financial Statement Analysis

BEGA CHEESE LIMITED

BEGA CHEESE LIMITED

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Statement Analysis 1

Executive Summary:

This report presents the financial statement analysis of one of the leading dairy corporation of

Australia, Bega Cheese Limited. The company is listed on the Australian Stock Exchange.

The analysis of financial performance of the company in 2014, 2015 and 2016 is undertaken

using the ratio analysis technique. It has been observed that the overall financial performance

of Bega has declined in 2015 and 2016 as compared to 2014. The profitability position of

business have deteriorated over the last three reported years as depicted by the declining

profitability ratios and increasing gearing ratios. Though, the solvency position is normal up

till 2016 but the gearing ratios of company have shown declining trend over the 3 years.

Also, the assets like inventories and accounts receivables of Bega are not found to be

efficiently managed by the company and hence excessive funds are tied up in holding these

assets. The working capital management practices of the business are not found to be

adequate enough as indicated by the weak current and quick ratios results. The use of graphs

has been made to clearly represent the state of financial performance of Bega from different

aspects.

Executive Summary:

This report presents the financial statement analysis of one of the leading dairy corporation of

Australia, Bega Cheese Limited. The company is listed on the Australian Stock Exchange.

The analysis of financial performance of the company in 2014, 2015 and 2016 is undertaken

using the ratio analysis technique. It has been observed that the overall financial performance

of Bega has declined in 2015 and 2016 as compared to 2014. The profitability position of

business have deteriorated over the last three reported years as depicted by the declining

profitability ratios and increasing gearing ratios. Though, the solvency position is normal up

till 2016 but the gearing ratios of company have shown declining trend over the 3 years.

Also, the assets like inventories and accounts receivables of Bega are not found to be

efficiently managed by the company and hence excessive funds are tied up in holding these

assets. The working capital management practices of the business are not found to be

adequate enough as indicated by the weak current and quick ratios results. The use of graphs

has been made to clearly represent the state of financial performance of Bega from different

aspects.

Financial Statement Analysis 2

Table of Contents

Executive Summary:.............................................................................................................................1

Introduction...........................................................................................................................................3

Purpose of Analysis...........................................................................................................................3

Background of Bega..........................................................................................................................3

Financial analysis of Bega Cheese Limited...........................................................................................4

Profitability........................................................................................................................................4

Efficiency:.........................................................................................................................................6

Liquidity:...........................................................................................................................................7

Gearing:.............................................................................................................................................9

Recommendations and Conclusion......................................................................................................10

References:..........................................................................................................................................12

Appendix:............................................................................................................................................14

Table of Contents

Executive Summary:.............................................................................................................................1

Introduction...........................................................................................................................................3

Purpose of Analysis...........................................................................................................................3

Background of Bega..........................................................................................................................3

Financial analysis of Bega Cheese Limited...........................................................................................4

Profitability........................................................................................................................................4

Efficiency:.........................................................................................................................................6

Liquidity:...........................................................................................................................................7

Gearing:.............................................................................................................................................9

Recommendations and Conclusion......................................................................................................10

References:..........................................................................................................................................12

Appendix:............................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Statement Analysis 3

Introduction

Purpose of Analysis

The financial statements of the entity are prepared to meet the information needs of its

various stakeholders. Particularly, the providers of the finance are always keen to know about

the financial performance of the company in which they have invested their funds in order to

earn return on their investments. For the purpose of evaluating the financial strengths as well

as weakness of the company use of various tools and techniques can be made. Ratio analysis

is one of those important financial management techniques, which can be used to assess the

financial health of the business. In the present report, ratio analysis is conducted on the

financial statements of the Bega Cheese Limited for the years 2014, 2015 and 2016. As a part

of ratio analysis, the key components of financial statements are taken into account and ratios

in relation to such components have been determined and analysed by making comparative

study of all the three years.

Background of Bega Cheese Limited

Bega Cheese Limited is an Australian leading producer and supplier of cheese and other

associated food products. It was incorporated in 1899. It is specialised in supplying the

cheddar cheese in the local as well as international retail and service market. Bega Limited

exports its dairy and other food products to around 40 different countries such as Middle

East, North East, Pacific Island, Southeast Asia and Central as well as South America

(Bloomberg, 2018). It contributes positively to the national economy of Australia by

exporting its products for more than $100 million annually. Bega operates within the dairy

industry of Australia. Dairy farming is regarded as one of the main sectors in Australian

economy (Dairy Australia, 2017). Australian dairy was ranked third largest agricultural

commodity in farmgate value in 2016-17. Australia’s dairy farms are primarily owner

operated Small Medium Enterprises (ACCC, 2017). Bega Limited has two main segments:

Bega Cheese segment and Tatura Milk segment. In 1993, it had set up its 1st spray dying plant

at Tatura which produced large quantities of childhood nutritional powder. Bega is also

involved in the activities of contract packaging for various private proprietor brands,

supermarket brands and products of other dairy firms into their own brand packages. Bega

Limited has gained a sound reputation in the market as one of the most trusted iconic brands

in Australian company for its cheese products.

Introduction

Purpose of Analysis

The financial statements of the entity are prepared to meet the information needs of its

various stakeholders. Particularly, the providers of the finance are always keen to know about

the financial performance of the company in which they have invested their funds in order to

earn return on their investments. For the purpose of evaluating the financial strengths as well

as weakness of the company use of various tools and techniques can be made. Ratio analysis

is one of those important financial management techniques, which can be used to assess the

financial health of the business. In the present report, ratio analysis is conducted on the

financial statements of the Bega Cheese Limited for the years 2014, 2015 and 2016. As a part

of ratio analysis, the key components of financial statements are taken into account and ratios

in relation to such components have been determined and analysed by making comparative

study of all the three years.

Background of Bega Cheese Limited

Bega Cheese Limited is an Australian leading producer and supplier of cheese and other

associated food products. It was incorporated in 1899. It is specialised in supplying the

cheddar cheese in the local as well as international retail and service market. Bega Limited

exports its dairy and other food products to around 40 different countries such as Middle

East, North East, Pacific Island, Southeast Asia and Central as well as South America

(Bloomberg, 2018). It contributes positively to the national economy of Australia by

exporting its products for more than $100 million annually. Bega operates within the dairy

industry of Australia. Dairy farming is regarded as one of the main sectors in Australian

economy (Dairy Australia, 2017). Australian dairy was ranked third largest agricultural

commodity in farmgate value in 2016-17. Australia’s dairy farms are primarily owner

operated Small Medium Enterprises (ACCC, 2017). Bega Limited has two main segments:

Bega Cheese segment and Tatura Milk segment. In 1993, it had set up its 1st spray dying plant

at Tatura which produced large quantities of childhood nutritional powder. Bega is also

involved in the activities of contract packaging for various private proprietor brands,

supermarket brands and products of other dairy firms into their own brand packages. Bega

Limited has gained a sound reputation in the market as one of the most trusted iconic brands

in Australian company for its cheese products.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Statement Analysis 4

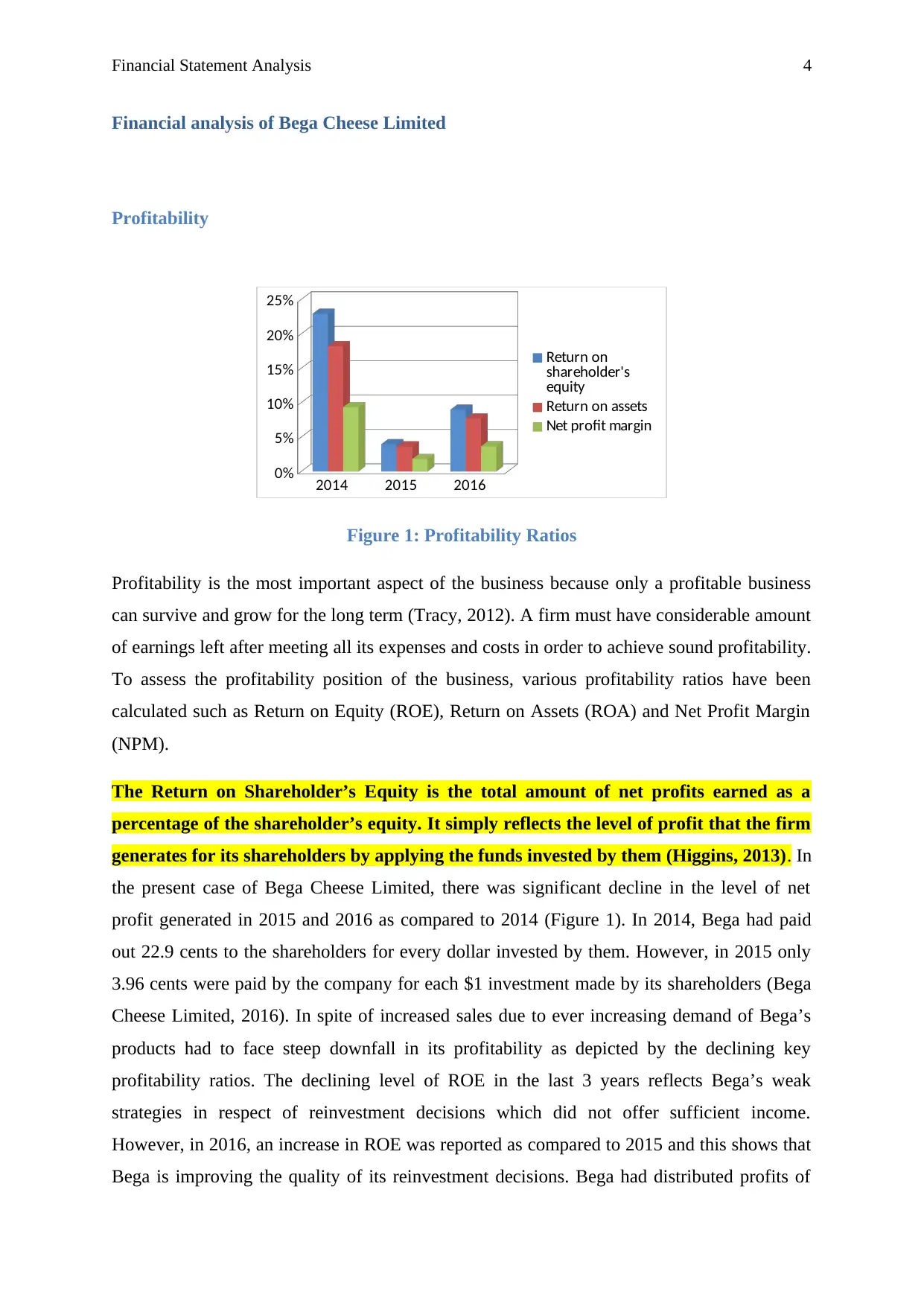

Financial analysis of Bega Cheese Limited

Profitability

2014 2015 2016

0%

5%

10%

15%

20%

25%

Return on

shareholder's

equity

Return on assets

Net profit margin

Figure 1: Profitability Ratios

Profitability is the most important aspect of the business because only a profitable business

can survive and grow for the long term (Tracy, 2012). A firm must have considerable amount

of earnings left after meeting all its expenses and costs in order to achieve sound profitability.

To assess the profitability position of the business, various profitability ratios have been

calculated such as Return on Equity (ROE), Return on Assets (ROA) and Net Profit Margin

(NPM).

The Return on Shareholder’s Equity is the total amount of net profits earned as a

percentage of the shareholder’s equity. It simply reflects the level of profit that the firm

generates for its shareholders by applying the funds invested by them (Higgins, 2013). In

the present case of Bega Cheese Limited, there was significant decline in the level of net

profit generated in 2015 and 2016 as compared to 2014 (Figure 1). In 2014, Bega had paid

out 22.9 cents to the shareholders for every dollar invested by them. However, in 2015 only

3.96 cents were paid by the company for each $1 investment made by its shareholders (Bega

Cheese Limited, 2016). In spite of increased sales due to ever increasing demand of Bega’s

products had to face steep downfall in its profitability as depicted by the declining key

profitability ratios. The declining level of ROE in the last 3 years reflects Bega’s weak

strategies in respect of reinvestment decisions which did not offer sufficient income.

However, in 2016, an increase in ROE was reported as compared to 2015 and this shows that

Bega is improving the quality of its reinvestment decisions. Bega had distributed profits of

Financial analysis of Bega Cheese Limited

Profitability

2014 2015 2016

0%

5%

10%

15%

20%

25%

Return on

shareholder's

equity

Return on assets

Net profit margin

Figure 1: Profitability Ratios

Profitability is the most important aspect of the business because only a profitable business

can survive and grow for the long term (Tracy, 2012). A firm must have considerable amount

of earnings left after meeting all its expenses and costs in order to achieve sound profitability.

To assess the profitability position of the business, various profitability ratios have been

calculated such as Return on Equity (ROE), Return on Assets (ROA) and Net Profit Margin

(NPM).

The Return on Shareholder’s Equity is the total amount of net profits earned as a

percentage of the shareholder’s equity. It simply reflects the level of profit that the firm

generates for its shareholders by applying the funds invested by them (Higgins, 2013). In

the present case of Bega Cheese Limited, there was significant decline in the level of net

profit generated in 2015 and 2016 as compared to 2014 (Figure 1). In 2014, Bega had paid

out 22.9 cents to the shareholders for every dollar invested by them. However, in 2015 only

3.96 cents were paid by the company for each $1 investment made by its shareholders (Bega

Cheese Limited, 2016). In spite of increased sales due to ever increasing demand of Bega’s

products had to face steep downfall in its profitability as depicted by the declining key

profitability ratios. The declining level of ROE in the last 3 years reflects Bega’s weak

strategies in respect of reinvestment decisions which did not offer sufficient income.

However, in 2016, an increase in ROE was reported as compared to 2015 and this shows that

Bega is improving the quality of its reinvestment decisions. Bega had distributed profits of

Financial Statement Analysis 5

8.99 cents as the dividend for every $1 of shareholder’s investment. The profit distribution in

2015 was quite lower than distribution of 22.9 cents which was made in 2014. Bega’s

profitability condition in 2016 was not as satisfactory as it was in 2014 but it was better than

that of 2015. In 2014, Bega had also earned a profit on sales of shares which had significantly

contributed to its total earnings.

Further, Return on Asset (ROA) ratio has been calculated in respect of all the 3 concerned

years. This ratio generally takes into account two features of the business i.e. its wealth

creation level and its efficiency to utilise its total assets. ROA reflects the level of profits

earned by the business by utilising its total assets effectively in the business (Tracy,

2012). In 2015, there has been reported a significant fall in Bega’s ROA as compared to that

of 2014. The major reasons behind the fall were decline in Bega’s net profit and the rise in

the level of company’s total assets. A large proportion of assets owned by the company have

remained idle during the year (Higgins, 2012). However, in 2016, the ROA had improved

slightly due to widened business operations of Bega (Bega Cheese Limited, 2017). There was

an increase of 4.03% in company’s ROA of 2016 as compared to 2015 due to increased

revenue and profits.

Furthermore, the net profit margin has been calculated to assess further the profitability

position of business. The net profit margin ratio shows the percentage of earnings left

after meeting all the expenses of business. It is observed that there was a downfall in the

Bega’s net profits of 2015 because of more operating expenses as compared to that of 2014.

In 2014, the NPM of 9.35% shows that each dollar of sales had generated 9.35 cents of profit

before interest and tax for Bega. However, in 2015 only 1.80 cents could be earned as profit

from each dollar of revenue from sales. This was due to increase in the operating expenses of

the business. Therefore, it can be said that the profitability position of the business had faced

a downfall over the 3 yeas reported in the report (Tracy, 2012).

Efficiency:

8.99 cents as the dividend for every $1 of shareholder’s investment. The profit distribution in

2015 was quite lower than distribution of 22.9 cents which was made in 2014. Bega’s

profitability condition in 2016 was not as satisfactory as it was in 2014 but it was better than

that of 2015. In 2014, Bega had also earned a profit on sales of shares which had significantly

contributed to its total earnings.

Further, Return on Asset (ROA) ratio has been calculated in respect of all the 3 concerned

years. This ratio generally takes into account two features of the business i.e. its wealth

creation level and its efficiency to utilise its total assets. ROA reflects the level of profits

earned by the business by utilising its total assets effectively in the business (Tracy,

2012). In 2015, there has been reported a significant fall in Bega’s ROA as compared to that

of 2014. The major reasons behind the fall were decline in Bega’s net profit and the rise in

the level of company’s total assets. A large proportion of assets owned by the company have

remained idle during the year (Higgins, 2012). However, in 2016, the ROA had improved

slightly due to widened business operations of Bega (Bega Cheese Limited, 2017). There was

an increase of 4.03% in company’s ROA of 2016 as compared to 2015 due to increased

revenue and profits.

Furthermore, the net profit margin has been calculated to assess further the profitability

position of business. The net profit margin ratio shows the percentage of earnings left

after meeting all the expenses of business. It is observed that there was a downfall in the

Bega’s net profits of 2015 because of more operating expenses as compared to that of 2014.

In 2014, the NPM of 9.35% shows that each dollar of sales had generated 9.35 cents of profit

before interest and tax for Bega. However, in 2015 only 1.80 cents could be earned as profit

from each dollar of revenue from sales. This was due to increase in the operating expenses of

the business. Therefore, it can be said that the profitability position of the business had faced

a downfall over the 3 yeas reported in the report (Tracy, 2012).

Efficiency:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Statement Analysis 6

2014 2015 2016

0

20

40

60

80

100

120

140

160

180

200

Inventory turnover

period (days)

Settlement period for

Accounts Receivable

(days)

Asset Turnover

Period (days)

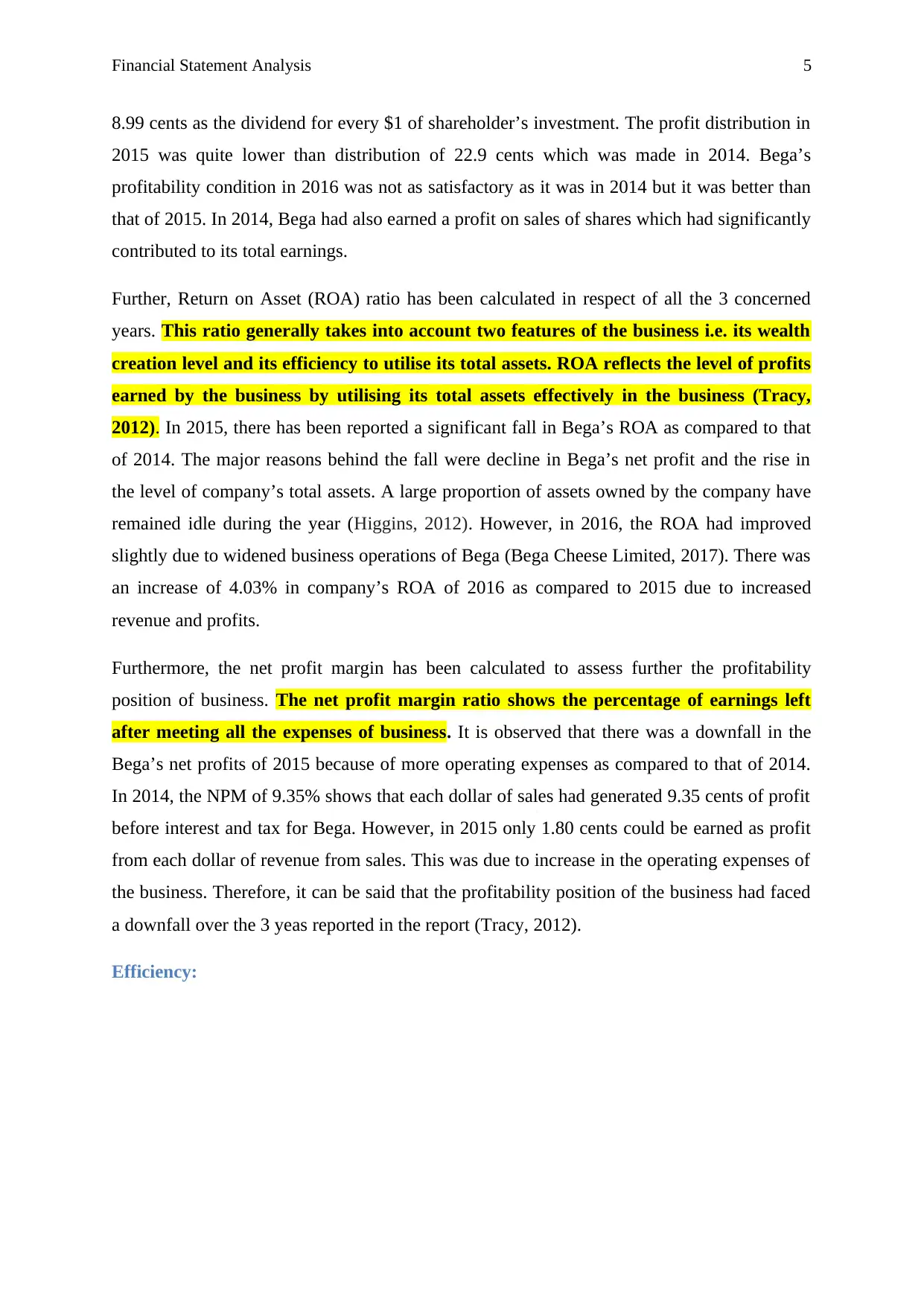

Figure 2: Efficiency Ratios

Secondly, the efficiency state of business has been analysed using various ratios such as

Inventory Turnover Ratio (ITR), Asset Turnover Ratio (ATR) and by determining the period

that was required to settle down the accounts receivables of the company. The efficiency

ratios are applied to assess the firm’s efficiency to manage its different assets.

The inventory turnover ratio measures the company’s efficiency in converting its

inventory into sales (Fridson & Alvarez, 2011). It measures the number of times a firm

sold its average inventory. As depicted from the graph above in Figure 2, inventory of Bega

Cheese Limited had slightly increased after 2014 and this shows that Bega had taken few

more days to convert its inventories into sales. Generally, it is preferred to maintain shorter

inventory turnover periods so as to avoid excessive inventory holding costs (Nissim &

Penman, 2001). Even, the length of settlement period of company’s accounts receivable had

also increased since 2014. It is the reflection of company’s liberal trade credit policies due to

which it was not able to quickly convert its credit sales into cash.

An asset turnover ratio of the firm reflects the level of efficiency with which the assets of

business are deployed in order to generate sales (Penman & Penman, 2001). The

declining asset turnover period shows company’s efficiency in managing its total assets

to generate higher sales revenue. Greater the number of days of asset turnover period, lower

the percentage of asset turnover ratio and generally higher ratio is preferred. Since the asset

turnover days have declined since 2014, Bega’s efficiency in managing its overall assets can

be said to have improved in 2016 (Annual Report, 2016).

Liquidity:

2014 2015 2016

0

20

40

60

80

100

120

140

160

180

200

Inventory turnover

period (days)

Settlement period for

Accounts Receivable

(days)

Asset Turnover

Period (days)

Figure 2: Efficiency Ratios

Secondly, the efficiency state of business has been analysed using various ratios such as

Inventory Turnover Ratio (ITR), Asset Turnover Ratio (ATR) and by determining the period

that was required to settle down the accounts receivables of the company. The efficiency

ratios are applied to assess the firm’s efficiency to manage its different assets.

The inventory turnover ratio measures the company’s efficiency in converting its

inventory into sales (Fridson & Alvarez, 2011). It measures the number of times a firm

sold its average inventory. As depicted from the graph above in Figure 2, inventory of Bega

Cheese Limited had slightly increased after 2014 and this shows that Bega had taken few

more days to convert its inventories into sales. Generally, it is preferred to maintain shorter

inventory turnover periods so as to avoid excessive inventory holding costs (Nissim &

Penman, 2001). Even, the length of settlement period of company’s accounts receivable had

also increased since 2014. It is the reflection of company’s liberal trade credit policies due to

which it was not able to quickly convert its credit sales into cash.

An asset turnover ratio of the firm reflects the level of efficiency with which the assets of

business are deployed in order to generate sales (Penman & Penman, 2001). The

declining asset turnover period shows company’s efficiency in managing its total assets

to generate higher sales revenue. Greater the number of days of asset turnover period, lower

the percentage of asset turnover ratio and generally higher ratio is preferred. Since the asset

turnover days have declined since 2014, Bega’s efficiency in managing its overall assets can

be said to have improved in 2016 (Annual Report, 2016).

Liquidity:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Statement Analysis 7

2014 2015 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Current Ratio

(times)

Quick Asset Ratio

(times)

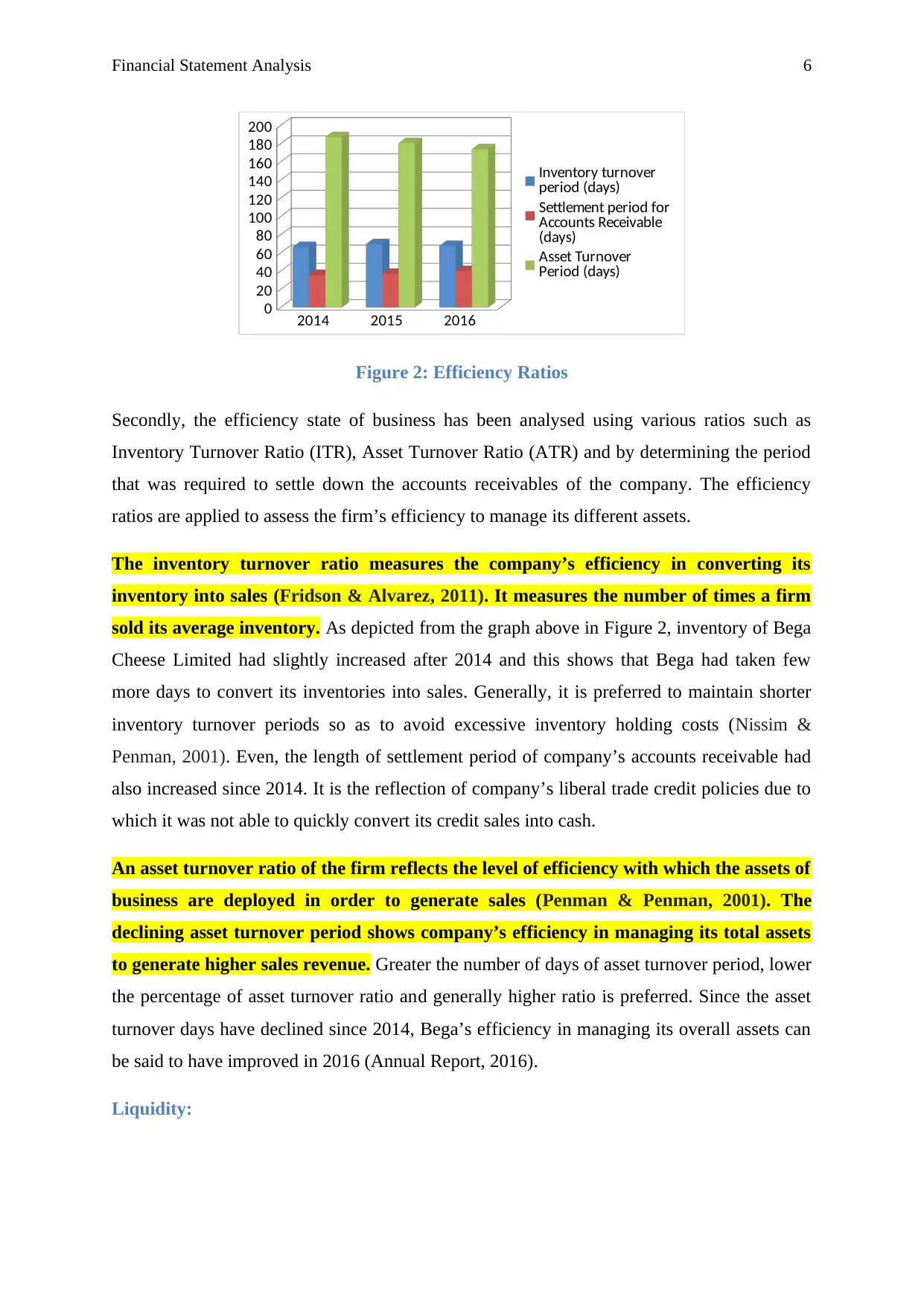

Figure 3: Liquidity Ratio

Thirdly, the liquidity position of the business has been analysed using the two main liquidity

ratios: current ratio and liquid ratio. Liquidity in business is achieved when the company is

capable of meeting its short term financial obligations as and when they become due, out of

its current assets without having the need to dispose-off its fixed assets. The ideal current

ratio is considered as 2:1, which implies that the firm must at least have the current

assets of twice the amount of its current liabilities so as to maintain its liquidity state in

the market (Higgins, 2013).

In the present case, the current ratio of Bega Cheese Limited in all the three years under

consideration was below the ratio of 2:1 as shown in graph above in Figure 3. This indicates

that Bega’s liquidity position was not satisfactory in all the 3 years. But, at the same time it

could be observed that liquidity state of its business had improved at the fluctuating rate in

2015 and 2016. In 2014, liquidity position was weakest among all the periods reported. In

2015, there has been reported a slight improvement of 0.32 times in the current ratio and this

shows that Bega had improved its working capital management practices. But, in 2016, the

current ratio had again declined to 1.65:1 and this shows that Bega would have to struggle to

meet its current liabilities in total using its current assets. It must improve its current assets

management so as to achieve liquidity position in the market (Papadopoulos, 2011).

The quick ratio reflects the proportion of quick assets available with the business to the

current liabilities of the business (Foster, 2004). It measures the ability of the firm to

pay out its current liabilities through the use only those assets that are readily and

conveniently converted into cash. The ideal quick ratio is 1:1 which means that the

company must at least have quick assets of value equivalent to the value of its current

2014 2015 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Current Ratio

(times)

Quick Asset Ratio

(times)

Figure 3: Liquidity Ratio

Thirdly, the liquidity position of the business has been analysed using the two main liquidity

ratios: current ratio and liquid ratio. Liquidity in business is achieved when the company is

capable of meeting its short term financial obligations as and when they become due, out of

its current assets without having the need to dispose-off its fixed assets. The ideal current

ratio is considered as 2:1, which implies that the firm must at least have the current

assets of twice the amount of its current liabilities so as to maintain its liquidity state in

the market (Higgins, 2013).

In the present case, the current ratio of Bega Cheese Limited in all the three years under

consideration was below the ratio of 2:1 as shown in graph above in Figure 3. This indicates

that Bega’s liquidity position was not satisfactory in all the 3 years. But, at the same time it

could be observed that liquidity state of its business had improved at the fluctuating rate in

2015 and 2016. In 2014, liquidity position was weakest among all the periods reported. In

2015, there has been reported a slight improvement of 0.32 times in the current ratio and this

shows that Bega had improved its working capital management practices. But, in 2016, the

current ratio had again declined to 1.65:1 and this shows that Bega would have to struggle to

meet its current liabilities in total using its current assets. It must improve its current assets

management so as to achieve liquidity position in the market (Papadopoulos, 2011).

The quick ratio reflects the proportion of quick assets available with the business to the

current liabilities of the business (Foster, 2004). It measures the ability of the firm to

pay out its current liabilities through the use only those assets that are readily and

conveniently converted into cash. The ideal quick ratio is 1:1 which means that the

company must at least have quick assets of value equivalent to the value of its current

Financial Statement Analysis 8

liabilities so that such liabilities could be met, whenever they fall due without facing any sort

of cash crisis in meeting those obligations. Looking at current and quick ratios in all the 3

years under consideration, it can be said that Bega had not held sufficient amount of current

assets in the business which were required to meet its current financial obligations (Innocent,

Mary & Matthew, 2013).

Gearing:

2014 2015 2016

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

Gearing Ratio

Debt to Assets

Figure 2: Gearing Ratios

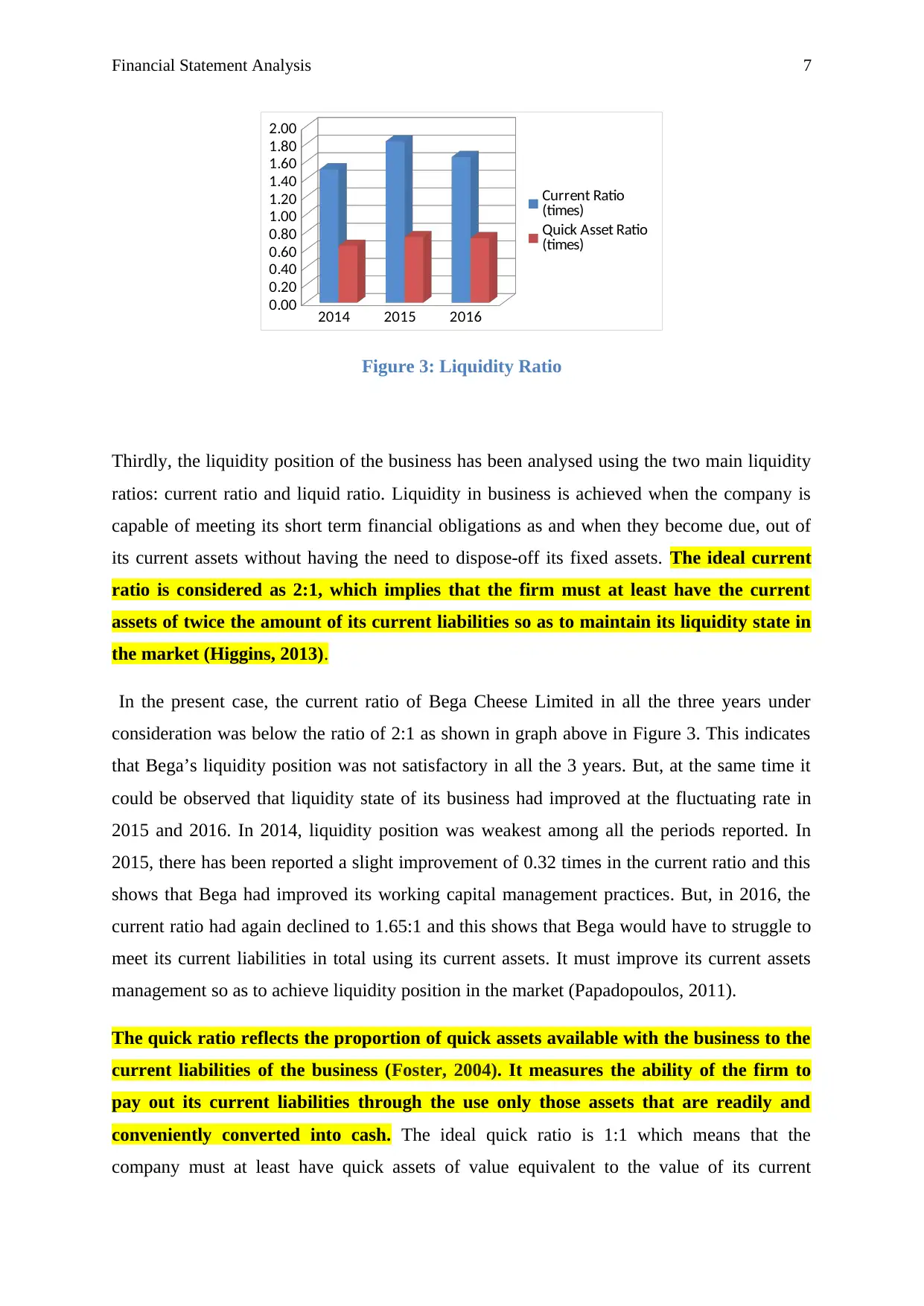

Lastly, the solvency position of the business has been analysed using the gearing ratios and

by evaluating the appropriateness of company’s capital structure. Solvency aspect of the

financial performance is important for the key stakeholders of company such as investors and

creditors. The gearing ratio determines the quantum of contribution made by long term

creditors of the business to the total capital structure of the business (equity as well as

non-current liabilities) (Fridson & Alvarez, 2011). The gearing level of the business

represents the financial leverage of the company. Higher the financial leverage, higher are the

chances of firm’s insolvency in the market because if more external debt is comprised in the

capital structure, the company has more legal commitments towards meeting the financial

obligations such as principle and interest costs on the regular basis (Higgins, 2012).

The graph in Figure 4 above shows that the gearing ratio of Bega had increased significantly

in 2015 as compared to 2014, which means that the debt portion of Bega has increased in

2015. However, gearing ratio lower than 50% is considered normal as it shows that majority

of company’s capital is raised through equity shareholders. However, gearing ratio in Bega’s

case is showing upward movement since 2014 till 2016 which signifies that the proportion of

company’s external debt was increasing in the subsequent years ahead of 2014. But, in 2016

liabilities so that such liabilities could be met, whenever they fall due without facing any sort

of cash crisis in meeting those obligations. Looking at current and quick ratios in all the 3

years under consideration, it can be said that Bega had not held sufficient amount of current

assets in the business which were required to meet its current financial obligations (Innocent,

Mary & Matthew, 2013).

Gearing:

2014 2015 2016

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

Gearing Ratio

Debt to Assets

Figure 2: Gearing Ratios

Lastly, the solvency position of the business has been analysed using the gearing ratios and

by evaluating the appropriateness of company’s capital structure. Solvency aspect of the

financial performance is important for the key stakeholders of company such as investors and

creditors. The gearing ratio determines the quantum of contribution made by long term

creditors of the business to the total capital structure of the business (equity as well as

non-current liabilities) (Fridson & Alvarez, 2011). The gearing level of the business

represents the financial leverage of the company. Higher the financial leverage, higher are the

chances of firm’s insolvency in the market because if more external debt is comprised in the

capital structure, the company has more legal commitments towards meeting the financial

obligations such as principle and interest costs on the regular basis (Higgins, 2012).

The graph in Figure 4 above shows that the gearing ratio of Bega had increased significantly

in 2015 as compared to 2014, which means that the debt portion of Bega has increased in

2015. However, gearing ratio lower than 50% is considered normal as it shows that majority

of company’s capital is raised through equity shareholders. However, gearing ratio in Bega’s

case is showing upward movement since 2014 till 2016 which signifies that the proportion of

company’s external debt was increasing in the subsequent years ahead of 2014. But, in 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Statement Analysis 9

the gearing level of Bega’s business had slightly declined as compared to that of 2015 which

shows that company is trying to optimise its capital structure.

Debt to total asset ratio determines the proportion of total assets of the firm that are

financed by the external debt (Fridson & Alvarez, 2011). In 2014 and 2015 around 43% of

the total assets were financed through the use of funds of creditors and remaining 57% of the

funds were financed through the internal sources such as equity capital and retaining

earnings. However, in 2016 the debt to asset ratio of Bega had increased slightly. The debt to

total assets ratio of 44% as reported in 2016 shows that company had acquired more assets

through the use of external financing. Since the gearing ratios of company in last 3 years are

below 50%, it can be said that the company is normally geared. But, if the trend of increasing

debt to total asset ratio is further followed in the subsequent years Bega will have to face

higher financial leverage (Kumbirai, 2010).

Recommendations and Conclusion

From the above analysis it can be stated that Bega Limited’s overall financial performance

has degraded over the last three reported financial years. The profitability position of the

company was highest in 2014 among all the three years. Bega Limited must invest its funds

prudently in further acquiring its business assets so as to avoid the situations where assets

remain idle throughout the year. Also, Bega Limited must make efforts to strengthen its

liquidity position in the market in the upcoming years by employing effective working capital

management practices such as making stringent trade credit policies, applying just in time

approach for the inventory management, investing in liquid assets etc. The operating

efficiency of Bega in respect of its assets like inventories and accounts receivables is not

found to be sound because the amount that is invested in these assets is not generating any

return for the business. It should rather minimise the duration of conversion of inventories

into sales and then credit sales into cash through the implementation of strong asset

management policies. The solvency position of Bega could be said to be normal as the

proportion of external debt in the entire capital structure is lower than the proportion of

equity. However, the increasing trend of gearing ratios must be controlled by the company in

order to prevent itself from the exposure to higher financial risk.

the gearing level of Bega’s business had slightly declined as compared to that of 2015 which

shows that company is trying to optimise its capital structure.

Debt to total asset ratio determines the proportion of total assets of the firm that are

financed by the external debt (Fridson & Alvarez, 2011). In 2014 and 2015 around 43% of

the total assets were financed through the use of funds of creditors and remaining 57% of the

funds were financed through the internal sources such as equity capital and retaining

earnings. However, in 2016 the debt to asset ratio of Bega had increased slightly. The debt to

total assets ratio of 44% as reported in 2016 shows that company had acquired more assets

through the use of external financing. Since the gearing ratios of company in last 3 years are

below 50%, it can be said that the company is normally geared. But, if the trend of increasing

debt to total asset ratio is further followed in the subsequent years Bega will have to face

higher financial leverage (Kumbirai, 2010).

Recommendations and Conclusion

From the above analysis it can be stated that Bega Limited’s overall financial performance

has degraded over the last three reported financial years. The profitability position of the

company was highest in 2014 among all the three years. Bega Limited must invest its funds

prudently in further acquiring its business assets so as to avoid the situations where assets

remain idle throughout the year. Also, Bega Limited must make efforts to strengthen its

liquidity position in the market in the upcoming years by employing effective working capital

management practices such as making stringent trade credit policies, applying just in time

approach for the inventory management, investing in liquid assets etc. The operating

efficiency of Bega in respect of its assets like inventories and accounts receivables is not

found to be sound because the amount that is invested in these assets is not generating any

return for the business. It should rather minimise the duration of conversion of inventories

into sales and then credit sales into cash through the implementation of strong asset

management policies. The solvency position of Bega could be said to be normal as the

proportion of external debt in the entire capital structure is lower than the proportion of

equity. However, the increasing trend of gearing ratios must be controlled by the company in

order to prevent itself from the exposure to higher financial risk.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Statement Analysis 10

References:

ACCC, 2017. The Australian dairy industry. Available at

https://www.accc.gov.au/system/files/Farmer%2520Power_0.pdf Accessed on 12 September

2018

Bega Cheese Limited, 2016. Annual Report. Available at:

https://www.begacheese.com.au/wp-content/uploads/2012/10/04-2015-ANNUAL-

REPORT.pdf accessed on 12 September 2018

Bega Cheese Limited, 2016. Annual Report. Available at:

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_BGA_2017.pdf

accessed on 12 September 2018

Bloomberg, 2018. Company Overview of Bega Cheese Limited. Available at:

https://www.investing.businessweek.wallst.com/research/stocks/snapshot/

snapshot_article.asp?ticker=BGA:AU accessed on 12 September 2018

Dairy Australia, 2017. The Australian dairy industry at a glance. 2016–17.Available at:

https://www.dairyaustralia.com.au/-/media/dairyaustralia/documents/about-dairy-australia/

key-publications/2017-in-focus.ashx?

la=en&hash=701F2B1E4ACFC95F62FAE99E25AE5CA4B9F7585C. accessed on 12

September 2018

Foster, G., 2004. Financial Statement Analysis, 2/e. Pearson Education India.

Fridson, M.S. and Alvarez, F., 2011. Financial statement analysis: a practitioner's

guide (Vol. 597). John Wiley & Sons.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Innocent, E.C., Mary, O.I. and Matthew, O.M., 2013. Financial ratio analysis as a

determinant of profitability in Nigerian pharmaceutical industry. International journal of

business and management, 8(8), p.107.

References:

ACCC, 2017. The Australian dairy industry. Available at

https://www.accc.gov.au/system/files/Farmer%2520Power_0.pdf Accessed on 12 September

2018

Bega Cheese Limited, 2016. Annual Report. Available at:

https://www.begacheese.com.au/wp-content/uploads/2012/10/04-2015-ANNUAL-

REPORT.pdf accessed on 12 September 2018

Bega Cheese Limited, 2016. Annual Report. Available at:

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_BGA_2017.pdf

accessed on 12 September 2018

Bloomberg, 2018. Company Overview of Bega Cheese Limited. Available at:

https://www.investing.businessweek.wallst.com/research/stocks/snapshot/

snapshot_article.asp?ticker=BGA:AU accessed on 12 September 2018

Dairy Australia, 2017. The Australian dairy industry at a glance. 2016–17.Available at:

https://www.dairyaustralia.com.au/-/media/dairyaustralia/documents/about-dairy-australia/

key-publications/2017-in-focus.ashx?

la=en&hash=701F2B1E4ACFC95F62FAE99E25AE5CA4B9F7585C. accessed on 12

September 2018

Foster, G., 2004. Financial Statement Analysis, 2/e. Pearson Education India.

Fridson, M.S. and Alvarez, F., 2011. Financial statement analysis: a practitioner's

guide (Vol. 597). John Wiley & Sons.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Innocent, E.C., Mary, O.I. and Matthew, O.M., 2013. Financial ratio analysis as a

determinant of profitability in Nigerian pharmaceutical industry. International journal of

business and management, 8(8), p.107.

Financial Statement Analysis 11

Kumbirai, M., 2010. A financial ratio analysis of commercial bank performance in South

Africa. African Review of Economics and Finance, 2(1), pp.30-53.

Nissim, D. and Penman, S.H., 2001. Ratio analysis and equity valuation: From research to

practice. Review of accounting studies, 6(1), pp.109-154.

Papadopoulos, P. 2011. Investment Report - Fundamental Analysis/ Ratio Analysis. GRIN

Verlag.

Penman, S.H. and Penman, S.H., 2001. Financial statement analysis and security valuation.

New York, NY: McGraw-Hill/Irwin.

Tracy, A. 2012. Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to

Analyse Any Business on the Planet. RatioAnalysis.net.

Kumbirai, M., 2010. A financial ratio analysis of commercial bank performance in South

Africa. African Review of Economics and Finance, 2(1), pp.30-53.

Nissim, D. and Penman, S.H., 2001. Ratio analysis and equity valuation: From research to

practice. Review of accounting studies, 6(1), pp.109-154.

Papadopoulos, P. 2011. Investment Report - Fundamental Analysis/ Ratio Analysis. GRIN

Verlag.

Penman, S.H. and Penman, S.H., 2001. Financial statement analysis and security valuation.

New York, NY: McGraw-Hill/Irwin.

Tracy, A. 2012. Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to

Analyse Any Business on the Planet. RatioAnalysis.net.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.