BEHAVIOURAL ECONOMICS (S1 2019) Assignment 2: Solutions and Analysis

VerifiedAdded on 2022/12/15

|12

|2269

|234

Homework Assignment

AI Summary

This document presents a comprehensive solution to Assignment 2 in a Behavioral Economics course. The solution covers multiple-choice questions and problem-solving scenarios. Key topics addressed include expected utility maximization, prospect theory, the Ellsberg Paradox, time consistency, Nash Equilibrium, and various discounting models (exponential and quasi-hyperbolic). The assignment analyzes decision-making under risk and uncertainty, exploring concepts such as reference points, loss aversion, and the impact of present bias on choices. The solution includes graphical representations of utility and value functions, along with detailed explanations of how individuals make decisions in different contexts, such as court cases, purchasing decisions, and group assignments. The assignment also examines the implications of different preference structures on strategic interactions. The solutions provided help students to understand and apply behavioral economic principles to real-world situations.

Course on

BEHAVIOURAL ECONOMICS (S1 2019)

Ralph-Christopher Bayer

Assignment 2

Deadline: End of Week 13 (Sunday June 16th, midnight)

Multiple Choice Questions

1. A person that chooses the alternative that has the highest Expected Value, when risk is

involved, violates the assumptions of expected utility maximization.

True. An individual chooses the outcome with the highest expected utility according to

expected utility maximization. So, on the basis of expected value, the assumption of

expected utility maximization is violated

2. An expected utility maximizer with u(x) = log(x) rejects all fair gambles (i.e. those

with an expected value of zero).

False. Because a common utility model suggested by Bernoulli, himself is logarithmic

function of the gamblers total wealth (x) and the concept of diminishing marginal utility

of money is built into it.

3. Prospect Theory can explain the Ellsberg Paradox.

False. The combining behavioral economic theory known as the prospect theory and it

can explain in Allais paradox not Ellsberg paradox.

1

BEHAVIOURAL ECONOMICS (S1 2019)

Ralph-Christopher Bayer

Assignment 2

Deadline: End of Week 13 (Sunday June 16th, midnight)

Multiple Choice Questions

1. A person that chooses the alternative that has the highest Expected Value, when risk is

involved, violates the assumptions of expected utility maximization.

True. An individual chooses the outcome with the highest expected utility according to

expected utility maximization. So, on the basis of expected value, the assumption of

expected utility maximization is violated

2. An expected utility maximizer with u(x) = log(x) rejects all fair gambles (i.e. those

with an expected value of zero).

False. Because a common utility model suggested by Bernoulli, himself is logarithmic

function of the gamblers total wealth (x) and the concept of diminishing marginal utility

of money is built into it.

3. Prospect Theory can explain the Ellsberg Paradox.

False. The combining behavioral economic theory known as the prospect theory and it

can explain in Allais paradox not Ellsberg paradox.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Sophisticated Quasi-Hyperbolic Discounters behave time consistently, as they know

that they will have a present bias in future decisions and therefore act to eliminate the

bias.

True. Hyperbolic discounters behave time inconsistent model of delay discounting.

5. The outcome resulting from a Nash Equilibirum is socially efficient, since in a Nash

Equilibrium all players play best responses to each other.

False. Nash Equilibrium is an outcome in which every player is doing the best possible

can be given other player’s choices. So, no player can benefit from unilaterally

changing his choice.

6. Rational preferences should only depend on the person’s own outcomes (such as their

own consumption, wealth, etc.)

True.

7. Jack, who has the utility function u(x,y) = x − γy, where x is his own material payoff,

while y is the material payoff of his neighbour, can be described as envious.

False

8. Somebody who plays the lottery cannot be an expected utility maximizer.

False

2

that they will have a present bias in future decisions and therefore act to eliminate the

bias.

True. Hyperbolic discounters behave time inconsistent model of delay discounting.

5. The outcome resulting from a Nash Equilibirum is socially efficient, since in a Nash

Equilibrium all players play best responses to each other.

False. Nash Equilibrium is an outcome in which every player is doing the best possible

can be given other player’s choices. So, no player can benefit from unilaterally

changing his choice.

6. Rational preferences should only depend on the person’s own outcomes (such as their

own consumption, wealth, etc.)

True.

7. Jack, who has the utility function u(x,y) = x − γy, where x is his own material payoff,

while y is the material payoff of his neighbour, can be described as envious.

False

8. Somebody who plays the lottery cannot be an expected utility maximizer.

False

2

9. If somebody is taking drugs, then that does not necessarily mean that she/he cannot be

an exponential discounter.

False

10. The Allais Paradox demonstrates that many humans evaluate the same lotteries

differently if they are combined with the same other lottery.

True. The lotteries are evaluated differently because the earlier ones are nested within

others and the new ones are of compound nature.

3

an exponential discounter.

False

10. The Allais Paradox demonstrates that many humans evaluate the same lotteries

differently if they are combined with the same other lottery.

True. The lotteries are evaluated differently because the earlier ones are nested within

others and the new ones are of compound nature.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Problems

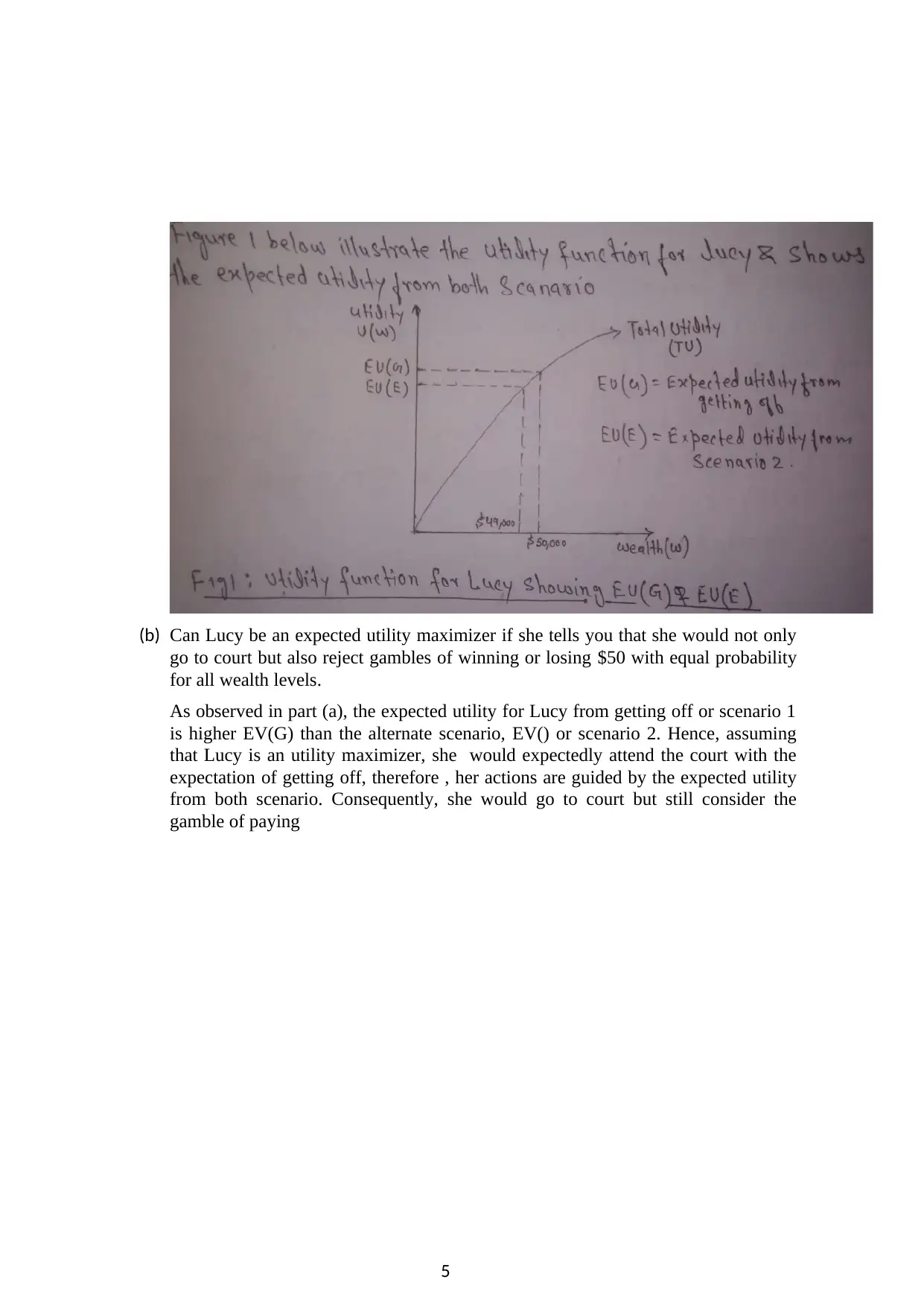

1. Lucy has current wealth of $100,000. She has just been sent a notice to pay $500 for

speeding. Lucy decides not to pay and to go to court. There she will either get off

(because of insufficient evidence)and pay nothing or will have to pay the fine plus the

court cost which together amount to $1,000. Lucy sees her chances of getting off at

50%.

(a) Suppose Lucy is an expected utility maximizer. Draw a graph with a utility function

that can explain Lucy’s choice. Clearly label the wealth axis. Mark the expected

utility of going to court and the utility of paying the fine.

Part a )

Current wealth of Lucy w=$ 100,000

Now, in scenario 1 Lucy can go to court and decide not to pay anything and get

which has a probability pr (Q)= 50 % or 0.5

In scenario 2 , she will have to pay the fine and the court expenses amounting to a

total of $ 1000. The probability of paying all the expenses, Pr(E)=50% or 0.5 as

well know

, the Expected utility (EV) =Pr (event 1).Gain from event 1+Pr(event 2). Gain from

event 2 + Pr (event 3). Gain from event +Pr (event n). Gain from event n.

In scenario 1 Lucy’s gain= $ 100,000as she pays nothing in scenario 2 her gain = ($

100,000-$ 1000)=$ 99,000

Lucy’s expected utility from scenario 1(getting off)= Pr(G)Gain from getting off

scenario 1.

=0.5 ($ 100,000)

=$ 50,000

= Ev (G)

Lucy’s expected utility from scenario 2 paying a total of $

1000

Pr (E) Gain from scenario 2

=0.5 ($ 99,00)

=$ 49,500=EV(E)

4

1. Lucy has current wealth of $100,000. She has just been sent a notice to pay $500 for

speeding. Lucy decides not to pay and to go to court. There she will either get off

(because of insufficient evidence)and pay nothing or will have to pay the fine plus the

court cost which together amount to $1,000. Lucy sees her chances of getting off at

50%.

(a) Suppose Lucy is an expected utility maximizer. Draw a graph with a utility function

that can explain Lucy’s choice. Clearly label the wealth axis. Mark the expected

utility of going to court and the utility of paying the fine.

Part a )

Current wealth of Lucy w=$ 100,000

Now, in scenario 1 Lucy can go to court and decide not to pay anything and get

which has a probability pr (Q)= 50 % or 0.5

In scenario 2 , she will have to pay the fine and the court expenses amounting to a

total of $ 1000. The probability of paying all the expenses, Pr(E)=50% or 0.5 as

well know

, the Expected utility (EV) =Pr (event 1).Gain from event 1+Pr(event 2). Gain from

event 2 + Pr (event 3). Gain from event +Pr (event n). Gain from event n.

In scenario 1 Lucy’s gain= $ 100,000as she pays nothing in scenario 2 her gain = ($

100,000-$ 1000)=$ 99,000

Lucy’s expected utility from scenario 1(getting off)= Pr(G)Gain from getting off

scenario 1.

=0.5 ($ 100,000)

=$ 50,000

= Ev (G)

Lucy’s expected utility from scenario 2 paying a total of $

1000

Pr (E) Gain from scenario 2

=0.5 ($ 99,00)

=$ 49,500=EV(E)

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b) Can Lucy be an expected utility maximizer if she tells you that she would not only

go to court but also reject gambles of winning or losing $50 with equal probability

for all wealth levels.

As observed in part (a), the expected utility for Lucy from getting off or scenario 1

is higher EV(G) than the alternate scenario, EV() or scenario 2. Hence, assuming

that Lucy is an utility maximizer, she would expectedly attend the court with the

expectation of getting off, therefore , her actions are guided by the expected utility

from both scenario. Consequently, she would go to court but still consider the

gamble of paying

5

go to court but also reject gambles of winning or losing $50 with equal probability

for all wealth levels.

As observed in part (a), the expected utility for Lucy from getting off or scenario 1

is higher EV(G) than the alternate scenario, EV() or scenario 2. Hence, assuming

that Lucy is an utility maximizer, she would expectedly attend the court with the

expectation of getting off, therefore , her actions are guided by the expected utility

from both scenario. Consequently, she would go to court but still consider the

gamble of paying

5

the fine or getting off as probability of both scenario are equal (50 %) and she can

be better off by getting off.

(c) Now suppose Lucy is behaving according to prospect theory and sees her current

wealth level as her reference point to which she evaluates changes. Draw a graph

with a value function that can explain Lucy’s choice to go to court. Clearly label the

wealth axis. Mark the expected valuation of going to court and the value of paying

the fine (assume that Lucy puts a probability weight of .5 on both winning and

losing in court).

Fig 2 above shows the gains/loss from both the scenario.

(d) In the same diagram show the expected valuation of the gamble of winning or

losing $50 with equal probability. Which feature of Prospect Theory is responsible

for Lucy rejecting the gamble?

6

be better off by getting off.

(c) Now suppose Lucy is behaving according to prospect theory and sees her current

wealth level as her reference point to which she evaluates changes. Draw a graph

with a value function that can explain Lucy’s choice to go to court. Clearly label the

wealth axis. Mark the expected valuation of going to court and the value of paying

the fine (assume that Lucy puts a probability weight of .5 on both winning and

losing in court).

Fig 2 above shows the gains/loss from both the scenario.

(d) In the same diagram show the expected valuation of the gamble of winning or

losing $50 with equal probability. Which feature of Prospect Theory is responsible

for Lucy rejecting the gamble?

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

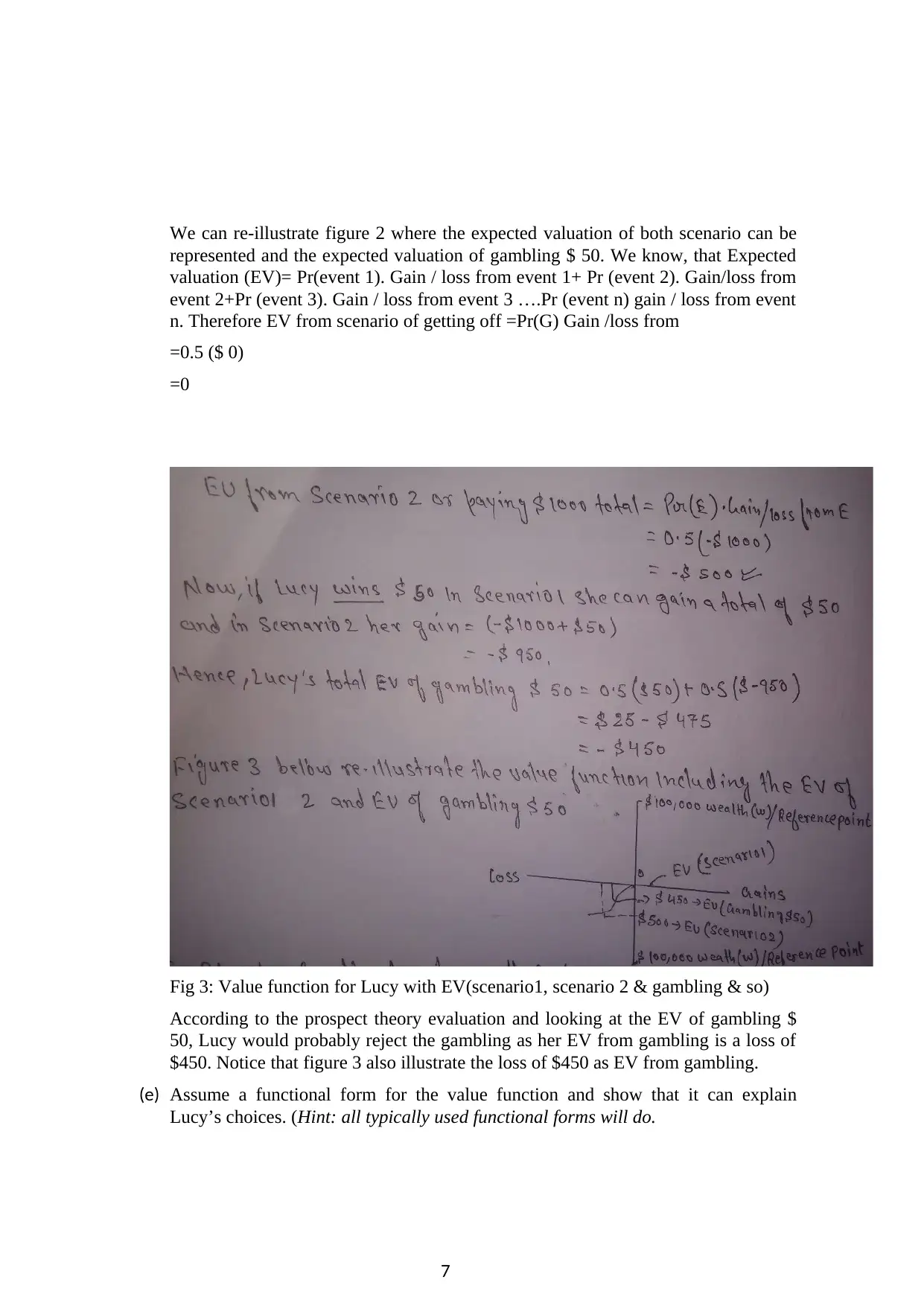

We can re-illustrate figure 2 where the expected valuation of both scenario can be

represented and the expected valuation of gambling $ 50. We know, that Expected

valuation (EV)= Pr(event 1). Gain / loss from event 1+ Pr (event 2). Gain/loss from

event 2+Pr (event 3). Gain / loss from event 3 ….Pr (event n) gain / loss from event

n. Therefore EV from scenario of getting off =Pr(G) Gain /loss from

=0.5 ($ 0)

=0

Fig 3: Value function for Lucy with EV(scenario1, scenario 2 & gambling & so)

According to the prospect theory evaluation and looking at the EV of gambling $

50, Lucy would probably reject the gambling as her EV from gambling is a loss of

$450. Notice that figure 3 also illustrate the loss of $450 as EV from gambling.

(e) Assume a functional form for the value function and show that it can explain

Lucy’s choices. (Hint: all typically used functional forms will do.

7

represented and the expected valuation of gambling $ 50. We know, that Expected

valuation (EV)= Pr(event 1). Gain / loss from event 1+ Pr (event 2). Gain/loss from

event 2+Pr (event 3). Gain / loss from event 3 ….Pr (event n) gain / loss from event

n. Therefore EV from scenario of getting off =Pr(G) Gain /loss from

=0.5 ($ 0)

=0

Fig 3: Value function for Lucy with EV(scenario1, scenario 2 & gambling & so)

According to the prospect theory evaluation and looking at the EV of gambling $

50, Lucy would probably reject the gambling as her EV from gambling is a loss of

$450. Notice that figure 3 also illustrate the loss of $450 as EV from gambling.

(e) Assume a functional form for the value function and show that it can explain

Lucy’s choices. (Hint: all typically used functional forms will do.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

We can write/express Lucy’s value function as:

V=Pr (G).Gain /loss from G (scenario)+Pr (E) Gain /loss from E(scenario 2) +Pr

(Gambling $ 50). Gain/loss from gambling $ 50.

Where E is the individual event, i=number of events r =gain/loss from the event.

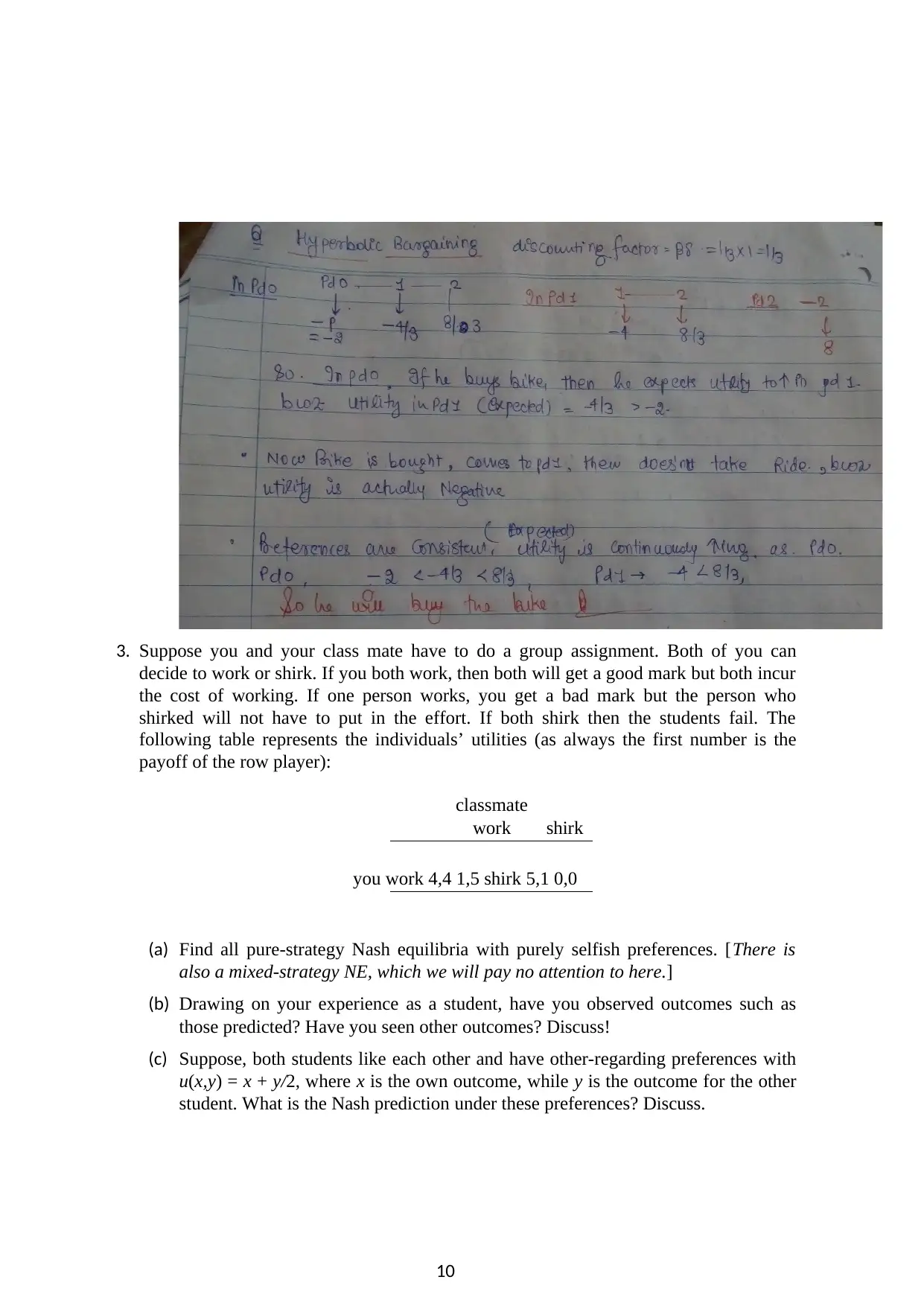

2. Suppose Tony is deciding on buying an expensive road bike. There are three periods:

Period 0 Tony decides to buy or not to buy the bike. The cost of the bike is equal to P

utility units. (u0(buy) = −P)

Period 1 If Tony has bought the bike, then he has to decide if he is going out for a ride.

If he goes for a ride, then his effort generates a utility cost of E units of utility.

(u1(ride) = −E)

Period 2 If Tony has bought a bike and has ridden on it, then a health benefit equivalent

to B utility units accrues. (u2(ride) = B)

(a) Suppose Tony does not discount future utility. Which choices will he take in

periods

0 and 1 if B > E + P? What will he do if B < E + P?

if B> E+P then Benefit is higher than total cost which makes a choice to buy a

bike feasible

if B<E+P then Benefit is less than total cost that makes buying bike isnt feasible

(b) Now suppose Tony is discounting future utility exponentially with a discount

factor of δ < 1 per period. Will Tony for any δ buy the bike and then not ride it?

Explain why or why not? (You do not have to calculate anything here yet. Use

your knowledge about how exponential discounters behave instead.)

P is the utility in time period 0

\delta B+\delta ^2 E this is discounted payoff in period 1 and 2 respectively

To buy or not to buy is indifferent we have

P=\delta B+\delta ^2 E

-\delta B+\delta ^2 E-P=0

\delta ^2 +\delta B/E-P/E=0

8

V=Pr (G).Gain /loss from G (scenario)+Pr (E) Gain /loss from E(scenario 2) +Pr

(Gambling $ 50). Gain/loss from gambling $ 50.

Where E is the individual event, i=number of events r =gain/loss from the event.

2. Suppose Tony is deciding on buying an expensive road bike. There are three periods:

Period 0 Tony decides to buy or not to buy the bike. The cost of the bike is equal to P

utility units. (u0(buy) = −P)

Period 1 If Tony has bought the bike, then he has to decide if he is going out for a ride.

If he goes for a ride, then his effort generates a utility cost of E units of utility.

(u1(ride) = −E)

Period 2 If Tony has bought a bike and has ridden on it, then a health benefit equivalent

to B utility units accrues. (u2(ride) = B)

(a) Suppose Tony does not discount future utility. Which choices will he take in

periods

0 and 1 if B > E + P? What will he do if B < E + P?

if B> E+P then Benefit is higher than total cost which makes a choice to buy a

bike feasible

if B<E+P then Benefit is less than total cost that makes buying bike isnt feasible

(b) Now suppose Tony is discounting future utility exponentially with a discount

factor of δ < 1 per period. Will Tony for any δ buy the bike and then not ride it?

Explain why or why not? (You do not have to calculate anything here yet. Use

your knowledge about how exponential discounters behave instead.)

P is the utility in time period 0

\delta B+\delta ^2 E this is discounted payoff in period 1 and 2 respectively

To buy or not to buy is indifferent we have

P=\delta B+\delta ^2 E

-\delta B+\delta ^2 E-P=0

\delta ^2 +\delta B/E-P/E=0

8

\delta = (-B/E)+sqrt(B^2/E^2+4P/E)/2<1

if \delta>sqrt(B^2/E^2+4P/E) then we can say buying a bike is feasible otherwise

not

(c) Suppose Tony has a discount factor and P = 2, E = 4 and B = 8. What is he

going to do in periods 0 and 1? P=2, E=4 and B=8

P+

Hence 42/9>32/9 ie Cost is higher than Benefit therefore buying a bike is not a

good option

(d) Is it possible that Tony for some values of B,E,P buys the bike and then does

not ride it if he is a naive quasi-hyperbolic discounter. Give an intuition for why or

why not instead of calculating.

Yes it is possible if discounting rate stands at 0 then he will not wait for benefits to

be earned in period 2 because then present worth of B will be less and each time

so B < P+E

(e) What if he is a sophisticated quasi-hyperbolic discounter? Explain.

No. it is not possible if discounting rate stands at 0 then he will not wait for

benefits to be earned in period 2 because then present worth of B will be less and

each time so B < P+E

(f) Suppose Tony is naive and absolutely patient in the long term (δ = 1) but has a

severe present bias ( ). Assume again P = 2, E = 4 and B = 8. Is he in

period 0 expecting to ride in period 1 if he buys the bike? Is he actually going to

ride if he has bought a bike and arrives at period 1? Is he going to buy the bike?

9

if \delta>sqrt(B^2/E^2+4P/E) then we can say buying a bike is feasible otherwise

not

(c) Suppose Tony has a discount factor and P = 2, E = 4 and B = 8. What is he

going to do in periods 0 and 1? P=2, E=4 and B=8

P+

Hence 42/9>32/9 ie Cost is higher than Benefit therefore buying a bike is not a

good option

(d) Is it possible that Tony for some values of B,E,P buys the bike and then does

not ride it if he is a naive quasi-hyperbolic discounter. Give an intuition for why or

why not instead of calculating.

Yes it is possible if discounting rate stands at 0 then he will not wait for benefits to

be earned in period 2 because then present worth of B will be less and each time

so B < P+E

(e) What if he is a sophisticated quasi-hyperbolic discounter? Explain.

No. it is not possible if discounting rate stands at 0 then he will not wait for

benefits to be earned in period 2 because then present worth of B will be less and

each time so B < P+E

(f) Suppose Tony is naive and absolutely patient in the long term (δ = 1) but has a

severe present bias ( ). Assume again P = 2, E = 4 and B = 8. Is he in

period 0 expecting to ride in period 1 if he buys the bike? Is he actually going to

ride if he has bought a bike and arrives at period 1? Is he going to buy the bike?

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Suppose you and your class mate have to do a group assignment. Both of you can

decide to work or shirk. If you both work, then both will get a good mark but both incur

the cost of working. If one person works, you get a bad mark but the person who

shirked will not have to put in the effort. If both shirk then the students fail. The

following table represents the individuals’ utilities (as always the first number is the

payoff of the row player):

classmate

work shirk

you work 4,4 1,5 shirk 5,1 0,0

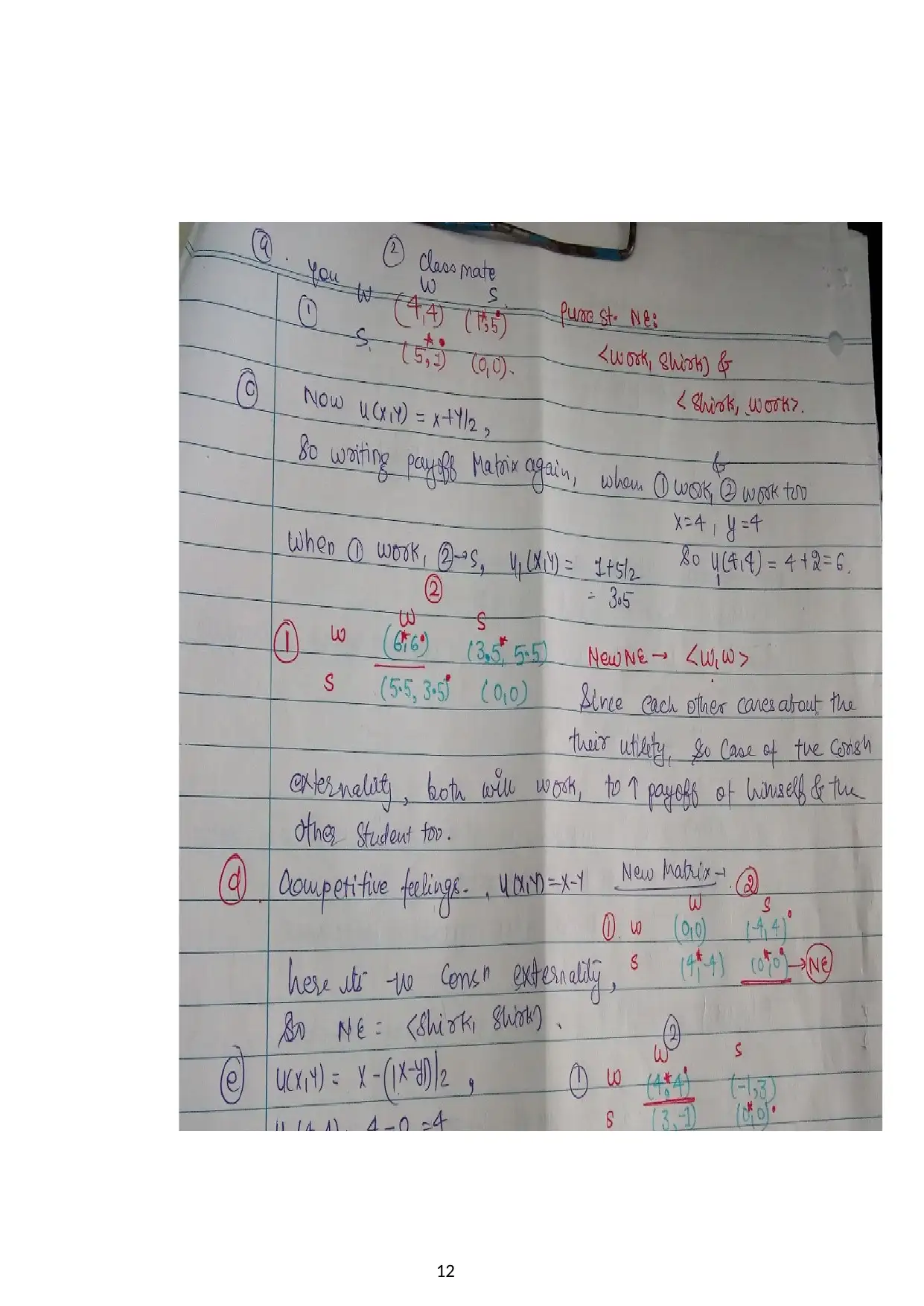

(a) Find all pure-strategy Nash equilibria with purely selfish preferences. [There is

also a mixed-strategy NE, which we will pay no attention to here.]

(b) Drawing on your experience as a student, have you observed outcomes such as

those predicted? Have you seen other outcomes? Discuss!

(c) Suppose, both students like each other and have other-regarding preferences with

u(x,y) = x + y/2, where x is the own outcome, while y is the outcome for the other

student. What is the Nash prediction under these preferences? Discuss.

10

decide to work or shirk. If you both work, then both will get a good mark but both incur

the cost of working. If one person works, you get a bad mark but the person who

shirked will not have to put in the effort. If both shirk then the students fail. The

following table represents the individuals’ utilities (as always the first number is the

payoff of the row player):

classmate

work shirk

you work 4,4 1,5 shirk 5,1 0,0

(a) Find all pure-strategy Nash equilibria with purely selfish preferences. [There is

also a mixed-strategy NE, which we will pay no attention to here.]

(b) Drawing on your experience as a student, have you observed outcomes such as

those predicted? Have you seen other outcomes? Discuss!

(c) Suppose, both students like each other and have other-regarding preferences with

u(x,y) = x + y/2, where x is the own outcome, while y is the outcome for the other

student. What is the Nash prediction under these preferences? Discuss.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(d) Suppose, both students have competitive preferences and care only about how

much better or worse off they are compared to the other student. In other words,

u(x,y) = x − y for both students. What is the Nash prediction now! Discuss.

(e) Suppose both students are inequality averse and lose half a unit of utility for each

unit difference in payoffs. In other words u(x,y) = x−(|x−y|)/2. Find all pure-

strategy Nash equilibria and discuss

All the answers for question a, b, c, d, e,f are provided below

11

much better or worse off they are compared to the other student. In other words,

u(x,y) = x − y for both students. What is the Nash prediction now! Discuss.

(e) Suppose both students are inequality averse and lose half a unit of utility for each

unit difference in payoffs. In other words u(x,y) = x−(|x−y|)/2. Find all pure-

strategy Nash equilibria and discuss

All the answers for question a, b, c, d, e,f are provided below

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.