Financial Analysis Report: Belgravia Hotels Finance

VerifiedAdded on 2020/12/09

|15

|4200

|57

Report

AI Summary

This finance report provides a comprehensive analysis of Belgravia Hotels, a UK-based hospitality company. The report begins by exploring the various sources of funds available to the company, including bank loans and the sale of assets. It then delves into the different methods of generating income, such as grants, sales, sponsorships, and sub-letting. The report also examines the elements of cost, including labor, overheads, and materials, and discusses the role of setting selling prices. Furthermore, it analyzes methods for controlling stock and cash, such as FIFO and contingency planning. The structure and sources of the trial balance are also discussed, along with an evaluation of the company's income statement and balance sheet, including adjusting entries. The report covers the process and purpose of budgetary control and analyzes variances from budgeted and actual figures. Finally, it includes a calculation and analysis of financial ratios and provides recommendations on appropriate future management strategies, concluding with an analysis of cost categorization, contribution per product, and short-term management decisions.

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of funds available for business and service industry..........................................1

1.2 Evaluation of contribution made by range of methods of generating income.................2

TASK 2............................................................................................................................................3

2.1 Elements of cost, gross profit percentages and selling prices for products and services. 3

2.2 Methods of controlling stock and cash in a business and service environment...............3

TASK 3............................................................................................................................................5

3.1 Sources and structure of trial balance...............................................................................5

3.2 Evaluation of business accounts, adjustments and notes..................................................6

3.3 Process and purpose of budgetary control........................................................................8

3.4 Analysis of variances from budgeted and actual figures..................................................8

TASK 4............................................................................................................................................9

4.1 Calculation and analysis of all ratios................................................................................9

4.2 Recommendation on appropriate future management strategies....................................10

TASK 5..........................................................................................................................................10

5.1 Categorisation of costs as fixed, variable and semi variable..........................................10

5.2 Calculation of contribution per product and explanation of cost/ profit/ volume

relationship...........................................................................................................................11

5.3 Justification of short term management decisions..........................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of funds available for business and service industry..........................................1

1.2 Evaluation of contribution made by range of methods of generating income.................2

TASK 2............................................................................................................................................3

2.1 Elements of cost, gross profit percentages and selling prices for products and services. 3

2.2 Methods of controlling stock and cash in a business and service environment...............3

TASK 3............................................................................................................................................5

3.1 Sources and structure of trial balance...............................................................................5

3.2 Evaluation of business accounts, adjustments and notes..................................................6

3.3 Process and purpose of budgetary control........................................................................8

3.4 Analysis of variances from budgeted and actual figures..................................................8

TASK 4............................................................................................................................................9

4.1 Calculation and analysis of all ratios................................................................................9

4.2 Recommendation on appropriate future management strategies....................................10

TASK 5..........................................................................................................................................10

5.1 Categorisation of costs as fixed, variable and semi variable..........................................10

5.2 Calculation of contribution per product and explanation of cost/ profit/ volume

relationship...........................................................................................................................11

5.3 Justification of short term management decisions..........................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Finance can be defined as the element which is the main requirement of a business entity

to operate a business successfully. If an organisation is not having appropriate funds than it is not

possible to perform operational and executional activities of business. It can be raised from

different sources like investments, equities, bank loan, overdrafts etc. Hospitality industry is

concerned with rendering services to the clients (del Mar Alonso-Almeida and Bremser, 2013). It

is essential for the sector to render good quality services to the customers so that large market

share can be captured. Main aim of this report is to analyse the sources of funds that are required

to an organisation for operating business within hospitality industry. The organisation which is

chosen for this report is Belgravia Hotels who is operating in lodging, contract services and

restaurants. This business entity based in UK and operating business there successfully. In this

assignment different topics are discussed including sources of funds and income, understanding

the business in terms of the elements of cost and evaluation of business accounts. Analysis of

business performance and application of the concept of marginal costing are also covered under

this report.

TASK 1

1.1 Sources of funds available for business and service industry

A UK based hospitality company Belgravia Hotels operates in different sectors including

lodging, contract services and restaurants. Now the hotel is willing to be developed and enhance

position of all its divisions. For this purpose, three different goals are decided by the

organisation. All of them are as follows:

Make investments in such projects that increase shareholder’s values (Vasquez, 2014).

Manage assets of the organisation.

Improve decision making so that profits can be enhanced.

To achieve all the above described objectives organisation needs to have sufficient funds

that can be acquired from following sources:

Sources of funds: These are the funds that are required by an organisation in order to

execute business. There are various types of sources that are helpful for Belgravia Hotels in

operating their business are discussed below:

1

Finance can be defined as the element which is the main requirement of a business entity

to operate a business successfully. If an organisation is not having appropriate funds than it is not

possible to perform operational and executional activities of business. It can be raised from

different sources like investments, equities, bank loan, overdrafts etc. Hospitality industry is

concerned with rendering services to the clients (del Mar Alonso-Almeida and Bremser, 2013). It

is essential for the sector to render good quality services to the customers so that large market

share can be captured. Main aim of this report is to analyse the sources of funds that are required

to an organisation for operating business within hospitality industry. The organisation which is

chosen for this report is Belgravia Hotels who is operating in lodging, contract services and

restaurants. This business entity based in UK and operating business there successfully. In this

assignment different topics are discussed including sources of funds and income, understanding

the business in terms of the elements of cost and evaluation of business accounts. Analysis of

business performance and application of the concept of marginal costing are also covered under

this report.

TASK 1

1.1 Sources of funds available for business and service industry

A UK based hospitality company Belgravia Hotels operates in different sectors including

lodging, contract services and restaurants. Now the hotel is willing to be developed and enhance

position of all its divisions. For this purpose, three different goals are decided by the

organisation. All of them are as follows:

Make investments in such projects that increase shareholder’s values (Vasquez, 2014).

Manage assets of the organisation.

Improve decision making so that profits can be enhanced.

To achieve all the above described objectives organisation needs to have sufficient funds

that can be acquired from following sources:

Sources of funds: These are the funds that are required by an organisation in order to

execute business. There are various types of sources that are helpful for Belgravia Hotels in

operating their business are discussed below:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bank loan: It is the most common source of fund which can be adopted by Belgravia

Hotels in order to develop its business. Bank requires a collateral security from the

borrower subject to borrowed loan. Bank may have sold the asset and recover all the

amount of loan, if the money is not received on time. Borrower have to pay an interest on

the loan on a fixed rate for a fix period (Papargyropoulou and et.al., 2016). Selling old and unusable assets: This is the another option which can be used by

Belgravia Hotels in order to get funds for the future development of the organisation.

When a company is having some old assets that cannot be used for business purpose than

these can be sold to raise funds. Acquired finance can be used for enterprise's perspective.

Both the above described options of sources of funds can be used by Belgravia Hotels in

order to enhance position of all the divisions of the company.

1.2 Evaluation of contribution made by range of methods of generating income

For every business like Belgravia Hotels there are various methods that helps to generate

incomes all of them are described below:

Grants: These are the non-repayable funds that are provided by one party to another.

Belgravia Hotels can generate funds from grants by acquiring them from external parties like

government, trusts and corporations etc.

Sales: It is the main source of generating income in which services are delivered to the

clients in order to increase sales. Higher incomes can be acquired by Belgravia Hotels by selling

or rendering good quality services to the customers (Wood, 2013).

Sponsorship: It can be defined as the financial support which provided by sponsors to an

organisation. Belgravia Hotels can generate income from sponsors by attracting them through

impressive presentation of business plan. If the company is having higher number of sponsors

than higher income can be acquired from them.

Sub-letting: It can be defined as the process of letting a business concern to other

outsider parties. Belgravia Hotels can generate income by letting some parts of the hotel to

externals. It will help to increase overall income of the organisation.

All the above described methods are used to generate income from different sources so

that business can be developed and all the divisions can be enhanced.

TASK 2

2

Hotels in order to develop its business. Bank requires a collateral security from the

borrower subject to borrowed loan. Bank may have sold the asset and recover all the

amount of loan, if the money is not received on time. Borrower have to pay an interest on

the loan on a fixed rate for a fix period (Papargyropoulou and et.al., 2016). Selling old and unusable assets: This is the another option which can be used by

Belgravia Hotels in order to get funds for the future development of the organisation.

When a company is having some old assets that cannot be used for business purpose than

these can be sold to raise funds. Acquired finance can be used for enterprise's perspective.

Both the above described options of sources of funds can be used by Belgravia Hotels in

order to enhance position of all the divisions of the company.

1.2 Evaluation of contribution made by range of methods of generating income

For every business like Belgravia Hotels there are various methods that helps to generate

incomes all of them are described below:

Grants: These are the non-repayable funds that are provided by one party to another.

Belgravia Hotels can generate funds from grants by acquiring them from external parties like

government, trusts and corporations etc.

Sales: It is the main source of generating income in which services are delivered to the

clients in order to increase sales. Higher incomes can be acquired by Belgravia Hotels by selling

or rendering good quality services to the customers (Wood, 2013).

Sponsorship: It can be defined as the financial support which provided by sponsors to an

organisation. Belgravia Hotels can generate income from sponsors by attracting them through

impressive presentation of business plan. If the company is having higher number of sponsors

than higher income can be acquired from them.

Sub-letting: It can be defined as the process of letting a business concern to other

outsider parties. Belgravia Hotels can generate income by letting some parts of the hotel to

externals. It will help to increase overall income of the organisation.

All the above described methods are used to generate income from different sources so

that business can be developed and all the divisions can be enhanced.

TASK 2

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.1 Elements of cost, gross profit percentages and selling prices for products and services

Cost: It can be defined as the combination of the expenses that are faced by Belgravia

Hotels in order to deliver services to the customers (Elements of cost, 2018). All the elements of

cost that may take place for Belgravia Hotels are described below:

Labour: These are the persons who are used in service industry to deliver services. In

case of Belgravia Hotels labours can be defies as waiters, managers, security staff,

cleaning staff etc. it is not possible to operate business without labour as they are

concerned with the delivery system of services (Detotto, Pulina and Brida, 2014).

Overheads: These are the expenses that may take place while services are delivered to

the clients. In Belgravia Hotels various overheads can take place while rendering services

to the visitors or to operate organisational activities. It includes rent, legal fees, supplies,

taxes and advertisement expenses.

Material: It is the material which is used by service industry to deliver their services. In

Belgravia Hotels the material that are utilised to render services are food items, beverages

etc.

Role of setting selling price: Prices in service sector are decided according to the cost

which has been faced by the organisation. If the price is not set according to the cost by

Belgravia Hotels appropriately than it would not be able to attract large number of clients. If the

delivered product is not suitable than they will not get attracted towards the hotel. In Belgravia

Hotels price is set by the managers according to the expenses, material and employees cost

which is involved in each service. It helps to set right or proper price that result in higher profits

as it is affordable for the customers (Harms, Memili and Steeger, 2015).

2.2 Methods of controlling stock and cash in a business and service environment

For all the business entities it is very important to control stock and cash so that business

can be operated in appropriate manner. Following are the methods that are used by Belgravia

Hotels in order to control its inventory and monetary resources:

FIFO (First in First out): This method is mainly used to appropriately utilise the

inventory which is used to deliver services to the customers. In this technique earlier received

stock is used to render services first. In Belgravia Hotels, FIFO is used as it can help to manage

the inventory and save funds by using old material first for services.

3

Cost: It can be defined as the combination of the expenses that are faced by Belgravia

Hotels in order to deliver services to the customers (Elements of cost, 2018). All the elements of

cost that may take place for Belgravia Hotels are described below:

Labour: These are the persons who are used in service industry to deliver services. In

case of Belgravia Hotels labours can be defies as waiters, managers, security staff,

cleaning staff etc. it is not possible to operate business without labour as they are

concerned with the delivery system of services (Detotto, Pulina and Brida, 2014).

Overheads: These are the expenses that may take place while services are delivered to

the clients. In Belgravia Hotels various overheads can take place while rendering services

to the visitors or to operate organisational activities. It includes rent, legal fees, supplies,

taxes and advertisement expenses.

Material: It is the material which is used by service industry to deliver their services. In

Belgravia Hotels the material that are utilised to render services are food items, beverages

etc.

Role of setting selling price: Prices in service sector are decided according to the cost

which has been faced by the organisation. If the price is not set according to the cost by

Belgravia Hotels appropriately than it would not be able to attract large number of clients. If the

delivered product is not suitable than they will not get attracted towards the hotel. In Belgravia

Hotels price is set by the managers according to the expenses, material and employees cost

which is involved in each service. It helps to set right or proper price that result in higher profits

as it is affordable for the customers (Harms, Memili and Steeger, 2015).

2.2 Methods of controlling stock and cash in a business and service environment

For all the business entities it is very important to control stock and cash so that business

can be operated in appropriate manner. Following are the methods that are used by Belgravia

Hotels in order to control its inventory and monetary resources:

FIFO (First in First out): This method is mainly used to appropriately utilise the

inventory which is used to deliver services to the customers. In this technique earlier received

stock is used to render services first. In Belgravia Hotels, FIFO is used as it can help to manage

the inventory and save funds by using old material first for services.

3

Cost: The cost for this method is very low as it does not require a skilled accountant to

keep appropriate record of the inventory because it is an easy and simple technique. The

organisation will not have to pay extra cost to the use this method.

Benefits: It is very simple method hence it will not create complexities for the managers

and also help to analyse accurate result (Singal, 2014).

Contingency planning: It is a technique which is used by the organisations to plan for

future complexities that may take place. In Belgravia Hotels this method is used by the managers

in order to manage its stock and cash because it can help to make plan so that future

consequences may not result in loss of cash and stock.

Cost: This technique does not cost for the company as it is done by the managers.

Benefits: It is very beneficial for the company as it can help to forecast possible future

events that can affect the organisation negatively. The managers may plan inn advance to

resolve all the problems so that it won’t harm the organisation in future.

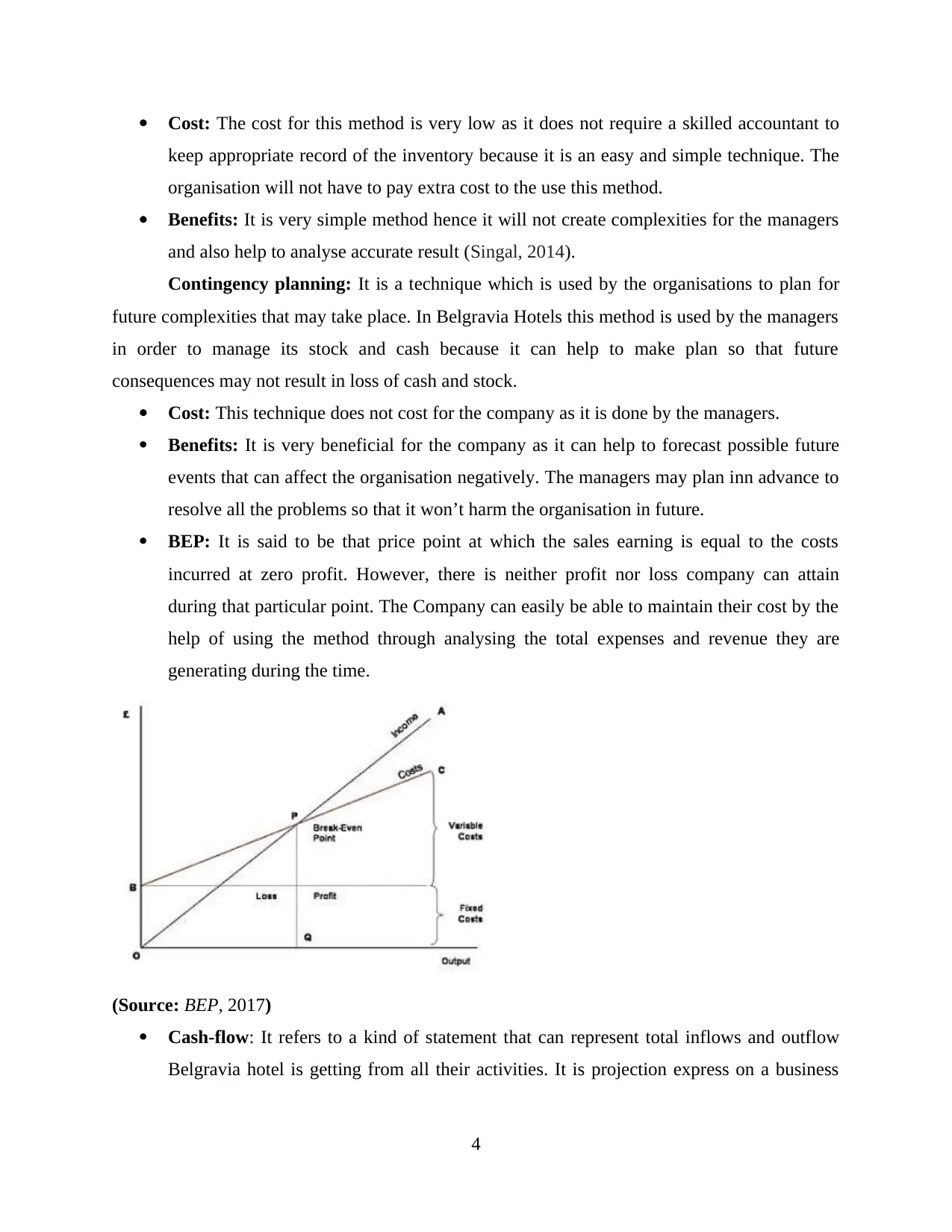

BEP: It is said to be that price point at which the sales earning is equal to the costs

incurred at zero profit. However, there is neither profit nor loss company can attain

during that particular point. The Company can easily be able to maintain their cost by the

help of using the method through analysing the total expenses and revenue they are

generating during the time.

(Source: BEP, 2017)

Cash-flow: It refers to a kind of statement that can represent total inflows and outflow

Belgravia hotel is getting from all their activities. It is projection express on a business

4

keep appropriate record of the inventory because it is an easy and simple technique. The

organisation will not have to pay extra cost to the use this method.

Benefits: It is very simple method hence it will not create complexities for the managers

and also help to analyse accurate result (Singal, 2014).

Contingency planning: It is a technique which is used by the organisations to plan for

future complexities that may take place. In Belgravia Hotels this method is used by the managers

in order to manage its stock and cash because it can help to make plan so that future

consequences may not result in loss of cash and stock.

Cost: This technique does not cost for the company as it is done by the managers.

Benefits: It is very beneficial for the company as it can help to forecast possible future

events that can affect the organisation negatively. The managers may plan inn advance to

resolve all the problems so that it won’t harm the organisation in future.

BEP: It is said to be that price point at which the sales earning is equal to the costs

incurred at zero profit. However, there is neither profit nor loss company can attain

during that particular point. The Company can easily be able to maintain their cost by the

help of using the method through analysing the total expenses and revenue they are

generating during the time.

(Source: BEP, 2017)

Cash-flow: It refers to a kind of statement that can represent total inflows and outflow

Belgravia hotel is getting from all their activities. It is projection express on a business

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

outcomes or plan in terms of cash in an out of the business without adjusting for accrued

revenue and expenses.

TASK 3

3.1 Sources and structure of trial balance

Trial balance: It is a statement which is formed by accountants of the organisation in

order to record all the credit and debit balances of different ledger accounts. In Belgravia Hotels

trial balance is formed to analyse that all the transactions that are recorded in ledger and journal.

Source for trial balance: All the ledger accounts that have credit or debit balance are the

sources for trial balance as it can help to form it in appropriate manner. Different accounts that

are recorded in trial balance are revenues, incomes, capital, assets and liabilities. Assets and

expenses have debut balance and liabilities, equities and revenues have credit balance

(Stephenson, 2014).

Structure of trial balance:

Particular Debit amount Credit amount

Cash and cash equillents Xxx

Bills receivables Xxx

Building Xxx

Machine Xxx

Rent Xxx

Wages and salaries Xxx

Legal fees Xxx

Bank loan Xxx

Bills payables Xxx

Stocks Xxx Xxx

Consulting earnings Xxx

TOTAL Xxx Xxx

3.2 Evaluation of business accounts, adjustments and notes

Business accounts of an organisation includes income statement and balance sheet. Both

the statements of Belgravia Hotels are as follows:

Income statement:

5

revenue and expenses.

TASK 3

3.1 Sources and structure of trial balance

Trial balance: It is a statement which is formed by accountants of the organisation in

order to record all the credit and debit balances of different ledger accounts. In Belgravia Hotels

trial balance is formed to analyse that all the transactions that are recorded in ledger and journal.

Source for trial balance: All the ledger accounts that have credit or debit balance are the

sources for trial balance as it can help to form it in appropriate manner. Different accounts that

are recorded in trial balance are revenues, incomes, capital, assets and liabilities. Assets and

expenses have debut balance and liabilities, equities and revenues have credit balance

(Stephenson, 2014).

Structure of trial balance:

Particular Debit amount Credit amount

Cash and cash equillents Xxx

Bills receivables Xxx

Building Xxx

Machine Xxx

Rent Xxx

Wages and salaries Xxx

Legal fees Xxx

Bank loan Xxx

Bills payables Xxx

Stocks Xxx Xxx

Consulting earnings Xxx

TOTAL Xxx Xxx

3.2 Evaluation of business accounts, adjustments and notes

Business accounts of an organisation includes income statement and balance sheet. Both

the statements of Belgravia Hotels are as follows:

Income statement:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

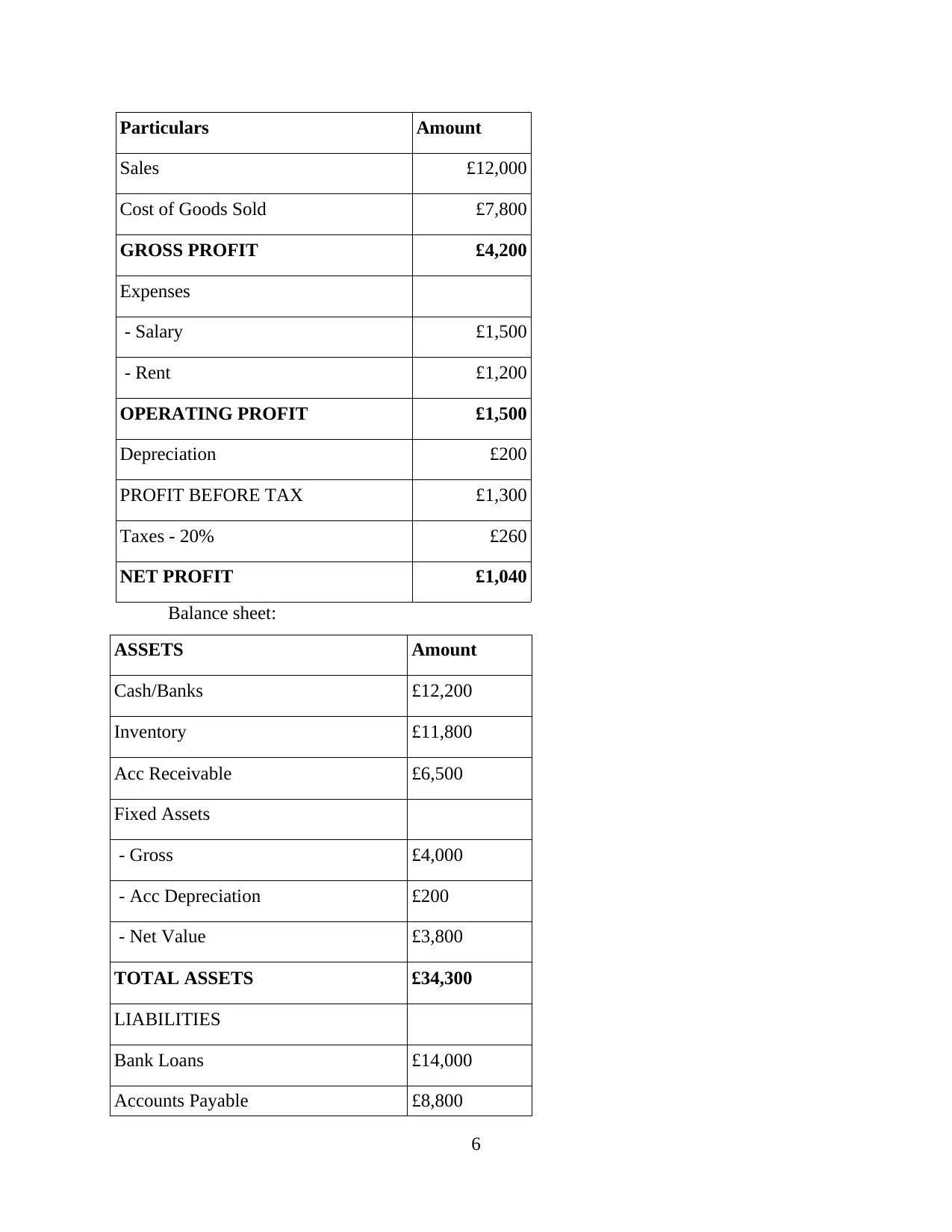

Particulars Amount

Sales £12,000

Cost of Goods Sold £7,800

GROSS PROFIT £4,200

Expenses

- Salary £1,500

- Rent £1,200

OPERATING PROFIT £1,500

Depreciation £200

PROFIT BEFORE TAX £1,300

Taxes - 20% £260

NET PROFIT £1,040

Balance sheet:

ASSETS Amount

Cash/Banks £12,200

Inventory £11,800

Acc Receivable £6,500

Fixed Assets

- Gross £4,000

- Acc Depreciation £200

- Net Value £3,800

TOTAL ASSETS £34,300

LIABILITIES

Bank Loans £14,000

Accounts Payable £8,800

6

Sales £12,000

Cost of Goods Sold £7,800

GROSS PROFIT £4,200

Expenses

- Salary £1,500

- Rent £1,200

OPERATING PROFIT £1,500

Depreciation £200

PROFIT BEFORE TAX £1,300

Taxes - 20% £260

NET PROFIT £1,040

Balance sheet:

ASSETS Amount

Cash/Banks £12,200

Inventory £11,800

Acc Receivable £6,500

Fixed Assets

- Gross £4,000

- Acc Depreciation £200

- Net Value £3,800

TOTAL ASSETS £34,300

LIABILITIES

Bank Loans £14,000

Accounts Payable £8,800

6

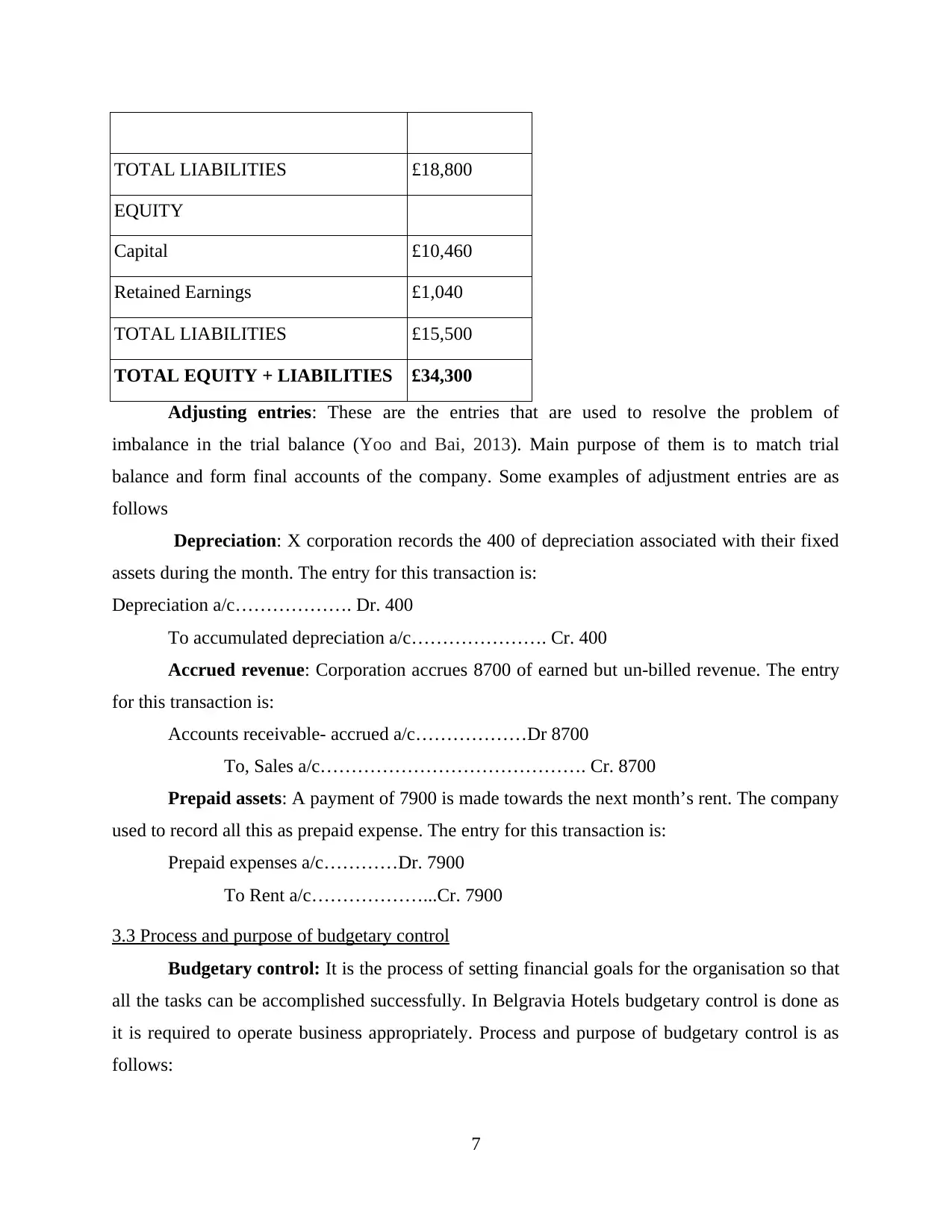

TOTAL LIABILITIES £18,800

EQUITY

Capital £10,460

Retained Earnings £1,040

TOTAL LIABILITIES £15,500

TOTAL EQUITY + LIABILITIES £34,300

Adjusting entries: These are the entries that are used to resolve the problem of

imbalance in the trial balance (Yoo and Bai, 2013). Main purpose of them is to match trial

balance and form final accounts of the company. Some examples of adjustment entries are as

follows

Depreciation: X corporation records the 400 of depreciation associated with their fixed

assets during the month. The entry for this transaction is:

Depreciation a/c………………. Dr. 400

To accumulated depreciation a/c…………………. Cr. 400

Accrued revenue: Corporation accrues 8700 of earned but un-billed revenue. The entry

for this transaction is:

Accounts receivable- accrued a/c………………Dr 8700

To, Sales a/c……………………………………. Cr. 8700

Prepaid assets: A payment of 7900 is made towards the next month’s rent. The company

used to record all this as prepaid expense. The entry for this transaction is:

Prepaid expenses a/c…………Dr. 7900

To Rent a/c………………...Cr. 7900

3.3 Process and purpose of budgetary control

Budgetary control: It is the process of setting financial goals for the organisation so that

all the tasks can be accomplished successfully. In Belgravia Hotels budgetary control is done as

it is required to operate business appropriately. Process and purpose of budgetary control is as

follows:

7

EQUITY

Capital £10,460

Retained Earnings £1,040

TOTAL LIABILITIES £15,500

TOTAL EQUITY + LIABILITIES £34,300

Adjusting entries: These are the entries that are used to resolve the problem of

imbalance in the trial balance (Yoo and Bai, 2013). Main purpose of them is to match trial

balance and form final accounts of the company. Some examples of adjustment entries are as

follows

Depreciation: X corporation records the 400 of depreciation associated with their fixed

assets during the month. The entry for this transaction is:

Depreciation a/c………………. Dr. 400

To accumulated depreciation a/c…………………. Cr. 400

Accrued revenue: Corporation accrues 8700 of earned but un-billed revenue. The entry

for this transaction is:

Accounts receivable- accrued a/c………………Dr 8700

To, Sales a/c……………………………………. Cr. 8700

Prepaid assets: A payment of 7900 is made towards the next month’s rent. The company

used to record all this as prepaid expense. The entry for this transaction is:

Prepaid expenses a/c…………Dr. 7900

To Rent a/c………………...Cr. 7900

3.3 Process and purpose of budgetary control

Budgetary control: It is the process of setting financial goals for the organisation so that

all the tasks can be accomplished successfully. In Belgravia Hotels budgetary control is done as

it is required to operate business appropriately. Process and purpose of budgetary control is as

follows:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Process of budgetary control: The process which is followed by the accountants of

Belgravia Hotels for budgetary control is as follows:

Preparing the budget: First of all, a budget is prepared by the managers and accountant

of the company in which all the incomes and expenses of future are recorded.

Communicating the budget: In next step the budget is communicated to the higher

authority of the organisation for their approval. When their approval is marked then it is

implemented within the organisation (Chen, 2012).

Measuring results: In this process the results for the implementation are measured by

the managers so that it can be analysed that it is implemented properly or not.

Comparison of results: In this stage the budget is compared with prior years to

determine that organisation is performing well or not.

Reporting and taking collective actions: In this stage analysed results of comparison

are presented in front of top management and ask them to take appropriate action if the

performance of the company is not good.

Purpose of budgetary control:

Main purpose of budgetary control is to control the overspending of the organisation is

order to save monetary funds for contingencies.

Budgetary control is conducted to successfully operate the business in limited resources

to enhance the performance.

3.4 Analysis of variances from budgeted and actual figures

Variances: It can be defined as the comparison of actual and budgeted results of the

organisation. The main purpose of the variances is to determine that organisation have attained

growth in current year or not. In Belgravia Hotels variances are calculated to enhance

performance by comparing actual and standard figures (Pacheco and Tavares, 2017). A

calculation of material and labour variance for Belgravia Hotels is as follows:

Actual units sold= 1500 Actual selling price= 50

Budgeted Units= 1800 Budgeted selling price= 40

Actual labour hours= 400 Per hour rate= 100

budgeted labour hours= 500 Per hour rate= 80

Calculation of variances:

Material cost variance= Total standard cost- total actual cost

8

Belgravia Hotels for budgetary control is as follows:

Preparing the budget: First of all, a budget is prepared by the managers and accountant

of the company in which all the incomes and expenses of future are recorded.

Communicating the budget: In next step the budget is communicated to the higher

authority of the organisation for their approval. When their approval is marked then it is

implemented within the organisation (Chen, 2012).

Measuring results: In this process the results for the implementation are measured by

the managers so that it can be analysed that it is implemented properly or not.

Comparison of results: In this stage the budget is compared with prior years to

determine that organisation is performing well or not.

Reporting and taking collective actions: In this stage analysed results of comparison

are presented in front of top management and ask them to take appropriate action if the

performance of the company is not good.

Purpose of budgetary control:

Main purpose of budgetary control is to control the overspending of the organisation is

order to save monetary funds for contingencies.

Budgetary control is conducted to successfully operate the business in limited resources

to enhance the performance.

3.4 Analysis of variances from budgeted and actual figures

Variances: It can be defined as the comparison of actual and budgeted results of the

organisation. The main purpose of the variances is to determine that organisation have attained

growth in current year or not. In Belgravia Hotels variances are calculated to enhance

performance by comparing actual and standard figures (Pacheco and Tavares, 2017). A

calculation of material and labour variance for Belgravia Hotels is as follows:

Actual units sold= 1500 Actual selling price= 50

Budgeted Units= 1800 Budgeted selling price= 40

Actual labour hours= 400 Per hour rate= 100

budgeted labour hours= 500 Per hour rate= 80

Calculation of variances:

Material cost variance= Total standard cost- total actual cost

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= (1800*40) -(1500*50)

=72000-75000

= -3000(A)

Labour usage variance= Total standard hours- Total actual hours

= (400*100) -(500*70)

=40000-35000

=5000(F)

From the above variances, it can be analysed that MCV of the organisation is adverse and

LUV is favourable which means the organisation needs to control all its resources that are

involved in material. It is suggested to the managers of Belgravia Hotels to reduce the usage of

resources.

TASK 4

4.1 Calculation and analysis of all ratios

Ratio analysis: It can be defined as the process of analysing different ratios of an

organisation in order to analyse that organisation is performing well or not. Some important

ratios that are calculated for Belgravia Hotels are as follows:

Name Formula Calculation

Current ratio Current assets/ current

liabilities

30500/8800= 3.47

Quick ratio Quick assets/ current liabilities 18700/8800= 2.13

Net profit ratio Net profit/ sales*100 1040/12000*100=8.67%

Gross profit ratio Gross profit/ sales*100 4200/12000*100=35%

Debt equity ratio Debts/equities 18800/15500=1.21

From the above calculations it has been analysed that organisation is having good

liquidity condition which has resulted in a high current and quick ratios. Net profits and gross

profit ratio of the organisation is also very high which means that it is having good profitability.

Debt equity ratio of the company is 1.21 which is lower than ideal ratio. The business entity is

suggested to use external funds more than internal funds.

9

=72000-75000

= -3000(A)

Labour usage variance= Total standard hours- Total actual hours

= (400*100) -(500*70)

=40000-35000

=5000(F)

From the above variances, it can be analysed that MCV of the organisation is adverse and

LUV is favourable which means the organisation needs to control all its resources that are

involved in material. It is suggested to the managers of Belgravia Hotels to reduce the usage of

resources.

TASK 4

4.1 Calculation and analysis of all ratios

Ratio analysis: It can be defined as the process of analysing different ratios of an

organisation in order to analyse that organisation is performing well or not. Some important

ratios that are calculated for Belgravia Hotels are as follows:

Name Formula Calculation

Current ratio Current assets/ current

liabilities

30500/8800= 3.47

Quick ratio Quick assets/ current liabilities 18700/8800= 2.13

Net profit ratio Net profit/ sales*100 1040/12000*100=8.67%

Gross profit ratio Gross profit/ sales*100 4200/12000*100=35%

Debt equity ratio Debts/equities 18800/15500=1.21

From the above calculations it has been analysed that organisation is having good

liquidity condition which has resulted in a high current and quick ratios. Net profits and gross

profit ratio of the organisation is also very high which means that it is having good profitability.

Debt equity ratio of the company is 1.21 which is lower than ideal ratio. The business entity is

suggested to use external funds more than internal funds.

9

4.2 Recommendation on appropriate future management strategies

From the above ratios it has been analysed that Belgravia Hotels is having low debt

equity ratio. It is very important for the company to use external funds to conduct business

activities so that internal funds can be saved for future contingencies. The managers of the

organisation are suggested to use appropriate management strategies in order to successfully

operate the business. The strategy which is recommended to the company is differentiation

which is described below:

Differentiation strategy: According to this strategy the companies should offer unique

products and services to the customers so that they can be retained and large market area can be

captured. This method can be used by Belgravia Hotels in order to attract large number of clients

by offering them such services that are unique as compare to the competitors. It will help to

expand the business successfully and also increase profitability (Brotherton, 2012).

TASK 5

5.1 Categorisation of costs as fixed, variable and semi variable

Cost: It is the total value of a particular product or service that include the cost of

material, labour and overheads. In Belgravia Hotels costs are divided in three different parts that

are fixed, variable and semi variable.

For example, an event is going to be organised in the lodge of Belgravia Hotels. The

event will be held in night and different type of food items including starters, main course and

dinner are going to be served to the guests. The costs for this event are categorised in following

parts:

Fixed cost: These are the cost that are fixed and does not change with the number of

guests and food items. It will be fixed for whole event.

Variable cost: The cost that varies with the number of guests and the food and beverage

items are called variable costs. This cost will vary during the event.

Semi variable cost: The costs that are partially fixed and partially variable are called

semi variable. It will be fixed for a certain level and will vary when the level is crossed.

5.2 Calculation of contribution per product and explanation of cost/ profit/ volume relationship

Calculation of contribution per units is based on assumption. All the figures that are

required to calculate it are as follows:

10

From the above ratios it has been analysed that Belgravia Hotels is having low debt

equity ratio. It is very important for the company to use external funds to conduct business

activities so that internal funds can be saved for future contingencies. The managers of the

organisation are suggested to use appropriate management strategies in order to successfully

operate the business. The strategy which is recommended to the company is differentiation

which is described below:

Differentiation strategy: According to this strategy the companies should offer unique

products and services to the customers so that they can be retained and large market area can be

captured. This method can be used by Belgravia Hotels in order to attract large number of clients

by offering them such services that are unique as compare to the competitors. It will help to

expand the business successfully and also increase profitability (Brotherton, 2012).

TASK 5

5.1 Categorisation of costs as fixed, variable and semi variable

Cost: It is the total value of a particular product or service that include the cost of

material, labour and overheads. In Belgravia Hotels costs are divided in three different parts that

are fixed, variable and semi variable.

For example, an event is going to be organised in the lodge of Belgravia Hotels. The

event will be held in night and different type of food items including starters, main course and

dinner are going to be served to the guests. The costs for this event are categorised in following

parts:

Fixed cost: These are the cost that are fixed and does not change with the number of

guests and food items. It will be fixed for whole event.

Variable cost: The cost that varies with the number of guests and the food and beverage

items are called variable costs. This cost will vary during the event.

Semi variable cost: The costs that are partially fixed and partially variable are called

semi variable. It will be fixed for a certain level and will vary when the level is crossed.

5.2 Calculation of contribution per product and explanation of cost/ profit/ volume relationship

Calculation of contribution per units is based on assumption. All the figures that are

required to calculate it are as follows:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.