Holmes Institute: HI5019 Bell Studio Expenditure Cycle Case Study

VerifiedAdded on 2023/01/23

|19

|3819

|91

Case Study

AI Summary

This case study report analyzes the expenditure cycle of Bell Studio, an Adelaide-based wholesaler of art suppliers. The report examines the purchases system, cash disbursement system, and payroll system, including their processes, risks, and internal controls. The study utilizes Data Flow Diagrams and system flowcharts to illustrate the systems. The report also identifies potential weaknesses and risks within each system, providing insights for the Chief Operating Officer to evaluate and improve the company's financial processes. The analysis covers the flow of goods, cash, and information, from initial purchase requisitions to cash disbursements and payroll processing, emphasizing the importance of internal controls to mitigate risks and ensure the efficiency and accuracy of financial operations.

Case Study – Bell Studio 1

CASE STUDY – BELL STUDIO REPORT ON THE EXPENDITURE CYCLE

Student’s Name

Student’s Code

Professor’s Name

Institution Affiliation

Date

CASE STUDY – BELL STUDIO REPORT ON THE EXPENDITURE CYCLE

Student’s Name

Student’s Code

Professor’s Name

Institution Affiliation

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Case Study – Bell Studio 2

Executive Summary

This paper is a report to the Chief Operating Officer in Bell Studio Organization, an

Adelaide-based wholesaler of art suppliers. The main aim of this report is to analyse

processes, risks and internal controls in the expenditure cycle. Considering the company’s

centralized accounting system with various networking terminals in different locations, this

paper composes an in-depth evaluation of the expenditure cycle process. In this rationale,

three systems that constitute the expenditure cycle will be discussed: purchases systems, cash

disbursement system and the payroll system before evaluating the risks of each system. The

first part of the paper will provide an overview of the reports and the conceptual systems Data

Flow Diagram (DFD) will be discussed in the second section. Afterward, the system

flowchart will be analyzed before the section that discusses the potential weaknesses and

risks of each system.

Executive Summary

This paper is a report to the Chief Operating Officer in Bell Studio Organization, an

Adelaide-based wholesaler of art suppliers. The main aim of this report is to analyse

processes, risks and internal controls in the expenditure cycle. Considering the company’s

centralized accounting system with various networking terminals in different locations, this

paper composes an in-depth evaluation of the expenditure cycle process. In this rationale,

three systems that constitute the expenditure cycle will be discussed: purchases systems, cash

disbursement system and the payroll system before evaluating the risks of each system. The

first part of the paper will provide an overview of the reports and the conceptual systems Data

Flow Diagram (DFD) will be discussed in the second section. Afterward, the system

flowchart will be analyzed before the section that discusses the potential weaknesses and

risks of each system.

Case Study – Bell Studio 3

Table of Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

Data Flow Diagram of Purchases and Cash Disbursements Systems........................................4

Purchase System.....................................................................................................................4

Cash Disbursement Systems..................................................................................................8

Data Flow Diagram of Payroll System......................................................................................9

System Flowchart of Purchases System...................................................................................11

System Flowchart of Cash Disbursements System..................................................................13

System Flowchart of Payroll System.......................................................................................14

Internal Control Weaknesses and Risks in Each System.........................................................15

Purchases System.................................................................................................................15

Cash Disbursement Systems................................................................................................15

Payroll Systems....................................................................................................................15

Conclusion................................................................................................................................16

References................................................................................................................................17

Table of Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

Data Flow Diagram of Purchases and Cash Disbursements Systems........................................4

Purchase System.....................................................................................................................4

Cash Disbursement Systems..................................................................................................8

Data Flow Diagram of Payroll System......................................................................................9

System Flowchart of Purchases System...................................................................................11

System Flowchart of Cash Disbursements System..................................................................13

System Flowchart of Payroll System.......................................................................................14

Internal Control Weaknesses and Risks in Each System.........................................................15

Purchases System.................................................................................................................15

Cash Disbursement Systems................................................................................................15

Payroll Systems....................................................................................................................15

Conclusion................................................................................................................................16

References................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Purchasing

Department

Inventory

Warehous

e

Cash

Disbursement

Department

Monitor inventory

records

Updates inventory

records

Receives Goods

Prepares Digital

Purchase Order

Updates Inventory

Control Access

Updates AP Control

Access

Updates digital AP

subsidiary ledger

Valid Vendor File

AP Pending File

Vendor

Account

Payable

Department

Inventory Subsidiary Ledger

Receiving File

Digital purchase order records

Purchase order copy 1

Purchase order copy 2

Receiving reports copy

Receiving report copy 2

Sends invoice

Sends invoice

Inventory level

Case Study – Bell Studio 4

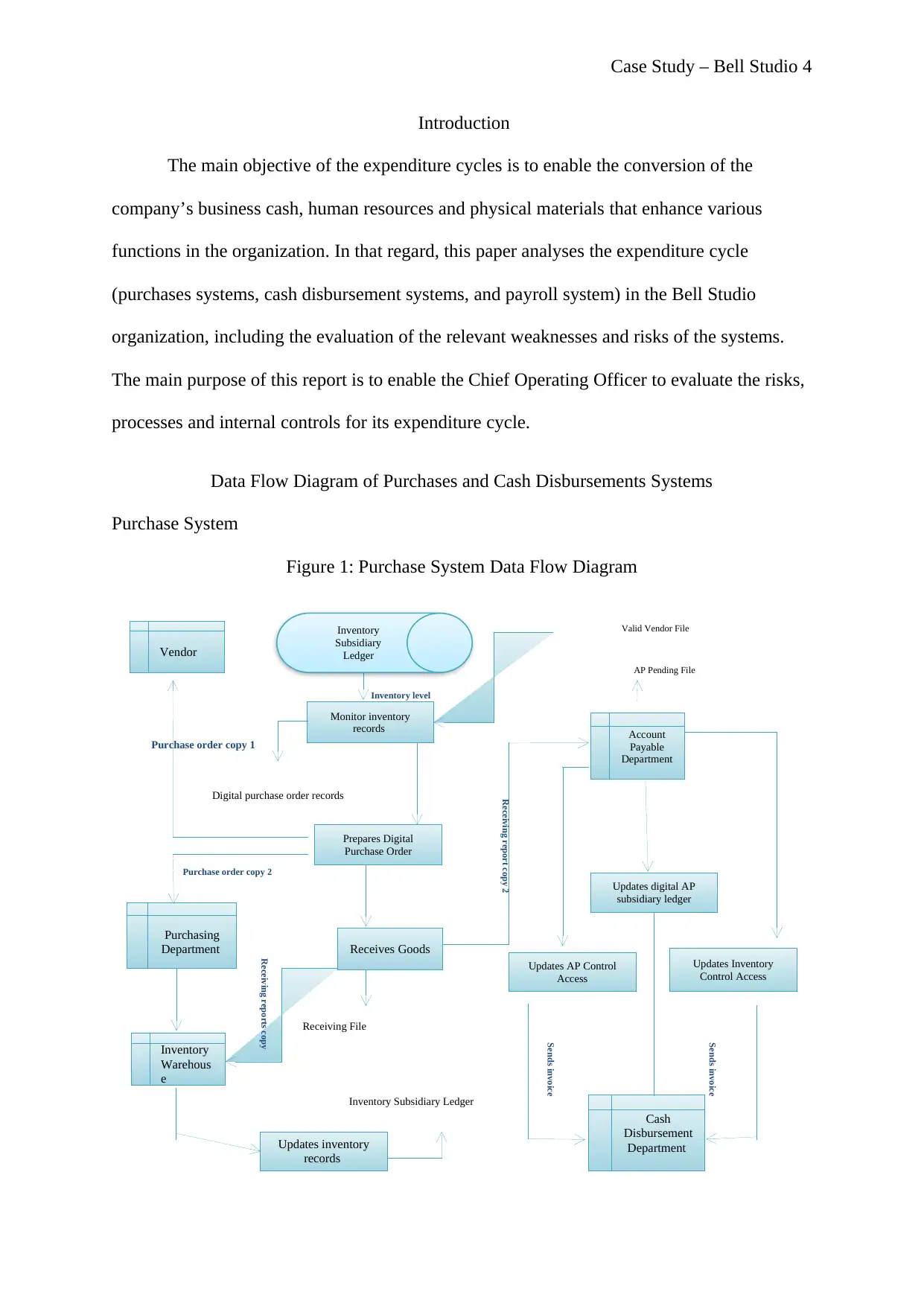

Introduction

The main objective of the expenditure cycles is to enable the conversion of the

company’s business cash, human resources and physical materials that enhance various

functions in the organization. In that regard, this paper analyses the expenditure cycle

(purchases systems, cash disbursement systems, and payroll system) in the Bell Studio

organization, including the evaluation of the relevant weaknesses and risks of the systems.

The main purpose of this report is to enable the Chief Operating Officer to evaluate the risks,

processes and internal controls for its expenditure cycle.

Data Flow Diagram of Purchases and Cash Disbursements Systems

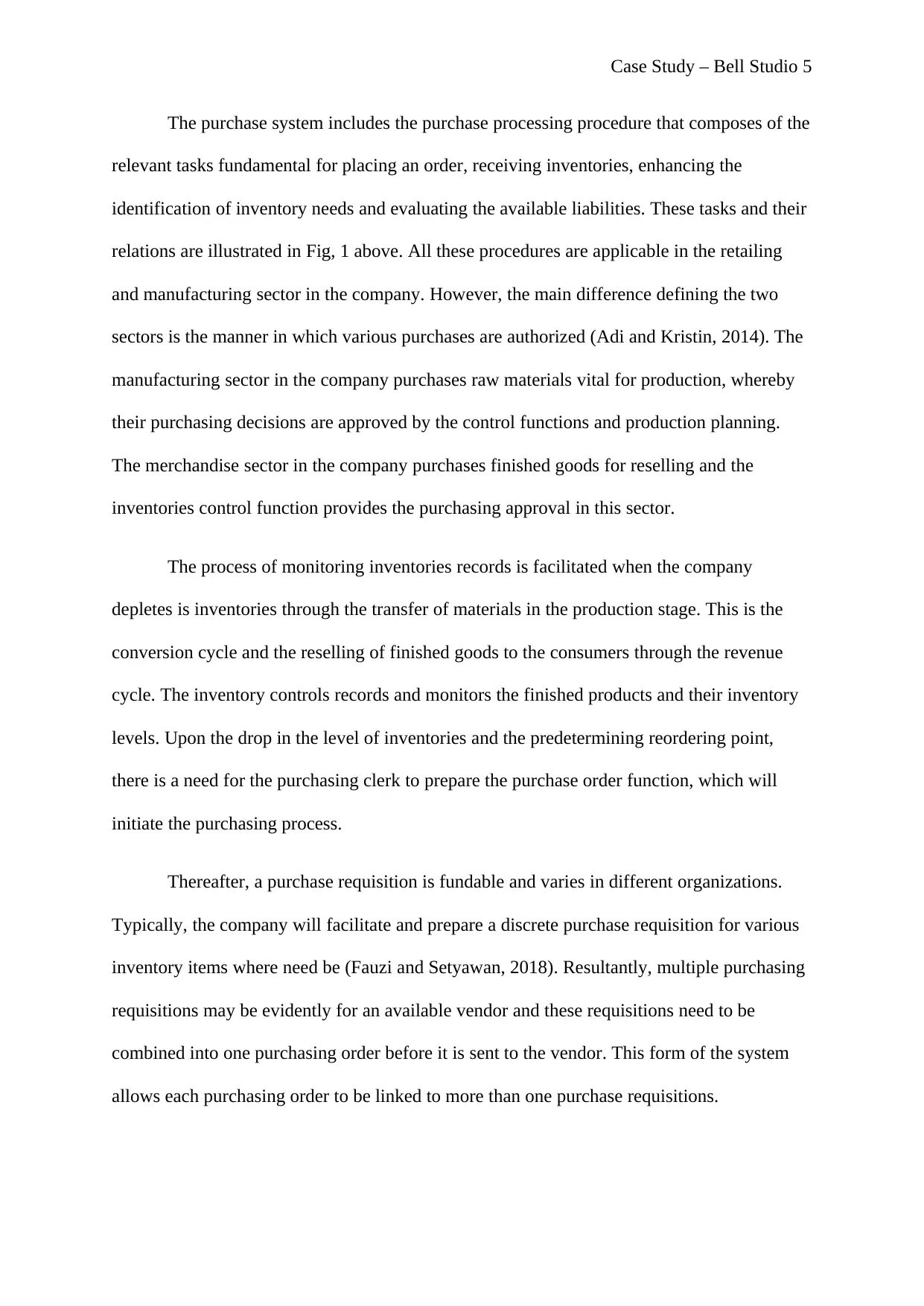

Purchase System

Figure 1: Purchase System Data Flow Diagram

Inventory

Subsidiary

Ledger

Department

Inventory

Warehous

e

Cash

Disbursement

Department

Monitor inventory

records

Updates inventory

records

Receives Goods

Prepares Digital

Purchase Order

Updates Inventory

Control Access

Updates AP Control

Access

Updates digital AP

subsidiary ledger

Valid Vendor File

AP Pending File

Vendor

Account

Payable

Department

Inventory Subsidiary Ledger

Receiving File

Digital purchase order records

Purchase order copy 1

Purchase order copy 2

Receiving reports copy

Receiving report copy 2

Sends invoice

Sends invoice

Inventory level

Case Study – Bell Studio 4

Introduction

The main objective of the expenditure cycles is to enable the conversion of the

company’s business cash, human resources and physical materials that enhance various

functions in the organization. In that regard, this paper analyses the expenditure cycle

(purchases systems, cash disbursement systems, and payroll system) in the Bell Studio

organization, including the evaluation of the relevant weaknesses and risks of the systems.

The main purpose of this report is to enable the Chief Operating Officer to evaluate the risks,

processes and internal controls for its expenditure cycle.

Data Flow Diagram of Purchases and Cash Disbursements Systems

Purchase System

Figure 1: Purchase System Data Flow Diagram

Inventory

Subsidiary

Ledger

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Case Study – Bell Studio 5

The purchase system includes the purchase processing procedure that composes of the

relevant tasks fundamental for placing an order, receiving inventories, enhancing the

identification of inventory needs and evaluating the available liabilities. These tasks and their

relations are illustrated in Fig, 1 above. All these procedures are applicable in the retailing

and manufacturing sector in the company. However, the main difference defining the two

sectors is the manner in which various purchases are authorized (Adi and Kristin, 2014). The

manufacturing sector in the company purchases raw materials vital for production, whereby

their purchasing decisions are approved by the control functions and production planning.

The merchandise sector in the company purchases finished goods for reselling and the

inventories control function provides the purchasing approval in this sector.

The process of monitoring inventories records is facilitated when the company

depletes is inventories through the transfer of materials in the production stage. This is the

conversion cycle and the reselling of finished goods to the consumers through the revenue

cycle. The inventory controls records and monitors the finished products and their inventory

levels. Upon the drop in the level of inventories and the predetermining reordering point,

there is a need for the purchasing clerk to prepare the purchase order function, which will

initiate the purchasing process.

Thereafter, a purchase requisition is fundable and varies in different organizations.

Typically, the company will facilitate and prepare a discrete purchase requisition for various

inventory items where need be (Fauzi and Setyawan, 2018). Resultantly, multiple purchasing

requisitions may be evidently for an available vendor and these requisitions need to be

combined into one purchasing order before it is sent to the vendor. This form of the system

allows each purchasing order to be linked to more than one purchase requisitions.

The purchase system includes the purchase processing procedure that composes of the

relevant tasks fundamental for placing an order, receiving inventories, enhancing the

identification of inventory needs and evaluating the available liabilities. These tasks and their

relations are illustrated in Fig, 1 above. All these procedures are applicable in the retailing

and manufacturing sector in the company. However, the main difference defining the two

sectors is the manner in which various purchases are authorized (Adi and Kristin, 2014). The

manufacturing sector in the company purchases raw materials vital for production, whereby

their purchasing decisions are approved by the control functions and production planning.

The merchandise sector in the company purchases finished goods for reselling and the

inventories control function provides the purchasing approval in this sector.

The process of monitoring inventories records is facilitated when the company

depletes is inventories through the transfer of materials in the production stage. This is the

conversion cycle and the reselling of finished goods to the consumers through the revenue

cycle. The inventory controls records and monitors the finished products and their inventory

levels. Upon the drop in the level of inventories and the predetermining reordering point,

there is a need for the purchasing clerk to prepare the purchase order function, which will

initiate the purchasing process.

Thereafter, a purchase requisition is fundable and varies in different organizations.

Typically, the company will facilitate and prepare a discrete purchase requisition for various

inventory items where need be (Fauzi and Setyawan, 2018). Resultantly, multiple purchasing

requisitions may be evidently for an available vendor and these requisitions need to be

combined into one purchasing order before it is sent to the vendor. This form of the system

allows each purchasing order to be linked to more than one purchase requisitions.

Case Study – Bell Studio 6

The preparation of the purchase order function obtains the purchasing requisitions,

organized by the vendor whenever needed. Afterward, the Purchase Order (PO) copy is

designed for the respective vendors as indicated in the Data Flow Diagram (DFD) in Fig 1.

Additionally, another copy is transferred to the purchasing department for set-up of the

Account Payable (AP) functions meant for temporary filing of the AP pending files.

Therefore, a blind copy of the file is then sent to Receiving Goods functions.

Many companies experience a time lag between receiving goods and placing an order.

During this stage, various PO copies will be included in the temporary files in the account

payable department, and no economic aspect is executed. At this juncture, the Bell Studio

organization has not yet received any inventories or incurred any financial obligations. In that

regard, there is no need for facilitating the making of formal entries in the accounting records

(Fedaghi, 2014). Nonetheless, the company may decide the make a memo entry in reference

to the pending inventory-related obligation and receipts.

The next stage in the cycle will involve the receipt inventories whereby goods arrive

and the receiving report is prepared. These goods are then reconciled with the packing slip

and Digital Purchase Order (DPO). The copies of the document include the data on the

quantity and prices of the items received. The main purpose of these documents is to enable

the receiving clerk to inspect and count inventories before drafting the receiving report.

Mostly, the receiving department is busy and their staff as subjected to the pressure of

unloading the delivery vehicles or signing lading bills (Gautam, 2010). In such cases, the

receiving clerk will only be provided with the relevant data on item quantity and accept

delivery of products in reference to the provided data.

In the cycle, the next stage in the provision of update regarding the inventory record.

Relative to the inventories valuation technique, the inventories controls technique varies in

The preparation of the purchase order function obtains the purchasing requisitions,

organized by the vendor whenever needed. Afterward, the Purchase Order (PO) copy is

designed for the respective vendors as indicated in the Data Flow Diagram (DFD) in Fig 1.

Additionally, another copy is transferred to the purchasing department for set-up of the

Account Payable (AP) functions meant for temporary filing of the AP pending files.

Therefore, a blind copy of the file is then sent to Receiving Goods functions.

Many companies experience a time lag between receiving goods and placing an order.

During this stage, various PO copies will be included in the temporary files in the account

payable department, and no economic aspect is executed. At this juncture, the Bell Studio

organization has not yet received any inventories or incurred any financial obligations. In that

regard, there is no need for facilitating the making of formal entries in the accounting records

(Fedaghi, 2014). Nonetheless, the company may decide the make a memo entry in reference

to the pending inventory-related obligation and receipts.

The next stage in the cycle will involve the receipt inventories whereby goods arrive

and the receiving report is prepared. These goods are then reconciled with the packing slip

and Digital Purchase Order (DPO). The copies of the document include the data on the

quantity and prices of the items received. The main purpose of these documents is to enable

the receiving clerk to inspect and count inventories before drafting the receiving report.

Mostly, the receiving department is busy and their staff as subjected to the pressure of

unloading the delivery vehicles or signing lading bills (Gautam, 2010). In such cases, the

receiving clerk will only be provided with the relevant data on item quantity and accept

delivery of products in reference to the provided data.

In the cycle, the next stage in the provision of update regarding the inventory record.

Relative to the inventories valuation technique, the inventories controls technique varies in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Case Study – Bell Studio 7

different organizations. A company that utilizes a standardized cost framework may execute

its inventory at a predetermined standardized figure irrespective of the charges being paid to a

given vendor (Bhoite, 2012). Presenting a standardized inventories ledger necessitates the

relevant data regarding the quantity attained. Since the receiving reports contain the item

quantity data, this file serves this purpose. Thus, updating the main cost inventory ledger

necessitates more financial data from the inventory warehouse. During the process of this

transaction, accounts payable needs a set-up. The AP function receives this setting the

temporary files of the receiving report and the PO is filed. The Bell Studio organization has

received these inventories from the respective vendors and realized its obligation to pay for

the received goods.

To end the process, the accounts payable clerk needs to evaluate the exact valuation

of the obligation up to the time the invoice is received (Hooshyar, Yusop, and Horng, 2015).

When the estimate is materially improper, an adjustment of the entry needs to be undertaken

to rectify the mistakes, Since the receipt of the received invoice trigger AP techniques and

processes, clerks need to evaluate all the liabilities that have not been recorded during the

time-end-closing. Upon the arrival of the inventories, the AP clerks reconcile the relevant

financial data with the PO and the receiving report in the available pending file. This is

known as three-way matching that verifies the quantity that has been obtained and its

respective prices (Jarrah, 2018). During this moment, the clerk progressively updates the

Digital Account Payable (DPO) subsidiary ledger, Account payable controls account and the

inventories controls account in the general ledger. Lastly, an involve, PO and receiving report

are then transferred

different organizations. A company that utilizes a standardized cost framework may execute

its inventory at a predetermined standardized figure irrespective of the charges being paid to a

given vendor (Bhoite, 2012). Presenting a standardized inventories ledger necessitates the

relevant data regarding the quantity attained. Since the receiving reports contain the item

quantity data, this file serves this purpose. Thus, updating the main cost inventory ledger

necessitates more financial data from the inventory warehouse. During the process of this

transaction, accounts payable needs a set-up. The AP function receives this setting the

temporary files of the receiving report and the PO is filed. The Bell Studio organization has

received these inventories from the respective vendors and realized its obligation to pay for

the received goods.

To end the process, the accounts payable clerk needs to evaluate the exact valuation

of the obligation up to the time the invoice is received (Hooshyar, Yusop, and Horng, 2015).

When the estimate is materially improper, an adjustment of the entry needs to be undertaken

to rectify the mistakes, Since the receipt of the received invoice trigger AP techniques and

processes, clerks need to evaluate all the liabilities that have not been recorded during the

time-end-closing. Upon the arrival of the inventories, the AP clerks reconcile the relevant

financial data with the PO and the receiving report in the available pending file. This is

known as three-way matching that verifies the quantity that has been obtained and its

respective prices (Jarrah, 2018). During this moment, the clerk progressively updates the

Digital Account Payable (DPO) subsidiary ledger, Account payable controls account and the

inventories controls account in the general ledger. Lastly, an involve, PO and receiving report

are then transferred

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AP Department

Updates

Documents

Document Receipts

Identification

of Liability

Due

Treasurer

Vendor

Preparation of

cheque for an

invoice account Signature

Mailing

Receiving

Receiving Report File

Invoice FileCheque Copy

Case Study – Bell Studio 8

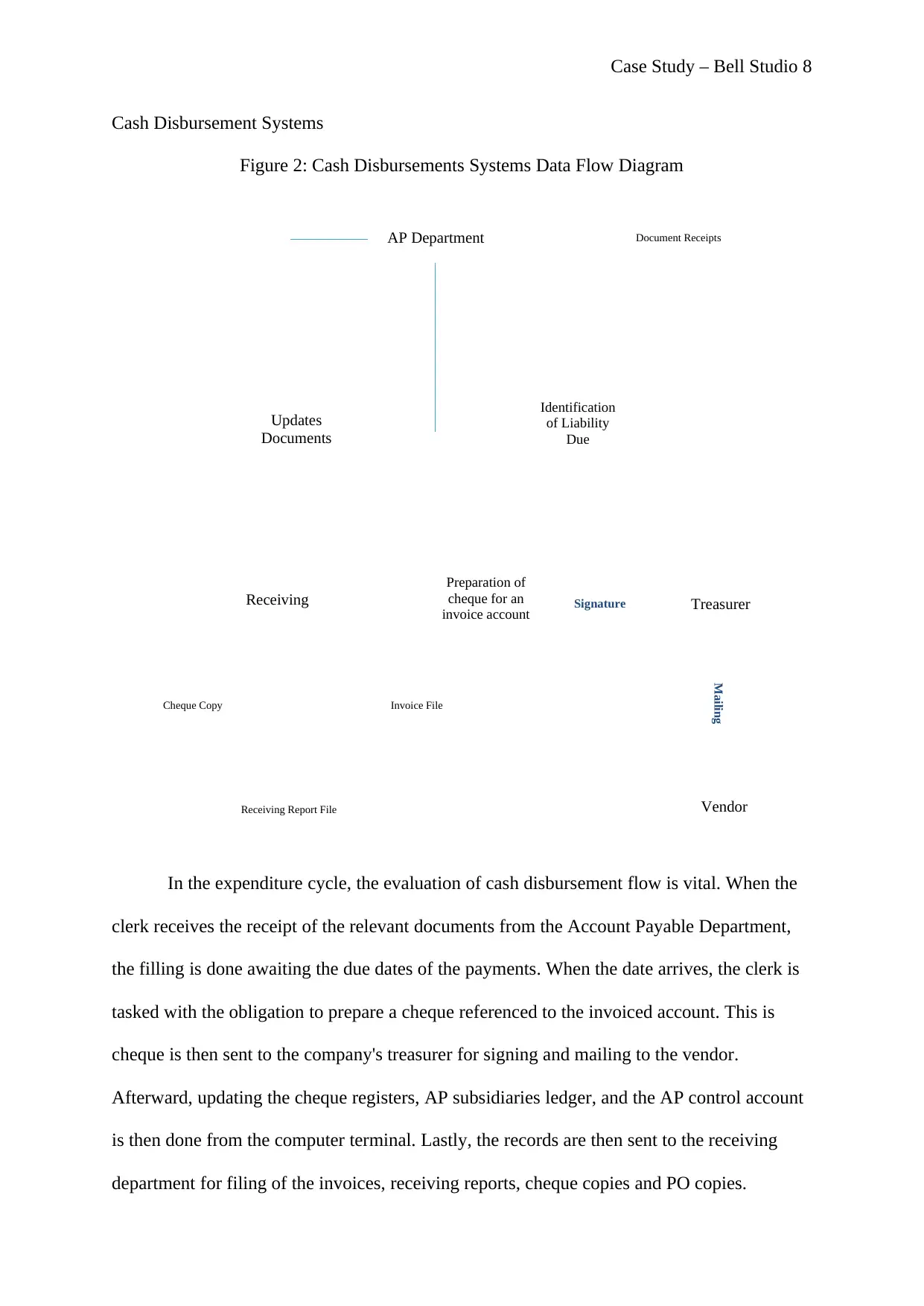

Cash Disbursement Systems

Figure 2: Cash Disbursements Systems Data Flow Diagram

In the expenditure cycle, the evaluation of cash disbursement flow is vital. When the

clerk receives the receipt of the relevant documents from the Account Payable Department,

the filling is done awaiting the due dates of the payments. When the date arrives, the clerk is

tasked with the obligation to prepare a cheque referenced to the invoiced account. This is

cheque is then sent to the company's treasurer for signing and mailing to the vendor.

Afterward, updating the cheque registers, AP subsidiaries ledger, and the AP control account

is then done from the computer terminal. Lastly, the records are then sent to the receiving

department for filing of the invoices, receiving reports, cheque copies and PO copies.

Updates

Documents

Document Receipts

Identification

of Liability

Due

Treasurer

Vendor

Preparation of

cheque for an

invoice account Signature

Mailing

Receiving

Receiving Report File

Invoice FileCheque Copy

Case Study – Bell Studio 8

Cash Disbursement Systems

Figure 2: Cash Disbursements Systems Data Flow Diagram

In the expenditure cycle, the evaluation of cash disbursement flow is vital. When the

clerk receives the receipt of the relevant documents from the Account Payable Department,

the filling is done awaiting the due dates of the payments. When the date arrives, the clerk is

tasked with the obligation to prepare a cheque referenced to the invoiced account. This is

cheque is then sent to the company's treasurer for signing and mailing to the vendor.

Afterward, updating the cheque registers, AP subsidiaries ledger, and the AP control account

is then done from the computer terminal. Lastly, the records are then sent to the receiving

department for filing of the invoices, receiving reports, cheque copies and PO copies.

Prepares cash

disbursement

vouchers

Payroll DepartmentEmployees Time Cards

Supervisors

Central Payroll SystemTime Card data

Payroll register

Payroll register

Supervisor

AC Department

Write ChequesCheque file

Imprest bank

General ledger

department

Cheque file

Department Employees

Reviews and submits

Hour’s records

Digital Employee Record

Reviews and submits

Deposits

Reviews

Check

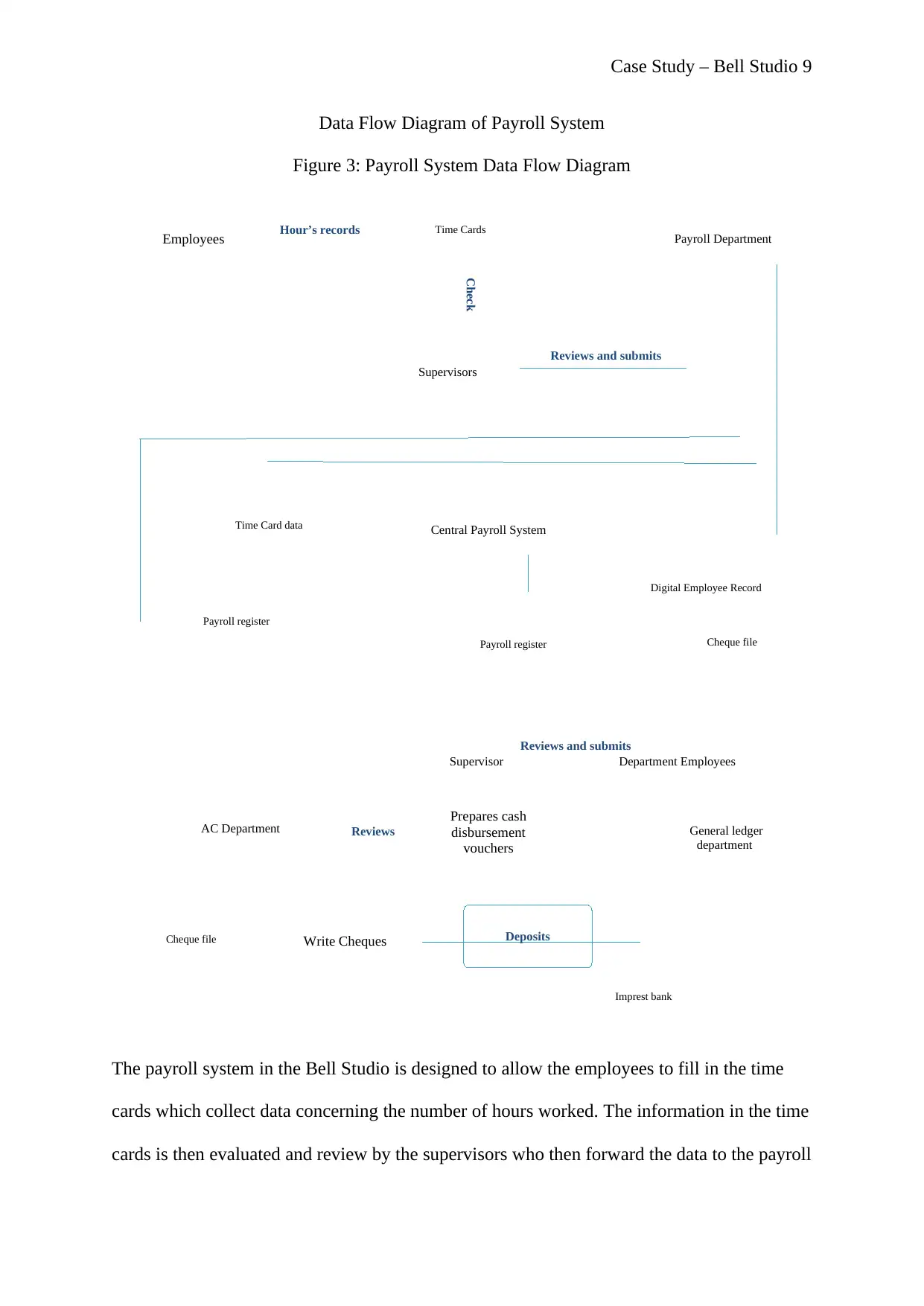

Case Study – Bell Studio 9

Data Flow Diagram of Payroll System

Figure 3: Payroll System Data Flow Diagram

The payroll system in the Bell Studio is designed to allow the employees to fill in the time

cards which collect data concerning the number of hours worked. The information in the time

cards is then evaluated and review by the supervisors who then forward the data to the payroll

disbursement

vouchers

Payroll DepartmentEmployees Time Cards

Supervisors

Central Payroll SystemTime Card data

Payroll register

Payroll register

Supervisor

AC Department

Write ChequesCheque file

Imprest bank

General ledger

department

Cheque file

Department Employees

Reviews and submits

Hour’s records

Digital Employee Record

Reviews and submits

Deposits

Reviews

Check

Case Study – Bell Studio 9

Data Flow Diagram of Payroll System

Figure 3: Payroll System Data Flow Diagram

The payroll system in the Bell Studio is designed to allow the employees to fill in the time

cards which collect data concerning the number of hours worked. The information in the time

cards is then evaluated and review by the supervisors who then forward the data to the payroll

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Case Study – Bell Studio 10

department. The payroll system is referenced from the central payroll system that is located

in the data processes department from which the clerk inputs data and prints copies of a

paycheque, payroll registers, and digital employees' records. From the payroll department, the

clerk possibly files the time cards and sends the employees' payment cheques to the

supervisors for distribution and review. Afterward, the clerk sends a copy of the payroll

register to the AP department and the other composed of the time cards to the payroll

department.

The AP clerks then review the register and prepare the cash disbursement voucher manually.

Afterward, the clerk then sends the payroll register and the voucher to the general ledgers

department and the AP clerk writers a cheque for the payroll and then deposits the cheque in

the imprest account at the Bank.

department. The payroll system is referenced from the central payroll system that is located

in the data processes department from which the clerk inputs data and prints copies of a

paycheque, payroll registers, and digital employees' records. From the payroll department, the

clerk possibly files the time cards and sends the employees' payment cheques to the

supervisors for distribution and review. Afterward, the clerk sends a copy of the payroll

register to the AP department and the other composed of the time cards to the payroll

department.

The AP clerks then review the register and prepare the cash disbursement voucher manually.

Afterward, the clerk then sends the payroll register and the voucher to the general ledgers

department and the AP clerk writers a cheque for the payroll and then deposits the cheque in

the imprest account at the Bank.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Case Study – Bell Studio 11

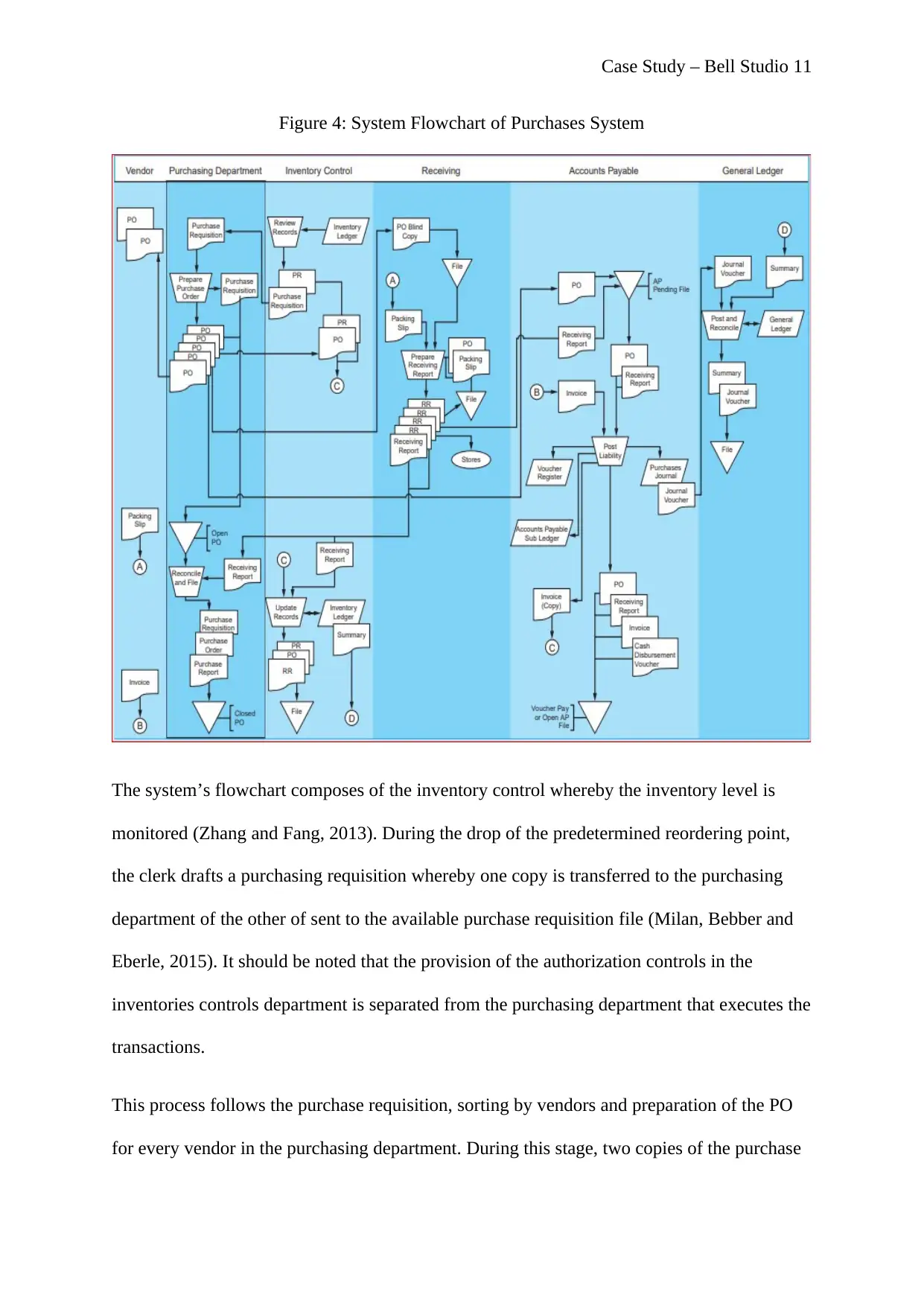

Figure 4: System Flowchart of Purchases System

The system’s flowchart composes of the inventory control whereby the inventory level is

monitored (Zhang and Fang, 2013). During the drop of the predetermined reordering point,

the clerk drafts a purchasing requisition whereby one copy is transferred to the purchasing

department of the other of sent to the available purchase requisition file (Milan, Bebber and

Eberle, 2015). It should be noted that the provision of the authorization controls in the

inventories controls department is separated from the purchasing department that executes the

transactions.

This process follows the purchase requisition, sorting by vendors and preparation of the PO

for every vendor in the purchasing department. During this stage, two copies of the purchase

Figure 4: System Flowchart of Purchases System

The system’s flowchart composes of the inventory control whereby the inventory level is

monitored (Zhang and Fang, 2013). During the drop of the predetermined reordering point,

the clerk drafts a purchasing requisition whereby one copy is transferred to the purchasing

department of the other of sent to the available purchase requisition file (Milan, Bebber and

Eberle, 2015). It should be noted that the provision of the authorization controls in the

inventories controls department is separated from the purchasing department that executes the

transactions.

This process follows the purchase requisition, sorting by vendors and preparation of the PO

for every vendor in the purchasing department. During this stage, two copies of the purchase

Case Study – Bell Studio 12

orders are transferred to the vendor and the PO copy is transferred to the inventory control for

filing with available purchasing requisition. The goods that originate from the vendors are

then reconciled with the blind copies of the PO. When the physical counting and inspection

process is complete, the receiving clerk then prepares different reports that state the condition

and quantity of the inventories (Nakamoto, 2017). One of the copies of the receiving reports

is sent to the inventory department accompanied by the physical inventory. The remaining

copy is transferred to the purchasing department and the clerk is then able to reconcile it with

the available PO.

In the accounts payable department, the clerk receives the arriving invoice whereby the

information is reconciled with the available pending document file. Thereafter, a record of

the relevant transactions in the journal purchases and points, including the AP subsidiary

ledger is then prepared. This follows a record of the liabilities, whereby the clerk sends the

sourced documents, receiving reports and available voucher payable files. During this stage,

an update of the digital account payable subsidiaries ledgers is done, including the AP

controls account and the inventories control accounts in the DL department from the

computer terminal. Lastly, the clerk transfers the invoices, PO copies and receiving reports to

the cash disbursement department.

orders are transferred to the vendor and the PO copy is transferred to the inventory control for

filing with available purchasing requisition. The goods that originate from the vendors are

then reconciled with the blind copies of the PO. When the physical counting and inspection

process is complete, the receiving clerk then prepares different reports that state the condition

and quantity of the inventories (Nakamoto, 2017). One of the copies of the receiving reports

is sent to the inventory department accompanied by the physical inventory. The remaining

copy is transferred to the purchasing department and the clerk is then able to reconcile it with

the available PO.

In the accounts payable department, the clerk receives the arriving invoice whereby the

information is reconciled with the available pending document file. Thereafter, a record of

the relevant transactions in the journal purchases and points, including the AP subsidiary

ledger is then prepared. This follows a record of the liabilities, whereby the clerk sends the

sourced documents, receiving reports and available voucher payable files. During this stage,

an update of the digital account payable subsidiaries ledgers is done, including the AP

controls account and the inventories control accounts in the DL department from the

computer terminal. Lastly, the clerk transfers the invoices, PO copies and receiving reports to

the cash disbursement department.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.