HI5019 Strategic Information Systems: Bell Studio Case Study Analysis

VerifiedAdded on 2023/01/04

|19

|3812

|95

Case Study

AI Summary

This case study analyzes Bell Studio's expenditure cycle, evaluating processes, risks, and internal controls within its purchase, cash disbursement, and payroll systems. The analysis includes data flow diagrams and system flowcharts to illustrate the processes. The study identifies internal control weaknesses and associated risks within each system, suggesting areas for improvement. The case study covers various aspects of the expenditure cycle, including the purchase order process, cash disbursement procedures, and payroll processing, providing a comprehensive overview of the organization's financial systems and potential vulnerabilities. The document also highlights the importance of effective internal controls to mitigate risks and ensure the efficient operation of these critical business functions.

Strategic Information Systems for Business and Enterprise 1

Strategic Information Systems for Business and Enterprise (Bell Studio

Case Study)

Student

Course

Tutor

Institutional Affiliations

State

Date

Strategic Information Systems for Business and Enterprise (Bell Studio

Case Study)

Student

Course

Tutor

Institutional Affiliations

State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Information Systems for Business and Enterprise 2

Strategic Information Systems for Business and Enterprise (Bell

Studio Case Study)

Executive summary

The purpose of this document is to analyze Bell Studio organization’s expenditure cycle

and evaluate the processes, risks and the internal controls for the expenditure cycle. In doing so

the document examines the three critical systems that is composed of the expenditure cycle

including the purchase system, the cash disbursement system and payroll system. Along with

that, various threats associated with each system is also discussed in the document. The analysis

suggest some improvements that are necessary for the organization. The structure of the paper

include: the introduction which discusses the overview of the document, this is followed by

presentation and analysis on data flow diagram for purchase and cash disbursement system, the

data flow diagram for payroll, the system flow chart of purchases system, the system flowchart

of cash disbursement system, the system flowchart of payroll and lastly the internal control

weakness in each system as well as the risks associated by the weaknesses.

Strategic Information Systems for Business and Enterprise (Bell

Studio Case Study)

Executive summary

The purpose of this document is to analyze Bell Studio organization’s expenditure cycle

and evaluate the processes, risks and the internal controls for the expenditure cycle. In doing so

the document examines the three critical systems that is composed of the expenditure cycle

including the purchase system, the cash disbursement system and payroll system. Along with

that, various threats associated with each system is also discussed in the document. The analysis

suggest some improvements that are necessary for the organization. The structure of the paper

include: the introduction which discusses the overview of the document, this is followed by

presentation and analysis on data flow diagram for purchase and cash disbursement system, the

data flow diagram for payroll, the system flow chart of purchases system, the system flowchart

of cash disbursement system, the system flowchart of payroll and lastly the internal control

weakness in each system as well as the risks associated by the weaknesses.

Strategic Information Systems for Business and Enterprise 3

Table of Contents

Executive summary...................................................................................................................................2

Table of Contents........................................................................................................................................3

Introduction...............................................................................................................................................4

Data flow diagram for purchase and cash disbursement systems..........................................................4

Purchase system.....................................................................................................................................4

Cash disbursement system....................................................................................................................8

Data flow diagram for payroll system......................................................................................................9

System flowchart of purchases system...................................................................................................11

System flowchart for cash disbursement system...................................................................................13

System flow chart of payroll system.......................................................................................................14

The internal control weakness in each system and risks associated by the identified weakness.......15

Purchase system...................................................................................................................................15

Cash disbursement system..................................................................................................................15

Payroll system......................................................................................................................................15

Conclusion................................................................................................................................................16

Table of Contents

Executive summary...................................................................................................................................2

Table of Contents........................................................................................................................................3

Introduction...............................................................................................................................................4

Data flow diagram for purchase and cash disbursement systems..........................................................4

Purchase system.....................................................................................................................................4

Cash disbursement system....................................................................................................................8

Data flow diagram for payroll system......................................................................................................9

System flowchart of purchases system...................................................................................................11

System flowchart for cash disbursement system...................................................................................13

System flow chart of payroll system.......................................................................................................14

The internal control weakness in each system and risks associated by the identified weakness.......15

Purchase system...................................................................................................................................15

Cash disbursement system..................................................................................................................15

Payroll system......................................................................................................................................15

Conclusion................................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Information Systems for Business and Enterprise 4

Introduction

Expenditure cycle is a very critical aspect in any business organization. It involves

buying goods and services with cash. The main objective of expenditure cycle is to reduce the

cost of acquiring and maintaining supplies, inventories and services. Expenditure cycle also help

to ensure that all goods and services get ordered and received as required as well as ensuring that

the goods are in good conditions as they were ordered (Trigo, Belfo and Estébanez, 2016,

pp.987-994; Hall, 2012, pp.02). Being such an essential aspect of a business model, I sought to

prepare this report (as a business analyst at Bell Studio, an Adelaide-based wholesaler of art

supplies) to the chief operating officer in order to evaluate the processes, risks as well as the

internal control for the organization’s expenditure cycle.

Data flow diagram for purchase and cash disbursement systems

Upon analysis on the organization’s data flow and purchase system, we came up with a

flow diagram on the systems presented in this section. The section will first show the diagram for

the purchase system followed by cash disbursement system.

Purchase system

This system involves a procedure for purchase processing that involve various

undertakings that are followed when an order is purchased as well as identification and receiving

inventories and evaluating liabilities that are available (Randall, and George, First Data Corp,

2010, pp.24-31). Figure 1 below summarizes the purchase system of Bell Studio organization.

Introduction

Expenditure cycle is a very critical aspect in any business organization. It involves

buying goods and services with cash. The main objective of expenditure cycle is to reduce the

cost of acquiring and maintaining supplies, inventories and services. Expenditure cycle also help

to ensure that all goods and services get ordered and received as required as well as ensuring that

the goods are in good conditions as they were ordered (Trigo, Belfo and Estébanez, 2016,

pp.987-994; Hall, 2012, pp.02). Being such an essential aspect of a business model, I sought to

prepare this report (as a business analyst at Bell Studio, an Adelaide-based wholesaler of art

supplies) to the chief operating officer in order to evaluate the processes, risks as well as the

internal control for the organization’s expenditure cycle.

Data flow diagram for purchase and cash disbursement systems

Upon analysis on the organization’s data flow and purchase system, we came up with a

flow diagram on the systems presented in this section. The section will first show the diagram for

the purchase system followed by cash disbursement system.

Purchase system

This system involves a procedure for purchase processing that involve various

undertakings that are followed when an order is purchased as well as identification and receiving

inventories and evaluating liabilities that are available (Randall, and George, First Data Corp,

2010, pp.24-31). Figure 1 below summarizes the purchase system of Bell Studio organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Information Systems for Business and Enterprise 5

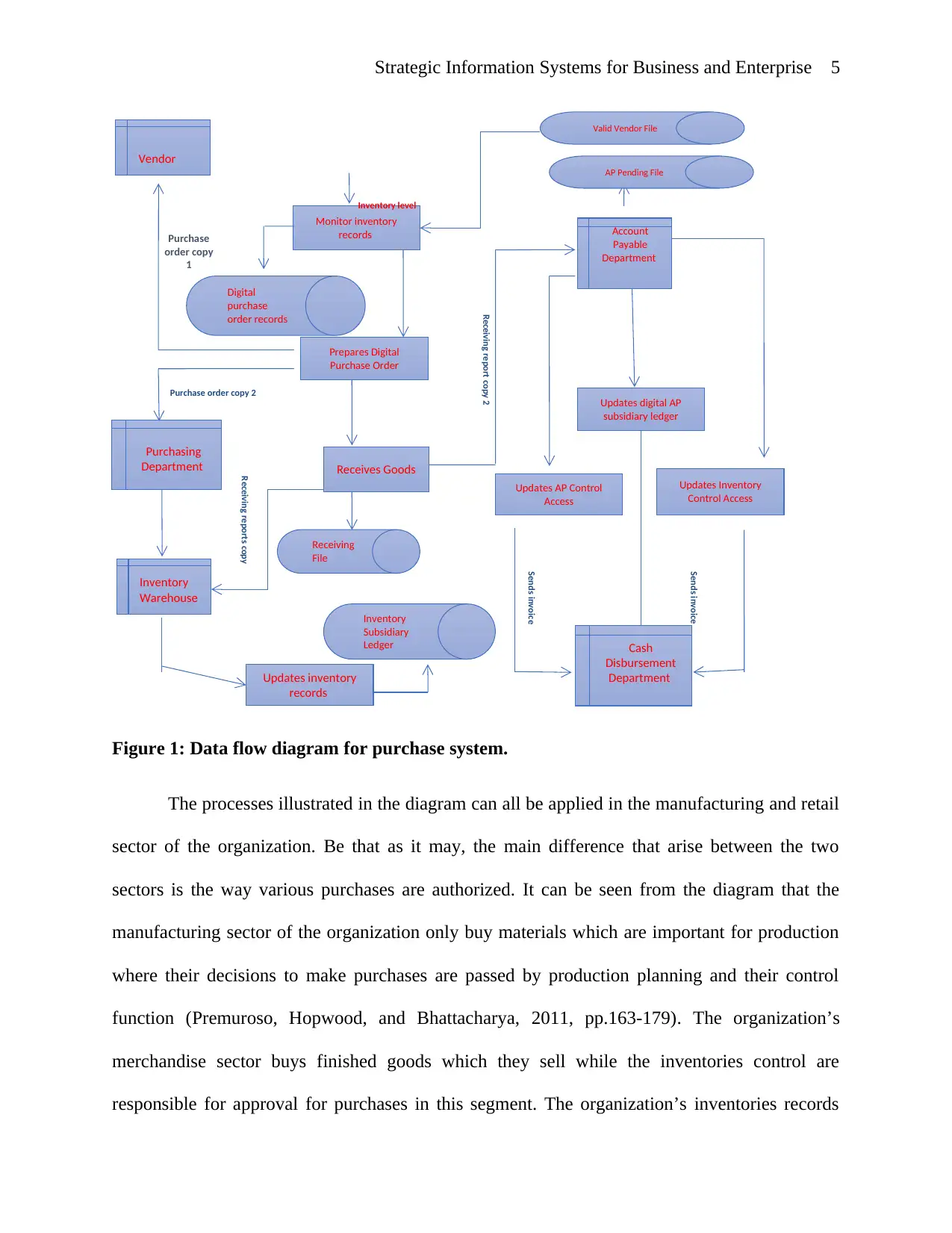

Figure 1: Data flow diagram for purchase system.

The processes illustrated in the diagram can all be applied in the manufacturing and retail

sector of the organization. Be that as it may, the main difference that arise between the two

sectors is the way various purchases are authorized. It can be seen from the diagram that the

manufacturing sector of the organization only buy materials which are important for production

where their decisions to make purchases are passed by production planning and their control

function (Premuroso, Hopwood, and Bhattacharya, 2011, pp.163-179). The organization’s

merchandise sector buys finished goods which they sell while the inventories control are

responsible for approval for purchases in this segment. The organization’s inventories records

Purchasing

Department

Inventory

Warehouse

Cash

Disbursement

Department

Monitor inventory

records

Updates inventory

records

Receives Goods

Prepares Digital

Purchase Order

Updates Inventory

Control Access

Updates AP Control

Access

Updates digital AP

subsidiary ledger

Valid Vendor File

AP Pending File

Vendor

Account

Payable

Department

Inventory

Subsidiary

Ledger

Receiving

File

Digital

purchase

order records

Purchase

order copy

1

Purchase order copy 2

Receiving reports copy

Receiving report copy 2

Sends invoice

Sends invoice

Inventory level

Figure 1: Data flow diagram for purchase system.

The processes illustrated in the diagram can all be applied in the manufacturing and retail

sector of the organization. Be that as it may, the main difference that arise between the two

sectors is the way various purchases are authorized. It can be seen from the diagram that the

manufacturing sector of the organization only buy materials which are important for production

where their decisions to make purchases are passed by production planning and their control

function (Premuroso, Hopwood, and Bhattacharya, 2011, pp.163-179). The organization’s

merchandise sector buys finished goods which they sell while the inventories control are

responsible for approval for purchases in this segment. The organization’s inventories records

Purchasing

Department

Inventory

Warehouse

Cash

Disbursement

Department

Monitor inventory

records

Updates inventory

records

Receives Goods

Prepares Digital

Purchase Order

Updates Inventory

Control Access

Updates AP Control

Access

Updates digital AP

subsidiary ledger

Valid Vendor File

AP Pending File

Vendor

Account

Payable

Department

Inventory

Subsidiary

Ledger

Receiving

File

Digital

purchase

order records

Purchase

order copy

1

Purchase order copy 2

Receiving reports copy

Receiving report copy 2

Sends invoice

Sends invoice

Inventory level

Strategic Information Systems for Business and Enterprise 6

are done when the organization completes its inventories by transferring its materials at the

production level. This refers to the conversion cycle as well as resell of the finished goods

through the revenue cycle to the consumers (Murray, Skene, and Haynes, 2017, pp.369-380).

The finished products are controlled, recorded and monitored by the inventory. When a drop in

level of the inventory is recorded, the purchase clerks will need to make the purchase order

function which will be intern used in making purchases.

Due to the reason that the purchase requisition is varies and is fundable in various

companies, Bell studio will participate in preparing the purchase requisition for inventory system

when required. As a result, a good number of purchasing requisition will be required and the

requisitions need to be complied into one requisition before they get submitted to the vendor

(Seifert, Sayor, and Baumgart, Western Union Co, 2010, pp.19; Killian et al. 2014, pp.180). By

this, each purchasing order will be linked to many purchase requisitions.

When the purchase order function is prepared, the purchasing requisitions organized by

the vendor can be obtained anytime it is required after which a copy of the purchase order is

designed for the respective vendors as the flow diagram in figure 1 depicts. Another copy of the

document can also be sent given to the purchasing department in order to set up the account

payable functions for its pending files.

Typically, a time lag between placing an order and receiving goods is experienced be

many organizations. at this time, various copies of purchase orders are included in temporary

files in the departments for account payable thus no economic aspect get accomplished (Zee,

2010, pp.123-124, pp.39). This is when Bell Studio has neither accessed any inventory nor

incurred any financial duty. If this is the case, the need to facilitate formal entry into the

are done when the organization completes its inventories by transferring its materials at the

production level. This refers to the conversion cycle as well as resell of the finished goods

through the revenue cycle to the consumers (Murray, Skene, and Haynes, 2017, pp.369-380).

The finished products are controlled, recorded and monitored by the inventory. When a drop in

level of the inventory is recorded, the purchase clerks will need to make the purchase order

function which will be intern used in making purchases.

Due to the reason that the purchase requisition is varies and is fundable in various

companies, Bell studio will participate in preparing the purchase requisition for inventory system

when required. As a result, a good number of purchasing requisition will be required and the

requisitions need to be complied into one requisition before they get submitted to the vendor

(Seifert, Sayor, and Baumgart, Western Union Co, 2010, pp.19; Killian et al. 2014, pp.180). By

this, each purchasing order will be linked to many purchase requisitions.

When the purchase order function is prepared, the purchasing requisitions organized by

the vendor can be obtained anytime it is required after which a copy of the purchase order is

designed for the respective vendors as the flow diagram in figure 1 depicts. Another copy of the

document can also be sent given to the purchasing department in order to set up the account

payable functions for its pending files.

Typically, a time lag between placing an order and receiving goods is experienced be

many organizations. at this time, various copies of purchase orders are included in temporary

files in the departments for account payable thus no economic aspect get accomplished (Zee,

2010, pp.123-124, pp.39). This is when Bell Studio has neither accessed any inventory nor

incurred any financial duty. If this is the case, the need to facilitate formal entry into the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Information Systems for Business and Enterprise 7

accounting records is not necessary. However, the organization may decide to, in reference to the

related inventory obligations and receipts that is pending, make a memo.

Afterwards, the receipt inventories through which reports for arrival and receiving of

goods will be prepared. The goods will then afterwards get reconciled with digital purchase order

and packing slips. The documents will show data on the quantity as well as costs of the materials

in order to allow the receiving clerk to count and inspect the inventories before a receiving report

is written by the clerk. In most cases, the departments which receives these goods get busy, as

such, the staff may end up signing the landing bills or unloading the delivery vehicles. During

such circumstances, the clerks are only given the relevant data on the quantity of items on basis

of which he will accept the product delivery.

In the stage involving provisions of updates on the inventory records, the inventory

controls differs in various companies. The organizations that uses the standardized cost

framework may have their inventory executed at a predetermined figure which is standardized

disregarding what is charged by a vendor. Providing a ledger for standardized inventories require

the relevant data showing the quantity that has been attained. Due to the fact that the receiving

report has data on the item quantity, the main inventory data will require financial data from the

inventory warehouse when it is updated (Hall, 2012, pp.71-79). The accounts payable will need a

set up during this transaction process. As such, these accounts will have the setting as purchase

order is filed. Bell Studio corporate has been given these documents by their vendors and has

realized their duty to pay for the items received.

To condense the process, it is imperative that the account payable clerks evaluate the

value of duty until invoice is received. On the off chance that the estimate is materially not

favorable, the entries will need to be adjusted in order to rectify the mistake. All the liabilities

accounting records is not necessary. However, the organization may decide to, in reference to the

related inventory obligations and receipts that is pending, make a memo.

Afterwards, the receipt inventories through which reports for arrival and receiving of

goods will be prepared. The goods will then afterwards get reconciled with digital purchase order

and packing slips. The documents will show data on the quantity as well as costs of the materials

in order to allow the receiving clerk to count and inspect the inventories before a receiving report

is written by the clerk. In most cases, the departments which receives these goods get busy, as

such, the staff may end up signing the landing bills or unloading the delivery vehicles. During

such circumstances, the clerks are only given the relevant data on the quantity of items on basis

of which he will accept the product delivery.

In the stage involving provisions of updates on the inventory records, the inventory

controls differs in various companies. The organizations that uses the standardized cost

framework may have their inventory executed at a predetermined figure which is standardized

disregarding what is charged by a vendor. Providing a ledger for standardized inventories require

the relevant data showing the quantity that has been attained. Due to the fact that the receiving

report has data on the item quantity, the main inventory data will require financial data from the

inventory warehouse when it is updated (Hall, 2012, pp.71-79). The accounts payable will need a

set up during this transaction process. As such, these accounts will have the setting as purchase

order is filed. Bell Studio corporate has been given these documents by their vendors and has

realized their duty to pay for the items received.

To condense the process, it is imperative that the account payable clerks evaluate the

value of duty until invoice is received. On the off chance that the estimate is materially not

favorable, the entries will need to be adjusted in order to rectify the mistake. All the liabilities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AP Department

Updates

Documents

Document Receipts

Identification

of Liability Due

Treasurer

Vendor

Preparation of

cheque for invoice

account Signature

Mailing

Receiving

Receiving Report File

Invoice FileCheque Copy

Strategic Information Systems for Business and Enterprise 8

that have not been recorded by the end time should be evaluated by clerks due to the reason that

the receipts of the received invoices may trigger the accounts payable processes and techniques.

Cash disbursement system

The flow diagram for the cash disbursement system is presented in figure 2 below.

Figure 2: Data flow diagram for cash disbursement system

Evaluation of the cash disbursement is a critical undertaking in an expenditure cycle.

When relevant documents are received by the clerk from the account payable departments, he

does fillings before payment day. During the payment date, the clerk will be tasked with the

responsibility to make cheques that are referenced to the accounts which invoiced. The cheque

Updates

Documents

Document Receipts

Identification

of Liability Due

Treasurer

Vendor

Preparation of

cheque for invoice

account Signature

Mailing

Receiving

Receiving Report File

Invoice FileCheque Copy

Strategic Information Systems for Business and Enterprise 8

that have not been recorded by the end time should be evaluated by clerks due to the reason that

the receipts of the received invoices may trigger the accounts payable processes and techniques.

Cash disbursement system

The flow diagram for the cash disbursement system is presented in figure 2 below.

Figure 2: Data flow diagram for cash disbursement system

Evaluation of the cash disbursement is a critical undertaking in an expenditure cycle.

When relevant documents are received by the clerk from the account payable departments, he

does fillings before payment day. During the payment date, the clerk will be tasked with the

responsibility to make cheques that are referenced to the accounts which invoiced. The cheque

Strategic Information Systems for Business and Enterprise 9

will then get submitted to the company’s treasure who will sign it and further mail it to vendors.

Consequently, the account payable control and account payable subsidiaries cheque get updated

from the computer terminals. Afterwards, the records will then get submitted to the receiving

departments to file invoices, receive copies of check and reports as well as copies of purchase

order.

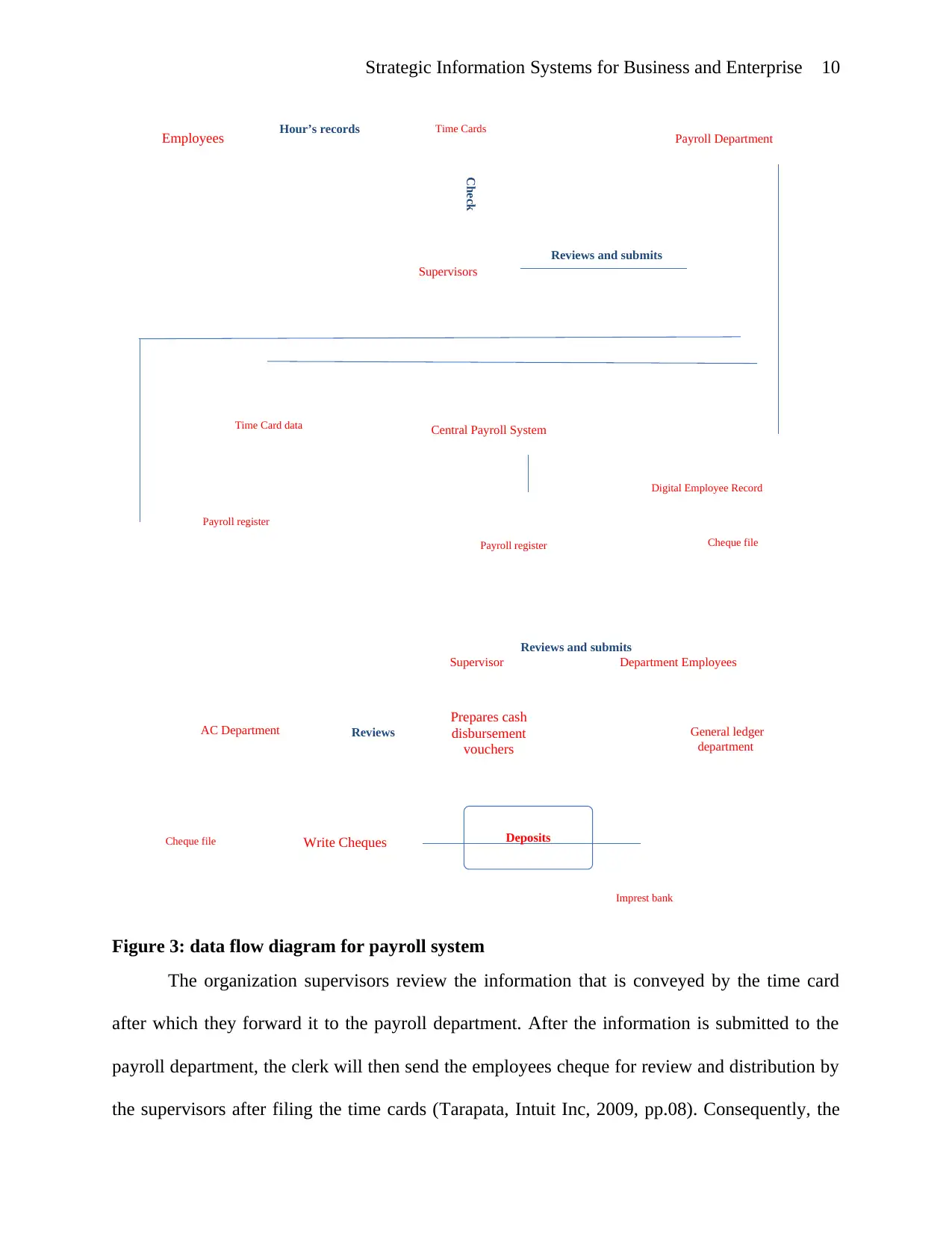

Data flow diagram for payroll system

The Bell Studio’s pay roll system is made to for the organization employees to fill time

cards in used for collecting data regarding the total hours that the employees have worked.

Figure 3 below shows a flow diagram for the payroll system.

will then get submitted to the company’s treasure who will sign it and further mail it to vendors.

Consequently, the account payable control and account payable subsidiaries cheque get updated

from the computer terminals. Afterwards, the records will then get submitted to the receiving

departments to file invoices, receive copies of check and reports as well as copies of purchase

order.

Data flow diagram for payroll system

The Bell Studio’s pay roll system is made to for the organization employees to fill time

cards in used for collecting data regarding the total hours that the employees have worked.

Figure 3 below shows a flow diagram for the payroll system.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Prepares cash

disbursement

vouchers

Payroll DepartmentEmployees Time Cards

Supervisors

Central Payroll SystemTime Card data

Payroll register

Payroll register

Supervisor

AC Department

Write ChequesCheque file

Imprest bank

General ledger

department

Cheque file

Department Employees

Reviews and submits

Hour’s records

Digital Employee Record

Reviews and submits

Deposits

Reviews

Check

Strategic Information Systems for Business and Enterprise 10

Figure 3: data flow diagram for payroll system

The organization supervisors review the information that is conveyed by the time card

after which they forward it to the payroll department. After the information is submitted to the

payroll department, the clerk will then send the employees cheque for review and distribution by

the supervisors after filing the time cards (Tarapata, Intuit Inc, 2009, pp.08). Consequently, the

disbursement

vouchers

Payroll DepartmentEmployees Time Cards

Supervisors

Central Payroll SystemTime Card data

Payroll register

Payroll register

Supervisor

AC Department

Write ChequesCheque file

Imprest bank

General ledger

department

Cheque file

Department Employees

Reviews and submits

Hour’s records

Digital Employee Record

Reviews and submits

Deposits

Reviews

Check

Strategic Information Systems for Business and Enterprise 10

Figure 3: data flow diagram for payroll system

The organization supervisors review the information that is conveyed by the time card

after which they forward it to the payroll department. After the information is submitted to the

payroll department, the clerk will then send the employees cheque for review and distribution by

the supervisors after filing the time cards (Tarapata, Intuit Inc, 2009, pp.08). Consequently, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Information Systems for Business and Enterprise 11

clerk will send payroll register copies to the accounts payable and other time card copies to the

payroll department.

Account payable clerks will then review the registers submitted and then manually make

the cash disbursement voucher then submit the register containing the payroll to the department

of general ledgers and the account payable clerk drafts a payroll cheque after which the checks

are submitted to banks.

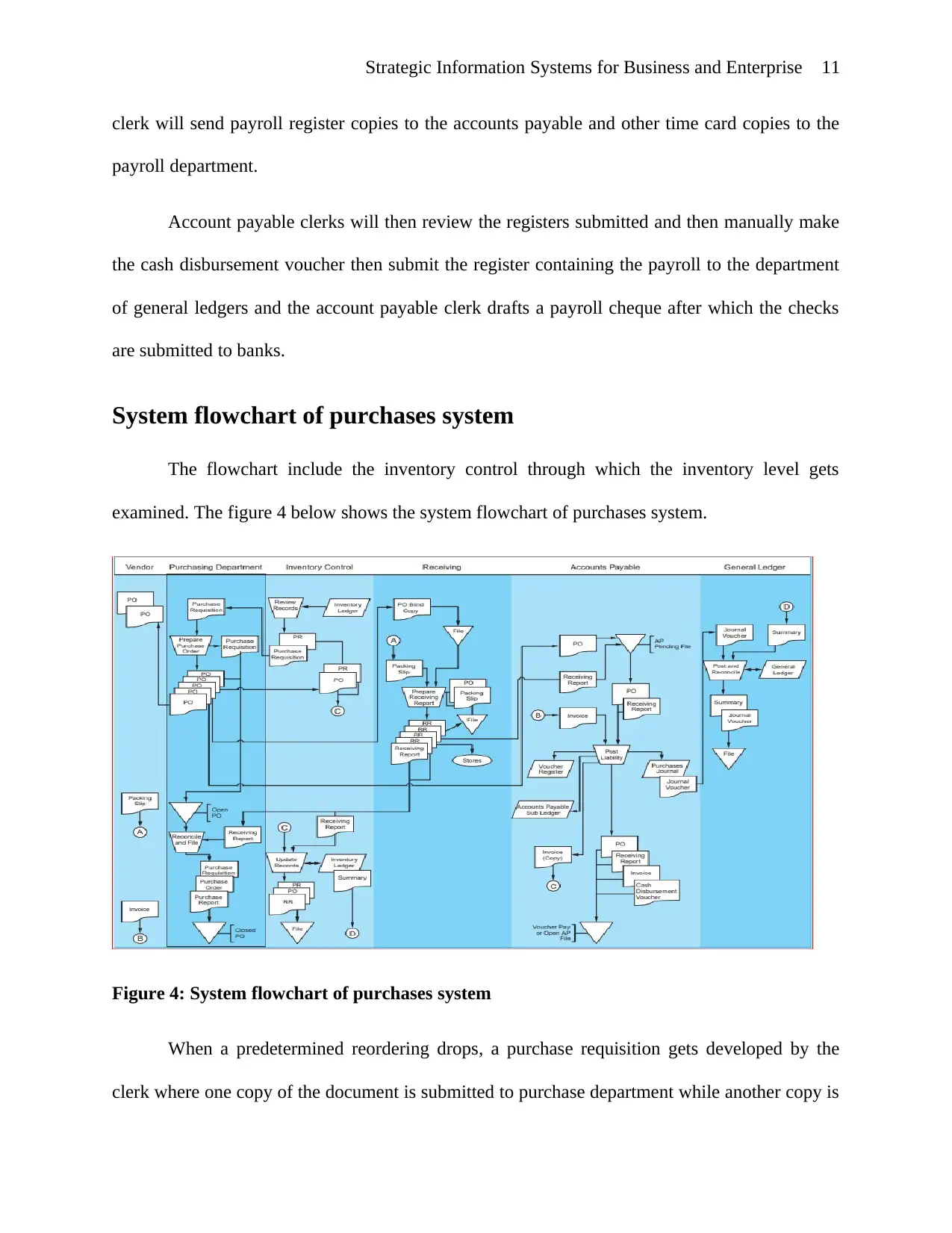

System flowchart of purchases system

The flowchart include the inventory control through which the inventory level gets

examined. The figure 4 below shows the system flowchart of purchases system.

Figure 4: System flowchart of purchases system

When a predetermined reordering drops, a purchase requisition gets developed by the

clerk where one copy of the document is submitted to purchase department while another copy is

clerk will send payroll register copies to the accounts payable and other time card copies to the

payroll department.

Account payable clerks will then review the registers submitted and then manually make

the cash disbursement voucher then submit the register containing the payroll to the department

of general ledgers and the account payable clerk drafts a payroll cheque after which the checks

are submitted to banks.

System flowchart of purchases system

The flowchart include the inventory control through which the inventory level gets

examined. The figure 4 below shows the system flowchart of purchases system.

Figure 4: System flowchart of purchases system

When a predetermined reordering drops, a purchase requisition gets developed by the

clerk where one copy of the document is submitted to purchase department while another copy is

Strategic Information Systems for Business and Enterprise 12

filed in the requisition file. The process follows the requisition purchase sorting by the vendors

and development of the purchase orders for vendors from relevant departments. The purchase

orders is produced into two copies which are submitted to the vendor while another copy

submitted to inventory control panel where they are filled with the present purchasing requisition

(Kim H.J., Kim D.Y., Sung, and Jin, Samsung Electronics Co Ltd, 2009, pp.51). Items from the

vendor will afterwards get reconciled with blind copies of purchase orders.

On completing the inspection and physical accounting process, the reports will be drafted

by the receiving clerks stating the quantities and conditions of inventories. The copies of the

report are submitted to the purchase and inventory departments after then the clerk will reconcile

it with the purchase orders available. The clerk will get the submitted invoices in the account

payable department from which the information is reconciled with the pending document files

that are available. On receiving these document, a record showing a relevant transaction get

arranged. Before, this is done, a record of liabilities through which a clerk sends his sourced and

send relevant files is done. At this point, the digital account payable subsidiaries ledgers get

updated. After this, the purchase orders copies, invoices and receiving reports are submitted to

the cash disbursement sectors.

filed in the requisition file. The process follows the requisition purchase sorting by the vendors

and development of the purchase orders for vendors from relevant departments. The purchase

orders is produced into two copies which are submitted to the vendor while another copy

submitted to inventory control panel where they are filled with the present purchasing requisition

(Kim H.J., Kim D.Y., Sung, and Jin, Samsung Electronics Co Ltd, 2009, pp.51). Items from the

vendor will afterwards get reconciled with blind copies of purchase orders.

On completing the inspection and physical accounting process, the reports will be drafted

by the receiving clerks stating the quantities and conditions of inventories. The copies of the

report are submitted to the purchase and inventory departments after then the clerk will reconcile

it with the purchase orders available. The clerk will get the submitted invoices in the account

payable department from which the information is reconciled with the pending document files

that are available. On receiving these document, a record showing a relevant transaction get

arranged. Before, this is done, a record of liabilities through which a clerk sends his sourced and

send relevant files is done. At this point, the digital account payable subsidiaries ledgers get

updated. After this, the purchase orders copies, invoices and receiving reports are submitted to

the cash disbursement sectors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.