Bell Studio Case Study Report: Analysis of Transaction Cycles, HI5019

VerifiedAdded on 2022/12/15

|17

|3572

|386

Case Study

AI Summary

This report presents a comprehensive analysis of the Bell Studio case study, focusing on its accounting information system and operational processes. The report examines the company's purchases, cash disbursement, and payroll systems, utilizing data flow diagrams and system flowcharts to illustrate the processes. The analysis covers transaction cycles, financial reporting, and management reporting systems, providing insights into the company's expenditure cycle. Furthermore, the report identifies internal control weaknesses within each system and assesses the associated risks. The study highlights the importance of accounting software in improving the accuracy and security of financial information, while also exploring the implications of increased shareholder numbers. Overall, the report provides a detailed overview of Bell Studio's operations and the critical role of information systems in its financial management and decision-making processes.

Bell Studio Case Study Report

Student’s name

Institution Affiliation(s)

Student’s name

Institution Affiliation(s)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................1

Executive Summary.........................................................................................................................3

Introduction......................................................................................................................................4

Data flow diagram of purchases and cash disbursements systems..................................................4

Data flow diagram of payroll system...............................................................................................7

System flowchart of purchases system............................................................................................8

System flowchart of cash disbursements system...........................................................................10

System flowchart of payroll system..............................................................................................11

Internal Control..............................................................................................................................13

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

Table of Figures

Figure 1: Data flow diagram of purchases and cash disbursements systems...............................................4

Figure 2: Data flow diagram of payroll system...........................................................................................6

Figure 3: System flowchart of purchases system.........................................................................................7

Figure 4: System flowchart of cash disbursements system..........................................................................9

Figure 5: System flowchart of payroll system...........................................................................................10

1

Table of Contents.............................................................................................................................1

Executive Summary.........................................................................................................................3

Introduction......................................................................................................................................4

Data flow diagram of purchases and cash disbursements systems..................................................4

Data flow diagram of payroll system...............................................................................................7

System flowchart of purchases system............................................................................................8

System flowchart of cash disbursements system...........................................................................10

System flowchart of payroll system..............................................................................................11

Internal Control..............................................................................................................................13

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

Table of Figures

Figure 1: Data flow diagram of purchases and cash disbursements systems...............................................4

Figure 2: Data flow diagram of payroll system...........................................................................................6

Figure 3: System flowchart of purchases system.........................................................................................7

Figure 4: System flowchart of cash disbursements system..........................................................................9

Figure 5: System flowchart of payroll system...........................................................................................10

1

Executive Summary

This is a report analyzing the Bell Studio Company which outsources its various

inventories from manufacturers around the world including New Zealand, Japan, China, and

Australia. Bell Studio uses a centralized accounting system that has networked terminals at each

of the company’s different locations. The report analyses the three main departments at Bell

Studio organization which are the purchases system, cash disbursement system and the payroll

system. The case study describes Bell Studio’s expenditure cycle procedures and their use of an

accounting information system.

2

This is a report analyzing the Bell Studio Company which outsources its various

inventories from manufacturers around the world including New Zealand, Japan, China, and

Australia. Bell Studio uses a centralized accounting system that has networked terminals at each

of the company’s different locations. The report analyses the three main departments at Bell

Studio organization which are the purchases system, cash disbursement system and the payroll

system. The case study describes Bell Studio’s expenditure cycle procedures and their use of an

accounting information system.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The report is prepared by a business analyst for use by the management and the decision

makers of Bell Studio. The report analyses the Bell Studio case study by describing the various

transaction cycles, financial reporting, e-commerce, and management reporting systems (Trigo,

Belfo, & Estébanez, 2014). The case study has identified three main departments that need

describing these departments are the payroll system, cash disbursement system and the purchases

system.

The report will be structured by having a cover page, an executive summary, an

introduction, the conclusion and the main body where these three systems will be described, that

is the purchases system, the cash disbursement system and the payroll system. The report will

use both data flow diagrams and system flowchart diagrams for easier analysis of the system. At

the end of the report, the internal control weakness in each of these three systems and the risk

associated with the identified weaknesses.

Data flow diagram of purchases and cash disbursements

systems

The use of accounting software has enabled the timely provision of financial statements

to the decision-makers for Bell Studio. For instance, the balance sheet shows the financial

position of the company in terms of asset, liabilities and equity availability (Belfo & Trigo,

2013). Since the previous data is also provided, the management of Bell Studio is able to notice

any favourable or unfavourable changes in the company’s assets, liabilities and equity levels. It,

therefore, eases the identification of items that exhibit unfavourable changes. For example, a

trend showing a reduction in the net profit of the company could be used to make decisions and

implement strategies that increase the cash flow generation for Bell Studio. Thus, the accounting

3

The report is prepared by a business analyst for use by the management and the decision

makers of Bell Studio. The report analyses the Bell Studio case study by describing the various

transaction cycles, financial reporting, e-commerce, and management reporting systems (Trigo,

Belfo, & Estébanez, 2014). The case study has identified three main departments that need

describing these departments are the payroll system, cash disbursement system and the purchases

system.

The report will be structured by having a cover page, an executive summary, an

introduction, the conclusion and the main body where these three systems will be described, that

is the purchases system, the cash disbursement system and the payroll system. The report will

use both data flow diagrams and system flowchart diagrams for easier analysis of the system. At

the end of the report, the internal control weakness in each of these three systems and the risk

associated with the identified weaknesses.

Data flow diagram of purchases and cash disbursements

systems

The use of accounting software has enabled the timely provision of financial statements

to the decision-makers for Bell Studio. For instance, the balance sheet shows the financial

position of the company in terms of asset, liabilities and equity availability (Belfo & Trigo,

2013). Since the previous data is also provided, the management of Bell Studio is able to notice

any favourable or unfavourable changes in the company’s assets, liabilities and equity levels. It,

therefore, eases the identification of items that exhibit unfavourable changes. For example, a

trend showing a reduction in the net profit of the company could be used to make decisions and

implement strategies that increase the cash flow generation for Bell Studio. Thus, the accounting

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information system has significantly reduced a great deal of the workload in the accounting

department of Bell Studio (Worrell, Gangi, & Bush, 2013)

Forecasting sales, profit/loss - using the historical information contained in the

Company’s financial statement, it is possible to forecast items such as sales level and profit or

loss in order to determine the future level of sales and profit/loss. Companies can, therefore, use

negative forecast information to make decisions and implement loss minimization strategies and

increase the profitability level (Brandas, Megan, & Didraga, 2015).

Figure 1: Data flow diagram of purchases and cash disbursements systems

4

department of Bell Studio (Worrell, Gangi, & Bush, 2013)

Forecasting sales, profit/loss - using the historical information contained in the

Company’s financial statement, it is possible to forecast items such as sales level and profit or

loss in order to determine the future level of sales and profit/loss. Companies can, therefore, use

negative forecast information to make decisions and implement loss minimization strategies and

increase the profitability level (Brandas, Megan, & Didraga, 2015).

Figure 1: Data flow diagram of purchases and cash disbursements systems

4

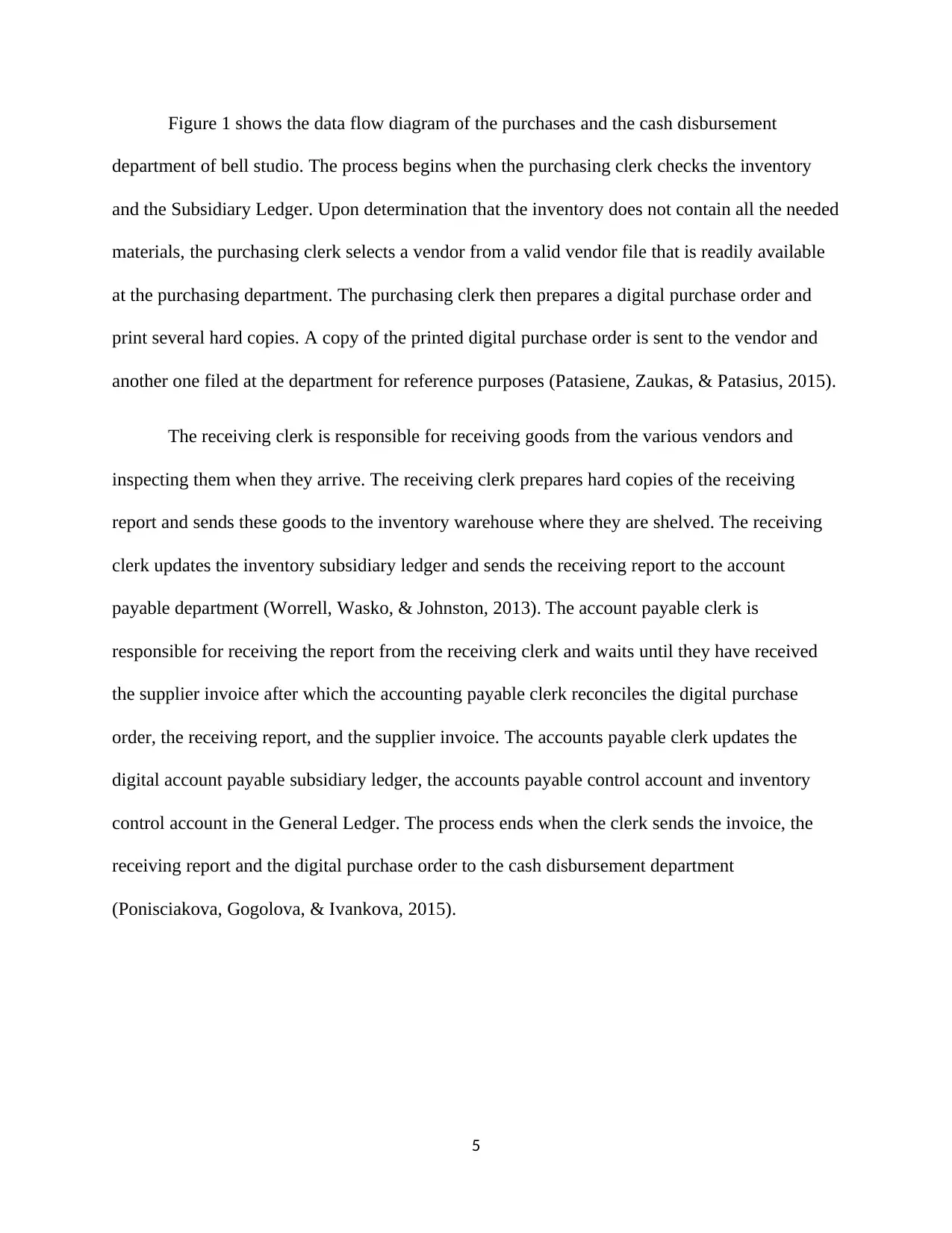

Figure 1 shows the data flow diagram of the purchases and the cash disbursement

department of bell studio. The process begins when the purchasing clerk checks the inventory

and the Subsidiary Ledger. Upon determination that the inventory does not contain all the needed

materials, the purchasing clerk selects a vendor from a valid vendor file that is readily available

at the purchasing department. The purchasing clerk then prepares a digital purchase order and

print several hard copies. A copy of the printed digital purchase order is sent to the vendor and

another one filed at the department for reference purposes (Patasiene, Zaukas, & Patasius, 2015).

The receiving clerk is responsible for receiving goods from the various vendors and

inspecting them when they arrive. The receiving clerk prepares hard copies of the receiving

report and sends these goods to the inventory warehouse where they are shelved. The receiving

clerk updates the inventory subsidiary ledger and sends the receiving report to the account

payable department (Worrell, Wasko, & Johnston, 2013). The account payable clerk is

responsible for receiving the report from the receiving clerk and waits until they have received

the supplier invoice after which the accounting payable clerk reconciles the digital purchase

order, the receiving report, and the supplier invoice. The accounts payable clerk updates the

digital account payable subsidiary ledger, the accounts payable control account and inventory

control account in the General Ledger. The process ends when the clerk sends the invoice, the

receiving report and the digital purchase order to the cash disbursement department

(Ponisciakova, Gogolova, & Ivankova, 2015).

5

department of bell studio. The process begins when the purchasing clerk checks the inventory

and the Subsidiary Ledger. Upon determination that the inventory does not contain all the needed

materials, the purchasing clerk selects a vendor from a valid vendor file that is readily available

at the purchasing department. The purchasing clerk then prepares a digital purchase order and

print several hard copies. A copy of the printed digital purchase order is sent to the vendor and

another one filed at the department for reference purposes (Patasiene, Zaukas, & Patasius, 2015).

The receiving clerk is responsible for receiving goods from the various vendors and

inspecting them when they arrive. The receiving clerk prepares hard copies of the receiving

report and sends these goods to the inventory warehouse where they are shelved. The receiving

clerk updates the inventory subsidiary ledger and sends the receiving report to the account

payable department (Worrell, Wasko, & Johnston, 2013). The account payable clerk is

responsible for receiving the report from the receiving clerk and waits until they have received

the supplier invoice after which the accounting payable clerk reconciles the digital purchase

order, the receiving report, and the supplier invoice. The accounts payable clerk updates the

digital account payable subsidiary ledger, the accounts payable control account and inventory

control account in the General Ledger. The process ends when the clerk sends the invoice, the

receiving report and the digital purchase order to the cash disbursement department

(Ponisciakova, Gogolova, & Ivankova, 2015).

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Data flow diagram of payroll system

Figure 2: Data flow diagram of payroll system

Figure 2 shows a data flow diagram for the payroll department of Bell Studio Company.

The payroll department processes starts when the payroll clerk receives time card from various

employees and inputs the data to the accounting system. The payroll clerk prints hard copies of

the time cards and posts the same to the digital employee’s record. The payroll clerk is also

responsible for filing these time cards in the payroll department (McLaren, Appleyard, &

Mitchell, 2016).

6

Figure 2: Data flow diagram of payroll system

Figure 2 shows a data flow diagram for the payroll department of Bell Studio Company.

The payroll department processes starts when the payroll clerk receives time card from various

employees and inputs the data to the accounting system. The payroll clerk prints hard copies of

the time cards and posts the same to the digital employee’s record. The payroll clerk is also

responsible for filing these time cards in the payroll department (McLaren, Appleyard, &

Mitchell, 2016).

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The payroll clerk sends cheque to the department supervisors for signing. Also, the

payroll clerk sends copies of the payroll register to the accounts payable department which is

responsible for reviewing them and then manually preparing disbursement vouchers. The

account payable clerk sends the payroll register and the disbursement voucher to the general

ledger department after which the general ledger department post these documents to the general

ledger and files a copy for use in the department (Spånberg & Shahnazarian, 2019).

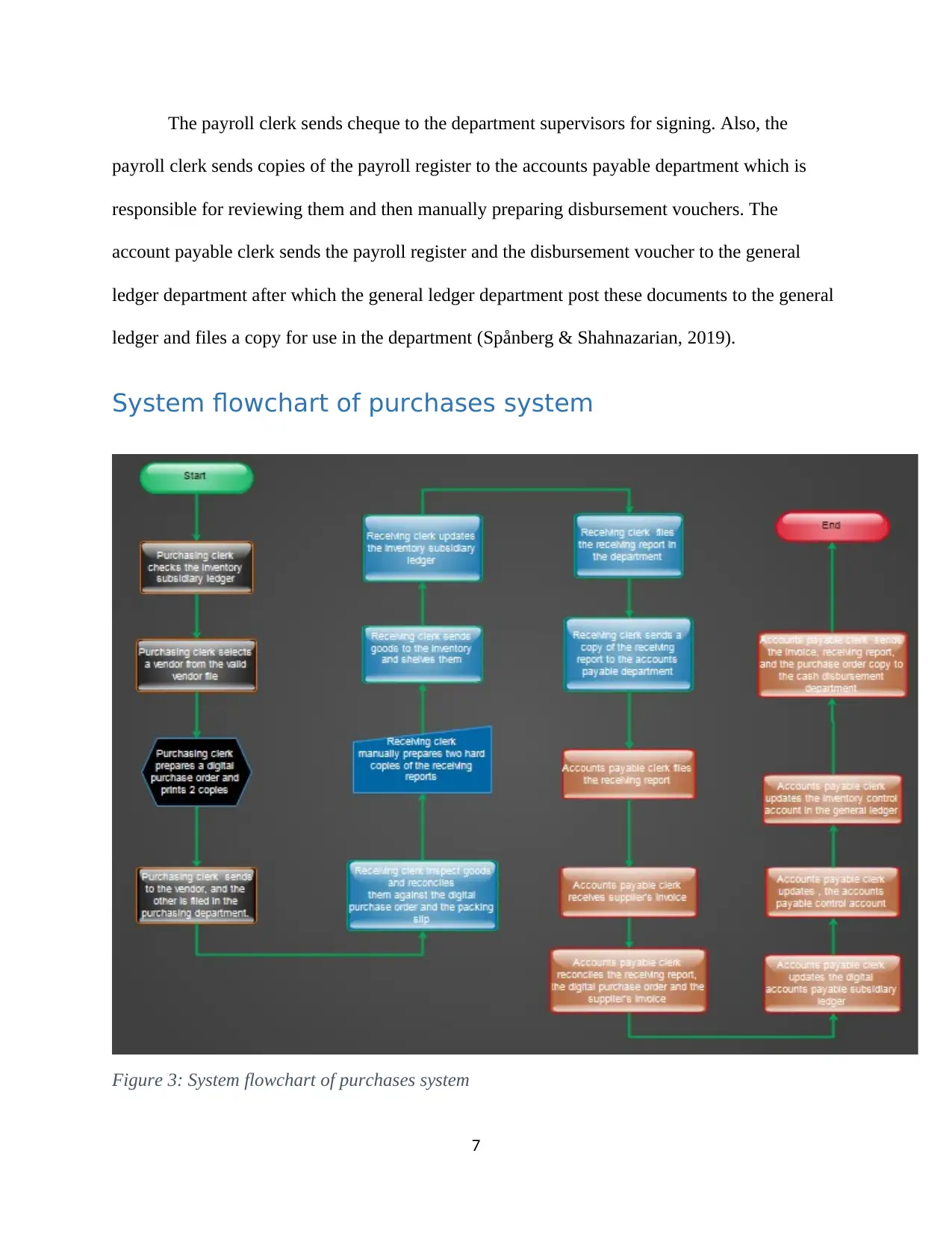

System flowchart of purchases system

Figure 3: System flowchart of purchases system

7

payroll clerk sends copies of the payroll register to the accounts payable department which is

responsible for reviewing them and then manually preparing disbursement vouchers. The

account payable clerk sends the payroll register and the disbursement voucher to the general

ledger department after which the general ledger department post these documents to the general

ledger and files a copy for use in the department (Spånberg & Shahnazarian, 2019).

System flowchart of purchases system

Figure 3: System flowchart of purchases system

7

Figure 3 shows the system flowchart for the purchases system. The purchasing

department of Bell Studio has the longest process that cuts across the purchasing department the

receiving department and the accounts payable department. Therefore, the purchasing clerk the

receiving clerk and the accounts payable clerks are involved in the major processes (Ghasemi,

Shafeiepour, Aslani, & Barvayeh, 2011).

The process starts when the purchasing clerk checks the inventory subsidiary ledger for

any goods or materials that are not enough or need refiling. Upon determining which materials

need to be ordered from the vendors, the purchasing clerk selects the most suitable vendor from a

list of vendors that is available at the purchasing department. The purchasing clerk prepares a

digital purchase order and print two copies. The digital purchase order is sent to the vendor and

the other one filed at the purchasing department for reference purposes. After this, the receiving

clerk takes on the process by inspecting the goods that are coming from the various vendors

against the digital purchase order and the packing slip (Thomas, 2016).

The receiving clerk is responsible for preparing a manual copy of the receiving report.

Two copies are prepared, and a copy of the receiving report is sent to the accounts payable

department. After preparing this report, the receiving clerk sends goods to the inventory

warehouse where they have shelved. The receiving clerk updates the inventory subsidiary ledger

and files a copy of the receiving report for use in the department. From here the accounts payable

clerk is responsible for the next phase of the process.

The accounts payable clerk is responsible for receiving the receiving report and files it

awaiting the arrival of the supplier invoice. On its arrival the accounts payable clerk reconciles

the three documents, that is, the receiving report the digital purchase order and the supplier's

invoice (Lapinskas & Shubentseva, 2014).

8

department of Bell Studio has the longest process that cuts across the purchasing department the

receiving department and the accounts payable department. Therefore, the purchasing clerk the

receiving clerk and the accounts payable clerks are involved in the major processes (Ghasemi,

Shafeiepour, Aslani, & Barvayeh, 2011).

The process starts when the purchasing clerk checks the inventory subsidiary ledger for

any goods or materials that are not enough or need refiling. Upon determining which materials

need to be ordered from the vendors, the purchasing clerk selects the most suitable vendor from a

list of vendors that is available at the purchasing department. The purchasing clerk prepares a

digital purchase order and print two copies. The digital purchase order is sent to the vendor and

the other one filed at the purchasing department for reference purposes. After this, the receiving

clerk takes on the process by inspecting the goods that are coming from the various vendors

against the digital purchase order and the packing slip (Thomas, 2016).

The receiving clerk is responsible for preparing a manual copy of the receiving report.

Two copies are prepared, and a copy of the receiving report is sent to the accounts payable

department. After preparing this report, the receiving clerk sends goods to the inventory

warehouse where they have shelved. The receiving clerk updates the inventory subsidiary ledger

and files a copy of the receiving report for use in the department. From here the accounts payable

clerk is responsible for the next phase of the process.

The accounts payable clerk is responsible for receiving the receiving report and files it

awaiting the arrival of the supplier invoice. On its arrival the accounts payable clerk reconciles

the three documents, that is, the receiving report the digital purchase order and the supplier's

invoice (Lapinskas & Shubentseva, 2014).

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The accounts payable clerk then update the digital accounts payable subsidiary ledger,

the account payable control account and the accounts payable inventory control account in the

general ledger. The process ends with the accounts payable clerk sending the receiving report,

the invoice and the purchasing order to the cash disbursement department.

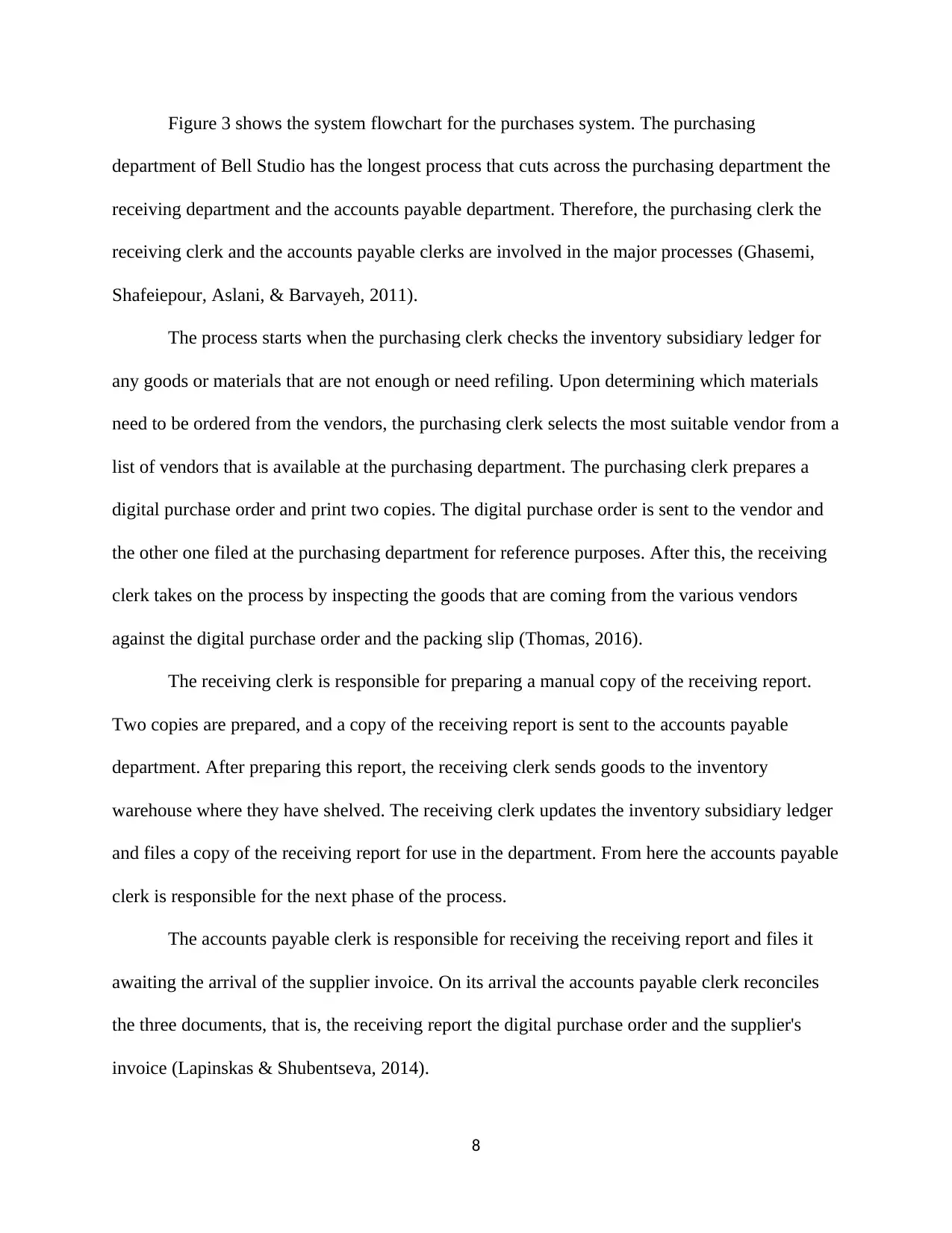

System flowchart of cash disbursements system

Figure 4: System flowchart of cash disbursements system

Figure 4 shows the system flowchart of the cash disbursement department. The process

starts when the cash disbursement clerk receives documents from the account payable

department and then files the received documents (Edmonds, Miller, & Savage, 2019).

9

the account payable control account and the accounts payable inventory control account in the

general ledger. The process ends with the accounts payable clerk sending the receiving report,

the invoice and the purchasing order to the cash disbursement department.

System flowchart of cash disbursements system

Figure 4: System flowchart of cash disbursements system

Figure 4 shows the system flowchart of the cash disbursement department. The process

starts when the cash disbursement clerk receives documents from the account payable

department and then files the received documents (Edmonds, Miller, & Savage, 2019).

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The cash disbursement clerk prepares a cheque for the invoiced accounts and then sends

this cheque to the department supervisors who are responsible for signing them. The clerk then

updates the check register, the accounts payable subsidiary ledger and the accounts payable

control account. When this is done the cash disbursement clerk handles the process to the

receiving clerk who files the invoice, the digital purchase order, the receiving report and a copy

of the cheque (Trigo, Belfo, & Estébanez, 2016).

System flowchart of payroll system

Figure 5: Payroll Department System flowchart

Figure 5 shows a system flowchart for the payroll department of Bell Studio Company.

The payroll department has its processes starting when the payroll clerk inputs data and time

card as received from various employees. The payroll clerk goes ahead to print hard copies of the

10

this cheque to the department supervisors who are responsible for signing them. The clerk then

updates the check register, the accounts payable subsidiary ledger and the accounts payable

control account. When this is done the cash disbursement clerk handles the process to the

receiving clerk who files the invoice, the digital purchase order, the receiving report and a copy

of the cheque (Trigo, Belfo, & Estébanez, 2016).

System flowchart of payroll system

Figure 5: Payroll Department System flowchart

Figure 5 shows a system flowchart for the payroll department of Bell Studio Company.

The payroll department has its processes starting when the payroll clerk inputs data and time

card as received from various employees. The payroll clerk goes ahead to print hard copies of the

10

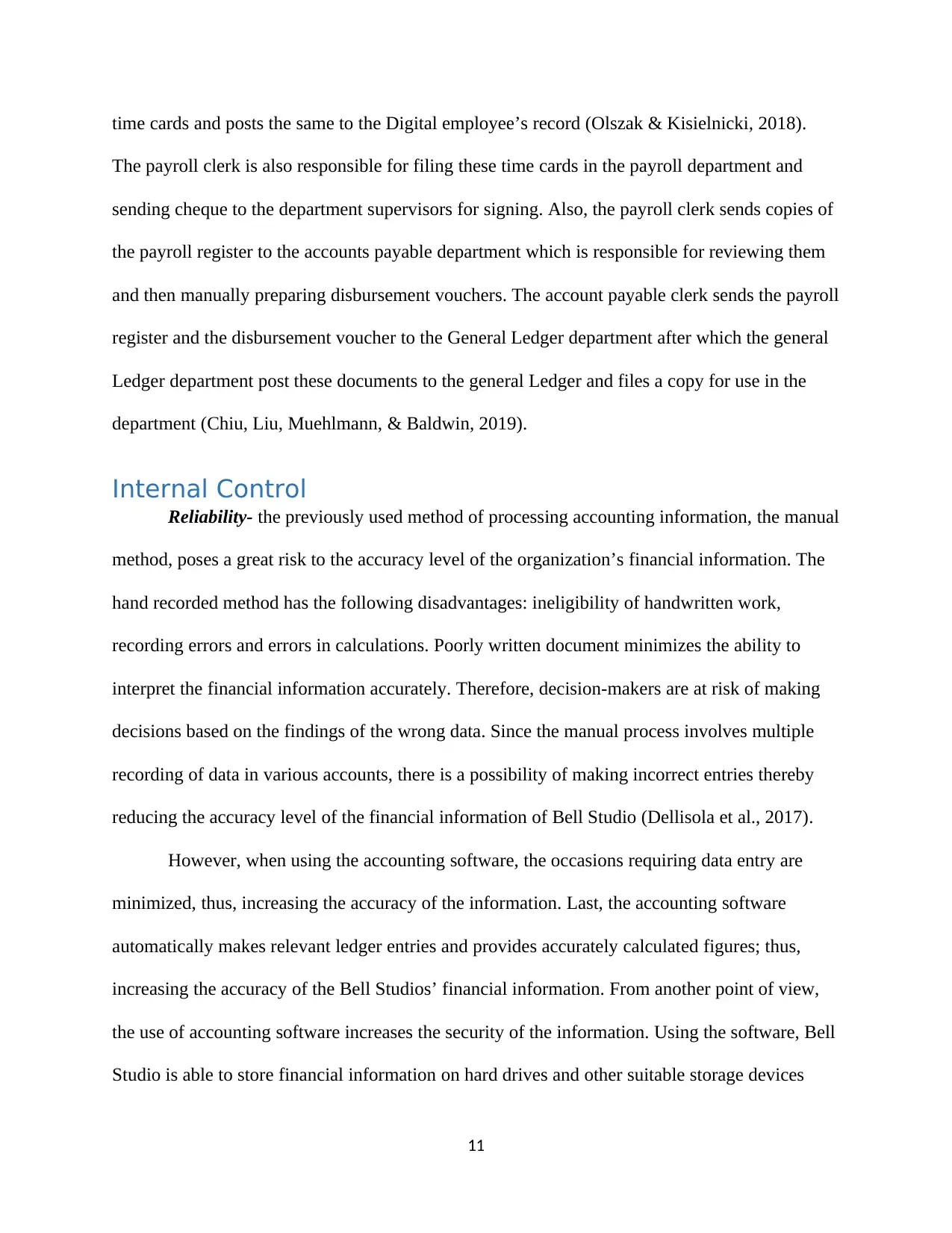

time cards and posts the same to the Digital employee’s record (Olszak & Kisielnicki, 2018).

The payroll clerk is also responsible for filing these time cards in the payroll department and

sending cheque to the department supervisors for signing. Also, the payroll clerk sends copies of

the payroll register to the accounts payable department which is responsible for reviewing them

and then manually preparing disbursement vouchers. The account payable clerk sends the payroll

register and the disbursement voucher to the General Ledger department after which the general

Ledger department post these documents to the general Ledger and files a copy for use in the

department (Chiu, Liu, Muehlmann, & Baldwin, 2019).

Internal Control

Reliability- the previously used method of processing accounting information, the manual

method, poses a great risk to the accuracy level of the organization’s financial information. The

hand recorded method has the following disadvantages: ineligibility of handwritten work,

recording errors and errors in calculations. Poorly written document minimizes the ability to

interpret the financial information accurately. Therefore, decision-makers are at risk of making

decisions based on the findings of the wrong data. Since the manual process involves multiple

recording of data in various accounts, there is a possibility of making incorrect entries thereby

reducing the accuracy level of the financial information of Bell Studio (Dellisola et al., 2017).

However, when using the accounting software, the occasions requiring data entry are

minimized, thus, increasing the accuracy of the information. Last, the accounting software

automatically makes relevant ledger entries and provides accurately calculated figures; thus,

increasing the accuracy of the Bell Studios’ financial information. From another point of view,

the use of accounting software increases the security of the information. Using the software, Bell

Studio is able to store financial information on hard drives and other suitable storage devices

11

The payroll clerk is also responsible for filing these time cards in the payroll department and

sending cheque to the department supervisors for signing. Also, the payroll clerk sends copies of

the payroll register to the accounts payable department which is responsible for reviewing them

and then manually preparing disbursement vouchers. The account payable clerk sends the payroll

register and the disbursement voucher to the General Ledger department after which the general

Ledger department post these documents to the general Ledger and files a copy for use in the

department (Chiu, Liu, Muehlmann, & Baldwin, 2019).

Internal Control

Reliability- the previously used method of processing accounting information, the manual

method, poses a great risk to the accuracy level of the organization’s financial information. The

hand recorded method has the following disadvantages: ineligibility of handwritten work,

recording errors and errors in calculations. Poorly written document minimizes the ability to

interpret the financial information accurately. Therefore, decision-makers are at risk of making

decisions based on the findings of the wrong data. Since the manual process involves multiple

recording of data in various accounts, there is a possibility of making incorrect entries thereby

reducing the accuracy level of the financial information of Bell Studio (Dellisola et al., 2017).

However, when using the accounting software, the occasions requiring data entry are

minimized, thus, increasing the accuracy of the information. Last, the accounting software

automatically makes relevant ledger entries and provides accurately calculated figures; thus,

increasing the accuracy of the Bell Studios’ financial information. From another point of view,

the use of accounting software increases the security of the information. Using the software, Bell

Studio is able to store financial information on hard drives and other suitable storage devices

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.