Financial Report Analysis: Auditing and Assurance of Bellamy's Limited

VerifiedAdded on 2022/08/13

|11

|2185

|29

Report

AI Summary

This report provides an analysis of the auditing and assurance of Bellamy's Australia Limited's financial performance. The report examines related party transactions, including the absence of borrowings or trade transactions between the company and associated parties. It evaluates changes in accounting policies, such as the adoption of AASB15 and AASB16, and their impact on the financial statements. Preliminary analytical procedures, including liquidity and profitability ratios, are calculated and assessed, with discussions on the current ratio, quick ratio, gross profit margin, net profit margin, and asset turnover. The report emphasizes the importance of the audit and risk committee, the external auditor's role, and the directors' responsibility for presenting accurate financial statements. The conclusion summarizes the key findings and reinforces the significance of financial statement compliance with Australian Accounting Standards and the Corporation Act 2001. The appendix provides a ratio analysis, comparing financial data from 2019 and 2018. The report concludes with a call for the directors and management to continue to strive for the company's growth and expansion.

Running head: AUDITING AND ASSURANCE

AUDITING AND ASSURANCE

Name of the Student:

Name of the University:

Author Note:

AUDITING AND ASSURANCE

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE

Executive Summary

The report focuses on annual report of Bellamy’s Australia Limited, which is one of the

dominant infant nutrition and food Brand Company in Australia and China. In this report, the

focus will be on the related party transaction during the financial year. Variations in

financials regulations and plans, how variations affect the company is evaluated. Specific

ratios are calculated, which reflects the profitability and position of the firm in the market.

Lastly, the ability of the company to operate in the long-run is discussed in the report.

Executive Summary

The report focuses on annual report of Bellamy’s Australia Limited, which is one of the

dominant infant nutrition and food Brand Company in Australia and China. In this report, the

focus will be on the related party transaction during the financial year. Variations in

financials regulations and plans, how variations affect the company is evaluated. Specific

ratios are calculated, which reflects the profitability and position of the firm in the market.

Lastly, the ability of the company to operate in the long-run is discussed in the report.

2AUDITING AND ASSURANCE

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

Related parties and transaction with relevant parties.............................................................4

Controlled entities..................................................................................................................4

Non-controlled entities...........................................................................................................4

Other related parties...............................................................................................................4

Transaction with related parties in the financial year............................................................5

Changes in accounting policies and the impact of changes...................................................5

Preliminary analytical procedures..........................................................................................6

Conclusion..................................................................................................................................8

Appendix....................................................................................................................................9

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

Related parties and transaction with relevant parties.............................................................4

Controlled entities..................................................................................................................4

Non-controlled entities...........................................................................................................4

Other related parties...............................................................................................................4

Transaction with related parties in the financial year............................................................5

Changes in accounting policies and the impact of changes...................................................5

Preliminary analytical procedures..........................................................................................6

Conclusion..................................................................................................................................8

Appendix....................................................................................................................................9

References................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE

Introduction

In this report, the discussion is about one of leading food brand company in Australia.

The company has almost forty products, such as organic food, toddler milk, infant milk, and

many more. It mainly aims to provide nutritious food and formula products useful for infants

and children. This company has almost forty products, such as organic food, toddler milk,

infant milk, and many more. It mainly aims to provide nutritious food and formula products

useful for infants and children. The company has almost forty products, such as organic food,

toddler milk, infant milk, and many more. It mainly aims to provide nutritious food and

formula products useful for infants and children. This company has almost forty products,

such as organic food, toddler milk, infant milk, and many more. It mainly aims to provide

nutritious food and formula products useful for infants and children. The report reflects

importance of audits in the company. Lastly, it concludes that directors are responsible for

preparing an accurate and fair annual report.

Introduction

In this report, the discussion is about one of leading food brand company in Australia.

The company has almost forty products, such as organic food, toddler milk, infant milk, and

many more. It mainly aims to provide nutritious food and formula products useful for infants

and children. This company has almost forty products, such as organic food, toddler milk,

infant milk, and many more. It mainly aims to provide nutritious food and formula products

useful for infants and children. The company has almost forty products, such as organic food,

toddler milk, infant milk, and many more. It mainly aims to provide nutritious food and

formula products useful for infants and children. This company has almost forty products,

such as organic food, toddler milk, infant milk, and many more. It mainly aims to provide

nutritious food and formula products useful for infants and children. The report reflects

importance of audits in the company. Lastly, it concludes that directors are responsible for

preparing an accurate and fair annual report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE

Discussion

Related parties and transaction with relevant parties

Related parties refer to the subsidiaries who are related to the company. There were

no borrowings transactions between the company and the associated parties during present

and previous year. Even a trade outstanding and trade receivable deal is not done during the

reporting date.

Controlled entities

The controlled entities of the Bellamy’s Australian Limited act in according to the

Corporation Act 2001. Even the accounting report of organization is in accordance with a

similar act (Abbott et al. 2016). The company and its controlled entities adhere to the

Australian Accounting Standards and the Corporation Regulation Act 2001. The financial

report of the organization reflects an accurate and equitable view of company and its

controlled entities. However, various proceedings between company and its controlled

subsidiaries are not mentioned in the annual financial report, even any disclosures relating to

them are not disclosed in notes to accounts.

Non-controlled entities

Any entity other than the group entity is known as a non-controlled entity. It refers to

any corporate undertaking or partnership that does not hold any controlling interest in the

company. In the annual financial report, there is no disclosure related to non-controlled

entities, which are related parties to the business. There has been the elimination of the non-

controlled entities on the consolidation statement and even in any notes to accounts.

Discussion

Related parties and transaction with relevant parties

Related parties refer to the subsidiaries who are related to the company. There were

no borrowings transactions between the company and the associated parties during present

and previous year. Even a trade outstanding and trade receivable deal is not done during the

reporting date.

Controlled entities

The controlled entities of the Bellamy’s Australian Limited act in according to the

Corporation Act 2001. Even the accounting report of organization is in accordance with a

similar act (Abbott et al. 2016). The company and its controlled entities adhere to the

Australian Accounting Standards and the Corporation Regulation Act 2001. The financial

report of the organization reflects an accurate and equitable view of company and its

controlled entities. However, various proceedings between company and its controlled

subsidiaries are not mentioned in the annual financial report, even any disclosures relating to

them are not disclosed in notes to accounts.

Non-controlled entities

Any entity other than the group entity is known as a non-controlled entity. It refers to

any corporate undertaking or partnership that does not hold any controlling interest in the

company. In the annual financial report, there is no disclosure related to non-controlled

entities, which are related parties to the business. There has been the elimination of the non-

controlled entities on the consolidation statement and even in any notes to accounts.

5AUDITING AND ASSURANCE

Other related parties

Key management personnel comes under the category of other associated parties of

the business. It includes directors and various members of the key management personnel.

Certain transactions, such as post-employment benefits, share-based payments and may more

employee benefits incurred during financial year (Išoraitė 2014). The director’s report of the

annual report contains information relating to variable remuneration associated with these

parties.

Transaction with related parties in the financial year

If there are any balances or transactions with associated parties, then it is to be

disclosed in the annual report for a clear understanding of business transaction. All the

stakeholders of the company depend on the yearly report for the decision-making process

(LU 2017). No transactions took place with related parties over entire financial year neither

in the previous year.

Changes in accounting policies and the impact of changes

Every company needs to operate in accordance with the accounting policies and

standards to provide a better understanding of accounting statements. If there are any changes

in accounting policies, proper disclosures should be there in the annual report and that, too,

with an appropriate reason for the particular changes. In this business, the accounting policies

are inconsistent with the standards however; there are changes in few cases such as the parent

entity recognize the dividends received as other incomes from Subsidiaries Company (Silviu-

Virgil 2014). If any investments are made in subsidiaries, it is recorded at cost less

impairment by the parent company (Spătărelu and Petec 2016).

Credit risk associated with the company is treated as an expense and not adjusted

against any revenue. The company needs to ensure that if the subsidiaries are using different

Other related parties

Key management personnel comes under the category of other associated parties of

the business. It includes directors and various members of the key management personnel.

Certain transactions, such as post-employment benefits, share-based payments and may more

employee benefits incurred during financial year (Išoraitė 2014). The director’s report of the

annual report contains information relating to variable remuneration associated with these

parties.

Transaction with related parties in the financial year

If there are any balances or transactions with associated parties, then it is to be

disclosed in the annual report for a clear understanding of business transaction. All the

stakeholders of the company depend on the yearly report for the decision-making process

(LU 2017). No transactions took place with related parties over entire financial year neither

in the previous year.

Changes in accounting policies and the impact of changes

Every company needs to operate in accordance with the accounting policies and

standards to provide a better understanding of accounting statements. If there are any changes

in accounting policies, proper disclosures should be there in the annual report and that, too,

with an appropriate reason for the particular changes. In this business, the accounting policies

are inconsistent with the standards however; there are changes in few cases such as the parent

entity recognize the dividends received as other incomes from Subsidiaries Company (Silviu-

Virgil 2014). If any investments are made in subsidiaries, it is recorded at cost less

impairment by the parent company (Spătărelu and Petec 2016).

Credit risk associated with the company is treated as an expense and not adjusted

against any revenue. The company needs to ensure that if the subsidiaries are using different

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE

accounting policies, then it should be consistent with the regulations of the group. If any

accounting policies and concepts are not as per the Australian Accounting Standards, the

group needs to revise the plans and to make sure that appropriate procedures are implemented

in the organization. The company has adopted AASB15 from 1 July 2018, and the main

principle of the standard is to recognize and measure all revenues and expenses incurred

during the accounting year. The standard introduces a single comprehensive model for

revenue recognition, and a model of contract-based revenue recognition is provided with a

measurement concept, which is based on the allotment of transaction costs. However, there

was no significant impact of accounting standards and interpretation in the financial

statement of the group. Modified retrospective concept is used to show the effects of

AASB15 on the financial statement of the group. The adoption of standards did not put any

effect on retained earnings of theorganization.

The standards and interpretations are not yet mandatory for the company, as it does

not use the rules for the financial year 2019. AASB16 lease was implemented in February

2016. This standard will record all contracts in consolidated balance sheet of company as

there will be no distinction between finance and operating lease; the short-term and low-value

rental are not included in this category. The primary impact of this standard will be on the

operating contracts of the business.

Preliminary analytical procedures

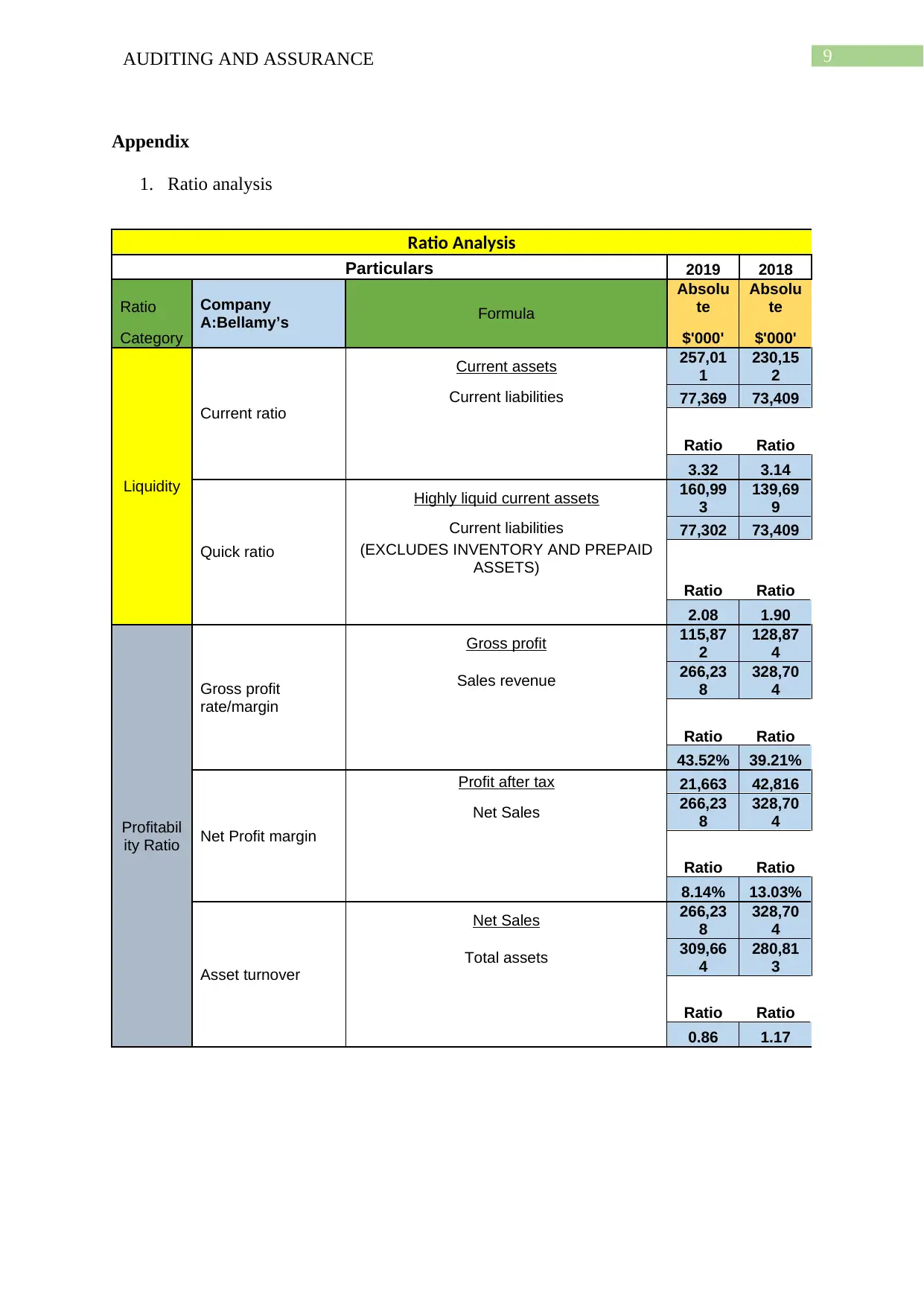

Liquidity ratios: The ratio explores the capability of business to meet its current debt

obligations, what is company's ability to pay off its current liabilities. The higher the ratio

more is the company's potentiality to pay off its debt and vice versa. Current ratio identifies

whether a company has ample resources to meet its present obligations. The quick ratio is

also known as acid test ratio (Gadoiu 2014). Comparison of total amount of cash and cash

equivalents, marketable securities, and account receivable is made to the total amount of

accounting policies, then it should be consistent with the regulations of the group. If any

accounting policies and concepts are not as per the Australian Accounting Standards, the

group needs to revise the plans and to make sure that appropriate procedures are implemented

in the organization. The company has adopted AASB15 from 1 July 2018, and the main

principle of the standard is to recognize and measure all revenues and expenses incurred

during the accounting year. The standard introduces a single comprehensive model for

revenue recognition, and a model of contract-based revenue recognition is provided with a

measurement concept, which is based on the allotment of transaction costs. However, there

was no significant impact of accounting standards and interpretation in the financial

statement of the group. Modified retrospective concept is used to show the effects of

AASB15 on the financial statement of the group. The adoption of standards did not put any

effect on retained earnings of theorganization.

The standards and interpretations are not yet mandatory for the company, as it does

not use the rules for the financial year 2019. AASB16 lease was implemented in February

2016. This standard will record all contracts in consolidated balance sheet of company as

there will be no distinction between finance and operating lease; the short-term and low-value

rental are not included in this category. The primary impact of this standard will be on the

operating contracts of the business.

Preliminary analytical procedures

Liquidity ratios: The ratio explores the capability of business to meet its current debt

obligations, what is company's ability to pay off its current liabilities. The higher the ratio

more is the company's potentiality to pay off its debt and vice versa. Current ratio identifies

whether a company has ample resources to meet its present obligations. The quick ratio is

also known as acid test ratio (Gadoiu 2014). Comparison of total amount of cash and cash

equivalents, marketable securities, and account receivable is made to the total amount of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE

current liabilities. Both the liquidity ratios are more than one; hence, the group reflects a

stable liquidity position and can pay off its current obligations.

Profitability ratios: These ratios are one type of financial ratios that reflects the

capability of business to gain earnings relating to its sales revenue, various assets, equities

and many more. The amount of investments used in assets of the organization can be

measured by evaluating asset turnover ratio, which is one type of profitability ratio. All

profitability ratios are in stable condition; however, the asset turnover ratio of 2019 is not

beneficial for the firm. The group needs to increase the asset turnover ratio in order to

increase the proficiency of the company to use its assets to obtain higher revenue.

The audit and risk committee helps the board and the management in carrying out its

responsibilities in an efficient manner (Abernathy et al. 2015). It assists the board regarding

financial reporting, internal control framework, external audit, and many more. The

Committee complies with the ASX listing rules and policies. If there is any material change

in the company, the committee reports the same to the board so that appropriate actions could

be taken to identify the reason for such material misstatements. Even the external auditor

complies with all the required auditing standards to provide a reasonable and fair audit report

for stakeholders of the company. Appropriate audit procedures are taken into consideration

for the identification of any material misstatement, which may occur due to fraud or error.

The audit procedure includes valuation of various assets such as goodwill, inventory, and

many more.

It is prime duty of directors and the management to produce an accurate and equitable

view of the financial statement as all the stakeholders of company to rely on the annual report

for the analysis of the position of the business in the market (Churet and Eccles 2014). The

directors need to ensure the report is free from any material misstatement and even make sure

current liabilities. Both the liquidity ratios are more than one; hence, the group reflects a

stable liquidity position and can pay off its current obligations.

Profitability ratios: These ratios are one type of financial ratios that reflects the

capability of business to gain earnings relating to its sales revenue, various assets, equities

and many more. The amount of investments used in assets of the organization can be

measured by evaluating asset turnover ratio, which is one type of profitability ratio. All

profitability ratios are in stable condition; however, the asset turnover ratio of 2019 is not

beneficial for the firm. The group needs to increase the asset turnover ratio in order to

increase the proficiency of the company to use its assets to obtain higher revenue.

The audit and risk committee helps the board and the management in carrying out its

responsibilities in an efficient manner (Abernathy et al. 2015). It assists the board regarding

financial reporting, internal control framework, external audit, and many more. The

Committee complies with the ASX listing rules and policies. If there is any material change

in the company, the committee reports the same to the board so that appropriate actions could

be taken to identify the reason for such material misstatements. Even the external auditor

complies with all the required auditing standards to provide a reasonable and fair audit report

for stakeholders of the company. Appropriate audit procedures are taken into consideration

for the identification of any material misstatement, which may occur due to fraud or error.

The audit procedure includes valuation of various assets such as goodwill, inventory, and

many more.

It is prime duty of directors and the management to produce an accurate and equitable

view of the financial statement as all the stakeholders of company to rely on the annual report

for the analysis of the position of the business in the market (Churet and Eccles 2014). The

directors need to ensure the report is free from any material misstatement and even make sure

8AUDITING AND ASSURANCE

that the financial report reflects a stable position of the business by which it can sustain for

the long-run. Matters related to going concern concept should be reflected in the financial

statement. For smooth and efficient functioning of the business, the company must be

following a going concern concept.

Conclusion

Lastly, the report concludes that all the related parties and various transactions related to

parties are discussed in detail. Liquidity and profitability ratios are calculated to reflect

position of the organization in market and to even sustain a long-run in the competitive

market situation. Analysis of annual reports to gain a clear picture of all transactions of the

business is done and financial statements should be in compliance with the Australian

Accounting Standards and the corporation act of 2001. Lastly, the report states that the

directors and the management should take steps for further growth and expansion of the

business.

that the financial report reflects a stable position of the business by which it can sustain for

the long-run. Matters related to going concern concept should be reflected in the financial

statement. For smooth and efficient functioning of the business, the company must be

following a going concern concept.

Conclusion

Lastly, the report concludes that all the related parties and various transactions related to

parties are discussed in detail. Liquidity and profitability ratios are calculated to reflect

position of the organization in market and to even sustain a long-run in the competitive

market situation. Analysis of annual reports to gain a clear picture of all transactions of the

business is done and financial statements should be in compliance with the Australian

Accounting Standards and the corporation act of 2001. Lastly, the report states that the

directors and the management should take steps for further growth and expansion of the

business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE

Appendix

1. Ratio analysis

Ratio Analysis

Particulars 2019 2018

Ratio Company

A:Bellamy’s Formula

Absolu

te

Absolu

te

Category $'000' $'000'

Liquidity

Current ratio

Current assets 257,01

1

230,15

2

Current liabilities 77,369 73,409

Ratio Ratio

3.32 3.14

Quick ratio

Highly liquid current assets 160,99

3

139,69

9

Current liabilities 77,302 73,409

(EXCLUDES INVENTORY AND PREPAID

ASSETS)

Ratio Ratio

2.08 1.90

Profitabil

ity Ratio

Gross profit

rate/margin

Gross profit 115,87

2

128,87

4

Sales revenue 266,23

8

328,70

4

Ratio Ratio

43.52% 39.21%

Net Profit margin

Profit after tax 21,663 42,816

Net Sales 266,23

8

328,70

4

Ratio Ratio

8.14% 13.03%

Asset turnover

Net Sales 266,23

8

328,70

4

Total assets 309,66

4

280,81

3

Ratio Ratio

0.86 1.17

Appendix

1. Ratio analysis

Ratio Analysis

Particulars 2019 2018

Ratio Company

A:Bellamy’s Formula

Absolu

te

Absolu

te

Category $'000' $'000'

Liquidity

Current ratio

Current assets 257,01

1

230,15

2

Current liabilities 77,369 73,409

Ratio Ratio

3.32 3.14

Quick ratio

Highly liquid current assets 160,99

3

139,69

9

Current liabilities 77,302 73,409

(EXCLUDES INVENTORY AND PREPAID

ASSETS)

Ratio Ratio

2.08 1.90

Profitabil

ity Ratio

Gross profit

rate/margin

Gross profit 115,87

2

128,87

4

Sales revenue 266,23

8

328,70

4

Ratio Ratio

43.52% 39.21%

Net Profit margin

Profit after tax 21,663 42,816

Net Sales 266,23

8

328,70

4

Ratio Ratio

8.14% 13.03%

Asset turnover

Net Sales 266,23

8

328,70

4

Total assets 309,66

4

280,81

3

Ratio Ratio

0.86 1.17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ASSURANCE

References

Abbott, L.J., Daugherty, B., Parker, S. and Peters, G.F., 2016. Internal audit quality and

financial reporting quality: The joint importance of independence and competence. Journal

of Accounting Research, 54(1), pp.3-40.

Abernathy, J.L., Beyer, B., Masli, A. and Stefaniak, C.M., 2015. How the source of audit

committee accounting expertise influences financial reporting timeliness. Current Issues in

Auditing, 9(1), pp.P1-P9.

Churet, C. and Eccles, R.G., 2014. Integrated reporting, quality of management, and financial

performance. Journal of Applied Corporate Finance, 26(1), pp.56-64.

Gadoiu, M., 2014. Advantages and limitations of the financial ratios used in the financial

diagnosis of the enterprise. Scientific Bulletin-Economic Sciences, 13(2), pp.87-95. Liquidity

ratio

Išoraitė, M., 2014. Importance of strategic alliances in company’s activity.

LU, H., 2017. Related Party Transactions (Doctoral dissertation).

Silviu-Virgil, C., 2014. The importance of the accounting information for the decisional

process. THE ANNALS OF THE UNIVERSITY OF ORADEA, p.591. Accong policy

importance

Spătărelu, I. and Petec, D., 2016. The importance of accounting information in decision

making. Ovidius University Annals, Economic Sciences, pp.611-615. Accong policy

importance

References

Abbott, L.J., Daugherty, B., Parker, S. and Peters, G.F., 2016. Internal audit quality and

financial reporting quality: The joint importance of independence and competence. Journal

of Accounting Research, 54(1), pp.3-40.

Abernathy, J.L., Beyer, B., Masli, A. and Stefaniak, C.M., 2015. How the source of audit

committee accounting expertise influences financial reporting timeliness. Current Issues in

Auditing, 9(1), pp.P1-P9.

Churet, C. and Eccles, R.G., 2014. Integrated reporting, quality of management, and financial

performance. Journal of Applied Corporate Finance, 26(1), pp.56-64.

Gadoiu, M., 2014. Advantages and limitations of the financial ratios used in the financial

diagnosis of the enterprise. Scientific Bulletin-Economic Sciences, 13(2), pp.87-95. Liquidity

ratio

Išoraitė, M., 2014. Importance of strategic alliances in company’s activity.

LU, H., 2017. Related Party Transactions (Doctoral dissertation).

Silviu-Virgil, C., 2014. The importance of the accounting information for the decisional

process. THE ANNALS OF THE UNIVERSITY OF ORADEA, p.591. Accong policy

importance

Spătărelu, I. and Petec, D., 2016. The importance of accounting information in decision

making. Ovidius University Annals, Economic Sciences, pp.611-615. Accong policy

importance

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.