Corporate Accounting Report: Bellamy's Financial Performance Analysis

VerifiedAdded on 2020/06/06

|11

|3111

|185

Report

AI Summary

This report provides a comprehensive financial analysis of Bellamy's Australia Ltd. It begins by examining the company's current financial challenges, including the impact of the CNCA license suspension on share prices. The report then delves into the company's goodwill acquisition and cash position in 2016, analyzing the financial statements to determine the impairment test. Furthermore, it assesses the income statement for 2017, focusing on administrative costs. The analysis also includes advice for clients regarding the recent share price decline and trading halt. Part 2 of the report focuses on the necessities of continuous financial reporting and financial disclosure, evaluating the legal framework of the Corporate Act 2001 and the implications of breaching duties. The literature review explores the importance of financial disclosure for stakeholders and the legal consequences of non-compliance. The report incorporates various sources, including academic papers and corporate financial data, to support its analysis and conclusions, offering a critical assessment of Bellamy's financial performance and compliance with corporate regulations.

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1. Current Financial Predicament faced by Bellamy's Australia limited................................1

2 Goodwill acquisition and cash position of 2016.................................................................1

3 Income statement of 2017 in order to determine the impairment test, suspension of CNCA

licence and administrative costs.............................................................................................1

4 Advising the clients relevant with the decline in the recent share price and share trading halt.

................................................................................................................................................3

PART 2............................................................................................................................................3

ABSTRACT.....................................................................................................................................3

INTRODUCTION...........................................................................................................................3

LITERATURE REVIEW................................................................................................................4

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1. Current Financial Predicament faced by Bellamy's Australia limited................................1

2 Goodwill acquisition and cash position of 2016.................................................................1

3 Income statement of 2017 in order to determine the impairment test, suspension of CNCA

licence and administrative costs.............................................................................................1

4 Advising the clients relevant with the decline in the recent share price and share trading halt.

................................................................................................................................................3

PART 2............................................................................................................................................3

ABSTRACT.....................................................................................................................................3

INTRODUCTION...........................................................................................................................3

LITERATURE REVIEW................................................................................................................4

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Financial disclosure or presentation of data set will be beneficial in terms of facilitating

the suitable information to users of such accounts. In the present report, there will be discussion

based on the annual reports of Bellamy's Australian Ltd. which is relevant with financial

statements of the firm and the current scenario of the firm. This report also contains a critical

analysis over the Corporate Act, 2001 and the necessities of presenting the financial disclosure.

PART 1

1. Current Financial Predicament faced by Bellamy's Australia limited.

In accordance with the current financial scenario of Bellamy's, it can be said that the firm

is having increment in the share prices as the suspension of the CNCA license which will be

fruitful and profitable for the investors and the firm in terms of having surplus returns as well as

having strong capital structure.

2 Goodwill acquisition and cash position of 2016.

In accordance with disclosure of the financial statement of Bellamy's Australia Limited in

the year 2016, it consisted of the entire information which are relevant with the operations, gains

and expenditure of the firm (Hombach and Sellhorn, 2017). Therefore, in accordance with the

Goodwill acquisition and the cash in hand of the entity will be determined as follows:

Particulars Amount in 2016 ('000)

Goodwill or intangible assets 1704

Cash Position 32295

In accordance with the balance sheet and the cash flow statements for the year 2016 and

2017. There has been information in the disclosure of such elements. Therefore,the goodwill is

shown as the intangible asset to the firm so it has been mention in the financial position

statements and amounted as $1704. The cash balance for the same year is being analysed as

32295 after making reduction of all the inflows and outflows.

1

Financial disclosure or presentation of data set will be beneficial in terms of facilitating

the suitable information to users of such accounts. In the present report, there will be discussion

based on the annual reports of Bellamy's Australian Ltd. which is relevant with financial

statements of the firm and the current scenario of the firm. This report also contains a critical

analysis over the Corporate Act, 2001 and the necessities of presenting the financial disclosure.

PART 1

1. Current Financial Predicament faced by Bellamy's Australia limited.

In accordance with the current financial scenario of Bellamy's, it can be said that the firm

is having increment in the share prices as the suspension of the CNCA license which will be

fruitful and profitable for the investors and the firm in terms of having surplus returns as well as

having strong capital structure.

2 Goodwill acquisition and cash position of 2016.

In accordance with disclosure of the financial statement of Bellamy's Australia Limited in

the year 2016, it consisted of the entire information which are relevant with the operations, gains

and expenditure of the firm (Hombach and Sellhorn, 2017). Therefore, in accordance with the

Goodwill acquisition and the cash in hand of the entity will be determined as follows:

Particulars Amount in 2016 ('000)

Goodwill or intangible assets 1704

Cash Position 32295

In accordance with the balance sheet and the cash flow statements for the year 2016 and

2017. There has been information in the disclosure of such elements. Therefore,the goodwill is

shown as the intangible asset to the firm so it has been mention in the financial position

statements and amounted as $1704. The cash balance for the same year is being analysed as

32295 after making reduction of all the inflows and outflows.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

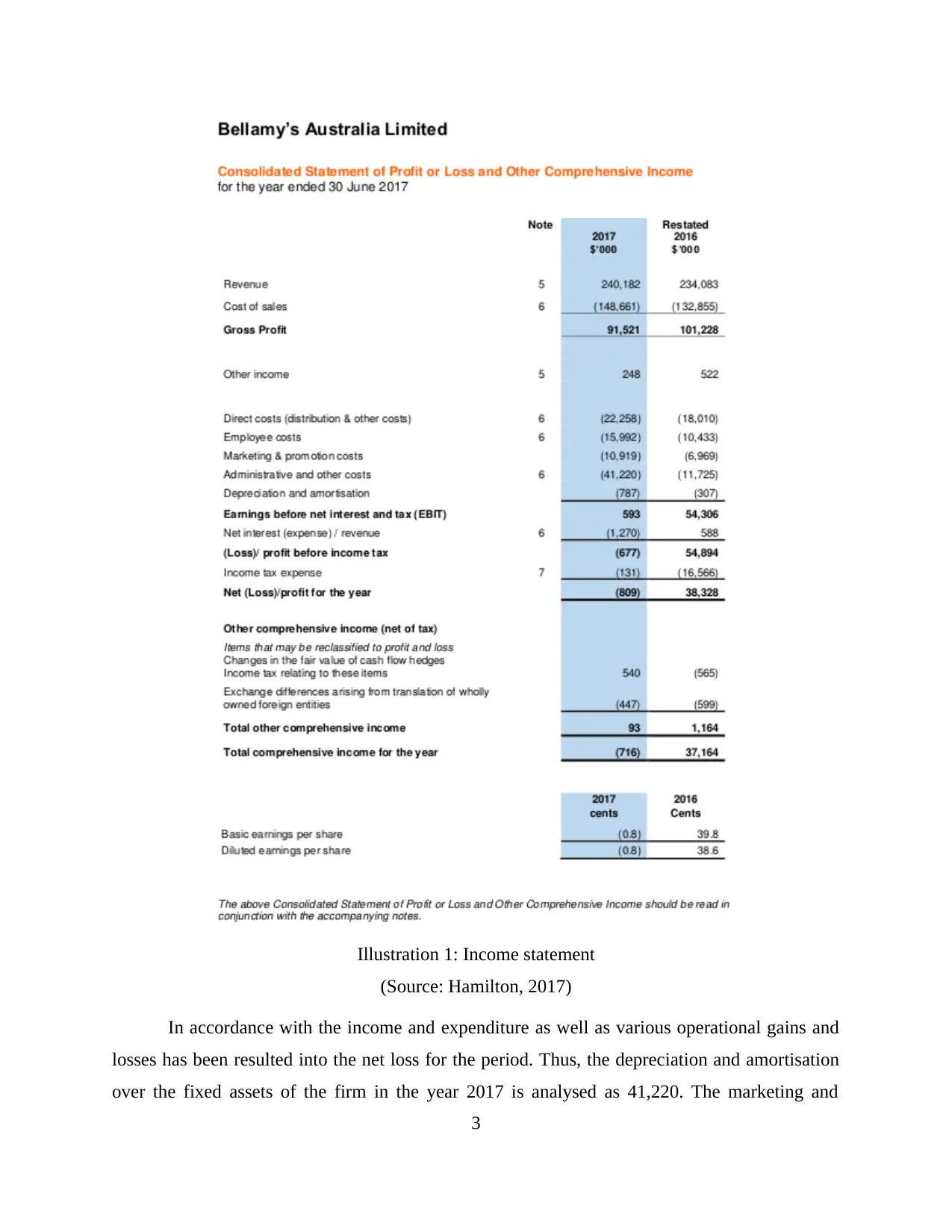

3 Income statement of 2017 in order to determine the impairment test, suspension of CNCA

licence and administrative costs.

In terms with Bellamy's operational functioning in the year 2016 and 2017, it can be

understood as per the below listed consolidated income statement such as:

2

licence and administrative costs.

In terms with Bellamy's operational functioning in the year 2016 and 2017, it can be

understood as per the below listed consolidated income statement such as:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Illustration 1: Income statement

(Source: Hamilton, 2017)

In accordance with the income and expenditure as well as various operational gains and

losses has been resulted into the net loss for the period. Thus, the depreciation and amortisation

over the fixed assets of the firm in the year 2017 is analysed as 41,220. The marketing and

3

(Source: Hamilton, 2017)

In accordance with the income and expenditure as well as various operational gains and

losses has been resulted into the net loss for the period. Thus, the depreciation and amortisation

over the fixed assets of the firm in the year 2017 is analysed as 41,220. The marketing and

3

promotional costs of the year is 15,992 while the administrative and other cost is measured as

10,919.

On the other side in relation with the suspension of CNCA licences of firm which

indicates that such operation has been profitable. The acquisition of 90% of stake in

Camperdown facility and the suspension of license which results into 10% variations in share

price of Bellamy's. Therefore, after suspension of this export license the business has bull in the

market share and due to which the stock value has increased.

4 Advising the clients relevant with the decline in the recent share price and share trading halt.

In accordance with the increase in the share price of the firm due the suspension of

licence, it can be said that it is the highest change which has been seen in the operations of the

business, thus, it can be said that with the help of having adequate increment in share prices and

the market value of the firm which will be fruitful for them in terms of having the strong capital

structure and better revenue gathering. Thus, on the other side the investors has to spend more to

acquire the shares of firm (Bellamy's suffers blow as China suspends export licence of new

canning facility, 2017). It can be estimated that the share price will have continuous increment in

the market. Thus, it will be beneficial for the investor in terms of having the profitable dividends

and the surplus value of the funds they have invested in the organisation.

PART 2

ABSTRACT

The study will be based on necessities of the continuous financial reporting and financial

disclosure of the entities. There will be analysis over disclosure and the fruitfulness in the

development of the business operations. The critical evaluation will be based on consideration of

the corporate act 2001 of commonwealth laws Australia. Therefore, there will be various

punishment and penalties which are to be facilitate to the shareholders, investors of various

stakeholders of the firm in consideration with beaching of duties and unlawful decision made by

firm.

INTRODUCTION

The financial disclosure will be helpful in terms of analysing the outcomes of the firm's

performance during the year as well as helps the stakeholders to make efficient decision. There

4

10,919.

On the other side in relation with the suspension of CNCA licences of firm which

indicates that such operation has been profitable. The acquisition of 90% of stake in

Camperdown facility and the suspension of license which results into 10% variations in share

price of Bellamy's. Therefore, after suspension of this export license the business has bull in the

market share and due to which the stock value has increased.

4 Advising the clients relevant with the decline in the recent share price and share trading halt.

In accordance with the increase in the share price of the firm due the suspension of

licence, it can be said that it is the highest change which has been seen in the operations of the

business, thus, it can be said that with the help of having adequate increment in share prices and

the market value of the firm which will be fruitful for them in terms of having the strong capital

structure and better revenue gathering. Thus, on the other side the investors has to spend more to

acquire the shares of firm (Bellamy's suffers blow as China suspends export licence of new

canning facility, 2017). It can be estimated that the share price will have continuous increment in

the market. Thus, it will be beneficial for the investor in terms of having the profitable dividends

and the surplus value of the funds they have invested in the organisation.

PART 2

ABSTRACT

The study will be based on necessities of the continuous financial reporting and financial

disclosure of the entities. There will be analysis over disclosure and the fruitfulness in the

development of the business operations. The critical evaluation will be based on consideration of

the corporate act 2001 of commonwealth laws Australia. Therefore, there will be various

punishment and penalties which are to be facilitate to the shareholders, investors of various

stakeholders of the firm in consideration with beaching of duties and unlawful decision made by

firm.

INTRODUCTION

The financial disclosure will be helpful in terms of analysing the outcomes of the firm's

performance during the year as well as helps the stakeholders to make efficient decision. There

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

will be presentation of various kinds of statements such as income statements, balance sheet,

change in equity as well as cash flows. Thus, the critical evaluation will help in highlighting the

usefulness of such data set in the growth of entity as well as evaluate the legalisations and legal

framework of CA, 2001 as to help in making the adequate growth of the business.

LITERATURE REVIEW

Di Maggio and Pagano, (2017) stated that the Corporation Act, 2001 of the

Commonwealth Acts has facilitated the guideline and the legal rules that all the entities have to

present the financial disclosure at the end of period. Therefore, it can be said that such legislation

has presented the firms with the motive to make the continues disclosure. In accordance with

Hombach and Sellhorn, (2017), the financial reports will be helpful as it will be used by various

potential users such as corporations, government bodies, banks, institution, investors, broker as

well as the internal stakeholders. It can be said that, these financial data set will be beneficial for

each of the stakeholders of the entity which will make the adequate use of such information such

as enhancing the operational activities, reducing the costs, planning to make expansion and tax

payments as well as dividend payments to the shareholders.

In accordance with the Section 234 and 235 of CA, 2001 it can be said that if there is any

reach of the duties by the directors than they will be punished for 5 years of imprisonment as

well as 200000 dollars of penalty. Thus, in accordance with the Beaton and Hamilton-Jewell,

(2017), the directors of board member have to be more responsible towards the firm in terms of

making the operational decision, planning for the expansion as well as keeping the confidential

data. Thus, as if such individual breach their duties the shareholder will have rights to suit the

case against company and its members. On the other side, it is also the main role of the entity as

to present the disclosure of the accounts which will be fruitful in terms of fetching the maximum

attention of the shareholders or investors because they have made their valuable investment

(Explainer: Continuous disclosure obligations, 2013). Thus, their contribution in rising the funds

of the organisation made them liable to have the entire information regarding the profitability

and the dividend policies of the business. In accordance with Hamilton, (2017), the information

which are presented in the financial disclosure must be relevant with the operational activities as

well as contains authenticate source as well as consist of income proposals and negotiations.

5

change in equity as well as cash flows. Thus, the critical evaluation will help in highlighting the

usefulness of such data set in the growth of entity as well as evaluate the legalisations and legal

framework of CA, 2001 as to help in making the adequate growth of the business.

LITERATURE REVIEW

Di Maggio and Pagano, (2017) stated that the Corporation Act, 2001 of the

Commonwealth Acts has facilitated the guideline and the legal rules that all the entities have to

present the financial disclosure at the end of period. Therefore, it can be said that such legislation

has presented the firms with the motive to make the continues disclosure. In accordance with

Hombach and Sellhorn, (2017), the financial reports will be helpful as it will be used by various

potential users such as corporations, government bodies, banks, institution, investors, broker as

well as the internal stakeholders. It can be said that, these financial data set will be beneficial for

each of the stakeholders of the entity which will make the adequate use of such information such

as enhancing the operational activities, reducing the costs, planning to make expansion and tax

payments as well as dividend payments to the shareholders.

In accordance with the Section 234 and 235 of CA, 2001 it can be said that if there is any

reach of the duties by the directors than they will be punished for 5 years of imprisonment as

well as 200000 dollars of penalty. Thus, in accordance with the Beaton and Hamilton-Jewell,

(2017), the directors of board member have to be more responsible towards the firm in terms of

making the operational decision, planning for the expansion as well as keeping the confidential

data. Thus, as if such individual breach their duties the shareholder will have rights to suit the

case against company and its members. On the other side, it is also the main role of the entity as

to present the disclosure of the accounts which will be fruitful in terms of fetching the maximum

attention of the shareholders or investors because they have made their valuable investment

(Explainer: Continuous disclosure obligations, 2013). Thus, their contribution in rising the funds

of the organisation made them liable to have the entire information regarding the profitability

and the dividend policies of the business. In accordance with Hamilton, (2017), the information

which are presented in the financial disclosure must be relevant with the operational activities as

well as contains authenticate source as well as consist of income proposals and negotiations.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Kaymak and Bektas, (2017) says that, the financial database is to be used by the internal

management of the organisation which in turn helps in analysing the returns acquired over the

invested projects and operations. They will become able to make the adequate plan in

consideration with improving the operations, lowering down the expenditure and planning for

controlling the costs. As per the views of Sun and Farooque, (2017), the internal stakeholder

seeks the information which are relevant with assets, capital, sales of the period and the net profit

acquired by the firm. Therefore, such information play the main role as they become able to

make the appropriate and suitable secretaries that will be relevant with increasing the

productivity, marketing of brand as well as improving the work efficiency of workers.

On the other side, financial reports help in presenting the information which are relevant

with the operational activities of the firm during the year. These data help the users to make

efficient decision which are relevant with making investment, executing the costs as well as

planning for the expansion of the business operations (Di Maggio and Pagano, 2017). Therefore,

the presentation will help firm in making the adequate increment in the profitability as well as

revenue gathering it will also help in enhancing the market value of the firm which results in

strengthening the capital structure.

According to Guay, Samuels and Taylor (2016), trade secret is a practice, process,

formula, design, instrument, pattern commercial method or compilation of information which is

not generally ascertainable by others through which a business is able to attain economic

advantage in comparison to the competitors. As per the legal aspect of some jurisdiction, it is

also referred to as confidential information or classified information. In this manner some of the

secrets of the government can be secured from disclosure with the help of certain laws and

practices. It not only helps in preserving the secrets of government but it also has a strong impact

on general trade practices of people which helps in protection of certain undisclosed information.

The trade secretes can be protected from the competitors. Adequate amount of support is

extended by technological and legal security measures in this aspect. Legal protection is

inclusive of Non-Disclosure Agreements (NDA), work for hire and non-compete clause being

mentioned in the provisions of law. An employee also has to sign an agreement where it is

mandatory to promise that he / she will not disclosure any internal functions of the workplace

unless and until it is not meant for disclosure. However, in contrast to this, as per the views of

6

management of the organisation which in turn helps in analysing the returns acquired over the

invested projects and operations. They will become able to make the adequate plan in

consideration with improving the operations, lowering down the expenditure and planning for

controlling the costs. As per the views of Sun and Farooque, (2017), the internal stakeholder

seeks the information which are relevant with assets, capital, sales of the period and the net profit

acquired by the firm. Therefore, such information play the main role as they become able to

make the appropriate and suitable secretaries that will be relevant with increasing the

productivity, marketing of brand as well as improving the work efficiency of workers.

On the other side, financial reports help in presenting the information which are relevant

with the operational activities of the firm during the year. These data help the users to make

efficient decision which are relevant with making investment, executing the costs as well as

planning for the expansion of the business operations (Di Maggio and Pagano, 2017). Therefore,

the presentation will help firm in making the adequate increment in the profitability as well as

revenue gathering it will also help in enhancing the market value of the firm which results in

strengthening the capital structure.

According to Guay, Samuels and Taylor (2016), trade secret is a practice, process,

formula, design, instrument, pattern commercial method or compilation of information which is

not generally ascertainable by others through which a business is able to attain economic

advantage in comparison to the competitors. As per the legal aspect of some jurisdiction, it is

also referred to as confidential information or classified information. In this manner some of the

secrets of the government can be secured from disclosure with the help of certain laws and

practices. It not only helps in preserving the secrets of government but it also has a strong impact

on general trade practices of people which helps in protection of certain undisclosed information.

The trade secretes can be protected from the competitors. Adequate amount of support is

extended by technological and legal security measures in this aspect. Legal protection is

inclusive of Non-Disclosure Agreements (NDA), work for hire and non-compete clause being

mentioned in the provisions of law. An employee also has to sign an agreement where it is

mandatory to promise that he / she will not disclosure any internal functions of the workplace

unless and until it is not meant for disclosure. However, in contrast to this, as per the views of

6

Ball, Li and Shivakumar (2015), trade secrets are the internal instruments which helps in

protecting certain information and which remains with the owner. They are not disclosed to

anybody. The secrecy agreement is inclusive of the government as well and all the information

regarding undisclosed aspects is kept confidential. It is an essential aspect for internal protection

where data is required to be protected from customers, independent contractors etc. In external

protection context, trade secrecy is important for employees and other stakeholders who have

direct or indirect interest in the organizational aspects.

According to Leuz and Wysocki (2016), a reasonable person may not want to disclose all

the information unless and until it has stronger impact on monetary and non-monetary aspects of

an individual. In that case, the individual has right to keep adequate amount of secrecy in its

functioning. Common functions of confidentiality include, protection data of the computer from

unauthorized access. Hence, the system being established at the workplace must have short time

screen savers, automated logouts. All the files must have restricted and should be password

protected. It helps in saving the enterprise from leaked financial or non-financial information.

However, in comparison to this, as per the views of Chung and Jung (2016), it is required to

disclose adequate amount of information to the stakeholders which can affect their decision-

making process. Hence, true and fair representation of facts and figures are required to be made.

In that proper disclosure from the side of top level management of the company is required.

Further, an amount of secrecy and confidentiality can be initiated by the owners with respect to

method of preparation of accounts, disclosing proof for each and every transaction etc.

According to Cao, Chychyla and Stewart (2015), an agreement related to maintenance of

confidentiality can be signed by the employees where they are bound not to disclose any

financial information to people. In that case, Non-Disclosure Agreement (NDA) is signed by the

employee’s so as to legally maintain this confidentiality. In that case, it is important for the

management to frame disclosure and non-disclosure policies so that no secret information is

discussed outside the working environment. Hence, after meetings and discussion, the

management decides regarding disclosure of financial information in the annual or semi-annual

books of accounts. It is also ensured that if any sensitive information is revealed, in that case, the

contract between employee and employer automatically gets terminated. Loss, misuse,

modification or any unauthorised access of financial information might result to huge loss for the

7

protecting certain information and which remains with the owner. They are not disclosed to

anybody. The secrecy agreement is inclusive of the government as well and all the information

regarding undisclosed aspects is kept confidential. It is an essential aspect for internal protection

where data is required to be protected from customers, independent contractors etc. In external

protection context, trade secrecy is important for employees and other stakeholders who have

direct or indirect interest in the organizational aspects.

According to Leuz and Wysocki (2016), a reasonable person may not want to disclose all

the information unless and until it has stronger impact on monetary and non-monetary aspects of

an individual. In that case, the individual has right to keep adequate amount of secrecy in its

functioning. Common functions of confidentiality include, protection data of the computer from

unauthorized access. Hence, the system being established at the workplace must have short time

screen savers, automated logouts. All the files must have restricted and should be password

protected. It helps in saving the enterprise from leaked financial or non-financial information.

However, in comparison to this, as per the views of Chung and Jung (2016), it is required to

disclose adequate amount of information to the stakeholders which can affect their decision-

making process. Hence, true and fair representation of facts and figures are required to be made.

In that proper disclosure from the side of top level management of the company is required.

Further, an amount of secrecy and confidentiality can be initiated by the owners with respect to

method of preparation of accounts, disclosing proof for each and every transaction etc.

According to Cao, Chychyla and Stewart (2015), an agreement related to maintenance of

confidentiality can be signed by the employees where they are bound not to disclose any

financial information to people. In that case, Non-Disclosure Agreement (NDA) is signed by the

employee’s so as to legally maintain this confidentiality. In that case, it is important for the

management to frame disclosure and non-disclosure policies so that no secret information is

discussed outside the working environment. Hence, after meetings and discussion, the

management decides regarding disclosure of financial information in the annual or semi-annual

books of accounts. It is also ensured that if any sensitive information is revealed, in that case, the

contract between employee and employer automatically gets terminated. Loss, misuse,

modification or any unauthorised access of financial information might result to huge loss for the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company. Some of types of private information, include, education, employment, person’s health

care and these have to be protected through privacy laws. However, in contrast to this, as per the

views of Maaloul and Zéghal (2015), disclosure of certain information can directly harm the

business. Hence, appropriate steps are required to be taken by top level management for the

same. To find the individual who disclosed the information, whistle blowing technique is used

where an individual is appointed from top level management where intentional disclosure is

made with the intention to alleged illegal or immoral actions.

CONCLUSION

On the basis of above report, there has been discussion based on financial disclosure

made by Bellamy's Australian Ltd for the year 2016 and 2017. Thus, the data set has been

analysed and the current changes in the firm's marketability has been considered. Thus, with the

help of such measurement, it has suggested to investors that increment in share value will have

continuous growth and that will help them in profitable returns. Further, the report contains

critical reviews over the validity of the financial disclosure.

8

care and these have to be protected through privacy laws. However, in contrast to this, as per the

views of Maaloul and Zéghal (2015), disclosure of certain information can directly harm the

business. Hence, appropriate steps are required to be taken by top level management for the

same. To find the individual who disclosed the information, whistle blowing technique is used

where an individual is appointed from top level management where intentional disclosure is

made with the intention to alleged illegal or immoral actions.

CONCLUSION

On the basis of above report, there has been discussion based on financial disclosure

made by Bellamy's Australian Ltd for the year 2016 and 2017. Thus, the data set has been

analysed and the current changes in the firm's marketability has been considered. Thus, with the

help of such measurement, it has suggested to investors that increment in share value will have

continuous growth and that will help them in profitable returns. Further, the report contains

critical reviews over the validity of the financial disclosure.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Ball, R., Li, X. and Shivakumar, L., (2015). Contractibility and transparency of financial

statement information prepared under IFRS: Evidence from debt contracts around IFRS

adoption. Journal of Accounting Research. 53(5). pp.915-963.

Beaton, J. and Hamilton-Jewell, C., (2017). The new registered organisations commission: An

enhanced regime for the regulation of registered organisations. Governance Directions.

69(2). p.92.

Cao, M., Chychyla, R. and Stewart, T., (2015). Big Data analytics in financial statement

audits. Accounting Horizons. 29(2). pp.423-429.

Chung, H. and Jung, W. O., (2016). Financial Disclosure Incentives and Organizational Form

Changes. Asia

‐Pacific Journal of Financial Studies. 45(6). pp.839-863.

Di Maggio, M. and Pagano, M., (2017). Financial disclosure and market transparency with costly

information processing. Review of Finance, p.rfx009.

Guay, W., Samuels, D. and Taylor, D., (2016). Guiding through the fog: Financial statement

complexity and voluntary disclosure. Journal of Accounting and Economics. 62(2). pp.234-

269.

Hamilton, J., (2017). Do I need an accountant or a lawyer when my company is in financial

trouble?. Governance Directions. 69(4). p.231.

Hombach, K. and Sellhorn, T., (2017). Financial Disclosure Regulation to Achieve Public Policy

Objectives: Evidence from Extractive Issuers. Working Paper, University of Munich.

Kaymak, T. and Bektas, E., (2017). Corporate Social Responsibility and Governance:

Information Disclosure in Multinational Corporations. Corporate Social Responsibility and

Environmental Management.

Leuz, C. and Wysocki, P. D., (2016). The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting

Research. 54(2). pp.525-622.

Maaloul, A. and Zéghal, D., 2015. Financial statement informativeness and intellectual capital

disclosure: an empirical analysis. Journal of Financial Reporting and Accounting. 13(1).

pp.66-90.

Sun, L. and Farooque, O. A., (2017). An Exploratory Analysis of Earnings Management Before

and after the Governance and Disclosure Regulatory Changes in Australia and New

Zealand.

Online:

Bellamy's suffers blow as China suspends export licence of new canning facility. (2017).

[Online]. Available through :<http://www.abc.net.au/news/2017-07-07/china-suspends-

export-licence-of-bellamys-new-canning-facility/8687168>.

Explainer: Continuous disclosure obligations. (2013). [Online]. Available through

:<https://theconversation.com/explainer-continuous-disclosure-obligations-16894>.

9

Books and Journals:

Ball, R., Li, X. and Shivakumar, L., (2015). Contractibility and transparency of financial

statement information prepared under IFRS: Evidence from debt contracts around IFRS

adoption. Journal of Accounting Research. 53(5). pp.915-963.

Beaton, J. and Hamilton-Jewell, C., (2017). The new registered organisations commission: An

enhanced regime for the regulation of registered organisations. Governance Directions.

69(2). p.92.

Cao, M., Chychyla, R. and Stewart, T., (2015). Big Data analytics in financial statement

audits. Accounting Horizons. 29(2). pp.423-429.

Chung, H. and Jung, W. O., (2016). Financial Disclosure Incentives and Organizational Form

Changes. Asia

‐Pacific Journal of Financial Studies. 45(6). pp.839-863.

Di Maggio, M. and Pagano, M., (2017). Financial disclosure and market transparency with costly

information processing. Review of Finance, p.rfx009.

Guay, W., Samuels, D. and Taylor, D., (2016). Guiding through the fog: Financial statement

complexity and voluntary disclosure. Journal of Accounting and Economics. 62(2). pp.234-

269.

Hamilton, J., (2017). Do I need an accountant or a lawyer when my company is in financial

trouble?. Governance Directions. 69(4). p.231.

Hombach, K. and Sellhorn, T., (2017). Financial Disclosure Regulation to Achieve Public Policy

Objectives: Evidence from Extractive Issuers. Working Paper, University of Munich.

Kaymak, T. and Bektas, E., (2017). Corporate Social Responsibility and Governance:

Information Disclosure in Multinational Corporations. Corporate Social Responsibility and

Environmental Management.

Leuz, C. and Wysocki, P. D., (2016). The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting

Research. 54(2). pp.525-622.

Maaloul, A. and Zéghal, D., 2015. Financial statement informativeness and intellectual capital

disclosure: an empirical analysis. Journal of Financial Reporting and Accounting. 13(1).

pp.66-90.

Sun, L. and Farooque, O. A., (2017). An Exploratory Analysis of Earnings Management Before

and after the Governance and Disclosure Regulatory Changes in Australia and New

Zealand.

Online:

Bellamy's suffers blow as China suspends export licence of new canning facility. (2017).

[Online]. Available through :<http://www.abc.net.au/news/2017-07-07/china-suspends-

export-licence-of-bellamys-new-canning-facility/8687168>.

Explainer: Continuous disclosure obligations. (2013). [Online]. Available through

:<https://theconversation.com/explainer-continuous-disclosure-obligations-16894>.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.