Financial Analysis of Benedict Company: Stakeholder & Ratio Review

VerifiedAdded on 2023/04/21

|23

|4675

|103

Report

AI Summary

This report provides a comprehensive financial analysis of Benedict Company, incorporating a stakeholder analysis of Tesco as a benchmark. It delves into various financial ratios, including liquidity ratios (current and quick ratios), long-term solvency ratios (debt-to-equity and debt-to-total assets), financial leverage ratios, and profitability ratios (gross profit, net profit, return on assets, and return on equity). Activity ratios like trade receivables, trade payables, and inventory turnover are also examined. The analysis identifies potential causes of concern within Benedict Company's financial performance and offers recommendations for improvement. The report references academic sources to support its findings and conclusions, providing a well-researched assessment of the company's financial health and stakeholder relationships.

BENEDICT COMPANY 1

Benedict Company

Benedict Company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BENEDICT COMPANY 2

Table of Contents

Introduction......................................................................................................................................1

Stakeholder Analysis of the Tesco Company..............................................................................2

Ratio Analysis..................................................................................................................................3

Current ratio.................................................................................................................................4

Quick Ratio..................................................................................................................................5

Long Term Solvency Ratios............................................................................................................6

Debt to Equity ratio......................................................................................................................6

Debt ot total assets of the company.............................................................................................7

Financial Leverage Ratios............................................................................................................8

Profitability ratios............................................................................................................................8

Gross Profit..................................................................................................................................9

Net Profit....................................................................................................................................10

Return on Assets........................................................................................................................10

Return on Equity........................................................................................................................11

Activity Ratios...............................................................................................................................12

Trade Receivables Ratio............................................................................................................13

Trade Payable Ratio...................................................................................................................13

Inventory Turnover Ratio...........................................................................................................14

Table of Contents

Introduction......................................................................................................................................1

Stakeholder Analysis of the Tesco Company..............................................................................2

Ratio Analysis..................................................................................................................................3

Current ratio.................................................................................................................................4

Quick Ratio..................................................................................................................................5

Long Term Solvency Ratios............................................................................................................6

Debt to Equity ratio......................................................................................................................6

Debt ot total assets of the company.............................................................................................7

Financial Leverage Ratios............................................................................................................8

Profitability ratios............................................................................................................................8

Gross Profit..................................................................................................................................9

Net Profit....................................................................................................................................10

Return on Assets........................................................................................................................10

Return on Equity........................................................................................................................11

Activity Ratios...............................................................................................................................12

Trade Receivables Ratio............................................................................................................13

Trade Payable Ratio...................................................................................................................13

Inventory Turnover Ratio...........................................................................................................14

BENEDICT COMPANY 3

Cause of Concern...........................................................................................................................14

Recommendations and Conclusions..............................................................................................15

References......................................................................................................................................16

Cause of Concern...........................................................................................................................14

Recommendations and Conclusions..............................................................................................15

References......................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BENEDICT COMPANY 4

Introduction

Financial Reports are the key elements for any company and stakeholders have a deep interest in

the financial reports of the company. To analyze how well the company is operating is the major

concern for any stakeholder and therefore it is necessary to conduct a financial analysis. The

below report discusses about the stakeholder analysis of the Tesco company and the

sustainability and the corporate governance of the Tesco with reference to the stakeholders.

Furthermore, the analysis of the Benedict Company has been undertaken in order to maintain the

potential customers, investors, lenders and the suppliers and the members of the company

(Wood, 2016).

Stakeholder Analysis of the Tesco Company

Stakeholders are the specific group or people who have the partial interest in the products or

services the organization provides. Internal stakeholders also include the management,

employees, administrators, whereas the external stakeholder also includes the suppliers,

investors, community groups and the governmental organizations (Bailey, Mankin, Kelliher and

Garavan, 2018).

Tesco mainly operates with three major stakeholders

Customer: Customer timings and meetings are precious like diamond and the staff hears

everything with regards to the services given to the customers in stores and the community.

Staff: With the assistance of the Viewpoint staff survey, Staff Question time and Staff forum

process the feedback is given to the management of the company and the same is required to

keep a track of the operations of the staff (Wood, 2016).

Introduction

Financial Reports are the key elements for any company and stakeholders have a deep interest in

the financial reports of the company. To analyze how well the company is operating is the major

concern for any stakeholder and therefore it is necessary to conduct a financial analysis. The

below report discusses about the stakeholder analysis of the Tesco company and the

sustainability and the corporate governance of the Tesco with reference to the stakeholders.

Furthermore, the analysis of the Benedict Company has been undertaken in order to maintain the

potential customers, investors, lenders and the suppliers and the members of the company

(Wood, 2016).

Stakeholder Analysis of the Tesco Company

Stakeholders are the specific group or people who have the partial interest in the products or

services the organization provides. Internal stakeholders also include the management,

employees, administrators, whereas the external stakeholder also includes the suppliers,

investors, community groups and the governmental organizations (Bailey, Mankin, Kelliher and

Garavan, 2018).

Tesco mainly operates with three major stakeholders

Customer: Customer timings and meetings are precious like diamond and the staff hears

everything with regards to the services given to the customers in stores and the community.

Staff: With the assistance of the Viewpoint staff survey, Staff Question time and Staff forum

process the feedback is given to the management of the company and the same is required to

keep a track of the operations of the staff (Wood, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BENEDICT COMPANY 5

Suppliers: the main policy of the Tesco is to treat the people the way they want to treat

themselves, and it’s something they apply firmly to give the relationship a new touch among the

suppliers and the management.

Tesco’s Environmental and Social Review

The Tesco’s Environmental and Social Review and the Corporate Governance Report

demonstrates the performance of the company in terms of the responsibilities to two stakeholders

namely customers and the suppliers it is the corporate responsibility of the management to build

a strong governance to keep the company ahead in the ethical environment. In terms of the

customer the company was majorly indulged in the boosting the confidence of the customer as

well ensuring that the customer operations are smooth and working timely. The company also

worked upon the reduction of the carbon footprint by introducing the 100% renewable enrgy and

for the purpose the company had invested pound 700 million in energy and refrigeration

efficiency which helped in reduction of the emission by 41% (Tesco PLC, 2018).

With the suppliers the overall approach of the company has always been to use the dibble crop

which is inclusive of different shapes and sizes. Moreover in the year 2017 the new crops have

been introduced and the new range with the facility of the flexibility ordering, where the range of

the volume is high to increase the supply. Since the stakeholders are the key members that can

drive the entire organization and therefore the entire approach of the company changes with

respect to the suppliers as they are interested in the corporate governance feature of the Tesco

(Tonchia, 2018).

Suppliers: the main policy of the Tesco is to treat the people the way they want to treat

themselves, and it’s something they apply firmly to give the relationship a new touch among the

suppliers and the management.

Tesco’s Environmental and Social Review

The Tesco’s Environmental and Social Review and the Corporate Governance Report

demonstrates the performance of the company in terms of the responsibilities to two stakeholders

namely customers and the suppliers it is the corporate responsibility of the management to build

a strong governance to keep the company ahead in the ethical environment. In terms of the

customer the company was majorly indulged in the boosting the confidence of the customer as

well ensuring that the customer operations are smooth and working timely. The company also

worked upon the reduction of the carbon footprint by introducing the 100% renewable enrgy and

for the purpose the company had invested pound 700 million in energy and refrigeration

efficiency which helped in reduction of the emission by 41% (Tesco PLC, 2018).

With the suppliers the overall approach of the company has always been to use the dibble crop

which is inclusive of different shapes and sizes. Moreover in the year 2017 the new crops have

been introduced and the new range with the facility of the flexibility ordering, where the range of

the volume is high to increase the supply. Since the stakeholders are the key members that can

drive the entire organization and therefore the entire approach of the company changes with

respect to the suppliers as they are interested in the corporate governance feature of the Tesco

(Tonchia, 2018).

BENEDICT COMPANY 6

Ratio Analysis

Ratio analysis is the technique which fosters the demands of the potential investors, customers,

shareholders, suppliers and the management of the company as well. The ratios are calculated

keeping an idea of measuring the financial performance of the company in terms of the liquidity,

efficiency and the profitability of the business. The ratios are the key determinants that can be

sued to compare the inter as well the intra industry and company comparison to find out the

position of the company and the place at which it stands in terms of the competitors. Ratio

analysis helps in making aware about the variances to the company.

The first ratio that shall be selected by the company are Liquidity ratios, which are used to

measure the financial position of the business in terms of how liquid the company can become to

meet its current obligations on time. The company shall have sufficient amount to pay back the

current liabilities efficiently and effectively. The liquidity ratios are further segregated into the

current ratio, quick ratio (Kowalik, 2018).

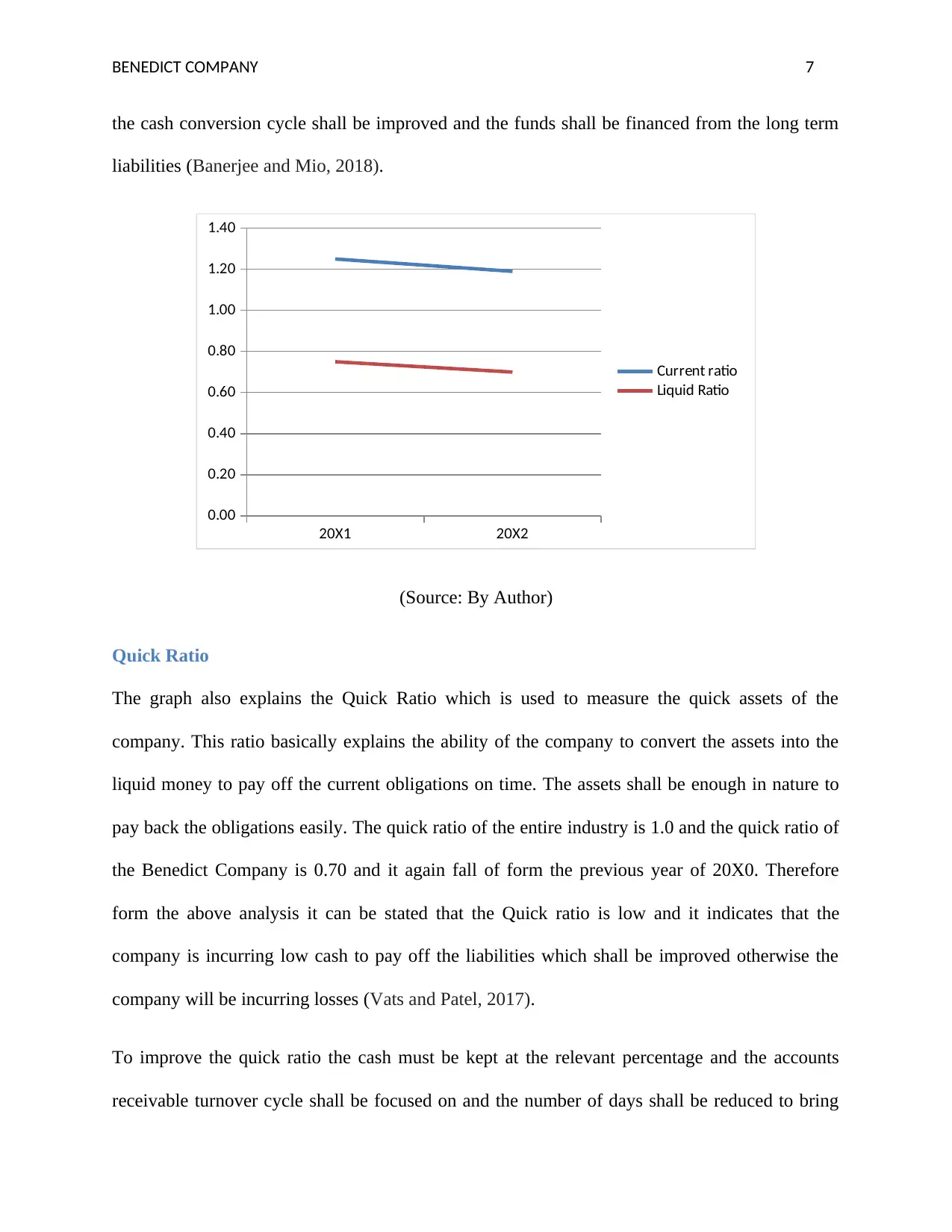

Current ratio

Current Ratio is the ratio calculated to find out the ability of the company to payback its current

liabilities on the virtue of the current assets. The current ratio is ideally 2:1 however the current

ratio differs as the sector differs. Moreover as it can be observed from the table and the graph

below and in comparison to the industry as well the current ratio of the Benedict Company is

1.19 which has been reduced from 1.25 whereas in comparison to the industry benchmark the

company is performing better than the industry in this ratio (Arora and Kohli, 2018).

Therefore it can be concluded that the current ratio is better yet has some ore room for the

improvement and to improve the ratio the useless assets shall be eradicated from the company,

Ratio Analysis

Ratio analysis is the technique which fosters the demands of the potential investors, customers,

shareholders, suppliers and the management of the company as well. The ratios are calculated

keeping an idea of measuring the financial performance of the company in terms of the liquidity,

efficiency and the profitability of the business. The ratios are the key determinants that can be

sued to compare the inter as well the intra industry and company comparison to find out the

position of the company and the place at which it stands in terms of the competitors. Ratio

analysis helps in making aware about the variances to the company.

The first ratio that shall be selected by the company are Liquidity ratios, which are used to

measure the financial position of the business in terms of how liquid the company can become to

meet its current obligations on time. The company shall have sufficient amount to pay back the

current liabilities efficiently and effectively. The liquidity ratios are further segregated into the

current ratio, quick ratio (Kowalik, 2018).

Current ratio

Current Ratio is the ratio calculated to find out the ability of the company to payback its current

liabilities on the virtue of the current assets. The current ratio is ideally 2:1 however the current

ratio differs as the sector differs. Moreover as it can be observed from the table and the graph

below and in comparison to the industry as well the current ratio of the Benedict Company is

1.19 which has been reduced from 1.25 whereas in comparison to the industry benchmark the

company is performing better than the industry in this ratio (Arora and Kohli, 2018).

Therefore it can be concluded that the current ratio is better yet has some ore room for the

improvement and to improve the ratio the useless assets shall be eradicated from the company,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BENEDICT COMPANY 7

the cash conversion cycle shall be improved and the funds shall be financed from the long term

liabilities (Banerjee and Mio, 2018).

20X1 20X2

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Current ratio

Liquid Ratio

(Source: By Author)

Quick Ratio

The graph also explains the Quick Ratio which is used to measure the quick assets of the

company. This ratio basically explains the ability of the company to convert the assets into the

liquid money to pay off the current obligations on time. The assets shall be enough in nature to

pay back the obligations easily. The quick ratio of the entire industry is 1.0 and the quick ratio of

the Benedict Company is 0.70 and it again fall of form the previous year of 20X0. Therefore

form the above analysis it can be stated that the Quick ratio is low and it indicates that the

company is incurring low cash to pay off the liabilities which shall be improved otherwise the

company will be incurring losses (Vats and Patel, 2017).

To improve the quick ratio the cash must be kept at the relevant percentage and the accounts

receivable turnover cycle shall be focused on and the number of days shall be reduced to bring

the cash conversion cycle shall be improved and the funds shall be financed from the long term

liabilities (Banerjee and Mio, 2018).

20X1 20X2

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Current ratio

Liquid Ratio

(Source: By Author)

Quick Ratio

The graph also explains the Quick Ratio which is used to measure the quick assets of the

company. This ratio basically explains the ability of the company to convert the assets into the

liquid money to pay off the current obligations on time. The assets shall be enough in nature to

pay back the obligations easily. The quick ratio of the entire industry is 1.0 and the quick ratio of

the Benedict Company is 0.70 and it again fall of form the previous year of 20X0. Therefore

form the above analysis it can be stated that the Quick ratio is low and it indicates that the

company is incurring low cash to pay off the liabilities which shall be improved otherwise the

company will be incurring losses (Vats and Patel, 2017).

To improve the quick ratio the cash must be kept at the relevant percentage and the accounts

receivable turnover cycle shall be focused on and the number of days shall be reduced to bring

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BENEDICT COMPANY 8

the cash back into the industry so that then company can utilize those funds and pay to the

creditors and the suppliers of the Benedict Company. Henceforth both the ratios are equally

important and are of core value in the eyes of the management.

Long Term Solvency Ratios

Solvency ratio is the key metric used to measure the ability of the enterprise to meet its

obligations in the form of the debt. This basically determines whether the capacity of the

company is sufficient or not to meet its short term and long term liabilities. Moreover the

solvency is the critical measure of the solvency as it does not measure the net income but rather

measures the cash flows of the in relation to all the liabilities (Thornblad, Zeitzmann and

Carlson, 2018). It takes into account all the liabilities and not just short term liabilities. This way

the company can assess the long term health by evaluating and analyzing the overall position of

the company and the impact of the interest as well.

The debt to Equity ratio, the debt to total assets and the financial leverage ratios are the further

categorized ratios under the long term solvency ratios.

Debt to Equity ratio

The major purpose of this ratio is to calculate the financial leverage of the company. If the

amount of debt used by the company is more to finance the company it can potentially generate

more earnings and income than it could without financing. The debt to equity ratio of the

company is 1.01 in the year 20X0 and it increased to 1.20 whereas in comparison to the

benchmark set by the industry at 1.41. The value of the debt to equity increased in case of the

Benedict Company and hence the dent financing outweighs the earnings generated and the share

values will decline.

the cash back into the industry so that then company can utilize those funds and pay to the

creditors and the suppliers of the Benedict Company. Henceforth both the ratios are equally

important and are of core value in the eyes of the management.

Long Term Solvency Ratios

Solvency ratio is the key metric used to measure the ability of the enterprise to meet its

obligations in the form of the debt. This basically determines whether the capacity of the

company is sufficient or not to meet its short term and long term liabilities. Moreover the

solvency is the critical measure of the solvency as it does not measure the net income but rather

measures the cash flows of the in relation to all the liabilities (Thornblad, Zeitzmann and

Carlson, 2018). It takes into account all the liabilities and not just short term liabilities. This way

the company can assess the long term health by evaluating and analyzing the overall position of

the company and the impact of the interest as well.

The debt to Equity ratio, the debt to total assets and the financial leverage ratios are the further

categorized ratios under the long term solvency ratios.

Debt to Equity ratio

The major purpose of this ratio is to calculate the financial leverage of the company. If the

amount of debt used by the company is more to finance the company it can potentially generate

more earnings and income than it could without financing. The debt to equity ratio of the

company is 1.01 in the year 20X0 and it increased to 1.20 whereas in comparison to the

benchmark set by the industry at 1.41. The value of the debt to equity increased in case of the

Benedict Company and hence the dent financing outweighs the earnings generated and the share

values will decline.

BENEDICT COMPANY 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BENEDICT COMPANY 10

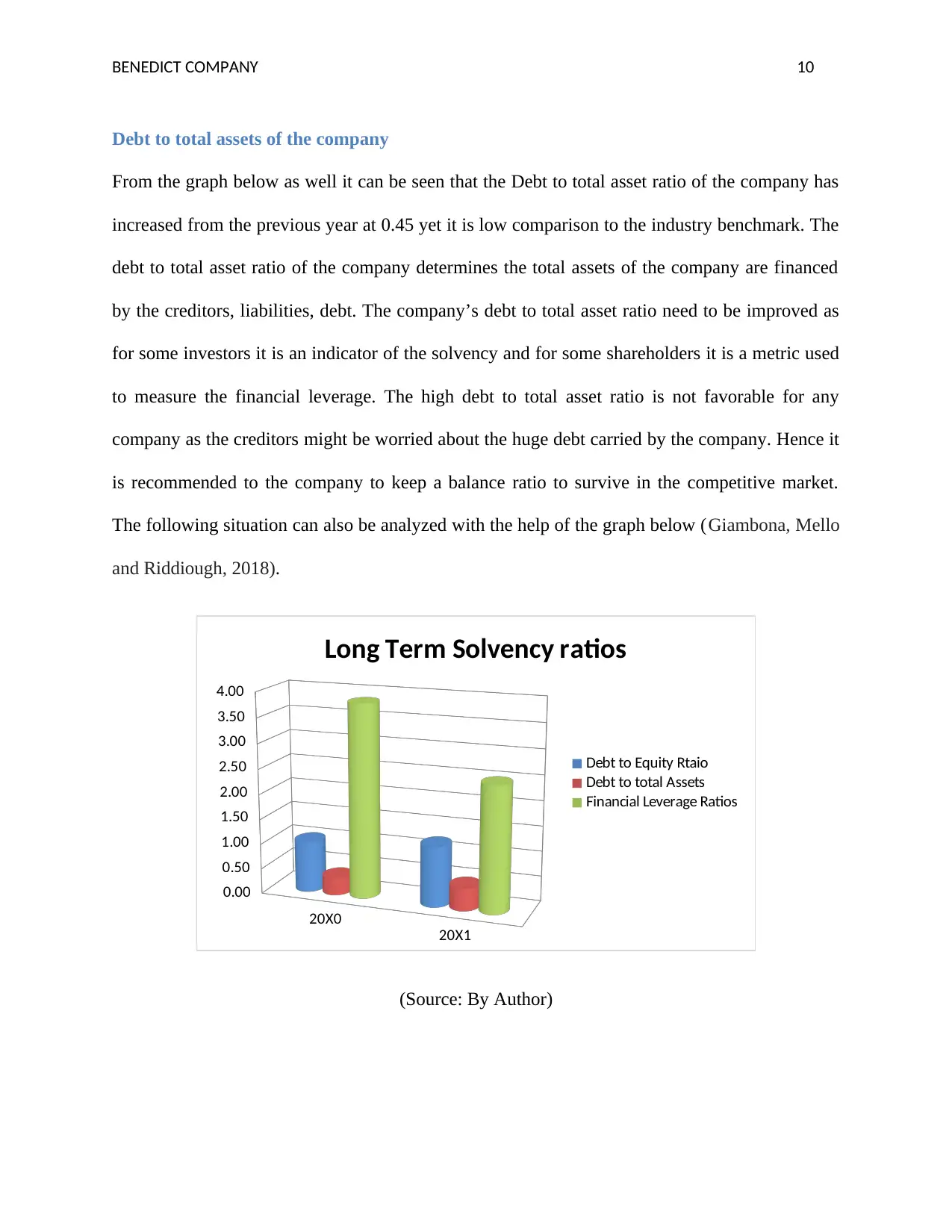

Debt to total assets of the company

From the graph below as well it can be seen that the Debt to total asset ratio of the company has

increased from the previous year at 0.45 yet it is low comparison to the industry benchmark. The

debt to total asset ratio of the company determines the total assets of the company are financed

by the creditors, liabilities, debt. The company’s debt to total asset ratio need to be improved as

for some investors it is an indicator of the solvency and for some shareholders it is a metric used

to measure the financial leverage. The high debt to total asset ratio is not favorable for any

company as the creditors might be worried about the huge debt carried by the company. Hence it

is recommended to the company to keep a balance ratio to survive in the competitive market.

The following situation can also be analyzed with the help of the graph below (Giambona, Mello

and Riddiough, 2018).

20X0

20X1

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Long Term Solvency ratios

Debt to Equity Rtaio

Debt to total Assets

Financial Leverage Ratios

(Source: By Author)

Debt to total assets of the company

From the graph below as well it can be seen that the Debt to total asset ratio of the company has

increased from the previous year at 0.45 yet it is low comparison to the industry benchmark. The

debt to total asset ratio of the company determines the total assets of the company are financed

by the creditors, liabilities, debt. The company’s debt to total asset ratio need to be improved as

for some investors it is an indicator of the solvency and for some shareholders it is a metric used

to measure the financial leverage. The high debt to total asset ratio is not favorable for any

company as the creditors might be worried about the huge debt carried by the company. Hence it

is recommended to the company to keep a balance ratio to survive in the competitive market.

The following situation can also be analyzed with the help of the graph below (Giambona, Mello

and Riddiough, 2018).

20X0

20X1

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Long Term Solvency ratios

Debt to Equity Rtaio

Debt to total Assets

Financial Leverage Ratios

(Source: By Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BENEDICT COMPANY 11

Financial Leverage Ratios

The financial leverage ratios of the company are the ratios which represents the financial

performance of the company. Financial leverage ratios mainly measure the equity value in a

company by making an evaluation of the debt in overall sense. The main aim of the financial

leverage ratios is to show that how much of the assets of the company are belonging to the

shareholders rather than they belong to the creditors (Barbiero Popov and Wolski, 2018). Form

the above graph it can be observed that the average total assets of the company when divided by

the average equity have decreased as the assets have not been utilized by the company in the

most critical value. The ratio increased from 1.08 to 2.49 and hence the company needs to value

the performance of the company.

Profitability ratios

Profitability ratios of the company are the ones that are calculated to determine whether the

company is operating profitably or not. Profitability ratios are also important form the point of

view of the investors and the shareholders as most of the earnings are the key drivers for the

shareholders (Ponikvar, Kejžar and Peljhan, 2018). The profitability is the most important factor

in terms of the inter as well intra company comparison so that it gives the idea to the

management about whether the company shall improve the performance of the company, or

whether it is operating well or not or suffering from losses that needs to be recovered (Laitinen

and Laitinen, 2018).

Gross Profit

The gross profit ratio is the ratio which the company makes after the deduction of the costs

incurred by the company to bring the product into the saleable condition. It is basically the

Financial Leverage Ratios

The financial leverage ratios of the company are the ratios which represents the financial

performance of the company. Financial leverage ratios mainly measure the equity value in a

company by making an evaluation of the debt in overall sense. The main aim of the financial

leverage ratios is to show that how much of the assets of the company are belonging to the

shareholders rather than they belong to the creditors (Barbiero Popov and Wolski, 2018). Form

the above graph it can be observed that the average total assets of the company when divided by

the average equity have decreased as the assets have not been utilized by the company in the

most critical value. The ratio increased from 1.08 to 2.49 and hence the company needs to value

the performance of the company.

Profitability ratios

Profitability ratios of the company are the ones that are calculated to determine whether the

company is operating profitably or not. Profitability ratios are also important form the point of

view of the investors and the shareholders as most of the earnings are the key drivers for the

shareholders (Ponikvar, Kejžar and Peljhan, 2018). The profitability is the most important factor

in terms of the inter as well intra company comparison so that it gives the idea to the

management about whether the company shall improve the performance of the company, or

whether it is operating well or not or suffering from losses that needs to be recovered (Laitinen

and Laitinen, 2018).

Gross Profit

The gross profit ratio is the ratio which the company makes after the deduction of the costs

incurred by the company to bring the product into the saleable condition. It is basically the

BENEDICT COMPANY 12

revenue left over after the deduction of the direct costs from the sale value. The gross profit is

important because it reflects the core profitability of the business before the occurrence of the

overhead costs. It also illustrates the financial success of the product or the service (Rosita,

Nurwahyuni and Sari, 2018).

It can be observed that the gross profit of the company is 48% in the year 20X1 and same has

been increased from the previous year where the gross profit margin was at 42%. The ratio has

been increased which thereby reflects the fact that company is reducing the cost of goods sold

and the other operating direct costs to make most of the revenue (Ross, 2016).

Net Profit

The net profit ratio is the ratio calculated after deducting the interest as well as the tax expense to

get the overall situation of the company. The net profit ratio of the benedict company is 21% in

the current year in comparison to the previous year which was 28%. The net profit of the

company seems to have fallen due to the increase in the administrative expenses as well as the

distribution costs too. Therefore it is advised to the Benedict Company to keep a check and

review the costs and get rid of the extra costs (Liang, Lu, Tsai and Shih, 2016).

Return on Assets

It is a sort of a ratio which is utilized to figure out the productivity of the organization in

connection to the aggregate resources available within the organization. Such proportion helps in

breaking down the effectiveness of the administration of the business in association to produce

benefits. The return on assets in simpler terms is how much the company is earning to pay off the

contractual obligations out of its assets (Barillas and Shanken, 2018)

revenue left over after the deduction of the direct costs from the sale value. The gross profit is

important because it reflects the core profitability of the business before the occurrence of the

overhead costs. It also illustrates the financial success of the product or the service (Rosita,

Nurwahyuni and Sari, 2018).

It can be observed that the gross profit of the company is 48% in the year 20X1 and same has

been increased from the previous year where the gross profit margin was at 42%. The ratio has

been increased which thereby reflects the fact that company is reducing the cost of goods sold

and the other operating direct costs to make most of the revenue (Ross, 2016).

Net Profit

The net profit ratio is the ratio calculated after deducting the interest as well as the tax expense to

get the overall situation of the company. The net profit ratio of the benedict company is 21% in

the current year in comparison to the previous year which was 28%. The net profit of the

company seems to have fallen due to the increase in the administrative expenses as well as the

distribution costs too. Therefore it is advised to the Benedict Company to keep a check and

review the costs and get rid of the extra costs (Liang, Lu, Tsai and Shih, 2016).

Return on Assets

It is a sort of a ratio which is utilized to figure out the productivity of the organization in

connection to the aggregate resources available within the organization. Such proportion helps in

breaking down the effectiveness of the administration of the business in association to produce

benefits. The return on assets in simpler terms is how much the company is earning to pay off the

contractual obligations out of its assets (Barillas and Shanken, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.