BEO1105 Assignment Tri 1 2018: Economic Principles & Market Analysis

VerifiedAdded on 2023/06/11

|11

|1627

|363

Homework Assignment

AI Summary

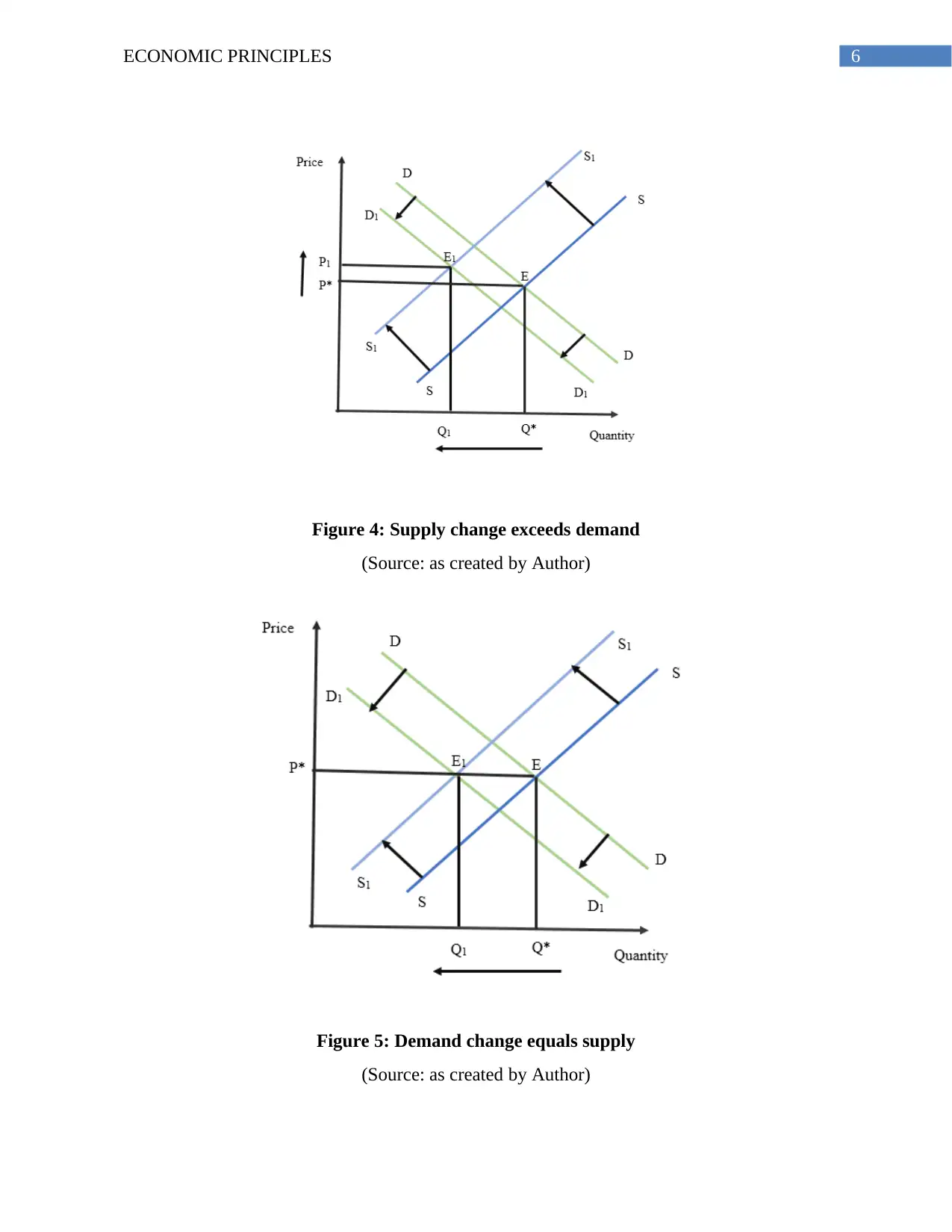

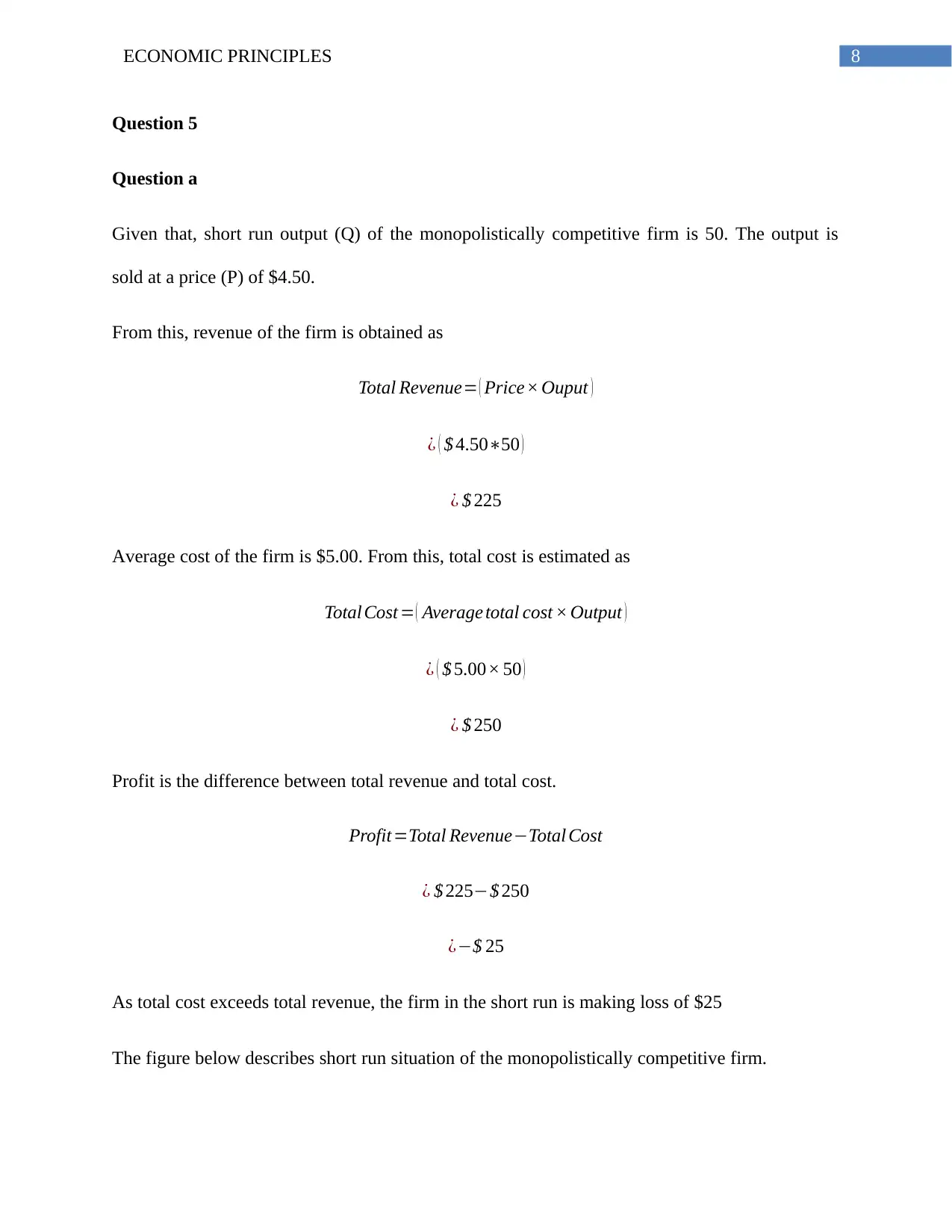

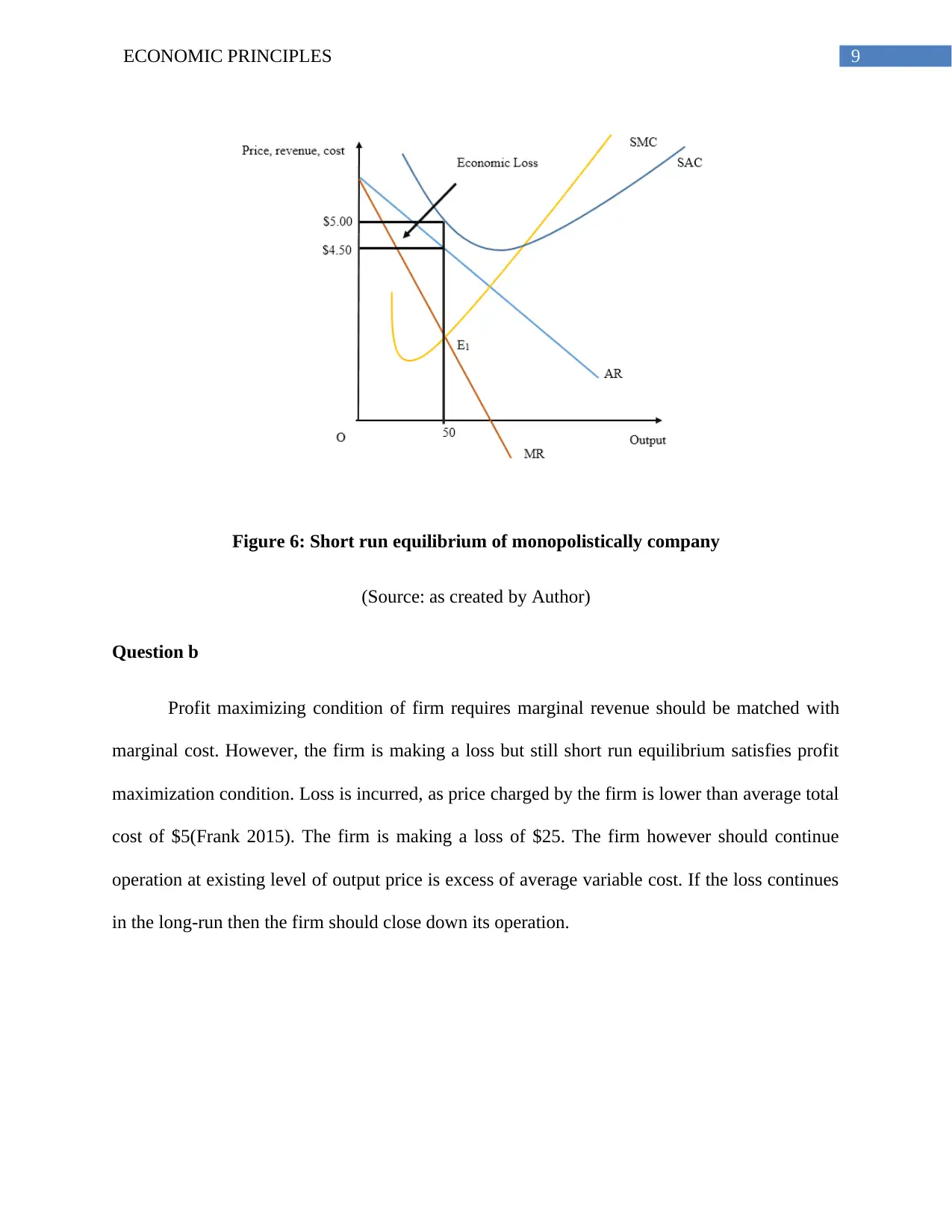

This assignment delves into key economic principles, analyzing market dynamics and elasticity through various scenarios. It examines the relationship between price and demand, the impact of supply shocks on market equilibrium (using the French and Australian wine markets as examples), and the effects of changes in both demand and supply on the orange juice market. The assignment further explores price elasticity of demand in the context of taxi fares and analyzes the short-run equilibrium of a monopolistically competitive firm, determining profitability and optimal operational decisions. The analysis is supported by graphical illustrations to explain the shifts in demand and supply curves and their impact on market outcomes.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.