Berkshire Hathaway's Acquisition - Warren E Buffet 2005 Case Analysis

VerifiedAdded on 2023/06/03

|20

|4233

|375

Case Study

AI Summary

This case study analyzes Berkshire Hathaway's acquisition of PacifiCorp in 2005, examining the market reaction, valuation methods, and bid assessment. It evaluates the deal's impact on Berkshire Hathaway's market value and explores the financial implications of the acquisition. The analysis includes a review of Berkshire Hathaway's investment in MidAmerican Energy Holdings and its past performance, along with an assessment of its investments in companies like American Express and Coca-Cola. The study uses earnings multiple methods to value PacifiCorp and assesses the investment's potential to create value, providing a comprehensive overview of the financial strategies and outcomes associated with the acquisition.

Running head: FINANCE

Warren E Buffet 2005

Name of the Student:

Name of the University:

Author’s Note:

Warren E Buffet 2005

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1WARREN E BUFFET

Table of Contents

In Response to Question 1...............................................................................................................2

In Response to Question 2...............................................................................................................3

In Response to Question 3...............................................................................................................5

In Response to Question 4...............................................................................................................7

In Response to Question 5...............................................................................................................8

In Response to Question 6...............................................................................................................9

In Response to Question 7.............................................................................................................10

Reference.......................................................................................................................................11

Appendix........................................................................................................................................13

Table of Contents

In Response to Question 1...............................................................................................................2

In Response to Question 2...............................................................................................................3

In Response to Question 3...............................................................................................................5

In Response to Question 4...............................................................................................................7

In Response to Question 5...............................................................................................................8

In Response to Question 6...............................................................................................................9

In Response to Question 7.............................................................................................................10

Reference.......................................................................................................................................11

Appendix........................................................................................................................................13

2WARREN E BUFFET

In Response to Question 1

The acquisition of Pacific Corp by Berkshire Hathaway subsidiary company

MidAmerican Energy Holdings was done on May 24, 2005. The Berkshire Hathaway

Incorporation through its investment company MidAmerican Energy Holdings Company did the

acquisition. The parent company for the Pacific Corp was the Scottish Power plc, for an all 9.4

billion, which was a mix of debt and equity. The stock market took this acquisition as a positive

news for the Berkshire Hathaway Incorporation where the shares of the company rose by around

2.4% for that day when the acquisition was announced which represented an all-total rise of 2.55

billion dollars in the market value of the company (Peterson and Malko 2015).

The Berkshire Hathaway was having more than around 43 billion dollars of its

investment parked in Cash and Cash equivalents that were not earning sufficient for the investors

and stakeholders. Since the year 2001, it is crucial to note that the company was in search of

some potential investments that could bring potential source of revenue generation for the

company. The company was in search of an elephant i.e.., a company or an industry where the

investment done by the company is viable and the same was done by the company when the

company found that in the year 2004 (Sunderasan 2015). The return the Berkshire Hathaway saw

in the Energy Industry was lucrative and especially the company Pacific Corp was one of the

lucrative company. The company had some key feature such as it was one of the leading in terms

of market share; the low cost output and the 1.6 million-customer base were some of the key

feature. The company would create value for the MidAmerican Energy Holding Company,

which in turn will create the value for the Berkshire Hathaway company through the sources of

the investment done in the company. The Berkshire Company was having an ideal amount of

In Response to Question 1

The acquisition of Pacific Corp by Berkshire Hathaway subsidiary company

MidAmerican Energy Holdings was done on May 24, 2005. The Berkshire Hathaway

Incorporation through its investment company MidAmerican Energy Holdings Company did the

acquisition. The parent company for the Pacific Corp was the Scottish Power plc, for an all 9.4

billion, which was a mix of debt and equity. The stock market took this acquisition as a positive

news for the Berkshire Hathaway Incorporation where the shares of the company rose by around

2.4% for that day when the acquisition was announced which represented an all-total rise of 2.55

billion dollars in the market value of the company (Peterson and Malko 2015).

The Berkshire Hathaway was having more than around 43 billion dollars of its

investment parked in Cash and Cash equivalents that were not earning sufficient for the investors

and stakeholders. Since the year 2001, it is crucial to note that the company was in search of

some potential investments that could bring potential source of revenue generation for the

company. The company was in search of an elephant i.e.., a company or an industry where the

investment done by the company is viable and the same was done by the company when the

company found that in the year 2004 (Sunderasan 2015). The return the Berkshire Hathaway saw

in the Energy Industry was lucrative and especially the company Pacific Corp was one of the

lucrative company. The company had some key feature such as it was one of the leading in terms

of market share; the low cost output and the 1.6 million-customer base were some of the key

feature. The company would create value for the MidAmerican Energy Holding Company,

which in turn will create the value for the Berkshire Hathaway company through the sources of

the investment done in the company. The Berkshire Company was having an ideal amount of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3WARREN E BUFFET

investment to be deployed put in cash and cash equivalents however; the company due to scarce

investment asset class could not utilize the same (Aggarwal and Burgess 2014).

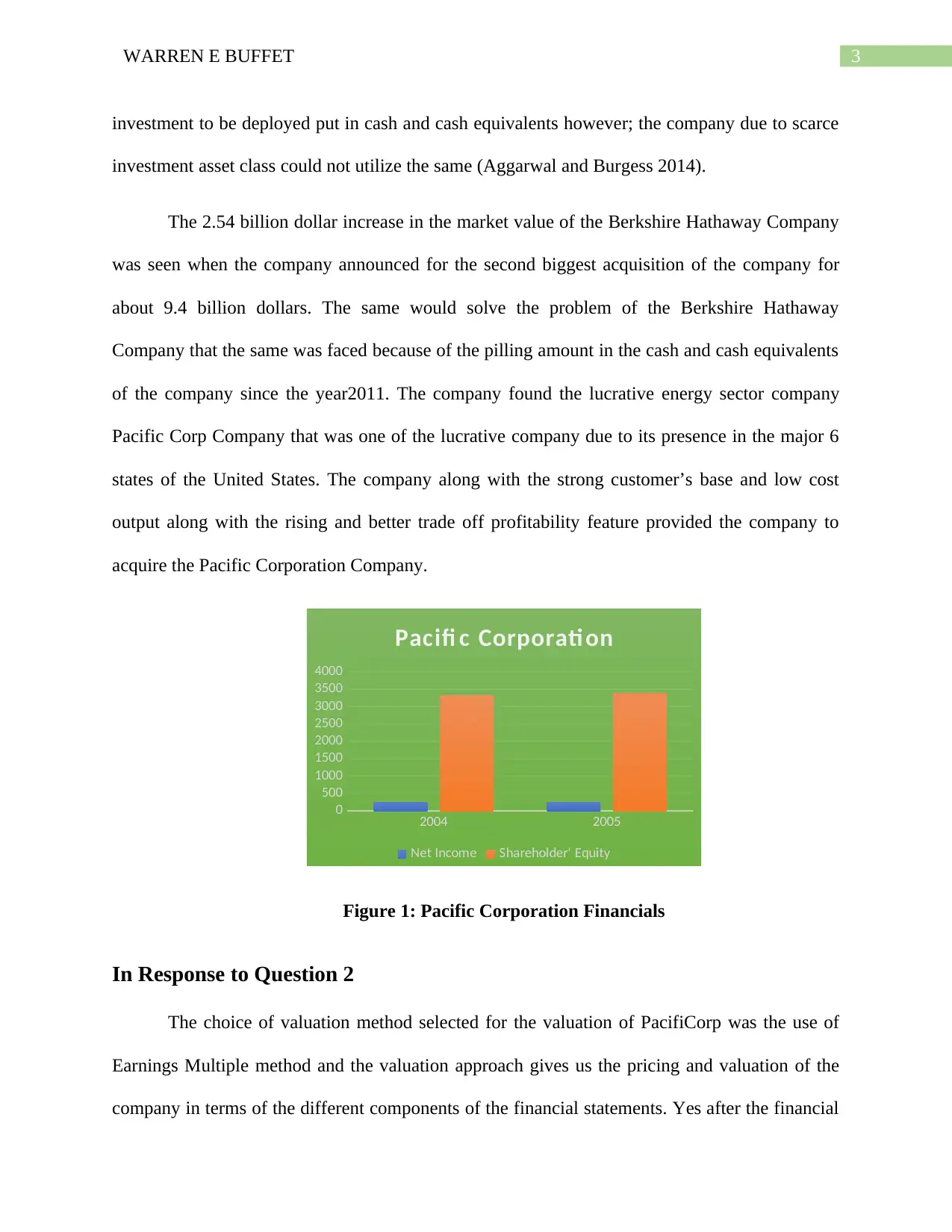

The 2.54 billion dollar increase in the market value of the Berkshire Hathaway Company

was seen when the company announced for the second biggest acquisition of the company for

about 9.4 billion dollars. The same would solve the problem of the Berkshire Hathaway

Company that the same was faced because of the pilling amount in the cash and cash equivalents

of the company since the year2011. The company found the lucrative energy sector company

Pacific Corp Company that was one of the lucrative company due to its presence in the major 6

states of the United States. The company along with the strong customer’s base and low cost

output along with the rising and better trade off profitability feature provided the company to

acquire the Pacific Corporation Company.

2004 2005

0

500

1000

1500

2000

2500

3000

3500

4000

Pacifi c Corporati on

Net Income Shareholder' Equity

Figure 1: Pacific Corporation Financials

In Response to Question 2

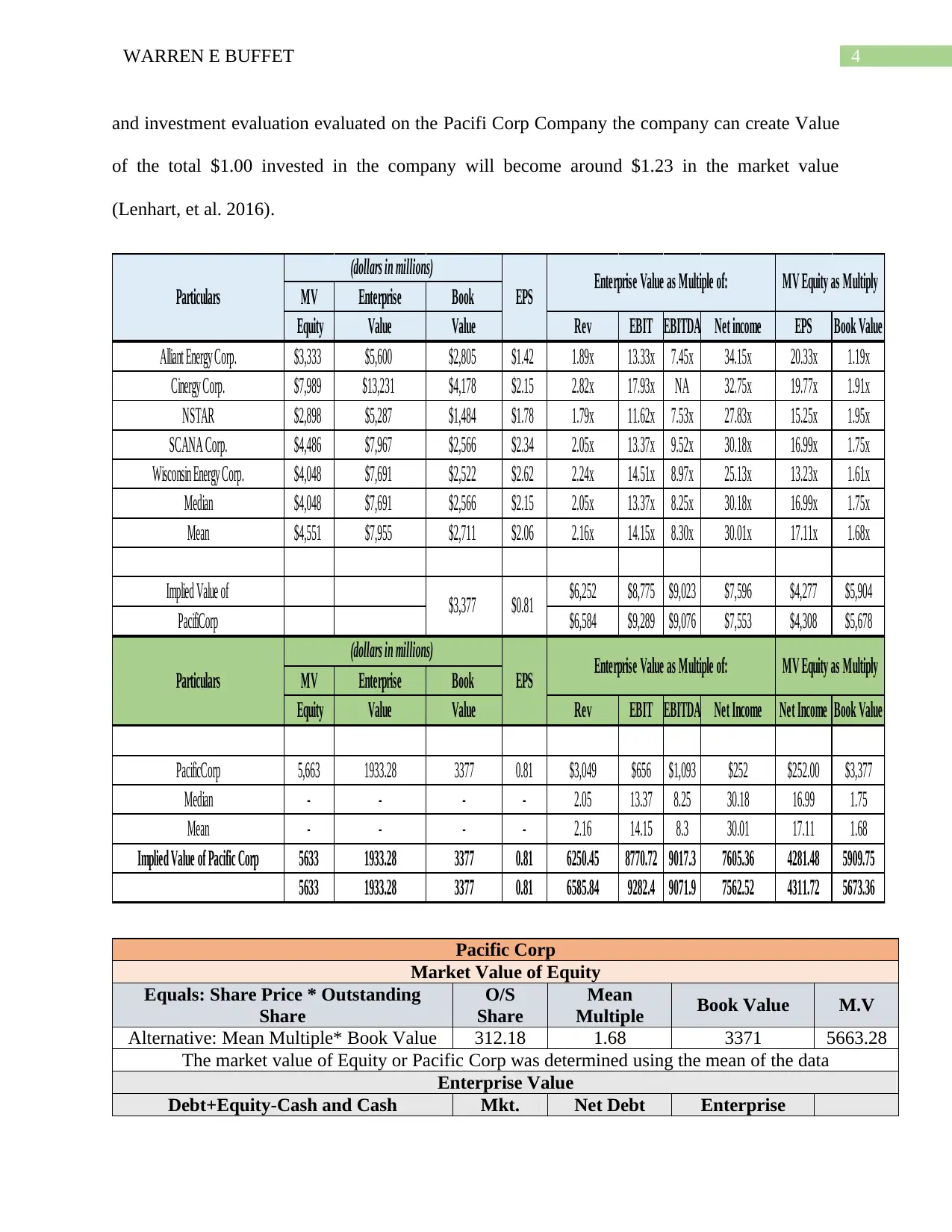

The choice of valuation method selected for the valuation of PacifiCorp was the use of

Earnings Multiple method and the valuation approach gives us the pricing and valuation of the

company in terms of the different components of the financial statements. Yes after the financial

investment to be deployed put in cash and cash equivalents however; the company due to scarce

investment asset class could not utilize the same (Aggarwal and Burgess 2014).

The 2.54 billion dollar increase in the market value of the Berkshire Hathaway Company

was seen when the company announced for the second biggest acquisition of the company for

about 9.4 billion dollars. The same would solve the problem of the Berkshire Hathaway

Company that the same was faced because of the pilling amount in the cash and cash equivalents

of the company since the year2011. The company found the lucrative energy sector company

Pacific Corp Company that was one of the lucrative company due to its presence in the major 6

states of the United States. The company along with the strong customer’s base and low cost

output along with the rising and better trade off profitability feature provided the company to

acquire the Pacific Corporation Company.

2004 2005

0

500

1000

1500

2000

2500

3000

3500

4000

Pacifi c Corporati on

Net Income Shareholder' Equity

Figure 1: Pacific Corporation Financials

In Response to Question 2

The choice of valuation method selected for the valuation of PacifiCorp was the use of

Earnings Multiple method and the valuation approach gives us the pricing and valuation of the

company in terms of the different components of the financial statements. Yes after the financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4WARREN E BUFFET

and investment evaluation evaluated on the Pacifi Corp Company the company can create Value

of the total $1.00 invested in the company will become around $1.23 in the market value

(Lenhart, et al. 2016).

MV Enterprise Book

Equity Value Value Rev EBIT EBITDA Net income EPS Book Value

Alliant Energy Corp. $3,333 $5,600 $2,805 $1.42 1.89x 13.33x 7.45x 34.15x 20.33x 1.19x

Cinergy Corp. $7,989 $13,231 $4,178 $2.15 2.82x 17.93x NA 32.75x 19.77x 1.91x

NSTAR $2,898 $5,287 $1,484 $1.78 1.79x 11.62x 7.53x 27.83x 15.25x 1.95x

SCANA Corp. $4,486 $7,967 $2,566 $2.34 2.05x 13.37x 9.52x 30.18x 16.99x 1.75x

Wisconsin Energy Corp. $4,048 $7,691 $2,522 $2.62 2.24x 14.51x 8.97x 25.13x 13.23x 1.61x

Median $4,048 $7,691 $2,566 $2.15 2.05x 13.37x 8.25x 30.18x 16.99x 1.75x

Mean $4,551 $7,955 $2,711 $2.06 2.16x 14.15x 8.30x 30.01x 17.11x 1.68x

Implied Value of $6,252 $8,775 $9,023 $7,596 $4,277 $5,904

PacifiCorp $6,584 $9,289 $9,076 $7,553 $4,308 $5,678

MV Enterprise Book

Equity Value Value Rev EBIT EBITDA Net Income Net Income Book Value

PacificCorp 5,663 1933.28 3377 0.81 $3,049 $656 $1,093 $252 $252.00 $3,377

Median - - - - 2.05 13.37 8.25 30.18 16.99 1.75

Mean - - - - 2.16 14.15 8.3 30.01 17.11 1.68

Implied Value of Pacific Corp 5633 1933.28 3377 0.81 6250.45 8770.72 9017.3 7605.36 4281.48 5909.75

5633 1933.28 3377 0.81 6585.84 9282.4 9071.9 7562.52 4311.72 5673.36

(dollars in millions) Enterprise Value as Multiple of:

MV Equity as Multiply

MV Equity as Multiply

Particulars EPS

EPSParticulars

(dollars in millions) Enterprise Value as Multiple of:

$3,377 $0.81

Pacific Corp

Market Value of Equity

Equals: Share Price * Outstanding

Share

O/S

Share

Mean

Multiple Book Value M.V

Alternative: Mean Multiple* Book Value 312.18 1.68 3371 5663.28

The market value of Equity or Pacific Corp was determined using the mean of the data

Enterprise Value

Debt+Equity-Cash and Cash Mkt. Net Debt Enterprise

and investment evaluation evaluated on the Pacifi Corp Company the company can create Value

of the total $1.00 invested in the company will become around $1.23 in the market value

(Lenhart, et al. 2016).

MV Enterprise Book

Equity Value Value Rev EBIT EBITDA Net income EPS Book Value

Alliant Energy Corp. $3,333 $5,600 $2,805 $1.42 1.89x 13.33x 7.45x 34.15x 20.33x 1.19x

Cinergy Corp. $7,989 $13,231 $4,178 $2.15 2.82x 17.93x NA 32.75x 19.77x 1.91x

NSTAR $2,898 $5,287 $1,484 $1.78 1.79x 11.62x 7.53x 27.83x 15.25x 1.95x

SCANA Corp. $4,486 $7,967 $2,566 $2.34 2.05x 13.37x 9.52x 30.18x 16.99x 1.75x

Wisconsin Energy Corp. $4,048 $7,691 $2,522 $2.62 2.24x 14.51x 8.97x 25.13x 13.23x 1.61x

Median $4,048 $7,691 $2,566 $2.15 2.05x 13.37x 8.25x 30.18x 16.99x 1.75x

Mean $4,551 $7,955 $2,711 $2.06 2.16x 14.15x 8.30x 30.01x 17.11x 1.68x

Implied Value of $6,252 $8,775 $9,023 $7,596 $4,277 $5,904

PacifiCorp $6,584 $9,289 $9,076 $7,553 $4,308 $5,678

MV Enterprise Book

Equity Value Value Rev EBIT EBITDA Net Income Net Income Book Value

PacificCorp 5,663 1933.28 3377 0.81 $3,049 $656 $1,093 $252 $252.00 $3,377

Median - - - - 2.05 13.37 8.25 30.18 16.99 1.75

Mean - - - - 2.16 14.15 8.3 30.01 17.11 1.68

Implied Value of Pacific Corp 5633 1933.28 3377 0.81 6250.45 8770.72 9017.3 7605.36 4281.48 5909.75

5633 1933.28 3377 0.81 6585.84 9282.4 9071.9 7562.52 4311.72 5673.36

(dollars in millions) Enterprise Value as Multiple of:

MV Equity as Multiply

MV Equity as Multiply

Particulars EPS

EPSParticulars

(dollars in millions) Enterprise Value as Multiple of:

$3,377 $0.81

Pacific Corp

Market Value of Equity

Equals: Share Price * Outstanding

Share

O/S

Share

Mean

Multiple Book Value M.V

Alternative: Mean Multiple* Book Value 312.18 1.68 3371 5663.28

The market value of Equity or Pacific Corp was determined using the mean of the data

Enterprise Value

Debt+Equity-Cash and Cash Mkt. Net Debt Enterprise

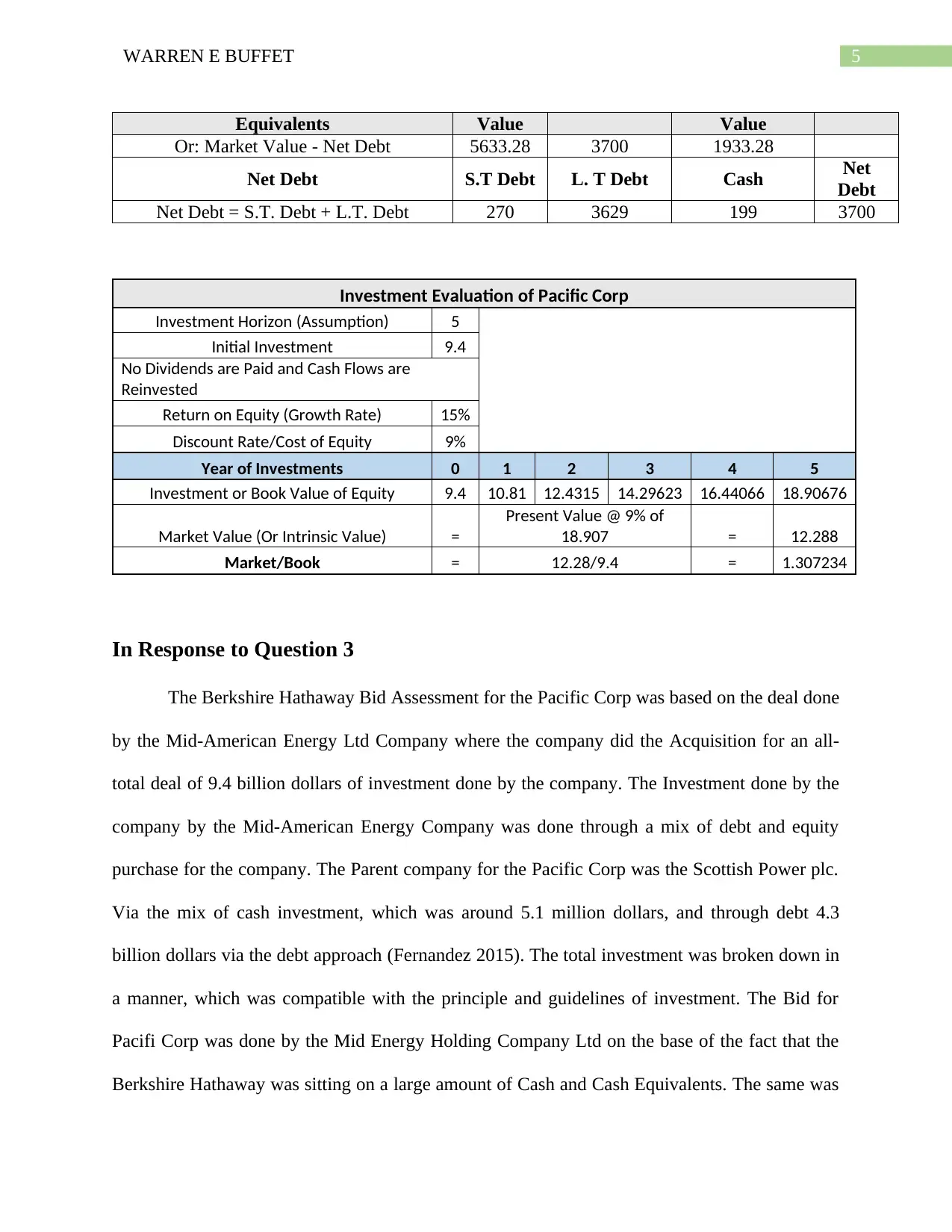

5WARREN E BUFFET

Equivalents Value Value

Or: Market Value - Net Debt 5633.28 3700 1933.28

Net Debt S.T Debt L. T Debt Cash Net

Debt

Net Debt = S.T. Debt + L.T. Debt 270 3629 199 3700

Investment Evaluation of Pacific Corp

Investment Horizon (Assumption) 5

Initial Investment 9.4

No Dividends are Paid and Cash Flows are

Reinvested

Return on Equity (Growth Rate) 15%

Discount Rate/Cost of Equity 9%

Year of Investments 0 1 2 3 4 5

Investment or Book Value of Equity 9.4 10.81 12.4315 14.29623 16.44066 18.90676

Market Value (Or Intrinsic Value) =

Present Value @ 9% of

18.907 = 12.288

Market/Book = 12.28/9.4 = 1.307234

In Response to Question 3

The Berkshire Hathaway Bid Assessment for the Pacific Corp was based on the deal done

by the Mid-American Energy Ltd Company where the company did the Acquisition for an all-

total deal of 9.4 billion dollars of investment done by the company. The Investment done by the

company by the Mid-American Energy Company was done through a mix of debt and equity

purchase for the company. The Parent company for the Pacific Corp was the Scottish Power plc.

Via the mix of cash investment, which was around 5.1 million dollars, and through debt 4.3

billion dollars via the debt approach (Fernandez 2015). The total investment was broken down in

a manner, which was compatible with the principle and guidelines of investment. The Bid for

Pacifi Corp was done by the Mid Energy Holding Company Ltd on the base of the fact that the

Berkshire Hathaway was sitting on a large amount of Cash and Cash Equivalents. The same was

Equivalents Value Value

Or: Market Value - Net Debt 5633.28 3700 1933.28

Net Debt S.T Debt L. T Debt Cash Net

Debt

Net Debt = S.T. Debt + L.T. Debt 270 3629 199 3700

Investment Evaluation of Pacific Corp

Investment Horizon (Assumption) 5

Initial Investment 9.4

No Dividends are Paid and Cash Flows are

Reinvested

Return on Equity (Growth Rate) 15%

Discount Rate/Cost of Equity 9%

Year of Investments 0 1 2 3 4 5

Investment or Book Value of Equity 9.4 10.81 12.4315 14.29623 16.44066 18.90676

Market Value (Or Intrinsic Value) =

Present Value @ 9% of

18.907 = 12.288

Market/Book = 12.28/9.4 = 1.307234

In Response to Question 3

The Berkshire Hathaway Bid Assessment for the Pacific Corp was based on the deal done

by the Mid-American Energy Ltd Company where the company did the Acquisition for an all-

total deal of 9.4 billion dollars of investment done by the company. The Investment done by the

company by the Mid-American Energy Company was done through a mix of debt and equity

purchase for the company. The Parent company for the Pacific Corp was the Scottish Power plc.

Via the mix of cash investment, which was around 5.1 million dollars, and through debt 4.3

billion dollars via the debt approach (Fernandez 2015). The total investment was broken down in

a manner, which was compatible with the principle and guidelines of investment. The Bid for

Pacifi Corp was done by the Mid Energy Holding Company Ltd on the base of the fact that the

Berkshire Hathaway was sitting on a large amount of Cash and Cash Equivalents. The same was

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6WARREN E BUFFET

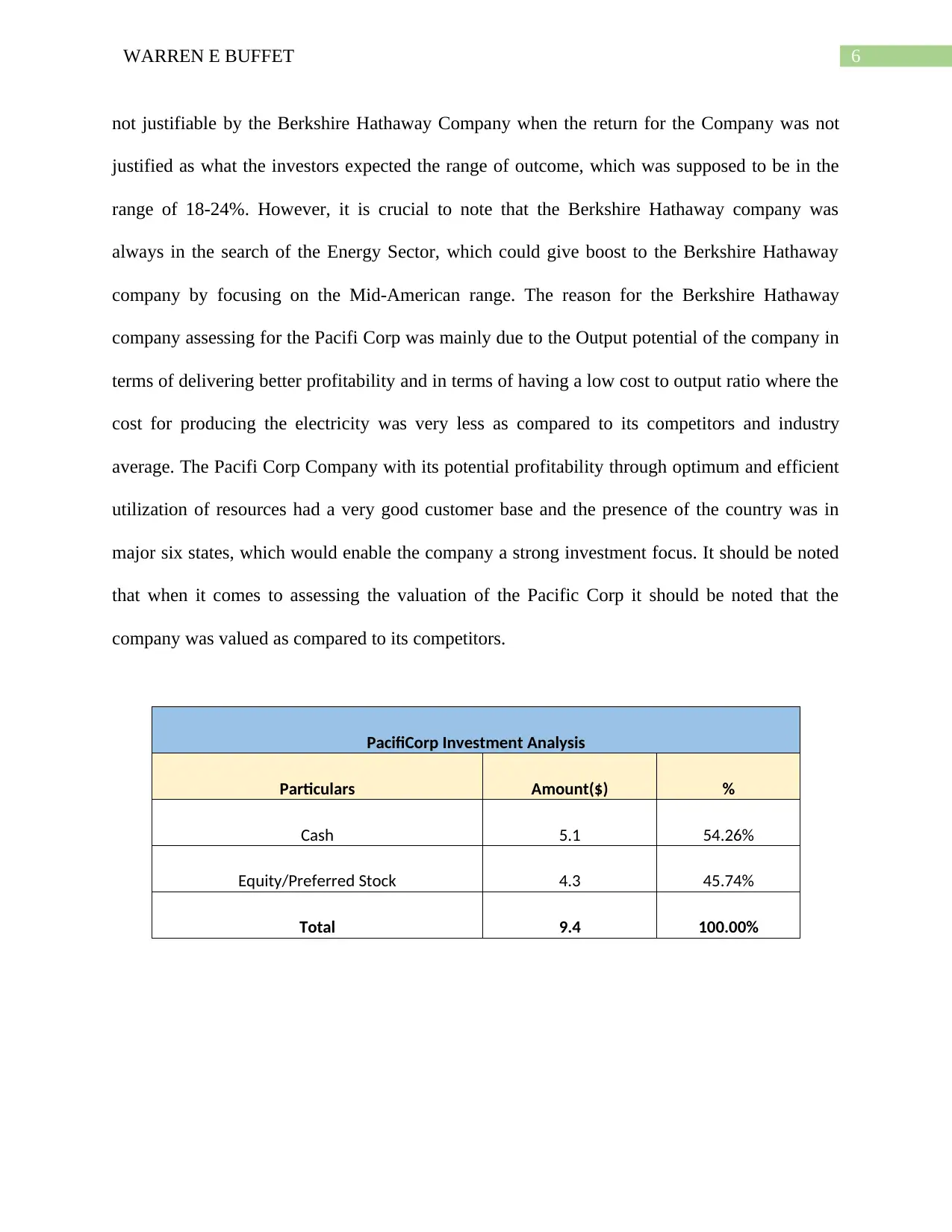

not justifiable by the Berkshire Hathaway Company when the return for the Company was not

justified as what the investors expected the range of outcome, which was supposed to be in the

range of 18-24%. However, it is crucial to note that the Berkshire Hathaway company was

always in the search of the Energy Sector, which could give boost to the Berkshire Hathaway

company by focusing on the Mid-American range. The reason for the Berkshire Hathaway

company assessing for the Pacifi Corp was mainly due to the Output potential of the company in

terms of delivering better profitability and in terms of having a low cost to output ratio where the

cost for producing the electricity was very less as compared to its competitors and industry

average. The Pacifi Corp Company with its potential profitability through optimum and efficient

utilization of resources had a very good customer base and the presence of the country was in

major six states, which would enable the company a strong investment focus. It should be noted

that when it comes to assessing the valuation of the Pacific Corp it should be noted that the

company was valued as compared to its competitors.

PacifiCorp Investment Analysis

Particulars Amount($) %

Cash 5.1 54.26%

Equity/Preferred Stock 4.3 45.74%

Total 9.4 100.00%

not justifiable by the Berkshire Hathaway Company when the return for the Company was not

justified as what the investors expected the range of outcome, which was supposed to be in the

range of 18-24%. However, it is crucial to note that the Berkshire Hathaway company was

always in the search of the Energy Sector, which could give boost to the Berkshire Hathaway

company by focusing on the Mid-American range. The reason for the Berkshire Hathaway

company assessing for the Pacifi Corp was mainly due to the Output potential of the company in

terms of delivering better profitability and in terms of having a low cost to output ratio where the

cost for producing the electricity was very less as compared to its competitors and industry

average. The Pacifi Corp Company with its potential profitability through optimum and efficient

utilization of resources had a very good customer base and the presence of the country was in

major six states, which would enable the company a strong investment focus. It should be noted

that when it comes to assessing the valuation of the Pacific Corp it should be noted that the

company was valued as compared to its competitors.

PacifiCorp Investment Analysis

Particulars Amount($) %

Cash 5.1 54.26%

Equity/Preferred Stock 4.3 45.74%

Total 9.4 100.00%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7WARREN E BUFFET

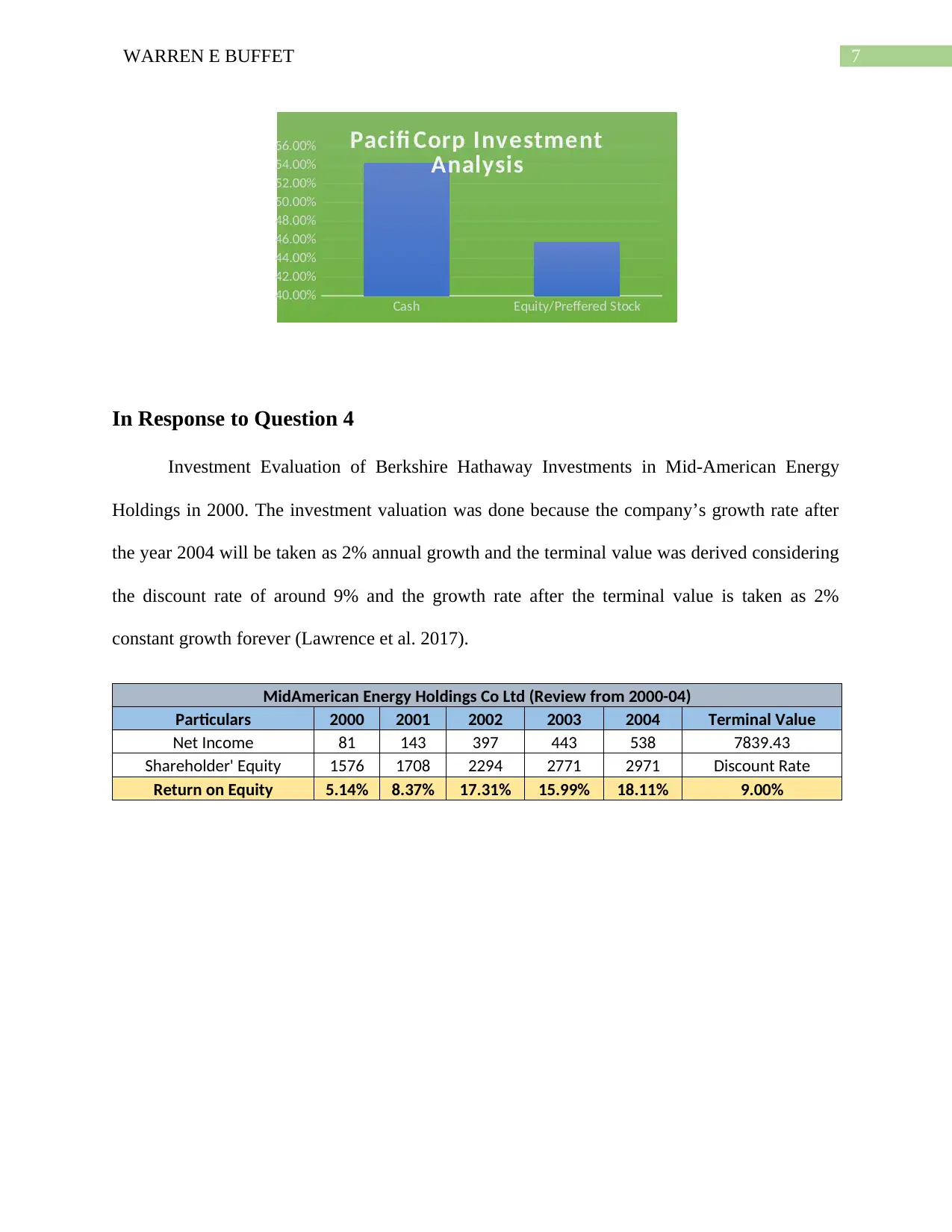

In Response to Question 4

Investment Evaluation of Berkshire Hathaway Investments in Mid-American Energy

Holdings in 2000. The investment valuation was done because the company’s growth rate after

the year 2004 will be taken as 2% annual growth and the terminal value was derived considering

the discount rate of around 9% and the growth rate after the terminal value is taken as 2%

constant growth forever (Lawrence et al. 2017).

MidAmerican Energy Holdings Co Ltd (Review from 2000-04)

Particulars 2000 2001 2002 2003 2004 Terminal Value

Net Income 81 143 397 443 538 7839.43

Shareholder' Equity 1576 1708 2294 2771 2971 Discount Rate

Return on Equity 5.14% 8.37% 17.31% 15.99% 18.11% 9.00%

Cash Equity/Preffered Stock

40.00%

42.00%

44.00%

46.00%

48.00%

50.00%

52.00%

54.00%

56.00% Pacifi Corp Investment

Analysis

In Response to Question 4

Investment Evaluation of Berkshire Hathaway Investments in Mid-American Energy

Holdings in 2000. The investment valuation was done because the company’s growth rate after

the year 2004 will be taken as 2% annual growth and the terminal value was derived considering

the discount rate of around 9% and the growth rate after the terminal value is taken as 2%

constant growth forever (Lawrence et al. 2017).

MidAmerican Energy Holdings Co Ltd (Review from 2000-04)

Particulars 2000 2001 2002 2003 2004 Terminal Value

Net Income 81 143 397 443 538 7839.43

Shareholder' Equity 1576 1708 2294 2771 2971 Discount Rate

Return on Equity 5.14% 8.37% 17.31% 15.99% 18.11% 9.00%

Cash Equity/Preffered Stock

40.00%

42.00%

44.00%

46.00%

48.00%

50.00%

52.00%

54.00%

56.00% Pacifi Corp Investment

Analysis

8WARREN E BUFFET

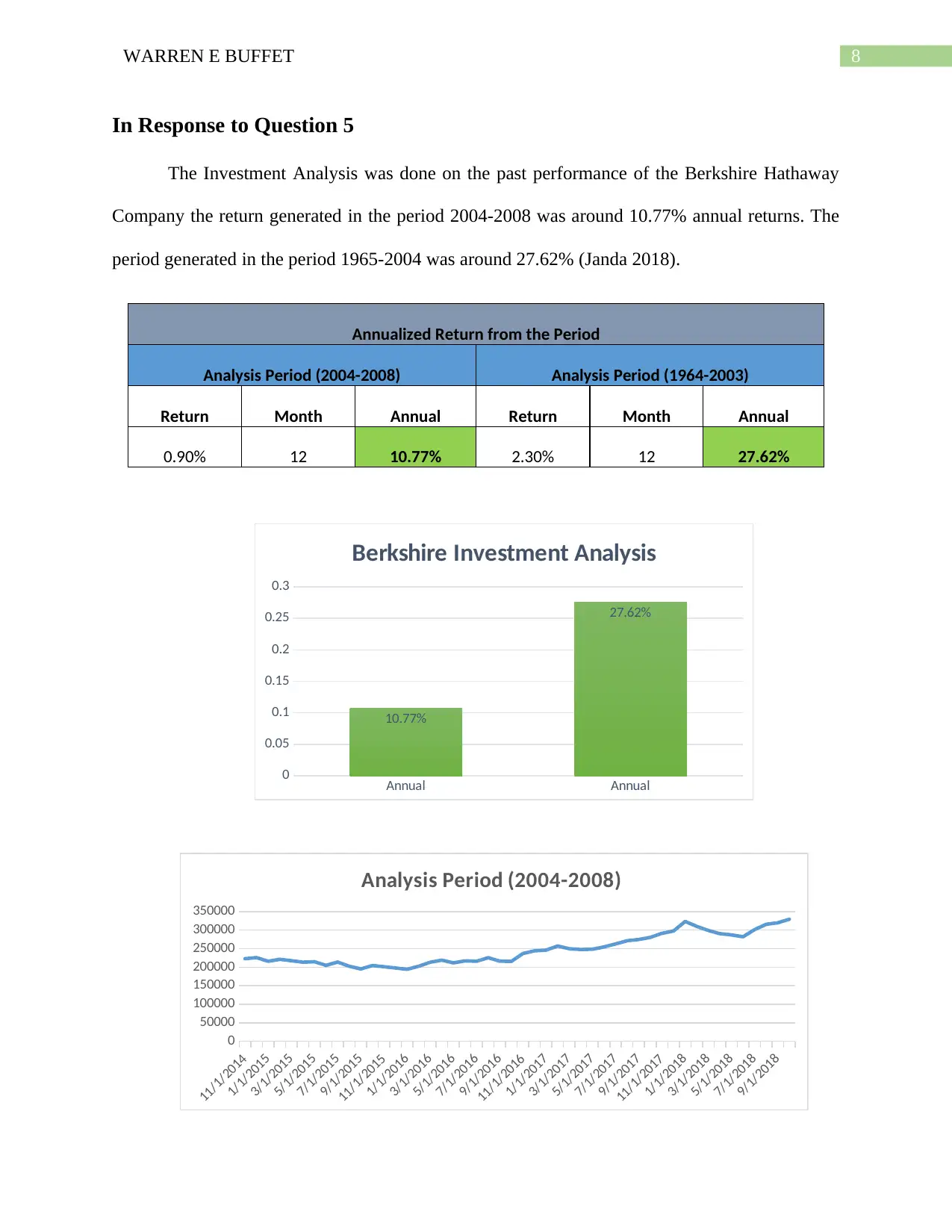

In Response to Question 5

The Investment Analysis was done on the past performance of the Berkshire Hathaway

Company the return generated in the period 2004-2008 was around 10.77% annual returns. The

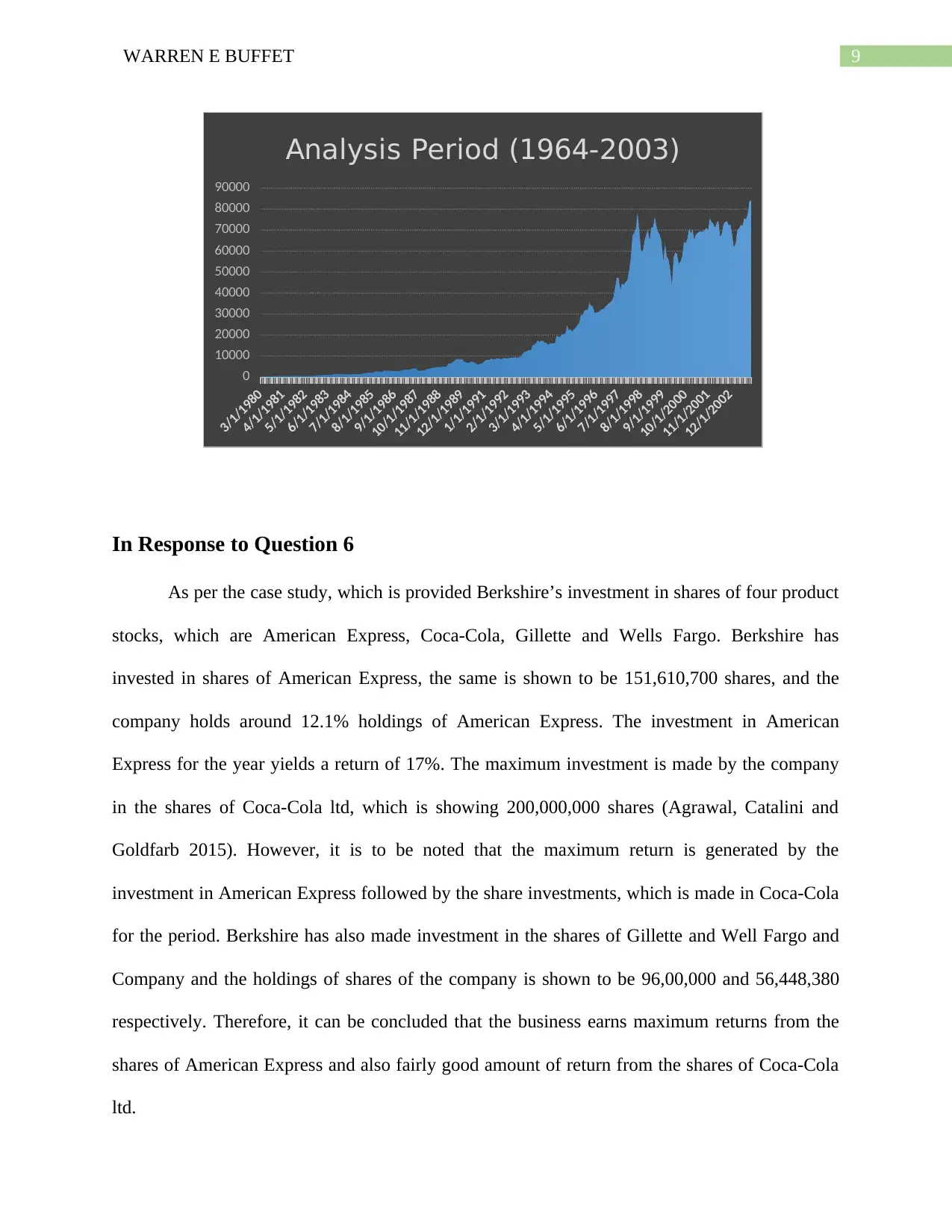

period generated in the period 1965-2004 was around 27.62% (Janda 2018).

Annualized Return from the Period

Analysis Period (2004-2008) Analysis Period (1964-2003)

Return Month Annual Return Month Annual

0.90% 12 10.77% 2.30% 12 27.62%

Annual Annual

0

0.05

0.1

0.15

0.2

0.25

0.3

10.77%

27.62%

Berkshire Investment Analysis

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

1/1/2017

3/1/2017

5/1/2017

7/1/2017

9/1/2017

11/1/2017

1/1/2018

3/1/2018

5/1/2018

7/1/2018

9/1/2018

0

50000

100000

150000

200000

250000

300000

350000

Analysis Period (2004-2008)

In Response to Question 5

The Investment Analysis was done on the past performance of the Berkshire Hathaway

Company the return generated in the period 2004-2008 was around 10.77% annual returns. The

period generated in the period 1965-2004 was around 27.62% (Janda 2018).

Annualized Return from the Period

Analysis Period (2004-2008) Analysis Period (1964-2003)

Return Month Annual Return Month Annual

0.90% 12 10.77% 2.30% 12 27.62%

Annual Annual

0

0.05

0.1

0.15

0.2

0.25

0.3

10.77%

27.62%

Berkshire Investment Analysis

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

1/1/2017

3/1/2017

5/1/2017

7/1/2017

9/1/2017

11/1/2017

1/1/2018

3/1/2018

5/1/2018

7/1/2018

9/1/2018

0

50000

100000

150000

200000

250000

300000

350000

Analysis Period (2004-2008)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9WARREN E BUFFET

In Response to Question 6

As per the case study, which is provided Berkshire’s investment in shares of four product

stocks, which are American Express, Coca-Cola, Gillette and Wells Fargo. Berkshire has

invested in shares of American Express, the same is shown to be 151,610,700 shares, and the

company holds around 12.1% holdings of American Express. The investment in American

Express for the year yields a return of 17%. The maximum investment is made by the company

in the shares of Coca-Cola ltd, which is showing 200,000,000 shares (Agrawal, Catalini and

Goldfarb 2015). However, it is to be noted that the maximum return is generated by the

investment in American Express followed by the share investments, which is made in Coca-Cola

for the period. Berkshire has also made investment in the shares of Gillette and Well Fargo and

Company and the holdings of shares of the company is shown to be 96,00,000 and 56,448,380

respectively. Therefore, it can be concluded that the business earns maximum returns from the

shares of American Express and also fairly good amount of return from the shares of Coca-Cola

ltd.

3/1/1980

4/1/1981

5/1/1982

6/1/1983

7/1/1984

8/1/1985

9/1/1986

10/1/1987

11/1/1988

12/1/1989

1/1/1991

2/1/1992

3/1/1993

4/1/1994

5/1/1995

6/1/1996

7/1/1997

8/1/1998

9/1/1999

10/1/2000

11/1/2001

12/1/2002

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

Analysis Period (1964-2003)

In Response to Question 6

As per the case study, which is provided Berkshire’s investment in shares of four product

stocks, which are American Express, Coca-Cola, Gillette and Wells Fargo. Berkshire has

invested in shares of American Express, the same is shown to be 151,610,700 shares, and the

company holds around 12.1% holdings of American Express. The investment in American

Express for the year yields a return of 17%. The maximum investment is made by the company

in the shares of Coca-Cola ltd, which is showing 200,000,000 shares (Agrawal, Catalini and

Goldfarb 2015). However, it is to be noted that the maximum return is generated by the

investment in American Express followed by the share investments, which is made in Coca-Cola

for the period. Berkshire has also made investment in the shares of Gillette and Well Fargo and

Company and the holdings of shares of the company is shown to be 96,00,000 and 56,448,380

respectively. Therefore, it can be concluded that the business earns maximum returns from the

shares of American Express and also fairly good amount of return from the shares of Coca-Cola

ltd.

3/1/1980

4/1/1981

5/1/1982

6/1/1983

7/1/1984

8/1/1985

9/1/1986

10/1/1987

11/1/1988

12/1/1989

1/1/1991

2/1/1992

3/1/1993

4/1/1994

5/1/1995

6/1/1996

7/1/1997

8/1/1998

9/1/1999

10/1/2000

11/1/2001

12/1/2002

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

Analysis Period (1964-2003)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10WARREN E BUFFET

In Response to Question 7

As per the investment philosophy of the business, the management of the company

believes in economic reality of the financial information and not just the accounting reality. The

management of the company rightly believes that the consolidated annual reports do not

discloses all relevant financial information of the business (Barton and Wiseman 2014). The

economic reality as stated by Buffet covers aspects such as long-term prosperity, operational

history of business and unlike accounting reality considers the cash flows of the business in order

to determine the worth (Ma, Zhao and Xi 2016). Another consideration which is considered by

the Buffet’s philosophy is related to opportunity costs and therefore in assessing an investment

an alternative investment must also be considered which will be an opportunity lost in case the

business select the current investment (Wong 2015). Another concept on which Buffet provided

emphasis is the concept of time value of money, which is an integral part for assessing the

performance of the investment and the worth of the investment.

In Response to Question 7

As per the investment philosophy of the business, the management of the company

believes in economic reality of the financial information and not just the accounting reality. The

management of the company rightly believes that the consolidated annual reports do not

discloses all relevant financial information of the business (Barton and Wiseman 2014). The

economic reality as stated by Buffet covers aspects such as long-term prosperity, operational

history of business and unlike accounting reality considers the cash flows of the business in order

to determine the worth (Ma, Zhao and Xi 2016). Another consideration which is considered by

the Buffet’s philosophy is related to opportunity costs and therefore in assessing an investment

an alternative investment must also be considered which will be an opportunity lost in case the

business select the current investment (Wong 2015). Another concept on which Buffet provided

emphasis is the concept of time value of money, which is an integral part for assessing the

performance of the investment and the worth of the investment.

11WARREN E BUFFET

Reference

Aggarwal, S. and Burgess, E., 2014. Performance-based models to address utility challenges.

The Electricity Journal, 27(6), pp.48-60.

Agrawal, A., Catalini, C. and Goldfarb, A., 2015. Crowdfunding: Geography, social networks,

and the timing of investment decisions. Journal of Economics & Management Strategy, 24(2),

pp.253-274.

Barton, D. and Wiseman, M., 2014. Focusing capital on the long term. Harvard Business

Review, 92(1/2), pp.44-51.

Fernandez, P., 2015. How to value a seasonal company discounting cash flows.

Janda, K., 2018. Earnings Stability and Peer Selection for Indirect Valuation (No. 2018/14).

Charles University Prague, Faculty of Social Sciences, Institute of Economic Studies.

Lawrence, K., de la Hoz, E., Barker, J. and Waldrip, J., 2017. Principal Aquatic Scientist.

Lenhart, S., Nelson-Marsh, N., Wilson, E.J. and Solan, D., 2016. Electricity governance and the

Western energy imbalance market in the United States: The necessity of interorganizational

collaboration. Energy Research & Social Science, 19, pp.94-107.

Ma, Y., Zhao, Q. and Xi, M., 2016. Decision-makings in safety investment: an opportunity cost

perspective. Safety science, 83, pp.31-39.

Peterson, C.E. and Malko, J.R., 2015. Ring Fencing Rocky Mountain Power in Utah. The

Electricity Journal, 28(6), pp.63-71.

Reference

Aggarwal, S. and Burgess, E., 2014. Performance-based models to address utility challenges.

The Electricity Journal, 27(6), pp.48-60.

Agrawal, A., Catalini, C. and Goldfarb, A., 2015. Crowdfunding: Geography, social networks,

and the timing of investment decisions. Journal of Economics & Management Strategy, 24(2),

pp.253-274.

Barton, D. and Wiseman, M., 2014. Focusing capital on the long term. Harvard Business

Review, 92(1/2), pp.44-51.

Fernandez, P., 2015. How to value a seasonal company discounting cash flows.

Janda, K., 2018. Earnings Stability and Peer Selection for Indirect Valuation (No. 2018/14).

Charles University Prague, Faculty of Social Sciences, Institute of Economic Studies.

Lawrence, K., de la Hoz, E., Barker, J. and Waldrip, J., 2017. Principal Aquatic Scientist.

Lenhart, S., Nelson-Marsh, N., Wilson, E.J. and Solan, D., 2016. Electricity governance and the

Western energy imbalance market in the United States: The necessity of interorganizational

collaboration. Energy Research & Social Science, 19, pp.94-107.

Ma, Y., Zhao, Q. and Xi, M., 2016. Decision-makings in safety investment: an opportunity cost

perspective. Safety science, 83, pp.31-39.

Peterson, C.E. and Malko, J.R., 2015. Ring Fencing Rocky Mountain Power in Utah. The

Electricity Journal, 28(6), pp.63-71.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.