Acquisition Proposal: Berkshire Hathaway's Acquisition of Sony Corp

VerifiedAdded on 2022/09/12

|15

|3517

|21

Project

AI Summary

This project presents an acquisition proposal where Berkshire Hathaway Inc. is proposed to acquire Sony Corporation. The proposal explores the benefits for both companies, including diversification, market expansion, and synergy creation. The document includes a valuation analysis of Sony Corporation using intrinsic value, price-earnings ratio, and the Capital Asset Pricing Model (CAPM). The acquisition is justified by analyzing the benefits, the financial implications of the deal, and the increase in shareholder value. The analysis includes a comparison of the companies' financial metrics before and after the acquisition, and the impact on earnings per share. The proposal also discusses the regulatory and financial implications of a cross-border acquisition, the challenges, and potential reasons for failure. The assignment is a comprehensive analysis of a potential merger or acquisition, demonstrating an understanding of finance principles and strategic planning.

Acquistion Proposal

[Document subtitle]

[Document subtitle]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Acquisition Proposal

Table of Contents

Part 1................................................................................................................................................2

Berkshire Hathaway Inc..................................................................................................................2

Sony Corporation.............................................................................................................................2

Benefits from Acquisition................................................................................................................3

Valuation of Sony............................................................................................................................6

Part 2 Personal Reflection...............................................................................................................9

References......................................................................................................................................13

1

Table of Contents

Part 1................................................................................................................................................2

Berkshire Hathaway Inc..................................................................................................................2

Sony Corporation.............................................................................................................................2

Benefits from Acquisition................................................................................................................3

Valuation of Sony............................................................................................................................6

Part 2 Personal Reflection...............................................................................................................9

References......................................................................................................................................13

1

Acquisition Proposal

Part 1

The acquisition is one of the very common business activities where one company acquires or

purchase a majority of stake in another company in exchange for cash or kind. Purchasing more

than 50% of the stocks or assets of the other company will in achieving economies of scale,

diversify into new markets and increase the synergy along with a reduction in cost (Kenton,

2019). Cross border acquisition also enables the company to enter into the new markets. In this

talk we will propose an acquisition strategy through with Berkshire Hathaway Inc can acquire

Sony Corporation and explain the feasibility, justification of consideration and benefits that will

be derived by both the companies out of this proposal.

Berkshire Hathaway Inc.

Berkshire Hathaway is a multinational conglomerate company led by Warren E Buffet. It holds

controlling as well as economic interest in many national and international giants. The company

is headquartered in Omaha, Nebraska which started its business with a group of textiles milling

plants. The holdings of the company are massive that its main business has become acquiring an

interest in other companies and gaining value from the sound performance of those companies

(Hargrave, 2020). Some of the most popular companies owned are GEICO and Fruits and

Looms. The company also holds some economic interest in giants like Apple, Bank of America,

Coca Cola and Wells Fargo. The company’s key goals are to acquire economically sound

companies that have a sustainable competitive advantage. The companies acquired makes

Berkshire Hathaway’s presence in multiple industries which makes its portfolio a very well

diverse one (Alpert, 2020).

2

Part 1

The acquisition is one of the very common business activities where one company acquires or

purchase a majority of stake in another company in exchange for cash or kind. Purchasing more

than 50% of the stocks or assets of the other company will in achieving economies of scale,

diversify into new markets and increase the synergy along with a reduction in cost (Kenton,

2019). Cross border acquisition also enables the company to enter into the new markets. In this

talk we will propose an acquisition strategy through with Berkshire Hathaway Inc can acquire

Sony Corporation and explain the feasibility, justification of consideration and benefits that will

be derived by both the companies out of this proposal.

Berkshire Hathaway Inc.

Berkshire Hathaway is a multinational conglomerate company led by Warren E Buffet. It holds

controlling as well as economic interest in many national and international giants. The company

is headquartered in Omaha, Nebraska which started its business with a group of textiles milling

plants. The holdings of the company are massive that its main business has become acquiring an

interest in other companies and gaining value from the sound performance of those companies

(Hargrave, 2020). Some of the most popular companies owned are GEICO and Fruits and

Looms. The company also holds some economic interest in giants like Apple, Bank of America,

Coca Cola and Wells Fargo. The company’s key goals are to acquire economically sound

companies that have a sustainable competitive advantage. The companies acquired makes

Berkshire Hathaway’s presence in multiple industries which makes its portfolio a very well

diverse one (Alpert, 2020).

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Acquisition Proposal

Sony Corporation

Sony Corporation is another multinational conglomerate specializing in electronic equipment for

a wide range of domestic as well as commercial use. The company designs develop and

manufacture and markets the equipment and devices. The sales are made in almost every sector

and industry and the company has a leading position in the markets of many countries. Mobile

communications, Gaming, Image products and solution and entertainment are some of the

segments where the company has already marked its presence. It also into film and television

production, distribution. It also records sells and manages licensing requirement of music in

many countries. It has manufacturing units present in many Asian countries including Japan

apart from third-party contractors used by the company. It has many subsidiaries in the United

States. Thus, marketing is done mainly through sales subsidiaries across the globe (Reuters,

2020). In 2019 the company reported an annual turnover of JPY 87 million, EBITDA of JPY

12.68 million and Earnings per share of JPY 723. The company has also recently established a

$100 million COVID-19 relief fund (Sony , 2020). Sony has wide reach business in the USA

named as Sony Corporation of America. Headquartered in New York the principal business is of

electronics, interactive entertainment, pictures, music entertainment and Sony/ATV Music

Publishing company. The US division has a sale of approximately $78 billion for the fiscal year

ended March 31, 2019, and has approximately 114,400 employees (Sony, 2020).

Benefits from Acquisition

Currently, in the electronic segment, Berkshire Hathaway owns companies such as TTI, Mouser

and Sager electronics, etc. The company does not own any subsidiary that deals in consumer

electronics, entertainment and music sector like Sony (Worth, 2018). The acquisition of Sony

will enable Berkshire to set foot into the new industry through a highly reputed brand name. The

3

Sony Corporation

Sony Corporation is another multinational conglomerate specializing in electronic equipment for

a wide range of domestic as well as commercial use. The company designs develop and

manufacture and markets the equipment and devices. The sales are made in almost every sector

and industry and the company has a leading position in the markets of many countries. Mobile

communications, Gaming, Image products and solution and entertainment are some of the

segments where the company has already marked its presence. It also into film and television

production, distribution. It also records sells and manages licensing requirement of music in

many countries. It has manufacturing units present in many Asian countries including Japan

apart from third-party contractors used by the company. It has many subsidiaries in the United

States. Thus, marketing is done mainly through sales subsidiaries across the globe (Reuters,

2020). In 2019 the company reported an annual turnover of JPY 87 million, EBITDA of JPY

12.68 million and Earnings per share of JPY 723. The company has also recently established a

$100 million COVID-19 relief fund (Sony , 2020). Sony has wide reach business in the USA

named as Sony Corporation of America. Headquartered in New York the principal business is of

electronics, interactive entertainment, pictures, music entertainment and Sony/ATV Music

Publishing company. The US division has a sale of approximately $78 billion for the fiscal year

ended March 31, 2019, and has approximately 114,400 employees (Sony, 2020).

Benefits from Acquisition

Currently, in the electronic segment, Berkshire Hathaway owns companies such as TTI, Mouser

and Sager electronics, etc. The company does not own any subsidiary that deals in consumer

electronics, entertainment and music sector like Sony (Worth, 2018). The acquisition of Sony

will enable Berkshire to set foot into the new industry through a highly reputed brand name. The

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Acquisition Proposal

company will have to make no efforts to improve the working of Sony. It will gain the benefit of

earning revenue through the well set platform. The international acquisition arrangement will

open more opportunities to expand for Sony (Japanese company) in the USA through being a

company of Berkshire Hathaway group.

According to the modern portfolio theory suggested by Harry Markowitz, the investor should be

able to maximize return through taking an optimum risk. It is possible to design such a portfolio

that does not advocate the theory of higher the risk, high are the returns. It includes the

application of the concepts of diversification of securities and class of assets and also

understanding the relationship between different classes of assets that a company owns in its

portfolio. The theory suggests that the company faces both systematic as well as unsystematic

risks. The systematic risk is the risk arising from market and industry condition and the

organization does not have much control over it. However, the organization has control over the

unsystematic risk as it is majorly related to how the internal matters of the company are being

managed (Mcclure, 2020). However, if the portfolio is poorly diversified it cannot prevent the

organization from systematic risk. Thus, Berkshire, if includes Sony in its portfolio the

systematic risk in the electronic segment of company’s holding, will be spread and it will add a

new company type thus making Berkshire Hathaway’s portfolio more diversified.

Capital Asset Pricing Model is a widely used formula in the finance field that is used to evaluate

the expected return on investment. CAPM model also accounts for the beta that represents the

possibilities of price fluctuation in a security and also market risk premium which is the extra

risk borne by the investor by investing in a particular security. The acquisition of Sony will be

justified only when the expected return is more than the weighted average cost of capital for

Berkshire Hathaway (ACCA Global, n.d.).

4

company will have to make no efforts to improve the working of Sony. It will gain the benefit of

earning revenue through the well set platform. The international acquisition arrangement will

open more opportunities to expand for Sony (Japanese company) in the USA through being a

company of Berkshire Hathaway group.

According to the modern portfolio theory suggested by Harry Markowitz, the investor should be

able to maximize return through taking an optimum risk. It is possible to design such a portfolio

that does not advocate the theory of higher the risk, high are the returns. It includes the

application of the concepts of diversification of securities and class of assets and also

understanding the relationship between different classes of assets that a company owns in its

portfolio. The theory suggests that the company faces both systematic as well as unsystematic

risks. The systematic risk is the risk arising from market and industry condition and the

organization does not have much control over it. However, the organization has control over the

unsystematic risk as it is majorly related to how the internal matters of the company are being

managed (Mcclure, 2020). However, if the portfolio is poorly diversified it cannot prevent the

organization from systematic risk. Thus, Berkshire, if includes Sony in its portfolio the

systematic risk in the electronic segment of company’s holding, will be spread and it will add a

new company type thus making Berkshire Hathaway’s portfolio more diversified.

Capital Asset Pricing Model is a widely used formula in the finance field that is used to evaluate

the expected return on investment. CAPM model also accounts for the beta that represents the

possibilities of price fluctuation in a security and also market risk premium which is the extra

risk borne by the investor by investing in a particular security. The acquisition of Sony will be

justified only when the expected return is more than the weighted average cost of capital for

Berkshire Hathaway (ACCA Global, n.d.).

4

Acquisition Proposal

Before deciding on to valuation of the company any mode of offer the company has to evaluate

various implications as the acquisition is a cross border deal which may have various monetary

and regulatory implications. Many incentives can be derived out of these transactions and the

trade relations between the two companies also impact the merger process. There are many

regulatory and taxation related norms applicable in the USA as well as Japan that have an impact

on the transaction. The viability of the proposal is also dependent on the implications. Thus,

regulatory approvals, political support, and other risk factors should be studied and their

implications should be evaluated.

Valuation of Sony

Now to enable the commencement of acquisition, we will draft an acquisition proposal that will

constitute the valuation of the company. There are various valuation methods used commonly in

trade but we need to choose an appropriate valuation method that justifies the price paid for the

acquisition and is also fair for both the parties.

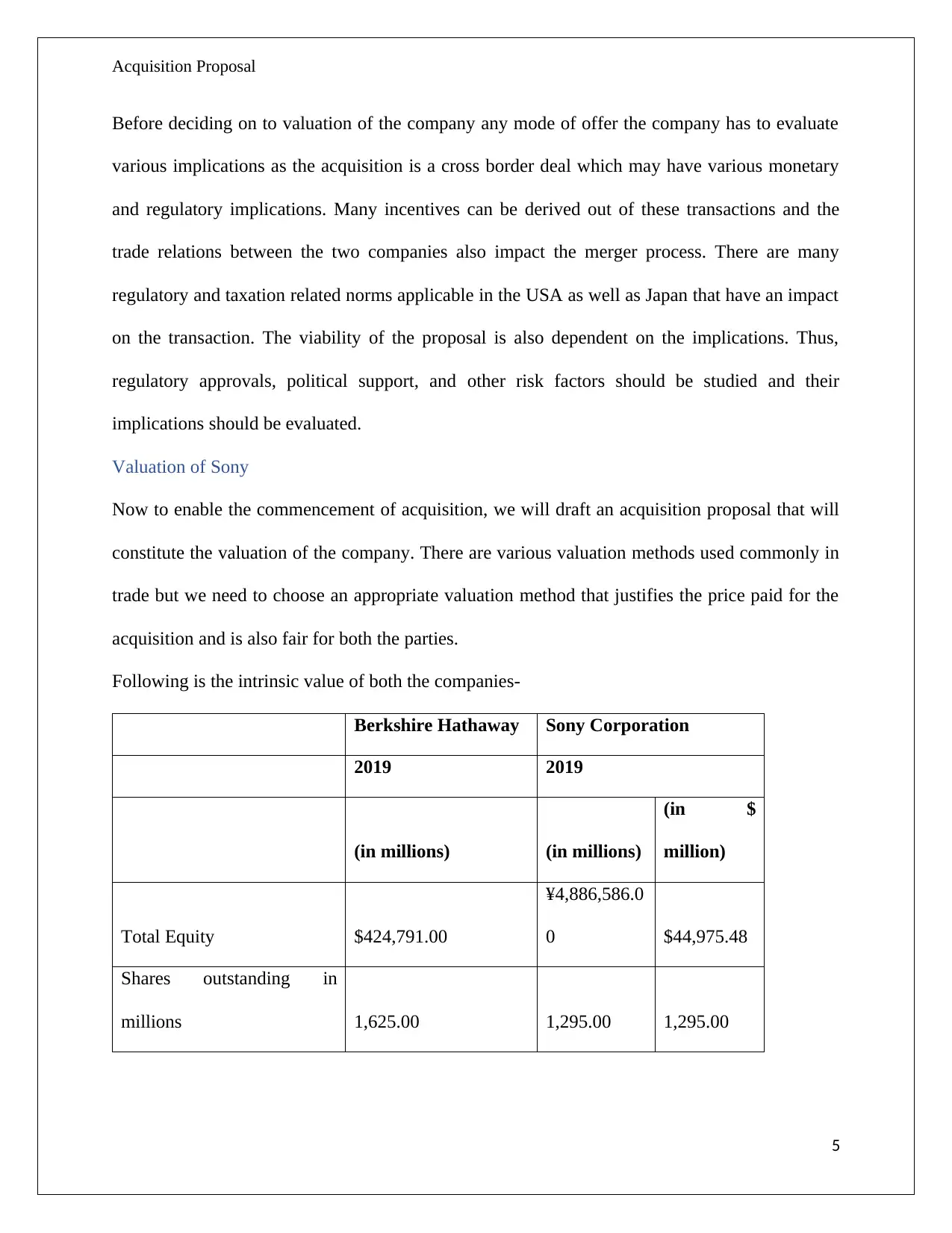

Following is the intrinsic value of both the companies-

Berkshire Hathaway Sony Corporation

2019 2019

(in millions) (in millions)

(in $

million)

Total Equity $424,791.00

¥4,886,586.0

0 $44,975.48

Shares outstanding in

millions 1,625.00 1,295.00 1,295.00

5

Before deciding on to valuation of the company any mode of offer the company has to evaluate

various implications as the acquisition is a cross border deal which may have various monetary

and regulatory implications. Many incentives can be derived out of these transactions and the

trade relations between the two companies also impact the merger process. There are many

regulatory and taxation related norms applicable in the USA as well as Japan that have an impact

on the transaction. The viability of the proposal is also dependent on the implications. Thus,

regulatory approvals, political support, and other risk factors should be studied and their

implications should be evaluated.

Valuation of Sony

Now to enable the commencement of acquisition, we will draft an acquisition proposal that will

constitute the valuation of the company. There are various valuation methods used commonly in

trade but we need to choose an appropriate valuation method that justifies the price paid for the

acquisition and is also fair for both the parties.

Following is the intrinsic value of both the companies-

Berkshire Hathaway Sony Corporation

2019 2019

(in millions) (in millions)

(in $

million)

Total Equity $424,791.00

¥4,886,586.0

0 $44,975.48

Shares outstanding in

millions 1,625.00 1,295.00 1,295.00

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Acquisition Proposal

Equity Outstanding per

share $261,409.85 ¥3,773.43 $34.73

The above data is based on the annual reports of the company as on 31st December,2020. It

shows the intrinsic value per share of both the companies on that date. The Shareholder’s equity

is divided by the number of shares outstanding. For better comparison the data available in

Japanese on the data available in Japanese Yen of Sony corporation has been converted into

USD using the USD to JPY rate as in 31st December 2019.

However if we follow earning based approach of the performance the company as of today, then

Berkshire Hathaway’s intrinsic value would be $826,314 (GuruFocus, 2020) and Sony

Corporation’s intrinsic value would be $74.65 while the stock market price of the company is

only $60 (Guru Focus, 2020). Thus, the acquisition strategy of the company should be based on

the intrinsic value derived out of the free cash flows which shows that the shares of Sony

Corporation are undervaluing in the US.

We can apply the price earning ratio model to value the shares of Sony corporation by Berkshire

Hathaway Inc. This method will ensure that the valuation is done and the price offered takes into

account the current stock market price as well as earning potential of the company. Thus, the

income statement in the financial report and stock market price decided by the market both are

present in the valuation process. The current Price Earning Ratio of Berkshire Hathaway is 18.94

while that of 12.72. The earnings per share of Sony Corporation is ¥182.89 which is $ terms

amounts to $1.68. Thus, the maximum acceptable per-share value of Sony corporation would be

$1.68* 18.94, i.e., $31.881.

6

Equity Outstanding per

share $261,409.85 ¥3,773.43 $34.73

The above data is based on the annual reports of the company as on 31st December,2020. It

shows the intrinsic value per share of both the companies on that date. The Shareholder’s equity

is divided by the number of shares outstanding. For better comparison the data available in

Japanese on the data available in Japanese Yen of Sony corporation has been converted into

USD using the USD to JPY rate as in 31st December 2019.

However if we follow earning based approach of the performance the company as of today, then

Berkshire Hathaway’s intrinsic value would be $826,314 (GuruFocus, 2020) and Sony

Corporation’s intrinsic value would be $74.65 while the stock market price of the company is

only $60 (Guru Focus, 2020). Thus, the acquisition strategy of the company should be based on

the intrinsic value derived out of the free cash flows which shows that the shares of Sony

Corporation are undervaluing in the US.

We can apply the price earning ratio model to value the shares of Sony corporation by Berkshire

Hathaway Inc. This method will ensure that the valuation is done and the price offered takes into

account the current stock market price as well as earning potential of the company. Thus, the

income statement in the financial report and stock market price decided by the market both are

present in the valuation process. The current Price Earning Ratio of Berkshire Hathaway is 18.94

while that of 12.72. The earnings per share of Sony Corporation is ¥182.89 which is $ terms

amounts to $1.68. Thus, the maximum acceptable per-share value of Sony corporation would be

$1.68* 18.94, i.e., $31.881.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Acquisition Proposal

The total number of shares that are currently outstanding in Sony Corporation is 1295 million.

Thus, to acquire Sony, Berkshire has to buy at least 51%, i.e., 660 million shares for which the

consideration to be paid would be $21,055 million.

Now we need to determine whether cash offer should be made by Berkshire Hathaway or a share

offer to acquire the target company.

Since the equity value as per the annual reports of the companies were $424791 million and

$44975 respectively. If the consideration is paid in cash to then the Berkshire’s value will be

increased to $448,711.48.

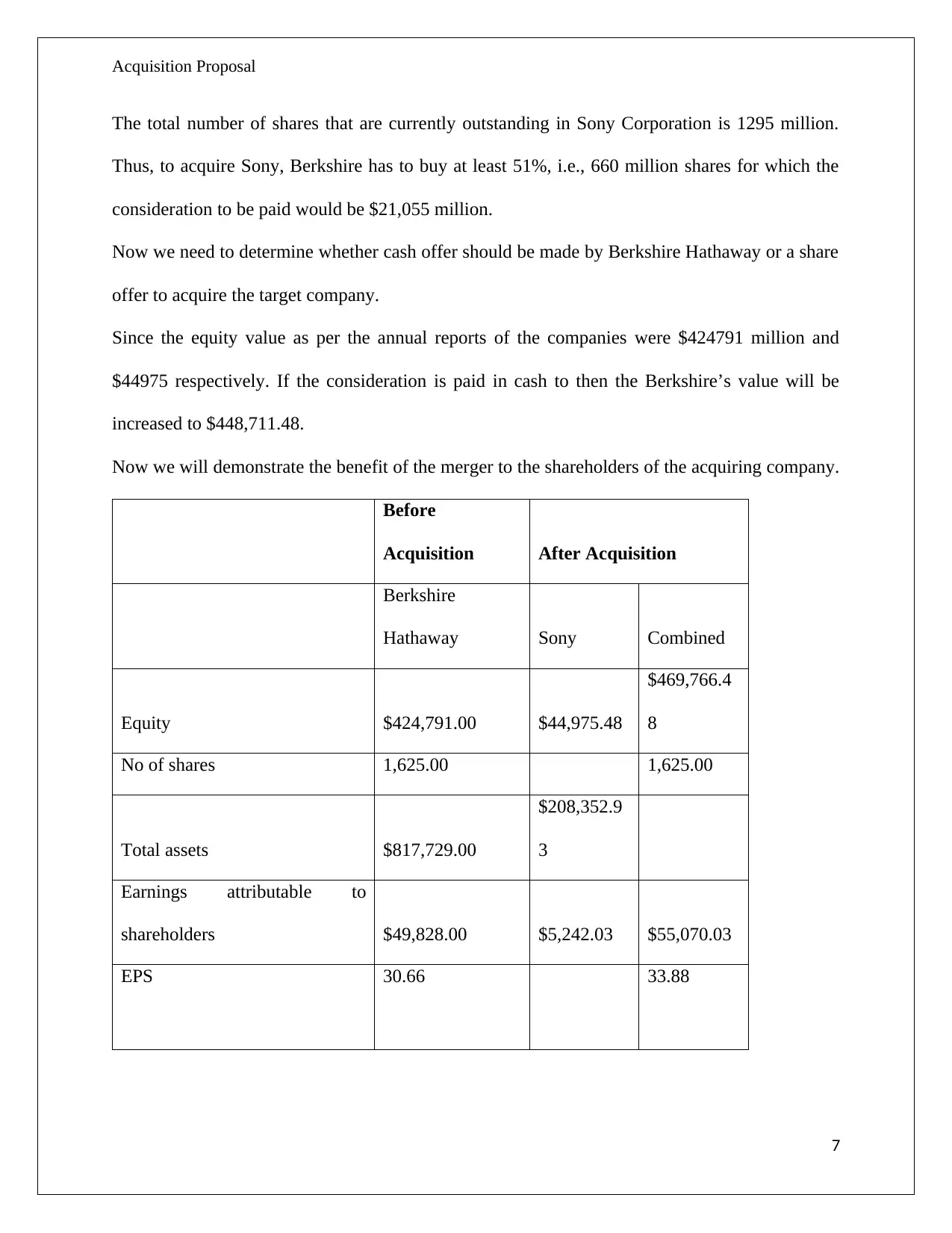

Now we will demonstrate the benefit of the merger to the shareholders of the acquiring company.

Before

Acquisition After Acquisition

Berkshire

Hathaway Sony Combined

Equity $424,791.00 $44,975.48

$469,766.4

8

No of shares 1,625.00 1,625.00

Total assets $817,729.00

$208,352.9

3

Earnings attributable to

shareholders $49,828.00 $5,242.03 $55,070.03

EPS 30.66 33.88

7

The total number of shares that are currently outstanding in Sony Corporation is 1295 million.

Thus, to acquire Sony, Berkshire has to buy at least 51%, i.e., 660 million shares for which the

consideration to be paid would be $21,055 million.

Now we need to determine whether cash offer should be made by Berkshire Hathaway or a share

offer to acquire the target company.

Since the equity value as per the annual reports of the companies were $424791 million and

$44975 respectively. If the consideration is paid in cash to then the Berkshire’s value will be

increased to $448,711.48.

Now we will demonstrate the benefit of the merger to the shareholders of the acquiring company.

Before

Acquisition After Acquisition

Berkshire

Hathaway Sony Combined

Equity $424,791.00 $44,975.48

$469,766.4

8

No of shares 1,625.00 1,625.00

Total assets $817,729.00

$208,352.9

3

Earnings attributable to

shareholders $49,828.00 $5,242.03 $55,070.03

EPS 30.66 33.88

7

Acquisition Proposal

By acquiring Sony corporation, the profit-generating capacity of Berkshire will improve in real

terms and it will also increase the EPS of the shareholders as the profit generated by Sony will

increase Berkshire’s wealth by the percentage of holdings that the company has in Sony (51%).

The portion of earnings attributable to Berkshire Hathaway will ensure the company’s wealth

maximization. Also, the high performing assets and cash flow from sales will improve the cash

richness of Berkshire. However, if the full consideration is paid in cash and not in kind it will

have a major impact on the liquidity of the company. Thus, the cash offer will not dilute the

holding of the shareholders but it will have a major impact on liquidity of the company. The

liquidity crisis will however be recovered as their recovery of the lost surplus when the company

starts to get the cash flows from the acquired company.

Part 2 Personal Reflection

In the previous part of this task, we have analyzed and proposed a merger proposal between

Berkshire Hathaway and Sony Corporation. Both are multinational Conglomerates and they have

strong profitability and market capitalization. Apart from the financial aspects, the merger is a

profitable deal as the acquirer will get the chance to enter into consumer electronics,

entertainment and other segments which were untouched before. The proposal is a cash offer and

will improve the earning capacity of the acquiring company. However, in the process of merger

or an acquisition both the companies may have different valuation approaches which may lead to

conflicting opinions about the target company’s value and the expectations of the shareholders.

Also, in cross border transaction there is ongoing currency fluctuation which may lead to varying

results in the valuation.

8

By acquiring Sony corporation, the profit-generating capacity of Berkshire will improve in real

terms and it will also increase the EPS of the shareholders as the profit generated by Sony will

increase Berkshire’s wealth by the percentage of holdings that the company has in Sony (51%).

The portion of earnings attributable to Berkshire Hathaway will ensure the company’s wealth

maximization. Also, the high performing assets and cash flow from sales will improve the cash

richness of Berkshire. However, if the full consideration is paid in cash and not in kind it will

have a major impact on the liquidity of the company. Thus, the cash offer will not dilute the

holding of the shareholders but it will have a major impact on liquidity of the company. The

liquidity crisis will however be recovered as their recovery of the lost surplus when the company

starts to get the cash flows from the acquired company.

Part 2 Personal Reflection

In the previous part of this task, we have analyzed and proposed a merger proposal between

Berkshire Hathaway and Sony Corporation. Both are multinational Conglomerates and they have

strong profitability and market capitalization. Apart from the financial aspects, the merger is a

profitable deal as the acquirer will get the chance to enter into consumer electronics,

entertainment and other segments which were untouched before. The proposal is a cash offer and

will improve the earning capacity of the acquiring company. However, in the process of merger

or an acquisition both the companies may have different valuation approaches which may lead to

conflicting opinions about the target company’s value and the expectations of the shareholders.

Also, in cross border transaction there is ongoing currency fluctuation which may lead to varying

results in the valuation.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Acquisition Proposal

However, there are many factors which may lead to failure of this proposal and the deal might

not materialize despite being viable for both the parties. There can be several reasons for the

failure of a merger deals some of which can internal and some can be external causes which are

not in the hands of any of the organization. In some cases, there can be factors that might come

up which were not forecasted earlier by the company. There were many deals in the corporate

world which could not be materialized despite being well-drafted and has wide media coverage.

Common reasons for the failure of a merger can be the misleading value of an investment, poor

communication between the parties, cultural gap between the two parties, disagreement during

the negotiation that becomes a deadlock eventually, different strategies of the two businesses and

different corporate goals.

In this essay, we will study how a poor valuation can lead to the failing of the merger deal.

Valuation is the most integral part and essence of a merger. The target company will accept the

proposal only when the deals are profitable enough. A company which is already in profits and

had flourished in the global market like our target company in task 1, i.e., Sony there is a high

chance that the company will expect a premium price for the locking in the deal. Synergies are

the technical know-how that one company gains from others through a merger. It can be in the

form of research, abilities of the manpower and other intellectual properties that the target posses

and will benefit the acquirer. The valuation of these benefits and the premium paid by the

acquiring company may be different from what the target company is expecting. Sony has some

world-class technology for various products that it sells. Being a technical giant, the company

will expect a high premium price from the acquiring company. If the acquirer does not value the

target company’s synergies that it will derive as much as the target company does the merger

may fail. Thus, Berkshire should verify whether the proposed amount sufficiently justifies the

9

However, there are many factors which may lead to failure of this proposal and the deal might

not materialize despite being viable for both the parties. There can be several reasons for the

failure of a merger deals some of which can internal and some can be external causes which are

not in the hands of any of the organization. In some cases, there can be factors that might come

up which were not forecasted earlier by the company. There were many deals in the corporate

world which could not be materialized despite being well-drafted and has wide media coverage.

Common reasons for the failure of a merger can be the misleading value of an investment, poor

communication between the parties, cultural gap between the two parties, disagreement during

the negotiation that becomes a deadlock eventually, different strategies of the two businesses and

different corporate goals.

In this essay, we will study how a poor valuation can lead to the failing of the merger deal.

Valuation is the most integral part and essence of a merger. The target company will accept the

proposal only when the deals are profitable enough. A company which is already in profits and

had flourished in the global market like our target company in task 1, i.e., Sony there is a high

chance that the company will expect a premium price for the locking in the deal. Synergies are

the technical know-how that one company gains from others through a merger. It can be in the

form of research, abilities of the manpower and other intellectual properties that the target posses

and will benefit the acquirer. The valuation of these benefits and the premium paid by the

acquiring company may be different from what the target company is expecting. Sony has some

world-class technology for various products that it sells. Being a technical giant, the company

will expect a high premium price from the acquiring company. If the acquirer does not value the

target company’s synergies that it will derive as much as the target company does the merger

may fail. Thus, Berkshire should verify whether the proposed amount sufficiently justifies the

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Acquisition Proposal

technical know-how and synergies it will gain by the acquisition of Sony Corporation (Business

Matters, 2013).

The merger is a lengthy and time-consuming process. The market conditions may change and the

events happening in between when the merger is in pipeline might have a vital impact on the

numbers that are used in the merger. The decision of acquisition is taken looking at some

benefits and synergies that will benefit the acquiring company without putting in many efforts.

However, there can be some market condition that might change before the conclusion of a

merger and make it unviable. In this case, the valuation done becomes impractical and not

beneficial to one or both the parties. For example, the corona outbreak has hampered global

economy and it must have failed many of the merger proposals that were in pipeline. This can be

also possible in a positive way where the market conditions of the target company might improve

due to an event and the valuation of the company done by the acquirer may fall short of what it

will expect when the condition becomes favorable for the target company. In such cases a deal

can be saved only when the valuation is revised and the target company as well as acquiring

company is ready to seal the deal at the revised price.

At times when a statute requires consent of the shareholders before finalizing a merger, the

shareholders might have objection with the valuation or the mode of disbursement of such value.

When share offer is made by a company there can be objection among the shareholders as such

offer will dilute their control and voting power in the company. Also, the shareholders may not

agree to the value being paid and might be getting higher bidding from another party. In such

cases there can be a deadlock and merger may fail if the shareholders do not pass the required

resolution as they do not agree with the valuation and price that is offered. The stock price of the

10

technical know-how and synergies it will gain by the acquisition of Sony Corporation (Business

Matters, 2013).

The merger is a lengthy and time-consuming process. The market conditions may change and the

events happening in between when the merger is in pipeline might have a vital impact on the

numbers that are used in the merger. The decision of acquisition is taken looking at some

benefits and synergies that will benefit the acquiring company without putting in many efforts.

However, there can be some market condition that might change before the conclusion of a

merger and make it unviable. In this case, the valuation done becomes impractical and not

beneficial to one or both the parties. For example, the corona outbreak has hampered global

economy and it must have failed many of the merger proposals that were in pipeline. This can be

also possible in a positive way where the market conditions of the target company might improve

due to an event and the valuation of the company done by the acquirer may fall short of what it

will expect when the condition becomes favorable for the target company. In such cases a deal

can be saved only when the valuation is revised and the target company as well as acquiring

company is ready to seal the deal at the revised price.

At times when a statute requires consent of the shareholders before finalizing a merger, the

shareholders might have objection with the valuation or the mode of disbursement of such value.

When share offer is made by a company there can be objection among the shareholders as such

offer will dilute their control and voting power in the company. Also, the shareholders may not

agree to the value being paid and might be getting higher bidding from another party. In such

cases there can be a deadlock and merger may fail if the shareholders do not pass the required

resolution as they do not agree with the valuation and price that is offered. The stock price of the

10

Acquisition Proposal

target company sees high fluctuations during a merger which may also result in opposing a

merger (Bloomenthal, 2020).

Valuation is considered as a key to implement a smooth and successful merger. If the valuation

is not done diligently and the acquisition deal gets locked it there are high chances that the

collaboration will fail in future. The valuation model used should be selected carefully and

results derived by applying different methods should be derived and compared with each other

before finalizing an offer price. The result gained by applying a method of valuation should be

compared and modified to give the effect of the non-monetary factors.

The value derived by the acquirer should be compared with other companies that belong to the

same industry as that of target company. Comparison method will enable the valuation team to

find out plus points of the company over its competitors and what it lacks. This will give realistic

figures which the target company will also expect on the basis of self-evaluation. When the

valuation models are complicated, communication is the key to gain the trust of shareholders and

management of the target company. The valuation proposal should be carefully drafted and must

include all the key aspects that may impact the important features that led to the value which is

being offered. The gain that will flow to the target company’s shareholders should be

demonstrated and over what period and in which form the benefits will be derived should also be

explained to the shareholders through the proposal of acquisition. Thus, if the target company’s

shareholders are satisfied with the future benefits and consideration of acquisition the valuation

will never result into the failure of merger deal.

11

target company sees high fluctuations during a merger which may also result in opposing a

merger (Bloomenthal, 2020).

Valuation is considered as a key to implement a smooth and successful merger. If the valuation

is not done diligently and the acquisition deal gets locked it there are high chances that the

collaboration will fail in future. The valuation model used should be selected carefully and

results derived by applying different methods should be derived and compared with each other

before finalizing an offer price. The result gained by applying a method of valuation should be

compared and modified to give the effect of the non-monetary factors.

The value derived by the acquirer should be compared with other companies that belong to the

same industry as that of target company. Comparison method will enable the valuation team to

find out plus points of the company over its competitors and what it lacks. This will give realistic

figures which the target company will also expect on the basis of self-evaluation. When the

valuation models are complicated, communication is the key to gain the trust of shareholders and

management of the target company. The valuation proposal should be carefully drafted and must

include all the key aspects that may impact the important features that led to the value which is

being offered. The gain that will flow to the target company’s shareholders should be

demonstrated and over what period and in which form the benefits will be derived should also be

explained to the shareholders through the proposal of acquisition. Thus, if the target company’s

shareholders are satisfied with the future benefits and consideration of acquisition the valuation

will never result into the failure of merger deal.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.