Financial Analysis of Bertie PLC and Hill Ranch Project Investment

VerifiedAdded on 2019/12/03

|13

|3425

|120

Report

AI Summary

This report presents a comprehensive analysis of Bertie PLC's financial performance, encompassing its operations in the UK and US markets. The report delves into the interpretation of profitability statements, market segment analysis, and the statement of cash flow to assess the company's financial health. Key areas examined include liquidity, working capital, and solvency, providing insights into Bertie PLC's ability to meet its financial obligations. Furthermore, the report evaluates the viability of the Hill Ranch project through various investment appraisal techniques, such as payback period, accounting rate of return, and net present value. The analysis reveals declining operational performance due to factors like lower gross margin and net margin, while also highlighting the challenges faced in the US market. The report concludes with recommendations for improving financial performance and making informed investment decisions.

ACCOUNTING &

DECISION

MAKING

BERTIE

24 FEB 2016

DECISION

MAKING

BERTIE

24 FEB 2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING &

DECISION

MAKING

2 | P a g e

DECISION

MAKING

2 | P a g e

Table of Contents

Executive summary....................................................................................................................1

BUSINESS REPORT:......................................................................................................1

Part 1 .........................................................................................................................................1

Interpretation of the profitability statement......................................................................1

Market Segment Analysis.................................................................................................3

Statement of Cash Flow ..................................................................................................4

Liquidity and working capital:..........................................................................................4

Solvency............................................................................................................................5

PART 2 ......................................................................................................................................6

Investment appraisal ........................................................................................................6

Sources of internal finance................................................................................................7

REFERENCES...........................................................................................................................9

3 | P a g e

Executive summary....................................................................................................................1

BUSINESS REPORT:......................................................................................................1

Part 1 .........................................................................................................................................1

Interpretation of the profitability statement......................................................................1

Market Segment Analysis.................................................................................................3

Statement of Cash Flow ..................................................................................................4

Liquidity and working capital:..........................................................................................4

Solvency............................................................................................................................5

PART 2 ......................................................................................................................................6

Investment appraisal ........................................................................................................6

Sources of internal finance................................................................................................7

REFERENCES...........................................................................................................................9

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EXECUTIVE SUMMARY

Bertie plc is a global retail company, established in the UK in 1945 selling food and

groceries and operates in Europe, Asia and the US. The present project report will help us to

determine company's performance analysis in UK and US. In addition to it, Bertie Plc

considered to invest funds in Hill Ranch project of £10m. Henceforth, different investment

appraisals techniques such as pay back period, accounting rate of return and net present value

have been used to determine assess viability of its Hill Ranch project.

BUSINESS REPORT:

Financial performance analysis reported that Bertie Plc operational performance is

declined because of lower GM and NM. Declined sales, throat cut competition, price

instability, market uncertainties are the reason behind it. Moreover, Bertie Plc liquidity and

solvency position is also decreased due to high debts that contribute to higher the risk. On

contrary, extended creditors payment terms and reduce the inventory holding period implied

more cash availability for Bertie Plc. In addition to it, inventory appraisal method suggested

that Bertie Plc should make investment in Hill Ranch project because it posses positive NPV

of 6915000£. In addition to it, US Market segment analysis indicated that its performance is

not as good as other segment performance. The reason behind this is it is new market

segment, facing competition from Walmart and incurred operating losses.

PART 1

Interpretation of the profitability statement

Revenue: In 2015, Bertie plc improved its overall sales by only 1.424%. The

possible reason for such increase is company starts online sales delivery resulted in high

customer demand and growth in sales as well. However, in UK, it dropped by 1.49% because

UK is highly competitive market for retail industry. Fierce level of competition, price war,

price sensitive customers and recession are the reason for declined sales. On contrary, in US

market, it is significantly increased by 111.63% which contributed to enhance overall Bertie

plc performance.

1 | P a g e

Bertie plc is a global retail company, established in the UK in 1945 selling food and

groceries and operates in Europe, Asia and the US. The present project report will help us to

determine company's performance analysis in UK and US. In addition to it, Bertie Plc

considered to invest funds in Hill Ranch project of £10m. Henceforth, different investment

appraisals techniques such as pay back period, accounting rate of return and net present value

have been used to determine assess viability of its Hill Ranch project.

BUSINESS REPORT:

Financial performance analysis reported that Bertie Plc operational performance is

declined because of lower GM and NM. Declined sales, throat cut competition, price

instability, market uncertainties are the reason behind it. Moreover, Bertie Plc liquidity and

solvency position is also decreased due to high debts that contribute to higher the risk. On

contrary, extended creditors payment terms and reduce the inventory holding period implied

more cash availability for Bertie Plc. In addition to it, inventory appraisal method suggested

that Bertie Plc should make investment in Hill Ranch project because it posses positive NPV

of 6915000£. In addition to it, US Market segment analysis indicated that its performance is

not as good as other segment performance. The reason behind this is it is new market

segment, facing competition from Walmart and incurred operating losses.

PART 1

Interpretation of the profitability statement

Revenue: In 2015, Bertie plc improved its overall sales by only 1.424%. The

possible reason for such increase is company starts online sales delivery resulted in high

customer demand and growth in sales as well. However, in UK, it dropped by 1.49% because

UK is highly competitive market for retail industry. Fierce level of competition, price war,

price sensitive customers and recession are the reason for declined sales. On contrary, in US

market, it is significantly increased by 111.63% which contributed to enhance overall Bertie

plc performance.

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of sales: In 2015, Bertie Plc cost of sales has been raised by 3.79% while in UK;

it got increased by 10.3%. It is higher in UK market because of high prices for raw material

and fuel. Food prices got increased by 10% whilst high oil and fuel prices impose high

transportation cost to bertie plc. Thus, it became clear that cost got increased due to market

changes hence, out of company's control.

Overheads: Bertie plc administrative cost has been increased by 13.02% in 2015.

High employee's salaries, hiring more staff and increased other expenses such as rent may be

the reason for extra administration cost and affects Bertie plc profits negatively. These

expenses are under control of the company so bertie plc should pay focus on reducing their

administrative expenses.

Finance cost: Bertie plc finance cost got inclined from 279£ to 687£. Henceforth, it

has been increased by 146% arisen because of using high long term borrowings to invest in

Hill Ranch.

Profitability analysis

Gross profit ratio: Bertie plc GM got declined from 8.44% to 6.31% by 2.13%

which is bad. The reason behind this is revenue growth is slightly lower than cost increases.

This in turn, Bertie plc GP got dropped by 24.23% in 2015. Political instability, unfavourable

market conditions, price sensitive customers and throat cut competition are the reason for it.

Net profit ratio: NM got declined from 6.75% to 4.08% by 2.67% in 2015. It

indicates worst operational performance and decreasing the operating incomes by 60.26%

and rising in company's overheads are the reasons for lower profits. This in turn, net profit

2 | P a g e

UK US Total revenue

0

10000

20000

30000

40000

50000

60000

70000

47632

1392

63916

46918

2946

64826

it got increased by 10.3%. It is higher in UK market because of high prices for raw material

and fuel. Food prices got increased by 10% whilst high oil and fuel prices impose high

transportation cost to bertie plc. Thus, it became clear that cost got increased due to market

changes hence, out of company's control.

Overheads: Bertie plc administrative cost has been increased by 13.02% in 2015.

High employee's salaries, hiring more staff and increased other expenses such as rent may be

the reason for extra administration cost and affects Bertie plc profits negatively. These

expenses are under control of the company so bertie plc should pay focus on reducing their

administrative expenses.

Finance cost: Bertie plc finance cost got inclined from 279£ to 687£. Henceforth, it

has been increased by 146% arisen because of using high long term borrowings to invest in

Hill Ranch.

Profitability analysis

Gross profit ratio: Bertie plc GM got declined from 8.44% to 6.31% by 2.13%

which is bad. The reason behind this is revenue growth is slightly lower than cost increases.

This in turn, Bertie plc GP got dropped by 24.23% in 2015. Political instability, unfavourable

market conditions, price sensitive customers and throat cut competition are the reason for it.

Net profit ratio: NM got declined from 6.75% to 4.08% by 2.67% in 2015. It

indicates worst operational performance and decreasing the operating incomes by 60.26%

and rising in company's overheads are the reasons for lower profits. This in turn, net profit

2 | P a g e

UK US Total revenue

0

10000

20000

30000

40000

50000

60000

70000

47632

1392

63916

46918

2946

64826

got declined by 38.68%. Therefore, it considered advisable that Bertie plc should make huge

efforts for increasing its sales and maintain effective control over the cost (Suto, Clare, and

Holland, 2007).

Operating profit ratio: In 2015, 38.68% declined in OP indicate poor management.

High administrative cost and lowering operating incomes by 60.26% are the reasons for this.

ROCE: Lower revenue growth and high administration and operating cost resulted in

decreased ROCE from 14.84% to 7.06% in 2015 which is bad. Another reason for such

decreases is company took high amount of borrowings which impose high finance cost.

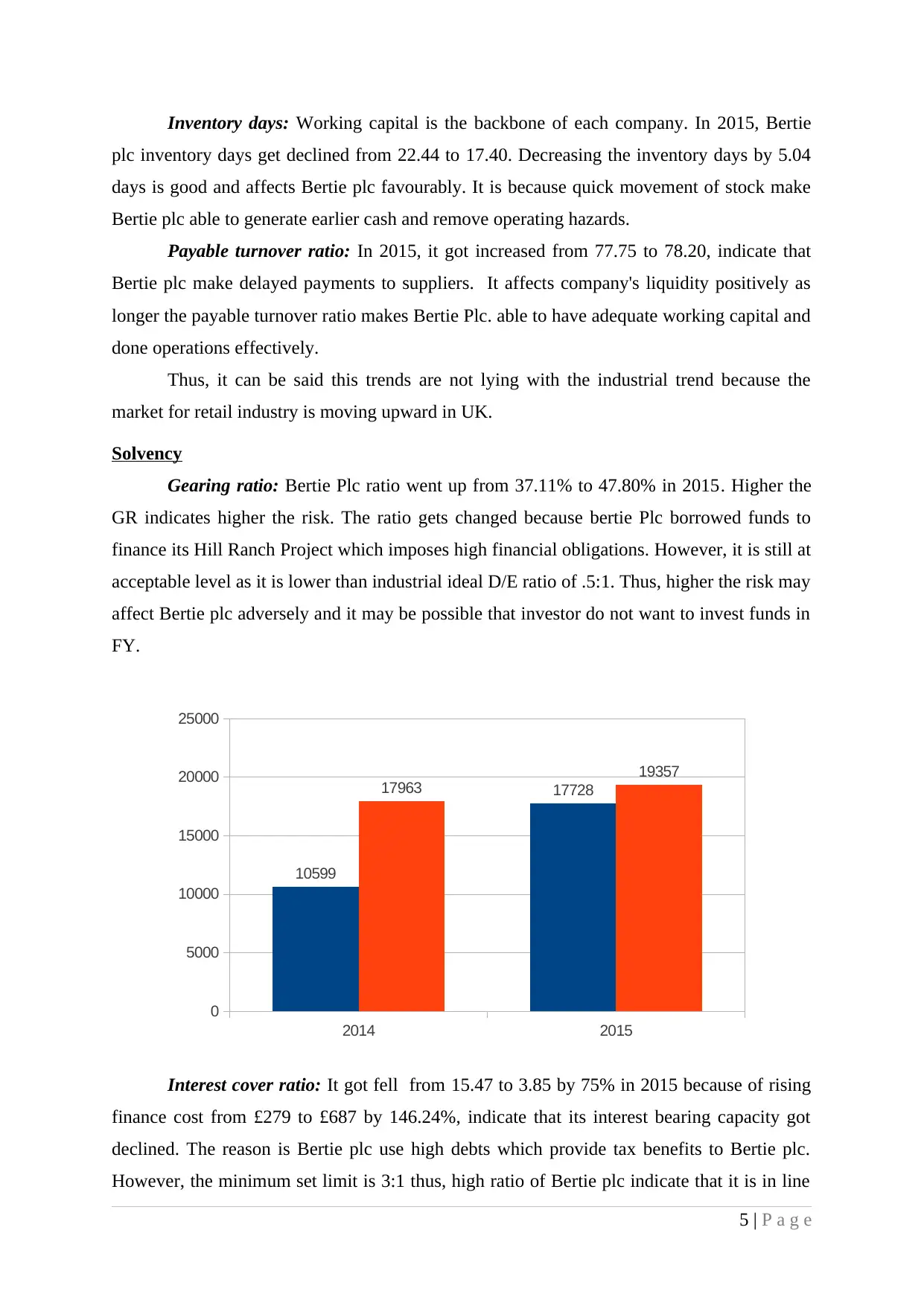

Market Segment Analysis

The financial performance of US segment is not as good as other segments

performance.

US is a newly opened market segment although its revenue got improved by 111.63%

higher than overall revenue increases of 1.424%. It is because UK is mature market for retail

sectors. However, its cost got enhanced by 110.83% very high than overall cost increases of

3.79% in turn; GM got improved from 3.16% to 3.53% by 0.37% while Bertie Plc GM got

dropped by 2.3%. Another, its expenses got improved by 98.02% whilst Bertie plc overall

expenses got increased by only 33.51%. It is because of hiring staff, paying rent, purchasing

office equipment, more advertisement and marketing expenditures to make public awareness

about its offered services. Thus, huge increase in cost of sales and operating expenses

negatively impact the company's operations. US segment is incurring NL from its operating

activities indicate worst performance. Moreover, its OL got inclined by 82.40% while overall

OP got reduced by 38.68%. It indicates poor performance of US market segment. In addition

to it, property, plant and equipment expense got increased by 455.99% whilst total expenses

was increased by 29.06% only. Thus, huge investment in fixed assets do not contributed to

enhance its revenue urgently. Another, the difference between TA and CL got inclined by

426.77% because of expansion. However, Bertie plc overall difference got enhanced by

28.67%.

In context to competition in US, Walmart is the leading supermarket chain generates

more than 50% of the revenue. It is regularly decreasing its food prices to grab large market

share bring some difficulties for Bertie Plc US segment.

Three reasons:

Newly opened market hence, required high operating cost.

Operating loss incurred because of ineffective and unskilled management.

Competition from WalMart as a leading retail company.

3 | P a g e

efforts for increasing its sales and maintain effective control over the cost (Suto, Clare, and

Holland, 2007).

Operating profit ratio: In 2015, 38.68% declined in OP indicate poor management.

High administrative cost and lowering operating incomes by 60.26% are the reasons for this.

ROCE: Lower revenue growth and high administration and operating cost resulted in

decreased ROCE from 14.84% to 7.06% in 2015 which is bad. Another reason for such

decreases is company took high amount of borrowings which impose high finance cost.

Market Segment Analysis

The financial performance of US segment is not as good as other segments

performance.

US is a newly opened market segment although its revenue got improved by 111.63%

higher than overall revenue increases of 1.424%. It is because UK is mature market for retail

sectors. However, its cost got enhanced by 110.83% very high than overall cost increases of

3.79% in turn; GM got improved from 3.16% to 3.53% by 0.37% while Bertie Plc GM got

dropped by 2.3%. Another, its expenses got improved by 98.02% whilst Bertie plc overall

expenses got increased by only 33.51%. It is because of hiring staff, paying rent, purchasing

office equipment, more advertisement and marketing expenditures to make public awareness

about its offered services. Thus, huge increase in cost of sales and operating expenses

negatively impact the company's operations. US segment is incurring NL from its operating

activities indicate worst performance. Moreover, its OL got inclined by 82.40% while overall

OP got reduced by 38.68%. It indicates poor performance of US market segment. In addition

to it, property, plant and equipment expense got increased by 455.99% whilst total expenses

was increased by 29.06% only. Thus, huge investment in fixed assets do not contributed to

enhance its revenue urgently. Another, the difference between TA and CL got inclined by

426.77% because of expansion. However, Bertie plc overall difference got enhanced by

28.67%.

In context to competition in US, Walmart is the leading supermarket chain generates

more than 50% of the revenue. It is regularly decreasing its food prices to grab large market

share bring some difficulties for Bertie Plc US segment.

Three reasons:

Newly opened market hence, required high operating cost.

Operating loss incurred because of ineffective and unskilled management.

Competition from WalMart as a leading retail company.

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Statement of Cash Flow

Bertie plc profitability statement reported 1.96£ million of profit before tax payments

whilst its SOCF reported that Bertie Plc NCF got dropped from 1572£ to (142£) in 2015.

As per SOCF, operating activities indicated the CF increased from 3579£ to 3910£

hence, shows a little bit increases. The reason includes decrease in inventories, delayed

receipts from trade receivables and higher payment to trade payables (Cesarini and et. al.,

2010). Moreover, high interest payment has been arisen due to excessive borrowings. On

contrary, its total interest and income tax obligations have been reduced to 936£ and 693£

respectively. Moreover, depreciation of 2046£ increase Bertie plc cash flows. However,

investing activities comprises acquisition and dispose of Bertie plc fixed assets such as

property, plant and equipment. Investing operations showed that Bertie Plc made high cash

payment for acquiring fixed assets such as property, plant and equipment amounted to

12786£ for investing in Hill Ranch. However, sales proceeds are only for 875£. This in turn,

negative CF got enhanced to 11911£. On contrary, financing activity showed that Bertie Plc

generated funds through borrowings of 7129£ and share capital of 1000£ for Hill Ranch

project. However, repayment of loan was only amounted to 270£. It improve cash inflows

from (201£) to 7859£. Although, ending cash balance indicated adverse balance of 142£.

Thus, it can be said that Bertie Plc do not have cash available to run the operations and cause

operational difficulties. Thus, it will be advised that manager's have to find alternative

sources to support its daily functions so that Bertie plc can operate efficiently and without

any operational hazards.

Liquidity and working capital:

Current ratio: The current ratio of the Bertie Plc is decreased from 0.46 to 0.39 it is

not in line with the industrial trends because the industrial idle CR is 2:1. It results in

decreasing the credit worthiness of the company to pay its short term obligations. Moreover,

no working capital is not available to the company for operations. Although, as large retail

organizations, suppliers provided credit to Bertie plc without any problems. However,

companies maintain their receivables through getting prompt payments. In this year,

receivable days got reduced to 1.10 days (197/64826*365) from 1.35 days (237/63916*365).

Quick Ratio: Bertie plc QR get fell from 0.19 to 0.18 hence, It will decrease Bertie

Plc ability to discharge its short term obligations. Moreover, it is lower than industrial idle

ratio of 1:1, thus, it is not inline with the industry standard. The possible reason may be that

company sold its some of the inventories to pay off its obligations.

4 | P a g e

Bertie plc profitability statement reported 1.96£ million of profit before tax payments

whilst its SOCF reported that Bertie Plc NCF got dropped from 1572£ to (142£) in 2015.

As per SOCF, operating activities indicated the CF increased from 3579£ to 3910£

hence, shows a little bit increases. The reason includes decrease in inventories, delayed

receipts from trade receivables and higher payment to trade payables (Cesarini and et. al.,

2010). Moreover, high interest payment has been arisen due to excessive borrowings. On

contrary, its total interest and income tax obligations have been reduced to 936£ and 693£

respectively. Moreover, depreciation of 2046£ increase Bertie plc cash flows. However,

investing activities comprises acquisition and dispose of Bertie plc fixed assets such as

property, plant and equipment. Investing operations showed that Bertie Plc made high cash

payment for acquiring fixed assets such as property, plant and equipment amounted to

12786£ for investing in Hill Ranch. However, sales proceeds are only for 875£. This in turn,

negative CF got enhanced to 11911£. On contrary, financing activity showed that Bertie Plc

generated funds through borrowings of 7129£ and share capital of 1000£ for Hill Ranch

project. However, repayment of loan was only amounted to 270£. It improve cash inflows

from (201£) to 7859£. Although, ending cash balance indicated adverse balance of 142£.

Thus, it can be said that Bertie Plc do not have cash available to run the operations and cause

operational difficulties. Thus, it will be advised that manager's have to find alternative

sources to support its daily functions so that Bertie plc can operate efficiently and without

any operational hazards.

Liquidity and working capital:

Current ratio: The current ratio of the Bertie Plc is decreased from 0.46 to 0.39 it is

not in line with the industrial trends because the industrial idle CR is 2:1. It results in

decreasing the credit worthiness of the company to pay its short term obligations. Moreover,

no working capital is not available to the company for operations. Although, as large retail

organizations, suppliers provided credit to Bertie plc without any problems. However,

companies maintain their receivables through getting prompt payments. In this year,

receivable days got reduced to 1.10 days (197/64826*365) from 1.35 days (237/63916*365).

Quick Ratio: Bertie plc QR get fell from 0.19 to 0.18 hence, It will decrease Bertie

Plc ability to discharge its short term obligations. Moreover, it is lower than industrial idle

ratio of 1:1, thus, it is not inline with the industry standard. The possible reason may be that

company sold its some of the inventories to pay off its obligations.

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory days: Working capital is the backbone of each company. In 2015, Bertie

plc inventory days get declined from 22.44 to 17.40. Decreasing the inventory days by 5.04

days is good and affects Bertie plc favourably. It is because quick movement of stock make

Bertie plc able to generate earlier cash and remove operating hazards.

Payable turnover ratio: In 2015, it got increased from 77.75 to 78.20, indicate that

Bertie plc make delayed payments to suppliers. It affects company's liquidity positively as

longer the payable turnover ratio makes Bertie Plc. able to have adequate working capital and

done operations effectively.

Thus, it can be said this trends are not lying with the industrial trend because the

market for retail industry is moving upward in UK.

Solvency

Gearing ratio: Bertie Plc ratio went up from 37.11% to 47.80% in 2015. Higher the

GR indicates higher the risk. The ratio gets changed because bertie Plc borrowed funds to

finance its Hill Ranch Project which imposes high financial obligations. However, it is still at

acceptable level as it is lower than industrial ideal D/E ratio of .5:1. Thus, higher the risk may

affect Bertie plc adversely and it may be possible that investor do not want to invest funds in

FY.

Interest cover ratio: It got fell from 15.47 to 3.85 by 75% in 2015 because of rising

finance cost from £279 to £687 by 146.24%, indicate that its interest bearing capacity got

declined. The reason is Bertie plc use high debts which provide tax benefits to Bertie plc.

However, the minimum set limit is 3:1 thus, high ratio of Bertie plc indicate that it is in line

5 | P a g e

2014 2015

0

5000

10000

15000

20000

25000

10599

1772817963

19357

plc inventory days get declined from 22.44 to 17.40. Decreasing the inventory days by 5.04

days is good and affects Bertie plc favourably. It is because quick movement of stock make

Bertie plc able to generate earlier cash and remove operating hazards.

Payable turnover ratio: In 2015, it got increased from 77.75 to 78.20, indicate that

Bertie plc make delayed payments to suppliers. It affects company's liquidity positively as

longer the payable turnover ratio makes Bertie Plc. able to have adequate working capital and

done operations effectively.

Thus, it can be said this trends are not lying with the industrial trend because the

market for retail industry is moving upward in UK.

Solvency

Gearing ratio: Bertie Plc ratio went up from 37.11% to 47.80% in 2015. Higher the

GR indicates higher the risk. The ratio gets changed because bertie Plc borrowed funds to

finance its Hill Ranch Project which imposes high financial obligations. However, it is still at

acceptable level as it is lower than industrial ideal D/E ratio of .5:1. Thus, higher the risk may

affect Bertie plc adversely and it may be possible that investor do not want to invest funds in

FY.

Interest cover ratio: It got fell from 15.47 to 3.85 by 75% in 2015 because of rising

finance cost from £279 to £687 by 146.24%, indicate that its interest bearing capacity got

declined. The reason is Bertie plc use high debts which provide tax benefits to Bertie plc.

However, the minimum set limit is 3:1 thus, high ratio of Bertie plc indicate that it is in line

5 | P a g e

2014 2015

0

5000

10000

15000

20000

25000

10599

1772817963

19357

with the industrial trend. The ratio implies that company is still able to make timely interest

payments to lenders.

PART 2

Investment appraisal

Management Forecast: Bertie Plc management forecasted the initial required

investment of £10m while net cash flow (NCF) has been estimated through determining the

difference between total revenues and variable costs. The benefit is that it shows an inclining

trend as it got increased from £300 to £11345. It makes Bertie plc managers able to predict

the future return on the investment proposal. The limitation is this are only the estimated

figures and actual cash flows may be different from this prediction. What may get happen in

FY is uncertain and cannot be decided. It may fall or decrease due to market uncertainties

such as changing the competition level, customer demand, inflation rates, taxation rates, food

prices, unstable political situations and others. Thus, it cannot be said that estimated cash

flows will be incur in FY.

Pay back period: Bertie Plc uses this method to determine the required time period of

Hill Ranch project to recover the initial investment of £10m. Hill Ranch investment takes 7

year 10 months to get its initial investment of £10m. The benefit is that through using this

technique, Bertie plc will be able to identify the recovery period of project, very easy to

compute and can be used for comparison. The limitation is it ignores time value and post pay

back profitability. However, it may be possible that an investment proposal that have longer

pay back period but provide high post pay back profitability seems to be more beneficial for

the company. For example, due to inflationary pressure, prices got increase by some

percentage than it will contribute to decrease food demand and affect sales revenues. Thus,

lower the sales revenues will reduce NCF this in turn, PP will be increased. However, if

actual cash flows became higher than projected NCF than PP will be reduced. Thus, it can be

concluded that it is not an appropriate tool for taking effective capital decisions.

Accounting rate of return: It can be calculated by dividing the average profits to the

initial investment. Bertie plc decided target ARR of 50% while Hill Ranch project provides

52% ARR. High project ARR indicated that Bertie Plc should invest funds in this project

because it provides high return than targeted ARR. The benefit of ARR is that it provides an

idea about the future profit percentages which can be generated on Hill Ranch investment. It

is quicker and easier method and provide information about the project return. Henceforth, it

6 | P a g e

payments to lenders.

PART 2

Investment appraisal

Management Forecast: Bertie Plc management forecasted the initial required

investment of £10m while net cash flow (NCF) has been estimated through determining the

difference between total revenues and variable costs. The benefit is that it shows an inclining

trend as it got increased from £300 to £11345. It makes Bertie plc managers able to predict

the future return on the investment proposal. The limitation is this are only the estimated

figures and actual cash flows may be different from this prediction. What may get happen in

FY is uncertain and cannot be decided. It may fall or decrease due to market uncertainties

such as changing the competition level, customer demand, inflation rates, taxation rates, food

prices, unstable political situations and others. Thus, it cannot be said that estimated cash

flows will be incur in FY.

Pay back period: Bertie Plc uses this method to determine the required time period of

Hill Ranch project to recover the initial investment of £10m. Hill Ranch investment takes 7

year 10 months to get its initial investment of £10m. The benefit is that through using this

technique, Bertie plc will be able to identify the recovery period of project, very easy to

compute and can be used for comparison. The limitation is it ignores time value and post pay

back profitability. However, it may be possible that an investment proposal that have longer

pay back period but provide high post pay back profitability seems to be more beneficial for

the company. For example, due to inflationary pressure, prices got increase by some

percentage than it will contribute to decrease food demand and affect sales revenues. Thus,

lower the sales revenues will reduce NCF this in turn, PP will be increased. However, if

actual cash flows became higher than projected NCF than PP will be reduced. Thus, it can be

concluded that it is not an appropriate tool for taking effective capital decisions.

Accounting rate of return: It can be calculated by dividing the average profits to the

initial investment. Bertie plc decided target ARR of 50% while Hill Ranch project provides

52% ARR. High project ARR indicated that Bertie Plc should invest funds in this project

because it provides high return than targeted ARR. The benefit of ARR is that it provides an

idea about the future profit percentages which can be generated on Hill Ranch investment. It

is quicker and easier method and provide information about the project return. Henceforth, it

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

can be used for satisfying shareholder's expectations. Limitation is ARR consider the profits

rather than cash flows. Hence, it not consider the real cash flow and taken into consideration

all the non-cash affecting transactions also. Moreover, it does not consider the time value of

money.

Net present value: Hill Ranch investment indicated that at 10% cost of capital, total

discounted CI and CO are £16915000 and £10m, indicates positive NPV of £691, 5000

hence, should be accepted by Bertie plc. The benefit is it considers the time value of money

and determines future value of the NCF through discounting. Moreover, it considers overall

cash flows during project life and provides more accurate estimation about the project return.

Its limitation is it is very difficult to determine an appropriate discount factor for the

investment project. For instance, market uncertainties, weather conditions, inflation rates, tax

regulations, foreign exchange rates, consumer demand and market risk will impact the cash

flows and also the cost of capital. Therefore, decisions based on this method is highly

depends upon the managers skills and quality of estimations used.

Sources of internal finance

Short term finance source (STFS)

Reducing Inventory holdings: Bertie Plc inventory days is decreased from 22.44 days

to 17.40 days hence; it is good sign. It implies that in 2015 inventory is hold for less time

period compare to PY contributed to enhance sales. Further, through quicker movement of

goods Bertie Plc is able to get cash quickly and support the operating functions. It will

enhance company's ability to pay off its short term obligations and do not stuck the money in

inventory. Moreover, it indicates that Bertie Plc managers are establishing effective supply

chain management and marketing campaign. Thus, it became clear that through reducing the

holding period, Bertie Plc is managing their cash for short-term finance. On the other hand, if

demand suddenly changes in upward direction, then it might be possible for Bertie plc to face

some difficulties. For instance, high rising in demand will lower performance. The reason is

without having goods in stock, Bertie Plc will not be able to satisfy customer demands

immediately.

Extending Supplier payment terms: It got reduced from 77.75 days to 78.20 days in

2015. It indicates the time period that the supplier given to company for making payments is

relaxed. It represents that Bertie plc is paying delayed payments to the suppliers so more

STFS will be available which Bertie Plc can utilize to run operations. Further, in 2015,

7 | P a g e

rather than cash flows. Hence, it not consider the real cash flow and taken into consideration

all the non-cash affecting transactions also. Moreover, it does not consider the time value of

money.

Net present value: Hill Ranch investment indicated that at 10% cost of capital, total

discounted CI and CO are £16915000 and £10m, indicates positive NPV of £691, 5000

hence, should be accepted by Bertie plc. The benefit is it considers the time value of money

and determines future value of the NCF through discounting. Moreover, it considers overall

cash flows during project life and provides more accurate estimation about the project return.

Its limitation is it is very difficult to determine an appropriate discount factor for the

investment project. For instance, market uncertainties, weather conditions, inflation rates, tax

regulations, foreign exchange rates, consumer demand and market risk will impact the cash

flows and also the cost of capital. Therefore, decisions based on this method is highly

depends upon the managers skills and quality of estimations used.

Sources of internal finance

Short term finance source (STFS)

Reducing Inventory holdings: Bertie Plc inventory days is decreased from 22.44 days

to 17.40 days hence; it is good sign. It implies that in 2015 inventory is hold for less time

period compare to PY contributed to enhance sales. Further, through quicker movement of

goods Bertie Plc is able to get cash quickly and support the operating functions. It will

enhance company's ability to pay off its short term obligations and do not stuck the money in

inventory. Moreover, it indicates that Bertie Plc managers are establishing effective supply

chain management and marketing campaign. Thus, it became clear that through reducing the

holding period, Bertie Plc is managing their cash for short-term finance. On the other hand, if

demand suddenly changes in upward direction, then it might be possible for Bertie plc to face

some difficulties. For instance, high rising in demand will lower performance. The reason is

without having goods in stock, Bertie Plc will not be able to satisfy customer demands

immediately.

Extending Supplier payment terms: It got reduced from 77.75 days to 78.20 days in

2015. It indicates the time period that the supplier given to company for making payments is

relaxed. It represents that Bertie plc is paying delayed payments to the suppliers so more

STFS will be available which Bertie Plc can utilize to run operations. Further, in 2015,

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

interest free credit of 59.7 days (17.40+1.10-78.20) is also available to Bertie plc resulted in

better availability of STFS. On the other hand, in industry context, supplier provide credit for

90 days hence, Bertie plc can increase the payable days more by 10 days. Thus, Bertie Plc

can negotiate supplier payments and will be able to avail more cash sources to run its

operative functions.

8 | P a g e

better availability of STFS. On the other hand, in industry context, supplier provide credit for

90 days hence, Bertie plc can increase the payable days more by 10 days. Thus, Bertie Plc

can negotiate supplier payments and will be able to avail more cash sources to run its

operative functions.

8 | P a g e

REFERENCES

Books and Journals

Alkaraan, F., 2015. Strategic investment decision-making perspectives. Advances in Mergers

and Acquisitions. 14. pp. 53-66.

Atrill, P. & McLaney, E., 2013. Accounting and finance for non-specialists. 8th Ed. Harlow,

UK: Pearson Publishing. Making Capital Investment Decisions. pp.344-385.

Brealey, R. A., 2012. Principles of corporate finance. Tata McGraw-Hill Education.

Carmichael, D. G., 2011. An alternative approach to capital investment appraisal. The

Engineering Economist. 56(2). pp. 123-139.

Cesarini and et. al., 2010. Genetic Variation in Financial Decision‐Making. The Journal of

Finance. 65(5). pp. 1725-1754.

Clemen, R. and Reilly, T., 2013. Making hard decisions with DecisionTools. Cengage

Learning.

Götze, U., Northcott, D. and Schuster, P., 2015. Selected Further Applications of Investment

Appraisal Methods. In Investment Appraisal. Springer Berlin Heidelberg. pp. 105-159.

Maclean, L. and Ziemba, T. W., 2013. Handbook of the Fundamental of Financial Decision

Making: In 2 parts. World Scientific.

Suto, I., Clare, H. C. I. and Holland, T., 2007. Financial-decision making: Guidance for

supporting Financial Decision Making By People With Learning Disabilities. BILD

Publications.

Thaler, R. H., 2010. The end of behavioral finance.

Online

Grocery Stores Industry, 2015. [Online]. Available through:

<http://csimarket.com/Industry/industry_Profitability_Ratios.php?ind=1305>.

[Accessed on 2nd Feburary, 2016].

M & S Annual Report and Financial Statements, 2014. [Pdf]. Avaialble through:

<corporate.marksandspencer.com/investors/b73df1d3e4f54f429210f115ab11e2f6>.

[ Accessed on 28th November, 2015].

Robinson, J. O., Bond, L. R. and Roiser, P. J., 2015. The Impact of stress on financial

decision-making varies as a function of depression and anxiety symptoms. [Pdf].

Available through: <https://peerj.com/articles/770.pdf>. [Accessed on 19th November,

2015].

9 | P a g e

Books and Journals

Alkaraan, F., 2015. Strategic investment decision-making perspectives. Advances in Mergers

and Acquisitions. 14. pp. 53-66.

Atrill, P. & McLaney, E., 2013. Accounting and finance for non-specialists. 8th Ed. Harlow,

UK: Pearson Publishing. Making Capital Investment Decisions. pp.344-385.

Brealey, R. A., 2012. Principles of corporate finance. Tata McGraw-Hill Education.

Carmichael, D. G., 2011. An alternative approach to capital investment appraisal. The

Engineering Economist. 56(2). pp. 123-139.

Cesarini and et. al., 2010. Genetic Variation in Financial Decision‐Making. The Journal of

Finance. 65(5). pp. 1725-1754.

Clemen, R. and Reilly, T., 2013. Making hard decisions with DecisionTools. Cengage

Learning.

Götze, U., Northcott, D. and Schuster, P., 2015. Selected Further Applications of Investment

Appraisal Methods. In Investment Appraisal. Springer Berlin Heidelberg. pp. 105-159.

Maclean, L. and Ziemba, T. W., 2013. Handbook of the Fundamental of Financial Decision

Making: In 2 parts. World Scientific.

Suto, I., Clare, H. C. I. and Holland, T., 2007. Financial-decision making: Guidance for

supporting Financial Decision Making By People With Learning Disabilities. BILD

Publications.

Thaler, R. H., 2010. The end of behavioral finance.

Online

Grocery Stores Industry, 2015. [Online]. Available through:

<http://csimarket.com/Industry/industry_Profitability_Ratios.php?ind=1305>.

[Accessed on 2nd Feburary, 2016].

M & S Annual Report and Financial Statements, 2014. [Pdf]. Avaialble through:

<corporate.marksandspencer.com/investors/b73df1d3e4f54f429210f115ab11e2f6>.

[ Accessed on 28th November, 2015].

Robinson, J. O., Bond, L. R. and Roiser, P. J., 2015. The Impact of stress on financial

decision-making varies as a function of depression and anxiety symptoms. [Pdf].

Available through: <https://peerj.com/articles/770.pdf>. [Accessed on 19th November,

2015].

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.