Applying Management Accounting Techniques: A Report on Beztec Limited

VerifiedAdded on 2023/06/04

|12

|3086

|160

Report

AI Summary

This report provides a detailed analysis of Beztec Limited's costing methods and profitability using management accounting techniques. It begins by emphasizing the importance of accurate product costing in various areas such as budgeting, income statement preparation, asset valuation, make-or-buy decisions, and product pricing. The report then critiques Beztec's current traditional costing method, advocating for the implementation of activity-based costing (ABC) to improve the accuracy of cost allocation. The report includes a detailed application of ABC, calculating overhead costs for different activities and allocating them to Lexon and Protox printers. Furthermore, it presents a comparative analysis of the profitability of each printer model based on the ABC method, highlighting the impact on gross profit per unit. The report addresses an ethical dilemma faced by the management accountant, who is pressured to manipulate the ABC results for personal gain, emphasizing the importance of adhering to ethical principles such as integrity, objectivity, professional behavior, and competence. It concludes by recommending that Beztec adopt ABC to make informed decisions about product phasing and overall profitability.

Management Accounting Techniques 0

Management Accounting

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting Techniques 1

Question 1

Accuracy is important to manage the finances of business. The financial results of an entity in

a particular year depict its true financial position when all the results are accurately

determined and analysed. From the perspective of preparation of financial statements as well

as tax filing, the correctness of all the financial information regarding the business is of

utmost importance. In a manufacturing concern, product costing is the function of assigning

cost to each individual product on the basis of quantum consumption of various resources

such as time, materials etc. in the production process of such products. In a trading concern,

product costing is the function of adding cost of value addition to the cost of the product

which is purchased from the market (Hilton & Platt, 2013). In service organisation, services

are the products of such concerns as in these organisations information is being provided

which is collected by conducting various interviews, data searches and analysis, discussions

or consultations and so on. The costing of such organisation is undertaken using the

information related to the consumption of time and other resources in provision of such

services to the ultimate client (Maelah & Ibrahim, 2007). The importance of accurate product

costing can be clearly observed in following particular areas:

Budget Impact: When all the expenses or costs which are going to be incurred in the

budgeted period are not accurately estimated there are possibilities of the situation

when the company has to lose track from the entire budgeted statement in the course

of carrying out of the actual operations. If the product costs are calculated incorrectly,

there are higher chances of errors in the budgeting process which may result in

excessive spending against the budgeted cost, causing financial strain for the entity.

Income Statement Preparation: To prepare the income statement, it is necessary to

determine the correct amount of cost of goods sold ((Lambert, Leuz & Verrecchia,

Question 1

Accuracy is important to manage the finances of business. The financial results of an entity in

a particular year depict its true financial position when all the results are accurately

determined and analysed. From the perspective of preparation of financial statements as well

as tax filing, the correctness of all the financial information regarding the business is of

utmost importance. In a manufacturing concern, product costing is the function of assigning

cost to each individual product on the basis of quantum consumption of various resources

such as time, materials etc. in the production process of such products. In a trading concern,

product costing is the function of adding cost of value addition to the cost of the product

which is purchased from the market (Hilton & Platt, 2013). In service organisation, services

are the products of such concerns as in these organisations information is being provided

which is collected by conducting various interviews, data searches and analysis, discussions

or consultations and so on. The costing of such organisation is undertaken using the

information related to the consumption of time and other resources in provision of such

services to the ultimate client (Maelah & Ibrahim, 2007). The importance of accurate product

costing can be clearly observed in following particular areas:

Budget Impact: When all the expenses or costs which are going to be incurred in the

budgeted period are not accurately estimated there are possibilities of the situation

when the company has to lose track from the entire budgeted statement in the course

of carrying out of the actual operations. If the product costs are calculated incorrectly,

there are higher chances of errors in the budgeting process which may result in

excessive spending against the budgeted cost, causing financial strain for the entity.

Income Statement Preparation: To prepare the income statement, it is necessary to

determine the correct amount of cost of goods sold ((Lambert, Leuz & Verrecchia,

Management Accounting Techniques 2

2007). The value of Cost of goods sold can only be determined correctly when the

firm has accurate information of cost of production. If accurate information regarding

the true cost involved in the production process is not available then correct level of

gross profit of the company cannot be determined.

Assets and Inventory Valuation: The valuation of inventories held by an entity

depends on the accurate reporting of all the direct costs related to the products dealt

by such entity (Edwards, 2013). If product cost is not calculated correctly, the value

of the inventory will also go incorrect and in such cases overstatement or

understatement of profit will occur in the financial statements. if true profitability

position is not depicted by the financial statements, it may lead to incorrect decision

making by the managers.

Make or buy decisions: Many a times a firm has to decide as to whether the raw

materials requisite for their manufacturing processes shall be internally manufactured

or to be procured from the market. To undertake such decisions a cost benefit analysis

is undertaken by the management accountants of the firm. This analysis can allow the

managers to reach at the appropriate decision when accurate cost information is used

under the cost benefit analysis.

Product price fixation: Determining the appropriate selling price of the products

manufactured by the company is quite a necessary process. It requires adding a

desirable profit margin to the total cost involved in the production process of the

manufacturing concern. If accurate information regarding the actual cost incurred in

the manufacturing process is not available with the company, it becomes difficult to

set a reasonable price. In absence of such information, the company may have to face

situations of losses or low profits due to low price fixation of the products (Schmidt,

Nakajima, 2013).

2007). The value of Cost of goods sold can only be determined correctly when the

firm has accurate information of cost of production. If accurate information regarding

the true cost involved in the production process is not available then correct level of

gross profit of the company cannot be determined.

Assets and Inventory Valuation: The valuation of inventories held by an entity

depends on the accurate reporting of all the direct costs related to the products dealt

by such entity (Edwards, 2013). If product cost is not calculated correctly, the value

of the inventory will also go incorrect and in such cases overstatement or

understatement of profit will occur in the financial statements. if true profitability

position is not depicted by the financial statements, it may lead to incorrect decision

making by the managers.

Make or buy decisions: Many a times a firm has to decide as to whether the raw

materials requisite for their manufacturing processes shall be internally manufactured

or to be procured from the market. To undertake such decisions a cost benefit analysis

is undertaken by the management accountants of the firm. This analysis can allow the

managers to reach at the appropriate decision when accurate cost information is used

under the cost benefit analysis.

Product price fixation: Determining the appropriate selling price of the products

manufactured by the company is quite a necessary process. It requires adding a

desirable profit margin to the total cost involved in the production process of the

manufacturing concern. If accurate information regarding the actual cost incurred in

the manufacturing process is not available with the company, it becomes difficult to

set a reasonable price. In absence of such information, the company may have to face

situations of losses or low profits due to low price fixation of the products (Schmidt,

Nakajima, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting Techniques 3

Product continuance or discontinuation decisions: Many a times, managers have to

decide on the matters like business expansion or termination of a particular product

line because of resource constraints. In such cases, it is important to determine the

profitability potential of the product unit in order to select the appropriate product unit

for the termination. For such purposes availability of accurate cost information is

necessary.

In the instant case of Beztec Limited is currently employing traditional costing

method to determine the cost of the printers manufactured by it. As a part of

traditional costing, all the overhead costs are allocated to both the printing machines

models i.e. Lexon and Protox on the basis of overhead recovery rate. The said rate is

applied to the actual machine hours consumed in manufacturing both the types of

printers. However, not all the activities that are involved in the manufacturing process

of Beztec Limited relates to the machine hours. Hence, it is not an appropriate

management accounting practice to allocate all the production related overheads of

the machine on the basis of single overhead recovery rate (Granof & Platt &

Vaysman, 2000). Rather, the company must implement the activity based costing

method for the allocation of different overhead costs to both the product lines. ABC

method will allow the reasonable allocation of production overheads to Lexon

Printers and Protox Printers on the basis of activities that are driving the cost of

respective overheads. Under ABC, the overheads related to the soldering activity will

be allocated to both the printer divisions on the basis of number of soldering points

involved in the activity. Further, the shipment cost will be allocated to both the

printers on the basis of number of shipments undertaken in respect of each division.

The quality cost incurred for the inspection of the product quality will be apportioned

to the products on the basis of number of inspections conducted in respect of each

Product continuance or discontinuation decisions: Many a times, managers have to

decide on the matters like business expansion or termination of a particular product

line because of resource constraints. In such cases, it is important to determine the

profitability potential of the product unit in order to select the appropriate product unit

for the termination. For such purposes availability of accurate cost information is

necessary.

In the instant case of Beztec Limited is currently employing traditional costing

method to determine the cost of the printers manufactured by it. As a part of

traditional costing, all the overhead costs are allocated to both the printing machines

models i.e. Lexon and Protox on the basis of overhead recovery rate. The said rate is

applied to the actual machine hours consumed in manufacturing both the types of

printers. However, not all the activities that are involved in the manufacturing process

of Beztec Limited relates to the machine hours. Hence, it is not an appropriate

management accounting practice to allocate all the production related overheads of

the machine on the basis of single overhead recovery rate (Granof & Platt &

Vaysman, 2000). Rather, the company must implement the activity based costing

method for the allocation of different overhead costs to both the product lines. ABC

method will allow the reasonable allocation of production overheads to Lexon

Printers and Protox Printers on the basis of activities that are driving the cost of

respective overheads. Under ABC, the overheads related to the soldering activity will

be allocated to both the printer divisions on the basis of number of soldering points

involved in the activity. Further, the shipment cost will be allocated to both the

printers on the basis of number of shipments undertaken in respect of each division.

The quality cost incurred for the inspection of the product quality will be apportioned

to the products on the basis of number of inspections conducted in respect of each

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting Techniques 4

product division (Maelah & Ibrahim, 2007). In this way, all the production overheads

of the company will be allocated to both the printing machines in the most appropriate

basis. ABC method will enable the managers of the company to determine the true

cost of the printers by offering accurate product costing information which could be

relied on for the important decisions of the business.

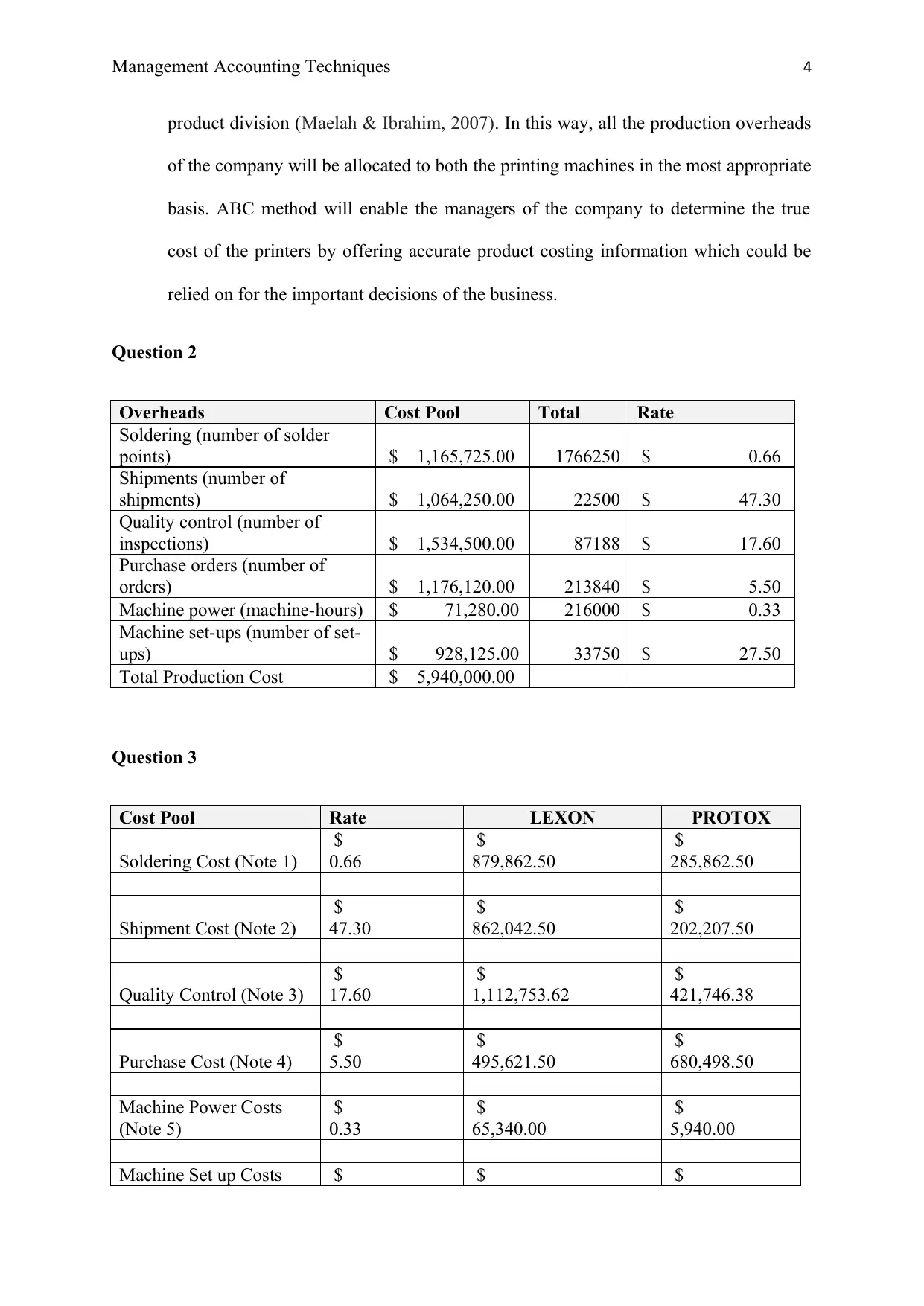

Question 2

Overheads Cost Pool Total Rate

Soldering (number of solder

points) $ 1,165,725.00 1766250 $ 0.66

Shipments (number of

shipments) $ 1,064,250.00 22500 $ 47.30

Quality control (number of

inspections) $ 1,534,500.00 87188 $ 17.60

Purchase orders (number of

orders) $ 1,176,120.00 213840 $ 5.50

Machine power (machine-hours) $ 71,280.00 216000 $ 0.33

Machine set-ups (number of set-

ups) $ 928,125.00 33750 $ 27.50

Total Production Cost $ 5,940,000.00

Question 3

Cost Pool Rate LEXON PROTOX

Soldering Cost (Note 1)

$

0.66

$

879,862.50

$

285,862.50

Shipment Cost (Note 2)

$

47.30

$

862,042.50

$

202,207.50

Quality Control (Note 3)

$

17.60

$

1,112,753.62

$

421,746.38

Purchase Cost (Note 4)

$

5.50

$

495,621.50

$

680,498.50

Machine Power Costs

(Note 5)

$

0.33

$

65,340.00

$

5,940.00

Machine Set up Costs $ $ $

product division (Maelah & Ibrahim, 2007). In this way, all the production overheads

of the company will be allocated to both the printing machines in the most appropriate

basis. ABC method will enable the managers of the company to determine the true

cost of the printers by offering accurate product costing information which could be

relied on for the important decisions of the business.

Question 2

Overheads Cost Pool Total Rate

Soldering (number of solder

points) $ 1,165,725.00 1766250 $ 0.66

Shipments (number of

shipments) $ 1,064,250.00 22500 $ 47.30

Quality control (number of

inspections) $ 1,534,500.00 87188 $ 17.60

Purchase orders (number of

orders) $ 1,176,120.00 213840 $ 5.50

Machine power (machine-hours) $ 71,280.00 216000 $ 0.33

Machine set-ups (number of set-

ups) $ 928,125.00 33750 $ 27.50

Total Production Cost $ 5,940,000.00

Question 3

Cost Pool Rate LEXON PROTOX

Soldering Cost (Note 1)

$

0.66

$

879,862.50

$

285,862.50

Shipment Cost (Note 2)

$

47.30

$

862,042.50

$

202,207.50

Quality Control (Note 3)

$

17.60

$

1,112,753.62

$

421,746.38

Purchase Cost (Note 4)

$

5.50

$

495,621.50

$

680,498.50

Machine Power Costs

(Note 5)

$

0.33

$

65,340.00

$

5,940.00

Machine Set up Costs $ $ $

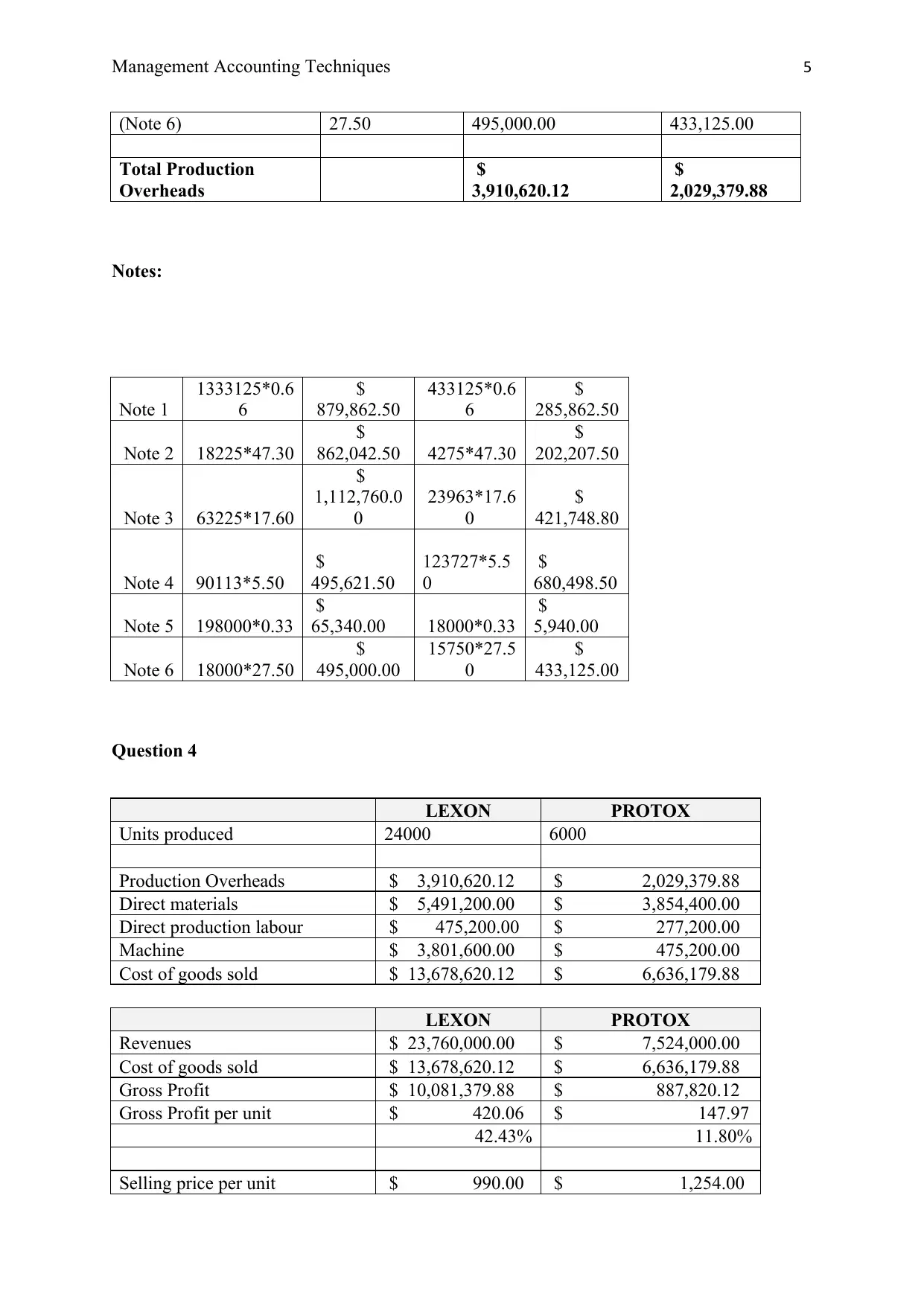

Management Accounting Techniques 5

(Note 6) 27.50 495,000.00 433,125.00

Total Production

Overheads

$

3,910,620.12

$

2,029,379.88

Notes:

Note 1

1333125*0.6

6

$

879,862.50

433125*0.6

6

$

285,862.50

Note 2 18225*47.30

$

862,042.50 4275*47.30

$

202,207.50

Note 3 63225*17.60

$

1,112,760.0

0

23963*17.6

0

$

421,748.80

Note 4 90113*5.50

$

495,621.50

123727*5.5

0

$

680,498.50

Note 5 198000*0.33

$

65,340.00 18000*0.33

$

5,940.00

Note 6 18000*27.50

$

495,000.00

15750*27.5

0

$

433,125.00

Question 4

LEXON PROTOX

Units produced 24000 6000

Production Overheads $ 3,910,620.12 $ 2,029,379.88

Direct materials $ 5,491,200.00 $ 3,854,400.00

Direct production labour $ 475,200.00 $ 277,200.00

Machine $ 3,801,600.00 $ 475,200.00

Cost of goods sold $ 13,678,620.12 $ 6,636,179.88

LEXON PROTOX

Revenues $ 23,760,000.00 $ 7,524,000.00

Cost of goods sold $ 13,678,620.12 $ 6,636,179.88

Gross Profit $ 10,081,379.88 $ 887,820.12

Gross Profit per unit $ 420.06 $ 147.97

42.43% 11.80%

Selling price per unit $ 990.00 $ 1,254.00

(Note 6) 27.50 495,000.00 433,125.00

Total Production

Overheads

$

3,910,620.12

$

2,029,379.88

Notes:

Note 1

1333125*0.6

6

$

879,862.50

433125*0.6

6

$

285,862.50

Note 2 18225*47.30

$

862,042.50 4275*47.30

$

202,207.50

Note 3 63225*17.60

$

1,112,760.0

0

23963*17.6

0

$

421,748.80

Note 4 90113*5.50

$

495,621.50

123727*5.5

0

$

680,498.50

Note 5 198000*0.33

$

65,340.00 18000*0.33

$

5,940.00

Note 6 18000*27.50

$

495,000.00

15750*27.5

0

$

433,125.00

Question 4

LEXON PROTOX

Units produced 24000 6000

Production Overheads $ 3,910,620.12 $ 2,029,379.88

Direct materials $ 5,491,200.00 $ 3,854,400.00

Direct production labour $ 475,200.00 $ 277,200.00

Machine $ 3,801,600.00 $ 475,200.00

Cost of goods sold $ 13,678,620.12 $ 6,636,179.88

LEXON PROTOX

Revenues $ 23,760,000.00 $ 7,524,000.00

Cost of goods sold $ 13,678,620.12 $ 6,636,179.88

Gross Profit $ 10,081,379.88 $ 887,820.12

Gross Profit per unit $ 420.06 $ 147.97

42.43% 11.80%

Selling price per unit $ 990.00 $ 1,254.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting Techniques 6

Cost of goods sold $ 569.94 $ 1,106.03

Gross Profit $ 420.06 $ 147.97

Question 5

In the case of Beztec Limited, Steve Kay, the CEO of the company has suggested Sue Smith

who is the management accountant of the company to alter the results obtained by him by the

adoption of system of activity based costing for the personal interests that the CEO has in the

company (Klimek & Wenell, 2011). Beztec Limited has been paying bonuses to its top

management executives on the basis of the revenues generated by each of its product

division. Due to the fear of significant decline in the performance based incentives, Kay has

refused to accept the results of activity based costing. This situation raises the ethical concern

for the management accountant of the company as it is professional accountant’s duty to act

in public interest. Therefore, Miss Smith has to apply all the professional knowledge and

competence while performing the professional services (APES 110). Also, it is the duty of the

management accountant to strictly adhere to all the principles of ethical code of conduct as

prescribed by the board of accounting professional and ethical standards (Smith, L.M., 2003).

There are five fundamental principles prescribed under the said code and the professional

accountants have to follow each and every principle while fulfilling their responsibilities

towards the profession so as to avoid any legal or regulatory interventions. Following are the

principles as prescribed under APES 110 Code of Ethics, that are applicable to the present

case of Steve Smith while performance of professional services for Beztec Limited.

Principle of integrity: This principle requires the accountant to act in the most

straight-forward and loyal manner towards the professional obligations while

engaging themselves with the client or employer.

Cost of goods sold $ 569.94 $ 1,106.03

Gross Profit $ 420.06 $ 147.97

Question 5

In the case of Beztec Limited, Steve Kay, the CEO of the company has suggested Sue Smith

who is the management accountant of the company to alter the results obtained by him by the

adoption of system of activity based costing for the personal interests that the CEO has in the

company (Klimek & Wenell, 2011). Beztec Limited has been paying bonuses to its top

management executives on the basis of the revenues generated by each of its product

division. Due to the fear of significant decline in the performance based incentives, Kay has

refused to accept the results of activity based costing. This situation raises the ethical concern

for the management accountant of the company as it is professional accountant’s duty to act

in public interest. Therefore, Miss Smith has to apply all the professional knowledge and

competence while performing the professional services (APES 110). Also, it is the duty of the

management accountant to strictly adhere to all the principles of ethical code of conduct as

prescribed by the board of accounting professional and ethical standards (Smith, L.M., 2003).

There are five fundamental principles prescribed under the said code and the professional

accountants have to follow each and every principle while fulfilling their responsibilities

towards the profession so as to avoid any legal or regulatory interventions. Following are the

principles as prescribed under APES 110 Code of Ethics, that are applicable to the present

case of Steve Smith while performance of professional services for Beztec Limited.

Principle of integrity: This principle requires the accountant to act in the most

straight-forward and loyal manner towards the professional obligations while

engaging themselves with the client or employer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting Techniques 7

Principle of objectivity: This principle requires the accountant to apply professional

judgement during the course of performance of professional duties. The accountant

must avoid any kind of biasness or conflict of interest that overrides his professional

opinion.

Principle of professional behaviour: It is the professional duty of the accountant to

abide by all the rules and regulations as well as technical standards so as to avoid the

circumstances that discredits the accounting profession.

Principle of professional competence and due care:

According to this principle accountant shall apply professional knowledge,

competence as well as care while performing the accounting functions for any of the

client or appointing organisation. Professional services must be performed by them on

the basis of the techniques and standards applicable in the relevant to the field of

accounting (Armstrong, Ketz & Owsen, 2003).

In the instant case of Beztec Limited, the management accountant has to decide whether to

act in the given situation as per the principles of ethical behaviour as provided by the

regulators of profession or to act in the personal interest of the CEO of the company by

altering the results of activity based costing.

The results that have been obtained by the management accountant of Beztec Limited by the

application of activity based costing technique are not favourable to the top management of

the company which has actually hired the accountant. The results of ABC are in opposition of

the results derived by the application of conventional cost accounting. The results of

traditional costing have revealed that Lexon Model is less profitable than the Protox Model.

However, the results of activity based costing have allowed the management accountant to

reach at the conclusion that Lexon Model has the more profitable avenues than Protox Model.

Principle of objectivity: This principle requires the accountant to apply professional

judgement during the course of performance of professional duties. The accountant

must avoid any kind of biasness or conflict of interest that overrides his professional

opinion.

Principle of professional behaviour: It is the professional duty of the accountant to

abide by all the rules and regulations as well as technical standards so as to avoid the

circumstances that discredits the accounting profession.

Principle of professional competence and due care:

According to this principle accountant shall apply professional knowledge,

competence as well as care while performing the accounting functions for any of the

client or appointing organisation. Professional services must be performed by them on

the basis of the techniques and standards applicable in the relevant to the field of

accounting (Armstrong, Ketz & Owsen, 2003).

In the instant case of Beztec Limited, the management accountant has to decide whether to

act in the given situation as per the principles of ethical behaviour as provided by the

regulators of profession or to act in the personal interest of the CEO of the company by

altering the results of activity based costing.

The results that have been obtained by the management accountant of Beztec Limited by the

application of activity based costing technique are not favourable to the top management of

the company which has actually hired the accountant. The results of ABC are in opposition of

the results derived by the application of conventional cost accounting. The results of

traditional costing have revealed that Lexon Model is less profitable than the Protox Model.

However, the results of activity based costing have allowed the management accountant to

reach at the conclusion that Lexon Model has the more profitable avenues than Protox Model.

Management Accounting Techniques 8

Since, the top management of the company is intending to phase out one of the printer

machine manufacturing it is indispensible for the company to consider the option of product

phasing out diligently and prudently so as to reach at the appropriate conclusion. The

decision of phasing out of Lexon Printers merely by emphasising on the results of traditional

costing will not be appropriate.

Therefore, Miss Steve must try to encourage the top management of the company to adopt

activity based costing as the approach of determination of true overhead cost involved in the

printing machine manufacturing process. Activity based costing will provide the accurate cost

information to the company and it will also enable the management of the company to

formulate requisite strategies and policies for the long term profitability of the business

(Friedl, Küpper & Pedell, 2005).

Question 6:

Under-application or over-application of overheads takes places in the situations when the

actual overheads are not in line with budgeted overheads which are determined on the basis

of pre-determined overhead recovery rate (Horngren, 2009). Overheads are said to be under

applied when applied overheads are less than the actual overheads. Applied overheads are

determined by multiplying the actual hours consumed in the production with the pre-

determined overhead recovery rate. The reason of the variation in the actual and applied

overheads is that the overhead recovery rate is determined well-before starting the

manufacturing process (Horngren, et. al, 2010).

The manner of disposition of under or over applied overhead majorly depends on the

significance of the amount which is under or over applied. If the amount is not significant

enough, it is to be closed out through the account of cost of goods sold. If overheads are

under-applied then such amount of overhead shall be applied to the manufacturing process

Since, the top management of the company is intending to phase out one of the printer

machine manufacturing it is indispensible for the company to consider the option of product

phasing out diligently and prudently so as to reach at the appropriate conclusion. The

decision of phasing out of Lexon Printers merely by emphasising on the results of traditional

costing will not be appropriate.

Therefore, Miss Steve must try to encourage the top management of the company to adopt

activity based costing as the approach of determination of true overhead cost involved in the

printing machine manufacturing process. Activity based costing will provide the accurate cost

information to the company and it will also enable the management of the company to

formulate requisite strategies and policies for the long term profitability of the business

(Friedl, Küpper & Pedell, 2005).

Question 6:

Under-application or over-application of overheads takes places in the situations when the

actual overheads are not in line with budgeted overheads which are determined on the basis

of pre-determined overhead recovery rate (Horngren, 2009). Overheads are said to be under

applied when applied overheads are less than the actual overheads. Applied overheads are

determined by multiplying the actual hours consumed in the production with the pre-

determined overhead recovery rate. The reason of the variation in the actual and applied

overheads is that the overhead recovery rate is determined well-before starting the

manufacturing process (Horngren, et. al, 2010).

The manner of disposition of under or over applied overhead majorly depends on the

significance of the amount which is under or over applied. If the amount is not significant

enough, it is to be closed out through the account of cost of goods sold. If overheads are

under-applied then such amount of overhead shall be applied to the manufacturing process

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting Techniques 9

and the closing process leads to increase in the cost of goods sold (Kim & Ballard, 2002).

Conversely, when overheads are said to over-applied to the production process, then they

need to be disposed-off by way of reduction in the amount of cost of goods sold account.

However, if the amount of under or overhead overheads is material enough, it must be

proportionately allocated to the three accounts i.e. Work in Process Inventory Account

(WIP), Finished Goods Inventory Account and Cost of Goods Sold Account. The allocation

leads to change in the closing balances of the said accounts (Garrison, et. al, 2010).

In practicality second method is more appropriate than the first method.

and the closing process leads to increase in the cost of goods sold (Kim & Ballard, 2002).

Conversely, when overheads are said to over-applied to the production process, then they

need to be disposed-off by way of reduction in the amount of cost of goods sold account.

However, if the amount of under or overhead overheads is material enough, it must be

proportionately allocated to the three accounts i.e. Work in Process Inventory Account

(WIP), Finished Goods Inventory Account and Cost of Goods Sold Account. The allocation

leads to change in the closing balances of the said accounts (Garrison, et. al, 2010).

In practicality second method is more appropriate than the first method.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting Techniques 10

References:

APESB, 2010. APES 110: Code of Ethics for Professional Accountants. Available at:

https://www.apesb.org.au/uploads/standards/apesb_standards/standard1.pdf Accessed on

17.09.2018.

Armstrong, M.B., Ketz, J.E. and Owsen, D., 2003. Ethics education in accounting: Moving

toward ethical motivation and ethical behavior. Journal of Accounting education, 21(1), pp.1-

16.

Edwards, J.R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Friedl, G., Küpper, H.U. and Pedell, B., 2005. Relevance added: combining ABC with

German cost accounting. Strategic Finance, 86(12), p.56.

Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., 2010. Managerial

accounting. Issues in Accounting Education, 25(4), pp.792-793.

Granof, M.H., Platt, D.E. and Vaysman, I., 2000. Using activity-based costing to manage

more effectively. PricewaterhouseCoopers Endowment for the Business of Government.

Hilton, R.W. and Platt, D.E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Horngren, C.T., 2009. Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Horngren, C.T., Foster, G., Datar, S.M., Rajan, M., Ittner, C. and Baldwin, A.A., 2010. Cost

accounting: A managerial emphasis. Issues in Accounting Education, 25(4), pp.789-790.

Kim, Y.W. and Ballard, G., 2002. Case study–Overhead cost analysis. Proceedings IGLC,

Gramado, Brasil.

References:

APESB, 2010. APES 110: Code of Ethics for Professional Accountants. Available at:

https://www.apesb.org.au/uploads/standards/apesb_standards/standard1.pdf Accessed on

17.09.2018.

Armstrong, M.B., Ketz, J.E. and Owsen, D., 2003. Ethics education in accounting: Moving

toward ethical motivation and ethical behavior. Journal of Accounting education, 21(1), pp.1-

16.

Edwards, J.R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Friedl, G., Küpper, H.U. and Pedell, B., 2005. Relevance added: combining ABC with

German cost accounting. Strategic Finance, 86(12), p.56.

Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., 2010. Managerial

accounting. Issues in Accounting Education, 25(4), pp.792-793.

Granof, M.H., Platt, D.E. and Vaysman, I., 2000. Using activity-based costing to manage

more effectively. PricewaterhouseCoopers Endowment for the Business of Government.

Hilton, R.W. and Platt, D.E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Horngren, C.T., 2009. Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Horngren, C.T., Foster, G., Datar, S.M., Rajan, M., Ittner, C. and Baldwin, A.A., 2010. Cost

accounting: A managerial emphasis. Issues in Accounting Education, 25(4), pp.789-790.

Kim, Y.W. and Ballard, G., 2002. Case study–Overhead cost analysis. Proceedings IGLC,

Gramado, Brasil.

Management Accounting Techniques 11

Klimek, J. and Wenell, K., 2011. Ethics in accounting: an indispensable course?. Academy of

Educational Leadership Journal, 15(4), p.107.

Lambert, R., Leuz, C. and Verrecchia, R.E., 2007. Accounting information, disclosure, and

the cost of capital. Journal of accounting research, 45(2), pp.385-420.

Maelah, R. and Ibrahim, D.N., 2006. Activity based costing (ABC) adoption among

manufacturing organizations-the case of Malaysia. International Journal of Business and

Society, 7(1), pp.70-101.

Maelah, R. and Ibrahim, D.N., 2007. Factors influencing activity based costing (ABC)

adoption in manufacturing industry. Investment Management and Financial

Innovations, 4(2), pp.113-124.

Schmidt, M. and Nakajima, M., 2013. Material flow cost accounting as an approach to

improve resource efficiency in manufacturing companies. Resources, 2(3), pp.358-369.

Smith, L.M., 2003. A fresh look at accounting ethics (or Dr. Smith goes to

Washington). Accounting Horizons, 17(1), pp.47-49.

Klimek, J. and Wenell, K., 2011. Ethics in accounting: an indispensable course?. Academy of

Educational Leadership Journal, 15(4), p.107.

Lambert, R., Leuz, C. and Verrecchia, R.E., 2007. Accounting information, disclosure, and

the cost of capital. Journal of accounting research, 45(2), pp.385-420.

Maelah, R. and Ibrahim, D.N., 2006. Activity based costing (ABC) adoption among

manufacturing organizations-the case of Malaysia. International Journal of Business and

Society, 7(1), pp.70-101.

Maelah, R. and Ibrahim, D.N., 2007. Factors influencing activity based costing (ABC)

adoption in manufacturing industry. Investment Management and Financial

Innovations, 4(2), pp.113-124.

Schmidt, M. and Nakajima, M., 2013. Material flow cost accounting as an approach to

improve resource efficiency in manufacturing companies. Resources, 2(3), pp.358-369.

Smith, L.M., 2003. A fresh look at accounting ethics (or Dr. Smith goes to

Washington). Accounting Horizons, 17(1), pp.47-49.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.