Business Analytics Report: Analysis of Business Performance for BF Ltd

VerifiedAdded on 2022/12/30

|11

|1646

|60

Report

AI Summary

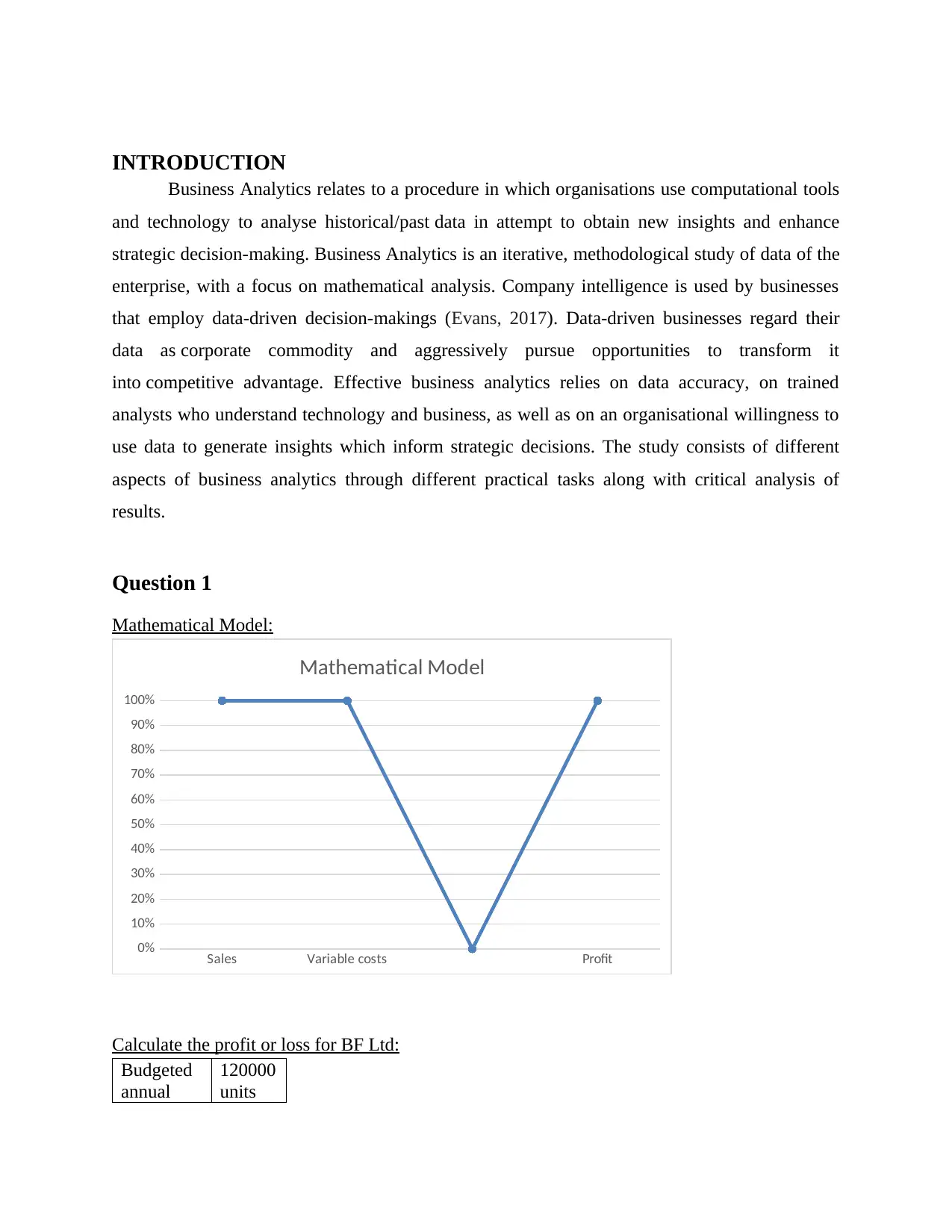

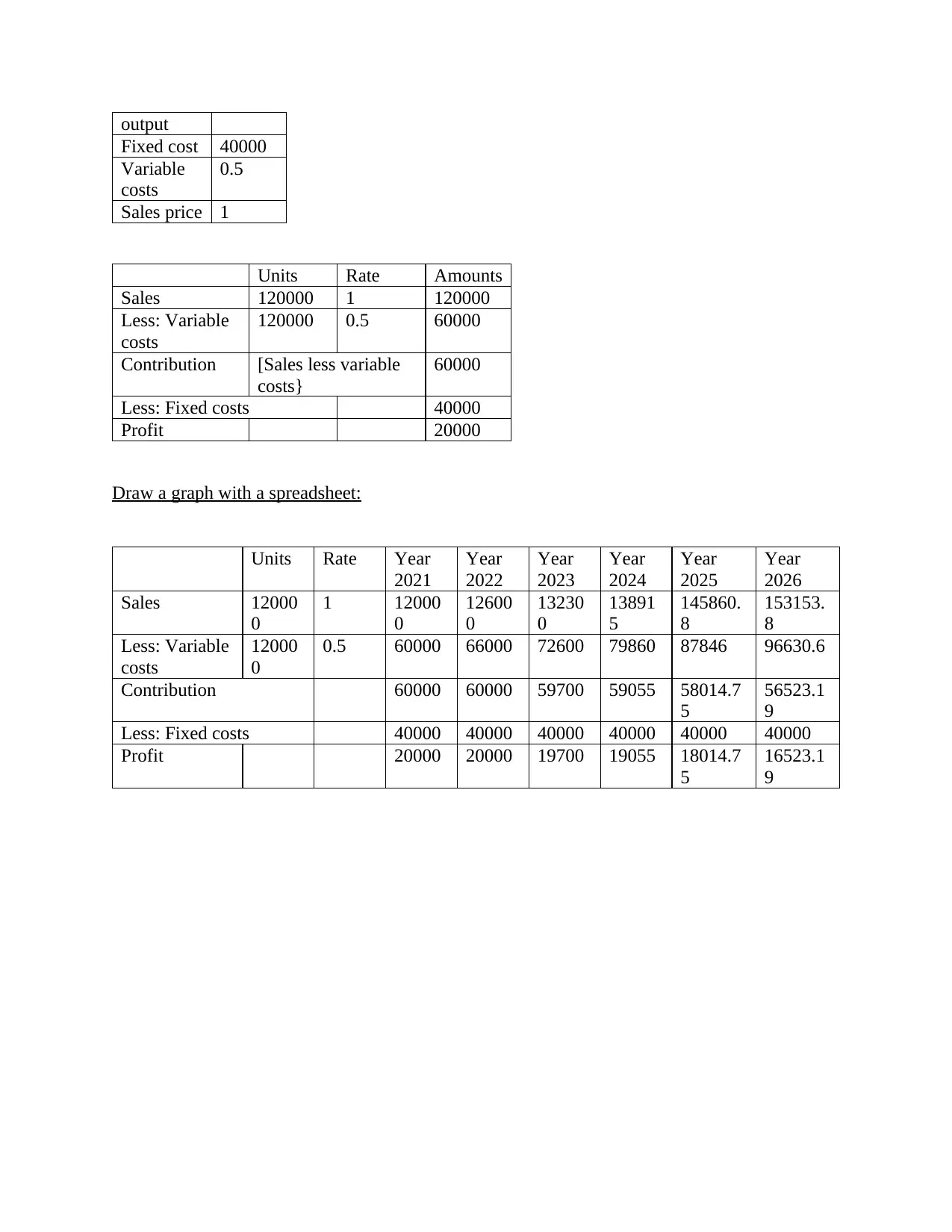

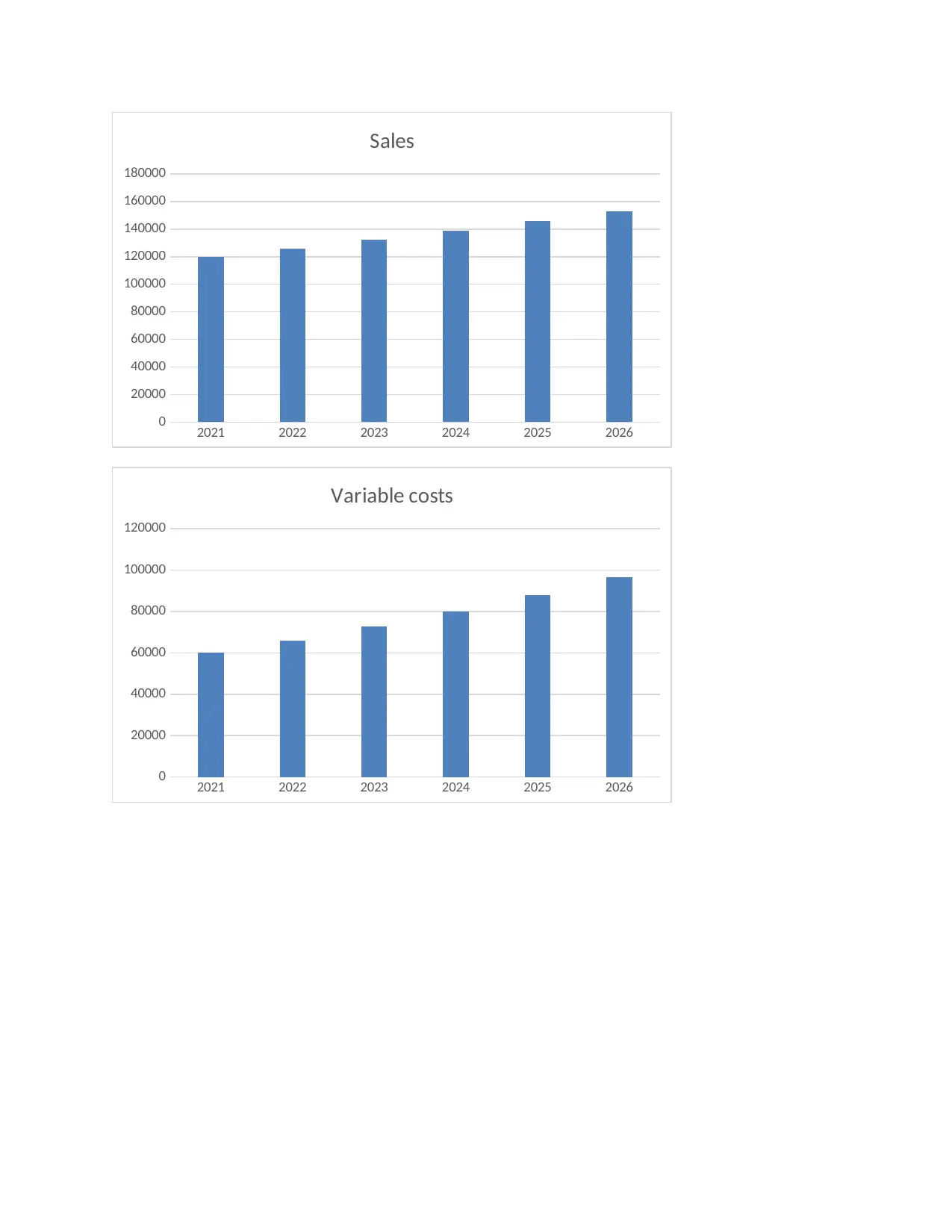

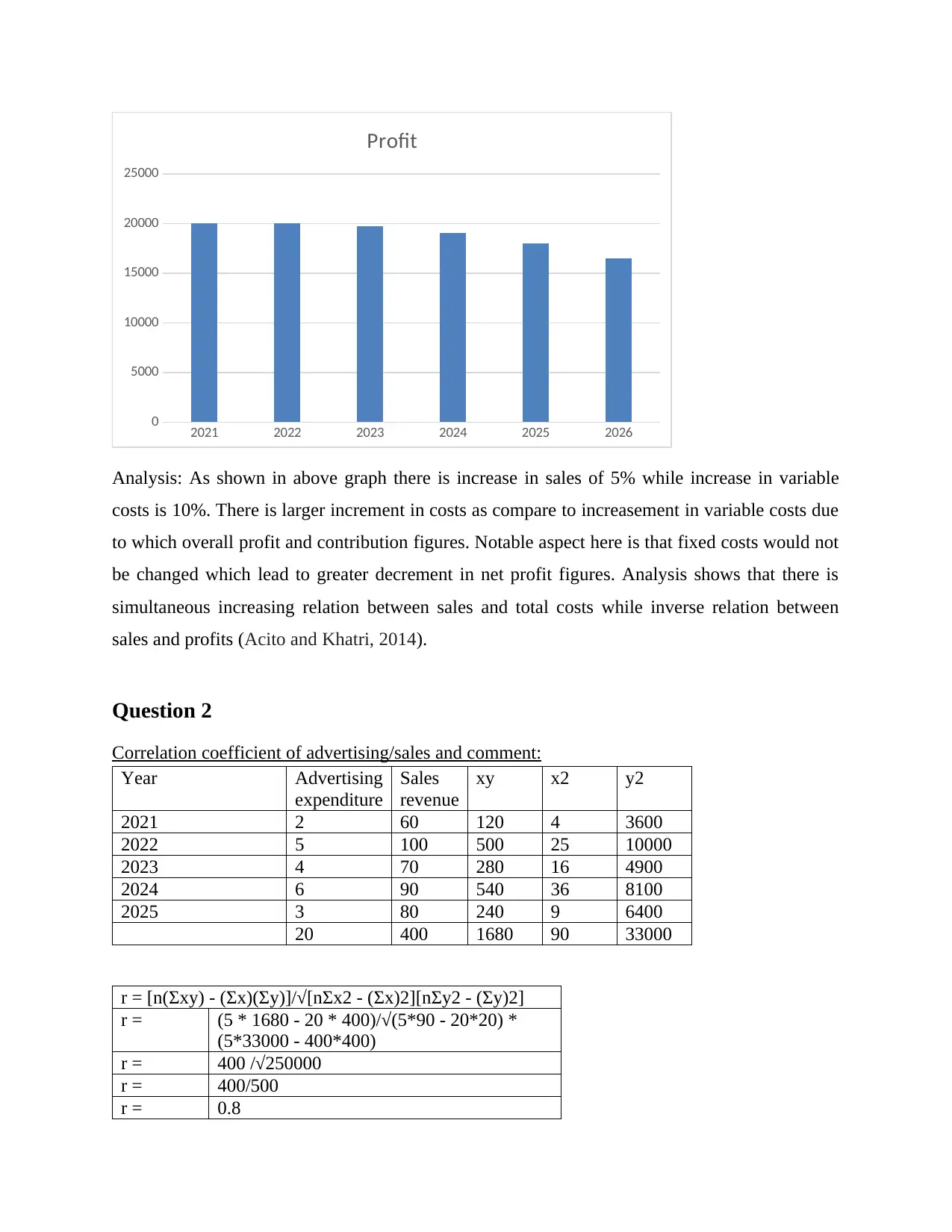

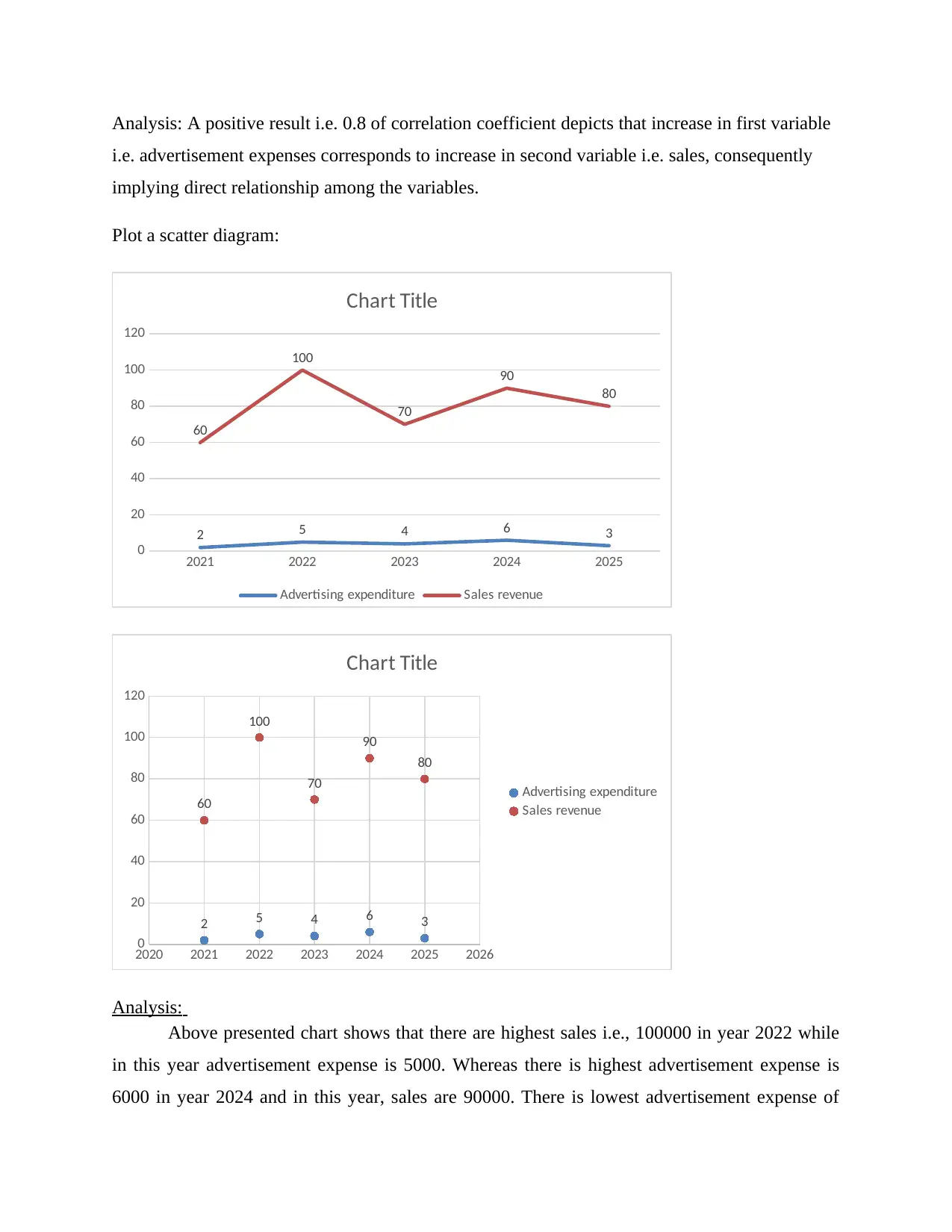

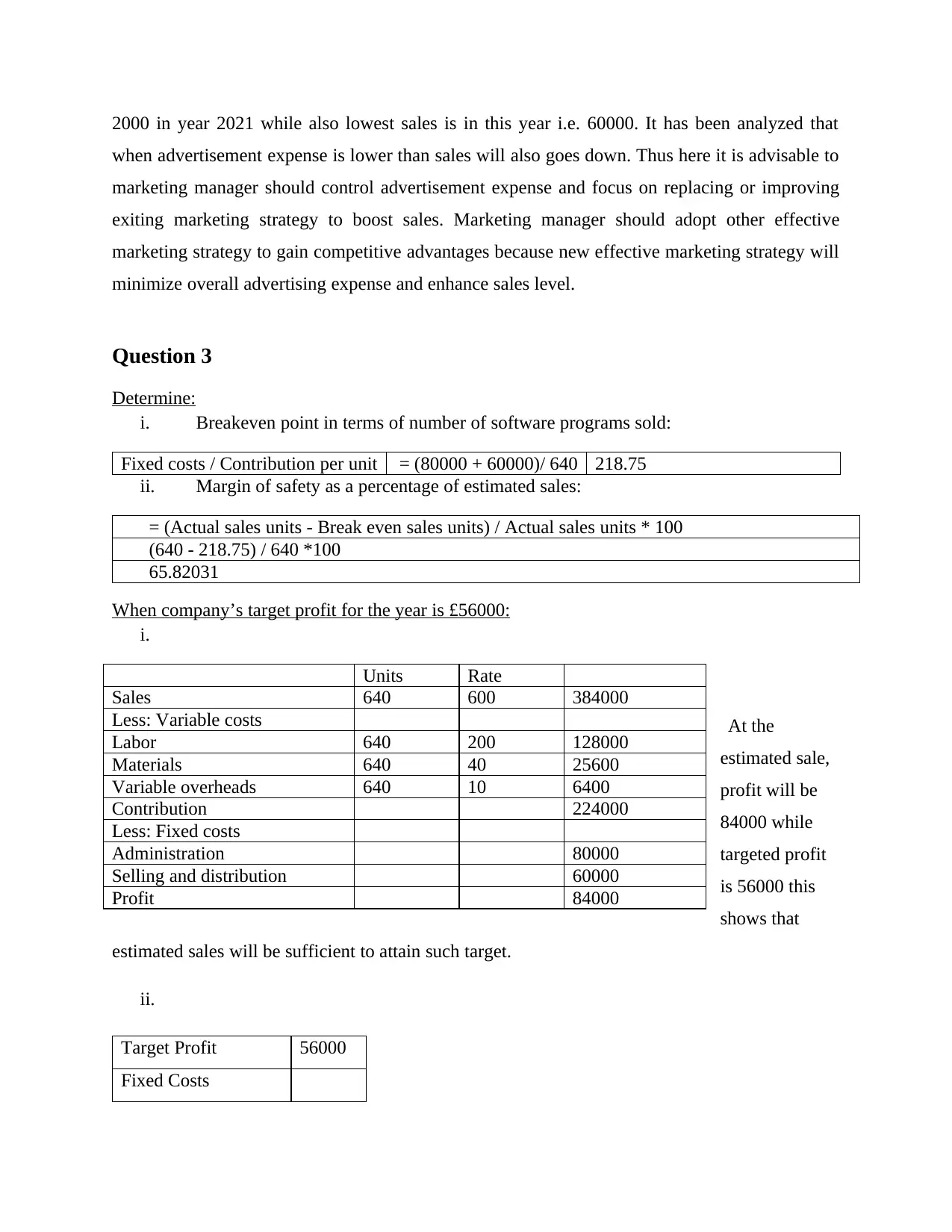

This report presents a comprehensive business analytics analysis of BF Ltd, encompassing various aspects of financial performance and strategic decision-making. The report begins with an introduction to business analytics, emphasizing its role in data-driven decision-making. It then delves into a mathematical model to calculate profit and loss, followed by a graphical representation of sales and variable costs. The analysis includes correlation coefficients to evaluate the relationship between advertising expenditure and sales revenue, alongside a scatter diagram visualization. Furthermore, the report determines break-even points, margin of safety, and target profit analysis, supported by a break-even chart. It concludes with a critical analysis of the benefits and limitations of the break-even model, providing valuable insights for business development and financial planning. This report is available on Desklib, a platform offering AI-based study tools and resources for students.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.