BFA714 Australian Tax Law Assignment 1: Income, Deductions, & Tax

VerifiedAdded on 2023/01/04

|13

|2105

|54

Homework Assignment

AI Summary

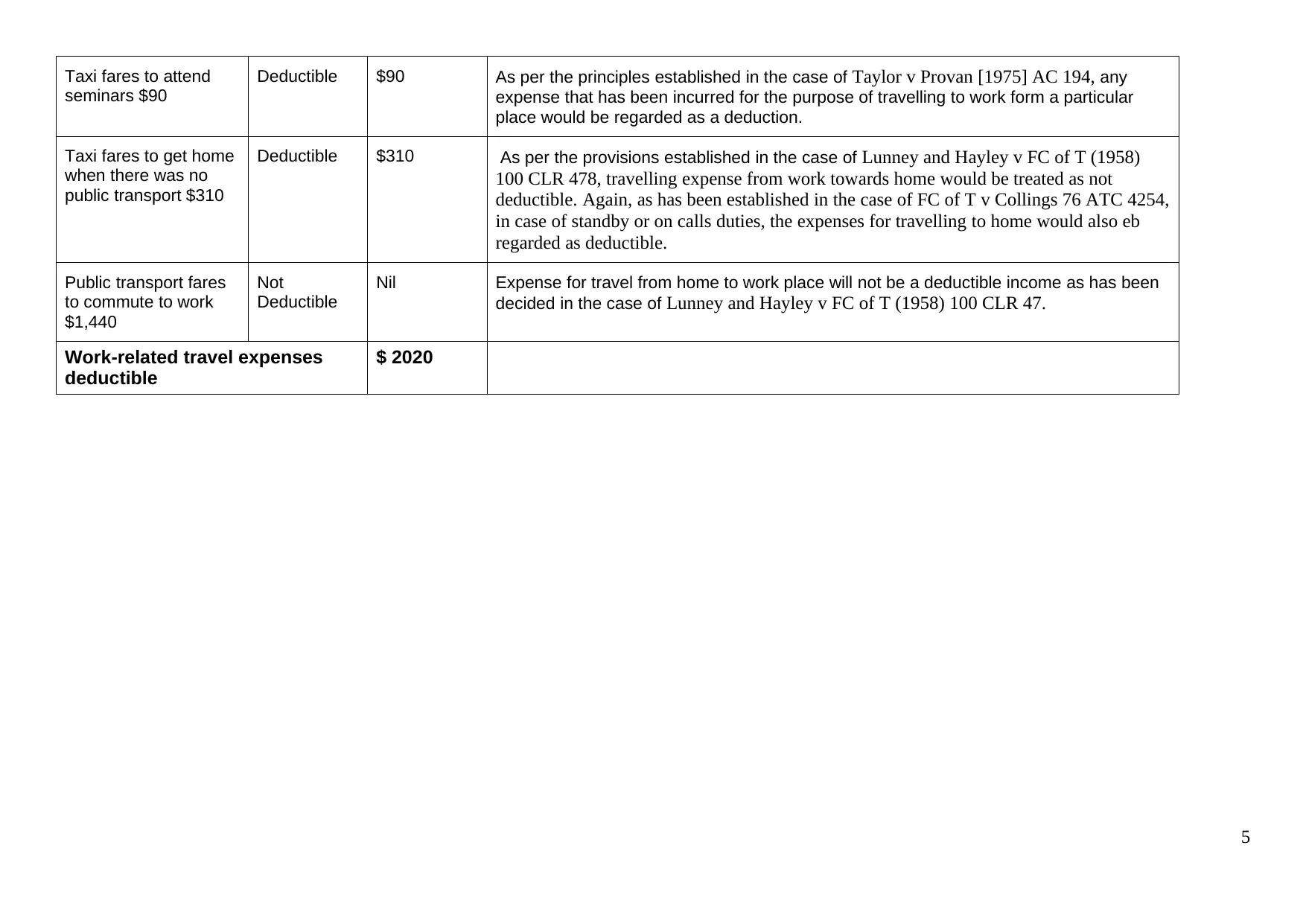

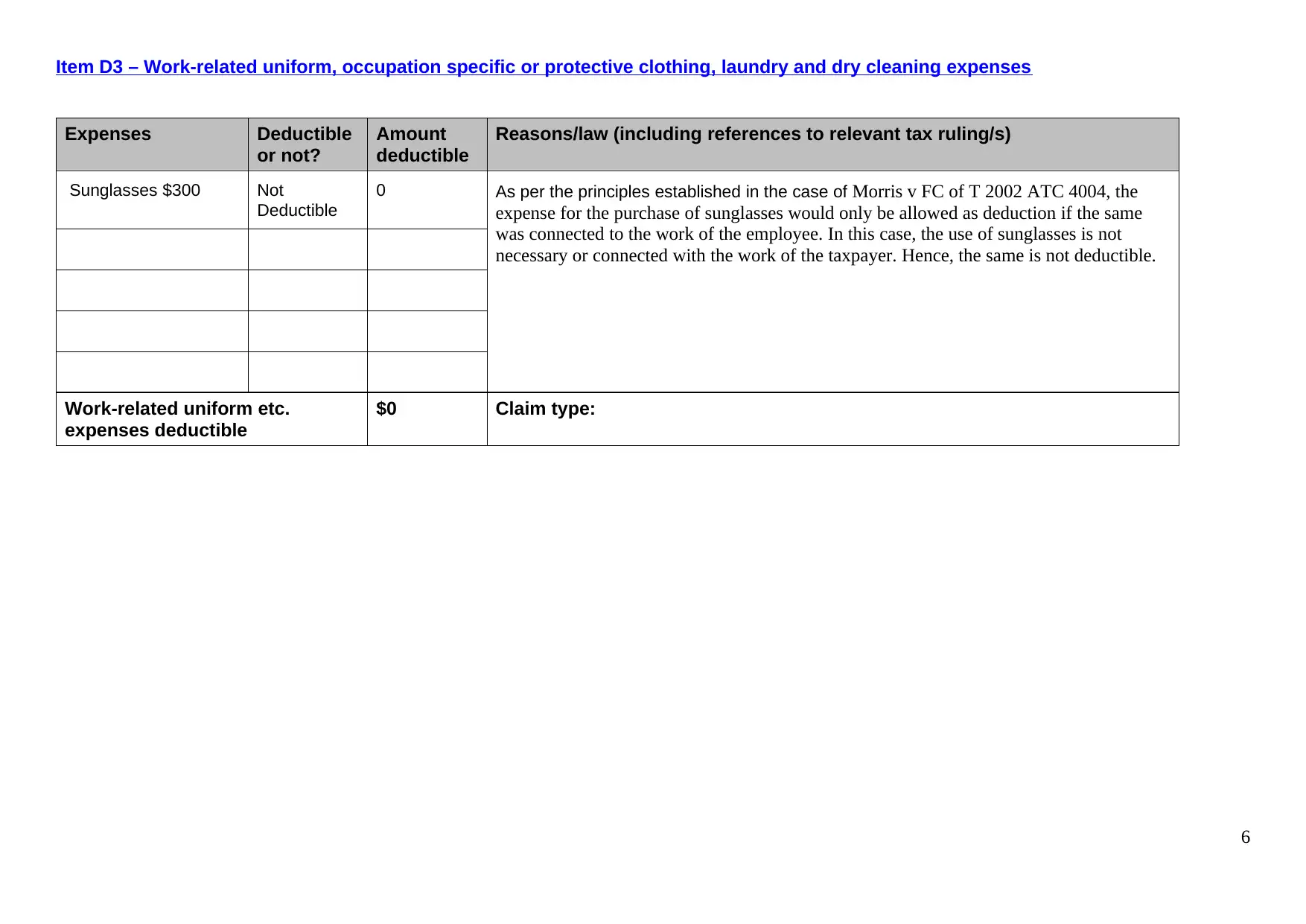

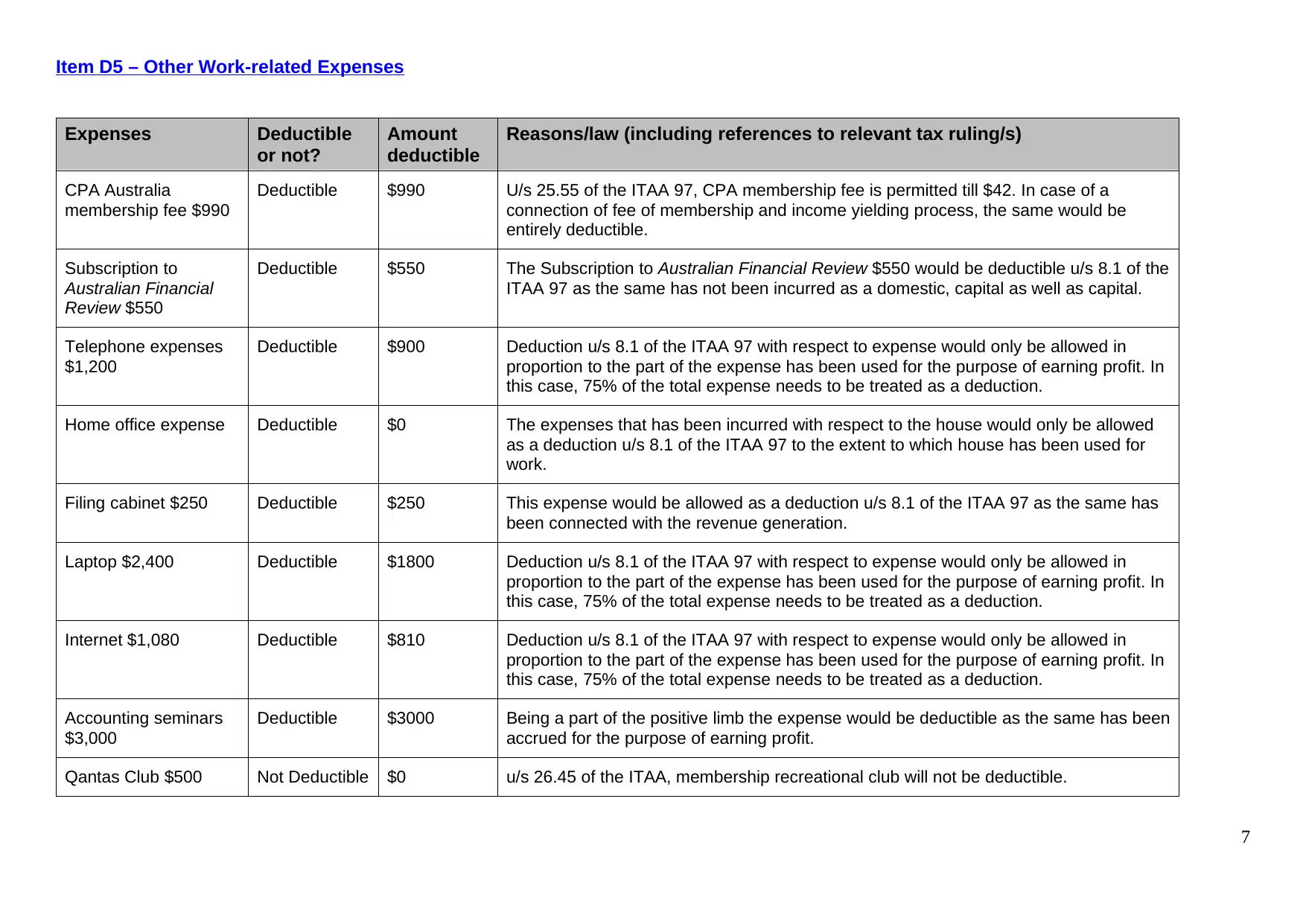

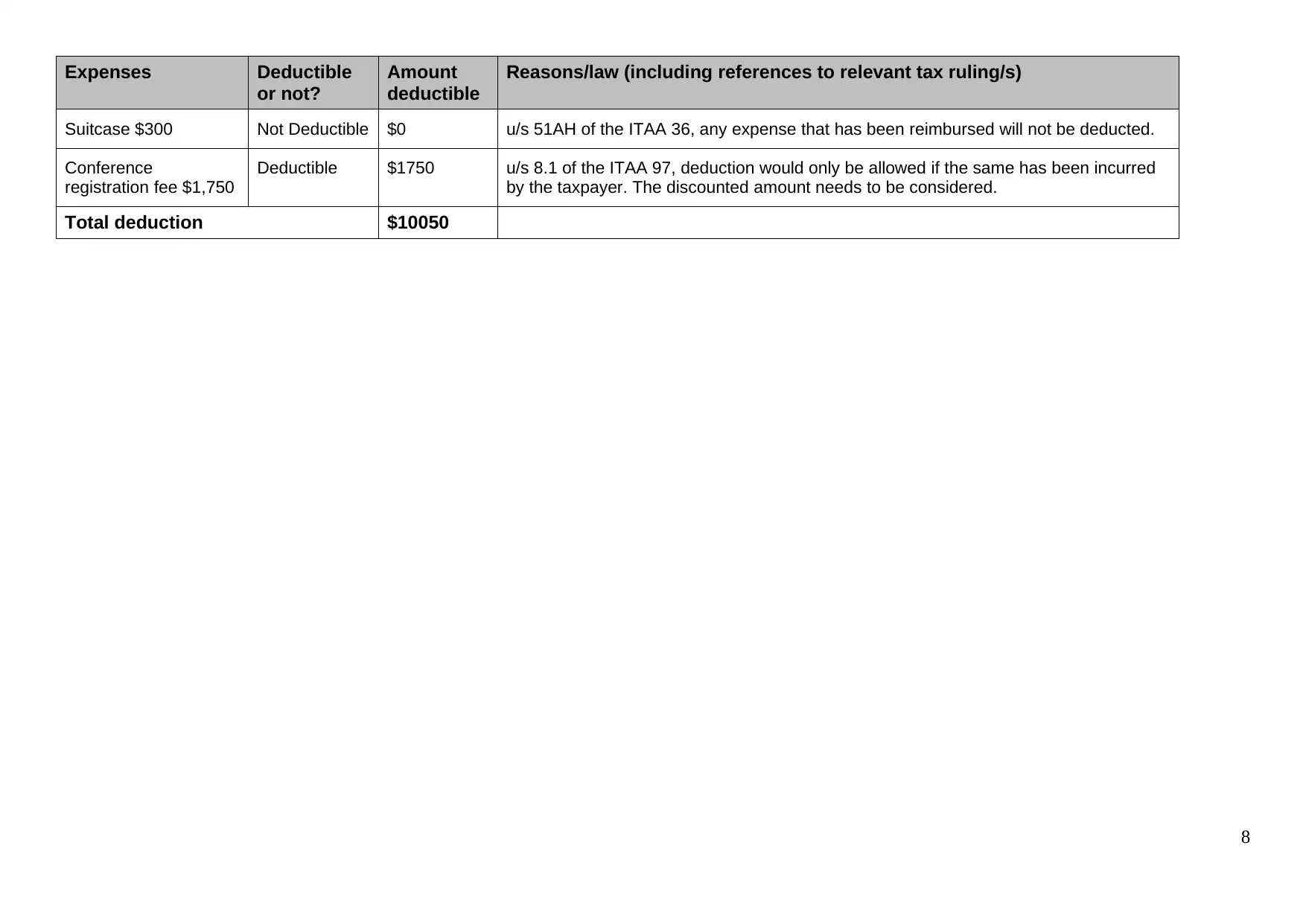

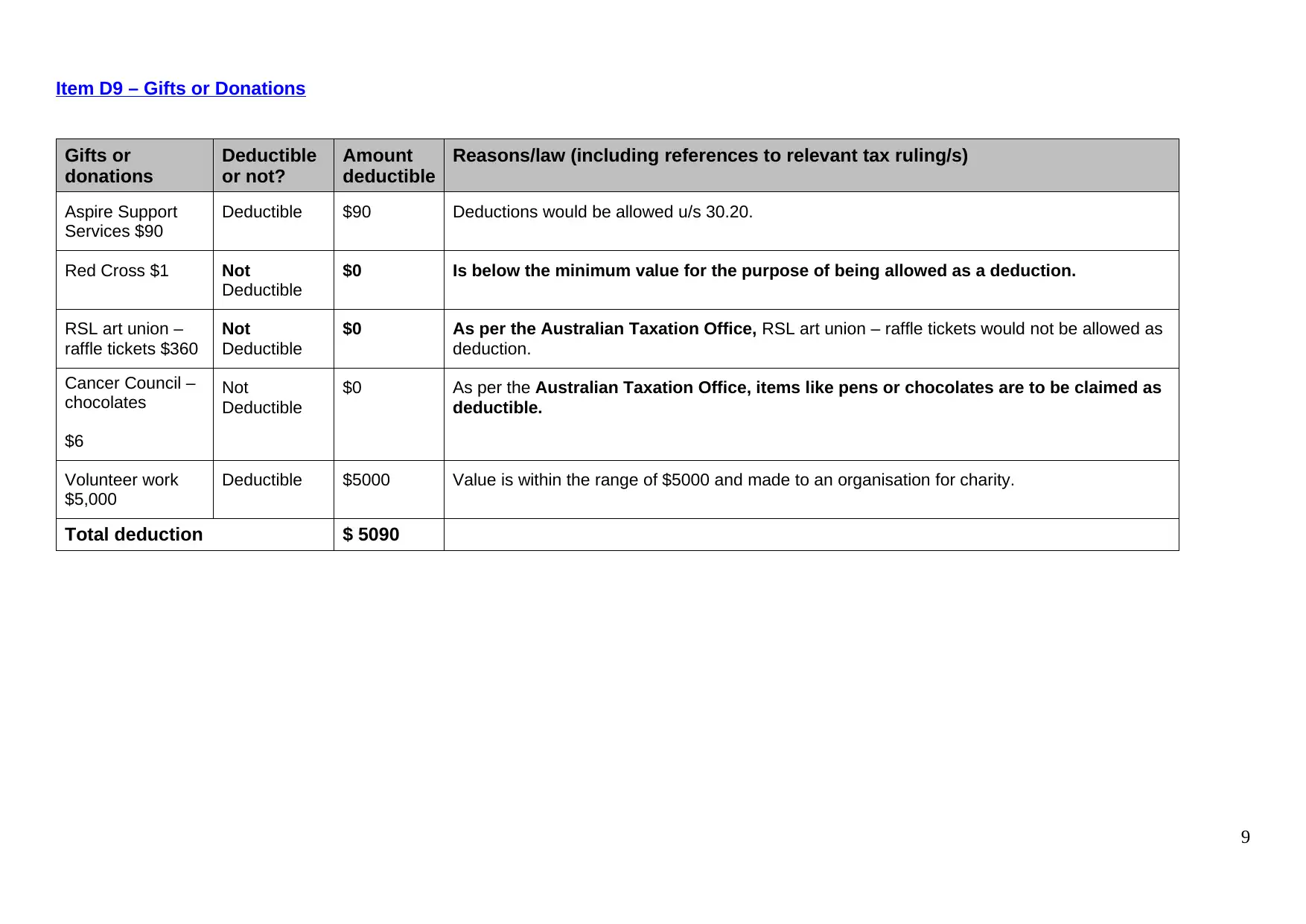

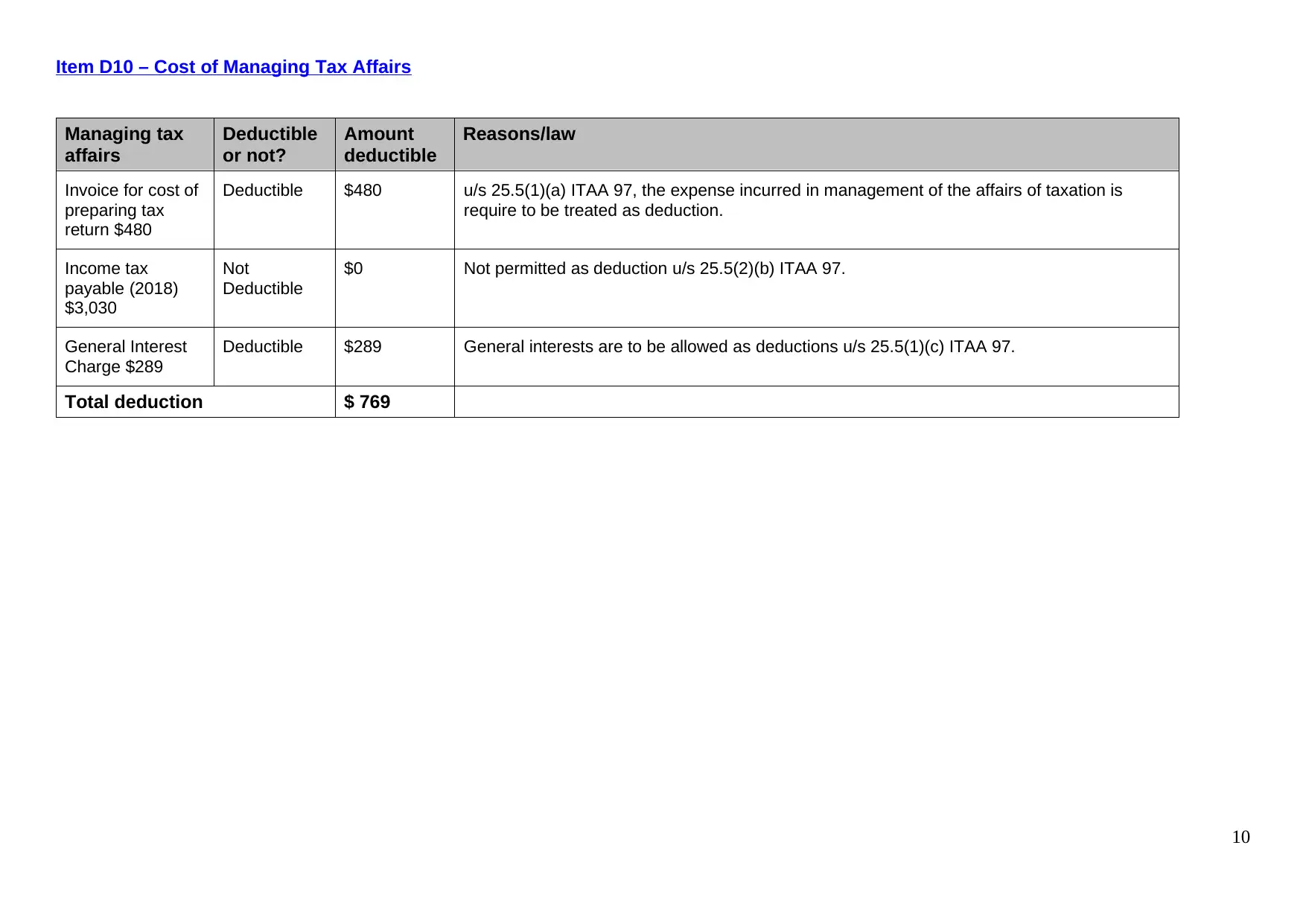

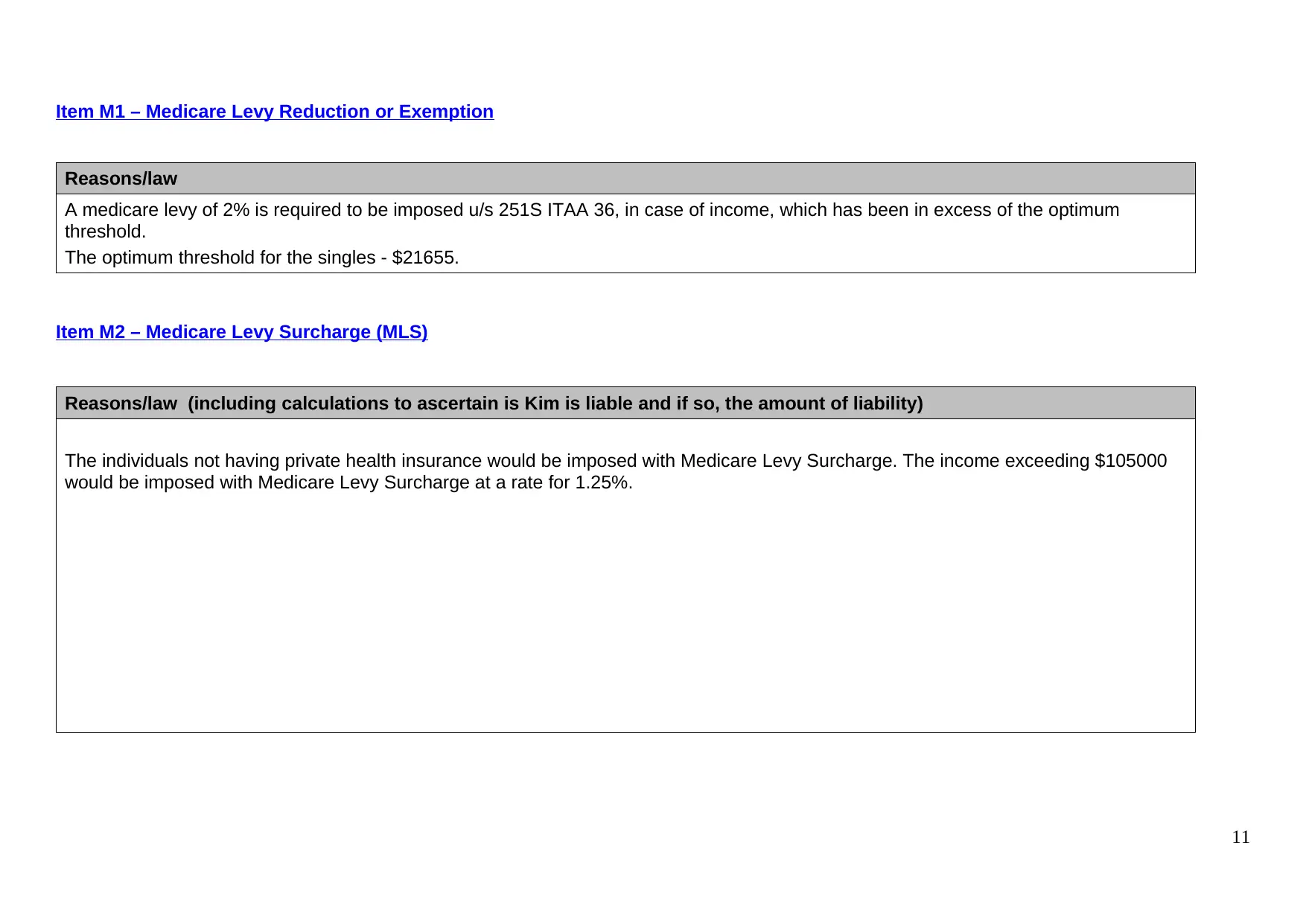

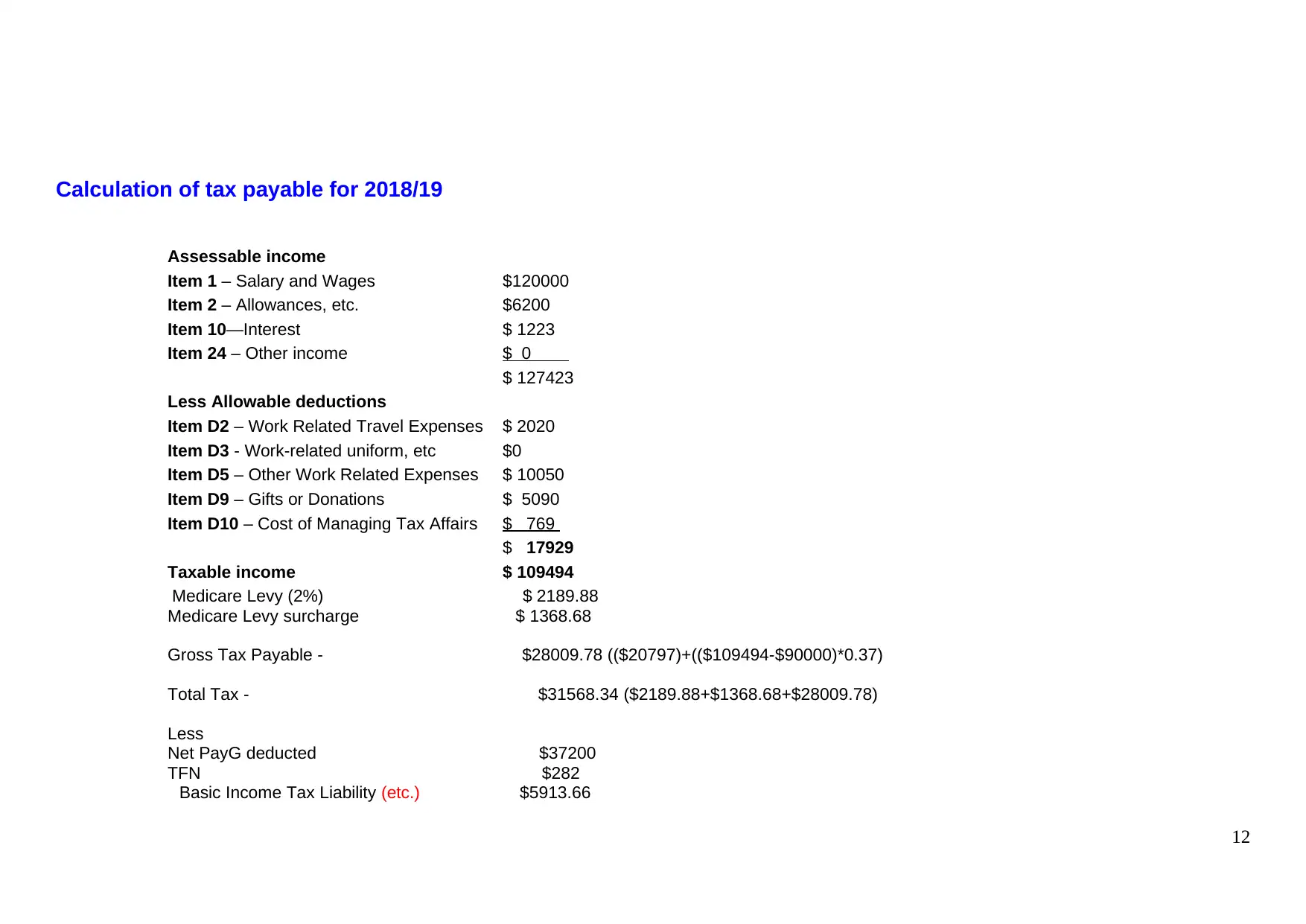

This document presents a comprehensive solution to BFA714 Australian Tax Law Assignment 1, focusing on the tax implications of an individual's income and expenses for the 2018/19 financial year. The assignment analyzes various income sources, including salary, allowances, interest, and royalty income, determining their assessability based on relevant tax legislation. It also examines a range of work-related expenses, such as travel, uniforms, and other work-related costs, assessing their deductibility and citing relevant tax rulings. Furthermore, the solution calculates the individual's taxable income, Medicare levy, and tax payable, providing a detailed breakdown of the calculations. The document provides a step-by-step approach, including the relevant sections of the ITAA 97, to arrive at the final tax liability. It covers various aspects of Australian tax law, offering a practical application of the concepts taught in the course and demonstrates the application of the relevant tax laws and rulings.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.