BHP Billiton Audit, Assurance, and Compliance Analysis Report 2017

VerifiedAdded on 2023/06/04

|12

|2560

|451

Report

AI Summary

This report provides a comprehensive analysis of audit, assurance, and compliance procedures, with a specific focus on BHP Billiton Limited's financial year 2017. It delves into key aspects such as auditor independence, non-audit services provided by KPMG, and a detailed examination of key audit matters (KAMs) including asset valuation, taxation, the Samarco Dam failure, and closure and rehabilitation provisions. The report also discusses the role and responsibilities of the audit committee, the unqualified audit opinion issued, and the distinction between management and auditor responsibilities. Furthermore, it highlights subsequent material events and provides an overall assessment of the audit report's effectiveness, concluding with the expectation that readers will gain a thorough understanding of the financial statements and audit procedures from BHP Billiton's annual report. Desklib provides a platform for students to access similar solved assignments and study resources.

Audit, Assurance and Compliance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

The process of audit has become an integral part of business management and it is useful for

every stakeholders that is interested directly or indirectly in a particular business. This report

is focused on new regulation implemented on business organisations operating in Australia

and New Zealand to disclose key audit matters faced during the process of audit. Main

objective of this regulation is to improve quality of audit conducted for business

organisations. This report has successfully identified all the key audit matters and discussed

reason of their inclusion and Audit procedures used by auditor in relation to such matters.

2

The process of audit has become an integral part of business management and it is useful for

every stakeholders that is interested directly or indirectly in a particular business. This report

is focused on new regulation implemented on business organisations operating in Australia

and New Zealand to disclose key audit matters faced during the process of audit. Main

objective of this regulation is to improve quality of audit conducted for business

organisations. This report has successfully identified all the key audit matters and discussed

reason of their inclusion and Audit procedures used by auditor in relation to such matters.

2

Contents

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

Report.........................................................................................................................................5

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

3

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

Report.........................................................................................................................................5

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Audit is a process of giving objective expression of financial information provided in

financial statements of a particular company. Process of audit for a large organisations takes

around 30 days to be completed which involves detailed examination of financial statements

and internal controls implemented by management. Final outcome of this audit process is

expressed and audit report prepared and presented along with financial statements to

stakeholders at the Annual General Meeting. The information provided by auditor and Audit

opinion paragraph of audit report might not be very sufficient to take important decisions by

stakeholders. This resulted in inclusion of key audit matters paragraph in financial reporting

framework of the company. This paragraph provides the information in relation to audit

procedures conducted by auditor on special and important key matters discussed with

management. This requirement was included in audit reporting framework in December 2016

i.e. every company has to include key audit matters in their annual report starting from

financial year ending 2017 (Carson, Fargher and Zhang, 2016). Inclusion of this paragraph as

elaborated the quality of audit report in conducted by management and auditor. This report

has a conducted financial statement and Audit procedures analysis for BHP Billiton Limited

for the year ending 2017. Numerous factors in relation to audit procedures and Audit

engagement will be discussed in this report.

4

Audit is a process of giving objective expression of financial information provided in

financial statements of a particular company. Process of audit for a large organisations takes

around 30 days to be completed which involves detailed examination of financial statements

and internal controls implemented by management. Final outcome of this audit process is

expressed and audit report prepared and presented along with financial statements to

stakeholders at the Annual General Meeting. The information provided by auditor and Audit

opinion paragraph of audit report might not be very sufficient to take important decisions by

stakeholders. This resulted in inclusion of key audit matters paragraph in financial reporting

framework of the company. This paragraph provides the information in relation to audit

procedures conducted by auditor on special and important key matters discussed with

management. This requirement was included in audit reporting framework in December 2016

i.e. every company has to include key audit matters in their annual report starting from

financial year ending 2017 (Carson, Fargher and Zhang, 2016). Inclusion of this paragraph as

elaborated the quality of audit report in conducted by management and auditor. This report

has a conducted financial statement and Audit procedures analysis for BHP Billiton Limited

for the year ending 2017. Numerous factors in relation to audit procedures and Audit

engagement will be discussed in this report.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Report

Auditor's independence

For the financial year ending 2017 audit of the company was conducted by KPMG which is

one of the big four audit firms in the world. KPMG is known for providing Quality

Assurance and Audit services for any organisation. During the year under consideration

KPMG has provided directors and Audit committee of the company a declaration certificate

that states auditor of the company has conducted their function with Independence and

unbiased state of mind. All the rules and regulations in relation to Corporation Act 2001

along with ethical and professional standards has been followed by auditor. Corporation Act

2001 and professional and ethical standards issued by auditing and assurance standard board

comply is that auditor should be independent while giving opinion financial statement of the

company (Higgins, Milne and Van Gramberg, 2015).

There are various rules and regulations in relation to business activities conducted by auditor

with their clients such as non-audit services provided by auditor during the financial year.

There are various restrictions provided in these rules and regulation and all these restrictions

are complied with during the Year and in 2017.

Non audit services

As already mentioned that there are various restrictions in relation to non-audit services

provided by auditor during the same financial year that auditor is conducting External Audit

services for the same company. It is primary responsibility of Management to check that

services provided by auditor are not in contravention with any of the rules and regulation in

relation to non-audit services. This is the reason that audit committee is formulated by board

of directors of a company. One of the important functions of audit committee is to check that

independence of auditor is maintained throughout the financial year in which such auditor is

conducting statutory audit and providing restricted non audit services are one of the

contravention (Tepalagul and Lin, 2015). There are some services that are allowed to be

provided by external auditor to business organisation.

During the financial year under consideration auditor has provided some non-audit services to

Limited. All the services are within the permitted definition of Non audit services and it does

not affect independence of auditor. Proper precautions has been taken by auditor and audit

5

Auditor's independence

For the financial year ending 2017 audit of the company was conducted by KPMG which is

one of the big four audit firms in the world. KPMG is known for providing Quality

Assurance and Audit services for any organisation. During the year under consideration

KPMG has provided directors and Audit committee of the company a declaration certificate

that states auditor of the company has conducted their function with Independence and

unbiased state of mind. All the rules and regulations in relation to Corporation Act 2001

along with ethical and professional standards has been followed by auditor. Corporation Act

2001 and professional and ethical standards issued by auditing and assurance standard board

comply is that auditor should be independent while giving opinion financial statement of the

company (Higgins, Milne and Van Gramberg, 2015).

There are various rules and regulations in relation to business activities conducted by auditor

with their clients such as non-audit services provided by auditor during the financial year.

There are various restrictions provided in these rules and regulation and all these restrictions

are complied with during the Year and in 2017.

Non audit services

As already mentioned that there are various restrictions in relation to non-audit services

provided by auditor during the same financial year that auditor is conducting External Audit

services for the same company. It is primary responsibility of Management to check that

services provided by auditor are not in contravention with any of the rules and regulation in

relation to non-audit services. This is the reason that audit committee is formulated by board

of directors of a company. One of the important functions of audit committee is to check that

independence of auditor is maintained throughout the financial year in which such auditor is

conducting statutory audit and providing restricted non audit services are one of the

contravention (Tepalagul and Lin, 2015). There are some services that are allowed to be

provided by external auditor to business organisation.

During the financial year under consideration auditor has provided some non-audit services to

Limited. All the services are within the permitted definition of Non audit services and it does

not affect independence of auditor. Proper precautions has been taken by auditor and audit

5

committee of the company. Following are some of the services that are provided in the nature

of non-audit services during the financial year-

Audit and Audit related services- the services are the extension of audit services provided by

auditor such as preparation of tax report, filing of report, tax compliances, tax consultancy

etc. proper agreement has been made by management and auditor to conduct these services

and there has been no contravention of any legal obligations.

Advisory services- During the process of audit or determined find some loopholes or

deficiencies in internal control of the company (Causholli, Chambers and Payne, 2015). In

addition to reporting these deficiencies in audit report, auditor might also give some advice to

management in order to correct and improve the efficiency of the company.

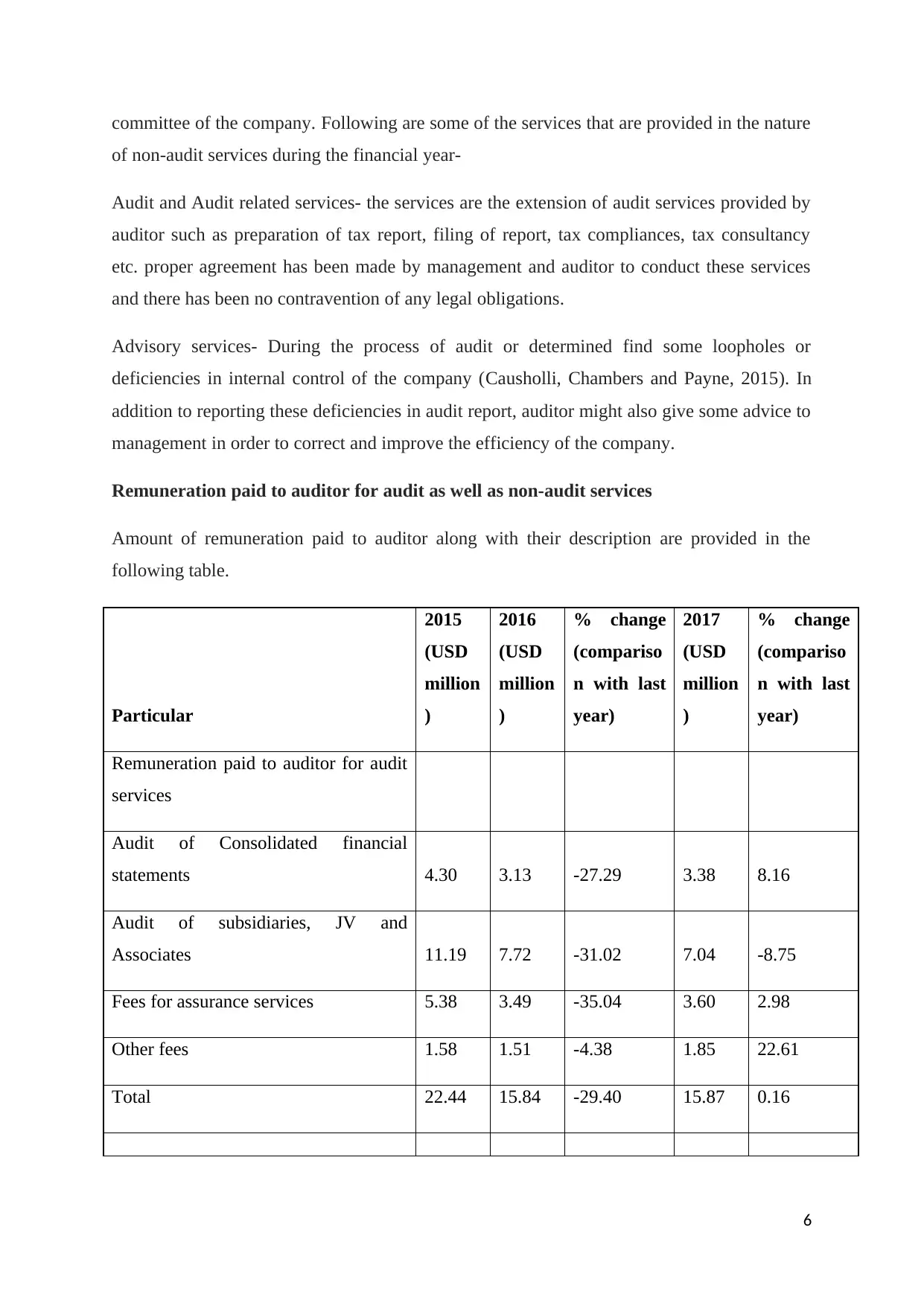

Remuneration paid to auditor for audit as well as non-audit services

Amount of remuneration paid to auditor along with their description are provided in the

following table.

Particular

2015

(USD

million

)

2016

(USD

million

)

% change

(compariso

n with last

year)

2017

(USD

million

)

% change

(compariso

n with last

year)

Remuneration paid to auditor for audit

services

Audit of Consolidated financial

statements 4.30 3.13 -27.29 3.38 8.16

Audit of subsidiaries, JV and

Associates 11.19 7.72 -31.02 7.04 -8.75

Fees for assurance services 5.38 3.49 -35.04 3.60 2.98

Other fees 1.58 1.51 -4.38 1.85 22.61

Total 22.44 15.84 -29.40 15.87 0.16

6

of non-audit services during the financial year-

Audit and Audit related services- the services are the extension of audit services provided by

auditor such as preparation of tax report, filing of report, tax compliances, tax consultancy

etc. proper agreement has been made by management and auditor to conduct these services

and there has been no contravention of any legal obligations.

Advisory services- During the process of audit or determined find some loopholes or

deficiencies in internal control of the company (Causholli, Chambers and Payne, 2015). In

addition to reporting these deficiencies in audit report, auditor might also give some advice to

management in order to correct and improve the efficiency of the company.

Remuneration paid to auditor for audit as well as non-audit services

Amount of remuneration paid to auditor along with their description are provided in the

following table.

Particular

2015

(USD

million

)

2016

(USD

million

)

% change

(compariso

n with last

year)

2017

(USD

million

)

% change

(compariso

n with last

year)

Remuneration paid to auditor for audit

services

Audit of Consolidated financial

statements 4.30 3.13 -27.29 3.38 8.16

Audit of subsidiaries, JV and

Associates 11.19 7.72 -31.02 7.04 -8.75

Fees for assurance services 5.38 3.49 -35.04 3.60 2.98

Other fees 1.58 1.51 -4.38 1.85 22.61

Total 22.44 15.84 -29.40 15.87 0.16

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

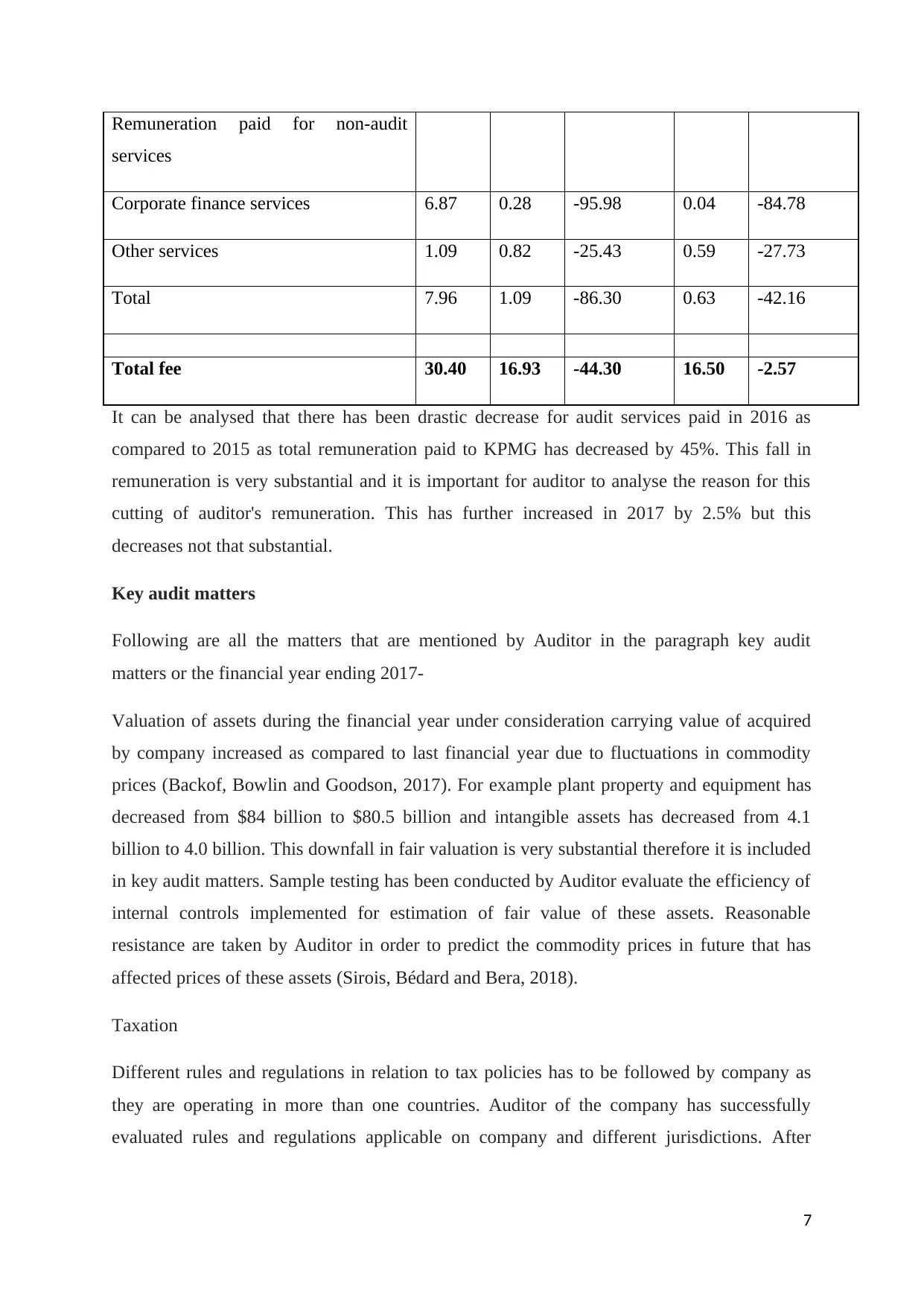

Remuneration paid for non-audit

services

Corporate finance services 6.87 0.28 -95.98 0.04 -84.78

Other services 1.09 0.82 -25.43 0.59 -27.73

Total 7.96 1.09 -86.30 0.63 -42.16

Total fee 30.40 16.93 -44.30 16.50 -2.57

It can be analysed that there has been drastic decrease for audit services paid in 2016 as

compared to 2015 as total remuneration paid to KPMG has decreased by 45%. This fall in

remuneration is very substantial and it is important for auditor to analyse the reason for this

cutting of auditor's remuneration. This has further increased in 2017 by 2.5% but this

decreases not that substantial.

Key audit matters

Following are all the matters that are mentioned by Auditor in the paragraph key audit

matters or the financial year ending 2017-

Valuation of assets during the financial year under consideration carrying value of acquired

by company increased as compared to last financial year due to fluctuations in commodity

prices (Backof, Bowlin and Goodson, 2017). For example plant property and equipment has

decreased from $84 billion to $80.5 billion and intangible assets has decreased from 4.1

billion to 4.0 billion. This downfall in fair valuation is very substantial therefore it is included

in key audit matters. Sample testing has been conducted by Auditor evaluate the efficiency of

internal controls implemented for estimation of fair value of these assets. Reasonable

resistance are taken by Auditor in order to predict the commodity prices in future that has

affected prices of these assets (Sirois, Bédard and Bera, 2018).

Taxation

Different rules and regulations in relation to tax policies has to be followed by company as

they are operating in more than one countries. Auditor of the company has successfully

evaluated rules and regulations applicable on company and different jurisdictions. After

7

services

Corporate finance services 6.87 0.28 -95.98 0.04 -84.78

Other services 1.09 0.82 -25.43 0.59 -27.73

Total 7.96 1.09 -86.30 0.63 -42.16

Total fee 30.40 16.93 -44.30 16.50 -2.57

It can be analysed that there has been drastic decrease for audit services paid in 2016 as

compared to 2015 as total remuneration paid to KPMG has decreased by 45%. This fall in

remuneration is very substantial and it is important for auditor to analyse the reason for this

cutting of auditor's remuneration. This has further increased in 2017 by 2.5% but this

decreases not that substantial.

Key audit matters

Following are all the matters that are mentioned by Auditor in the paragraph key audit

matters or the financial year ending 2017-

Valuation of assets during the financial year under consideration carrying value of acquired

by company increased as compared to last financial year due to fluctuations in commodity

prices (Backof, Bowlin and Goodson, 2017). For example plant property and equipment has

decreased from $84 billion to $80.5 billion and intangible assets has decreased from 4.1

billion to 4.0 billion. This downfall in fair valuation is very substantial therefore it is included

in key audit matters. Sample testing has been conducted by Auditor evaluate the efficiency of

internal controls implemented for estimation of fair value of these assets. Reasonable

resistance are taken by Auditor in order to predict the commodity prices in future that has

affected prices of these assets (Sirois, Bédard and Bera, 2018).

Taxation

Different rules and regulations in relation to tax policies has to be followed by company as

they are operating in more than one countries. Auditor of the company has successfully

evaluated rules and regulations applicable on company and different jurisdictions. After

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

search evaluation auditor has been able to collect sufficient audit evidence that all that rules

and regulations are properly followed by the organisation.

Samarco

Management of the company has taken some Complex accounting measures uses in order to

account for losses incurred on Samarco Dam failure. Auditor has examined all the key

assumptions made by management in order to record the losses occurring from this project

(Cordoş and Fülöp, 2015). Consultation has also been taken with auditor of Samarco Dam

project who identify any material misstatement or audit matters identified during audit

process conducted on Samarco dam.

Closure and rehabilitation provision

It is one of the main functions of business to close, restore and rehabilitate sites. Accounting

procedures in relation to such business activity can be very complex and therefore it is

included in the audit matters discussed with management. Complexity of this accounting

process increases due to various assumption that are required to be made in relation to

valuation (Brasel, Doxey, Grenier & Reffett, 2016). All these assumptions and internal

controls implemented in accounting for rehabilitation provisions are properly examined by

auditor. Calculation of discount rates exchange rates and net present value evaluated by

Auditor in order to identify accuracy of these provisions. Final outcome of these provisions

are compared with market available data for checking its accuracy.

Audit committee

Audit committee risk and Audit committee of established in 2011 and first person that was

appointed in this audit committee was Lindsay Maxsted that was also appointed as chairman

of this committee. Formal charter has been maintained by board of directors for define

structure, scope and roles and responsibilities of the audit committee. According to this

charter, audit committee is responsible for conducting meetings with internal auditor and

external auditor for defining scope of audit. In addition to that this audit committee is also

responsible for all the functions in relation to preparation of financial statements and process

of audit conducted on such financial statement.

Audit opinion

8

and regulations are properly followed by the organisation.

Samarco

Management of the company has taken some Complex accounting measures uses in order to

account for losses incurred on Samarco Dam failure. Auditor has examined all the key

assumptions made by management in order to record the losses occurring from this project

(Cordoş and Fülöp, 2015). Consultation has also been taken with auditor of Samarco Dam

project who identify any material misstatement or audit matters identified during audit

process conducted on Samarco dam.

Closure and rehabilitation provision

It is one of the main functions of business to close, restore and rehabilitate sites. Accounting

procedures in relation to such business activity can be very complex and therefore it is

included in the audit matters discussed with management. Complexity of this accounting

process increases due to various assumption that are required to be made in relation to

valuation (Brasel, Doxey, Grenier & Reffett, 2016). All these assumptions and internal

controls implemented in accounting for rehabilitation provisions are properly examined by

auditor. Calculation of discount rates exchange rates and net present value evaluated by

Auditor in order to identify accuracy of these provisions. Final outcome of these provisions

are compared with market available data for checking its accuracy.

Audit committee

Audit committee risk and Audit committee of established in 2011 and first person that was

appointed in this audit committee was Lindsay Maxsted that was also appointed as chairman

of this committee. Formal charter has been maintained by board of directors for define

structure, scope and roles and responsibilities of the audit committee. According to this

charter, audit committee is responsible for conducting meetings with internal auditor and

external auditor for defining scope of audit. In addition to that this audit committee is also

responsible for all the functions in relation to preparation of financial statements and process

of audit conducted on such financial statement.

Audit opinion

8

After examination of all financial statement auditor of the company has provided unqualified

audit opinion on financial statements. Unqualified opinion means that financial statements of

the company are clean and presenting position of company in market. There were some

difficulties faced by Auditor in conducting the process of audit which are mentioned in audit

matters paragraph. It can be said that financial statement of the company are free from

material misstatement, frauds and error and presenting true value of company.

Difference between management and auditor's responsibility

There is a clear and distinct difference between responsibilities of an auditor and

Management in relation to internal controls and financial statements of the company.

Management of the company is responsible for implementation of internal control and

improving the efficiency of these internal control. On the other hand auditory is only

responsible for checking the efficiency of these internal control and giving their opinion on

efficiency evaluated by them (Chan and Vasarhelyi, 2018). Similarity in case of preparation

of financial statements, management is responsible for preparation whereas auditor is

responsible for checking accuracy of such financial statements.

Subsequent material events

Board of directors of the company has approved an investment of 2.5 million dollars for the

purpose of developing Spence growth options and construction of copper concentrate which

can increase the life of Spence mine by around 50 years. This is a material event that

occurred after the closing of balance sheet. This event will have positive impact on financial

position of the company and it can also increase market valuation of company in stock

exchange (AICPA, 2017).

Analysis of audit report

All rules and regulations issued in Corporation Act 2001 and professional and ethical or code

of conduct or properly followed by the organisation and auditor. It can be said that external

audit conducted for the year 2017 is very effective and efficient. All the material

misstatement car properly disclosed and chances of under reporting are very low. At the

Annual General Meeting auditor of the company can be asked about the future plans of the

company that can affect decision making process of stakeholders.

9

audit opinion on financial statements. Unqualified opinion means that financial statements of

the company are clean and presenting position of company in market. There were some

difficulties faced by Auditor in conducting the process of audit which are mentioned in audit

matters paragraph. It can be said that financial statement of the company are free from

material misstatement, frauds and error and presenting true value of company.

Difference between management and auditor's responsibility

There is a clear and distinct difference between responsibilities of an auditor and

Management in relation to internal controls and financial statements of the company.

Management of the company is responsible for implementation of internal control and

improving the efficiency of these internal control. On the other hand auditory is only

responsible for checking the efficiency of these internal control and giving their opinion on

efficiency evaluated by them (Chan and Vasarhelyi, 2018). Similarity in case of preparation

of financial statements, management is responsible for preparation whereas auditor is

responsible for checking accuracy of such financial statements.

Subsequent material events

Board of directors of the company has approved an investment of 2.5 million dollars for the

purpose of developing Spence growth options and construction of copper concentrate which

can increase the life of Spence mine by around 50 years. This is a material event that

occurred after the closing of balance sheet. This event will have positive impact on financial

position of the company and it can also increase market valuation of company in stock

exchange (AICPA, 2017).

Analysis of audit report

All rules and regulations issued in Corporation Act 2001 and professional and ethical or code

of conduct or properly followed by the organisation and auditor. It can be said that external

audit conducted for the year 2017 is very effective and efficient. All the material

misstatement car properly disclosed and chances of under reporting are very low. At the

Annual General Meeting auditor of the company can be asked about the future plans of the

company that can affect decision making process of stakeholders.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

This report has evaluated all the functions of auditing that are conducted in the financial year

2017. Activities like disclosure of key audit matters, declaration of auditor’s independence,

audit committee and their functionality, etc. are discussed in detail with respect to BHP

Billiton. At the end of this report it is expected that a reader will get all the information in

relation to efficiency of financial statements and Audit procedures from annual report of the

company.

10

This report has evaluated all the functions of auditing that are conducted in the financial year

2017. Activities like disclosure of key audit matters, declaration of auditor’s independence,

audit committee and their functionality, etc. are discussed in detail with respect to BHP

Billiton. At the end of this report it is expected that a reader will get all the information in

relation to efficiency of financial statements and Audit procedures from annual report of the

company.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reference

AICPA. (2017). Statement on Auditing Standards, Number 126: The Auditor's Consideration

of an Entity's Ability to Continue as a Going Concern (No. 126). John Wiley & Sons.

Backof, A., Bowlin, K., & Goodson, B. (2017). The impact of proposed changes to the

content of the audit report on jurors’ assessments of auditor negligence.

Brasel, K., Doxey, M. M., Grenier, J. H., & Reffett, A. (2016). Risk disclosure preceding

negative outcomes: The effects of reporting critical audit matters on judgments of auditor

liability. The Accounting Review, 91(5), 1345-1362.

Carson, E., Fargher, N., & Zhang, Y. (2016). Trends in auditor reporting in Australia: a

synthesis and opportunities for research. Australian Accounting Review, 26(3), 226-242.

Causholli, M., Chambers, D. J., & Payne, J. L. (2015). Does selling non-audit services impair

auditor independence? New Research Says,“Yes”. Current Issues in Auditing, 9(2), P1-

P6.

Chan, D. Y., & Vasarhelyi, M. A. (2018). Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing

Limited.

Cordoş, G. S., & Fülöp, M. T. (2015). Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Higgins, C., Milne, M. J., & Van Gramberg, B. (2015). The uptake of sustainability reporting

in Australia. Journal of Business Ethics, 129(2), 445-468.

Sirois, L. P., Bédard, J., & Bera, P. (2018). The informational value of key audit matters in

the auditor's report: evidence from an Eye-tracking study. Accounting Horizons.

Tepalagul, N., & Lin, L. (2015). Auditor independence and audit quality: A literature

review. Journal of Accounting, Auditing & Finance, 30(1), 101-121.

11

AICPA. (2017). Statement on Auditing Standards, Number 126: The Auditor's Consideration

of an Entity's Ability to Continue as a Going Concern (No. 126). John Wiley & Sons.

Backof, A., Bowlin, K., & Goodson, B. (2017). The impact of proposed changes to the

content of the audit report on jurors’ assessments of auditor negligence.

Brasel, K., Doxey, M. M., Grenier, J. H., & Reffett, A. (2016). Risk disclosure preceding

negative outcomes: The effects of reporting critical audit matters on judgments of auditor

liability. The Accounting Review, 91(5), 1345-1362.

Carson, E., Fargher, N., & Zhang, Y. (2016). Trends in auditor reporting in Australia: a

synthesis and opportunities for research. Australian Accounting Review, 26(3), 226-242.

Causholli, M., Chambers, D. J., & Payne, J. L. (2015). Does selling non-audit services impair

auditor independence? New Research Says,“Yes”. Current Issues in Auditing, 9(2), P1-

P6.

Chan, D. Y., & Vasarhelyi, M. A. (2018). Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing

Limited.

Cordoş, G. S., & Fülöp, M. T. (2015). Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Higgins, C., Milne, M. J., & Van Gramberg, B. (2015). The uptake of sustainability reporting

in Australia. Journal of Business Ethics, 129(2), 445-468.

Sirois, L. P., Bédard, J., & Bera, P. (2018). The informational value of key audit matters in

the auditor's report: evidence from an Eye-tracking study. Accounting Horizons.

Tepalagul, N., & Lin, L. (2015). Auditor independence and audit quality: A literature

review. Journal of Accounting, Auditing & Finance, 30(1), 101-121.

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.