Corporate Accounting Report: BHP Billiton Financial Analysis

VerifiedAdded on 2021/06/14

|14

|3007

|385

Report

AI Summary

This report provides a comprehensive analysis of BHP Billiton's corporate accounting practices. It begins with an executive summary and table of contents, followed by an introduction outlining the importance of financial statement analysis. The discussion section delves into the qualitative characteristics of financial reports, focusing on relevance and comparability, using BHP Billiton's financial statements as examples. It also examines BHP's environmental practices and disclosure reports, including climate change initiatives and energy consumption reporting. The report offers recommendations to BHP's management for strengthening disclosure compliance, emphasizing the need for clear data presentation and comparable environmental reports. Part B explores pre-acquisition entries, dividend considerations, and the differentiation between pre and post-acquisition dividends, alongside a discussion of goodwill calculation methods (partial and full). The report concludes by summarizing the key findings and insights into BHP Billiton's corporate accounting strategies.

Running head: CORPORATE ACCOUNTING

Name of the Student

Name of the University

Author note

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Executive Summary:

The following report deals with the various kinds of disclosure reports and their

contents of BHP Billiton Company. It delves into the specific areas of the disclosure reports

of the company in order to portray a clearer understanding of the same. In this way, certain

important merits of the disclosure report of the company has also been mentioned and some

useful suggestions towards the management of the company for successful reporting in the

future has also been provided. Along with this the important aspects of amalgamation and the

relative adjustment entries in the case of pre and post-acquisition dividends have also been

mentioned in this report.

Executive Summary:

The following report deals with the various kinds of disclosure reports and their

contents of BHP Billiton Company. It delves into the specific areas of the disclosure reports

of the company in order to portray a clearer understanding of the same. In this way, certain

important merits of the disclosure report of the company has also been mentioned and some

useful suggestions towards the management of the company for successful reporting in the

future has also been provided. Along with this the important aspects of amalgamation and the

relative adjustment entries in the case of pre and post-acquisition dividends have also been

mentioned in this report.

2CORPORATE ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................3

Part A:....................................................................................................................................3

Part B:.....................................................................................................................................8

Conclusion:..............................................................................................................................11

References:...............................................................................................................................12

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................3

Part A:....................................................................................................................................3

Part B:.....................................................................................................................................8

Conclusion:..............................................................................................................................11

References:...............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Introduction:

Analysis of the financial statements of any company plays a vital role in the arena of

corporate accounting. These financial statements serve as the performance report card of the

company’s annual performance. The importance of the consolidated balance sheet,

comprehensive income statement, cash flow statement and the statement showing equity

changes, cannot altogether be ignored, as they serve as the most important source of

information for the stakeholders of the company. With these things at the very core of this

report, it tends to provide examples of the various qualities of the financial statements, its

environmental practices, the various information disclosures and some recommendations to

the top management regarding the disclosure compliance. Along with this, acquisition related

adjustments have been discussed. All these things have been compiled and discussed in the

context of BHP, Billiton, which is the largest mining company in the world, in terms of the

market capitalisation (Finance.yahoo.com, 2018). The aim remains to enquire into the various

intricacies of corporate accounting with the help of a standard company, BHP.

Discussion:

Part A:

1) a The qualitative characteristics of any company’s financial reports is mainly

consists of reliability, comparability, understand ability and reliability. Here, only the

principles of comparability and relevance of the financial statements with reference to

BHP’s financial statements.

Relevance: The relevance feature of the financial statements states that the financial

reports and the statements must be relevant to the various kinds of needs of the different

Introduction:

Analysis of the financial statements of any company plays a vital role in the arena of

corporate accounting. These financial statements serve as the performance report card of the

company’s annual performance. The importance of the consolidated balance sheet,

comprehensive income statement, cash flow statement and the statement showing equity

changes, cannot altogether be ignored, as they serve as the most important source of

information for the stakeholders of the company. With these things at the very core of this

report, it tends to provide examples of the various qualities of the financial statements, its

environmental practices, the various information disclosures and some recommendations to

the top management regarding the disclosure compliance. Along with this, acquisition related

adjustments have been discussed. All these things have been compiled and discussed in the

context of BHP, Billiton, which is the largest mining company in the world, in terms of the

market capitalisation (Finance.yahoo.com, 2018). The aim remains to enquire into the various

intricacies of corporate accounting with the help of a standard company, BHP.

Discussion:

Part A:

1) a The qualitative characteristics of any company’s financial reports is mainly

consists of reliability, comparability, understand ability and reliability. Here, only the

principles of comparability and relevance of the financial statements with reference to

BHP’s financial statements.

Relevance: The relevance feature of the financial statements states that the financial

reports and the statements must be relevant to the various kinds of needs of the different

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

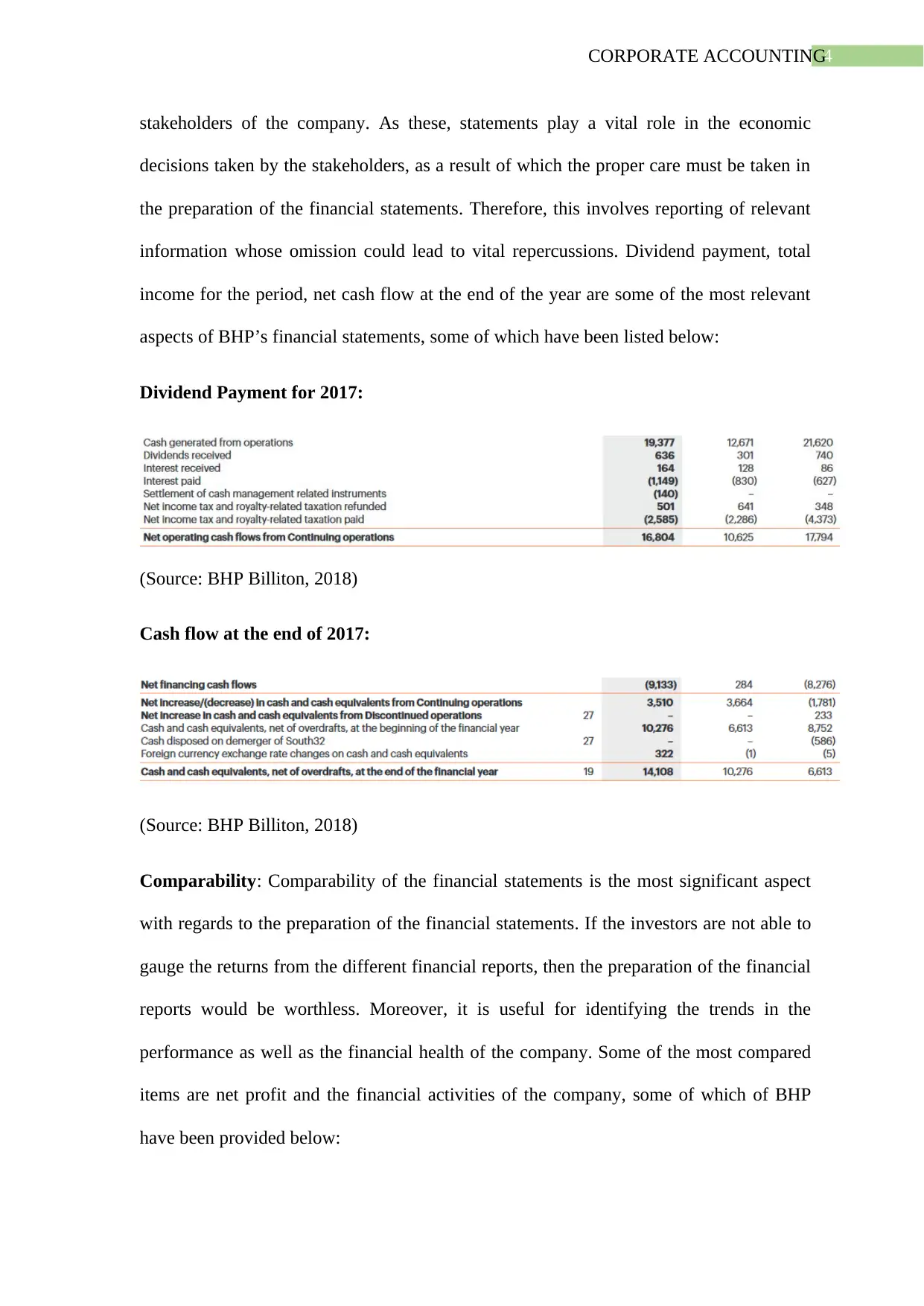

stakeholders of the company. As these, statements play a vital role in the economic

decisions taken by the stakeholders, as a result of which the proper care must be taken in

the preparation of the financial statements. Therefore, this involves reporting of relevant

information whose omission could lead to vital repercussions. Dividend payment, total

income for the period, net cash flow at the end of the year are some of the most relevant

aspects of BHP’s financial statements, some of which have been listed below:

Dividend Payment for 2017:

(Source: BHP Billiton, 2018)

Cash flow at the end of 2017:

(Source: BHP Billiton, 2018)

Comparability: Comparability of the financial statements is the most significant aspect

with regards to the preparation of the financial statements. If the investors are not able to

gauge the returns from the different financial reports, then the preparation of the financial

reports would be worthless. Moreover, it is useful for identifying the trends in the

performance as well as the financial health of the company. Some of the most compared

items are net profit and the financial activities of the company, some of which of BHP

have been provided below:

stakeholders of the company. As these, statements play a vital role in the economic

decisions taken by the stakeholders, as a result of which the proper care must be taken in

the preparation of the financial statements. Therefore, this involves reporting of relevant

information whose omission could lead to vital repercussions. Dividend payment, total

income for the period, net cash flow at the end of the year are some of the most relevant

aspects of BHP’s financial statements, some of which have been listed below:

Dividend Payment for 2017:

(Source: BHP Billiton, 2018)

Cash flow at the end of 2017:

(Source: BHP Billiton, 2018)

Comparability: Comparability of the financial statements is the most significant aspect

with regards to the preparation of the financial statements. If the investors are not able to

gauge the returns from the different financial reports, then the preparation of the financial

reports would be worthless. Moreover, it is useful for identifying the trends in the

performance as well as the financial health of the company. Some of the most compared

items are net profit and the financial activities of the company, some of which of BHP

have been provided below:

5CORPORATE ACCOUNTING

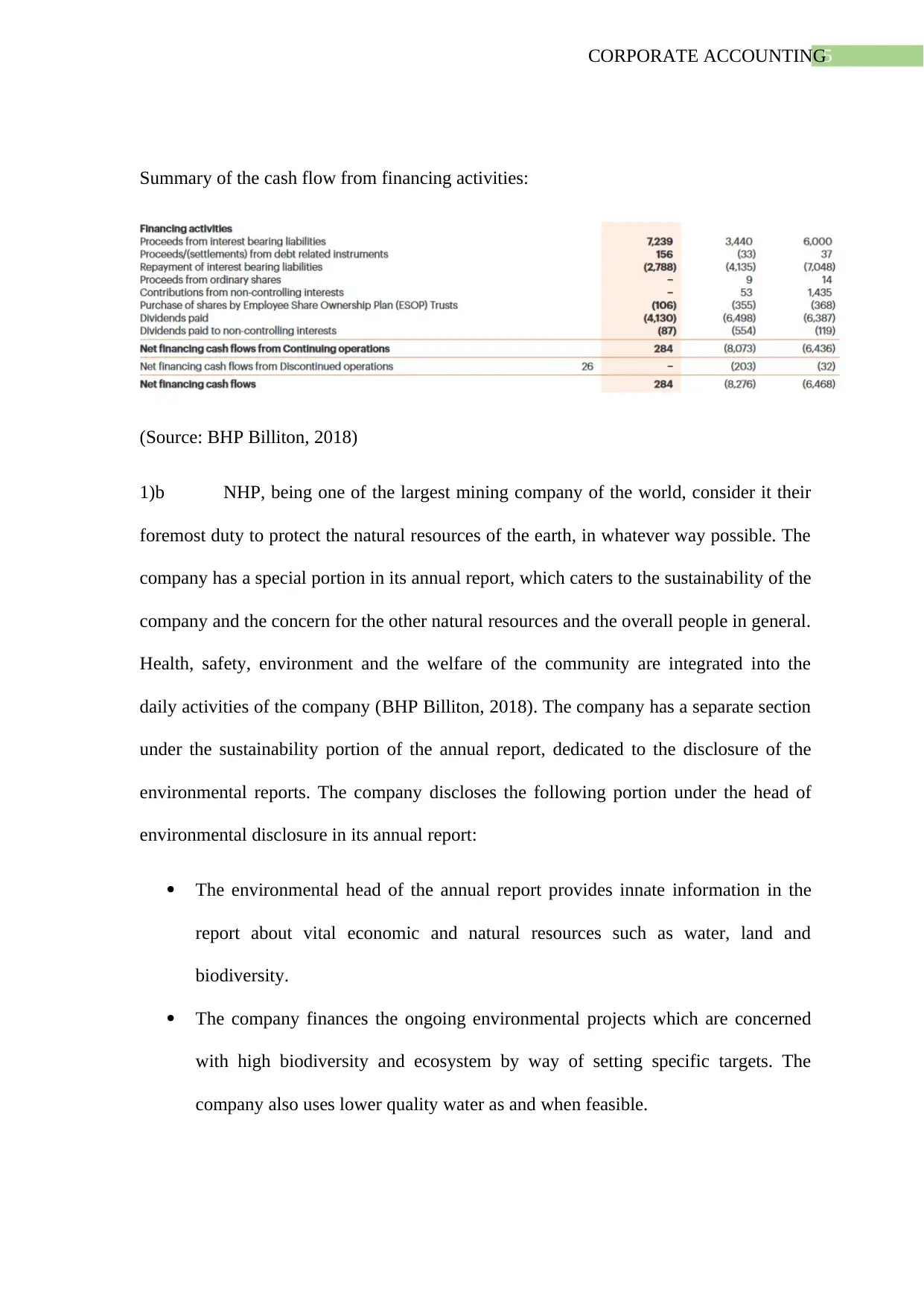

Summary of the cash flow from financing activities:

(Source: BHP Billiton, 2018)

1)b NHP, being one of the largest mining company of the world, consider it their

foremost duty to protect the natural resources of the earth, in whatever way possible. The

company has a special portion in its annual report, which caters to the sustainability of the

company and the concern for the other natural resources and the overall people in general.

Health, safety, environment and the welfare of the community are integrated into the

daily activities of the company (BHP Billiton, 2018). The company has a separate section

under the sustainability portion of the annual report, dedicated to the disclosure of the

environmental reports. The company discloses the following portion under the head of

environmental disclosure in its annual report:

The environmental head of the annual report provides innate information in the

report about vital economic and natural resources such as water, land and

biodiversity.

The company finances the ongoing environmental projects which are concerned

with high biodiversity and ecosystem by way of setting specific targets. The

company also uses lower quality water as and when feasible.

Summary of the cash flow from financing activities:

(Source: BHP Billiton, 2018)

1)b NHP, being one of the largest mining company of the world, consider it their

foremost duty to protect the natural resources of the earth, in whatever way possible. The

company has a special portion in its annual report, which caters to the sustainability of the

company and the concern for the other natural resources and the overall people in general.

Health, safety, environment and the welfare of the community are integrated into the

daily activities of the company (BHP Billiton, 2018). The company has a separate section

under the sustainability portion of the annual report, dedicated to the disclosure of the

environmental reports. The company discloses the following portion under the head of

environmental disclosure in its annual report:

The environmental head of the annual report provides innate information in the

report about vital economic and natural resources such as water, land and

biodiversity.

The company finances the ongoing environmental projects which are concerned

with high biodiversity and ecosystem by way of setting specific targets. The

company also uses lower quality water as and when feasible.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

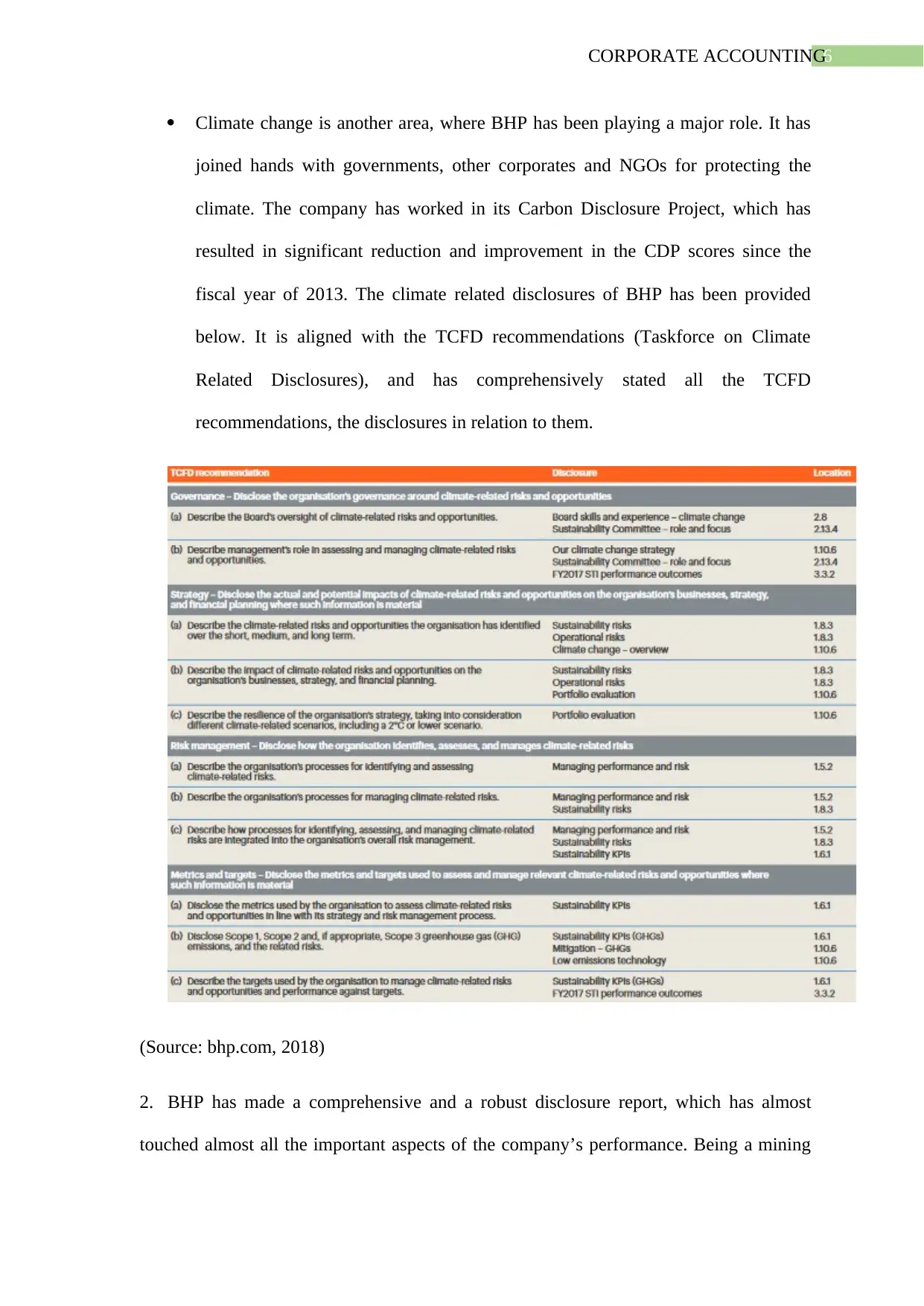

Climate change is another area, where BHP has been playing a major role. It has

joined hands with governments, other corporates and NGOs for protecting the

climate. The company has worked in its Carbon Disclosure Project, which has

resulted in significant reduction and improvement in the CDP scores since the

fiscal year of 2013. The climate related disclosures of BHP has been provided

below. It is aligned with the TCFD recommendations (Taskforce on Climate

Related Disclosures), and has comprehensively stated all the TCFD

recommendations, the disclosures in relation to them.

(Source: bhp.com, 2018)

2. BHP has made a comprehensive and a robust disclosure report, which has almost

touched almost all the important aspects of the company’s performance. Being a mining

Climate change is another area, where BHP has been playing a major role. It has

joined hands with governments, other corporates and NGOs for protecting the

climate. The company has worked in its Carbon Disclosure Project, which has

resulted in significant reduction and improvement in the CDP scores since the

fiscal year of 2013. The climate related disclosures of BHP has been provided

below. It is aligned with the TCFD recommendations (Taskforce on Climate

Related Disclosures), and has comprehensively stated all the TCFD

recommendations, the disclosures in relation to them.

(Source: bhp.com, 2018)

2. BHP has made a comprehensive and a robust disclosure report, which has almost

touched almost all the important aspects of the company’s performance. Being a mining

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

company, it has, reportedly disclosed various important aspects of its mining and other

environmental related activities. The main heads of its disclosure reports are concerned

with the following:

Climate change

Tax and Transparency

Accurate and comprehensive annual financial statements

Environmental report

Anti-competitive policy

Anti-corruption

Energy consumption report.

The company has provided a sufficient amount of information about each of the topic which

plays a vital role in its mining operations. Be it climate change or any other aspect of the

environment, where the company has a significant amount of influence due to its mining

operations. BHP has also been very efficient in the presentation of its energy consumption by

stating the greenhouse emissions of the company. Along with this, the company has also been

very vocal about the anti-corruption as well as the anti-competitive policy, with a view of

being an example to the other companies in and around the world. Thus, it can be said that

the company has become very vocal about all the important things associated with its

business, which can lead to the establishment of the fact that the company has provided

sufficient amount of items in its disclosure reports.

3. The two most important recommendations to the management of BHP for

strengthening its compliance with the disclosure reports of the company are as follows:

One of the most important aspects of the disclosure reports of the company is the

accurate, friendly and adequate representation of all the important aspects of the

company, it has, reportedly disclosed various important aspects of its mining and other

environmental related activities. The main heads of its disclosure reports are concerned

with the following:

Climate change

Tax and Transparency

Accurate and comprehensive annual financial statements

Environmental report

Anti-competitive policy

Anti-corruption

Energy consumption report.

The company has provided a sufficient amount of information about each of the topic which

plays a vital role in its mining operations. Be it climate change or any other aspect of the

environment, where the company has a significant amount of influence due to its mining

operations. BHP has also been very efficient in the presentation of its energy consumption by

stating the greenhouse emissions of the company. Along with this, the company has also been

very vocal about the anti-corruption as well as the anti-competitive policy, with a view of

being an example to the other companies in and around the world. Thus, it can be said that

the company has become very vocal about all the important things associated with its

business, which can lead to the establishment of the fact that the company has provided

sufficient amount of items in its disclosure reports.

3. The two most important recommendations to the management of BHP for

strengthening its compliance with the disclosure reports of the company are as follows:

One of the most important aspects of the disclosure reports of the company is the

accurate, friendly and adequate representation of all the important aspects of the

8CORPORATE ACCOUNTING

company. This requires the company, to provide a robust, pictorial presentation of all

the data associated with the company’s financial performance along with the

company’s environmental, biodiversity reports. Only when the users of the financial

information could understand the financial reports of the company, then only it will be

considered as successful. BHP must properly publication of pictorial presentation of

data more extensively.

The company must also try to present the environmental impact and climate change

reports more quantitatively, by way of graphs and tables. This will help the users of

financial statements to have a better view of the reports. Along with this, the company

must provide more past information about the environmental and other significant

aspects of the sustainability report in order to provide a comparable report (Dobele, et

al., 2014). For example, the environmental disclosure as well as the climate change

report of the company for the year must be present in a tabular form with all the

impact and implications of the previous year, such as 2016. This will create a

comparable data, which will be more helpful in gauging the overall impact of the

company’s ecological exploits, while performing its mining related activities.

Part B:

1. There are various important considerations which work behind the purpose of pre-

acquisition entries in the preparation of the consolidated financial statements. Some of

the most important ones are:

To prevent the double counting of the assets of the concerned company.

It is also done in order to prevent the double counting the equities of the

concerned company.

For the purpose of recognising any kind of gain or bargain purchase for the

company.

company. This requires the company, to provide a robust, pictorial presentation of all

the data associated with the company’s financial performance along with the

company’s environmental, biodiversity reports. Only when the users of the financial

information could understand the financial reports of the company, then only it will be

considered as successful. BHP must properly publication of pictorial presentation of

data more extensively.

The company must also try to present the environmental impact and climate change

reports more quantitatively, by way of graphs and tables. This will help the users of

financial statements to have a better view of the reports. Along with this, the company

must provide more past information about the environmental and other significant

aspects of the sustainability report in order to provide a comparable report (Dobele, et

al., 2014). For example, the environmental disclosure as well as the climate change

report of the company for the year must be present in a tabular form with all the

impact and implications of the previous year, such as 2016. This will create a

comparable data, which will be more helpful in gauging the overall impact of the

company’s ecological exploits, while performing its mining related activities.

Part B:

1. There are various important considerations which work behind the purpose of pre-

acquisition entries in the preparation of the consolidated financial statements. Some of

the most important ones are:

To prevent the double counting of the assets of the concerned company.

It is also done in order to prevent the double counting the equities of the

concerned company.

For the purpose of recognising any kind of gain or bargain purchase for the

company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

2. There are two main conditions which are to be taken care of when the case of

payment of dividend on the date of acquisition of the company is being done. The two

conditions are as follows:

Payment of Cum dividend: If on the date of acquisition, dividend is paid by the

subsidiary company, in such a case, if it is found out that the dividend is

declared and is included with the final amount, then that dividend is to be

included and an entry must be passed in the books for it. Thus in the case of

cum dividend, even if it is paid as on the date of acquisition, it would be

considered and would be deducted from the total acquisition value of the

amalgamation. This signifies the acceptance of the dividend as on the date of

acquisition (Ljungvall and Patel, 2014). If during the middle of the year, if it

is again repeated, then the normal process of taking the dividend into account

is done by the company and is consequently adjusted in the consolidated

financial statements at the end of the year.

Payment of ex-dividend: If the subsidiary company is paying ex-dividend on

the date of acquisition, then that dividend payment is not included and is

consequently not accounted for during the preparation of the financial

accounts.

2. There are two main conditions which are to be taken care of when the case of

payment of dividend on the date of acquisition of the company is being done. The two

conditions are as follows:

Payment of Cum dividend: If on the date of acquisition, dividend is paid by the

subsidiary company, in such a case, if it is found out that the dividend is

declared and is included with the final amount, then that dividend is to be

included and an entry must be passed in the books for it. Thus in the case of

cum dividend, even if it is paid as on the date of acquisition, it would be

considered and would be deducted from the total acquisition value of the

amalgamation. This signifies the acceptance of the dividend as on the date of

acquisition (Ljungvall and Patel, 2014). If during the middle of the year, if it

is again repeated, then the normal process of taking the dividend into account

is done by the company and is consequently adjusted in the consolidated

financial statements at the end of the year.

Payment of ex-dividend: If the subsidiary company is paying ex-dividend on

the date of acquisition, then that dividend payment is not included and is

consequently not accounted for during the preparation of the financial

accounts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

3. The differentiation into the pre and post dividend portions are very significant from

the financial perspective of the company. When the dividend is declared from the pre-

acquisition profits and later on received by the buyer of the investment, then such

amount of investment is completely deducted from the total cost of the investment.

Therefore, dividend received from the pre-acquisition profit is known as pre

acquisition dividend. Post-acquisition dividend is credited to the profit and loss

account of the company, consequently, dividend received from the post-acquisition

profits is known as the post-acquisition dividend (Mall, C.P. and Singh, 2013). For

this purpose of differentiating their source of origination, these two dividends are

separated from the by the suffixes of pre and post.

4. In the process of acquisition analysis, the monetary consideration transferred is

compared to the different kinds of identifiable net assets of the subsidiary company

which have been acquired. In addition to this, any goodwill which is present in the

financial books of the subsidiary company does not qualify as an identifiable asset of

the company. In the books of accounts of the subsidiary company, the goodwill is not

at all considered, which has been recorded in the books of the subsidiary company.

In this case, there are two main methods of calculating goodwill which are the partial

goodwill method and the full goodwill method. In each of these cases, there are separate

treatment for the goodwill which is received from the subsidiary company on the date of

the company (Lombrano and Zanin, 2013). In the case of the partial goodwill method,

only the goodwill which is received from the transaction is recorded in the books of

accounts of the company. This does not happen in the case of the full goodwill method. In

the case of the full goodwill method, there are some reservations, in this case. The

company includes both the goodwill which is received from the subsidiary as well as the

one which is earned from the transaction of the company. The company ultimately

3. The differentiation into the pre and post dividend portions are very significant from

the financial perspective of the company. When the dividend is declared from the pre-

acquisition profits and later on received by the buyer of the investment, then such

amount of investment is completely deducted from the total cost of the investment.

Therefore, dividend received from the pre-acquisition profit is known as pre

acquisition dividend. Post-acquisition dividend is credited to the profit and loss

account of the company, consequently, dividend received from the post-acquisition

profits is known as the post-acquisition dividend (Mall, C.P. and Singh, 2013). For

this purpose of differentiating their source of origination, these two dividends are

separated from the by the suffixes of pre and post.

4. In the process of acquisition analysis, the monetary consideration transferred is

compared to the different kinds of identifiable net assets of the subsidiary company

which have been acquired. In addition to this, any goodwill which is present in the

financial books of the subsidiary company does not qualify as an identifiable asset of

the company. In the books of accounts of the subsidiary company, the goodwill is not

at all considered, which has been recorded in the books of the subsidiary company.

In this case, there are two main methods of calculating goodwill which are the partial

goodwill method and the full goodwill method. In each of these cases, there are separate

treatment for the goodwill which is received from the subsidiary company on the date of

the company (Lombrano and Zanin, 2013). In the case of the partial goodwill method,

only the goodwill which is received from the transaction is recorded in the books of

accounts of the company. This does not happen in the case of the full goodwill method. In

the case of the full goodwill method, there are some reservations, in this case. The

company includes both the goodwill which is received from the subsidiary as well as the

one which is earned from the transaction of the company. The company ultimately

11CORPORATE ACCOUNTING

calculates the differences between the two, which is ultimately taken as the goodwill of

the parent company.

5. In the case, when the parent acquires a controlling interest in a subsidiary, the

carrying amounts of the subsidiary’s assets are not equal to fair value, which is a

common phenomenon, as there are certain adjustments which needs to be made in this

regard.

One of the most important factors behind the compulsion of all these adjustments is

the fact that there remains a net fair value of the assets which are actually acquired

during the entire; process of amalgamation or consolidation. When a particular

company acquires any kind of assets due to the process of amalgamation from the

group of assets of another company, then certain amount of adjustments becomes

necessary (Ina and Adriana., 2013). This is because, when the company acquires any

asset, during this process, the asset has some specific amount of fair value and a

specific amount of market value. Difference between the two exists, all the time, as a

result of this, to provide a true and fair view of the financial statements, the asset is

shown in the current net value, in the consolidated financial statements. Failing to do

so, would lead to payment of more taxes, if the market value or the book value has

been considered, ignoring the net present value. This would cause a loss to the

company.

Conclusion:

One of the most important aspects of corporate accounting is the presence of the

disclosure reports of the activities of the company. It is one of the most significant

performance measure of the company and deals with the important aspects of the various

kinds of operations conducted by it under the radar. A company which is presenting a vivid

calculates the differences between the two, which is ultimately taken as the goodwill of

the parent company.

5. In the case, when the parent acquires a controlling interest in a subsidiary, the

carrying amounts of the subsidiary’s assets are not equal to fair value, which is a

common phenomenon, as there are certain adjustments which needs to be made in this

regard.

One of the most important factors behind the compulsion of all these adjustments is

the fact that there remains a net fair value of the assets which are actually acquired

during the entire; process of amalgamation or consolidation. When a particular

company acquires any kind of assets due to the process of amalgamation from the

group of assets of another company, then certain amount of adjustments becomes

necessary (Ina and Adriana., 2013). This is because, when the company acquires any

asset, during this process, the asset has some specific amount of fair value and a

specific amount of market value. Difference between the two exists, all the time, as a

result of this, to provide a true and fair view of the financial statements, the asset is

shown in the current net value, in the consolidated financial statements. Failing to do

so, would lead to payment of more taxes, if the market value or the book value has

been considered, ignoring the net present value. This would cause a loss to the

company.

Conclusion:

One of the most important aspects of corporate accounting is the presence of the

disclosure reports of the activities of the company. It is one of the most significant

performance measure of the company and deals with the important aspects of the various

kinds of operations conducted by it under the radar. A company which is presenting a vivid

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.